Will Good Service Quality Promote Real Estate Value? Evidence from Beijing, China

Abstract

1. Introduction

2. Literature Review

3. Conceptual Framework, Hypotheses and Data

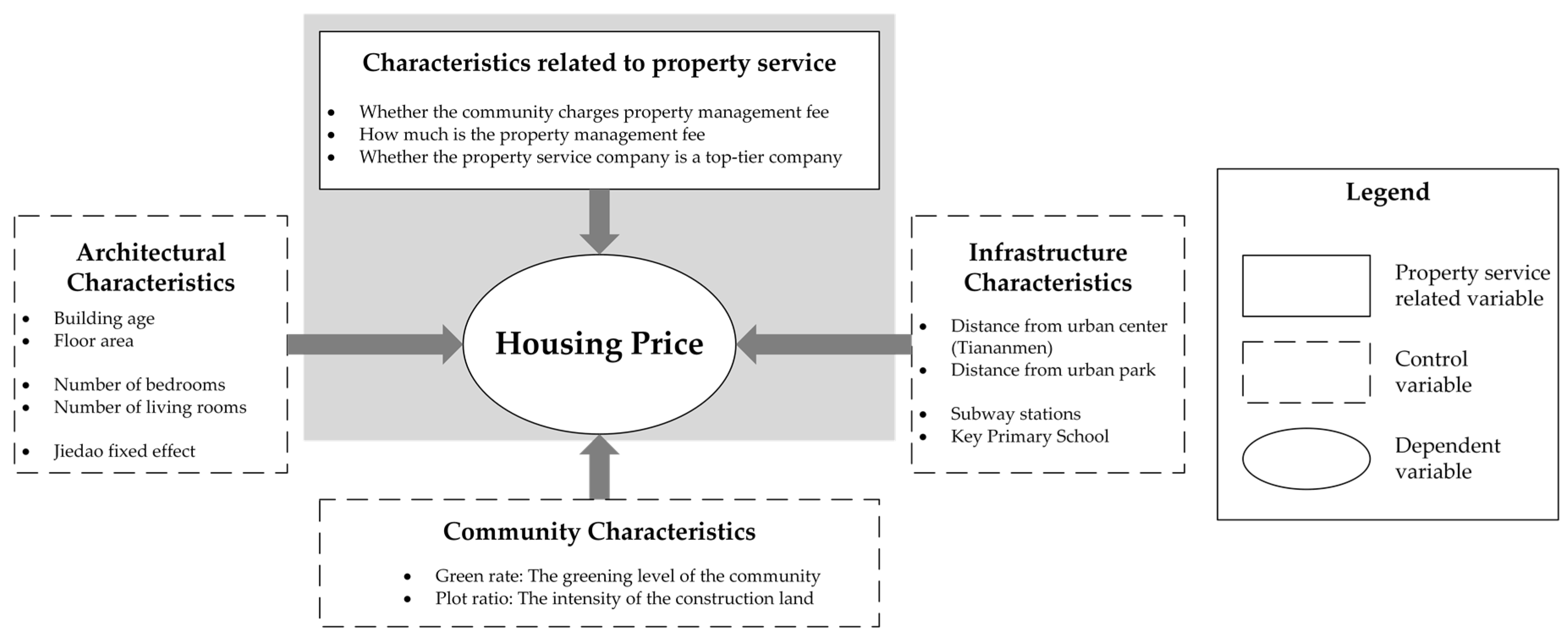

3.1. Conceptual Framework

3.2. Hypotheses and Empirical Models

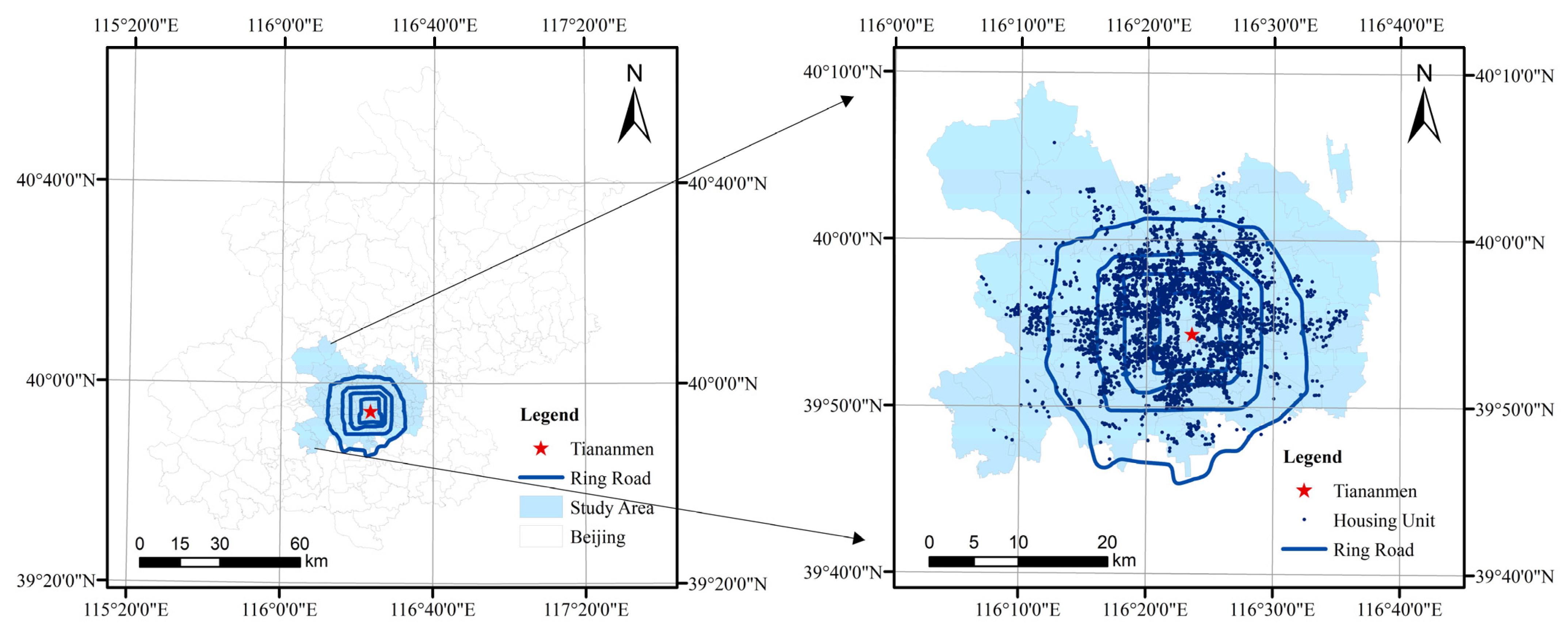

3.3. Data

3.4. Definition of Variables and Basic Descriptive Statistics

4. Empirical Results

4.1. Good Service Quality Does Show Premium in Real Estate Value

4.1.1. Compared with No Property Service, Houses with Service Do Have Higher Value

4.1.2. The Better the Service Quality, the Higher the Real Estate Value-Added

4.1.3. Top-Tier Service Quality Shows More Premium in Real Estate Value

4.2. The Premium of Good Service Quality in Real Estate Value Keeps Increasing over Time

4.3. The Premium of Good Service Quality in Real Estate Value Is Heterogeneous

5. Discussion

6. Conclusions

Author Contributions

Funding

Data Availability Statement

Acknowledgments

Conflicts of Interest

Appendix A

{kind=link}

{kind=link}

| (1) | (2) | (3) | (4) | |

|---|---|---|---|---|

| Ln_price | Ln_price | Ln_price | Ln_price | |

| D_PS | 0.050 *** | |||

| (18.465) | ||||

| PS | 0.031 *** | 0.087 *** | ||

| (49.292) | (45.637) | |||

| PS2 | −0.009 *** | |||

| (−29.156) | ||||

| D_top100 | 0.033 *** | |||

| (14.242) | ||||

| Age | −0.019 *** | −0.015 *** | −0.014 *** | −0.019 *** |

| (−114.817) | (−83.437) | (−78.349) | (−113.426) | |

| Area | −0.002 *** | −0.002 *** | −0.002 *** | −0.002 *** |

| (−54.172) | (−60.959) | (−62.600) | (−52.478) | |

| Bedroom | 0.043 *** | 0.049 *** | 0.051 *** | 0.042 *** |

| (36.356) | (40.402) | (42.395) | (34.783) | |

| Living_room | 0.055 *** | 0.057 *** | 0.056 *** | 0.055 *** |

| (52.450) | (53.518) | (53.184) | (51.640) | |

| Dis_tam | −0.035 *** | −0.030 *** | −0.035 *** | −0.035 *** |

| (−31.422) | (−26.307) | (−30.704) | (−31.017) | |

| Dispark | −0.032 *** | −0.028 *** | −0.033 *** | −0.032 *** |

| (−21.551) | (−18.800) | (−21.972) | (−21.086) | |

| Subway | 0.066 *** | 0.063 *** | 0.058 *** | 0.067 *** |

| (42.010) | (39.879) | (36.838) | (42.162) | |

| Education | 0.078 *** | 0.079 *** | 0.083 *** | 0.071 *** |

| (34.299) | (32.088) | (33.773) | (28.797) | |

| Greenrate | 0.443 *** | 0.385 *** | 0.365 *** | 0.467 *** |

| (52.802) | (43.093) | (40.945) | (53.005) | |

| Plotratio | −0.024 *** | −0.024 *** | −0.025 *** | −0.024 *** |

| (−47.557) | (−46.030) | (−47.563) | (−45.047) | |

| Constant | 10.770 *** | 10.644 *** | 10.710 *** | 10.831 *** |

| (474.056) | (457.541) | (460.721) | (464.930) | |

| Year-fixed effect | Yes | Yes | Yes | Yes |

| Grid-fixed effect | Yes | Yes | Yes | Yes |

| Observations | 155,845 | 150,400 | 150,400 | 150,400 |

| R2 | 0.778 | 0.783 | 0.785 | 0.778 |

References

- Du, H.; Mulley, C. The short-term land value impacts of urban rail transit: Quantitative evidence from Sunderland, UK. Land Use Policy 2007, 24, 223–233. [Google Scholar] [CrossRef]

- Cervero, R.; Kang, C.D. Bus rapid transit impacts on land uses and land values in Seoul, Korea. Transp. Policy 2011, 18, 102–116. [Google Scholar] [CrossRef]

- Kong, F.; Yin, H.; Nakagoshi, N. Using GIS and landscape metrics in the hedonic price modeling of the amenity value of urban green space: A case study in Jinan City, China. Landsc. Urban Plan. 2007, 79, 240–252. [Google Scholar] [CrossRef]

- Teck-Hong, T. Neighborhood preferences of house buyers: The case of Klang Valley, Malaysia. Int. J. Hous. Mark. Anal. 2011, 4, 58–69. [Google Scholar] [CrossRef]

- Tita, G.E.; Petras, T.L.; Greenbaum, R.T. Crime and Residential Choice: A Neighborhood Level Analysis of the Impact of Crime on Housing Prices. J. Quant. Criminol. 2006, 22, 299–317. [Google Scholar] [CrossRef]

- DiPasquale, D.; Wheaton, W.C. Urban Economics and Real Estate Market; Prentice Hall: Englewood Cliffs, NJ, USA, 1996. [Google Scholar]

- Yang, H.; Fu, M.; Wang, L.; Tang, F. Mixed Land Use Evaluation and Its Impact on Housing Prices in Beijing Based on Multi-Source Big Data. Land 2021, 10, 1103. [Google Scholar] [CrossRef]

- Zuo, W.; Zhang, X.; Zeng, S.; Liu, L. A LINMAP Method Based on the Bounded Rationality of Evaluators for Property Service Quality Evaluation. IEEE Access 2021, 9, 122668–122684. [Google Scholar] [CrossRef]

- Dai, J.; Lv, P.; Ma, Z.; Bi, J.; Wen, T. Environmental risk and housing price: An empirical study of Nanjing, China. J. Clean. Prod. 2020, 252, 119828. [Google Scholar] [CrossRef]

- Li, S.; Jiang, Y.; Ke, S.; Nie, K.; Wu, C. Understanding the Effects of Influential Factors on Housing Prices by Combining Extreme Gradient Boosting and a Hedonic Price Model (XGBoost-HPM). Land 2021, 10, 533. [Google Scholar] [CrossRef]

- Luo, J.; Zhang, X.; Wu, Y.; Shen, J.; Shen, L.; Xing, X. Urban land expansion and the floating population in China: For production or for living? Cities 2018, 74, 219–228. [Google Scholar] [CrossRef]

- Wang, P.; Zeng, C.; Song, Y.; Guo, L.; Liu, W.; Zhang, W. The Spatial Effect of Administrative Division on Land-Use Intensity. Land 2021, 10, 543. [Google Scholar] [CrossRef]

- Gao, Y.; Li, H.; Song, Y. Interaction Relationship between Urbanization and Land Use Multifunctionality: Evidence from Han River Basin, China. Land 2021, 10, 938. [Google Scholar] [CrossRef]

- Muth, R. The Derived Demand for Urban Residential Land. Urban Stud. 1971, 8, 243–254. [Google Scholar] [CrossRef]

- Manning, C.A. The Determinants of Intercity Home Building Site Price Differences. Land Econ. 1988, 64, 1–14. [Google Scholar] [CrossRef]

- Wen, H.; Goodman, A.C. Relationship between urban land price and housing price: Evidence from 21 provincial capitals in China. Habitat Int. 2013, 40, 9–17. [Google Scholar] [CrossRef]

- Liu, R.Q.; Jiang, Y.M. Study on housing price determining land price and passingly discuss current macro policy on real estate industry. Soc. Sci. Res. 2005, 6, 44–48. [Google Scholar]

- Bishop, K.C.; Murphy, A.D. Estimating the Willingness to Pay to Avoid Violent Crime: A Dynamic Approach. Am. Econ. Rev. 2011, 101, 625–629. [Google Scholar] [CrossRef]

- Wang, Y.; Ran, R.; Deng, G. Neighborhood Quality and Housing Value: Evidence from Urban Micro Data. J. Manag. Sustain. 2012, 2, 128. [Google Scholar] [CrossRef]

- Clapp, J.M.; Nanda, A.; Ross, S.L. Which school attributes matter? The influence of school district performance and demographic composition on property values. J. Urban Econ. 2008, 63, 451–466. [Google Scholar] [CrossRef]

- Wen, H.; Xiao, Y.; Hui, E.C.M.; Zhang, L. Education quality, accessibility, and housing price: Does spatial heterogeneity exist in education capitalization? Habitat Int. 2018, 78, 68–82. [Google Scholar] [CrossRef]

- Gibbons, S. Paying for Good Neighbours: Estimating the Value of an Implied Educated Community. Urban Stud. 2003, 40, 809–833. [Google Scholar] [CrossRef]

- Zhang, S.; Wang, L.; Lu, F. Exploring Housing Rent by Mixed Geographically Weighted Regression: A Case Study in Nanjing. ISPRS Int. J. Geo-Inf. 2019, 8, 431. [Google Scholar] [CrossRef]

- Wu, C.; Ye, X.; Du, Q.; Luo, P. Spatial effects of accessibility to parks on housing prices in Shenzhen, China. Habitat Int. 2017, 63, 45–54. [Google Scholar] [CrossRef]

- Dai, X.; Bai, X.; Xu, M. The influence of Beijing rail transfer stations on surrounding housing prices. Habitat Int. 2016, 55, 79–88. [Google Scholar] [CrossRef]

- Schwarz, N.; Haase, A.; Haase, D.; Kabisch, N.; Kabisch, S.; Liebelt, V.; Rink, D.; Strohbach, M.W.; Welz, J.; Wolff, M. How Are Urban Green Spaces and Residential Development Related? A Synopsis of Multi-Perspective Analyses for Leipzig, Germany. Land 2021, 10, 630. [Google Scholar] [CrossRef]

- Chen, W.Y.; Jim, C.Y. Amenities and disamenities: A hedonic analysis of the heterogeneous urban landscape in Shenzhen (China). Geogr. J. 2010, 176, 227–240. [Google Scholar] [CrossRef]

- Kim, H.-S.; Lee, G.-E.; Lee, J.-S.; Choi, Y. Understanding the local impact of urban park plans and park typology on housing price: A case study of the Busan metropolitan region, Korea. Landsc. Urban Plan. 2019, 184, 1–11. [Google Scholar] [CrossRef]

- Xiao, Y.; Hui, E.C.M.; Wen, H. Effects of floor level and landscape proximity on housing price: A hedonic analysis in Hangzhou, China. Habitat Int. 2019, 87, 11–26. [Google Scholar] [CrossRef]

- Zhang, Y.; Zhang, T.; Zeng, Y.; Yu, C.; Zheng, S. The rising and heterogeneous demand for urban green space by Chinese urban residents: Evidence from Beijing. J. Clean. Prod. 2021, 313, 127781. [Google Scholar] [CrossRef]

- Lynch, A.K.; Rasmussen, D.W. Measuring the impact of crime on house prices. Appl. Econ. 2010, 33, 1981–1989. [Google Scholar] [CrossRef]

- Buonanno, P.; Montolio, D.; Raya-Vílchez, J.M. Housing prices and crime perception. Empir. Econ. 2012, 45, 305–321. [Google Scholar] [CrossRef]

- Foster, W.; Anríquez, G.; Melo, O.; Yupanqui, D.; Ortega, J. Geographic disparities in rural land appreciation in a transforming economy: Chile, 1980 to 2007. Land Use Policy 2016, 57, 655–668. [Google Scholar] [CrossRef]

- Ge, K.; Zou, S.; Chen, D.; Lu, X.; Ke, S. Research on the Spatial Differences and Convergence Mechanism of Urban Land Use Efficiency under the Background of Regional Integration: A Case Study of the Yangtze River Economic Zone, China. Land 2021, 10, 1100. [Google Scholar] [CrossRef]

- Read, D.C.; Carswell, A. Is property management viewed as a value-added service? Prop. Manag. 2019, 37, 262–274. [Google Scholar] [CrossRef]

- Huang, Y.-H.; Lee, P.-C. Role of Property Management in Service Demands of Elderly Residents of Apartment Complexes. Int. J. Strateg. Prop. Manag. 2019, 24, 24–37. [Google Scholar] [CrossRef]

- Liu, G.; Wang, X.; Gu, J.; Liu, Y.; Zhou, T. Temporal and spatial effects of a ‘Shan Shui’ landscape on housing price: A case study of Chongqing, China. Habitat Int. 2019, 94, 102068. [Google Scholar] [CrossRef]

- Tyrväinen, L.; Miettinen, A. Property Prices and Urban Forest Amenities. J. Environ. Econ. Manag. 2000, 39, 205–223. [Google Scholar] [CrossRef]

- Price, C. Valuation of unpriced products: Contingent valuation, cost–benefit analysis and participatory democracy. Land Use Policy 2000, 17, 187–196. [Google Scholar] [CrossRef]

- Zheng, S.; Sun, W.; Wang, R. Land Supply and Capitalization of Public Goods in Housing Prices: Evidence from Beijing. J. Reg. Sci. 2014, 54, 550–568. [Google Scholar] [CrossRef]

- Chen, P. Conservative Governance of urban grassroots community: A case study of the property fee adjustment process in B City in May. Qiusuo 2018, 11, 107–117. [Google Scholar] [CrossRef]

- Chen, P. Urban community property cost dilemma and its countermeasures. Soc. Gov. 2018, 6, 48–53. [Google Scholar] [CrossRef]

- Chen, Q.; Tang, J. Research on Pricing Actualization Mechanism of Residential Property Management Fee Based on Recessive Monopolization. Int. Conf. Appl. Soc. Sci. Res. 2013, 8, 83–86. [Google Scholar] [CrossRef][Green Version]

- Yin, M. Property management in Community governance: The impact of service quality on residents’ sense of belonging. Southeast Acad. 2020, 10, 162–171. [Google Scholar] [CrossRef]

- Zhang, Y.; Li, X.; Nie, T.; Qi, J.; Chen, J.; Wu, Q. Source apportionment of PM2.5 pollution in the central six districts of Beijing, China. J. Clean. Prod. 2018, 174, 661–669. [Google Scholar] [CrossRef]

- Zheng, S.; Hu, W.; Wang, R. How Much Is a Good School Worth in Beijing? Identifying Price Premium with Paired Resale and Rental Data. J. Real Estate Financ. Econ. 2015, 53, 184–199. [Google Scholar] [CrossRef]

- Zhang, T.; Zeng, Y.; Zhang, Y.; Song, Y.; Li, H. The Heterogenous Demand for Urban Parks between Home Buyers and Renters: Evidence from Beijing. Sustainability 2020, 12, 9058. [Google Scholar] [CrossRef]

- Chen, W.Y. Environmental externalities of urban river pollution and restoration: A hedonic analysis in Guangzhou (China). Landsc. Urban Plan. 2017, 157, 170–179. [Google Scholar] [CrossRef]

- Zheng, S.; Wu, J.; Kahn, M.E.; Deng, Y. The nascent market for “green” real estate in Beijing. Eur. Econ. Rev. 2012, 56, 974–984. [Google Scholar] [CrossRef]

- Brookshire, D.S.; Thayer, M.A.; Schulze, W.D.; d’Arge, R.C. Valuing Public Goods: A Comparison of Survey and Hedonic Approaches. Am. Econ. Rev. 1982, 72, 165–177. [Google Scholar]

- Wu, Y.; Chen, Y.; Deng, X.; Hui, E.C.M. Development of characteristic towns in China. Habitat Int. 2018, 77, 21–31. [Google Scholar] [CrossRef]

- Wu, Y.; Shan, L.; Zheng, S.; Lai, S.-K.; Xia, B. Regional Planning Reconfiguration in China Based on Inclusiveness: Examining Development and Control Orientation. J. Urban Plan. Dev. 2020, 146, 05020012. [Google Scholar] [CrossRef]

| Variable Type | Variable Name | Variable Meaning | Descriptive Statistics | |

|---|---|---|---|---|

| Mean | Standard Deviation | |||

| Dependent variable | Ln_price | The natural logarithm of the housing price per square meter | 10.88 | 0.37 |

| Characteristics related to property service | D_PS | Whether the community charges property management fee: yes = 1; otherwise = 0 | 0.91 | 0.29 |

| PS | Property management fee of the community (yuan/m2/month) | 1.96 | 1.15 | |

| D_top100 | Whether the property service company is a top-tier company: yes = 1; otherwise = 0 | 0.06 | 0.24 | |

| Architectural characteristics | Age | Housing age (years) | 21.47 | 9.06 |

| Area | The total area of the house (square meters) | 80.75 | 37.34 | |

| Bedroom | Number of bedrooms in the house | 2.00 | 0.77 | |

| Living_room | Number of living rooms in the house | 1.13 | 0.48 | |

| Infrastructure characteristics | Dis_tam | The distance from the community to Tiananmen Square (km) | 9.05 | 3.78 |

| Dispark | The distance from the community to the nearest park (km) | 1.23 | 0.63 | |

| Subway | The number of subway stations within 1 km of the neighborhood | 0.76 | 0.43 | |

| Education | Whether there are key primary schools around the neighborhood: yes = 1; otherwise = 0 | 0.10 | 0.30 | |

| Community characteristics | Greenrate | The greening level of the community (percent) | 0.32 | 0.07 |

| Plotratio | The intensity of the construction land used in the community (percent) | 2.64 | 1.23 | |

| (1) | (2) | (3) | (4) | |

|---|---|---|---|---|

| Ln_price | Ln_price | Ln_price | Ln_price | |

| D_PS | 0.042 *** | |||

| (15.793) | ||||

| PS | 0.036 *** | 0.074 *** | ||

| (60.114) | (42.459) | |||

| PS2 | −0.006 *** | |||

| (−21.840) | ||||

| D_top100 | 0.030 *** | |||

| (13.765) | ||||

| Age | −0.020 *** | −0.014 *** | −0.014 *** | −0.020 *** |

| (−129.630) | (−84.919) | (−80.392) | (−127.286) | |

| Area | −0.002 *** | −0.002 *** | −0.002 *** | −0.002 *** |

| (−54.378) | (−62.767) | (−63.198) | (−52.741) | |

| Bedroom | 0.041 *** | 0.047 *** | 0.048 *** | 0.040 *** |

| (35.216) | (39.526) | (40.341) | (33.308) | |

| Living_room | 0.054 *** | 0.055 *** | 0.055 *** | 0.055 *** |

| (50.998) | (51.533) | (51.439) | (50.630) | |

| Dis_tam | −0.041 *** | −0.036 *** | −0.036 *** | −0.042 *** |

| (−82.299) | (−72.313) | (−72.514) | (−82.297) | |

| Dispark | −0.036 *** | −0.035 *** | −0.038 *** | −0.036 *** |

| (−30.028) | (−28.772) | (−30.728) | (−28.951) | |

| Subway | 0.047 *** | 0.039 *** | 0.038 *** | 0.048 *** |

| (35.622) | (29.201) | (28.847) | (35.941) | |

| Education | 0.051 *** | 0.052 *** | 0.056 *** | 0.042 *** |

| (26.015) | (25.644) | (27.981) | (20.400) | |

| Greenrate | 0.416 *** | 0.377 *** | 0.363 *** | 0.447 *** |

| (50.079) | (43.421) | (42.033) | (51.679) | |

| Plotratio | −0.019 *** | −0.019 *** | −0.020 *** | −0.020 *** |

| (−38.062) | (−36.642) | (−38.145) | (−37.923) | |

| Constant | 10.699 *** | 10.553 *** | 10.503 *** | 10.736 *** |

| (991.495) | (1025.196) | (1000.539) | (1012.185) | |

| Year-fixed effect | Yes | Yes | Yes | Yes |

| Jiedao-fixed effect | Yes | Yes | Yes | Yes |

| Observations | 155,845 | 150,400 | 150,400 | 150,400 |

| R2 | 0.773 | 0.781 | 0.782 | 0.774 |

| (1) | (2) | |

|---|---|---|

| Ln_price | Ln_price | |

| D_PS | 0.028 *** | |

| (4.965) | ||

| D_PS × Year | 0.003 *** | |

| (2.803) | ||

| PS | 0.023 *** | |

| (18.130) | ||

| PS × Year | 0.003 *** | |

| (11.204) | ||

| Year | 0.112 *** | 0.109 *** |

| (99.908) | (166.274) | |

| Constant | 10.598 *** | 10.468 *** |

| (898.055) | (989.059) | |

| Control other variables | Yes | Yes |

| Year-fixed effect | Yes | Yes |

| Jiedao-fixed effect | Yes | Yes |

| Observations | 155,845 | 150,400 |

| R2 | 0.773 | 0.781 |

| (1) | (2) | (3) | (4) | (5) | |

|---|---|---|---|---|---|

| Ln_price | Ln_price | Ln_price | Ln_price | Ln_price | |

| D_highprice × PS | 0.027 *** | 0.017 *** | |||

| (31.271) | (17.021) | ||||

| D_highprice | 0.094 *** | 0.145 *** | |||

| (39.242) | (54.744) | ||||

| D_large × PS | 0.030 *** | 0.006 *** | |||

| (30.743) | (5.915) | ||||

| D_large | −0.097 *** | −0.096 *** | |||

| (−43.546) | (−39.806) | ||||

| D_old × PS | −0.021 *** | −0.016 *** | |||

| (−20.245) | (−16.062) | ||||

| D_old | −0.046 *** | −0.006 ** | |||

| (−18.837) | (−2.489) | ||||

| D_suburbs × PS | 0.027 *** | 0.024 *** | |||

| (27.008) | (26.132) | ||||

| D_suburbs | −0.151 *** | −0.135 *** | |||

| (−44.393) | (−43.561) | ||||

| PS | 0.022 *** | 0.012 *** | 0.042 *** | 0.024 *** | 0.014 *** |

| (33.002) | (14.299) | (62.964) | (29.194) | (14.042) | |

| Constant | 10.615 *** | 10.618 *** | 10.458 *** | 10.537 *** | 10.514 *** |

| (1117.656) | (1032.164) | (984.890) | (1018.480) | (1079.082) | |

| Control other variables | Yes | Yes | Yes | Yes | Yes |

| Year-fixed effect | Yes | Yes | Yes | Yes | Yes |

| Jiedao-fixed effect | Yes | Yes | Yes | Yes | Yes |

| Observations | 150,400 | 150,400 | 150,400 | 150,400 | 150,400 |

| R2 | 0.806 | 0.775 | 0.780 | 0.784 | 0.815 |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2022 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Liu, F.; Chen, K.; Zhang, T.; Zhang, Y.; Song, Y. Will Good Service Quality Promote Real Estate Value? Evidence from Beijing, China. Land 2022, 11, 166. https://doi.org/10.3390/land11020166

Liu F, Chen K, Zhang T, Zhang Y, Song Y. Will Good Service Quality Promote Real Estate Value? Evidence from Beijing, China. Land. 2022; 11(2):166. https://doi.org/10.3390/land11020166

Chicago/Turabian StyleLiu, Fangyuan, Kaili Chen, Tianzheng Zhang, Yingjie Zhang, and Yan Song. 2022. "Will Good Service Quality Promote Real Estate Value? Evidence from Beijing, China" Land 11, no. 2: 166. https://doi.org/10.3390/land11020166

APA StyleLiu, F., Chen, K., Zhang, T., Zhang, Y., & Song, Y. (2022). Will Good Service Quality Promote Real Estate Value? Evidence from Beijing, China. Land, 11(2), 166. https://doi.org/10.3390/land11020166