Integrating Sustainability in Organisations: An Activity-Based Sustainability Model

Abstract

:1. Introduction

2. Literature Review

2.1. Sustainable Organisations

- From a strategic perspective, integrated sustainability incorporates the responsibility of organisations towards the market. Organisations achieve economic growth by increasing competitiveness and environmental protection in two aspects (social and environmental), always with a long-term vision [27]. It must involve the entire organisation in achieving the objectives included in the three dimensions of sustainability (social, economic, and environmental), which entails a change in the understanding of the relationships with nature and people [8]. Hediger’s idea [28] is also noteworthy: sustainability should maximise corporate value without depreciating with the passage of time [9,27,29]. This approach is mainly developed through the concept of Corporate Sustainability (CS) [30,31] or CSR [32].

- From an operational approach, it must be accompanied by sustainable management that is responsible for including the environmental and social factors of organisational activities. It must consider economic performance [33], and its objective must be to achieve an individualised result for each dimension of sustainability [3].

2.2. Sustainability Integration Models in Organisations

- (1)

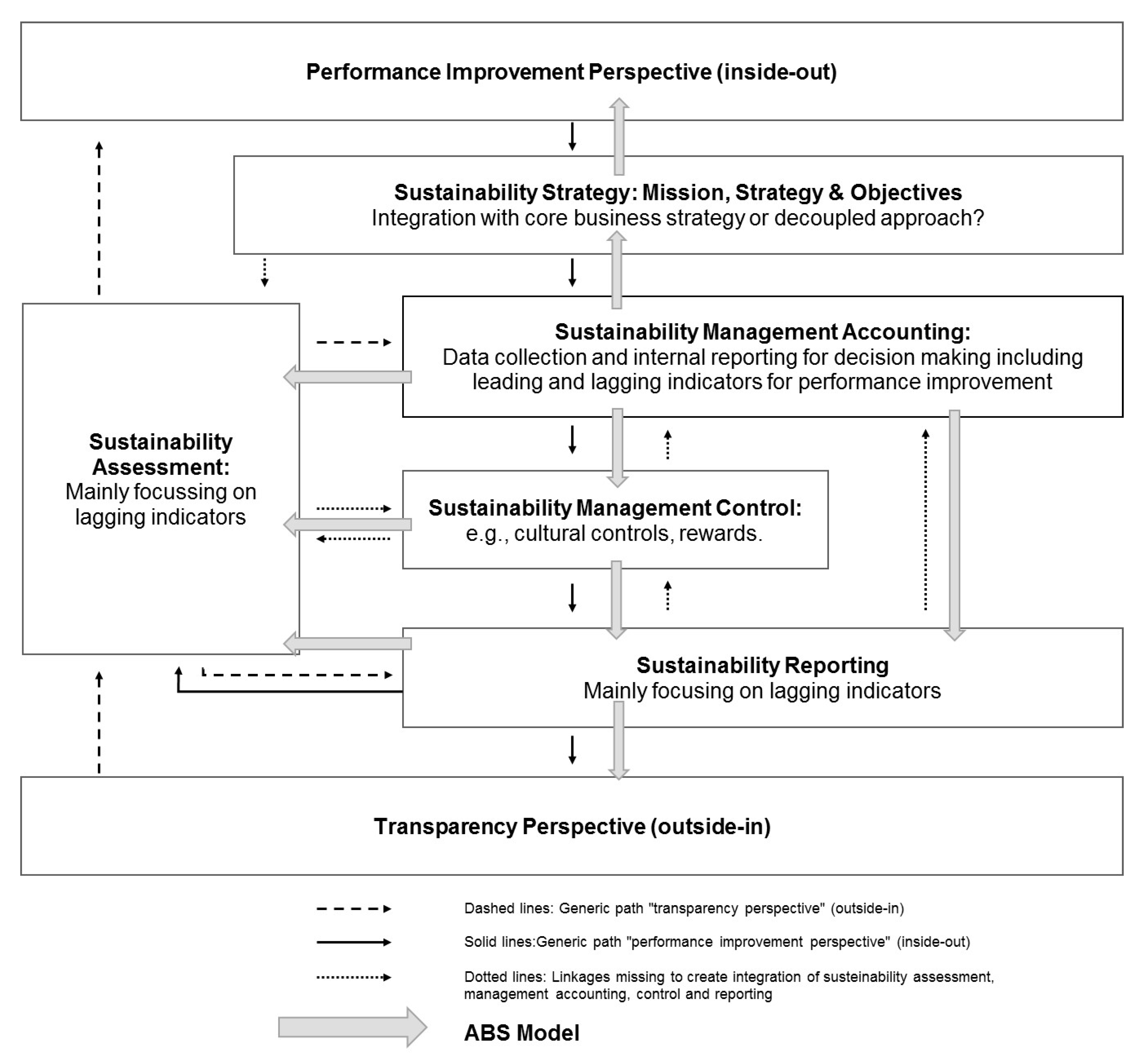

- The performance improvement perspective (inside-out). Sustainability is achieved with the improvement of sustainable performance and through the development of strategies based on quantification. A management accounting system that enables the appropriate selection of sustainability indicators is necessary. These indicators will facilitate system management in line with the objectives proposed in the strategy. This perspective simplifies the flow of information in the communication processes.

- (2)

- The transparency perspective (outside-in). Pressure from stakeholders exerts a substantial impact on the behaviour of organisations, which influences organisational performance. Therefore, the development of high-quality sustainability reports is necessary, implying close and fluid communication with stakeholders.

- Sustainable control management. This linkage includes designing and using controls (both formal and informal) that guarantee and ensure alignment between the behaviour and decisions of an organisation’s employees and the objectives and strategies of the organisation [57].

- (1)

- Capabilities are defined as the adaptive capacity of the organisation to implement necessary changes in its culture and structure in pursuit of sustainability [69].

- (2)

- Processes and practices contribute to sustainability when they are aligned with sustainability strategy principles. Therefore, they must be associated with a sustainable value chain (SVC) [33], include good practices in collaboration with suppliers [70], and consider the information from the operations performed in the organisation [71] (such as green purchasing [72], eco-design [73], or the use of quality management and environmental management systems [74,75]).

- (3)

- (4)

- Elements related to the development of competitive advantages and their contribution to sustainable development are defined as the effort that organisations make to create sustainable value and promote the wellbeing of society and environmental conservation [77].

- (1)

- The performance improvement perspective (inside-out), in which there is a lack of connection between sustainable strategy and the assessment of sustainability.

- (2)

- The transparency perspective (outside-in), in which there is a lack of connection between sustainable communication and sustainability control management and, within this, sustainable accounting management.

- (3)

- Both perspectives: Maas et al. [12] identify a disconnection between sustainability control management and sustainability assessment, and between sustainable management accounting and sustainable communication.

2.3. Sustainable Value Chain

- (1)

- The inside-out perspective: Each activity in the value chain is considered to have an impact on the community in which it operates, and to have positive and/or negative social consequences.

- (2)

- The outside-in perspective: Organisations develop their activities in a competitive environment. Therefore, understanding the dimensions of the external environment will enable the organisation to develop actions that improve productivity and help it to execute its strategy.

3. Activity-Based Sustainability Model (ABS Model)

3.1. ABS Model Foundations

- (1)

- It is a model applicable to any type of organisation, regardless of structure.

- (2)

- It is an approximate representation of the relationship between the productive system and the corporate level.

- (3)

- It is an invaluable tool for conducting an internal analysis of organisations, as it represents all the relevant activities that a company must perform to generate sustainable value through the sale of a product, service, and/or idea.

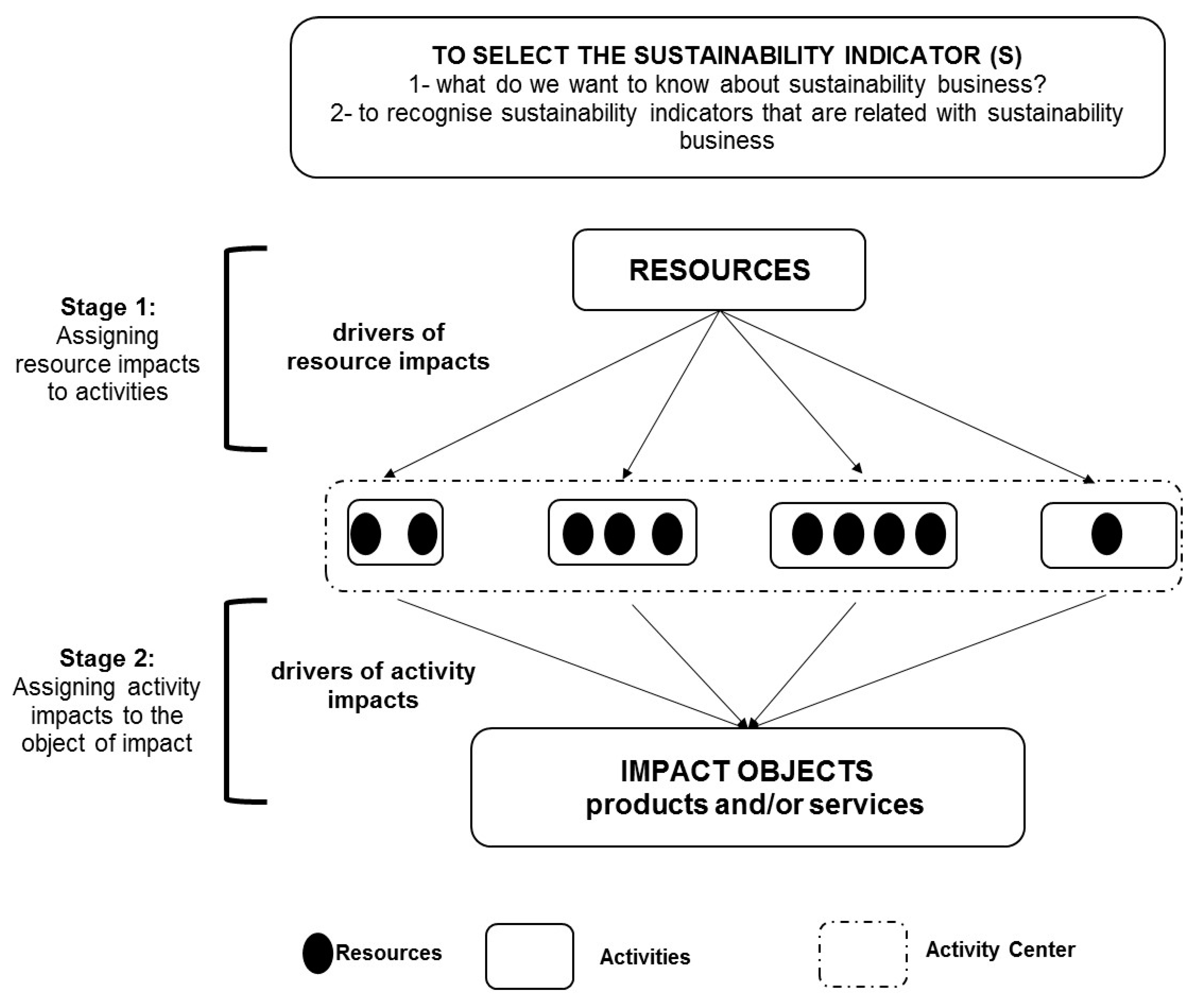

3.2. The ABS Model Process

3.3. Scope of the ABS Model

- Sustainability assessment allows the measurement of sustainability through useful, relevant, understandable, and comparable indicators.

- Sustainable management control facilitates the analysis of deviations between actual and planned data.

- Sustainable management accounting serves to support sustainability standards and management, fulfilling the functions of capturing, measuring, and assessing production activities. It influences planning, resource rationalisation, and controlling activities (as well as the organisation’s decision-making process).

- Sustainable communication for the learning process and organisational improvement.

4. Implications of the ABS Model for Sustainability Integration Models

4.1. The ABS Model and the Sustainability Integration Model in Organisations

- (1)

- The link between management control systems and sustainability assessment methods: The most immediate result of the ABS model is sustainability indicators that, due to their characteristics and those of the ABS model, can (a) describe the organisation’s situation with regard to sustainable topics; and (b) establish a control mechanism with regard to the actions implemented to reduce their impacts (because the ABS model establishes a relationship between activity and impact, that allows the implementation of specific reduction and/or elimination actions). These can be verified on the basis of the fulfilment of the established objectives (otherwise, it enables error identification to correct actions that generate deviations from the established objectives).

- (2)

- The link between sustainable management accounting and sustainable communication: One result of the ABS model is a sustainability indicator. It can provide information about the organisation’s actions, fulfilling the requirements of the standards for the preparation of sustainability reports. For example, if the organisation wants to know its contribution to climate change, it can measure its carbon footprint with the ABS model and can include this measurement among the climate change indicators of the GRI report.

- (1)

- The link between measuring sustainability and sustainable management control. One of the objectives of cost accounting is to plan and control operations, activities, and resources. Thus, an analysis of the organisation’s internal efficiency is developed. The ABS model provides information on the impact generated by these activities. Therefore, one of the model’s results is an analysis of the organisational structure regarding the assessment of environmental sustainability.

- (2)

- The link between sustainable management accounting and sustainable communication. Communication aims to provide information to stakeholders on the organisation’s activities with respect to sustainability. Thus, the ABS model provides sustainability indicators that comply with this use for communication.

4.2. The ABS Model and the Sustainability Integration Model Based on Organisational Performance

- Capabilities: Knowledge of the resources consumed by the activities and the transformation process of the organisation allows for (1) determination of what type of technology to use and how to use it to be more sustainable; (2) knowledge of the resources available and how they should be used for greater efficiency; (3) knowledge of what type of resources are needed to achieve sustainability; and (4) knowledge of the competencies that must be acquired to create a sustainable organisation.

- Offerings: If a sustainable transformation process is achieved, the product/service will be sustainable. The result of the ABS model is the impact, good or bad, of the product or service generated in the organisation.

- Contributions to sustainable development as a competitive advantage: The ABS model implies the development of sustainable competitive advantages because it is based on the concept of SVC (defined by Porter and Kramer) [1]. In addition, the ABS model contributes to sustainable development because its purpose is the integration of sustainability into the organisation, which (according to Morioka and Carvalho [13]) is how organisations can contribute to sustainable development.

- (1)

- The ABS model allows the sustainable management of the organisation’s value chain and supply chain, based on the impacts (good and/or bad) that are generated by the activities and processes involved. Thus, the ABS model can be applied to any organisation that wants to introduce sustainability criteria into its internal processes.

- (2)

- The output of the ABS model is a sustainability indicator that reflects the efficiency of the structure of the organisation, and thus facilitates the assessment of the organisation’s sustainable performance. Therefore, it provides a useful tool for assessing the sustainability performance of organisations, which is lacking in the model of Morioka and Carvallo [13].

- (3)

- The ABS model facilitates the quantification of the Triple Bottom Line because it is able to analyse any indicator related to the sustainability strategy of an organisation.

- (4)

- The ABS model follows the CSR criteria and takes into account the stakeholders. Therefore, it must comply with current legislation (both in general and with regard to the economic sector to which it belongs), and act respectfully and in view of the improvement of the environment (both environmental and social).

5. Conclusions

Author Contributions

Conflicts of Interest

References

- Porter, M.E.; Kramer, M.R. Strategy & Society: The link between competitive advantage and corporate social responsibility. Harv. Bus. Rev. 2006, 84, 78–92. [Google Scholar] [PubMed]

- Figge, F.; Hahn, T. Sustainable value added—Measuring corporate contributions to sustainability beyond eco-efficiency. Ecol. Econ. 2004, 48, 173–187. [Google Scholar] [CrossRef]

- Lankoski, L. Alternative conceptions of sustainability in a business context. J. Clean. Prod. 2016, 139, 847–857. [Google Scholar] [CrossRef]

- Asif, M.; Searcy, C.; Zutshi, A.; Fisscher, O.A.M. An integrated management systems approach to corporate social responsibility. J. Clean. Prod. 2013, 56, 7–17. [Google Scholar] [CrossRef]

- Waage, S.A.; Geiser, K.; Irwin, F.; Weissman, A.B.; Bertolucci, M.D.; Fisk, P.; Basile, G.; Cowan, S.; Cauley, H.; McPherson, A. Fitting together the building blocks for sustainability: A revised model for integrating ecological, social and financial factor into business decision-making. J. Clean. Prod. 2005, 13, 1145–1164. [Google Scholar] [CrossRef]

- Hart, S.L.; Christensen, C.M. The Great Leap. Driving Innovation form the “Base of the Pyramid”. MIT Sloan Manag. Rev. 2002, 44, 51–57. [Google Scholar]

- Robinson, J. Squaring the circle? Some thoughts on the idea of sustainable development. Ecol. Econ. 2004, 48, 369–384. [Google Scholar] [CrossRef]

- Hopwood, B.; Mellor, M.; O’Brien, G. Sustainable development: Mapping different approaches. Sustain. Dev. 2005, 13, 38–52. [Google Scholar] [CrossRef]

- Shrivastava, P.; Hart, S.L. Creating Sustainable Corporations. Bus. Strategy Environ. 1995, 4, 154–165. [Google Scholar] [CrossRef]

- Carter, C.R.; Rogers, D.S. A framework of sustainability supply chain management: Moving toward new theory. Int. J. Phys. Distrib. Logist. Manag. 2008, 35, 177–194. [Google Scholar] [CrossRef]

- Maas, K.; Schaltegger, S.; Crutzen, N. Advancing the integration of corporate sustainability measurement, management and reporting. J. Clean. Prod. 2016, 133, 859–862. [Google Scholar] [CrossRef]

- Maas, K.; Schaltegger, S.; Crutzen, N. Integrating corporate sustainability assessment, management accounting, control and reporting. J. Clean. Prod. 2016, 136, 237–248. [Google Scholar] [CrossRef]

- Morioka, S.N.; de Carvalho, M.M. A systematic literature review towards a conceptual framework for integrating sustainability performance into business. J. Clean. Prod. 2016, 136, 134–146. [Google Scholar] [CrossRef]

- Mokate, K.M. Eficacia, Eficiencia, Equidad y Sostenibilidad: ¿Qué Queremos Decir? Banco Interamericano de Desarrollo; Departamento de Integración y Programa Regionales: Washington, DC, USA, 2001. (In Spanish) [Google Scholar]

- Marshall, J.D.; Toffel, M.W. Framing the elusive concept of sustainability: A sustainability hierarchy. Environ. Sci. Technol. 2005, 39, 673–682. [Google Scholar] [CrossRef] [PubMed]

- Bolis, I.; Morioka, S.N.; Sznelwar, L.I. When sustainable development risks losing its meaning. Delimiting the concept with a comprehensive literature review and a conceptual model. J. Clean. Prod. 2014, 83, 7–20. [Google Scholar] [CrossRef]

- Schalock, R.L.; Verdugo, M.; Lee, T. A systematic approach to an organisation’s sustainability. Eval. Progr. Plan. 2016, 56, 56–63. [Google Scholar] [CrossRef] [PubMed]

- Wiedmann, T.O.; Lenzen, M.; Barrett, J.R. Companies on the scale: Ecological foundations for corporate sustainability. J. Manag. Stud. 2009, 50, 307–336. [Google Scholar] [CrossRef]

- Ketola, T. Five laps to corporate sustainability through a corporate responsibility portfolio matrix. Corp. Soc. Responsib. Environ. Manag. 2010, 17, 320–336. [Google Scholar] [CrossRef]

- Schaltegger, S.; Wagner, M. Sustainable entrepreneurship and sustainability innovation: Categories and interactions. Bus. Strategy Environ. 2011, 20, 222–237. [Google Scholar] [CrossRef]

- Schrettle, S.; Hinz, A.; Scherrer-Rathje, M.; Friedli, T. Turning sustainability into action: Explaining firm’s sustainability efforts and their impact on firm performance. Int. J. Prod. Econ. 2014, 147, 73–84. [Google Scholar] [CrossRef]

- Figge, F.; Hahn, T.; Schaltegger, S.; Wagner, M. The sustainability balanced scorecard-linking sustainability management to business strategy. Bus. Strategy Environ. 2002, 11, 269–284. [Google Scholar] [CrossRef]

- Lozano, R. Developing collaborative and sustainable organisations. J. Clean. Prod. 2008, 16, 499–509. [Google Scholar] [CrossRef]

- Montiel, I. Corporate social responsibility and corporate sustainability: Separate pasta, common future. Organ. Environ. 2008, 21, 245–269. [Google Scholar] [CrossRef]

- Okoye, A. Theorising corporate social responsibility as an essentially contested concept: Is a definition necessary? J. Bus. Ethics 2009, 89, 613–627. [Google Scholar] [CrossRef]

- Lozano, R. A holistic perspective on corporate sustainability drivers. Corp. Soc. Responsib. Environ. Manag. 2015, 22, 32–44. [Google Scholar] [CrossRef]

- Elkintong, J. Partnerships from cannibals with forks: The triple bottom line of 21st Century Business. Environ. Qual. Manag. 1998, 8, 37–51. [Google Scholar] [CrossRef]

- Hediger, W. Welfare and capital-theoretic foundation of corporate social responsibility and corporate sustainability. J. Socio-Econ. 2010, 39, 518–526. [Google Scholar] [CrossRef]

- Toro, D. El enfoque estratégico de la responsabilidad social corporativa: Revisión de la literatura académica. Intang. Cap. 2006, 2, 338–358. (In Spanish) [Google Scholar]

- Dyllick, T.; Hockerts, K. Beyond the business case for corporate sustainability. Bus. Strategy Environ. 2002, 11, 130–141. [Google Scholar] [CrossRef]

- Lozano, R. Towards better embedding sustainability into companies’s systems: An analysis of voluntary corporate initiative. J. Clean. Prod. 2012, 25, 14–16. [Google Scholar] [CrossRef]

- Panagiotakopoulos, P.D.; Espinosa, A.; Walker, J. Sustainability management: Insights from the viable system model. J. Clean. Prod. 2016, 113, 792–806. [Google Scholar] [CrossRef]

- Seuring, S.; Müller, M. From literature review to a conceptual framework for sustainable supply chain management. J. Clean. Prod. 2008, 16, 1699–1710. [Google Scholar] [CrossRef]

- Rajak, S.; Vinodh, S. Application of fuzzy logic for social sustainability performance evaluation: A case study of an Indian automotive component manufacturing organisation. J. Clean. Prod. 2015, 108, 1184–1192. [Google Scholar] [CrossRef]

- Nunes, B.; Alamino, R.C.; Shaw, D.; Bennett, D. Modelling sustainability performance to achieve absolute reductions in socio-ecological systems. J. Clean. Prod. 2016, 132, 32–44. [Google Scholar] [CrossRef]

- Kurucz, E.C.; Colbert, B.A.; Lüdeke-Freund, F.; Upward, A.; Willard, B. Relational leadership for strategic sustainability: Practices and capabilities to advance the design and assessment of sustainable business models. J. Clean. Prod. 2016, 1–16. [Google Scholar] [CrossRef]

- Lu, I.-Y.; Lin, T.-S.; Tzeng, G.-H.; Huang, S.-L. Multicriteria Decision Analysis to develop effective sustainable development strategies for enhancing competitive advantage: Case of the TFT-LCD Industry in Taiwan. Sustainability 2016, 8, 646. [Google Scholar] [CrossRef]

- Leppelt, T.; Foerstl, K.; Reuter, C.; Hartmann, E. Sustainability management beyond organisational boundaries-sustainable supplier relationship management in the chemical industry. J. Clean. Prod. 2013, 56, 94–102. [Google Scholar] [CrossRef]

- Marcelino-Sábada, S.; Gónzalez-Jaen, L.F.; Pérez-Ezcurdia, A. Using Project management as a way to sustainability. From a comprehensive review to a framework definition. J. Clean. Prod. 2015, 99, 1–16. [Google Scholar] [CrossRef]

- Mustapha, M.A.; Manan, Z.A.; Alwi, S.R.W. Sustainbale Green Management System (SGMS)—An integrated approach towards organisational sustainability. J. Clean. Prod. 2016. [Google Scholar] [CrossRef]

- Svenson, G.; Wood, G.; Callaghan, M. A corporate Model of sustainable business practices: An ethical perspective. J. World Bus. 2010, 45, 335–345. [Google Scholar] [CrossRef]

- Hörisch, J.; Ortas, E.; Schaltegger, S.; Álvarez, I. Environmental effects of sustainability mangement tools: An empirical analysis of large companies. Ecol. Econ. 2015, 120, 241–249. [Google Scholar] [CrossRef]

- Angelakoglou, K.; Gaidajis, G. A review of methods contributing to the assessment of the environmental sustainability of industrial systems. J. Clean. Prod. 2015, 108, 725–747. [Google Scholar] [CrossRef]

- Phillips, J. The Geocybernetic Assessment Matrix (GAM)—A new assessment tool of evaluating the level and nature of sustainability or unsustainability. Environ. Impact Assess. Rev. 2016, 56, 88–101. [Google Scholar] [CrossRef]

- Rahdari, A.H.; Rostamy, A.A.A. Designing a General Set of Sustainability Indicators at the Corporate Level. J. Clean. Prod. 2015. [Google Scholar] [CrossRef]

- Kylili, A.; Fokaides, P.A.; Lopez-Jimenez, P.A. Key Performance Indicator (KPIs) approach in buildings renovation for the sustainability of the built environment: A review. Renew. Sustain. Energy Rev. 2016, 56, 906–915. [Google Scholar] [CrossRef]

- Garcia, S.; Cintra, Y.; Torres, R.C.S.R.; Lima, F.G. Corporate sustainability management: A proposed multi-criteria model to support balanced decision-making. J. Clean. Prod. 2016. [Google Scholar] [CrossRef]

- Pastakia, C.M.R.; Jensen, A. The rapid impact assessment matrix (RIAM) for EIA. Environ. Impact Assess. Rev. 1998, 18, 461–482. [Google Scholar] [CrossRef]

- Lozano, R.; Huisingh, D. Inter-linking issues and dimensions in sustainability reporting. J. Clean. Prod. 2011, 19, 99–107. [Google Scholar] [CrossRef]

- Fonseca, A.; McAllister, M.L.; Fitzpatrick, P. Sustainability reporting among mining corporations: A constructive critique of the GRI approach. J. Clean. Prod. 2014, 84, 70–83. [Google Scholar] [CrossRef]

- Hsu, C.W.; Lee, W.H.; Chao, W.C. Materiality analysis in sustainability reporting: A case study at Lite-On Technology Corporation. J. Clean. Prod. 2013, 57, 142–151. [Google Scholar] [CrossRef]

- Siew, R.Y.J. A review of corporate sustainability reporting tools (SRTs). J. Environ. Manag. 2015, 164, 180–195. [Google Scholar] [CrossRef] [PubMed]

- Pope, J.; Annandale, D.; Morrison-Saunders, A. Conceptualising sustainability assessment. Environ. Impact Assess. Rev. 2004, 24, 595–616. [Google Scholar] [CrossRef]

- Azzone, G.; Brophy, M.; Noci, G.; Welford, R.; Young, W. A stakeholder’s view of environmental reporting. Long Range Plan. 1997, 30, 699–709. [Google Scholar] [CrossRef]

- Schaltegger, S.; Burritt, R. Contemporary Environmental Accounting: Issues, Concepts and Practice; Greenleaf: Sheffield, UK, 2000; ISBN 1-874719-35-7. [Google Scholar]

- Schaltegger, S.; Burritt, R. Sustainability accounting for companies: Catchphrase or decision support for business leaders? J. World Bus. 2010, 45, 375–384. [Google Scholar] [CrossRef]

- Malmi, T.; Brown, D.A. Management control systems as a package-opportunities, challenges and research directions. Manag. Account. Res. 2008, 19, 287–300. [Google Scholar] [CrossRef]

- Christofi, A.; Chirstofi, P.; Sisaye, S. Corporate sustainability: Historical development and reporting practice. Manag. Res. Rev. 2012, 35, 157–172. [Google Scholar] [CrossRef]

- Hahn, R.; Kühnen, M. Determinants of sustainability reporting: A review of results, trend, theory and opportunities in an expending field of research. J. Clean. Prod. 2013, 59, 5–21. [Google Scholar] [CrossRef]

- Global Reposting Initiative (GRI). Sustainability Reporting Guidelines 2002. Available online: www.globalreporting.org (accessed on 20 January 2017).

- Zadek, S.; Merme, M. Redefining Materiality: Practice and Public Policy for Effective Corporate Reporting; Institute of Social and Ethical Accountability: London, UK, 2003. [Google Scholar]

- Kolk, A. Trends in sustainability reporting by the Fortune Global 2050. Bus. Strategy Environ. 2003, 12, 279–291. [Google Scholar] [CrossRef]

- Lindgreen, A.; Swaen, V. Corporate Social Responsibility. Int. J. Manag. Rev. 2010, 12, 1–7. [Google Scholar] [CrossRef]

- Weil, W.B.; Winter-Watson, B. The Internet and Sustainability Reporting: Improving Communication with stakeholders. In The Ecology of the New Economy: Sustainable Transformation of Global Information, Communications and Electronics Industries; Greenleaf Publishing in Association with GSE Research: Oxford, UK, 2002; pp. 85–95. [Google Scholar]

- Dentchev, N. Corporate social performance: Business rationale, competitiveness threats and management challenges. Bus. Soc. 2007, 46, 104–116. [Google Scholar] [CrossRef]

- Gadenne, D.; Mila, L.; Sand, J.; Winata, L.; Hooi, G. The influence of sustainability performance management practices on organisational sustainability performance. J. Account. Organ. Chang. 2012, 8, 201–235. [Google Scholar] [CrossRef]

- Klassen, R.D.; McLaughlin, C.P. The impact of environmental management on firm performance. Manag. Sci. 1996, 42, 1199–1214. [Google Scholar] [CrossRef]

- Kolk, A.; Mauser, A. The evolution of environmental management: From stage models to performance evaluation. Bus. Strategy Environ. 2002, 11, 14–31. [Google Scholar] [CrossRef]

- Pereira-Moliner, J.; Claver-Cortés, E.; Molina-Azorín, J.F.; Tarí, J.J. Quality management, environmental management and firm performance: Direct and mediating effects in the hotel industry. J. Clean. Prod. 2012, 37, 82–92. [Google Scholar] [CrossRef]

- Grosvold, J.; Hoejmdes, S.U.; Roehrich, J.K. Squaring the circle: Management, measurement and performance of sustainability in supply chains. Supply Chain Manag. Int. J. 2014, 19, 292–305. [Google Scholar] [CrossRef]

- Stefanelli, N.O.; Chiappetta Jabbour, C.J.; de Sousa Jabbour, A.B.L. Green supply chain management and environmental performance of firms in the bioenergy sector in Brazil: An exploratory survey. Energy Policy 2014, 75, 312–315. [Google Scholar] [CrossRef]

- Chiappetta Jabbour, C.J.; de Sousa Jabbour, A.B.L.; Govindan, K.; Teixeira, A.A.; de Souza Freitas, W.R. Environmental management and operational performance in Automotive companies in Brazil: The role of human resource management and lean manufacturing. J. Clean. Prod. 2013, 47, 129–140. [Google Scholar] [CrossRef]

- Chang, R.Y.K.; He, H.; Kai, H.; Wang, W.Y.C. Environmental orientation and corporate performance: The mediation mechanism of green supply chain management and moderating effect of competitive intensity. Ind. Mark. Manag. 2012, 41, 621–630. [Google Scholar] [CrossRef]

- Yang, M.G.; Hong, P.; Modi, S.B. Impact of lean manufacturing and environmental management on business performance: An empirical study of manufacturing firms. Int. J. Prod. Econ. 2011, 129, 251–261. [Google Scholar] [CrossRef]

- Benavides-Velasco, C.A.; Quintana-García, C.; Marchante-Lara, M. Management total quality management, corporate social responsibility and performance in the hotel industry. Int. J. Hosp. Manag. 2014, 41, 77–87. [Google Scholar] [CrossRef]

- Huang, Y.C.; Wong, Y.J.; Yang, M.L. Proactive environmental management and performance by a controlling family. Manag. Res. Rev. 2014, 37, 210–214. [Google Scholar] [CrossRef]

- Chinander, K.R. Aligning accountability and awareness for environmental performance in operations. Prod. Oper. Manag. 2001, 10, 276–291. [Google Scholar] [CrossRef]

- Porter, M.E. Competitive Advantage: Creating and Sustaining Superior Performance; Free Press: New York, NY, USA, 1985. [Google Scholar]

- Porter, M.E. Ventaja Competitiva. Creación y Sostenibilidad de un Rendimiento Superior; Ediciones Pirámide S.A.: Madrid, Spain, 2013. (In Spanish) [Google Scholar]

- Hart, S.L. A Natural Resource Based View of the Firm. Acad. Manag. Rev. 1995, 20, 986–1014. [Google Scholar]

- Menguzzato, M.; Renau, J.J. La Dirección Estratégica de la Empresa. Un Enfoque Innovador del Management; Editorial Ariel S.A.: Barcelona, Spain, 1991. (In Spanish) [Google Scholar]

{kind=link}

{kind=link}

{kind=link}

| Integration Approach | Authors | Scope/Basis | Integration Proposal |

|---|---|---|---|

| Sustainable performance | Rajak and Vinodh [34] | Approach to assessing sustainability from a social perspective | A social sustainability integration method divided into six steps: literature review, conceptual model development, assessment of social sustainability, approximation of linguistic terms by fuzzy numbers, determination of the Fuzzy Social Sustainability Index (FSSI), and identification and analysis of the Fuzzy Performance Importance Index (FPII) |

| Nunes et al. [35] | Systematic approach analyses the limits of the natural environment using a toy model to model the sustainability of systems | The integration of sustainability by modelling the evolution of systems under some restrictions; proposes the Sustainability Management Model in Sweden | |

| Sustainable strategy | Kurucz et al. [36] | Integrates the Framework for Strategic Sustainable Development (FSSD) and the Planet Boundary Approach (PBA) | The FSSD is structured into five levels: systems, success, strategic guidelines, actions, and tools |

| Kuo et al. [37] | Hybrid-modified Multiple Attribute Decision-Making model combined with the Decision-Making Trial and Evaluation Laboratory (DEMATEL) technique; considers sustainable competitive advantage an aspiration level; environmental approach | Constructs the Influential Network Relation Map (INRM); integrates sustainability and competitive advantage concepts to formulate the most effective allocation strategies for natural resources | |

| Management | Shrivastava and Hart [9] | Analysis of organisational design elements; sustainable organisation design | Integrated environmental management |

| Leppelt et al. [38] | Integrates Sustainable Supplier Relationship Management (SSRM) in Sustainable Performance Management (SPM) [41]; focuses on the chemical industry | Sustainability management beyond corporate limits | |

| Marcelino-Sábada et al. [39] | Identifies the lack of integration of sustainability in project management | A new concept of sustainable project management | |

| Mustapha et al. [40] | Integrates ISO standards, the Deming Cycle, or the PDCA Cycle | A green sustainable management system | |

| Schaclok et al. [17] | Incorporates continuous improvement criteria; drivers of change: accounting, leadership, and the organisation | The creation of a sustainability model through the systematic approach of continuous quality improvement | |

| Panagiotakopoulos et al. [32] | Incorporates ISO 26000 criteria in FSSD | The Viable System Model (VSM) | |

| Quantification | Hörisch et al. [42] | Environmental approach | Analysis of the effectiveness of management tools for sustainability in large companies |

| Angelakoglou and Gaidajis [43] | Focuses on assessing environmental sustainability | A review of quantification tools | |

| Phillips [44] | Rapid Impact Assessment Matrix [48] | The Geocybernetic Assessment Matrix (GAM) | |

| Rahdari and Rostamy [45] | Quantification of indicators in general | Designing sustainability indicators | |

| Kylili et al. [46] | Quantification of indicators linked to construction project management | Designing Performance Indicators (KPIs) | |

| García et al. [47] | Based on Hörisch et al. [42]; adaptation of the Integrated Environmental Evaluation of Water Resources Development (IEE) model; measures the Triple Bottom Line | The Integrated Environmental Evaluation-Sustainability Business (IEE-SB) model | |

| Communication | Lozano and Huisingh [49] | Analysis of Sustainability Reporting (SR) | Highlights the influence of sustainability reports as a mechanism for integrating sustainability in organisations |

| Fonseca et al. [50] | Based on Bellagio STAMP and how it covers the gaps of Global Reporting Initiative (GRI) reports; focuses on the mining sector | A conceptual proposal for sustainability evaluation and communication | |

| Hsu et al. [51] | Analysis of the importance of materiality for engaging stakeholders through sustainability reports; materiality analysis method: Failure Modes and Effects Analysis (FMEA); Risk Priority Numbers (RPNs); Analytic Network Process (ANP) | A proposal for a model to analyse the materiality of sustainability | |

| Siew [52] | A review of communication tools | ||

| Integration | Maas et al. [12] | Analysis of three factors of sustainability: quantification, management, and communication; perspectives of analysis: inside-out/outside-in | A sustainability integration model in organisations |

| Morioka and de Carvalho [13] | Four-factor analysis: processes and practices, capabilities, offerings, contribution to the development of competitive advantages; based on principles of CS and environmental factors | A sustainable performance integration model in organisations |

© 2017 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

Rodríguez-Olalla, A.; Avilés-Palacios, C. Integrating Sustainability in Organisations: An Activity-Based Sustainability Model. Sustainability 2017, 9, 1072. https://doi.org/10.3390/su9061072

Rodríguez-Olalla A, Avilés-Palacios C. Integrating Sustainability in Organisations: An Activity-Based Sustainability Model. Sustainability. 2017; 9(6):1072. https://doi.org/10.3390/su9061072

Chicago/Turabian StyleRodríguez-Olalla, Ana, and Carmen Avilés-Palacios. 2017. "Integrating Sustainability in Organisations: An Activity-Based Sustainability Model" Sustainability 9, no. 6: 1072. https://doi.org/10.3390/su9061072

APA StyleRodríguez-Olalla, A., & Avilés-Palacios, C. (2017). Integrating Sustainability in Organisations: An Activity-Based Sustainability Model. Sustainability, 9(6), 1072. https://doi.org/10.3390/su9061072