Diffusion of Electronic Water Payment Innovations in Urban Ghana. Evidence from Tema Metropolis

Abstract

1. Introduction

2. Materials and Methods

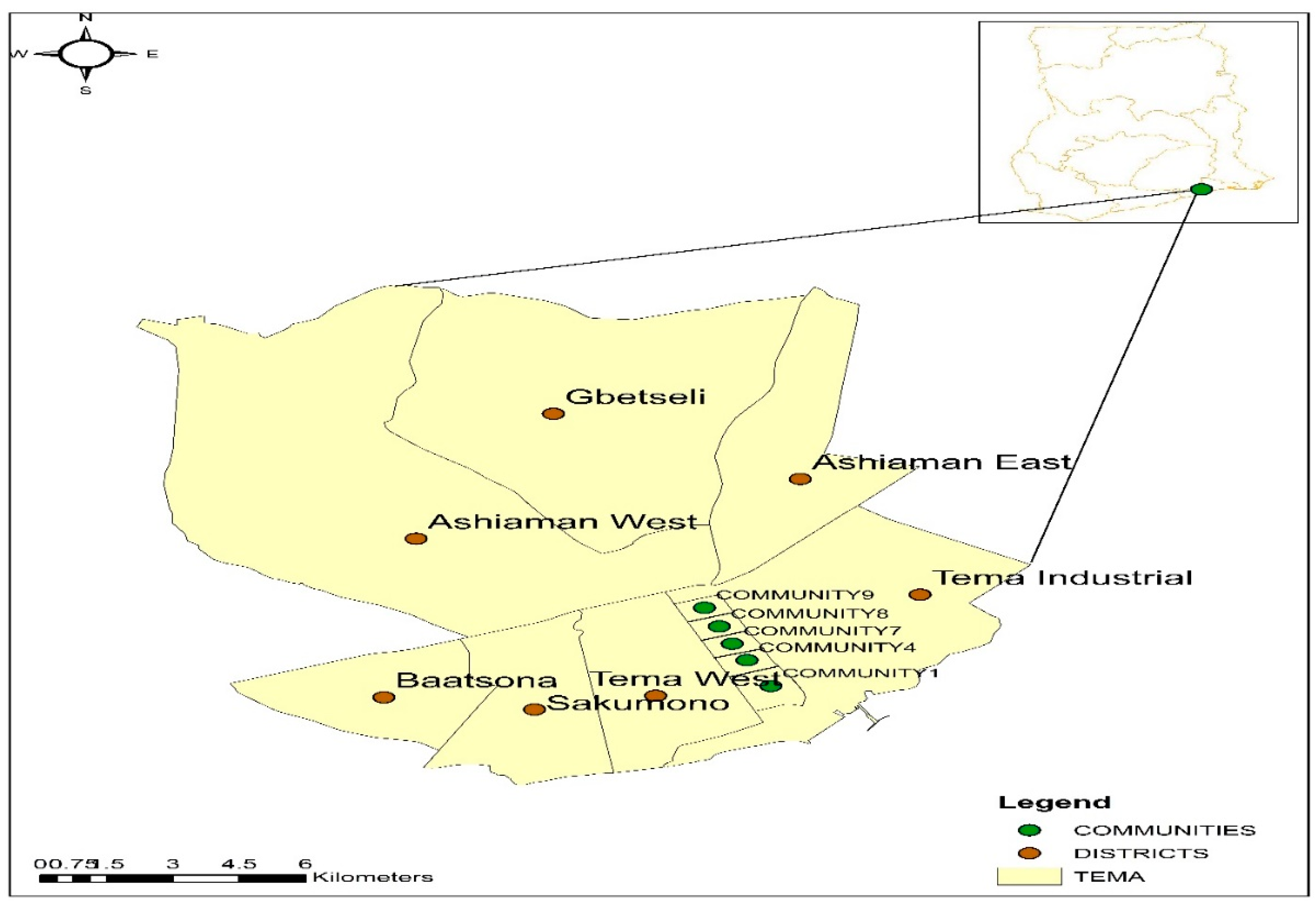

2.1. Study Design and Context

2.2. Sampling and Data Collection

2.3. Data Analysis

3. Results

3.1. Sample Characteristics and Determinants of Differences in EWP Awareness

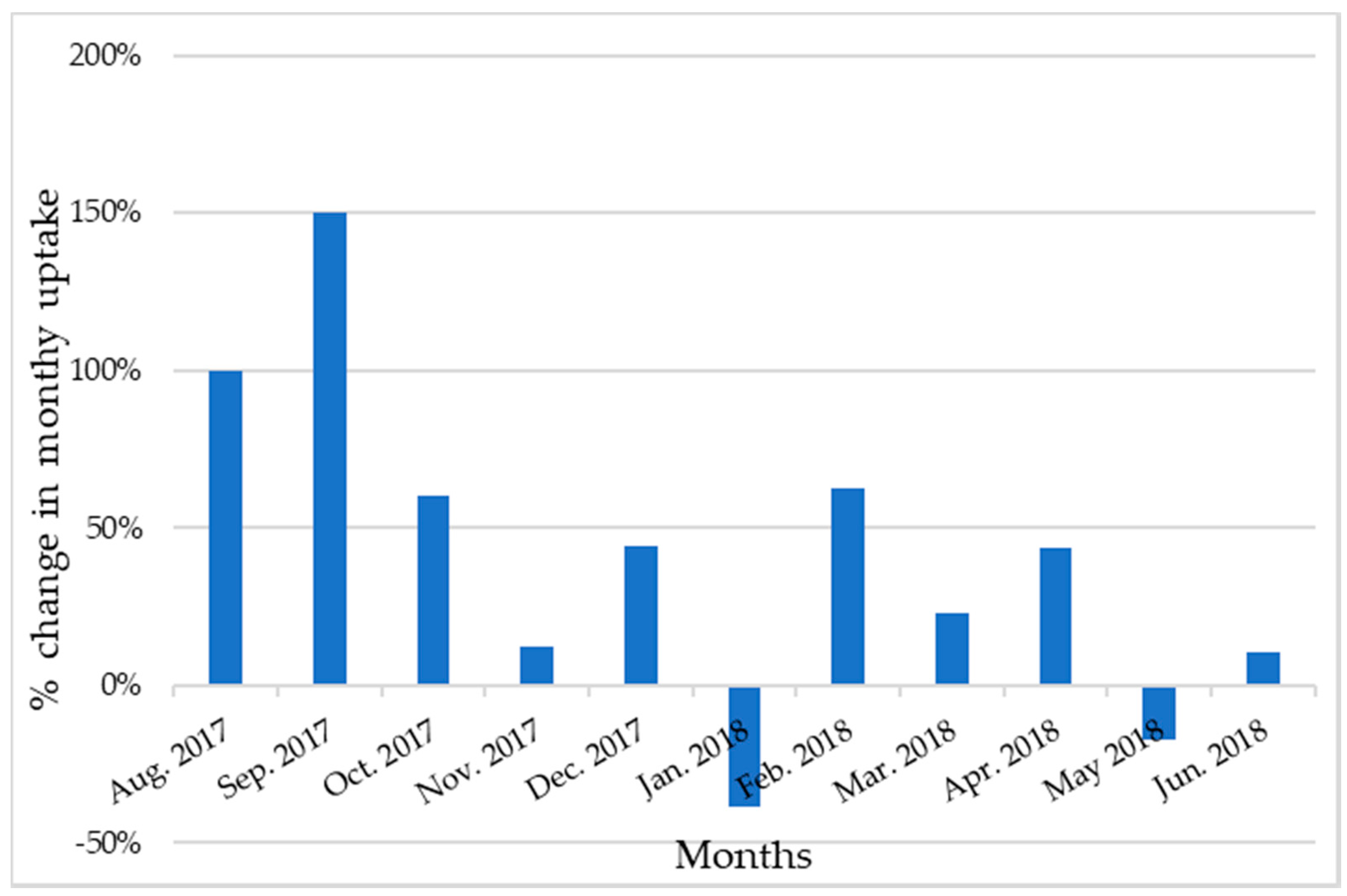

3.2. Level of EWP Diffusion

3.3. Water Use Variation by Payment Type

4. Discussion

5. Conclusions

Author Contributions

Funding

Acknowledgments

Conflicts of Interest

Data Availability

Abbreviations

Appendix A

{kind=link}

{kind=link}

| S/N | Items and Filters | Response Categories | |

|---|---|---|---|

| 001 | GWCL account Number | ||

| ( ) | |||

| Don’t know | ( ) | ||

| No answer | ( ) | ||

| 002 | Is it a single household? If No, go to 004 | No | ( ) |

| Yes | ( ) | ||

| 003 | If yes, what is the size of your household Actual number in box | 1–3 | ( ) |

| 4–6 | ( ) | ||

| 7–9 | ( ) | ||

| ≥10 | ( ) | ||

| Don’t want to answer | ( ) | ||

| 004 | If no, how many people regularly use the piped water |

| S/N | Items and Filters | Response Categories | |

|---|---|---|---|

| 101 | Which age group are you? | 18–30 years | ( ) |

| 31–40 years | ( ) | ||

| 41–50 years | ( ) | ||

| 51–60 years | ( ) | ||

| ≥61 years | ( ) | ||

| Don’t want to answer | ( ) | ||

| 102 | Gender? | Male | ( ) |

| Female | ( ) | ||

| Don’t want to answer | ( ) | ||

| 103 | Highest Educational level | Basic | ( ) |

| Secondary | ( ) | ||

| Tertiary | ( ) | ||

| No formal education | ( ) | ||

| Other | ( ) | ||

| Don’t want to answer | ( ) | ||

| 104 | Employment status | Not employed | ( ) |

| Employed (public sector) | ( ) | ||

| Employed (Private sector) | ( ) | ||

| Self employed | ( ) | ||

| Retired | ( ) | ||

| Other | ( ) | ||

| Don’t want to answer | ( ) | ||

| 105 | Estimated average monthly income? | ≤¢300 | ( ) |

| ¢301–700 | ( ) | ||

| ¢701–1000 | ( ) | ||

| ¢1001–1500 | ( ) | ||

| ¢1501–2000 | ( ) | ||

| ≥¢2000 | ( ) | ||

| Don’t want to answer | ( ) |

| S/N | Do You Have/Own Any of the Following | No | Yes | |

|---|---|---|---|---|

| 201 | Mobile phone | ( ) | ( ) | |

| 204 | Mobile money account | ( ) | ( ) | |

| 205 | Bank account | ( ) | ( ) | |

| S/N | In the Last Three Months Have You (Tick √ All That Apply): | No | Yes | |

| 206 | Used mobile device | ( ) | ( ) | |

| 207 | Phoned/ messaged a helpline (e.g., GWCL info Centre, etc) for water services | ( ) | ( ) | |

| 208 | Made any electronic transaction (utility) | ( ) | ( ) | |

| 209 | Do you use any mobile service | ( ) | ( ) | |

| 210 | If yes which services (network) do you use | Vodafone | ( ) | |

| MTN | ( ) | |||

| Airtel-Tigo | ( ) | |||

| Glo | ( ) | |||

| Others(Specify) | ( ) | |||

| 211 | How do you receive/ get your water bills? | SMS | ( ) | |

| ( ) | ||||

| Customer Portal (GWCL) | ( ) | |||

| Paper bills | ( ) | |||

| Other (Specify) | ( ) | |||

| S/N | Tick for All That Apply and Explain Where Appropriate | No | Yes | |

| 212 | Are you aware of Electronic Water Payment Systems (EWPs) If No, go to 301 | ( ) | ( ) | |

| 212a | If yes, what is it about (Explain) | |||

| 213 | Has GWCL ever given you information (e.g., a web address) on how to use EWPs? | ( ) | ( ) | |

| 214 | Do you use EWPs? | ( ) | ( ) | |

| 215 | Have you used GWCL EWPs for any water related transaction in the last three months? | ( ) | ( ) | |

References

- WWAP (UNESCO World Water Assessment Programme). The United Nations World Water Development Report 2019: Leaving No One Behind; UNESCO: Paris, France, 2019. [Google Scholar]

- Dos Santos, S.; Adams, E.A.; Neville, G.; Wada, Y.; de Sherbinin, A.; Bernhardt, E.M.; Adamo, S.B. Urban growth and water access in sub-Saharan Africa: Progress, challenges, and emerging research directions. Sci. Total Environ. 2017, 607, 497–508. [Google Scholar] [CrossRef] [PubMed]

- Adams, E.A.; Sambu, D.; Smiley, S.L. Urban water supply in Sub-Saharan Africa: Historical and emerging policies and institutional arrangements. Int. J. Water Resour. Dev. 2019, 35, 240–263. [Google Scholar] [CrossRef]

- World Health Organization; UNICEF. Progress on Drinking Water, Sanitation and Hygiene: 2017 Update and SDG Baselines; Licence: CC BY-NC-SA 3.0 IGO; World Health Organization (WHO) and the United Nations Children’s Fund (UNICEF): Geneva, Switzerland, 2017. [Google Scholar]

- Bakker, K. Privatizing Water: Governance Failure and the World’s Urban Water Crisis; Cornell University Press: London, UK, 2010. [Google Scholar]

- Gonzalez-Gomez, F.; Garcia-Rubio, M.; Guardiola, J. Why Is Non-Revenue Water So High in So Many Cities? Int. J. Water Resour. Dev. 2011, 27, 345–360. [Google Scholar] [CrossRef]

- Banerjee, S.G.; Morella, E. Africa’s Water and Sanitation Infrastructure: Access, Affordability, and Alternatives; The World Bank: Washington, DC, USA, 2011. [Google Scholar]

- Rouse, M. Institutional Governance and Regulation of Water Services: The Essential Elements, 2nd ed.; IWA Publishing: London, UK, 2013. [Google Scholar]

- Hope, R.; Foster, T.; Krolikowski, A.; Cohen, I. Mobile Water Payment Innovations in Urban Africa; School of Geography and the Environment and Skoll Centre for Social Entrepreneurship at Saïd Business School: Oxford, UK, December 2011; Available online: https://www.smithschool.ox.ac.uk/research/water/publications/Mobile-Water-Payment-Innovations.pdf (accessed on 5 January 2018).

- Hope, R.; Rouse, M. Risks and responses to universal drinking water security. Phil. Trans. R. Soc. A 2013, 371, 20120417. [Google Scholar] [CrossRef] [PubMed]

- Davis, J. Corruption in public service delivery: Experience from South Asia’s water and sanitation sector. World Dev. 2004, 32, 53–71. [Google Scholar] [CrossRef]

- Kayaga, S.; Franceys, R.; Sansom, K. Bill payment behaviour in urban water services: Empirical data from Uganda. J. Water Supply Res. Technol. Aqua 2004, 53, 339–349. [Google Scholar] [CrossRef][Green Version]

- Owen, D.A.L. Smart Water Technologies and Techniques: Data Capture and Analysis for Sustainable Water Management; John Wiley & Sons: Oxford, UK, 2018. [Google Scholar]

- GSMA. Key Trends in Mobile-Enabled Water Services: What’s Working and What’s Next. 2018. Available online: https://www.gsma.com/mobilefordevelopment/wp-content/uploads/2018/08/Key-trends-in-mobile-enabled-water-services-What%E2%80%99s-working-and-what%E2%80%99s-next.pdf (accessed on 25 August 2018).

- Foster, T.; Hope, R.; Thomas, M.; Cohen, I.; Krolikowski, A.; Nyaga, C. Impacts and implications of mobile water payments in East Africa. Water Int. 2012, 37, 788–804. [Google Scholar] [CrossRef]

- Hope, R.; Foster, T.; Money, A.; Rouse, M.; Money, N.; Thomas, M. Smart Water Systems; Project Report to UK DFID; Oxford University: Oxford, UK, April 2011. [Google Scholar]

- Hope, R.; Foster, T.; Money, A.; Rouse, M. Harnessing mobile communications innovations for water security. Glob. Policy 2012, 3, 433–442. [Google Scholar] [CrossRef]

- Krolikowski, A. Can mobile-enabled payment methods reduce petty corruption in urban water provision? Water Altern. 2014, 7, 235–255. [Google Scholar]

- Sualihu, M.A.; Rahman, M.A.; Tofik-Abu, Z. The Payment Behaviour of Water Utility Customers in the Greater Accra Region of Ghana: An Empirical Analysis. SAGE Open 2017, 7, 2158244017731494. [Google Scholar] [CrossRef]

- Boakye, E.; Nyieku, I.E. Cost Recovery Analysis of Ghana Water Company Limited (Gwcl): A Case Study of Sekondi-Takoradi Metropolis. Eur. J. Sci. Res. 2010, 46, 119–125. [Google Scholar]

- Joyfm. Ghana Water Company Rolls Out New Technology to Check Billing Challenges. 2017. Available online: https://www.myjoyonline.com/news/2017/october-24th/ghana-water-company-rolls-out-new-technology-to-check-billing-challenges.php (accessed on 12 January 2018).

- Sualihu, M.A.; Rahman, M.A. Defaulting on water utility bills: Evidence from the Greater Accra Region of Ghana. Indian J. Financ. 2014, 8, 22–34. [Google Scholar] [CrossRef]

- GWCL. Ghana Water Company Limited Portal. 2017. Available online: www.gwcl.com.gh/e-billing_press_release (accessed on 27 November 2017).

- NCA. Quarterly Statistical Bulletin on Communications in Ghana. July–September 2017. Available online: https://nca.org.gh/assets/Uploads/stats-bulletin-Q3-2018.pdf (accessed on 28 January 2018).

- GSMA. Country Overview, Ghana: Driving Mobile-Enabled Digital Transformation; GSMA: London, UK, 2017; Available online: https://www.gsmaintelligence.com/research/?file=986feba592e4e9c07ff793916212eb66&download (accessed on 12 January 2018).

- Boyle, T.; Giurco, D.; Mukheibir, P.; Liu, A.; Moy, C.; White, S.; Stewart, R. Intelligent metering for urban water: A review. Water 2013, 5, 1052–1081. [Google Scholar] [CrossRef]

- Amankwaa, G. Moving paperless? The Adoption of Electronic Water Payment Systems in Metropolitan Tema, Ghana. Master’s Thesis, University of Oxford, Oxford, UK, 2018. [Google Scholar]

- Ghana Statistical Service (GSS). 2010 Population and Housing Census; District Analytical Report, Tema Metropolitan, TMA; GSS: Accra, Ghana, 2014. [Google Scholar]

- GWCL. GWCL e-Billing Project: Progress Report; Number 21.12.07.18; Ghana Water Company Limited: Accra, Ghana, 2018. [Google Scholar]

- Bank of Ghana. Payment System Oversight: Annual Report. 2017. Available online: https://www.bog.gov.gh/privatecontent/Payment%20Systems/Payment%20Systems%20Annual%20Report%202017.pdf (accessed on 6 June 2018).

- Krolikowski, A.; Hope, R. Determinants of Customer Payment Behaviours in the Urban Water Sector; Evidence from Dar es Salaam, Tanzania; Smith School of Enterprise and the Environment; Water Programme, Working Paper 4; Oxford University: Oxford, UK, 2016; Available online: http://www.smithschool.ox.ac.uk/research/water/WaterProgramme_Working%20Paper04_20Mar16.pdf (accessed on 10 February 2018).

- Polasik, M.; Gorka, J.; Wilczewski, G.; Kunkowski, J.; Przenajkowska, K.; Tetkowska, N. Time Efficiency of Point-of-Sale Payment Methods: Empirical Results for Cash, Cards and Mobile Payments; Cordeiro, J., Maciaszek, L.A., Filipe, J., Eds.; Enterprise I: Wroclaw, Poland, 2013. [Google Scholar]

- Banafo, K.S. Water Consumption and Its Variations in Koforidua. Master’s Thesis, Unpublished. 2013. [Google Scholar]

| Traditional Cash Pay Methods | New Electronic Payment Methods | |

|---|---|---|

| Type | 1 Options/Provider | |

| GWCL collection and pay points | Mobile money | MTN, Vodafone, Airtel-Tigo |

| Cash/cheque at Accredited banks | E-services | Mobile banking, Slydpay, ExpressPay, eTransact |

| Third party cash collectors and vendors | GWCL Customer Portal and App | |

| Variable | Category | Aware n = 152 | Unaware n = 98 | Total N (%) 250(/100%/) | p-Value |

|---|---|---|---|---|---|

| Age | 18–30yrs | 45.2 | 54.8 | 31 (12.4%) | 0.000 * |

| 31–40yrs | 63 | 37 | 46 (18.4%) | ||

| 41–50yrs | 74 | 26 | 73 (29.2%) | ||

| 51–60yrs | 72.3 | 27.7 | 47 (18.8%) | ||

| above 60yrs | 41.2 | 58.8 | 51 (20.4%) | ||

| No answer | 0 | 100 | 2 (0.8%) | ||

| Gender | Male | 61.5 | 38.5 | 122 (48.8%) | 0.831 |

| Female | 60.2 | 39.8 | 128 (51.2%) | ||

| Highest educational level | Basic | 50 | 50 | 22 (8.8%) | 0.527 |

| Secondary | 58.5 | 41.5 | 118 (47.2%) | ||

| Tertiary | 66 | 34 | 103 (41.2%) | ||

| No formal education | 66.7 | 33.3 | 3 (1.2%) | ||

| Other | 50 | 50 | 4 (1.6%) | ||

| Employment status | Not yet employed | 50 | 50 | 18 (7.2%) | 0.003 * |

| Employed (Public sector) | 62.5 | 37.5 | 48 (19.2%) | ||

| Employed (private sector) | 60 | 40 | 5 (2%) | ||

| Self employed | 69.2 | 30.8 | 130 (52%) | ||

| Retired | 35.6 | 64.4 | 45 (18%) | ||

| Other | 100 | 0 | 2 (1.6%) | ||

| Income level | <300 | 28.6 | 71.4 | 14 (5.6%) | 0.001 * |

| 300–700 | 53.8 | 46.2 | 26 (10.4%) | ||

| 701–1000 | 42.9 | 57.1 | 42 (16.8%) | ||

| 1001–1500 | 76.2 | 23.8 | 21 (8.4%) | ||

| 1501–2000 | 60.9 | 39.1 | 23 (9.2%) | ||

| Above 2000 | 83.7 | 16.3 | 43 (17.2%) | ||

| No answer | 61.7 | 39.2 | 81 (32.4%) | ||

| MM account | No | 52.1 | 47.9 | 48 (19.3%) | 0.177 |

| Yes | 62.9 | 37.2 | 201 (80.7%) | ||

| How do you receive your water bill | SMS | 50 | 50 | 4 (1.6%) | 0.000 * |

| Both Email and Paper bills | 50 | 50 | 4 (1.6%) | ||

| Paper bills | 37.3 | 62.7 | 59 (23.6%) | ||

| Both SMS and Paper bills | 68.9 | 31.1 | 183 (73.2%) | ||

| Average household size | 4.98 | ||||

| Sub-total level of awareness | 60.8 | 39.2 | 100 | ||

| Months 1 n = 10826 | Percent of Payments with Traditional Cash Methods (Collection/Pay Points and Banks/Vendors) | Percent of Total Payments with EWP |

|---|---|---|

| July 17 | 99.9 | 0.1 |

| August 17 | 99.8 | 0.2 |

| September 17 | 99.5 | 0.5 |

| October 17 | 99.2 | 0.8 |

| November 17 | 99.1 | 0.9 |

| December 17 | 98.7 | 1.3 |

| January 18 | 99.2 | 0.8 |

| February 18 | 98.7 | 1.3 |

| March18 | 98.4 | 1.6 |

| April 18 | 97.7 | 2.3 |

| May 18 | 98.1 | 1.9 |

| June 18 | 97.9 | 2.1 |

| Other indicators | ||

| Collection efficiency ratio | 99.1% | |

| Domestic Water tariff | USD 1.06 | |

| EWP uptake from 250 survey sample ** | 2.8% | |

| Phone ownership ** | 100% |

| n = 181 | Payment Method | |||

|---|---|---|---|---|

| Traditional | EWP | |||

| Monthly Average | Daily Average | Monthly Average | Daily Average | |

| Sep-17 | 18.69 | 0.62 | 18.86 | 0.63 |

| Oct-17 | 17.4 | 0.56 | 17.88 | 0.58 |

| Nov-17 | 18.22 | 0.61 | 20.65 | 0.69 |

| Dec-17 | 14.56 | 0.45 | 14.92 | 0.48 |

| Jan-18 | 18.01 | 0.58 | 16.57 | 0.53 |

| Feb-18 | 16.82 | 0.6 | 16.14 | 0.58 |

| Mar-18 | 15.81 | 0.51 | 14.6 | 0.47 |

| Apr-18 | 16.38 | 0.55 | 15.25 | 0.51 |

| May-18 | 18.18 | 0.59 | 18.43 | 0.6 |

| Jun-18 | 15.11 | 0.5 | 14.18 | 0.47 |

| Average | 16.92 | 0.56 | 16.75 | 0.55 |

| Per capita water use (l/c/d) | 112 | 110 | ||

© 2020 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

Amankwaa, G.; Asaaga, F.A.; Fischer, C.; Awotwe, P. Diffusion of Electronic Water Payment Innovations in Urban Ghana. Evidence from Tema Metropolis. Water 2020, 12, 1011. https://doi.org/10.3390/w12041011

Amankwaa G, Asaaga FA, Fischer C, Awotwe P. Diffusion of Electronic Water Payment Innovations in Urban Ghana. Evidence from Tema Metropolis. Water. 2020; 12(4):1011. https://doi.org/10.3390/w12041011

Chicago/Turabian StyleAmankwaa, Godfred, Festus A. Asaaga, Christian Fischer, and Patrick Awotwe. 2020. "Diffusion of Electronic Water Payment Innovations in Urban Ghana. Evidence from Tema Metropolis" Water 12, no. 4: 1011. https://doi.org/10.3390/w12041011

APA StyleAmankwaa, G., Asaaga, F. A., Fischer, C., & Awotwe, P. (2020). Diffusion of Electronic Water Payment Innovations in Urban Ghana. Evidence from Tema Metropolis. Water, 12(4), 1011. https://doi.org/10.3390/w12041011