Mapping Online Geographical Indication: Agri-Food Markets on E-Retail Shelves

Abstract

:1. Introduction

2. Agri-Food GI Market

3. Methodology

4. Results

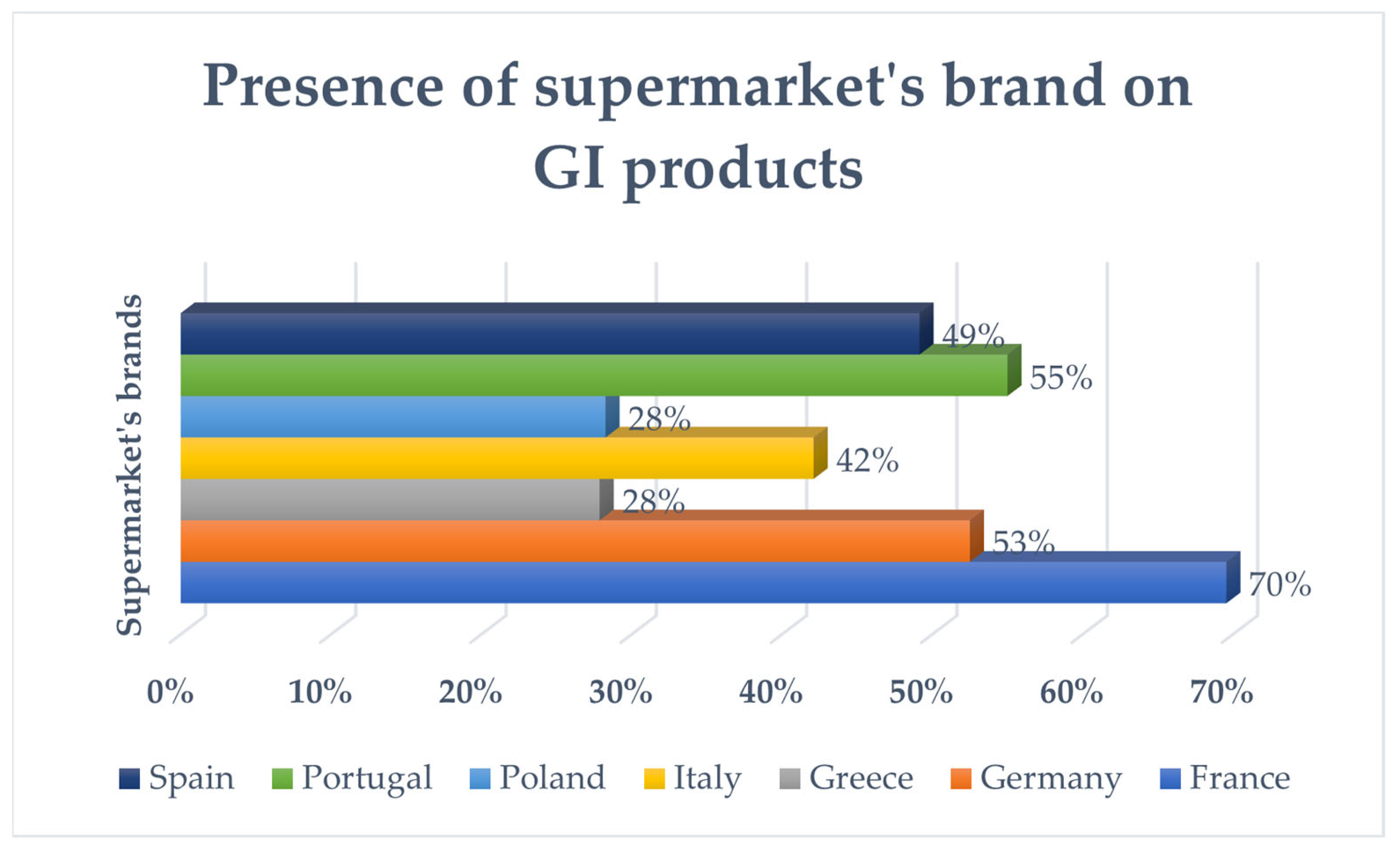

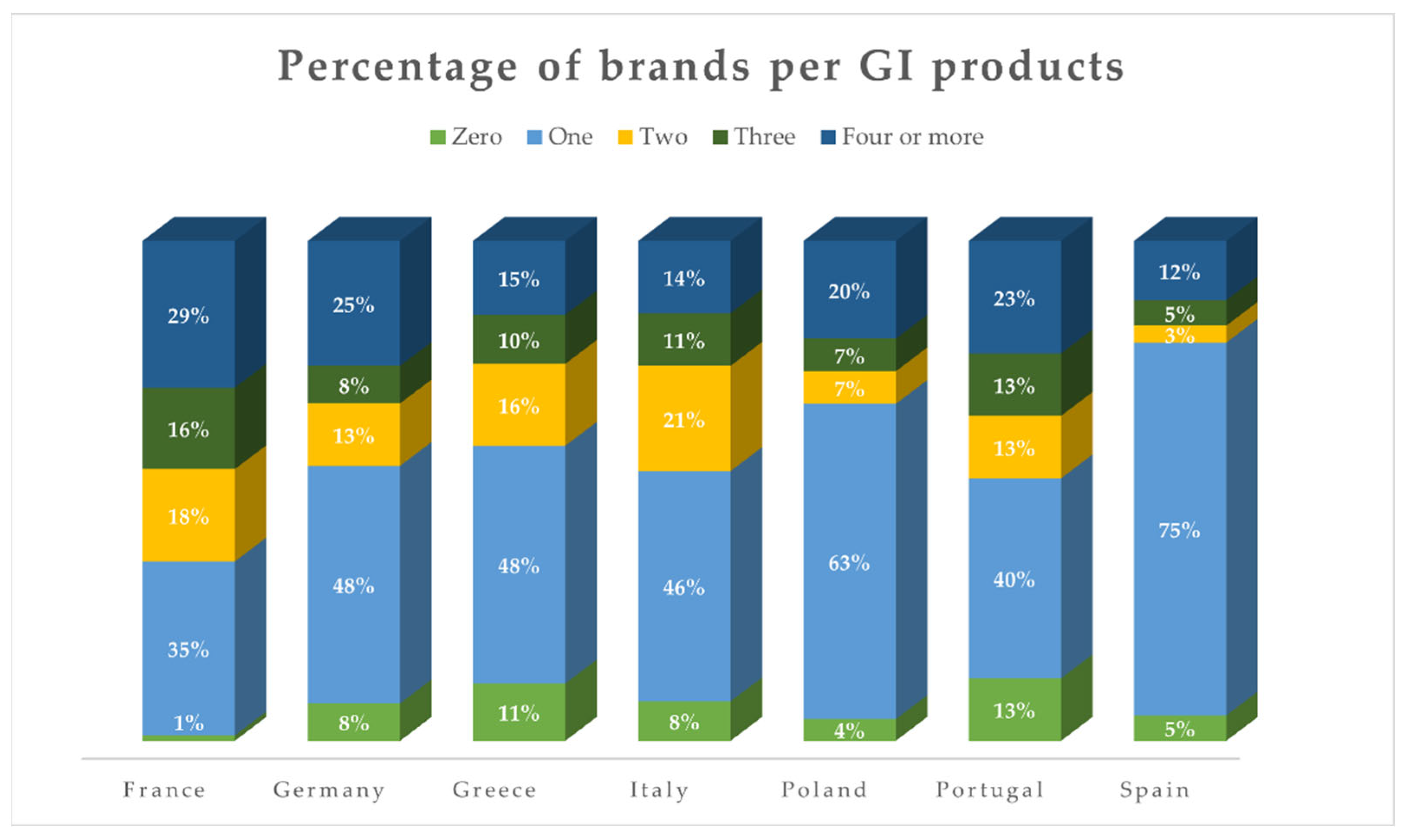

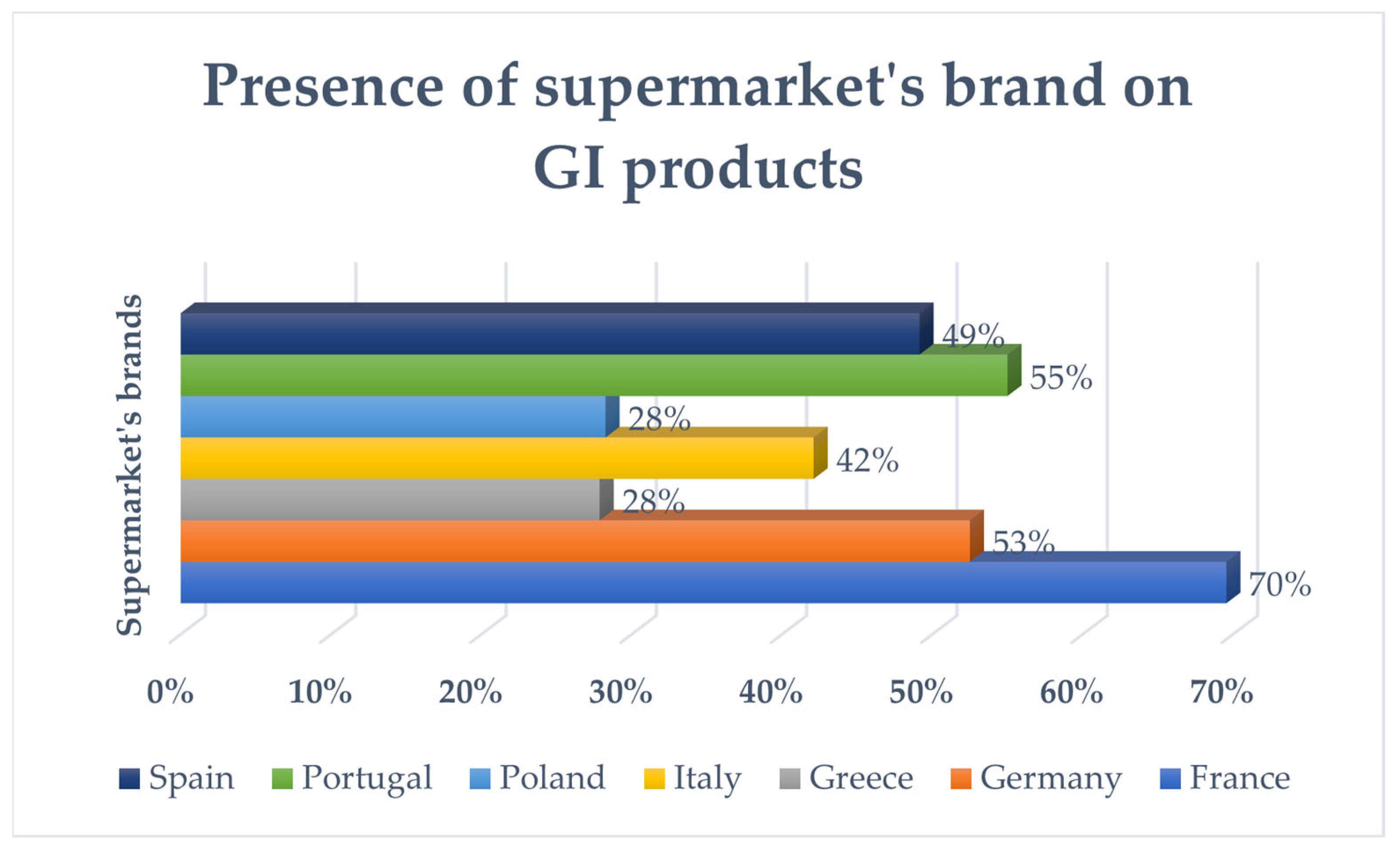

4.1. European Union

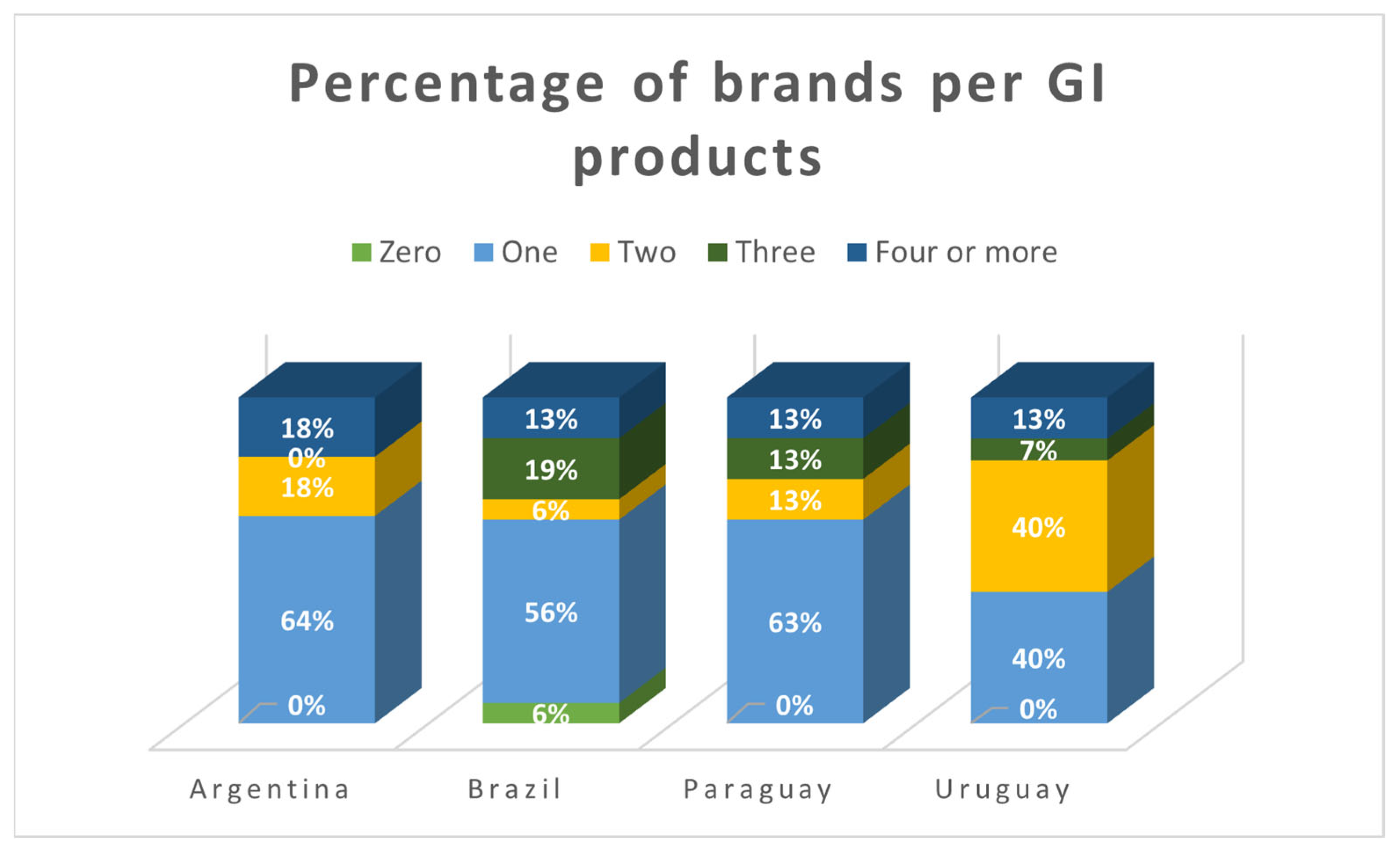

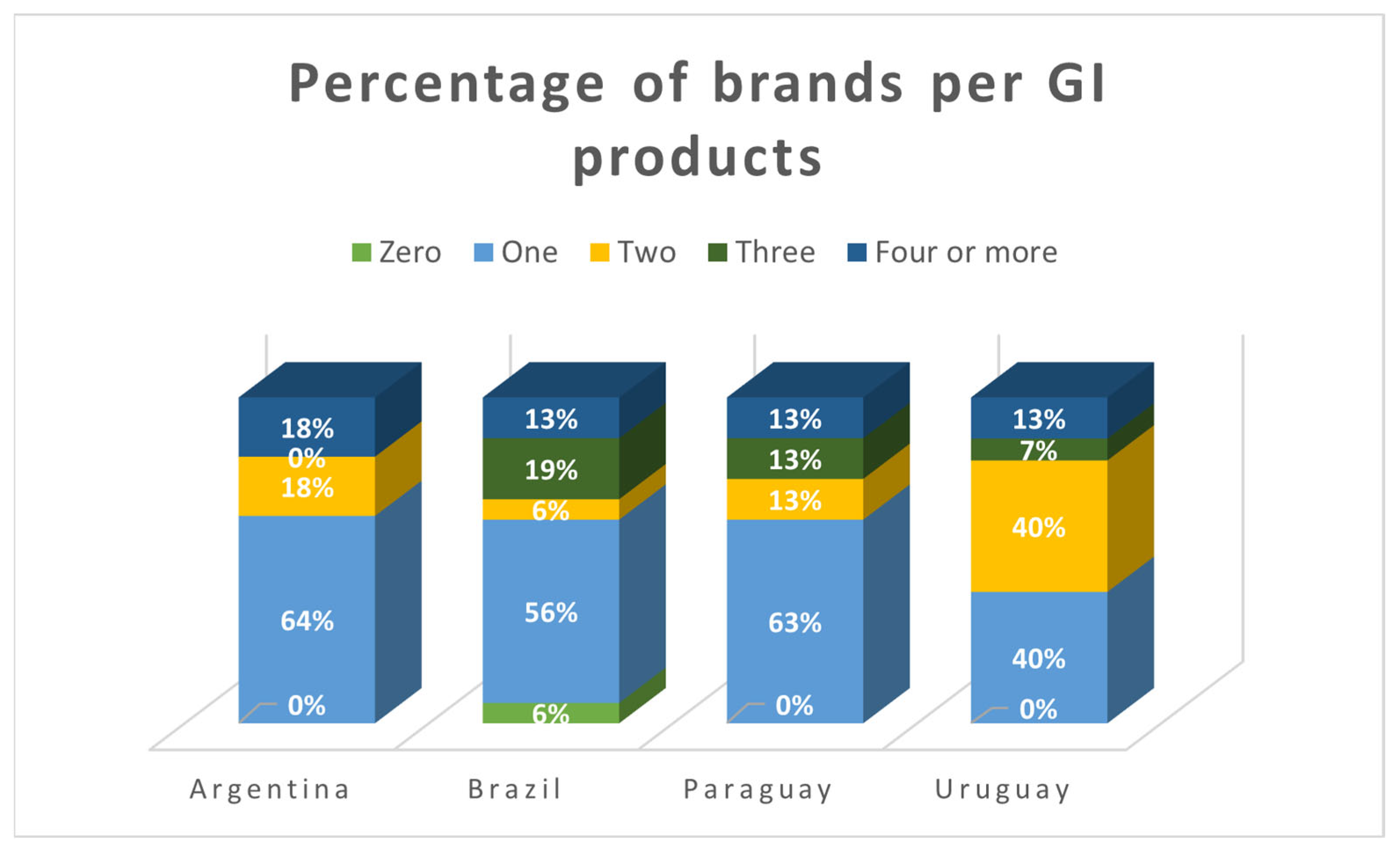

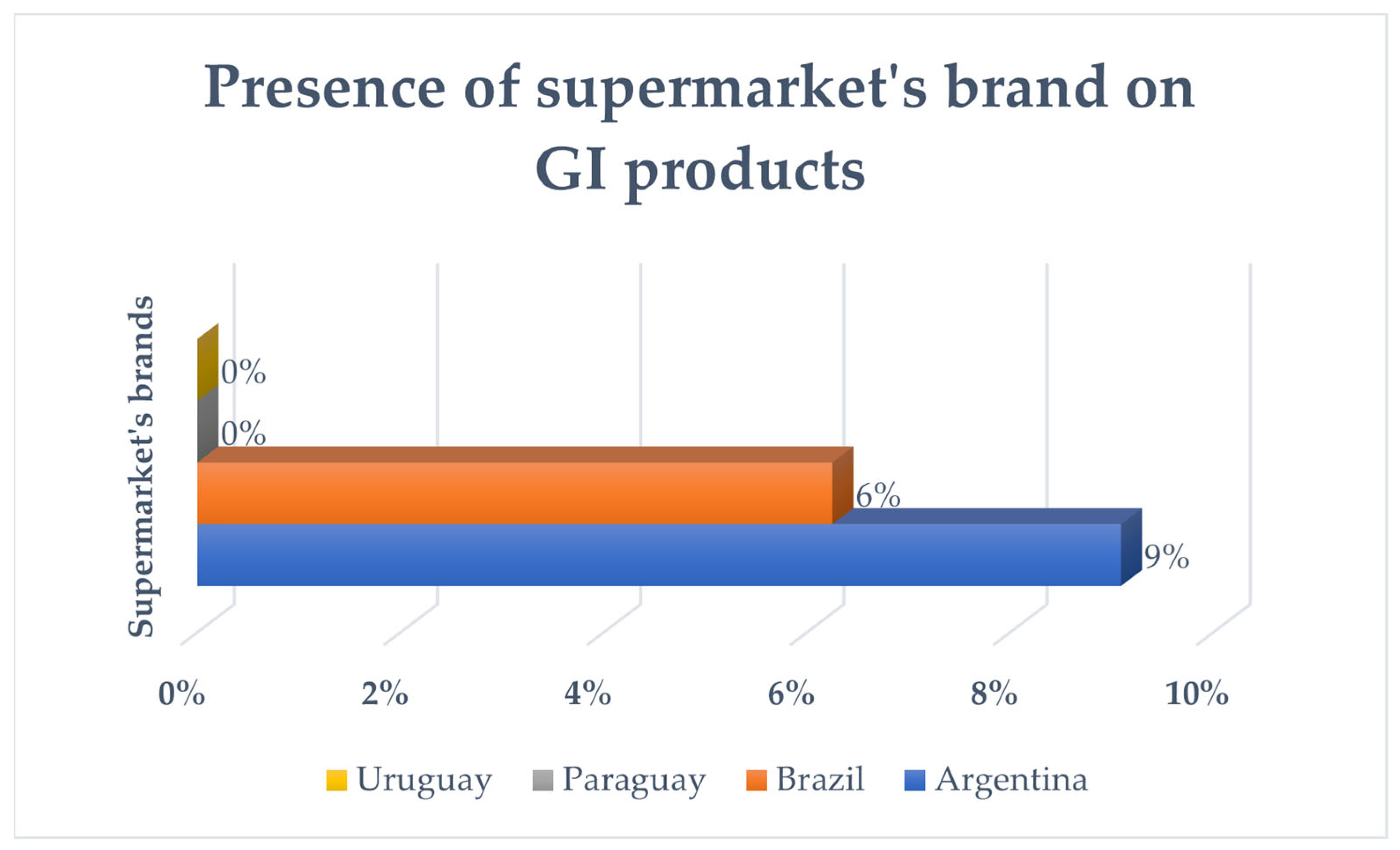

4.2. Mercosur

5. Discussion

6. Conclusions

Supplementary Materials

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Acknowledgments

Conflicts of Interest

References

- Say, J.-B. A Treatise on Political Economy; Routledge: Boca Raton, FL, USA, 2017; ISBN 978-1-351-31568-5. [Google Scholar]

- Fracarolli, G.S. Global Markets, Local Issues: The Hegemonic Process of Agri-Food Construction to Present Challenges. Land 2021, 10, 1182. [Google Scholar] [CrossRef]

- World Intellectual Property Organization Geographical Indications. Available online: https://www.wipo.int/geo_indications/en/index.html (accessed on 29 June 2021).

- Galtier, F.; Belletti, G.; Marescotti, A. Are Geographical Indications a Way to Decommodify the Coffee Market? In Proceedings of the European Association of Agricultural Economists, Ghent, Belgium, 26 August 2008; p. 15. [Google Scholar]

- Hinrichs, C.C. Embeddedness and Local Food Systems: Notes on Two Types of Direct Agricultural Market. J. Rural. Stud. 2000, 16, 295–303. [Google Scholar] [CrossRef]

- Barham, E. Translating terroir: The global challenge of French AOC labeling. J. Rural. Stud. 2003, 19, 127–138. [Google Scholar] [CrossRef]

- Allaire, G. Quality in economics: A cognitive perspective. In Qualities of Food; Manchester University Press: Manchester, UK, 2018; ISBN 0-7190-6854-1. [Google Scholar]

- Goodman, D. Rethinking Food Production-Consumption: Integrative Perspectives. Sociol. Rural. 2002, 42, 271–277. [Google Scholar] [CrossRef]

- Fracarolli, G.S. The Effects of Institutional Measures: Geographical Indication in Mercosur and the EU. Sustainability 2021, 13, 3476. [Google Scholar] [CrossRef]

- Fracarolli, G.S. Mapping Online Geographical Indication: Agrifood Products on E-Commerce Shelves of Mercosur and the European Union. Economies 2021, 9, 84. [Google Scholar] [CrossRef]

- Fligstein, N. Markets as Politics: A Political-Cultural Approach to Market Institutions. Am. Sociol. Rev. 1996, 61, 656. [Google Scholar] [CrossRef]

- Hodgson, G.M. Economics and Institutions: A Manifesto for a Modern Insitutional Economics; University of Pennsylvania Press: Philadelphia, PA, USA, 1988. [Google Scholar]

- North, D.C. Institutions. J. Econ. Perspect. 1991, 5, 97–112. [Google Scholar] [CrossRef]

- Acemoglu, D.; Johnson, S. Unbundling Institutions. J. Politi-Econ. 2005, 113, 949–995. [Google Scholar] [CrossRef] [Green Version]

- Allaire, G. Economics of Conventions and the New Economic Sociology and Our Understanding of Food Quality and New Food Markets and Trade Institutions: What are Markets that Pure Economics Does Not Know? In Proceedings of the Plenary Session 5 The New Landscape and the Need for an Extension to the Agricultural Economics Toolkit, Beijing, China, 16 August 2009. [Google Scholar]

- Allaire, G.; Wolf, S.A. Cognitive Representations and Institutional Hybridity in Agrofood Innovation. Sci. Technol. Hum. Values 2004, 29, 431–458. [Google Scholar] [CrossRef]

- Teuber, R. Consumers and producers expectations towards geographical indications. Br. Food J. 2011, 113, 900–918. [Google Scholar] [CrossRef] [Green Version]

- Agostino, M.; Trivieri, F. Geographical Indication and Wine Exports. An Empirical Investigation Considering the Major European Producers. Food Policy 2014, 46, 22–36. [Google Scholar] [CrossRef]

- Dentoni, D.; Menozzi, D.; Capelli, M.G. Group heterogeneity and cooperation on the geographical indication regulation: The case of the “Prosciutto di Parma” Consortium. Food Policy 2012, 37, 207–216. [Google Scholar] [CrossRef]

- de Mattos Fagundes, P.; Padilha, A.C.M.; Sluszz, T.; Padula, A.D. Geographical Indication as a Market Orientation Strategy: An Analysis of Producers of High-Quality Wines in Southern Brazil. J. Database Mark. Cust. Strategy Manag. 2012, 19, 163–178. [Google Scholar] [CrossRef] [Green Version]

- Ilbery, B.; Kneafsey, M.; Söderlund, A.; Dimara, E. Quality, imagery and marketing: Producer perspectives on quality products and services in the lagging rural regions of the european union. Geogr. Ann. Ser. B Hum. Geogr. 2001, 83, 27–40. [Google Scholar] [CrossRef]

- Roselli, L.; Giannoccaro, G.; Carlucci, D.; De Gennaro, B. EU Quality Labels in the Italian Olive Oil Market: How Much Overlap Is There between Geographical Indication and Organic Production? J. Food Prod. Mark. 2018, 24, 784–801. [Google Scholar] [CrossRef]

- Barjolle, D.; Paus, M.; Perret, A.O. Impacts of Geographical Indications-Review of Methods and Empirical Evidences. In Proceedings of the International Association of Agricultural Economists Conference, Beijing, China, 16–22 August 2009. [Google Scholar]

- Aprile, M.C.; Caputo, V.; Nayga Jr, R.M. Consumers’ Valuation of Food Quality Labels: The Case of the European Geographic Indication and Organic Farming Labels. Int. J. Consum. Stud. 2012, 36, 158–165. [Google Scholar] [CrossRef]

- Bonnet, C.; Simioni, M. Assessing Consumer Response to Protected Designation of Origin Labelling: A Mixed Multinomial Logit Approach. Eur. Rev. Agric. Econ. 2001, 28, 433–449. [Google Scholar] [CrossRef]

- Loureiro, M.L.; McCluskey, J.J. Assessing Consumer Response to Protected Geographical Identification Labeling. Agribus. Int. J. 2000, 16, 309–320. [Google Scholar] [CrossRef]

- Menapace, L.; Colson, G.; Grebitus, C.; Facendola, M. Consumers’ preferences for geographical origin labels: Evidence from the Canadian olive oil market. Eur. Rev. Agric. Econ. 2011, 38, 193–212. [Google Scholar] [CrossRef]

- Fligstein, N. Social Skill and the Theory of Fields. Sociol. Theory 2001, 19, 105–125. [Google Scholar] [CrossRef] [Green Version]

- Fligstein, N. The Architecture of Markets: An Economic Sociology of Twenty-First-Century Capitalist Societies; Princeton University Press: Princeton, NJ, USA, 2002; ISBN 0-691-10254-6. [Google Scholar]

- Fligstein, N. The Transformation of Corporate Control; Harvard University Press: Cambridge, MA, USA, 1993; ISBN 0-674-90359-5. [Google Scholar]

- Fligstein, N. Euroclash: The EU, European Identity, and the Future of Europe; Oxford University Press: Oxford, UK, 2008; ISBN 0-19-954256-2. [Google Scholar]

- Fligstein, N.; Dauter, L. The Sociology of Markets. Annu. Rev. Sociol. 2007, 33, 105–128. [Google Scholar] [CrossRef] [Green Version]

- Allaire, G. Applying Economic Sociology to Understand the Meaning of “Quality” in Food Markets. Agric. Econ. 2010, 41, 167–180. [Google Scholar] [CrossRef]

- Dervillé, M.; Allaire, G. Change of competition regime and regional innovative capacities: Evidence from dairy restructuring in France. Food Policy 2014, 49, 347–360. [Google Scholar] [CrossRef]

- Acemoğlu, D.; Robinson, J.A. Paths to inclusive political institutions. In Economic History of Warfare and State Formation. Studies in Economic History; Eloranta, J., Golson, E., Markevich, A., Wolf, N., Eds.; Springer: Singapore, 2016; pp. 3–50. ISBN 978-981-10-1605-9. [Google Scholar]

- Acemoglu, D.; Johnson, S.; Robinson, J.A. The Colonial Origins of Comparative Development: An Empirical Investigation. Am. Econ. Rev. 2001, 91, 1369–1401. [Google Scholar] [CrossRef]

- Acemoglu, D.; Johnson, S.; Robinson, J. The Rise of Europe: Atlantic Trade, Institutional Change, and Economic Growth. Am. Econ. Rev. 2005, 95, 546–579. [Google Scholar] [CrossRef] [Green Version]

- Fligstein, N. Social Skill and Institutional Theory. Am. Behav. Sci. 1997, 40, 397–405. [Google Scholar] [CrossRef]

- Powell, W.W.; DiMaggio, P.J. The New Institutionalism in Organizational Analysis; University of Chicago Press: Chicago, IL, USA, 2012; ISBN 978-0-226-18594-1. [Google Scholar]

- Kenney, M.; Lobao, L.M.; Curry, J.; Goe, W.R. Midwestern Agriculture in US Fordism: From the New Deal to Economic Restructuring. Sociol. Rural. 1989, 29, 131–148. [Google Scholar] [CrossRef]

- Bonanno, A.; Constance, D.H. Globalization, Fordism, and Post-Fordism in Agriculture and Food: A Critical Review of the Literature. Cult. Agric. 2001, 23, 1–18. [Google Scholar] [CrossRef]

- Campbell, I. The Australian Trade Union Movement and Post-Fordism-Revised Paper Presented to the Political Economy Conference. J. Aust. Political Econ. 1990, 26, 1–26. [Google Scholar]

- Gahan, P. Mathews and the New Production Concepts Debate-Reply to Mathews, John. New Production Systems: A Response to Critics and a Re Evaluation. J. Aust. Political Econ. 1993, 31, 74–88. [Google Scholar]

- Wilson, B.; Ewer, P. ‘New’ Production Concepts: Implications for Union Strategy. Labour Ind. A J. Soc. Econ. Relat. Work 1996, 7, 123–143. [Google Scholar] [CrossRef]

- Fernández-Zarza, M.; Amaya-Corchuelo, S.; Belletti, G.; Aguilar-Criado, E. Trust and Food Quality in the Valorisation of Geographical Indication Initiatives. Sustainability 2021, 13, 3168. [Google Scholar] [CrossRef]

- Barham, E.; Sylvander, B. Labels of Origin for Food: Local Development, Global Recognition; CABI: Wallingford, UK, 2011; ISBN 978-1-84593-352-4. [Google Scholar]

- Deselnicu, O.C.; Costanigro, M.; Souza-Monteiro, D.M.; McFadden, D.T. A Meta-Analysis of Geographical Indication Food Valuation Studies: What Drives the Premium for Origin-Based Labels? J. Agric. Resour. Econ. 2013, 38, 204–219. [Google Scholar]

- Cei, L.; Defrancesco, E.; Stefani, G. From Geographical Indications to Rural Development: A Review of the Economic Effects of European Union Policy. Sustainability 2018, 10, 3745. [Google Scholar] [CrossRef] [Green Version]

- Teuber, R. Geographical Indications of Origin as a Tool of Product Differentiation: The Case of Coffee. J. Int. Food Agribus. Mark. 2010, 22, 277–298. [Google Scholar] [CrossRef] [Green Version]

- Dias, C.; Mendes, L. Protected Designation of Origin (PDO), Protected Geographical Indication (PGI) and Traditional Speciality Guaranteed (TSG): A bibiliometric analysis. Food Res. Int. 2018, 103, 492–508. [Google Scholar] [CrossRef]

- Renard, M.-C. The Interstices of Globalization: The Example of Fair Coffee. Sociol. Rural. 1999, 39, 484–500. [Google Scholar] [CrossRef]

- Addor, F.; Grazioli, A. Geographical Indications beyond Wines and Spirits: A Roadmap for a Better Protection for Geographical Indications in the WTO/TRIPS Agreement. J. World Intell. Prop. 2002, 5, 865. [Google Scholar] [CrossRef]

- Jorge-Vázquez, J.; Chivite-Cebolla, M.P.; Salinas-Ramos, F. The Digitalization of the European Agri-Food Cooperative Sector. Determining Factors to Embrace Information and Communication Technologies. Agriculture 2021, 11, 514. [Google Scholar] [CrossRef]

- Cristobal-Fransi, E.; Montegut-Salla, Y.; Ferrer-Rosell, B.; Daries, N. Rural cooperatives in the digital age: An analysis of the Internet presence and degree of maturity of agri-food cooperatives’ e-commerce. J. Rural. Stud. 2019, 74, 55–66. [Google Scholar] [CrossRef]

- Lin, C. An empirical study on decision factors affecting fresh e-commerce purchasing geographical indications agricultural products. Acta Agric. Scand. Sect. B-Plant Soil Sci. 2020, 71, 541–551. [Google Scholar] [CrossRef]

- Carlucci, D.; De Gennaro, B.; Roselli, L.; Seccia, A. E-commerce retail of extra virgin olive oil: An hedonic analysis of Italian SMEs supply. Br. Food J. 2014, 116, 1600–1617. [Google Scholar] [CrossRef]

- Chilla, T.; Fink, B.; Balling, R.; Reitmeier, S.; Schober, K. The EU Food Label ‘Protected Geographical Indication’: Economic Implications and Their Spatial Dimension. Sustainability 2020, 12, 5503. [Google Scholar] [CrossRef]

- Smith, A. The Wealth of Nations; Modern Library: New York, NY, USA, 1994; ISBN 978-0679424734. [Google Scholar]

- Polanyi, K. The Great Transformation: The Political and Economic Origins of Our Time, 2nd ed.; Beacon Press: Boston, MA, USA, 2001. [Google Scholar]

- Granovetter, M. Economic Action and Social Structure: The Problem of Embeddedness. Am. J. Sociol. 1985, 91, 481–510. [Google Scholar] [CrossRef]

- Trigilia, C. Economic Sociology: State, Market, and Society in Modern Capitalism; John Wiley & Sons: Hoboken, NJ, USA, 2008; ISBN 978-0-470-69285-1. [Google Scholar]

- Fourcade, M. Theories of Markets and Theories of Society. Am. Behav. Sci. 2007, 50, 1015–1034. [Google Scholar] [CrossRef] [Green Version]

- Burt, R.S. Structural Holes; Harvard University Press: Cambridge, MA, USA, 2021. [Google Scholar]

- Granovetter, M. The Impact of Social Structure on Economic Outcomes. J. Econ. Perspect. 2005, 19, 33–50. [Google Scholar] [CrossRef]

- White, H.C. Where Do Markets Come From? Am. J. Sociol. 1981, 87, 517–547. [Google Scholar] [CrossRef]

- White, H.C. Markets from Networks: Socioeconomic Models of Production; Princeton University Press: Princeton, NJ, USA, 2018; ISBN 978-0-691-18762-4. [Google Scholar]

- Beunza, D.; Stark, D. Tools of the Trade: The Socio-Technology of Arbitrage in a Wall Street Trading Room. Ind. Corp. Chang. 2004, 13, 369–400. [Google Scholar] [CrossRef]

- Callon, M. Introduction: The Embeddedness of Economic Markets in Economics. Sociol. Rev. 1998, 46, 1–57. [Google Scholar] [CrossRef]

- Callon, M. What does it mean to say that economics is performative? In Do Economists Make Markets? MacKenzie, D., Muniesa, F., Siu, L., Eds.; Princeton University Press: Princeton, NJ, USA, 2020. [Google Scholar]

- MacKenzie, D.; Millo, Y. Constructing a Market, Performing Theory: The Historical Sociology of a Financial Derivatives Exchange. Am. J. Sociol. 2003, 109, 107–145. [Google Scholar] [CrossRef] [Green Version]

- MacKenzie, D. An Engine, Not a Camera: How Financial Models Shape Markets; MIT Press: Cambridge, MA, USA, 2008; ISBN 978-0-262-25004-7. [Google Scholar]

- Dobbin, F. Forging Industrial Policy: The United States, Britain, and France in the Railway Age; Cambridge University Press: Cambridge, UK, 1994; ISBN 978-0-521-62990-4. [Google Scholar]

- North, D.C. Transaction Costs, Institutions, and Economic Performance; Occasional Papers International Center for Economic Growth; ICS Press: San Francisco, CA, USA, 1992; ISBN 978-1-55815-211-3. [Google Scholar]

- Block, F.L. Capitalism: The Future of an Illusion; University of California Press: Los Angeles, CA, USA, 2018; ISBN 978-0-520-95907-1. [Google Scholar]

- Crouch, C.; Gales, P.L.; Trigilia, C.; Voelzkow, H. Local Production Systems in Europe: Rise or Demise? Oxford University Press: Oxford, UK, 2001. [Google Scholar]

- Trigilia, C. Social Capital and Local Development. Eur. J. Soc. Theory 2001, 4, 427–442. [Google Scholar] [CrossRef]

- Bourdieu, P. Distinction: A Social Critique of the Judgement of Taste; Harvard University Press: Cambridge, MA, USA, 1987; ISBN 978-0-674-26227-0. [Google Scholar]

- Bourdieu, P. Outline of a Theory of Practice; Reprint Edition; Cambridge University Press: Cambridge, MA, USA, 1977; ISBN 978-0-521-29164-4. [Google Scholar]

- Bourdieu, P. Pascalian Meditations; Stanford University Press: Stanford, CA, USA, 2000; ISBN 978-0-8047-3332-8. [Google Scholar]

- Fligstein, N. The Theory of Fields and Its Application to Corporate Governance. Seattle UL Rev. 2015, 39, 237. [Google Scholar]

- Fligstein, N.; McAdam, D. The Field of Theory. Contemp. Sociol. 2014, 43, 315–318. [Google Scholar] [CrossRef]

- Fligstein, N.; McAdam, D. A Theory of Fields; Oxford University Press: Oxford, UK, 2012; ISBN 0-19-985995-7. [Google Scholar]

- Fligstein, N.; Calder, R. Architecture of Markets. In Emerging Trends in the Social and Behavioral Sciences; John Wiley & Sons: Hoboken, NJ, USA, 2015; pp. 1–14. ISBN 978-1-118-90077-2. [Google Scholar]

- European Commission EAmbrosia. Available online: https://ec.europa.eu/info/food-farming-fisheries/food-safety-and-quality/certification/quality-labels/geographical-indications-register/ (accessed on 26 November 2020).

- INPI Pedidos de Indicação Geográfica no Brasil. Available online: https://www.gov.br/inpi/pt-br/servicos/indicacoes-geograficas/pedidos-de-indicacao-geografica-no-brasil (accessed on 26 November 2020).

- Prosur Proyecta Secreto Industrial. Available online: https://www.prosurproyecta.org/uruguay/categoria-explorador/secreto-industrial/ (accessed on 26 November 2020).

- Ministerio de Agricultura, Ganadería y Pesca Dirección Nacional de Alimentos y Bebidas–Indicación Geográfica y Denominación de Origen. Available online: http://www.alimentosargentinos.gob.ar/HomeAlimentos/IGeo/productos_reconocidos.php (accessed on 9 September 2020).

- Roselli, L.; Carlucci, D.; De Gennaro, B.C. What Is the Value of Extrinsic Olive Oil Cues in Emerging Markets? Empirical Evidence from the U.S. E-Commerce Retail Market. Agribusiness 2016, 32, 329–342. [Google Scholar] [CrossRef]

- Marlowe, B.; Lee, S. Conceptualizing Terroir Wine Tourism. Tour. Rev. Int. 2018, 22, 143–151. [Google Scholar] [CrossRef]

- Skuras, D.; Vakrou, A. Consumers’ Willingness to Pay for Origin Labelled Wine: A Greek Case Study. Br. Food J. 2002, 104, 898–912. [Google Scholar] [CrossRef]

- Barjolle, D.; Quiñones-Ruiz, X.F.; Bagal, M.; Comoé, H. The Role of the State for Geographical Indications of Coffee: Case Studies from Colombia and Kenya. World Dev. 2017, 98, 105–119. [Google Scholar] [CrossRef]

- Quiñones-Ruiz, X.F.; Penker, M.; Belletti, G.; Marescotti, A.; Scaramuzzi, S. Why Early Collective Action Pays off: Evidence from Setting Protected Geographical Indications. Renew. Agric. Food Syst. 2017, 32, 179–192. [Google Scholar] [CrossRef] [Green Version]

- Boatto, V.; Defrancesco, E.; Trestini, S. The Price Premium for Wine Quality Signals: Does Retailers’ Information Provision Matter? Br. Food J. 2011, 113, 669–679. [Google Scholar] [CrossRef]

- Yue, C.; Marette, S.; Beghin, J.C. 3 How to Promote Quality Perception: Brand Advertising or Geographical Indication? Frontiers of Economics and Globalization. In Nontariff Measures with Market Imperfections: Trade and Welfare Implications; Emerald Group Publishing: Bingley, UK, 2013; Volume 12, pp. 73–98. ISBN 9781781907542. [Google Scholar]

- Josling, T. The War on Terroir: Geographical Indications as a Transatlantic Trade Conflict. J. Agric. Econ. 2006, 57, 337–363. [Google Scholar] [CrossRef]

- Swinnen, J.F. Economics and Politics of Food Standards, Trade, and Development. Agric. Econ. 2016, 47, 7–19. [Google Scholar] [CrossRef] [Green Version]

- Huysmans, M.; Swinnen, J. No Terroir in the Cold? A Note on the Geography of Geographical Indications. J. Agric. Econ. 2019, 70, 550–559. [Google Scholar] [CrossRef]

- Meloni, G.; Swinnen, J. Trade and Terroir. The Political Economy of the World’s First Geographical Indications. Food Policy 2018, 81, 1–20. [Google Scholar] [CrossRef] [Green Version]

- Gade, D.W. Tradition, Territory, and Terroir in French Viniculture: Cassis, France, and Appellation Contrôlée. Ann. Assoc. Am. Geogr. 2004, 94, 848–867. [Google Scholar] [CrossRef]

- Giddens, A. The Constitution of Society: Outline of the Theory of Structuration; University of California Press: Berkeley, CA, USA, 1984; ISBN 978-0-520-05292-5. [Google Scholar]

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Category | Description |

|---|---|

| 1.1 | Fresh meat |

| 1.2 | Meat products |

| 1.3 | Cheeses |

| 1.4 | Other products of animal origin |

| 1.5 | Oils and fats |

| 1.6 | Fruits, vegetables and cereals fresh or processed |

| 1.7 | Fresh fish, mollusks and crustaceans and derived |

| 1.8 | Others such as spices |

| 2.1 | Beers |

| 2.2 | Chocolate and derived |

| 2.3 | Bread, pastry, cakes and alike |

| 2.4 | Beverages from plant extracts |

| 2.5 | Pasta |

| 2.6 | Salt |

| 2.7 | Natural gums and resins |

| 2.8 | Mustard paste |

| 2.9 | Hay |

| 2.10 | Essential oils |

| 2.11 | Cork |

| 2.12 | Cochineal |

| 2.13 | Flowers and ornamental plants |

| 2.14 | Cotton |

| 2.15 | Wool |

| 2.16 | Wicker |

| 2.17 | Scutched flax |

| 2.18 | Leather |

| 2.19 | Fur |

| 2.20 | Feather |

| Type | Description |

|---|---|

| PDO | Protected Designation of Origin |

| PGI | Protected Geographical Indication |

| TSG | Traditional Specialities Guaranteed |

| DO | Denominação de Origem (Designation of Origin) |

| IP | Indicação de Procedência (Indication of Source) |

| IG | Indicación Geográfica (Geographical Indication) |

| Economic Bloc | GIs Found | Existing GIs | Percentage |

|---|---|---|---|

| European Union | 286 | 1414 | 20.23% |

| Mercosur | 6 | 53 | 11.32% |

| Country | GI Category | Products Per Category | Total Products | Brands Per Category | Total Brands | Ratio Per Category | Total Ratio |

|---|---|---|---|---|---|---|---|

| France | 1.1 | 6 | 462 | 3 | 83 | 2 | 5.57 |

| 1.2 | 35 | 15 | 2.33 | ||||

| 1.3 | 267 | 48 | 5.56 | ||||

| 1.4 | 13 | 5 | 2.6 | ||||

| 1.5 | 19 | 10 | 1.9 | ||||

| 1.6 | 77 | 10 | 7.7 | ||||

| 1.8 | 36 | 14 | 2.57 | ||||

| 2.5 | 4 | 2 | 2 | ||||

| 2.6 | 5 | 3 | 1.67 | ||||

| Germany | 1.2 | 46 | 174 | 12 | 43 | 3.83 | 4.05 |

| 1.3 | 103 | 24 | 4.29 | ||||

| 1.4 | 3 | 1 | 3 | ||||

| 1.5 | 5 | 3 | 1.67 | ||||

| 1.6 | 7 | 5 | 1.4 | ||||

| 1.8 | 4 | 3 | 1.33 | ||||

| 2.3 | 4 | 3 | 1.33 | ||||

| 2.5 | 2 | 1 | 2 | ||||

| Greece | 1.2 | 3 | 283 | 2 | 87 | 1.5 | 3.25 |

| 1.3 | 235 | 67 | 3.51 | ||||

| 1.5 | 11 | 6 | 1.83 | ||||

| 1.6 | 26 | 14 | 1.86 | ||||

| 1.8 | 2 | 0 | N/A 1 | ||||

| 2.3 | 4 | 3 | 1.33 | ||||

| 2.7 | 2 | 0 | N/A 1 | ||||

| Italy | 1.1 | 1 | 330 | 0 | 65 | N/A 1 | 5.08 |

| 1.2 | 67 | 22 | 3.05 | ||||

| 1.3 | 130 | 18 | 7.22 | ||||

| 1.4 | 1 | 0 | N/A 1 | ||||

| 1.5 | 8 | 6 | 1.33 | ||||

| 1.6 | 31 | 11 | 2.82 | ||||

| 1.8 | 17 | 9 | 1.89 | ||||

| 2.1 | 2 | 1 | 2 | ||||

| 2.3 | 15 | 8 | 1.88 | ||||

| 2.5 | 58 | 3 | 19.33 | ||||

| Poland | 1.2 | 21 | 208 | 10 | 61 | 2.1 | 3.41 |

| 1.3 | 145 | 39 | 3.72 | ||||

| 1.5 | 10 | 5 | 2 | ||||

| 1.6 | 1 | 1 | 1 | ||||

| 1.7 | 11 | 1 | 11 | ||||

| 1.8 | 20 | 8 | 2.5 | ||||

| Portugal | 1.1 | 5 | 199 | 2 | 56 | 2.5 | 3.55 |

| 1.2 | 27 | 14 | 1.93 | ||||

| 1.3 | 94 | 29 | 3.24 | ||||

| 1.4 | 2 | 2 | 1 | ||||

| 1.5 | 38 | 12 | 3.17 | ||||

| 1.6 | 23 | 3 | 7.67 | ||||

| 1.8 | 10 | 4 | 2.5 | ||||

| Spain | 1.1 | 51 | 128 | 6 | 32 | 8.5 | 4 |

| 1.2 | 16 | 10 | 1.6 | ||||

| 1.3 | 31 | 16 | 1.94 | ||||

| 1.5 | 1 | 1 | 1 | ||||

| 1.6 | 18 | 8 | 2.25 | ||||

| 1.8 | 7 | 3 | 2.33 | ||||

| 2.3 | 4 | 2 | 2 |

| Country | GI Category | Products per Category | Total Products | Brands per Category | Total Brands | Ratio per Category | Total Ratio |

|---|---|---|---|---|---|---|---|

| Argentina | 1.2 | 22 | 180 | 5 | 37 | 4.4 | 4.86 |

| 1.3 | 10 | 7 | 1.43 | ||||

| 1.8 | 148 | 25 | 5.92 | ||||

| Brazil | 1.2 | 16 | 60 | 7 | 23 | 2.29 | 2.61 |

| 1.3 | 16 | 7 | 2.29 | ||||

| 1.5 | 5 | 2 | 2.5 | ||||

| 1.6 | 2 | 0 | N/A 1 | ||||

| 1.8 | 21 | 7 | 3.0 | ||||

| Paraguay | 1.2 | 7 | 43 | 2 | 13 | 3.5 | 3.31 |

| 1.3 | 13 | 6 | 2.17 | ||||

| 1.8 | 23 | 5 | 4.6 | ||||

| Uruguay | 1.2 | 38 | 105 | 10 | 29 | 3.8 | 3.62 |

| 1.3 | 43 | 12 | 3.58 | ||||

| 1.8 | 24 | 7 | 3.43 |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2021 by the author. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Fracarolli, G.S. Mapping Online Geographical Indication: Agri-Food Markets on E-Retail Shelves. Agronomy 2021, 11, 2385. https://doi.org/10.3390/agronomy11122385

Fracarolli GS. Mapping Online Geographical Indication: Agri-Food Markets on E-Retail Shelves. Agronomy. 2021; 11(12):2385. https://doi.org/10.3390/agronomy11122385

Chicago/Turabian StyleFracarolli, Guilherme Silva. 2021. "Mapping Online Geographical Indication: Agri-Food Markets on E-Retail Shelves" Agronomy 11, no. 12: 2385. https://doi.org/10.3390/agronomy11122385

APA StyleFracarolli, G. S. (2021). Mapping Online Geographical Indication: Agri-Food Markets on E-Retail Shelves. Agronomy, 11(12), 2385. https://doi.org/10.3390/agronomy11122385