The Effect of Carbon Tax in Aviation Industry on the Multilateral Simulation Game

Abstract

:1. Introduction

2. A Framework of Analytic Functions

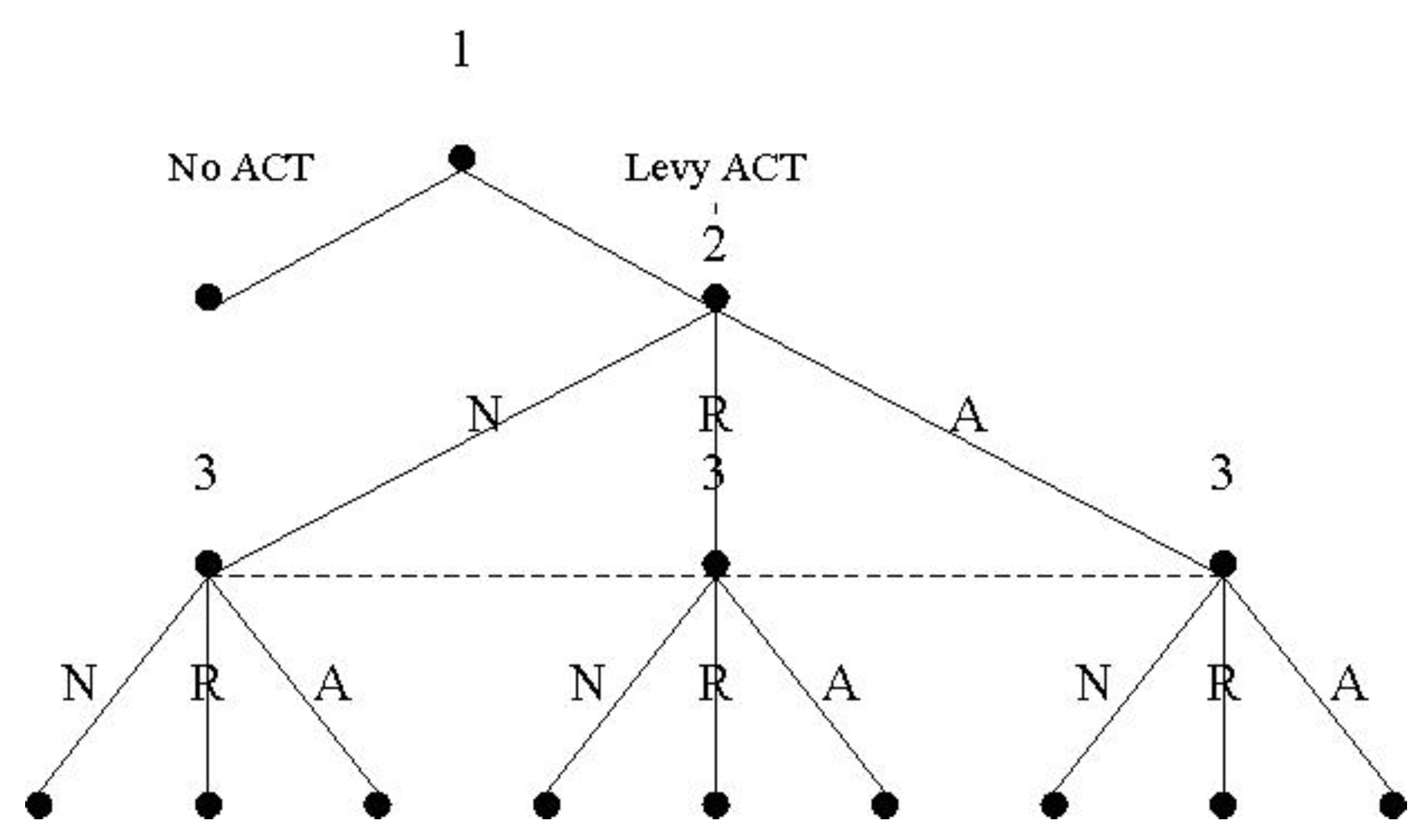

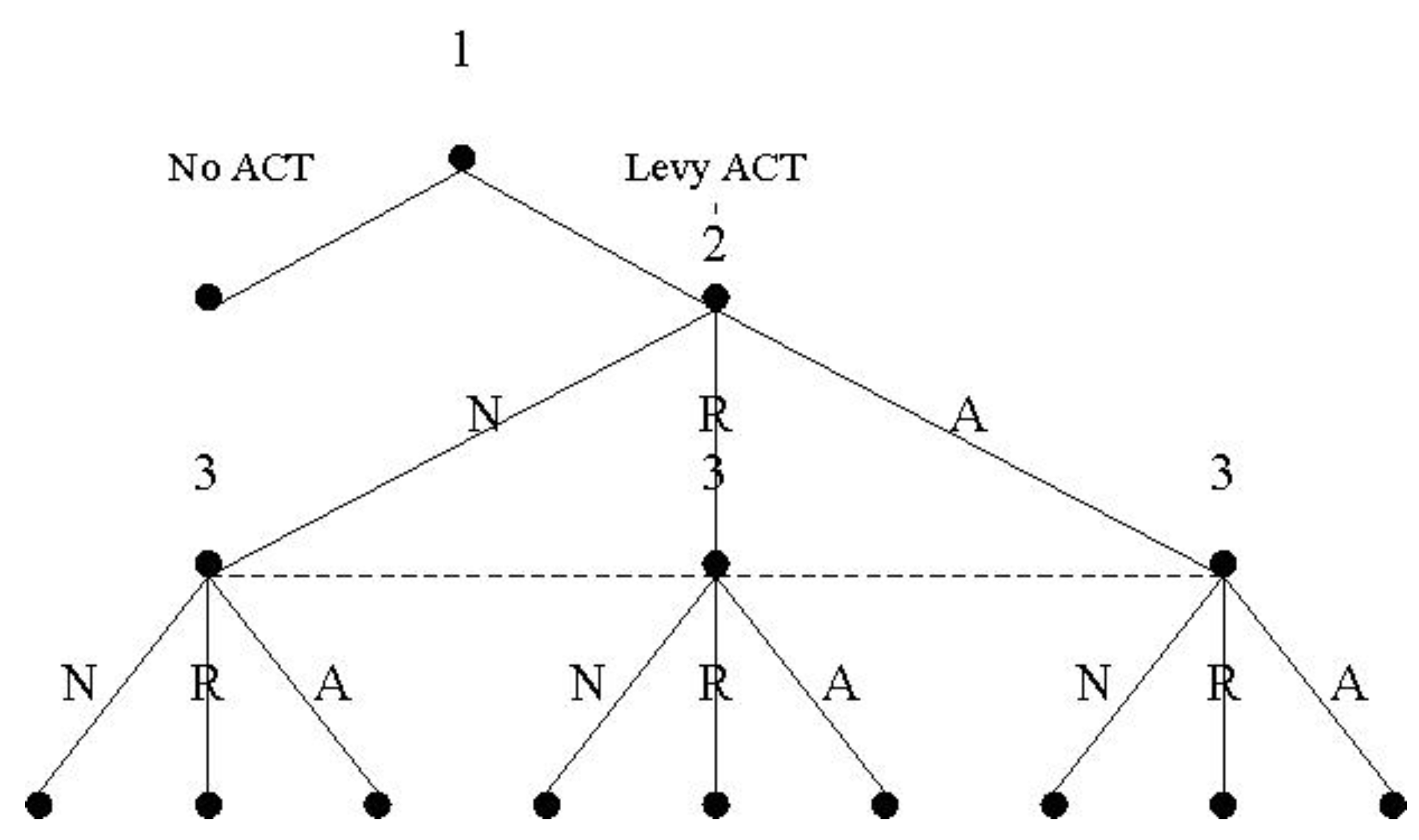

2.1. Players and Strategies

2.2. Symbols and Assumptions

2.3. Analyses and Scenarios

3. Two-Stage Game Models and Nash Equilibriums

3.1. Model 1: (R, R)

3.2. Model 2: (R, A)

3.3. Model 3: (A, R)

3.4. Model 4: (A, A)

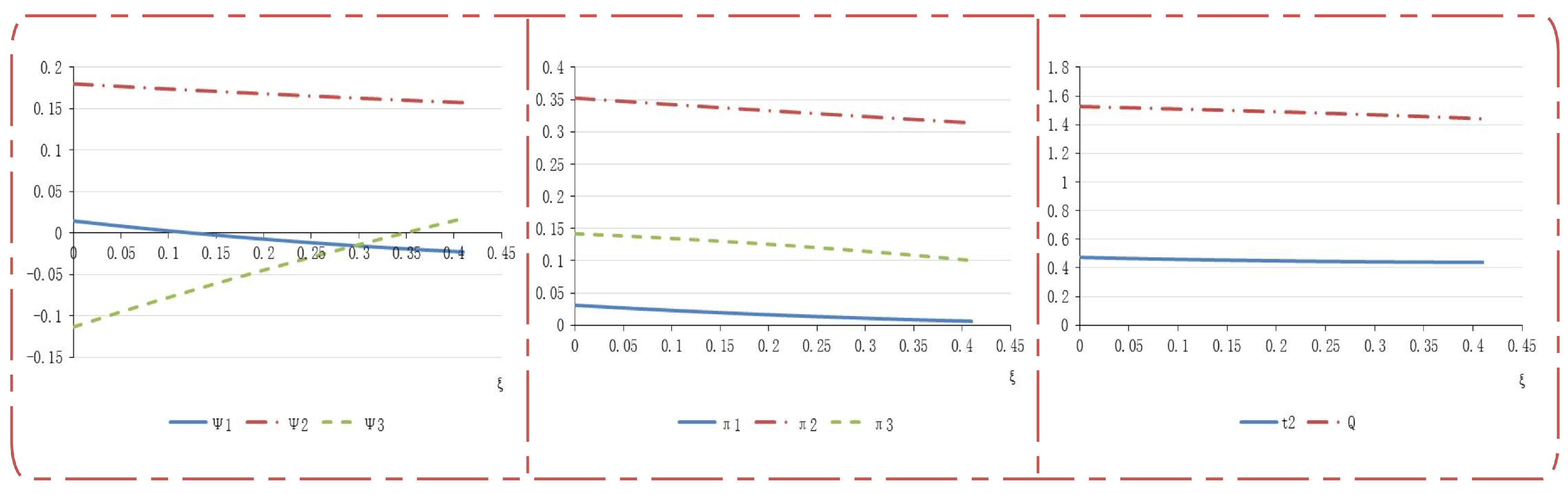

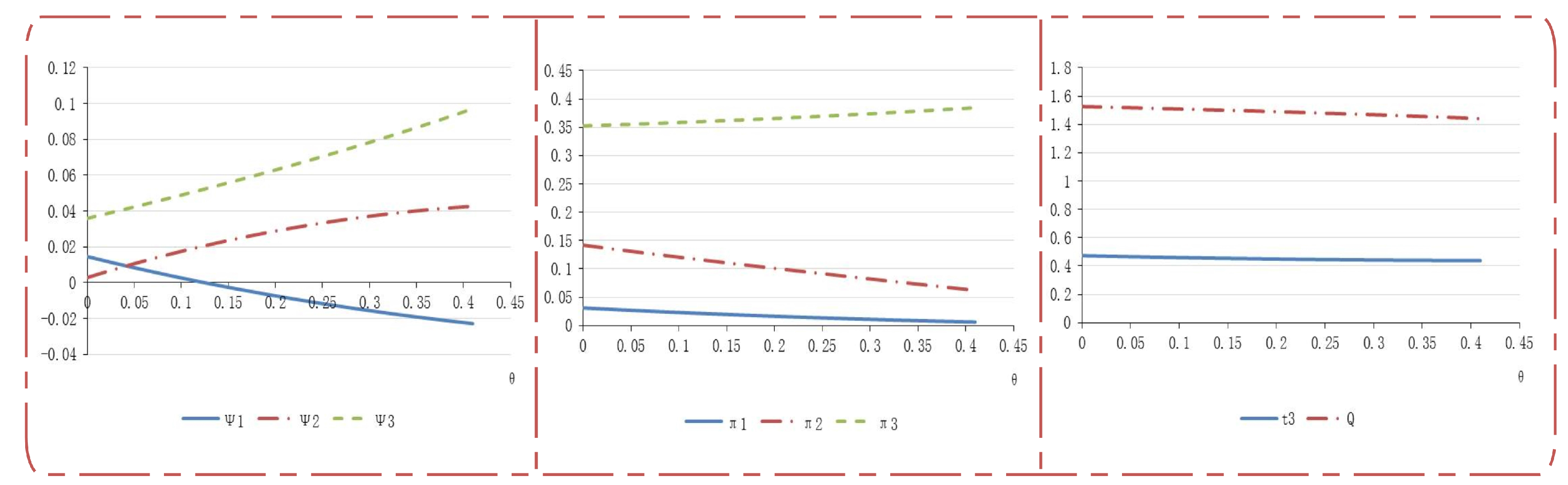

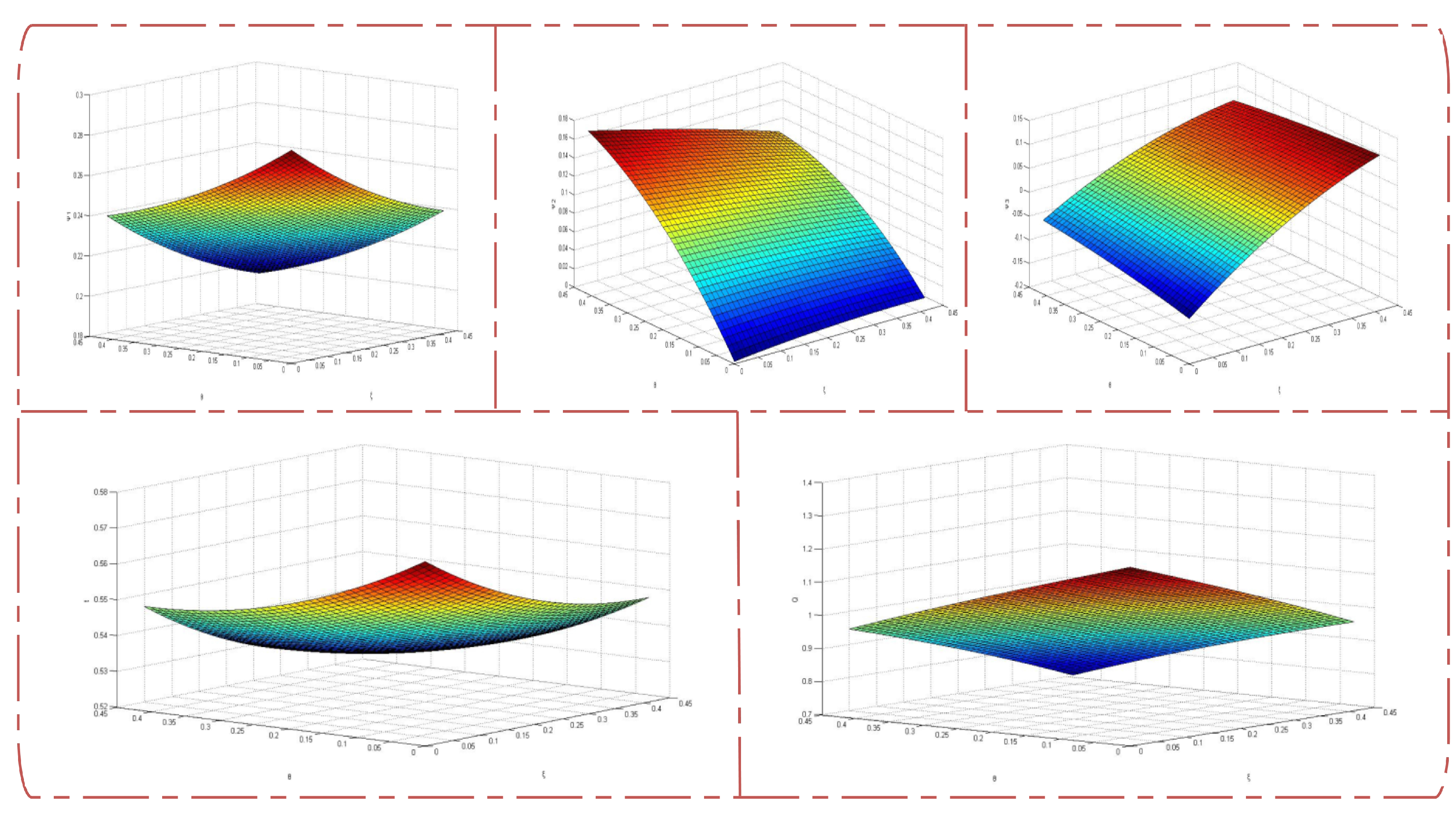

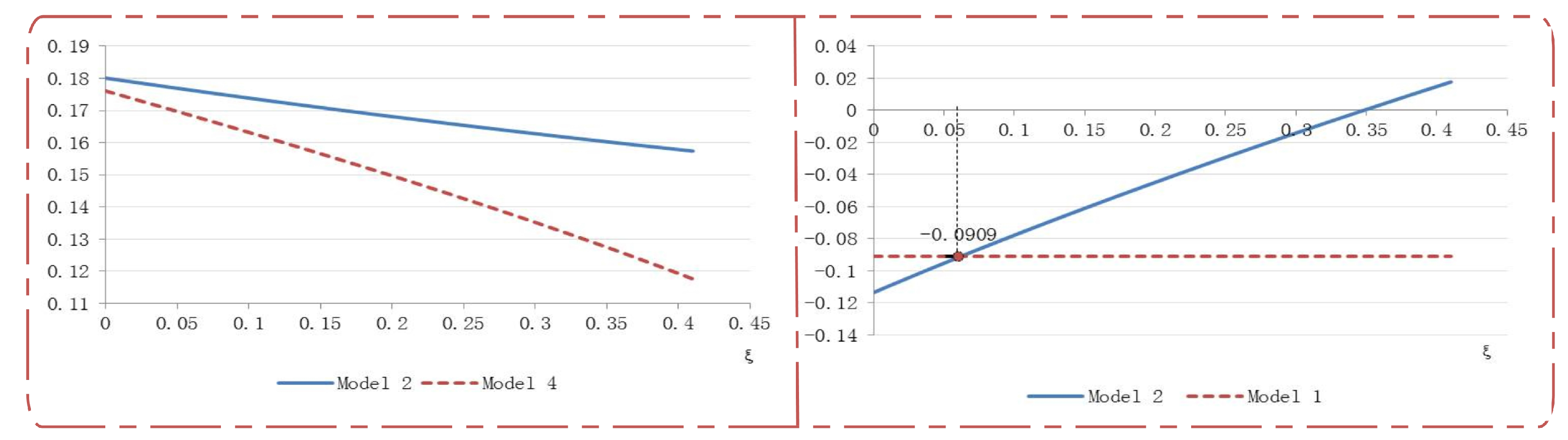

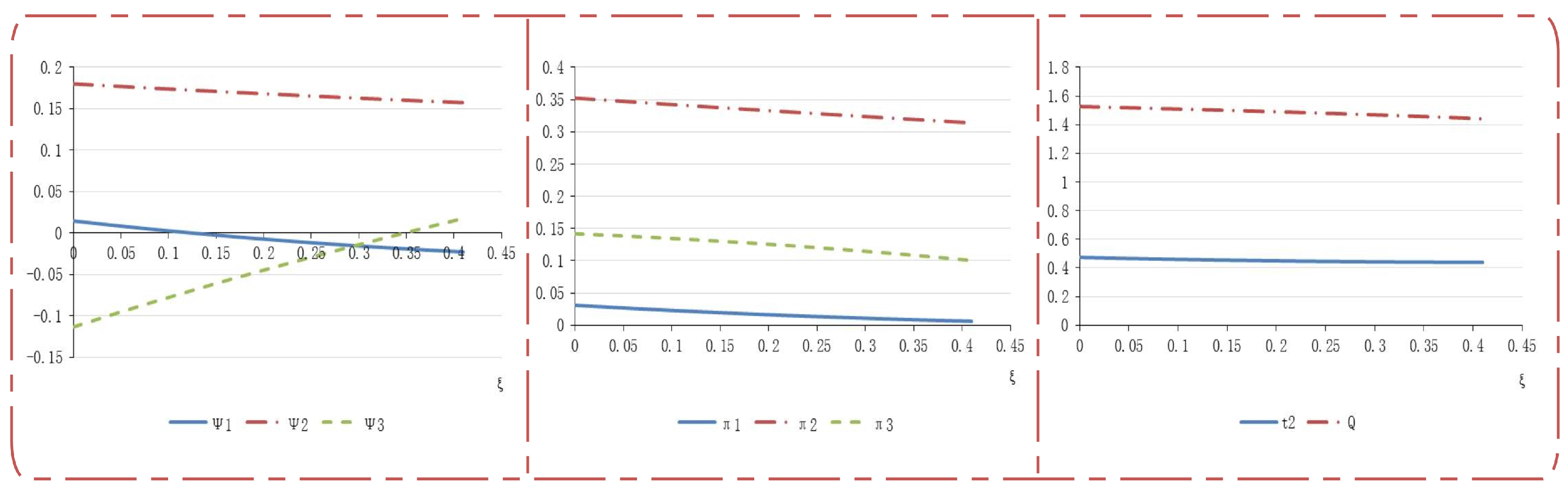

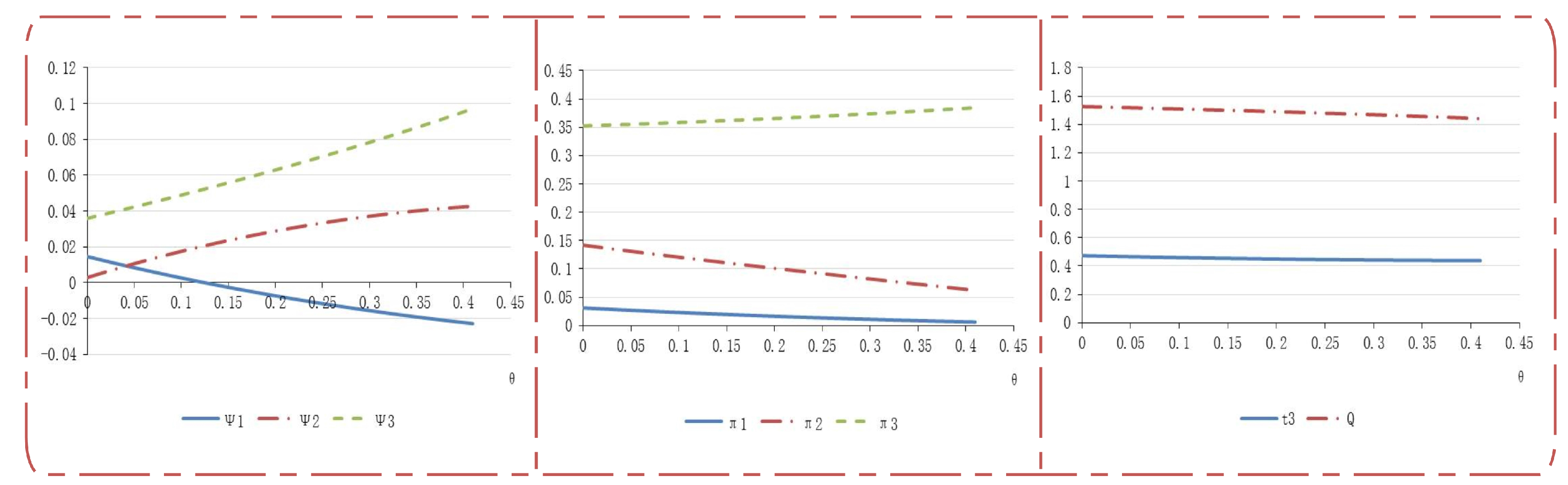

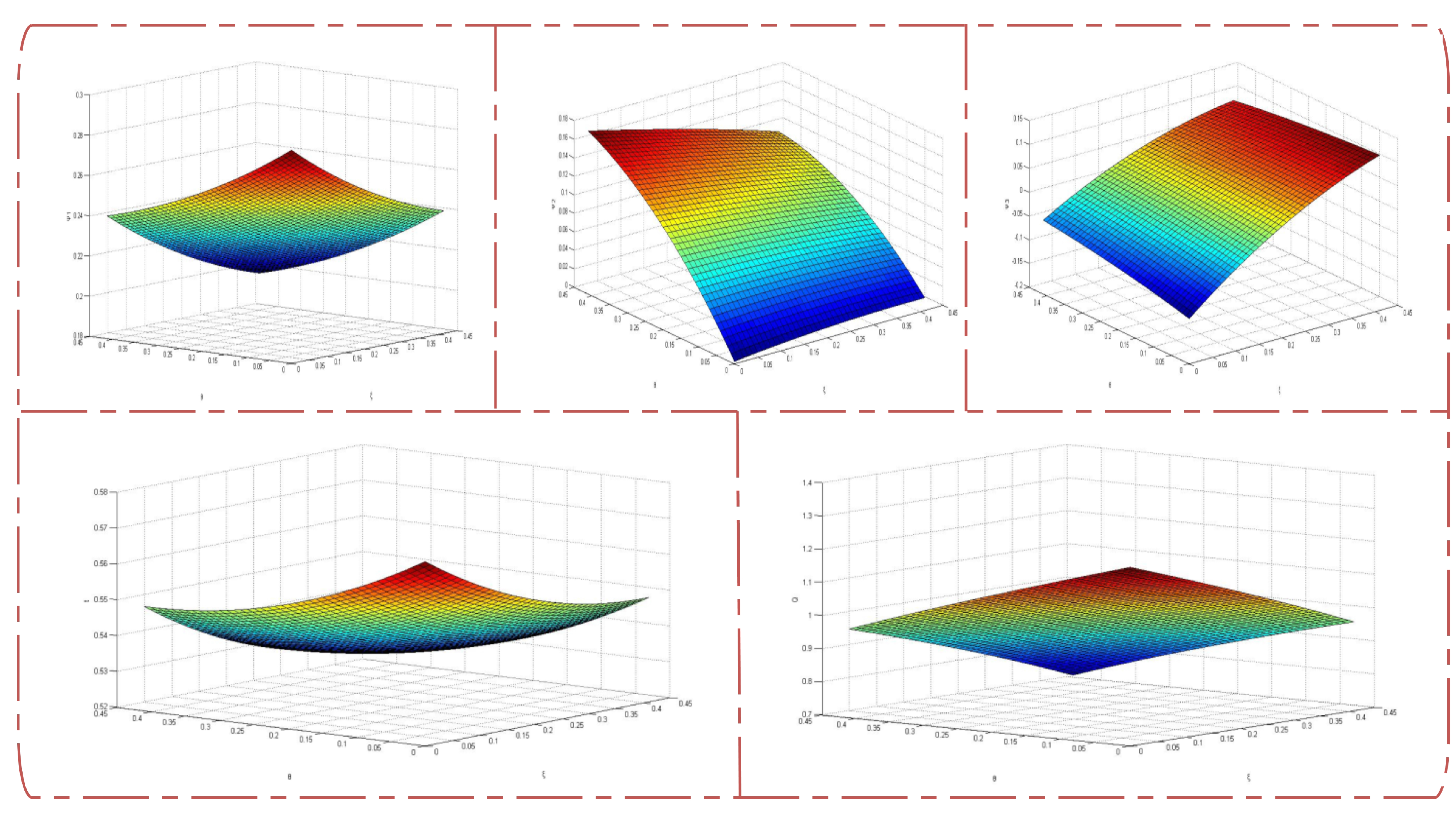

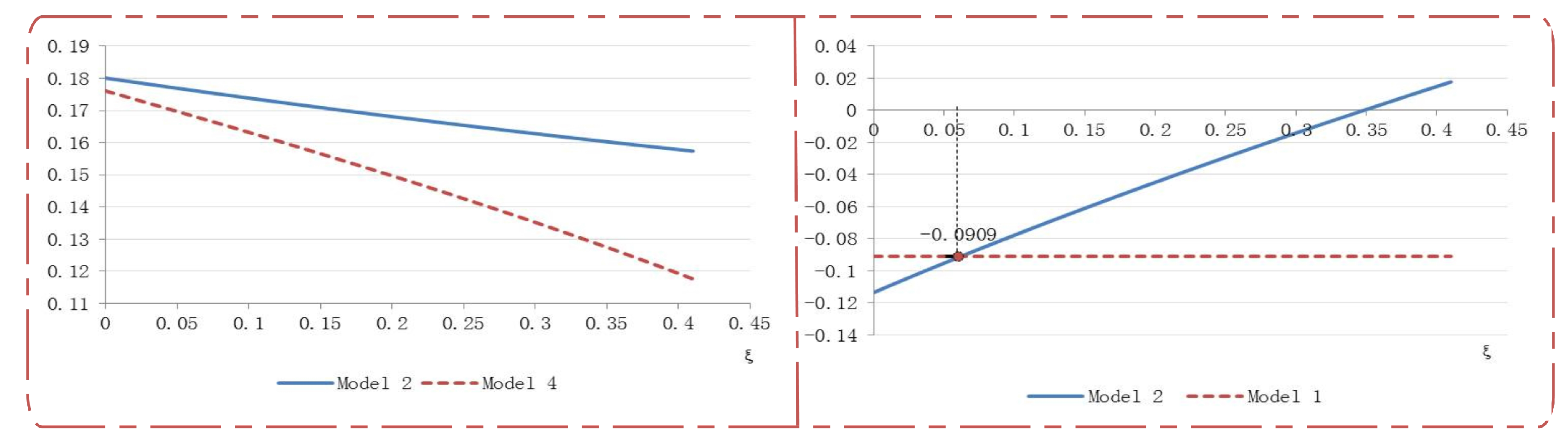

4. Numerical Simulation and Robust Test

4.1. Numerical Simulation

4.2. Robust Test

5. Discussion and Policy Implications

6. Conclusions

Acknowledgments

Author Contributions

Conflicts of Interest

Appendix A

Appendix B

References

- Babiker, M.H.; Rutherford, T.F. The economic effects of border measures in subglobal climate agreements. Energy J. 2005, 26, 99–126. [Google Scholar] [CrossRef]

- Asselt, H.V.; Brewer, T. Addressing competitiveness and leakage concerns in climate policy: An analysis of border adjustment measures in the US and the EU. Energy Policy 2010, 38, 42–51. [Google Scholar] [CrossRef]

- Dissou, Y.; Eyland, T. Carbon control policies, competitiveness, and border tax adjustments. Energy Econ. 2011, 33, 556–564. [Google Scholar] [CrossRef]

- Eyland, T.; Zaccour, G. Strategic effects of a border tax adjustment. Int. Game Theory Rev. 2012, 14, 1–22. [Google Scholar] [CrossRef]

- Sakai, M.; Barrett, J. Border carbon adjustments: Addressing emissions embodied in trade. Energy Policy 2016, 92, 102–110. [Google Scholar] [CrossRef]

- Ibitz, A. Towards a global scheme for carbon emissions reduction in aviation: China’s role in blocking the extension of the European Union’s Emissions Trading Scheme. Asia Eur. J. 2015, 13, 113–130. [Google Scholar] [CrossRef]

- Anger, A. Including aviation in the EU ETS: Impacts on the industry, CO2 emissions and macroeconomic activity in the EU. J. Air Transp. Manag. 2010, 16, 100–105. [Google Scholar] [CrossRef]

- Anger, A.; Köhler, J. Including aviation emissions in the EU ETS: Much ado about nothing? A review. Transp. Policy 2010, 17, 38–46. [Google Scholar] [CrossRef]

- Yoon, S.; Jeong, S. Carbon Emission Mitigation Potentials of Different Policy Scenarios and Their Effects on International Aviation in the Korean Context. Sustainability 2016, 8, 1179. [Google Scholar] [CrossRef]

- Scheelhaase, J.D.; Grimme, W.G. Emissions trading for international aviation—An estimation of the economic impact on selected European airlines. J. Air Transp. Manag. 2007, 13, 253–263. [Google Scholar] [CrossRef]

- Scheelhaase, J.; Grimme, W.; Schaefer, M. The inclusion of aviation into the EU emission trading scheme—Impacts on competition between European and non-European network airlines. Transp. Res. Part D Transp. Environ. 2010, 15, 14–25. [Google Scholar] [CrossRef]

- Vorster, S.; Ungerer, M.; Volschenk, J. 2050 Scenarios for long-haul tourism in the evolving global climate change regime. Sustainability 2012, 5, 1–51. [Google Scholar] [CrossRef]

- Sharp, H.; Grundius, J.; Heinonen, J. Carbon Footprint of Inbound Tourism to Iceland: A Consumption-Based Life-Cycle Assessment including Direct and Indirect Emissions. Sustainability 2016, 8, 1147. [Google Scholar] [CrossRef]

- Higham, J.; Cohen, S.A.; Cavaliere, C.T.; Reis, A.; Finkler, W. Climate change, tourist air travel and radical emissions reduction. J. Clean Prod. 2016, 111, 336–347. [Google Scholar] [CrossRef]

- Mayor, K.; Tol, R.S.J. The impact of the UK aviation tax on carbon dioxide emissions and visitor numbers. Transp. Policy 2007, 14, 507–513. [Google Scholar] [CrossRef]

- Tol, R.S.J. The impact of a carbon tax on international tourism. Transp. Res. Part D Transp. Environ. 2007, 12, 129–142. [Google Scholar] [CrossRef]

- Shi, Y.B. Reducing greenhouse gas emissions from international shipping: Is it time to consider market-based measures? Mar. Policy 2016, 64, 123–134. [Google Scholar] [CrossRef]

- Psaraftis, H.N. Green Maritime Transportation: Market Based Measures; Chapter Green Transportation Logistics; Springer International Publishing: Cham, Switzerland, 2016; pp. 267–297. [Google Scholar]

- Liang, S.; Zhu, L.; Ming, X.; Zhang, T.Z. Waste oil derived biofuels in China bring brightness for global GHG mitigation. Bioresour. Technol. 2013, 131, 139–145. [Google Scholar] [CrossRef] [PubMed]

- Moghaddam, R.F.; Moghaddam, F.F.; Cheriet, M. A modified GHG intensity indicator: Toward a sustainable global economy based on a carbon border tax and emissions trading. Energy Policy 2013, 57, 363–380. [Google Scholar] [CrossRef]

- Arjomandi, A.; Seufert, J.H. An evaluation of the world’s major airlines’ technical and environmental performance. Econ. Model. 2014, 41, 133–144. [Google Scholar] [CrossRef]

- Meunier, G.; Ponssard, J.P.; Quirion, P. Carbon leakage and capacity-based allocations: Is the EU right? J. Environ. Econ. Manag. 2014, 68, 262–279. [Google Scholar] [CrossRef]

- Hering, L.; Poncet, S. Environmental policy and exports: Evidence from Chinese cities. J. Environ. Econ. Manag. 2014, 68, 296–318. [Google Scholar] [CrossRef]

- Trotter, I.M.; Cunha, D.A.D.; Féres, J.G. The relationships between CDM project characteristics and CER market prices. Ecol. Econ. 2015, 119, 158–167. [Google Scholar] [CrossRef]

- Sun, C.W.; Yuan, X.; Yao, X. Social acceptance towards the air pollution in China: Evidence from public’s willingness to pay for smog mitigation. Energy Policy 2016, 92, 313–324. [Google Scholar] [CrossRef]

- Markandya, A.; Ricci, E.C. Green Taxes on Aviation: The Case of Italy. The Proposal of the Green Taxation Matrix; Chapter Environmental Taxes and Fiscal Reform; Palgrave Macmillan: London, UK, 2012; pp. 168–206. [Google Scholar]

- Peterson, E.B.; Lee, H.L. Implications of incorporating domestic margins into analyses of energy taxation and climate change policies. Econ. Model. 2009, 26, 370–378. [Google Scholar] [CrossRef]

- Bassi, A.M.; Yudken, J.S. Climate policy and energy-intensive manufacturing: A comprehensive analysis of the effectiveness of cost mitigation provisions in the American Energy and Security Act of 2009. Energy Policy 2011, 39, 4920–4931. [Google Scholar] [CrossRef]

- Carfì, D.; Schilirò, D. A coopetitive model for the green economy. Econ. Model. 2012, 29, 1215–1219. [Google Scholar] [CrossRef]

- Jayanthakumaran, K.; Liu, Y. Bi-lateral CO2 emissions embodied in Australia-China trade. Energy Policy 2016, 92, 205–213. [Google Scholar] [CrossRef]

- Wang, Q.W.; Su, B.; Zhou, P.; Chiu, C.R. Measuring total-factor CO2 emission performance and technology gaps using a non-radial directional distance function: A modified approach. Energy Econ. 2016, 56, 475–482. [Google Scholar] [CrossRef]

- Gong, C.Z.; Yu, S.W.; Zhu, K.J.; Hailu, A. Evaluating the influence of increasing block tariffs in residential gas sector using agent-based computational economics. Energy Policy 2016, 92, 334–347. [Google Scholar] [CrossRef]

- Fitzgerald, J.; Tol, R.S.J. Airline emissions of carbon dioxide in the European Trading System. CESifo Forum 2007, 1, 51–54. [Google Scholar]

- Mayor, K.; Tol, R.S.J. European Climate Policy and Aviation Emissions; ESRI Working Paper No. 241; ESRI Publishing: Dublin, Ireland, 2008. [Google Scholar]

- Mayor, K.; Tol, R.S.J. Scenarios of carbon dioxide emissions from aviation. Glob. Environ. Chang. 2010, 20, 65–73. [Google Scholar] [CrossRef]

- Elliott, J.; Weisbach, D. Trade and carbon taxes. Am. Econ. Rev. 2010, 100, 465–469. [Google Scholar] [CrossRef]

- Mcmanners, P.J. Developing policy integrating sustainability: A case study into aviation. Environ. Sci. Policy 2016, 57, 86–92. [Google Scholar] [CrossRef]

- Gunasekara, S.G. Environmental overreach: The EU’s carbon tax on international aviation. Wash. Lee J. Energy Clim. Environ. 2013, 5, 1. [Google Scholar]

- Horn, H.; Sapir, A. Can Border Carbon Taxes Fit into the Global Trade Regime? Policy Briefs 805; Bruegel Publishing: Brussels, Belgium, 2013. [Google Scholar]

- Keen, M.; Strand, J. Indirect taxes on international aviation. Fisc. Stud. 2007, 28, 1–41. [Google Scholar] [CrossRef]

- Karp, L.; Zhang, J.F. Taxes versus quantities for a stock pollutant with endogenous abatement costs and asymmetric information. Econ. Theory 2012, 49, 371–409. [Google Scholar] [CrossRef]

- Zhang, X.B.; Zhu, L. Strategic carbon taxation and energy pricing under the threat of climate tipping events. Econ. Model. 2017, 60, 352–363. [Google Scholar] [CrossRef]

- Wu, P.I.; Chen, C.T.; Cheng, P.C.; Liou, J.L. Climate game analyses for CO2 emission trading among various world organizations. Econ. Model. 2014, 36, 441–446. [Google Scholar] [CrossRef]

- Qiao, H.; Song, N.; Lu, B.; Hua, G.W.; Du, H.S. China’s optimal strategy against the European Union aviation carbon tax scheme: A two-stage game model analysis. Environ. Eng. Manag. J. 2015, 14, 1803–1811. [Google Scholar]

- Li, M.; Gao, G.K.; Wang, Y.C. International aviation carbon taxation: Game between EU and Non-EU countries. Adv. Appl. Econ. Financ. 2012, 3, 546–551. [Google Scholar]

- Dong, J.; Ma, Y.; Sun, H. From Pilot to the National Emissions Trading Scheme in China: International Practice and Domestic Experiences. Sustainability 2016, 8, 522. [Google Scholar] [CrossRef]

- Choi, Y.; Lee, H.S. Are Emissions Trading Policies Sustainable? A Study of the Petrochemical Industry in Korea. Sustainability 2016, 8, 1110. [Google Scholar] [CrossRef]

- Barrett, S. Self-enforcing international environmental agreements. Oxf. Econ. Pap. 1994, 46, 878–894. [Google Scholar] [CrossRef]

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| M3 | |||

| R | A | ||

| D2 | R | 0.0740, | (0.1574,0.1801), (,0.0177) |

| A | (0.0028,0.0427), (0.0359,0.0972) | (0.1177,0.1761), () | |

| (0, 0.2565) | [0.2565, 0.5077] | (0.5077, 1) | ||

|---|---|---|---|---|

| (0, 0.3947) | (R, R) | |||

| [0.3947, 0.6759] | (R, R) | |||

| (0.6759, 1) | ||||

© 2017 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

Zheng, J.; Qiao, H.; Wang, S. The Effect of Carbon Tax in Aviation Industry on the Multilateral Simulation Game. Sustainability 2017, 9, 1247. https://doi.org/10.3390/su9071247

Zheng J, Qiao H, Wang S. The Effect of Carbon Tax in Aviation Industry on the Multilateral Simulation Game. Sustainability. 2017; 9(7):1247. https://doi.org/10.3390/su9071247

Chicago/Turabian StyleZheng, Jiali, Han Qiao, and Shouyang Wang. 2017. "The Effect of Carbon Tax in Aviation Industry on the Multilateral Simulation Game" Sustainability 9, no. 7: 1247. https://doi.org/10.3390/su9071247

APA StyleZheng, J., Qiao, H., & Wang, S. (2017). The Effect of Carbon Tax in Aviation Industry on the Multilateral Simulation Game. Sustainability, 9(7), 1247. https://doi.org/10.3390/su9071247