1. Introduction

Urban sustainability encompasses the ability of a city to maintain economic, social, and environmental well-being while meeting the needs of its current and future residents. In urban systems, the development trajectories of regional economies are constantly evolving and subject to various shocks. To examine the resilience of regional economic systems to these shocks, scholars have drawn upon system equilibrium models from the fields of physics and ecology [

1,

2,

3] and have proposed the concept of “economic resilience”, which builds upon the principles of engineering and ecological resilience [

4]. This concept has gained traction due to its ability to capture the holistic and dynamic nature of socioeconomic systems and its potential to inform policy and academic research [

5,

6]. Resilience is considered an important expression of sustainability and is vividly referred to as the emergency room of sustainability [

7]. The importance of economic resilience for urban sustainability lies in its ability to maintain stability and foster growth amidst external disturbances, while also bolstering social unity and inclusivity, promoting environmental sustainability, and strengthening cities’ capacity to adapt to future challenges [

5,

8]. Recent years have witnessed heightened global uncertainty, stemming from events such as the 2008 financial crisis, trade tensions between China and the United States, the COVID-19 pandemic, and wars and conflicts, as well as other shocks that have generated ongoing economic turmoil. The ability of regions to withstand uncertainties in the economic system has become an increasingly pressing concern for governments and academics alike [

9,

10].

Financial development is a crucial driver of economic growth and prosperity. During the digital transition, the rise of financial technology (Fintech)

1, which integrates technology and financial services, provides new opportunities for the development of the traditional financial system [

12]. Digital transactions powered by Fintech optimize financial resource allocation, drive technological innovation, and facilitate the transformation and upgrading of financial infrastructure [

13]. This integration enhances financial efficiency, inclusivity, and innovation, satisfying the personalized financial needs of diverse businesses [

14]. According to the World Bank, global Fintech investment soared from less than

$10 billion annually before 2013 to

$215 billion in 2019 and then decreased to

$122 billion in the 2020 pandemic year. By the first half of 2021, global investments in Fintech had reached

$98 billion [

15]. Although existing studies have explored the impact of financial development on economic resilience [

16] and the influence of regional technological structures [

17,

18], as well as the effects of smart city construction, including its digital transitions, on economic resilience [

19], research specifically examining the direct impact of Fintech on economic resilience remains limited [

20,

21].

This study aims to examine economic resilience within the context of digital transformation in the financial sector. While past research has predominantly focused on economic resilience in response to shocks, we aim to broaden the horizon by examining the inherent resilience of regional economies and its relationship with Fintech innovation. In an era where Fintech is transforming traditional financial systems and playing an increasingly pivotal role in economic development, understanding its direct influence on economic resilience, regional variations, and its underlying mechanisms becomes not only relevant but also crucial. This understanding has the potential to provide valuable insights for policy decisions and strategic investments in a rapidly evolving urban and technological landscape.

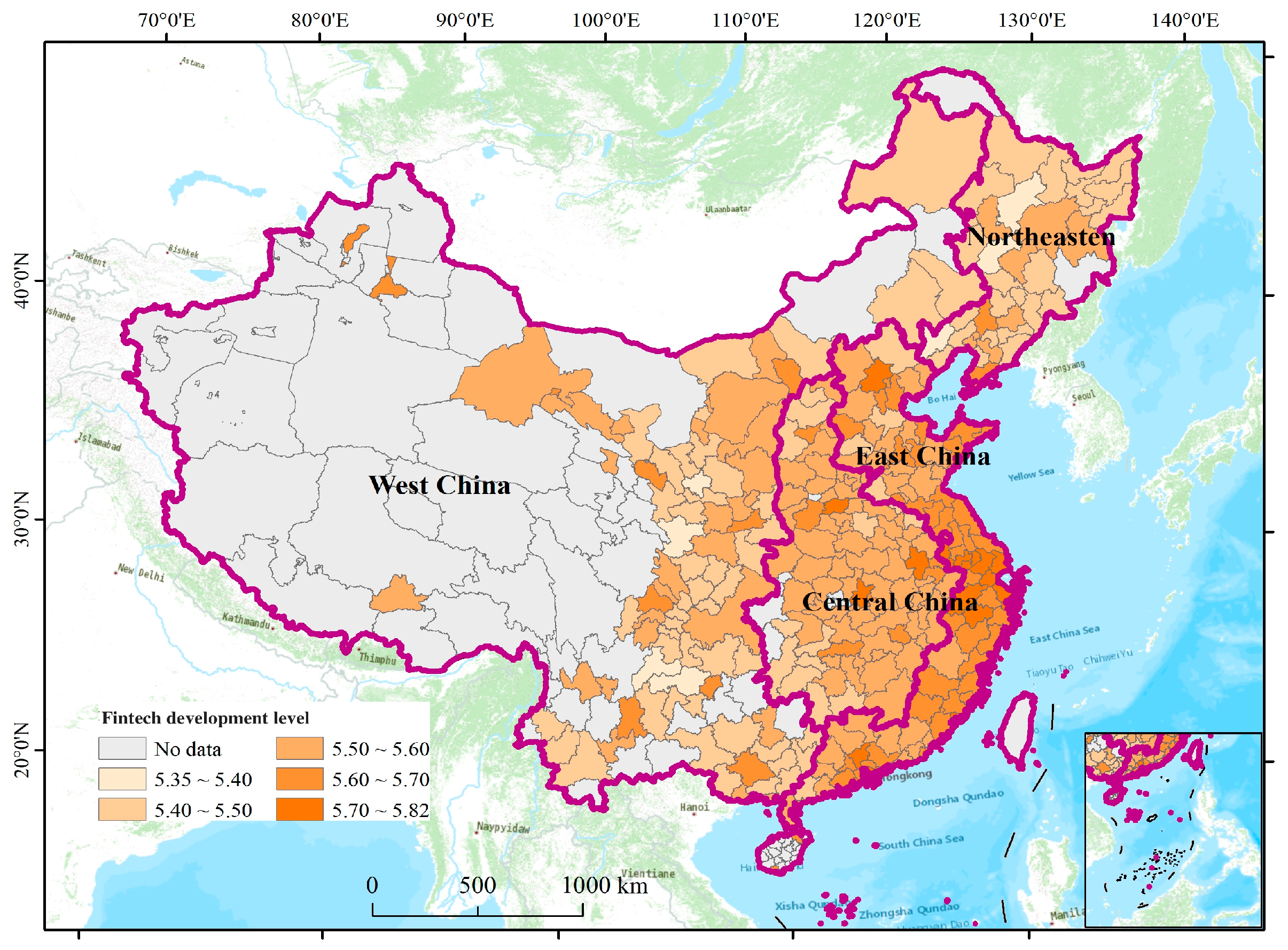

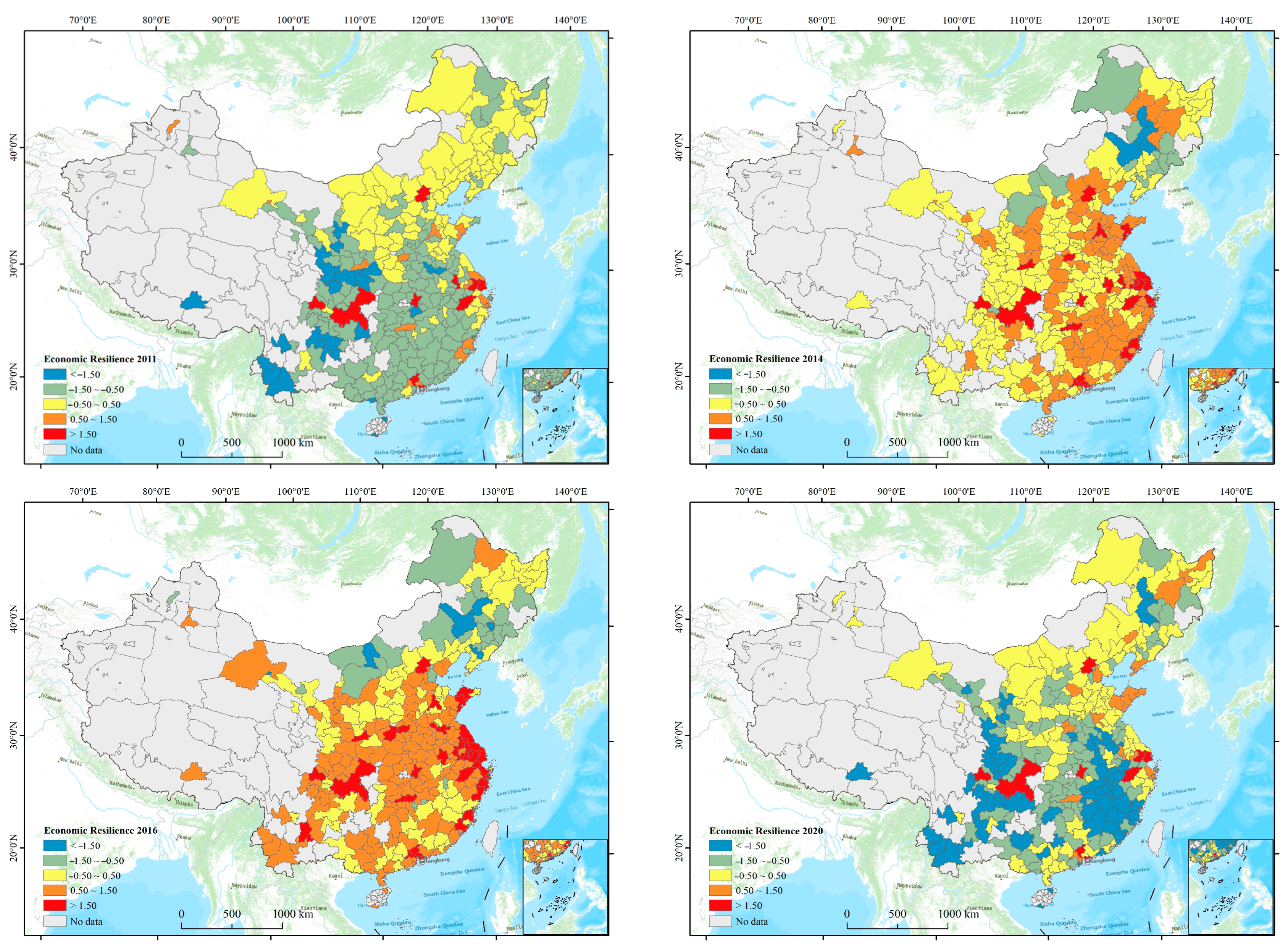

To address this research aim, this study commences by constructing a quantification method to assess regional economic resilience. Subsequently, it empirically examines the impact of Fintech on economic resilience using data from Chinese prefecture-level cities during the period from 2011 to 2020 (

Figure 1). The research delves into the underlying mechanisms, taking into consideration aspects like technological innovation and industrial structure upgrading, to explain this impact. Additionally, it employs cross-sectional analysis to accommodate the variations arising from geographical locations and city scales. The reasons for selecting China as the empirical case study region are as follows. The diverse geographic and economic landscape of China provides a rich and varied context for analyzing how different regions leverage technological innovation and industrial upgrades to enhance their economic resilience. In addition, China’s rapid digital transformation, especially in the financial sector, with widespread adoption of Fintech solutions like mobile payments and digital banking, presents a unique opportunity to explore how such technologies influence economic stability. This setting allows for a detailed examination of the dynamic interplay between digital transition and economic resilience across varying urban scales and geographical locations.

6. Conclusions and Enlightenment

This study ventured to enhance urban sustainability by examining economic resilience and digital transformation, aiming to broaden and redefine the traditional perception of economic resilience beyond mere shock response. It delved into economic resilience within the digital transformation of the financial technology sector, proposing a fresh perspective on navigating the complexities of modern urban development. We first introduced and employed an innovative conceptualization of economic resilience, framing it as an inherent attribute of regional economic systems. This novel perspective facilitates the analysis of economic resilience not only in the context of external disturbances but also as a fundamental characteristic, enabling a proactive assessment of a system’s inherent economic stability and robustness. This shift towards recognizing resilience as a constant feature provides deeper insights into the foundational strength of economic systems, allowing for a more comprehensive understanding of their capacity to withstand and adapt to changes.

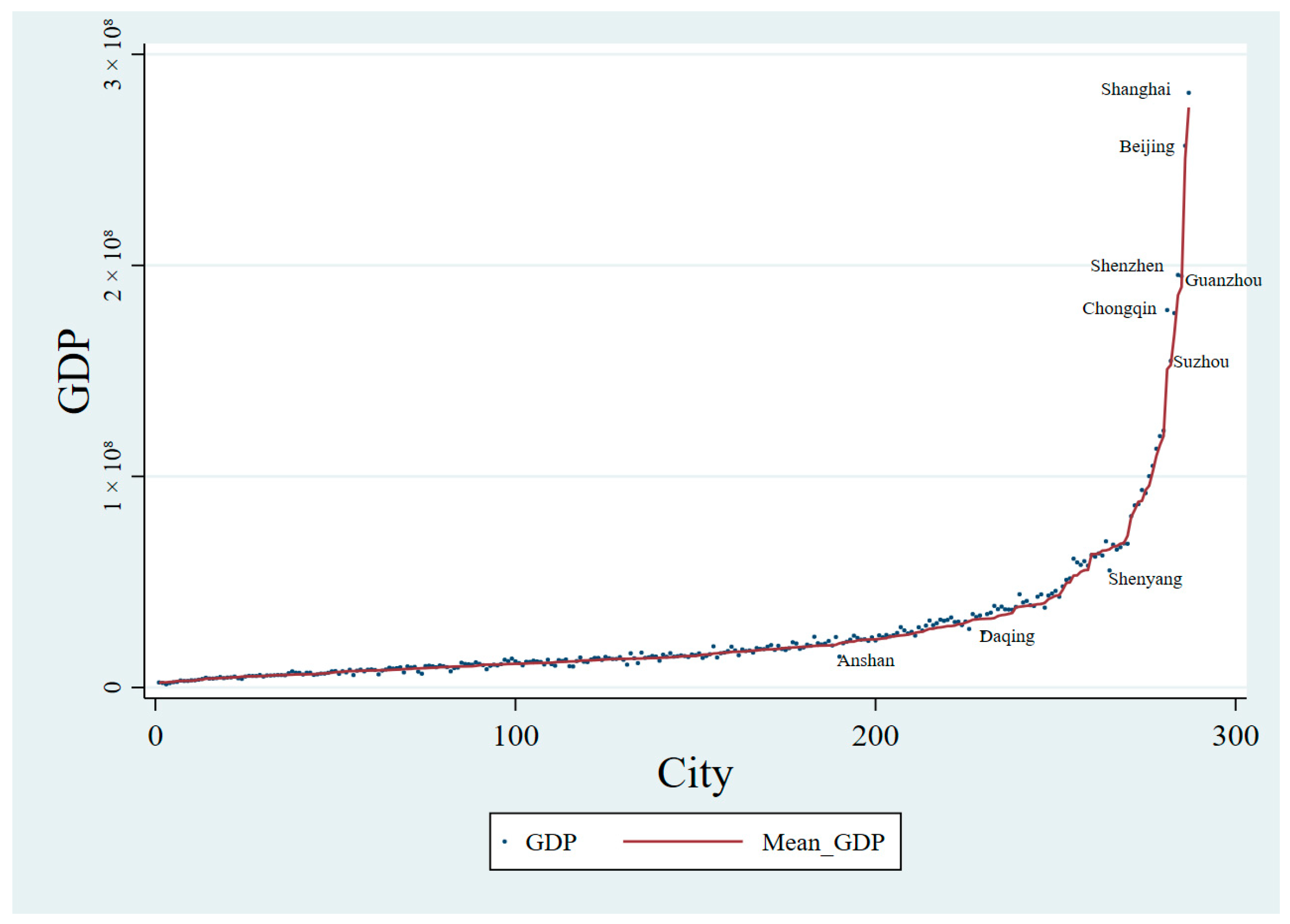

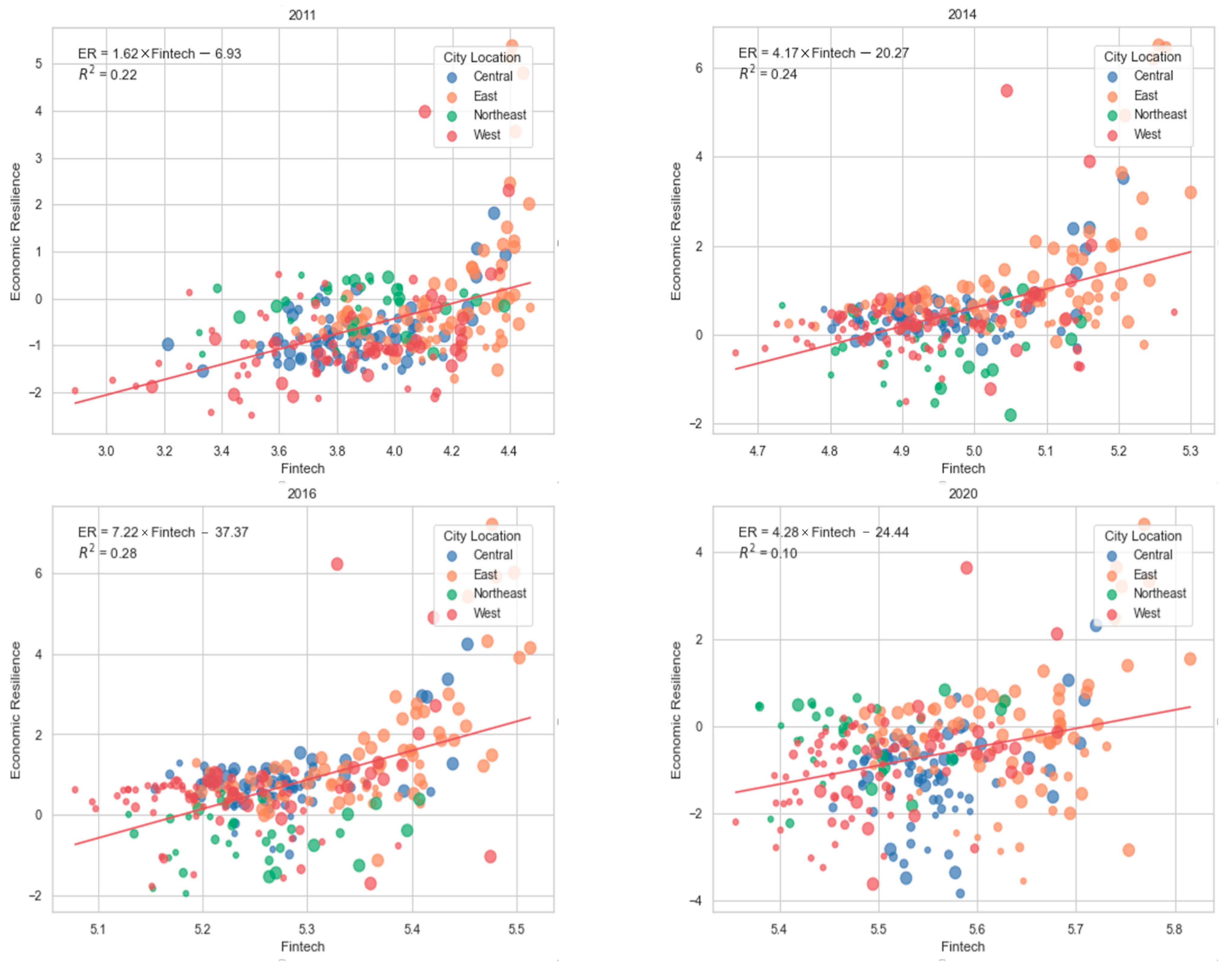

Secondly, this study developed a new method for quantifying economic resilience that adeptly captures the sensitivity and adaptability of economic systems without the prerequisite of a shock. This methodological innovation represents a significant leap forward in the quantification of economic resilience, offering a tool that can be applied universally, across various contexts and scenarios. Our empirical investigation, utilizing panel data from 286 prefecture-level cities in China from 2011 to 2020, demonstrates the utility of this method in examining the influence of Fintech on economic resilience and sheds light on the underlying mechanisms and the regional heterogeneity of this influence.

The empirical findings of this study reveal that the digital tools of Fintech significantly bolster economic resilience, serving as a new source of resilience through their facilitation of technological innovation and industrial structure upgrading. This underscores the critical role of Fintech in supporting the recovery, restructuring, and renewal of economies, thereby promoting high-quality economic growth. Our research aligns with and extends the findings of Zhou et al. [

58] and Shi et al. [

66], reinforcing the idea that Fintech is a pivotal catalyst for sustainable economic development.

However, this study is not without its limitations. Primarily, the measurement of economic resilience in this analysis was anchored solely on GDP as the input indicator. This choice, albeit grounded in the widespread availability and comparability of GDP data, may not fully encapsulate the multifaceted nature of economic resilience. Future studies could enrich our understanding of economic resilience by incorporating a broader spectrum of economic indicators, such as employment rates, industrial diversity, and innovation metrics. These additional indicators could offer a more nuanced and comprehensive view of the economic system’s resilience, capturing aspects of economic health and adaptability beyond mere output.

Furthermore, the methodology employed to calculate economic resilience indicators relied on annual aggregated GDP data, leading to a uniform adaptability value being assigned to each city throughout the study period. This approach, while facilitating a streamlined analysis, may not accurately reflect the dynamic nature of cities’ economic resilience, which can fluctuate significantly within shorter time frames due to various factors, including policy changes, market shifts, and external shocks. To address this limitation and enhance the granularity of resilience assessment, future research could leverage monthly data, or other more frequent economic indicators, to better capture the temporal variations in city’s adaptability values. Such an approach would allow for a more detailed and responsive analysis of economic resilience, providing insights into the immediate impacts of economic policies and external events on regional economies.

In summary, this research makes significant strides in the conceptualization and quantification of economic resilience and further applies this methodology to empirical examination, highlighting the transformative potential of Fintech in enhancing the resilience of economic systems. While acknowledging the limitations of the current study, we advocate for further exploration into this complex relationship, suggesting that the economic resilience calculation method proposed here can be adapted and applied in diverse contexts to explore various dimensions of resilience. This study not only contributes to academic discourse but also offers practical insights for policymakers and practitioners interested in leveraging digital transitions to fortify urban sustainability across different scales and regions.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}