Public Debt, Corruption and Sustainable Economic Growth

Abstract

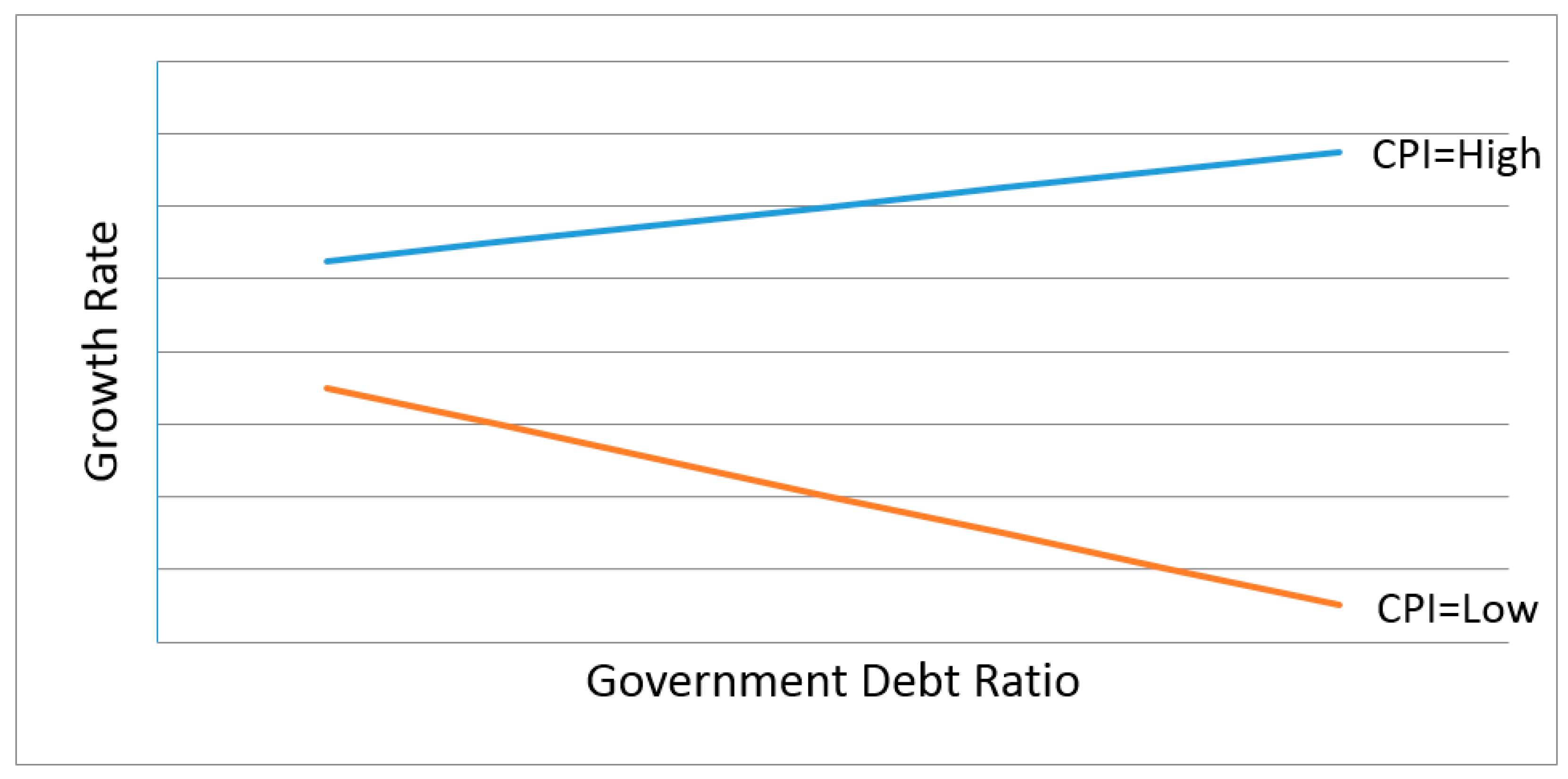

:1. Introduction

2. Background

2.1. Public Debt and Economic Growth

2.2. Public Debt, Institutions and Economic Growth (This Section Has Benefited Largely from the Comments of Two Anonymous Referees)

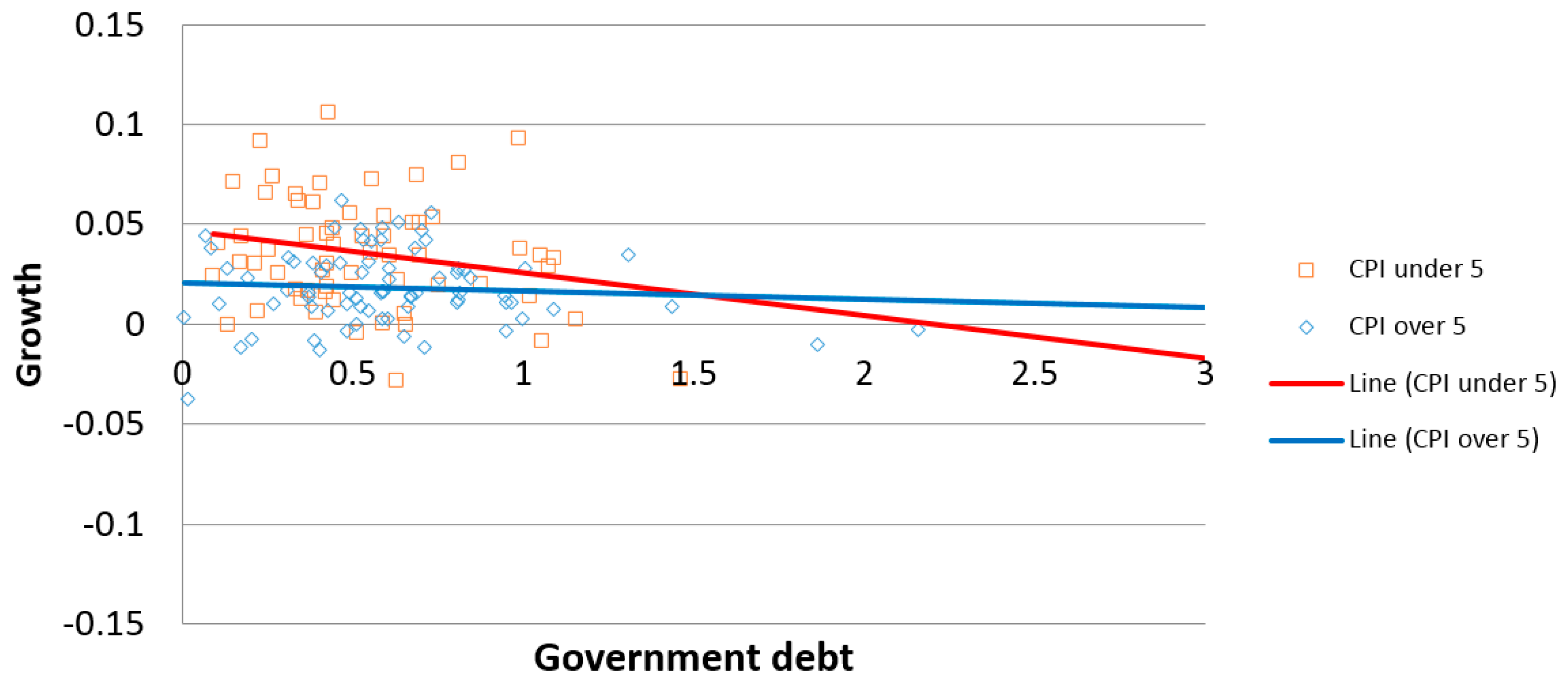

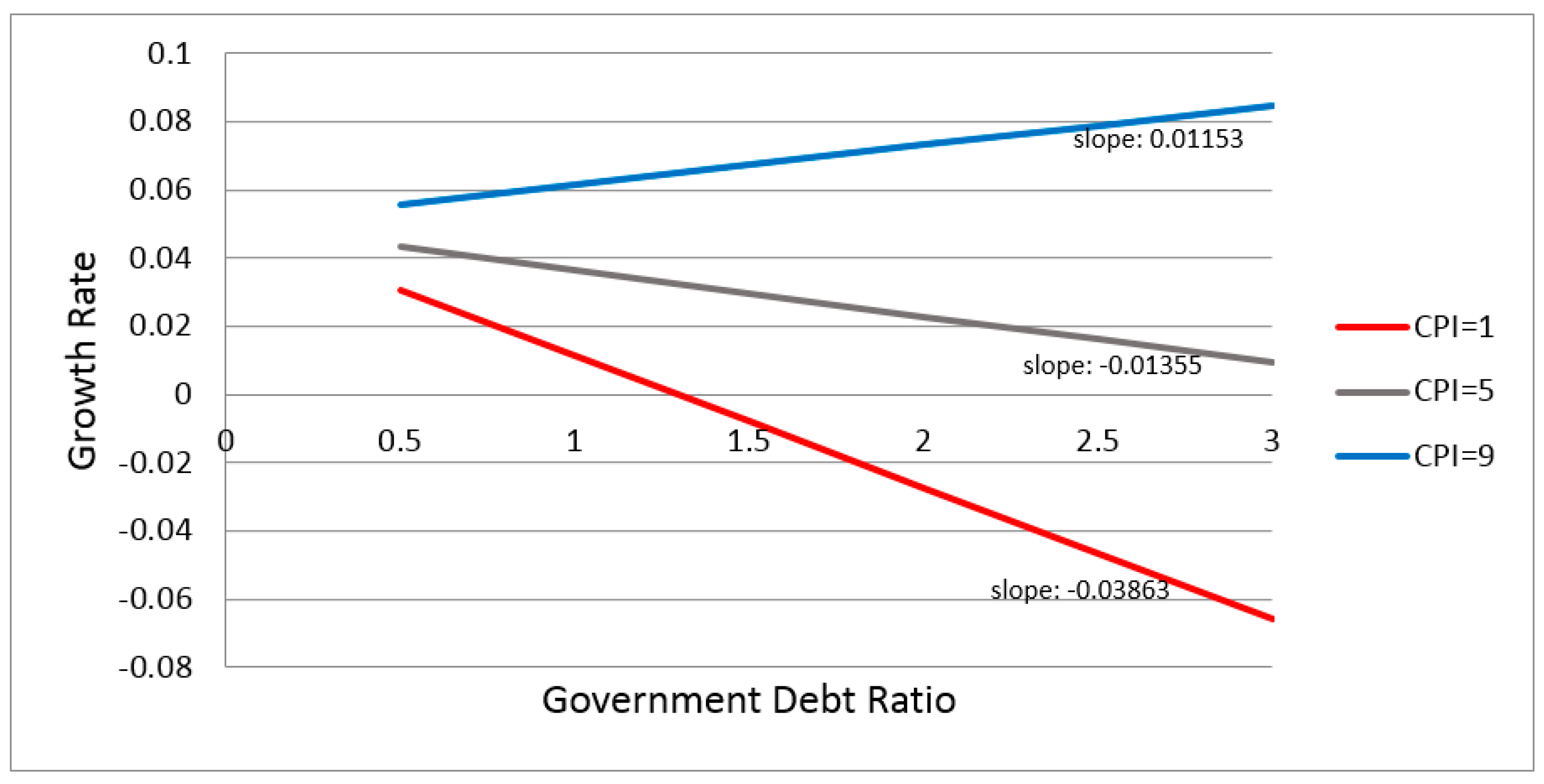

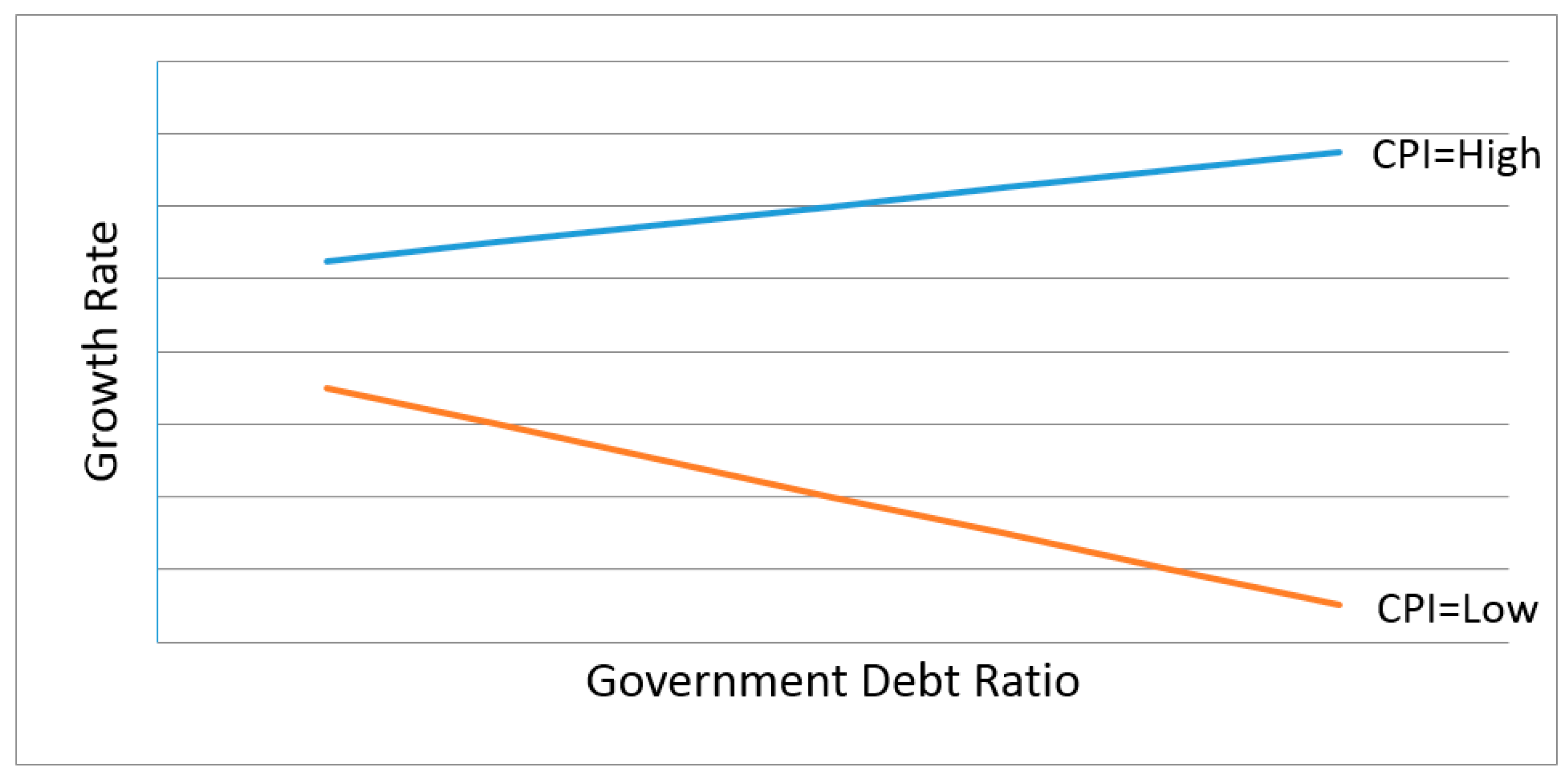

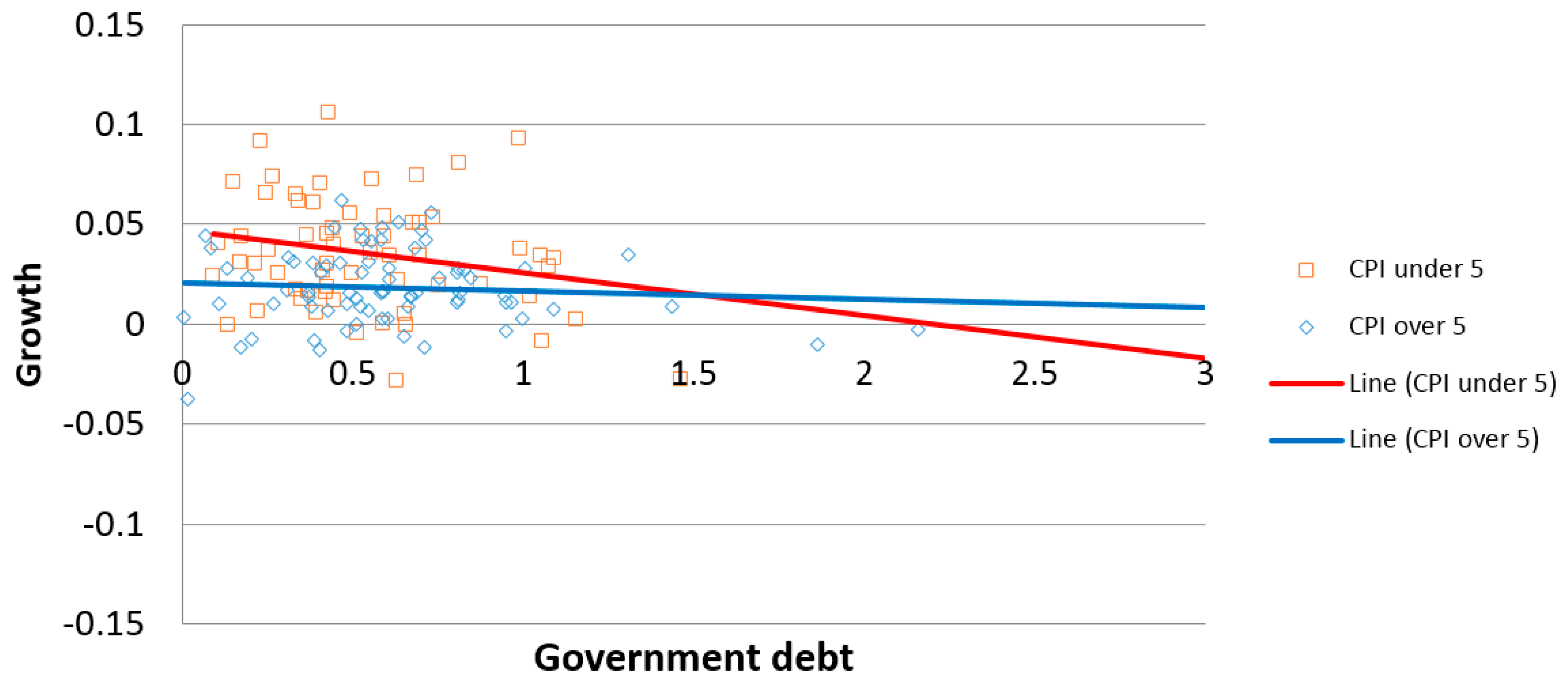

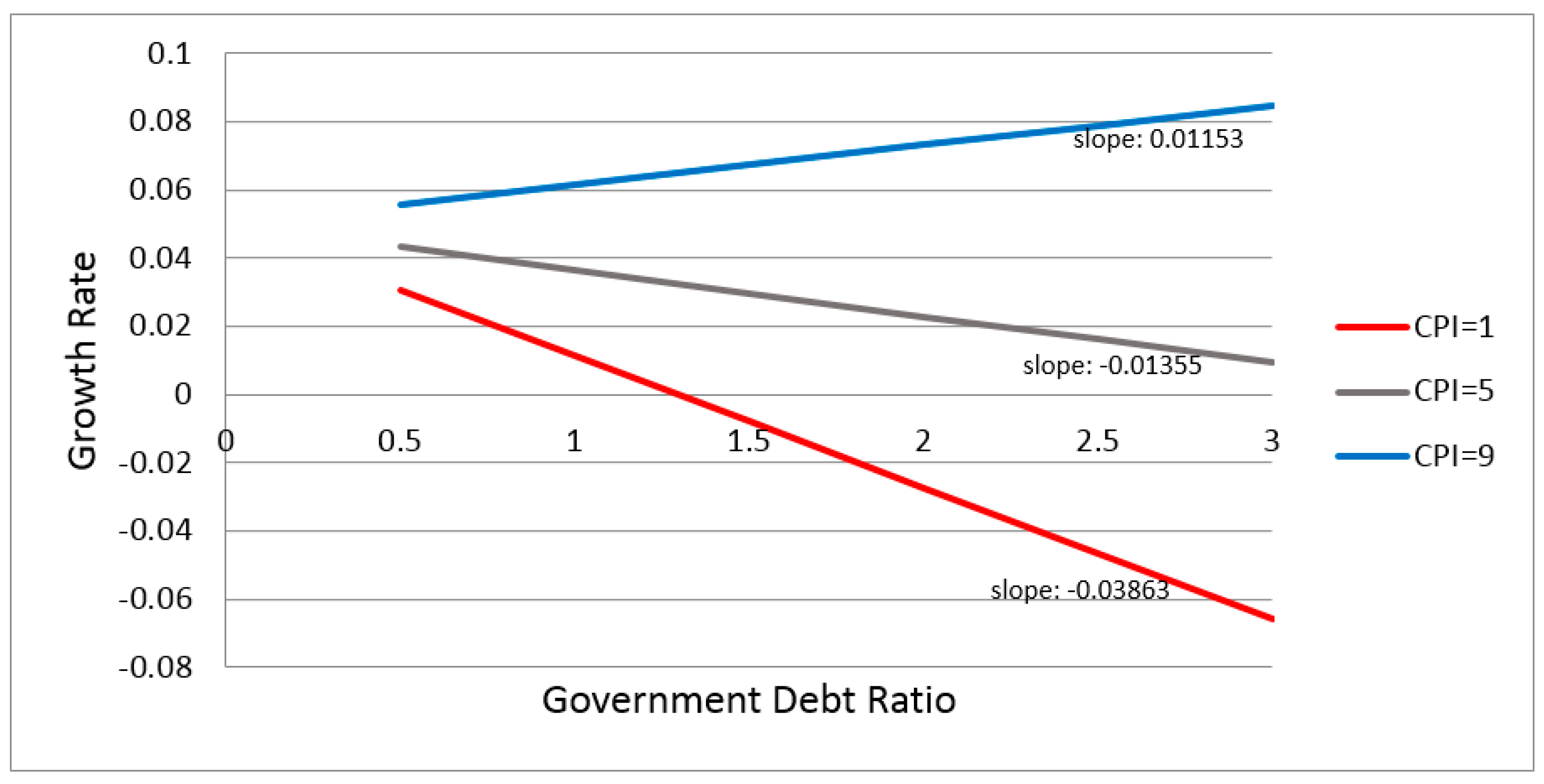

3. Empirical Analysis

3.1. Model Specification and Estimation Methodology

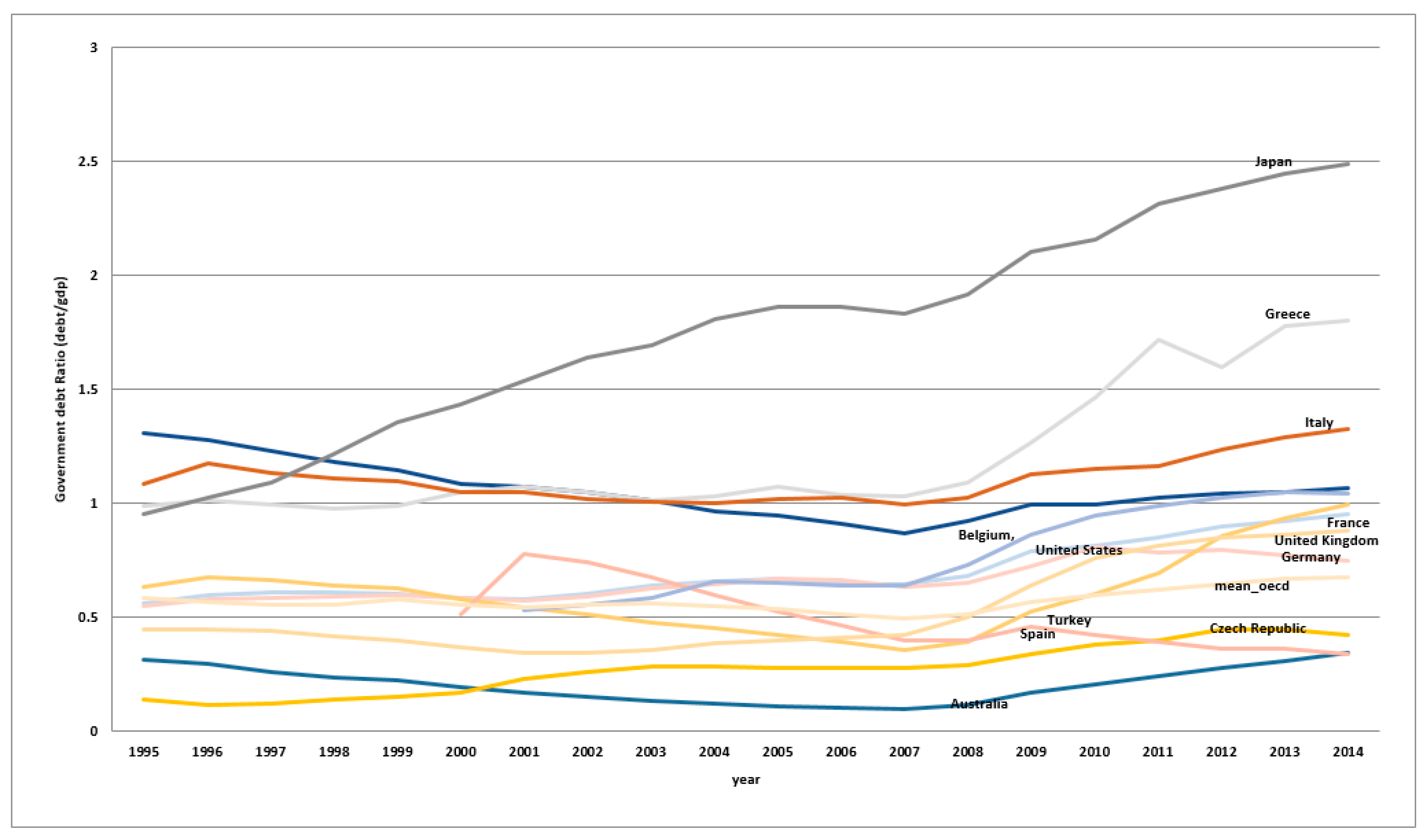

3.2. Data and Basic Findings

4. Robustness Check

5. Conclusions

Author Contributions

Conflicts of Interest

Appendix A

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Growth | Initial GDP | Human Capital | Inflation | Government Size | Trade Openness | Deficit | Debt | CPI | |

|---|---|---|---|---|---|---|---|---|---|

| Growth | 1 | ||||||||

| Initial GDP | −0.220 | 1 | |||||||

| Human Capital | −0.0793 | 0.822 | 1 | ||||||

| Inflation | −0.114 | −0.271 | −0.252 | 1 | |||||

| Government Size | 0.00540 | −0.0317 | 0.166 | 0.149 | 1 | ||||

| Trade Openness | 0.0285 | 0.456 | 0.345 | −0.244 | −0.0599 | 1 | |||

| Deficit | −0.0131 | −0.194 | −0.00340 | 0.0280 | 0.0982 | −0.227 | 1 | ||

| Debt | 0.0518 | −0.210 | −0.176 | 0.111 | 0.115 | −0.0382 | 0.172 | 1 | |

| CPI | −0.124 | 0.769 | 0.672 | −0.336 | −0.0905 | 0.513 | −0.190 | −0.0365 | 1 |

| WGI | −0.297 | 0.768 | 0.667 | −0.333 | −0.0567 | 0.552 | −0.131 | −0.0704 | 0.979 |

| List of 38 Countries | ||

| Australia | Germany | Poland |

| Austria | Greece | Portugal |

| Belgium | Hungary | Republic of Korea |

| Brazil | India | Russian Federation |

| Canada | Indonesia | Slovakia |

| Chile | Italy | South Africa |

| China | Japan | Spain |

| China, Hong Kong SAR | Malaysia | Sweden |

| Colombia | Mexico | Switzerland |

| Czech Republic | Netherlands | Turkey |

| Denmark | Pakistan | United Kingdom |

| Egypt | Peru | United States |

| France | Philippines | |

| List of 46 Countries: 38 + Countries Below | ||

| Finland | Israel | Norway |

| Iceland | Jordan | Singapore |

| Ireland | New Zealand | |

| List of 77 Countries: 46 Countries + Below | ||

| Bulgaria | Kuwait | Senegal |

| Bolivia (Plurinational State of) | Sri Lanka | Slovenia |

| Barbados | Lesotho | Swaziland |

| Costa Rica | Mozambique | Syrian Arab Republic |

| Cyprus | Mauritania | Togo |

| Ecuador | Mauritius | Trinidad and Tobago |

| Gambia | Nicaragua | Tunisia |

| Honduras | Panama | Uganda |

| Croatia | Romania | Uruguay |

| Iran (Islamic Republic of) | Rwanda | |

| Jamaica | Sudan (Former) | |

| Variables | Model (1) | Model (2) | Model (3) | Model (4) | Model (5) | Model (6) |

|---|---|---|---|---|---|---|

| OLS | OLS | Fixed Effect | Fixed Effect | GMM | GMM | |

| Initial GDP | −0.0197 *** | −0.0155 *** | −0.0759 *** | −0.0732 *** | −0.0936 *** | −0.0800 *** |

| (0.00475) | (0.00534) | (0.0140) | (0.0141) | (0.0203) | (0.0200) | |

| Human Capital | 0.00824 | 0.00652 | 0.128 *** | 0.128 *** | 0.152 *** | 0.144 *** |

| (0.00661) | (0.00664) | (0.0285) | (0.0284) | (0.0328) | (0.0317) | |

| Inflation | −0.0511 | −0.0640 | −0.105 | −0.109 | −0.0396 | −0.0655 |

| (0.0607) | (0.0607) | (0.0723) | (0.0722) | (0.0889) | (0.0863) | |

| Government Size | 0.0117 | −0.00328 | −0.454 *** | −0.455 *** | −0.253 * | −0.255 ** |

| (0.0421) | (0.0428) | (0.0947) | (0.0943) | (0.132) | (0.128) | |

| Trade Openness | −0.00401 | −0.00335 | −0.00369 | −0.00375 | 0.00611 | 0.000569 |

| (0.00374) | (0.00374) | (0.0109) | (0.0109) | (0.0136) | (0.0133) | |

| Deficit | 0.0533 | 0.0746 | 0.0343 | −0.00495 | −0.0588 | −0.114 |

| (0.0882) | (0.0885) | (0.120) | (0.123) | (0.138) | (0.139) | |

| Debt | −0.0291 * | −0.0567 ** | −0.0837 *** | −0.112 *** | −0.166 *** | −0.210 *** |

| (0.0158) | (0.0226) | (0.0277) | (0.0350) | (0.0380) | (0.0411) | |

| CPI | - | −0.00387 * | - | −0.00713 | - | −0.0123 ** |

| - | (0.00228) | - | (0.00545) | - | (0.00574) | |

| Debt*CPI | 0.00239 | 0.00650 ** | 0.0102 *** | 0.0149 *** | 0.0185 *** | 0.0268 *** |

| (0.00217) | (0.00324) | (0.00350) | (0.00502) | (0.00545) | (0.00616) | |

| Constant | 0.206 *** | 0.195 *** | 0.492 *** | 0.509 *** | 0.575 *** | 0.543 *** |

| (0.0372) | (0.0374) | (0.0948) | (0.0953) | (0.153) | (0.148) | |

| Observations | 137 | 137 | 137 | 137 | 73 | 73 |

| R-squared | 0.287 | 0.303 | 0.398 | 0.410 |

| Variables | Model (1) | Model (2) | Model (3) | Model (4) | Model (5) | Model (6) |

|---|---|---|---|---|---|---|

| OLS | OLS | Fixed Effect | Fixed Effect | GMM | GMM | |

| Initial GDP | −0.0253 *** | −0.0235 *** | −0.0906 *** | −0.0894 *** | −0.119 *** | −0.111 *** |

| (0.00464) | (0.00513) | (0.0121) | (0.0123) | (0.0202) | (0.0205) | |

| Human Capital | 0.00681 | 0.00593 | 0.0984 *** | 0.0966 *** | 0.140 *** | 0.130 *** |

| (0.00671) | (0.00680) | (0.0237) | (0.0239) | (0.0296) | (0.0298) | |

| Inflation | −0.0166 | −0.0263 | −0.119 | −0.125 * | −0.0311 | −0.0493 |

| (0.0649) | (0.0660) | (0.0722) | (0.0729) | (0.0974) | (0.0964) | |

| Government Size | −0.0233 | −0.0230 | −0.433 *** | −0.431 *** | −0.363 *** | −0.338 *** |

| (0.0411) | (0.0411) | (0.0783) | (0.0786) | (0.127) | (0.126) | |

| Trade Openness | 0.00419 | 0.00412 | 0.0251 *** | 0.0255 *** | 0.0239 * | 0.0219 * |

| (0.00332) | (0.00333) | (0.00876) | (0.00881) | (0.0134) | (0.0132) | |

| Deficit | −0.0358 | −0.0375 | 0.0676 | 0.0551 | 0.106 | 0.0613 |

| (0.0626) | (0.0627) | (0.0918) | (0.0940) | (0.126) | (0.130) | |

| Debt | −0.0324 ** | −0.0451 ** | −0.0996 *** | −0.114 *** | −0.187 *** | −0.224 *** |

| (0.0158) | (0.0220) | (0.0287) | (0.0366) | (0.0432) | (0.0477) | |

| CPI | - | −0.00175 | - | −0.00341 | - | −0.00989 |

| - | (0.00210) | - | (0.00519) | - | (0.00612) | |

| Debt*CPI | 0.00419 * | 0.00609 * | 0.0116 *** | 0.0139 *** | 0.0220 *** | 0.0280 *** |

| (0.00222) | (0.00319) | (0.00368) | (0.00510) | (0.00602) | (0.00690) | |

| Constant | 0.262 *** | 0.259 *** | 0.704 *** | 0.720 *** | 0.864 *** | 0.872 *** |

| (0.0367) | (0.0370) | (0.0808) | (0.0842) | (0.152) | (0.151) | |

| Observations | 168 | 168 | 168 | 168 | 89 | 89 |

| R-squared | 0.260 | 0.263 | 0.501 | 0.503 |

| Variables | Model (1) | Model (2) | Model (3) | Model (4) | Model (5) | Model (6) |

|---|---|---|---|---|---|---|

| OLS | OLS | Fixed Effect | Fixed Effect | GMM | GMM | |

| Initial GDP | −0.0207 *** | −0.0202 *** | −0.0968 *** | −0.0978 *** | −0.128 *** | −0.130 *** |

| (0.00382) | (0.00390) | (0.0113) | (0.0113) | (0.0174) | (0.0172) | |

| Human Capital | 0.0220 *** | 0.0224 *** | 0.0849 *** | 0.0882 *** | 0.107 *** | 0.111 *** |

| (0.00583) | (0.00585) | (0.0222) | (0.0222) | (0.0285) | (0.0284) | |

| Inflation | 0.0223 | 0.0144 | −0.128 ** | −0.0999 | −0.0879 | −0.0504 |

| (0.0547) | (0.0558) | (0.0606) | (0.0629) | (0.0763) | (0.0798) | |

| Government Size | −0.00844 | −0.0113 | −0.379 *** | −0.364 *** | −0.321 *** | −0.308 *** |

| (0.0373) | (0.0375) | (0.0722) | (0.0725) | (0.100) | (0.100) | |

| Trade Openness | 0.00226 | 0.00265 | 0.0264 *** | 0.0253 *** | 0.0341 ** | 0.0337 ** |

| (0.00364) | (0.00368) | (0.00964) | (0.00963) | (0.0148) | (0.0147) | |

| Deficit | −0.0835 * | −0.0822 * | 0.0313 | 0.0463 | 0.0425 | 0.0541 |

| (0.0461) | (0.0462) | (0.0862) | (0.0863) | (0.111) | (0.111) | |

| Debt | −0.00626 | −0.0135 | −0.0494 ** | −0.0321 | −0.0672 ** | −0.0514 * |

| (0.0129) | (0.0162) | (0.0209) | (0.0235) | (0.0285) | (0.0303) | |

| CPI | - | −0.00138 | - | 0.00706 | - | 0.00793 |

| - | (0.00186) | - | (0.00445) | - | (0.00517) | |

| Debt*CPI | 0.000463 | 0.00179 | 0.00599 * | 0.00243 | 0.00686 | 0.00337 |

| (0.00206) | (0.00273) | (0.00341) | (0.00407) | (0.00522) | (0.00569) | |

| Constant | 0.167 *** | 0.169 *** | 0.777 *** | 0.737 *** | 1.005 *** | 0.967 *** |

| (0.0284) | (0.0286) | (0.0781) | (0.0817) | (0.125) | (0.128) | |

| Observations | 257 | 257 | 257 | 257 | 143 | 143 |

| R-squared | 0.143 | 0.145 | 0.406 | 0.415 |

| Variables | Model (1) | Model (2) | Model (3) | Model (4) |

|---|---|---|---|---|

| OLS | OLS | Fixed Effect | Fixed Effect | |

| Initial GDP | 0.717 *** | 0.740 *** | 0.598 *** | 0.613 *** |

| (0.0507) | (0.0566) | (0.166) | (0.172) | |

| Human Capital | 0.0330 | 0.0243 | 0.774 *** | 0.808 ** |

| (0.0702) | (0.0709) | (0.268) | (0.280) | |

| Inflation | 0.738 | 0.556 | 0.923 | 0.386 |

| (1.104) | (1.124) | (1.185) | (1.568) | |

| Government Size | −0.00974 | −0.101 | −3.292 ** | −3.212 ** |

| (0.455) | (0.467) | (1.416) | (1.452) | |

| Trade Openness | −0.0397 | −0.0378 | −0.109 | −0.142 |

| (0.0381) | (0.0382) | (0.136) | (0.151) | |

| Deficit | 0.0125 | 0.282 | −3.129 | −3.305 * |

| (1.088) | (1.130) | (1.824) | (1.890) | |

| Debt | −0.420 ** | −0.597 ** | −1.077 ** | −1.334 * |

| (0.178) | (0.265) | (0.421) | (0.643) | |

| CPI | - | −0.0226 | - | −0.0331 |

| - | (0.0251) | - | (0.0616) | |

| Debt*CPI | 0.0485 ** | 0.0730 ** | 0.136 ** | 0.170 ** |

| (0.0236) | (0.0361) | (0.0475) | (0.0794) | |

| Constant | 1.920 *** | 1.890 *** | 1.665 | 1.683 |

| (0.393) | (0.395) | (1.205) | (1.230) | |

| Observations | 64 | 64 | 64 | 64 |

| R-squared | 0.953 | 0.954 | 0.916 | 0.918 |

| Variables | Model (1) | Model (2) | Model (3) | Model (4) |

|---|---|---|---|---|

| OLS | OLS | Fixed Effect | Fixed Effect | |

| Initial GDP | 0.675 *** | 0.683 *** | 0.204 | 0.222 |

| (0.0464) | (0.0503) | (0.150) | (0.150) | |

| Human Capital | 0.0310 | 0.0261 | 0.840 ** | 0.775 ** |

| (0.0698) | (0.0710) | (0.307) | (0.310) | |

| Inflation | 1.169 | 1.052 | 1.505 | 2.874 |

| (1.084) | (1.120) | (1.338) | (1.773) | |

| Government Size | −0.306 | −0.297 | −3.151 ** | −3.345 ** |

| (0.427) | (0.430) | (1.203) | (1.206) | |

| Trade Openness | 0.0265 | 0.0255 | 0.200 | 0.237 * |

| (0.0330) | (0.0332) | (0.118) | (0.121) | |

| Deficit | −0.982 | −0.985 | −0.648 | −0.387 |

| (0.683) | (0.687) | (1.258) | (1.269) | |

| Debt | −0.376 ** | −0.455 * | −1.093 ** | −0.457 |

| (0.170) | (0.242) | (0.496) | (0.735) | |

| CPI | - | −0.0102 | - | 0.0810 |

| - | (0.0223) | - | (0.0695) | |

| Debt*CPI | 0.0555 ** | 0.0671 * | 0.129 ** | 0.0450 |

| (0.0236) | (0.0346) | (0.0571) | (0.0917) | |

| Constant | 2.309 *** | 2.310 *** | 5.007 *** | 4.396 *** |

| (0.365) | (0.367) | (0.959) | (1.086) | |

| Observations | 79 | 79 | 79 | 79 |

| R-squared | 0.943 | 0.943 | 0.832 | 0.841 |

| Variables | Model (1) | Model (2) | Model (3) | Model (4) |

|---|---|---|---|---|

| OLS | OLS | Fixed Effect | Fixed Effect | |

| Initial GDP | 0.673 *** | 0.673 *** | 0.105 | 0.119 |

| (0.0384) | (0.0389) | (0.128) | (0.140) | |

| Human Capital | 0.242 *** | 0.243 *** | 0.857 *** | 0.844 *** |

| (0.0603) | (0.0614) | (0.279) | (0.287) | |

| Inflation | −0.0299 | −0.0350 | −0.134 | −0.0401 |

| (0.710) | (0.715) | (1.153) | (1.219) | |

| Government Size | −0.236 | −0.240 | −4.134 *** | −4.011 *** |

| (0.403) | (0.407) | (0.855) | (0.977) | |

| Trade Openness | 0.0337 | 0.0342 | 0.173 | 0.170 |

| (0.0380) | (0.0384) | (0.114) | (0.116) | |

| Deficit | −1.143 ** | −1.144 ** | 1.376 | 1.369 |

| (0.502) | (0.505) | (0.965) | (0.978) | |

| Debt | 0.0238 | 0.0128 | −0.715 ** | −0.688 ** |

| (0.143) | (0.176) | (0.269) | (0.290) | |

| CPI | - | −0.00213 | - | 0.0133 |

| - | (0.0198) | - | (0.0493) | |

| Debt*CPI | −2.01 × 10−5 | 0.00205 | 0.0767 * | 0.0700 |

| (0.0231) | (0.0302) | (0.0418) | (0.0491) | |

| Constant | 1.669 *** | 1.673 *** | 6.066 *** | 5.880 *** |

| (0.289) | (0.293) | (0.782) | (1.050) | |

| Observations | 121 | 121 | 121 | 121 |

| R-squared | 0.946 | 0.946 | 0.776 | 0.776 |

| Variables | Model (1) | Model (1) | Model (2) | Model (2) | Model (3) | Model (3) | Model (4) | Model (4) | Model (5) | Model (5) | Model (6) | Model (6) |

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| OLS CPI | OLS WGI | OLS CPI | OLS WGI | Fixed Effect CPI | Fixed Effect WGI | Fixed Effect CPI | Fixed Effect WGI | GMM CPI | GMM WGI | GMM CPI | GMM WGI | |

| Initial GDP | −0.0207 *** | −0.0214 *** | −0.0201 *** | −0.0206 *** | −0.0997 *** | −0.0967 *** | −0.101 *** | −0.0960 *** | −0.136 *** | −0.130 *** | −0.137 *** | −0.130 *** |

| (0.00388) | (0.00399) | (0.00392) | (0.00402) | (0.0117) | (0.0136) | (0.0116) | (0.0137) | (0.0157) | (0.0157) | (0.0157) | (0.0158) | |

| Human Capital | 0.0202 *** | 0.0260 *** | 0.0211 *** | 0.0271 *** | 0.0832 *** | 0.0706 *** | 0.0860 *** | 0.0733 *** | 0.0932 *** | 0.0864 *** | 0.0948 *** | 0.0841 *** |

| (0.00578) | (0.00594) | (0.00583) | (0.00597) | (0.0220) | (0.0265) | (0.0219) | (0.0269) | (0.0272) | (0.0276) | (0.0273) | (0.0280) | |

| Inflation | 0.00180 | 0.00544 | −0.00408 | −0.00108 | −0.127 *** | −0.127 ** | −0.110 ** | −0.121 ** | −0.0512 | −0.258 *** | −0.0398 | −0.264 *** |

| (0.0413) | (0.0456) | (0.0416) | (0.0457) | (0.0420) | (0.0500) | (0.0431) | (0.0507) | (0.0538) | (0.0767) | (0.0555) | (0.0778) | |

| Government Size | −0.00742 | 0.00607 | −0.0131 | −0.00129 | −0.357 *** | −0.286 *** | −0.344 *** | −0.276 *** | −0.267 *** | 0.0667 *** | −0.264 *** | 0.0659 *** |

| (0.0361) | (0.0382) | (0.0364) | (0.0385) | (0.0614) | (0.0752) | (0.0616) | (0.0768) | (0.0766) | (0.0140) | (0.0768) | (0.0140) | |

| Trade Openness | 0.00629 * | −0.000542 | 0.00690 * | 0.000645 | 0.0261 *** | 0.0484 *** | 0.0250 *** | 0.0490 *** | 0.0644 *** | 0.0709 | 0.0643 *** | 0.0621 |

| (0.00355) | (0.00432) | (0.00359) | (0.00439) | (0.00712) | (0.0132) | (0.00712) | (0.0132) | (0.0139) | (0.0659) | (0.0139) | (0.0672) | |

| Deficit | −0.0537 | −0.0839 ** | −0.0546 | −0.0892 ** | 0.0264 | −0.0181 | 0.0377 | −0.00893 | 0.0567 | −0.0103 | 0.0645 | −0.00961 |

| (0.0361) | (0.0362) | (0.0360) | (0.0363) | (0.0485) | (0.0599) | (0.0488) | (0.0614) | (0.0653) | (0.0118) | (0.0658) | (0.0119) | |

| Debt | −0.00314 | 0.000193 | −0.0135 | −0.00130 | −0.0300 * | −0.000151 | −0.0149 | −0.000905 | −0.0542 ** | −0.0703 | −0.0443 * | −0.0740 |

| (0.0124) | (0.00670) | (0.0155) | (0.00677) | (0.0179) | (0.0114) | (0.0201) | (0.0115) | (0.0229) | (0.0528) | (0.0251) | (0.0534) | |

| CPI or WGI | - | - | −0.00209 | −0.00572 | - | - | 0.00712 | 0.00753 | - | - | 0.00449 | −0.00575 |

| - | - | (0.00189) | (0.00401) | - | - | (0.00439) | (0.0109) | - | - | (0.00505) | (0.0113) | |

| Debt*CPI or WGI | 0.000558 | −0.00434 | 0.00259 | 0.000911 | 0.00678 ** | 0.0125 | 0.00322 | 0.00892 | 0.0101 ** | 0.0150 | 0.00783 | 0.0176 |

| (0.00206) | (0.00461) | (0.00276) | (0.00589) | (0.00317) | (0.00927) | (0.00384) | (0.0106) | (0.00474) | (0.00964) | (0.00541) | (0.0110) | |

| Constant | 0.167 *** | 0.160 *** | 0.171 *** | 0.153 *** | 0.796 *** | 0.772 *** | 0.759 *** | 0.753 *** | 1.067 *** | 1.028 *** | 1.044 *** | 1.036 *** |

| (0.0297) | (0.0308) | (0.0299) | (0.0311) | (0.0823) | (0.106) | (0.0850) | (0.109) | (0.118) | (0.117) | (0.122) | (0.121) | |

| Observations | 258 | 224 | 258 | 224 | 258 | 224 | 258 | 224 | 144 | 147 | 144 | 147 |

| R-squared | 0.133 | 0.208 | 0.137 | 0.216 | 0.468 | 0.413 | 0.476 | 0.415 |

| Variables | Model (1) | Model (1) | Model (2) | Model (2) | Model (3) | Model (3) | Model (4) | Model (4) | Model (5) | Model (5) | Model (6) | Model (6) |

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| OLS CPI | OLS WGI | OLS CPI | OLS WGI | Fixed Effect CPI | Fixed Effect WGI | Fixed Effect CPI | Fixed Effect WGI | GMM CPI | GMM WGI | GMM CPI | GMM WGI | |

| Initial GDP | −0.0214 *** | −0.0281 *** | −0.0188 *** | −0.0237 *** | −0.0740 *** | −0.0755 *** | −0.0734 *** | −0.0755 *** | −0.0993 *** | −0.0931 *** | −0.0921 *** | −0.0872 *** |

| (0.00478) | (0.00463) | (0.00523) | (0.00514) | (0.0146) | (0.0156) | (0.0148) | (0.0157) | (0.0220) | (0.0210) | (0.0222) | (0.0211) | |

| Human Capital | 0.0107 | 0.0128 ** | 0.00995 | 0.0117 * | 0.0994 *** | 0.123 *** | 0.0990 *** | 0.122 *** | 0.135 *** | 0.145 *** | 0.132 *** | 0.137 *** |

| (0.00649) | (0.00614) | (0.00650) | (0.00609) | (0.0271) | (0.0295) | (0.0272) | (0.0306) | (0.0331) | (0.0318) | (0.0329) | (0.0329) | |

| Inflation | −0.0438 | 0.0478 | −0.0470 | 0.0306 | −0.115 ** | −0.230 ** | −0.117 ** | −0.232 ** | −0.0811 | −0.205 ** | −0.101 * | −0.232 ** |

| (0.0413) | (0.0399) | (0.0413) | (0.0405) | (0.0448) | (0.0983) | (0.0455) | (0.101) | (0.0566) | (0.103) | (0.0575) | (0.105) | |

| Government Size | −0.00341 | −0.00290 | −0.0142 | −0.00198 | −0.393 *** | 0.0108 | −0.393 *** | 0.0107 | −0.248 ** | 0.0106 | −0.249 ** | 0.00516 |

| (0.0417) | (0.00375) | (0.0425) | (0.00373) | (0.0819) | (0.0118) | (0.0823) | (0.0120) | (0.107) | (0.0145) | (0.106) | (0.0147) | |

| Trade Openness | −0.00270 | −0.0630 | −0.00215 | −0.0611 | 0.00209 | −0.0419 | 0.00219 | −0.0425 | 0.0120 | −0.0602 | 0.00814 | −0.0706 |

| (0.00401) | (0.0613) | (0.00403) | (0.0605) | (0.0116) | (0.0796) | (0.0116) | (0.0805) | (0.0151) | (0.0888) | (0.0150) | (0.0891) | |

| Deficit | 0.0841 | −0.0113 | 0.0892 | −0.0195 ** | 0.139 ** | −0.0367 ** | 0.137 ** | −0.0369 ** | −0.0271 | −0.0415 ** | −0.0354 | −0.0446 ** |

| (0.0612) | (0.00806) | (0.0612) | (0.00907) | (0.0643) | (0.0174) | (0.0649) | (0.0176) | (0.0924) | (0.0198) | (0.0926) | (0.0201) | |

| Debt | −0.0226 | −0.0393 | −0.0415 * | −0.0462 | −0.0449 * | −0.0970 * | −0.0501 | −0.0975 * | −0.0786 * | −0.0750 | −0.105 ** | −0.0869 |

| (0.0148) | (0.0417) | (0.0213) | (0.0413) | (0.0269) | (0.0495) | (0.0326) | (0.0502) | (0.0403) | (0.0543) | (0.0432) | (0.0547) | |

| CPI or WGI | - | - | −0.00282 | −0.00846 * | - | - | −0.00150 | −0.00138 | - | - | −0.00805 | −0.0160 |

| - | - | (0.00228) | (0.00449) | - | - | (0.00531) | (0.0138) | - | - | (0.00621) | (0.0154) | |

| Debt*CPI or WGI | 0.00168 | 0.00311 | 0.00464 | 0.0112 * | 0.00627 * | 0.0261 *** | 0.00719 | 0.0268 ** | 0.00957 * | 0.0305 *** | 0.0148 ** | 0.0391 *** |

| (0.00212) | (0.00469) | (0.00319) | (0.00631) | (0.00341) | (0.00856) | (0.00473) | (0.0110) | (0.00573) | (0.00927) | (0.00658) | (0.0122) | |

| Constant | 0.214 *** | 0.267 *** | 0.209 *** | 0.237 *** | 0.534 *** | 0.458 *** | 0.539 *** | 0.461 *** | 0.660 *** | 0.562 *** | 0.647 *** | 0.549 *** |

| (0.0375) | (0.0372) | (0.0377) | (0.0401) | (0.101) | (0.115) | (0.103) | (0.120) | (0.173) | (0.164) | (0.171) | (0.163) | |

| Observations | 137 | 111 | 137 | 111 | 137 | 111 | 137 | 111 | 73 | 73 | 73 | 73 |

| R-squared | 0.281 | 0.483 | 0.289 | 0.501 | 0.384 | 0.398 | 0.384 | 0.398 | ||||

| Number of code | 38 | 38 | 38 | 38 |

| Variables | Model (1) | Model (1) | Model (2) | Model (2) | Model (3) | Model (3) | Model (4) | Model (4) | Model (5) | Model (5) | Model (6) | Model (6) |

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| OLS CPI | OLS WGI | OLS CPI | OLS WGI | Fixed Effect CPI | Fixed Effect WGI | Fixed Effect CPI | Fixed Effect WGI | GMM CPI | GMM WGI | GMM CPI | GMM WGI | |

| Initial GDP | −0.0197 *** | −0.0274 *** | −0.0155 *** | −0.0214 *** | −0.0759 *** | −0.0714 *** | −0.0732 *** | −0.0708 *** | −0.0936 *** | −0.0865 *** | −0.0800 *** | −0.0749 *** |

| (0.00475) | (0.00453) | (0.00534) | (0.00519) | (0.0140) | (0.0145) | (0.0141) | (0.0145) | (0.0203) | (0.0191) | (0.0200) | (0.0191) | |

| Human Capital | 0.00824 | 0.0112 * | 0.00652 | 0.00917 | 0.128 *** | 0.138 *** | 0.128 *** | 0.131 *** | 0.152 *** | 0.173 *** | 0.144 *** | 0.154 *** |

| (0.00661) | (0.00626) | (0.00664) | (0.00620) | (0.0285) | (0.0303) | (0.0284) | (0.0313) | (0.0328) | (0.0317) | (0.0317) | (0.0326) | |

| Inflation | −0.0511 | 0.0541 | −0.0640 | 0.0331 | −0.105 | −0.127 | −0.109 | −0.146 | −0.0396 | −0.183 | −0.0655 | −0.229 * |

| (0.0607) | (0.0401) | (0.0607) | (0.0404) | (0.0723) | (0.118) | (0.0722) | (0.120) | (0.0889) | (0.125) | (0.0863) | (0.124) | |

| Government Size | 0.0117 | −0.00356 | −0.00328 | −0.00251 | −0.454 *** | 0.0107 | −0.455 *** | 0.00947 | −0.253 * | 0.00441 | −0.255 ** | −0.00344 |

| (0.0421) | (0.00342) | (0.0428) | (0.00339) | (0.0947) | (0.0111) | (0.0943) | (0.0112) | (0.132) | (0.0129) | (0.128) | (0.0131) | |

| Trade Openness | −0.00401 | −0.0414 | −0.00335 | −0.0132 | −0.00369 | −0.190 | −0.00375 | −0.210 * | 0.00611 | −0.172 | 0.000569 | −0.222 * |

| (0.00374) | (0.0829) | (0.00374) | (0.0822) | (0.0109) | (0.120) | (0.0109) | (0.122) | (0.0136) | (0.131) | (0.0133) | (0.131) | |

| Deficit | 0.0533 | −0.0176 ** | 0.0746 | −0.0292 *** | 0.0343 | −0.0685 *** | −0.00495 | −0.0720 *** | −0.0588 | −0.0810 *** | −0.114 | −0.0867 *** |

| (0.0882) | (0.00829) | (0.0885) | (0.00959) | (0.120) | (0.0156) | (0.123) | (0.0160) | (0.138) | (0.0170) | (0.139) | (0.0174) | |

| Debt | −0.0291 * | −0.0281 | −0.0567 ** | −0.0484 | −0.0837 *** | −0.0181 | −0.112 *** | −0.0195 | −0.166 *** | −0.0284 | −0.210 *** | −0.0480 |

| (0.0158) | (0.0584) | (0.0226) | (0.0579) | (0.0277) | (0.0782) | (0.0350) | (0.0783) | (0.0380) | (0.0841) | (0.0411) | (0.0825) | |

| CPI or WGI | - | - | −0.00387 * | −0.0100 ** | - | - | −0.00713 | −0.0129 | - | - | −0.0123 ** | −0.0245 * |

| - | - | (0.00228) | (0.00442) | - | - | (0.00545) | (0.0134) | - | - | (0.00574) | (0.0144) | |

| Debt*CPI or WGI | 0.00239 | 0.00542 | 0.00650 ** | 0.0149 ** | 0.0102 *** | 0.0342 *** | 0.0149 *** | 0.0404 *** | 0.0185 *** | 0.0415 *** | 0.0268 *** | 0.0538 *** |

| (0.00217) | (0.00449) | (0.00324) | (0.00606) | (0.00350) | (0.00790) | (0.00502) | (0.0102) | (0.00545) | (0.00819) | (0.00616) | (0.0107) | |

| Constant | 0.206 *** | 0.266 *** | 0.195 *** | 0.224 *** | 0.492 *** | 0.367 *** | 0.509 *** | 0.394 *** | 0.575 *** | 0.433 *** | 0.543 *** | 0.407 *** |

| (0.0372) | (0.0361) | (0.0374) | (0.0398) | (0.0948) | (0.102) | (0.0953) | (0.106) | (0.153) | (0.142) | (0.148) | (0.138) | |

| Observations | 137 | 111 | 137 | 111 | 137 | 111 | 137 | 111 | 73 | 73 | 73 | 73 |

| R-squared | 0.287 | 0.495 | 0.303 | 0.520 | 0.398 | 0.468 | 0.410 | 0.475 |

| Variables | Model (1) | Model (1) | Model (2) | Model (2) | Model (3) | Model (3) | Model (4) | Model (4) | Model (5) | Model (5) | Model (6) | Model (6) |

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| OLS CPI | OLS WGI | OLS CPI | OLS WGI | Fixed Effect CPI | Fixed Effect WGI | Fixed Effect CPI | Fixed Effect WGI | GMM CPI | GMM WGI | GMM CPI | GMM WGI | |

| Initial GDP | −0.0253 *** | −0.0301 *** | −0.0235 *** | −0.0258 *** | −0.0906 *** | −0.0723 *** | −0.0894 *** | −0.0710 *** | −0.119 *** | −0.111 *** | −0.111 *** | −0.0997 *** |

| (0.00464) | (0.00435) | (0.00513) | (0.00490) | (0.0121) | (0.0141) | (0.0123) | (0.0139) | (0.0202) | (0.0201) | (0.0205) | (0.0202) | |

| Human Capital | 0.00681 | 0.0115 * | 0.00593 | 0.0100 | 0.0984 *** | 0.108 *** | 0.0966 *** | 0.0949 *** | 0.140 *** | 0.145 *** | 0.130 *** | 0.121 *** |

| (0.00671) | (0.00616) | (0.00680) | (0.00615) | (0.0237) | (0.0253) | (0.0239) | (0.0261) | (0.0296) | (0.0300) | (0.0298) | (0.0318) | |

| Inflation | −0.0166 | 0.0298 | −0.0263 | 0.0254 | −0.119 | −0.145 | −0.125 * | −0.175 | −0.0311 | −0.279 ** | −0.0493 | −0.305 ** |

| (0.0649) | (0.0396) | (0.0660) | (0.0393) | (0.0722) | (0.113) | (0.0729) | (0.112) | (0.0974) | (0.129) | (0.0964) | (0.126) | |

| Government Size | −0.0233 | 0.000303 | −0.0230 | 0.000380 | −0.433 *** | 0.0232 * | −0.431 *** | 0.0203 * | −0.363 *** | 0.0260 * | −0.338 *** | 0.0179 |

| (0.0411) | (0.00314) | (0.0411) | (0.00311) | (0.0783) | (0.0117) | (0.0786) | (0.0117) | (0.127) | (0.0135) | (0.126) | (0.0135) | |

| Trade Openness | 0.00419 | −0.0511 | 0.00412 | −0.0485 | 0.0251 *** | −0.0940 | 0.0255 *** | −0.125 | 0.0239 * | 0.0144 | 0.0219 * | −0.0323 |

| (0.00332) | (0.0571) | (0.00333) | (0.0565) | (0.00876) | (0.107) | (0.00881) | (0.107) | (0.0134) | (0.129) | (0.0132) | (0.129) | |

| Deficit | −0.0358 | −0.0140 * | −0.0375 | −0.0229 ** | 0.0676 | −0.0708 *** | 0.0551 | −0.0796 *** | 0.106 | −0.0796 *** | 0.0613 | −0.0929 *** |

| (0.0626) | (0.00773) | (0.0627) | (0.00900) | (0.0918) | (0.0166) | (0.0940) | (0.0171) | (0.126) | (0.0197) | (0.130) | (0.0205) | |

| Debt | −0.0324 ** | 0.000733 | −0.0451 ** | −0.0178 | −0.0996 *** | −0.0336 | −0.114 *** | −0.0390 | −0.187 *** | −0.0375 | −0.224 *** | −0.0636 |

| (0.0158) | (0.0609) | (0.0220) | (0.0611) | (0.0287) | (0.0832) | (0.0366) | (0.0821) | (0.0432) | (0.0973) | (0.0477) | (0.0948) | |

| CPI or WGI | - | - | −0.00175 | −0.00750 * | - | - | −0.00341 | −0.0242 * | - | - | −0.00989 | −0.0311 * |

| - | - | (0.00210) | (0.00402) | - | - | (0.00519) | (0.0134) | - | - | (0.00612) | (0.0159) | |

| Debt*CPI or WGI | 0.00419 * | 0.00636 | 0.00609 * | 0.0136 ** | 0.0116 *** | 0.0332 *** | 0.0139 *** | 0.0443 *** | 0.0220 *** | 0.0387 *** | 0.0280 *** | 0.0523 *** |

| (0.00222) | (0.00443) | (0.00319) | (0.00585) | (0.00368) | (0.00868) | (0.00510) | (0.0106) | (0.00602) | (0.00979) | (0.00690) | (0.0121) | |

| Constant | 0.262 *** | 0.290 *** | 0.259 *** | 0.260 *** | 0.704 *** | 0.453 *** | 0.720 *** | 0.509 *** | 0.864 *** | 0.744 *** | 0.872 *** | 0.749 *** |

| (0.0367) | (0.0352) | (0.0370) | (0.0383) | (0.0808) | (0.110) | (0.0842) | (0.113) | (0.152) | (0.151) | (0.151) | (0.147) | |

| Observations | 168 | 135 | 168 | 135 | 168 | 135 | 168 | 135 | 89 | 89 | 89 | 89 |

| R-squared | 0.260 | 0.456 | 0.263 | 0.471 | 0.501 | 0.399 | 0.503 | 0.422 |

| Variables | Model (1) | Model (1) | Model (2) | Model (2) | Model (3) | Model (3) | Model (4) | Model (4) | Model (5) | Model (5) | Model (6) | Model (6) |

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| OLS CPI | OLS WGI | OLS CPI | OLS WGI | Fixed Effect CPI | Fixed Effect WGI | Fixed Effect CPI | Fixed Effect WGI | GMM CPI | GMM WGI | GMM CPI | GMM WGI | |

| Initial GDP | −0.0207 *** | −0.0215 *** | −0.0202 *** | −0.0204 *** | −0.0968 *** | −0.0900 *** | −0.0978 *** | −0.0894 *** | −0.128 *** | −0.125 *** | −0.130 *** | −0.125 *** |

| (0.00382) | (0.00384) | (0.00390) | (0.00390) | (0.0113) | (0.0135) | (0.0113) | (0.0136) | (0.0174) | (0.0173) | (0.0172) | (0.0173) | |

| Human Capital | 0.0220 *** | 0.0278 *** | 0.0224 *** | 0.0283 *** | 0.0849 *** | 0.0760 *** | 0.0882 *** | 0.0785 *** | 0.107 *** | 0.109 *** | 0.111 *** | 0.108 *** |

| (0.00583) | (0.00589) | (0.00585) | (0.00589) | (0.0222) | (0.0258) | (0.0222) | (0.0263) | (0.0285) | (0.0283) | (0.0284) | (0.0290) | |

| Inflation | 0.0223 | 0.00367 | 0.0144 | −0.000236 | −0.128 ** | −0.198 ** | −0.0999 | −0.190 ** | −0.0879 | −0.288 *** | −0.0504 | −0.291 *** |

| (0.0547) | (0.0389) | (0.0558) | (0.0389) | (0.0606) | (0.0913) | (0.0629) | (0.0929) | (0.0763) | (0.0951) | (0.0798) | (0.0964) | |

| Government Size | −0.00844 | −0.00326 | −0.0113 | −0.00225 | −0.379 *** | 0.0269 * | −0.364 *** | 0.0279 ** | −0.321 *** | 0.0327 ** | −0.308 *** | 0.0319 ** |

| (0.0373) | (0.00395) | (0.0375) | (0.00401) | (0.0722) | (0.0137) | (0.0725) | (0.0139) | (0.100) | (0.0145) | (0.100) | (0.0147) | |

| Trade Openness | 0.00226 | −0.0917 ** | 0.00265 | −0.0930 ** | 0.0264 *** | −0.0819 | 0.0253 *** | −0.0774 | 0.0341 ** | 0.0228 | 0.0337 ** | 0.0176 |

| (0.00364) | (0.0453) | (0.00368) | (0.0452) | (0.00964) | (0.103) | (0.00963) | (0.104) | (0.0148) | (0.112) | (0.0147) | (0.112) | |

| Deficit | −0.0835 * | −0.00303 | −0.0822 * | −0.00531 | 0.0313 | −0.0230 * | 0.0463 | −0.0224 * | 0.0425 | −0.0340 *** | 0.0541 | −0.0341 *** |

| (0.0461) | (0.00675) | (0.0462) | (0.00693) | (0.0862) | (0.0122) | (0.0863) | (0.0123) | (0.111) | (0.0129) | (0.111) | (0.0130) | |

| Debt | −0.00626 | 0.0495 | −0.0135 | 0.0365 | −0.0494 ** | −0.144 ** | −0.0321 | −0.139 * | −0.0672 ** | −0.112 | −0.0514 * | −0.116 |

| (0.0129) | (0.0565) | (0.0162) | (0.0571) | (0.0209) | (0.0693) | (0.0235) | (0.0703) | (0.0285) | (0.0755) | (0.0303) | (0.0766) | |

| CPI or WGI | - | - | −0.00138 | −0.00545 | - | - | 0.00706 | 0.00577 | - | - | 0.00793 | −0.00320 |

| - | - | (0.00186) | (0.00389) | - | - | (0.00445) | (0.0113) | - | - | (0.00517) | (0.0120) | |

| Debt*CPI or WGI | 0.000463 | −0.00407 | 0.00179 | 0.000772 | 0.00599 * | 0.00801 | 0.00243 | 0.00552 | 0.00686 | 0.00567 | 0.00337 | 0.00684 |

| (0.00206) | (0.00441) | (0.00273) | (0.00559) | (0.00341) | (0.00914) | (0.00407) | (0.0104) | (0.00522) | (0.00969) | (0.00569) | (0.0110) | |

| Constant | 0.167 *** | 0.158 *** | 0.169 *** | 0.150 *** | 0.777 *** | 0.705 *** | 0.737 *** | 0.689 *** | 1.005 *** | 0.963 *** | 0.967 *** | 0.968 *** |

| (0.0284) | (0.0288) | (0.0286) | (0.0293) | (0.0781) | (0.102) | (0.0817) | (0.107) | (0.125) | (0.122) | (0.128) | (0.126) | |

| Observations | 257 | 223 | 257 | 223 | 257 | 223 | 257 | 223 | 143 | 146 | 143 | 146 |

| R-squared | 0.143 | 0.236 | 0.145 | 0.243 | 0.406 | 0.304 | 0.415 | 0.305 |

| Variables | Model (1) | Model (1) | Model (2) | Model (2) | Model (3) | Model (3) | Model (4) | Model (4) |

|---|---|---|---|---|---|---|---|---|

| OLS CPI | OLS WGI | OLS CPI | OLS WGI | Fixed Effect CPI | Fixed Effect WGI | Fixed Effect CPI | Fixed Effect WGI | |

| Initial GDP | 0.717 *** | 0.722 *** | 0.740 *** | 0.757 *** | 0.598 *** | 0.547 *** | 0.613 *** | 0.555 *** |

| (0.0507) | (0.0516) | (0.0566) | (0.0577) | (0.166) | (0.161) | (0.172) | (0.172) | |

| Human Capital | 0.0330 | 0.0434 | 0.0243 | 0.0313 | 0.774 *** | 0.937 *** | 0.808 ** | 0.935 *** |

| (0.0702) | (0.0714) | (0.0709) | (0.0715) | (0.268) | (0.264) | (0.280) | (0.271) | |

| Inflation | 0.738 | −0.0239 | 0.556 | −0.161 | 0.923 | −4.253 *** | 0.386 | −4.237 *** |

| (1.104) | (0.464) | (1.124) | (0.472) | (1.185) | (1.252) | (1.568) | (1.290) | |

| Government Size | −0.00974 | −0.0384 | −0.101 | −0.0333 | −3.292 ** | −0.136 | −3.212 ** | −0.146 |

| (0.455) | (0.0388) | (0.467) | (0.0387) | (1.416) | (0.140) | (1.452) | (0.155) | |

| Trade Openness | −0.0397 | −0.150 | −0.0378 | 0.289 | −0.109 | −2.572 | −0.142 | −2.635 |

| (0.0381) | (1.104) | (0.0382) | (1.145) | (0.136) | (1.790) | (0.151) | (1.879) | |

| Deficit | 0.0125 | −0.176 * | 0.282 | −0.280 ** | −3.129 | −0.321 | −3.305 * | −0.349 |

| (1.088) | (0.0993) | (1.130) | (0.126) | (1.824) | (0.192) | (1.890) | (0.259) | |

| Debt | −0.420 ** | 0.502 | −0.597 ** | 0.331 | −1.077 ** | −0.173 | −1.334 * | −0.247 |

| (0.178) | (1.110) | (0.265) | (1.110) | (0.421) | (1.294) | (0.643) | (1.400) | |

| CPI or WGI | - | - | −0.0226 | −0.0668 | - | - | −0.0331 | −0.0226 |

| - | - | (0.0251) | (0.0503) | - | - | (0.0616) | (0.133) | |

| Debt*CPI or WGI | 0.0485 ** | 0.0679 | 0.0730 ** | 0.139 * | 0.136 ** | 0.190 ** | 0.170 ** | 0.208 |

| (0.0236) | (0.0463) | (0.0361) | (0.0707) | (0.0475) | (0.0680) | (0.0794) | (0.127) | |

| Constant | 1.920 *** | 1.849 *** | 1.890 *** | 1.634 *** | 1.665 | 1.845 | 1.683 | 1.807 |

| (0.393) | (0.401) | (0.395) | (0.430) | (1.205) | (1.188) | (1.230) | (1.242) | |

| Observations | 64 | 64 | 64 | 64 | 64 | 64 | 64 | 64 |

| R-squared | 0.953 | 0.951 | 0.954 | 0.953 | 0.916 | 0.915 | 0.918 | 0.915 |

| Variables | Model (1) | Model (1) | Model (2) | Model (2) | Model (3) | Model (3) | Model (4) | Model (4) |

|---|---|---|---|---|---|---|---|---|

| OLS CPI | OLS WGI | OLS CPI | OLS WGI | Fixed Effect CPI | Fixed Effect WGI | Fixed Effect CPI | Fixed Effect WGI | |

| Initial GDP | 0.675 *** | 0.679 *** | 0.683 *** | 0.697 *** | 0.204 | 0.119 | 0.222 | 0.0960 |

| (0.0464) | (0.0473) | (0.0503) | (0.0515) | (0.150) | (0.153) | (0.150) | (0.159) | |

| Human Capital | 0.0310 | 0.0387 | 0.0261 | 0.0304 | 0.840 ** | 0.935 *** | 0.775 ** | 0.979 *** |

| (0.0698) | (0.0709) | (0.0710) | (0.0716) | (0.307) | (0.330) | (0.310) | (0.342) | |

| Inflation | 1.169 | −0.302 | 1.052 | −0.285 | 1.505 | −3.960 *** | 2.874 | −4.004 *** |

| (1.084) | (0.434) | (1.120) | (0.435) | (1.338) | (1.192) | (1.773) | (1.209) | |

| Government Size | −0.306 | 0.0304 | −0.297 | 0.0300 | −3.151 ** | 0.212 | −3.345 ** | 0.233 * |

| (0.427) | (0.0335) | (0.430) | (0.0335) | (1.203) | (0.125) | (1.206) | (0.131) | |

| Trade Openness | 0.0265 | −1.083 | 0.0255 | −1.078 | 0.200 | −0.555 | 0.237 * | −0.353 |

| (0.0330) | (0.693) | (0.0332) | (0.694) | (0.118) | (1.340) | (0.121) | (1.394) | |

| Deficit | −0.982 | −0.105 | −0.985 | −0.159 | −0.648 | −0.256 | −0.387 | −0.135 |

| (0.683) | (0.0883) | (0.687) | (0.107) | (1.258) | (0.250) | (1.269) | (0.317) | |

| Debt | −0.376 ** | 0.866 | −0.455 * | 0.682 | −1.093 ** | 0.770 | −0.457 | 1.174 |

| (0.170) | (1.084) | (0.242) | (1.105) | (0.496) | (1.472) | (0.735) | (1.623) | |

| CPI or WGI | - | - | −0.0102 | −0.0404 | - | - | 0.0810 | 0.105 |

| - | - | (0.0223) | (0.0453) | - | - | (0.0695) | (0.168) | |

| Debt*CPI or WGI | 0.0555 ** | 0.0814 * | 0.0671 * | 0.125 * | 0.129 ** | 0.113 | 0.0450 | 0.0303 |

| (0.0236) | (0.0466) | (0.0346) | (0.0673) | (0.0571) | (0.0900) | (0.0917) | (0.160) | |

| Constant | 2.309 *** | 2.249 *** | 2.310 *** | 2.146 *** | 5.007 *** | 5.639 *** | 4.396 *** | 5.575 *** |

| (0.365) | (0.375) | (0.367) | (0.393) | (0.959) | (0.951) | (1.086) | (0.969) | |

| Observations | 79 | 79 | 79 | 79 | 79 | 79 | 79 | 79 |

| R-squared | 0.943 | 0.941 | 0.943 | 0.942 | 0.832 | 0.810 | 0.841 | 0.813 |

| Variables | Model (1) | Model (1) | Model (2) | Model (2) | Model (3) | Model (3) | Model (4) | Model (4) |

|---|---|---|---|---|---|---|---|---|

| OLS CPI | OLS WGI | OLS CPI | OLS WGI | Fixed Effect CPI | Fixed Effect WGI | Fixed Effect CPI | Fixed Effect WGI | |

| Initial GDP | 0.673 *** | 0.680 *** | 0.673 *** | 0.682 *** | 0.105 | 0.109 | 0.119 | 0.124 |

| (0.0384) | (0.0377) | (0.0389) | (0.0381) | (0.128) | (0.136) | (0.140) | (0.141) | |

| Human Capital | 0.242 *** | 0.254 *** | 0.243 *** | 0.256 *** | 0.857 *** | 0.877 *** | 0.844 *** | 0.879 *** |

| (0.0603) | (0.0589) | (0.0614) | (0.0599) | (0.279) | (0.293) | (0.287) | (0.296) | |

| Inflation | −0.0299 | −0.308 | −0.0350 | −0.314 | −0.134 | −3.284 *** | −0.0401 | −3.172 *** |

| (0.710) | (0.402) | (0.715) | (0.404) | (1.153) | (0.806) | (1.219) | (0.851) | |

| Government Size | −0.236 | 0.0333 | −0.240 | 0.0345 | −4.134 *** | 0.141 | −4.011 *** | 0.144 |

| (0.403) | (0.0378) | (0.407) | (0.0383) | (0.855) | (0.120) | (0.977) | (0.121) | |

| Trade Openness | 0.0337 | −1.110 ** | 0.0342 | −1.114 ** | 0.173 | 0.554 | 0.170 | 0.449 |

| (0.0380) | (0.497) | (0.0384) | (0.500) | (0.114) | (0.988) | (0.116) | (1.025) | |

| Deficit | −1.143 ** | 0.0316 | −1.144 ** | 0.0283 | 1.376 | −0.271 ** | 1.369 | −0.258 ** |

| (0.502) | (0.0681) | (0.505) | (0.0698) | (0.965) | (0.121) | (0.978) | (0.126) | |

| Debt | 0.0238 | −0.189 | 0.0128 | −0.198 | −0.715 ** | −0.443 | −0.688 ** | −0.383 |

| (0.143) | (0.704) | (0.176) | (0.708) | (0.269) | (1.174) | (0.290) | (1.193) | |

| CPI or WGI | - | - | −0.00213 | −0.00904 | - | - | 0.0133 | 0.0452 |

| - | - | (0.0198) | (0.0384) | - | - | (0.0493) | (0.0999) | |

| Debt*CPI or WGI | −2.01 × 10−5 | −0.0167 | 0.00205 | −0.00836 | 0.0767 * | 0.0838 | 0.0700 | 0.0581 |

| (0.0231) | (0.0442) | (0.0302) | (0.0568) | (0.0418) | (0.0687) | (0.0491) | (0.0896) | |

| Constant | 1.669 *** | 1.581 *** | 1.673 *** | 1.570 *** | 6.066 *** | 5.823 *** | 5.880 *** | 5.635 *** |

| (0.289) | (0.285) | (0.293) | (0.290) | (0.782) | (0.821) | (1.050) | (0.927) | |

| Observations | 121 | 124 | 121 | 124 | 121 | 124 | 121 | 124 |

| R-squared | 0.946 | 0.949 | 0.946 | 0.949 | 0.776 | 0.737 | 0.776 | 0.738 |

References

- Rogoff, K.; Reinhart, C. Growth in a Time of Debt. Am. Econ. Rev. 2010, 100, 573–578. [Google Scholar]

- Keen, S. Household Debt: The Final Stage in an Artificially Extended Ponzi Bubble. Aust. Econ. Rev. 2009, 42, 347–357. [Google Scholar] [CrossRef]

- Hien, E.; van Treeck, T. Financialisation in Post-Keynesian Models of Distribution and Growth—A Systematic Review; IMK Working Paper 20/2008; Macroeconomic Policy Institute: Düsseldorf, Germany, 2008. [Google Scholar]

- Arellano, M.; Bond, S. Some Tests of Specification for Panel Data: Monte Carlo Evidence and Application to Employment Equations. Rev. Econ. Stud. 1991, 58, 277–297. [Google Scholar] [CrossRef]

- Jalles, T.J. The impact of democracy and corruption on the debt-growth relationship in developing countries. J. Econ. Dev. 2011, 36, 41–72. [Google Scholar]

- Mankiw, G.N.; Elmendorf, D.W. Government Debt. In Handbook of Macroeconomics; Elsevier: New York, NY, USA, 1999. [Google Scholar]

- Barro, R.J. Are government bonds net wealth? J. Political Econ. 1974, 82, 1095–1117. [Google Scholar] [CrossRef]

- Barsky, R.B.; Mankiw, G.N.; Zeldes, S.P. Ricardian Consumers with Keynesian Propensities. Am. Econ. Rev. 1986, 76, 676–691. [Google Scholar]

- Feldstein, M. The Effects of Fiscal Policies when Incomes Are Uncertain: A Contradiction to Ricardian Equivalence. Am. Econ. Rev. 1988, 78, 14–23. [Google Scholar]

- Hayford, M. Liquidity Constraints and the Ricardian Equivalence Theorem: A Note. J. Money Credit Bank. 1989, 21, 380–387. [Google Scholar] [CrossRef]

- Kotlikoff, L.J.; Razin, A.; Rosenthal, W.A. A Strategic Altruistic Model in which Ricardian Equivalence Does Not Hold. Econ. J. 1990, 100, 1261–1268. [Google Scholar]

- Leiderman, L.; Razin, A. Testing Ricardian Neutrality with an Intertemporal Stochastic Model. J. Money Credit Bank. 1988, 20, 1–21. [Google Scholar] [CrossRef]

- Evans, P. Are Consumers Ricardian? Evidence for the United States. J. Political Econ. 1988, 96, 983–1004. [Google Scholar] [CrossRef]

- Evans, P. Is Ricardian Equivalence a Good Approximation? Econ. Inq. 1991, 29, 626–644. [Google Scholar] [CrossRef]

- Haug, A.A. Ricardian Equivalence, Rational Expectations, and the Permanent Income Hypothesis. J. Money Credit Bank. 1990, 22, 305–326. [Google Scholar] [CrossRef]

- Batdelger, T.; Kandil, M. Determinants of the current account balance in the United States. Appl. Econ. 2012, 44, 653–669. [Google Scholar] [CrossRef]

- Craig, S.G.; Hoang, E.C.; Vollrath, D. Household Response to Government Debt: Evidence from Life Insurance Holdings. J. Money Credit Bank. 2015, 47, 819–845. [Google Scholar] [CrossRef]

- Linnemann, L.; Schabert, A. Debt Non-neutrality, Policy Interactions, and Macroeconomic Stability. Int. Econ. Rev. 2010, 51, 461–474. [Google Scholar] [CrossRef]

- Boyer, R. The Four Fallacies of Contemporary Austerity Policies: The Lost Keynesian Legacy. Camb. J. Econ. 2012, 36, 283–312. [Google Scholar] [CrossRef]

- Banzhaf, S.H.; Oates, W.E. On Fiscal Illusion in Local Public Finance: Re-examining Ricardian Equivalence and the Renter Effect. Natl. Tax J. 2013, 66, 511–540. [Google Scholar] [CrossRef]

- Evans, G.W.; Honkapohja, S.; Mitra, K. Does Ricardian Equivalence Hold When Expectations Are Not Rational? J. Money Credit Bank. 2012, 44, 1259–1283. [Google Scholar] [CrossRef]

- Wong, W.K. Consumption Response to Government Transfers: Behavioral Motives Revealed by Savers and Spenders. Contemp. Econ. Policy 2012, 30, 489–501. [Google Scholar] [CrossRef]

- De Castro, F.; Fernández, L. The Effects of Fiscal Shocks on the Exchange Rate in Spain. Econ. Soc. Rev. 2013, 44, 151–180. [Google Scholar] [CrossRef]

- Konya, L.; Abdullaev, B. Does Ricardian Equivalence Hold in Australia? A Revision Based on Testing Super Exogeneity with Impulse-Indicator Saturation. Empir. Econ. 2014, 49, 423–448. [Google Scholar] [CrossRef]

- Dumiter, F.; Berlingher, D.; Anca, O.; Todor, S. Double taxation conventions, structure and evolution of the American tax system. J. Leg. Stud. 2016, 17, 1–14. [Google Scholar] [CrossRef]

- Choi, D.F.S.; Holmes, M.J. Budget Deficits and Real Interest Rates: A Regime-Switching Reflection on Ricardian Equivalence. J. Econ. Financ. 2014, 38, 71–83. [Google Scholar] [CrossRef]

- Gale, W.G.; Orszag, P.R. The Economic Effects of Long-Term Fiscal Discipline; Urban-Brookings Tax Policy Center Discussion Paper; Urban Institute: Washington, DC, USA, 2002. [Google Scholar]

- Baldacci, E.; Kumar, M. Fiscal Deficits, Public Debt, and Sovereign Bond Yields; IMF Working Paper; IMF: Washington, DC, USA, 2010. [Google Scholar]

- Corsetti, G.; Kuester, K.; Meier, A.; Müller, G.J. Sovereign Risk, Fiscal Policy, and Macroeconomic Stability. Econ. J. 2013, 123, 99–132. [Google Scholar] [CrossRef]

- Barro, R.J. On the Determination of the Public Debt. J. Political Econ. 1979, 87, 940–971. [Google Scholar] [CrossRef]

- Dotsey, M. Some Unpleasant Supply side Arithmetic. J. Monet. Econ. 1994, 33, 507–524. [Google Scholar] [CrossRef]

- Aizenman, J.; Kletzer, K.; Pinto, B. Economic Growth with Constraints on Tax Revenues and Public Debt: Implications for Fiscal Policy and Cross-Country Differences; NBER Working Paper; NBER: Cambridge, MA, USA, 2007. [Google Scholar]

- Sargent, T.J.; Wallace, N. Some Unpleasant Monetarist Arithmetic. Fed. Reserv. Bank Minneap. Q. Rev. 1981, 5, 1–17. [Google Scholar]

- Barro, R.J. Inflation and Economic Growth; Quarterly Bulletin; Bank of England: London, UK, 1995. [Google Scholar]

- Cochrane, J.H. Determinacy and Identification with Taylor Rules. J. Political Econ. 2011, 119, 565–615. [Google Scholar] [CrossRef]

- Aghion, P.; Kharroubi, E. Cyclical Macro Policy and Industry Growth: The Effect of Counter-Cyclical Fiscal Policy; Harvard University: Cambridge, MA, USA, 2007. [Google Scholar]

- Woo, J. Why Do More Polarized Countries Run More Procyclical Fiscal Policy? Rev. Econ. Stat. 2009, 91, 850–870. [Google Scholar] [CrossRef]

- Burnside, C.; Eichenhaum, M.; Rebelo, S. On the Fiscal Implications of Twin Crises; NBER Working Paper; NBER: Cambridge, MA, USA, 2001. [Google Scholar]

- Hemming, R.; Kell, M.; Schimmelpgenning, A. Fiscal Vulnerability and Financial Crises in Emerging Market Economics; IMF Working Paper; IMF: Washington, DC, USA, 2003. [Google Scholar]

- Curutchet, A.S. Debt and Economic Growth in Developing and Industrial Countries; Working Papers No. 34; Lund University: Lund, Sweden, 2005. [Google Scholar]

- Caner, M.; Grennes, T.; Koehler-Geib, F. Finding the Tipping Point-When Sovereign Debt Turns Bad; Policy Research Working Paper 5391; The World Bank: Washington, DC, USA, 2010. [Google Scholar]

- Ursua, J.; Wilson, D. Risks to Growth from Build-Ups in Public Debt. Global Economics Weekly; The World Bank: Washington, DC, USA, 2012. [Google Scholar]

- Checherita, C.; Rother, P. The Impact of High and Growing Government Debt on Economic Growth: An Empirical Investigation for the Euro Area; Working paper 1237; European Central Bank: Frankfurt, Germany, 2010. [Google Scholar]

- Baum, A.; Checherita-Westphal, C.; Rother, P. Debt and Growth: New Evidence for the Euro Area; Working Paper 184; European Central Bank: Frankfurt, Germany, 2012. [Google Scholar]

- Cecheritti, S.G.; Mohanty, M.S.; Zampolli, F. The Real Effects of Debt. Bank for International Settlements; Working Paper 352; Bank for International Settlements: Basel, Switzerland, 2012. [Google Scholar]

- Panizza, U.; Presbitero, A.F. Public Debt and Economic Growth: Is There a Causal Effect? Università Politecnica delle Marche, MoFiR (Money and Finance Research Group): London, UK, 2012. [Google Scholar]

- Balassone, F.; Francese, M.; Pace, A. Public Debt and Economic Growth in Italy; Economic History Working Papers No. 11; Banca d’Ltalia: Rome, Italy, 2011. [Google Scholar]

- Casni, A.C.; Badurina, A.A.; Sertic, M.B. Public Debt and Growth: Evidence from Central, Eastern and Southern European countries. Proc. Rij. Fac. Econ. J. Econ. Bus. 2014, 32, 35–51. [Google Scholar]

- Woo, J.; Kumar, M.S. Public Debt and Growth. Economica 2015, 82, 705–739. [Google Scholar] [CrossRef]

- Modigliani, F.; Fitoussi, J.P.; Moro, B.; Snower, D.; Solow, R.; Steinherr, A.; Labini, P. ‘An economists’ manifesto on unemployment in the European Union. Banca Naz. Lav. Q. Rev. 1998, 51, 327–361. [Google Scholar] [CrossRef]

- Creel, J.; Fitoussi, J.P. How to Reform the European Central Bank; Centre for European Reform: London, UK, 2002. [Google Scholar]

- Le Cacheux, J. A golden rule for the euro area? In Proceedings of the CDC-IXIS & CEPII Fiscal Discipline Workshop, Paris, France, 27 November 2002.

- Blanchard, O.; Giavazzi, F. Improving the SGP through a Proper Accounting of Public Investment; Discussion Paper No. 4220; Centre for Economic Policy Research (CEPR): London, UK, 2004. [Google Scholar]

- Balassone, F.; Franco, D. Public investment, the Stability Pact and the golden rule. Fisc. Stud. 2000, 21, 207–229. [Google Scholar] [CrossRef]

- Buiter, W. Notes on a Code for Fiscal Stability. Oxf. Econ. Pap. 2001, 53, 1–9. [Google Scholar] [CrossRef]

- Buti, M.; Eijffinger, S.; Franco, D. Revisiting the SGP: Grand Design or Internal Adjustment? Discussion Paper No. 3692; Centre for Economic Policy Research (CEPR): London, UK, 2003. [Google Scholar]

- Minea, A.; Villieu, P. Borrowing to Finance Public Investment? The Golden Rule of Public Finance Reconsidered in an Endogenous Growth Setting. Fisc. Stud. 2009, 30, 103–133. [Google Scholar] [CrossRef]

- Pattillo, C.; Poirson, H.; Ricci, L.A. External Debt and Growth. Rev. Econ. Inst. 2011, 2, 1–30. [Google Scholar] [CrossRef]

- Cordella, T.; Ricci, L.A.; Ruiz-Arranz, M. Debt Overhang or Debt Irrelevance. IMF Staff Pap. 2010, 57, 1–24. [Google Scholar] [CrossRef]

- González-Fernández, M.; González-Velasco, C. Shadow economy, corruption and public debt in Spain. J. Policy Model. 2014, 36, 1101–1117. [Google Scholar] [CrossRef]

- Cooray, A.; Dzhumashev, R.; Schneider, F. How does corruption affect public debt? An empirical analysis. World Dev. 2017, 90, 115–127. [Google Scholar] [CrossRef]

- North, D.C. Institutions, Institutional Change and Economic Performance; Cambridge University: Cambridge, UK, 1990. [Google Scholar]

- Égert, B. Regulation, Institutions, and Productivity: New Macroeconomic Evidence from OECD Countries. Am. Econ. Rev. 2016, 106, 109–113. [Google Scholar] [CrossRef]

- Dort, T.; Méon, P.-G.; Sekkat, K. Does investment spur growth everywhere? Not where institutions are weak. Kyklos 2014, 67, 482–505. [Google Scholar] [CrossRef]

- Berggren, N.; Bergh, A.; Bjornskov, C. What Matters for Growth in Europe? Institutions versus Policies, Quality versus Instability. J. Econ. Policy Reform 2015, 18, 69–88. [Google Scholar] [CrossRef]

- Yun, J.J. How do we conquer the growth limits of capitalism? Schumpeterian Dynamics of Open Innovation. J. Open Innov. Technol. Market Complex. 2015, 1, 1–20. [Google Scholar] [CrossRef]

- Yun, J.J.; Cooke, P.; Kodama, F.; Phillips, F.; Gupta, A.K.; Gamboa, F.J.C.; Krishna, V.; Lee, K.; Lee, K.; Witt, U.; et al. An open letter to Mr. Secretary General of the United Nations to propose setting up global standards for conquering growth limits of capitalism. J. Open Innov. Technol. Market Complex. 2016, 2, 1–4. [Google Scholar] [CrossRef]

- Mauro, P. Corruption and Growth. Q. J. Econ. 1995, 110, 681–712. [Google Scholar] [CrossRef]

- Mo, P.H. Corruption and Economic Growth. J. Comp. Econ. 2001, 29, 66–79. [Google Scholar] [CrossRef]

- Tanzi, V.; Davoodi, H.R. Corruption, Growth and Public Finances; IMF Working Paper; International Monetary Fund: Washington, DC, USA, 2000. [Google Scholar]

- Brunetti, A.; Kisunko, G.; Weder, B. Credibility of Rules and Economic Growth—Evidence from a Worldwide Private Sector Survey; Background Paper for the World Development Report; The World Bank: Washington, DC, USA, 1997. [Google Scholar]

- Campos, E.; Lien, D.; Pradhan, S. The impact of corruption on investment: Predictability matters. World Dev. 1999, 27, 1059–1067. [Google Scholar] [CrossRef]

- Abed, G.; Davoodi, H. Corruption, structural reforms, and economic performance in the transition economies. In Governance, Corruption, & Economic Performance; Abed, G.T., Gupta, S., Eds.; International Monetary Fund, Publication Services: Washington, DC, USA, 2002. [Google Scholar]

- Wei, S.J. How taxing is corruption on international investors? Rev. Econ. Stat. 2000, 82, 1–11. [Google Scholar] [CrossRef]

- Lambsdorff, J.G. How corruption affects productivity? Kyklos 2003, 56, 457–474. [Google Scholar] [CrossRef]

- Al-Marhubi, F. Corruption and Inflation. Econ. Lett. 2000, 66, 199–202. [Google Scholar] [CrossRef]

- Blackburn, K.; Haque, M.E.; Neanidis, K.C. Corruption, Seigniorage and Growth: Theory and Evidence; CESifo Working Paper Series No. 2354, SSRN 1173622; SSRN eLibrary: Munchen, Germany, 2008. [Google Scholar]

- Friedman, E.; Johnson, S.; Kaufmann, D.; Zoido-Lobaton, P. Dodging the grabbing hand: the determinants of unofficial activity in 69 countries. J. Publ. Econ. 2000, 76, 459–493. [Google Scholar] [CrossRef]

- Johnson, S.; Kaufmann, D.; Shleifer, A. The unofficial economy in transition. Brook. Pap. Econ. Act. 1997, 27, 159–239. [Google Scholar] [CrossRef]

- Schneider, F.; Buehn, A.; Montenegro, C. Shadow Economies All over the World: New Estimates for 162 Countries from 1999–2007; World Bank Policy Research Working Paper No. 5356; World Bank: Washington, DC, USA, 2010. [Google Scholar]

- Mauro, P. Corruption and the composition of government expenditure. J. Publ. Econ. 1998, 69, 263–279. [Google Scholar] [CrossRef]

- Justesen, M.; Bjornskov, C. Exploiting the poor: Bureaucratic corruption and poverty in Africa. World Dev. 2014, 58, 106–115. [Google Scholar] [CrossRef]

- Dzhumashev, R. Corruption and growth: The role of governance, public spending, and economic development. Econ. Model. 2014, 37, 202–215. [Google Scholar] [CrossRef]

- D’Agostino, G.; Dunne, J.P.; Pieroni, L. Corruption and growth in Africa. Eur. J. Political Econ. 2016, 43, 71–88. [Google Scholar] [CrossRef]

- D’Agostino, G.; Dunne, J.P.; Pieroni, L. Government spending, corruption and economic growth. World Dev. 2016, 84, 190–205. [Google Scholar] [CrossRef]

- Leff, N. Economic development through bureaucratic corruption. Am. Behav. Sci. 1964, 8, 8–14. [Google Scholar] [CrossRef]

- Huntington, S.P. Political Order in Changing Societies; Yale University Press: New Haven, CT, USA, 1968. [Google Scholar]

- Johnson, E. An economic analysis of corrupt government, with special application for less developed countries. Kylos 1975, 28, 47–61. [Google Scholar] [CrossRef]

- Nye, J. Corruption and political development: A cost-benefit analysis. Am. Political Sci. Rev. 1967, 61, 417–427. [Google Scholar] [CrossRef]

- Wedeman, A. Looters, rent-scrapers, and dividend-collectors: Corruption and growth in Zaire, South Korea, and the Philippines. J. Dev. Areas 1997, 31, 457–478. [Google Scholar]

- Wei, S. Corruption in economic transition and development. In Proceedings of the UNECE Spring Seminar, Geneva, Switzerland, 7–8 May 2001.

- Lau, C.K.M.; Demir, E.; Bilgin, M.H. Experience-based corporate corruption and stock market volatility: Evidence from emerging markets. Emerg. Mark. Rev. 2013, 17, 1–13. [Google Scholar] [CrossRef]

- Acemoglu, D.; Johnson, S.; Querubin, P.; Robinson, J.A. When does policy reform work? The case of central bank independence. Brook. Pap. Econ. Act. 2008, 39, 351429. [Google Scholar]

- Aidt, T.S. Corruption, institutions, and economic development. Oxf. Rev. Econ. Policy 2009, 25, 271–291. [Google Scholar] [CrossRef]

- De Rosa, D.; Gooroochurn, N.; Gorg, H. Corruption and Productivity: Firm-Level Evidence from the BEEPS Survey; World Bank Policy Research Working Paper Series 5348; World Bank: Washington, DC, USA, 2010. [Google Scholar]

- Meon, P.; Sekkat, K. Does corruption grease or sand the wheels of growth? Publ. Choice 2005, 122, 69–97. [Google Scholar] [CrossRef]

- Meon, P.; Weill, L. Is corruption an efficient grease? World Dev. 2010, 38, 244–259. [Google Scholar] [CrossRef]

- La Porta, R.; Lopez-de-Silanes, F.; Shleifer, A.; Vishny, R. The quality of government. J. Law Econ. Organ. 1999, 15, 222–279. [Google Scholar] [CrossRef]

- Shleifer, A.; Vishny, R. Corruption. Q. J. Econ. 1993, 108, 599–618. [Google Scholar] [CrossRef]

- Mendez, F.; Sepulveda, F. Corruption, growth and political regimes: Cross country evidence. Eur. J. Political Econ. 2006, 22, 82–98. [Google Scholar] [CrossRef]

- Pattillo, C.; Poirson, H.; Ricci, L.A. Through What Channels Does External Debt Affects Growth? In Brookings Trade Forum; World Bank: Washington, DC, USA, 2003. [Google Scholar]

- Park, J. Corruption, soundness of the banking sector, and economic growth: A cross-study. J. Int. Money Financ. 2012, 31, 907–929. [Google Scholar] [CrossRef]

- Ciocchini, F.; Durbin, E.; Ng, D. Does Corruption Increase Emerging Market Bond Spreads? J. Econ. Bus. 2003, 55, 503–528. [Google Scholar] [CrossRef]

- Myrdal, G. Corruption: Its causes and effects. In Asian Drama: An Inquiry into the Poverty of Nations; Twentieth Century Fund: New York, NY, USA, 1968; Volume II. [Google Scholar]

- Krueger, A.O. The Political Economy of the Rent-Seeking Society. Am. Econ. Rev. 1974, 64, 291–303. [Google Scholar]

- Shleifer, A.; Vishny, R.W. A survey of corporate governance. J. Financ. 1997, 52, 737–783. [Google Scholar] [CrossRef]

- Lui, F.T. An equilibrium queuing model of bribery. J. Political Econ. 1985, 93, 760–781. [Google Scholar] [CrossRef]

- Klitgaard, R. Controlling Corruption; University of California Press: Berkeley, CA, USA, 1988. [Google Scholar]

- Colombatto, E. Why is corruption tolerated? Rev. Aust. Econ. 2003, 16, 363–379. [Google Scholar] [CrossRef]

- Knack, S.; Keefer, P. Institutions and Economic Performance: Cross-Country Tests Using Alternative Institutional Measures. Econ. Politics 1995, 7, 207–227. [Google Scholar] [CrossRef]

- Poirson, H. Economic Security, Private Investment, and Growth in Developing Countries; IMF Working Paper; International Monetary Fund: Washington, DC, USA, 1998. [Google Scholar]

- Weidmann, J.; Leite, C. Does Mother Nature Corrupt? Natural Resources, Corruption, and Economic Growth; IMF Working Paper; IMF: Washington, DC, USA, 1999. [Google Scholar]

- Gyimah-Brempong, K. Corruption, economic growth, and income inequality in Africa. Econ. Gov. 2002, 3, 183–209. [Google Scholar] [CrossRef]

- Wedeman, A. Looters, Rent-Scrapers, and Dividend-Collectors: Corruption and Growth in Zaire, South Korea, and the Philippines. J. Dev. Areas 2005, 31, 457–478. [Google Scholar]

- Svensson, J. Eight Questions about Corruption. J. Econ. Perspect. 2005, 19, 19–42. [Google Scholar] [CrossRef]

- Assiotis, A.; Sylwester, K. Do the effects of corruption upon growth differ between democracies and autocracies? Rev. Dev. Econ. 2014, 18, 581–594. [Google Scholar] [CrossRef]

- Ugur, M. Corruption’s Direct Effects on per-capita Income Growth: A meta-analysis. J. Econ. Surv. 2014, 28, 472–490. [Google Scholar] [CrossRef]

- Grossman, G.M.; Helpman, E. Innovation and Growth in the Global Economy; MIT Press: Cambridge, MA, USA, 1991. [Google Scholar]

- Sala-i-Martin, X.; Doppelhofer, G.; Miller, R.I. Determinants of Long-Term Growth: A Bayesian Averaging of Classical Estimates (BACE) Approach. J. Monet. Econ. 2004, 32, 485–512. [Google Scholar] [CrossRef]

- Fischer, S. The role of macroeconomic factors in growth. J. Monet. Econ. 1993, 32, 485–512. [Google Scholar] [CrossRef]

- Baldacci, E.; Clements, B.; Gupta, S.; Cui, Q. Social Spending, Human Capital, and Growth in Developing Countries: Implications for Achieving the MDGs; IMF Working Paper, No. wp/04/217; IMF: Washington, DC, USA, 2004. [Google Scholar]

| Variable Name | Definition | Source |

|---|---|---|

| GDP Per Capita | Log of real GDP per capita on the basis of the 2011 price | Penn World Table v9.0 |

| Human Capital | Log of average years of secondary schooling in the population over age 15 in the initial year of each period | Penn World Table v9.0 |

| Inflation | Logarithm of (1 + inflation rate) | IMF WEO data |

| Government Size | Government consumption ratio to GDP | Penn World Table v9.0 |

| Trade Openness | Sum of export and import as a percentage of GDP | Penn World Table v9.0 |

| Debt | The ratio of public debt to GDP. Debt is general government’s gross debt. | IMF WEO data |

| Deficit | The ratio of fiscal deficit to GDP, measured by the difference between government revenue and expenditure | IMF WEO data |

| CPI | CORRUPTION PERCEPTIONS INDEX published by Transparency International: the score has been rescaled in 2012 (from a 10-point scale to a 100-point scale). The scores from 2012 were converted to the scale before 2012. | Transparency International |

| Variable | Mean | Std. Dev. | Min | Max |

|---|---|---|---|---|

| GDP per capita | 19,730 | 16,168 | 592 | 75,920 |

| CPI | 5.202 | 2.300 | 1.100 | 10.000 |

| Human capital | 2.680 | 0.648 | 1.126 | 3.734 |

| Inflation | 0.043 | 0.065 | −0.040 | 0.619 |

| Government size | 0.179 | 0.059 | 0.043 | 0.409 |

| Trade openness | 0.674 | 0.596 | 0.077 | 4.615 |

| Deficit | 0.025 | 0.048 | −0.281 | 0.177 |

| Debt | 0.606 | 0.377 | 0.001 | 2.491 |

| Variables | Model (1) | Model (2) | Model (3) | Model (4) | Model (5) | Model (6) |

|---|---|---|---|---|---|---|

| OLS | OLS | Fixed Effect | Fixed Effect | GMM | GMM | |

| Initial GDP | −0.0207 *** | −0.0201 *** | −0.0997 *** | −0.101 *** | −0.136 *** | −0.137 *** |

| (0.00388) | (0.00392) | (0.0117) | (0.0116) | (0.0157) | (0.0157) | |

| Human Capital | 0.0202 *** | 0.0211 *** | 0.0832 *** | 0.0860 *** | 0.0932 *** | 0.0948 *** |

| (0.00578) | (0.00583) | (0.0220) | (0.0219) | (0.0272) | (0.0273) | |

| Inflation | 0.00180 | −0.00408 | −0.127 *** | −0.110 ** | −0.0512 | −0.0398 |

| (0.0413) | (0.0416) | (0.0420) | (0.0431) | (0.0538) | (0.0555) | |

| Government Size | −0.00742 | −0.0131 | −0.357 *** | −0.344 *** | −0.267 *** | −0.264 *** |

| (0.0361) | (0.0364) | (0.0614) | (0.0616) | (0.0766) | (0.0768) | |

| Trade Openness | 0.00629 * | 0.00690 * | 0.0261 *** | 0.0250 *** | 0.0644 *** | 0.0643 *** |

| (0.00355) | (0.00359) | (0.00712) | (0.00712) | (0.0139) | (0.0139) | |

| Deficit | −0.0537 | −0.0546 | 0.0264 | 0.0377 | 0.0567 | 0.0645 |

| (0.0361) | (0.0360) | (0.0485) | (0.0488) | (0.0653) | (0.0658) | |

| Debt | −0.00314 | −0.0135 | −0.0300 * | −0.0149 | −0.0542 ** | −0.0443 * |

| (0.0124) | (0.0155) | (0.0179) | (0.0201) | (0.0229) | (0.0251) | |

| CPI | - | −0.00209 | - | 0.00712 | - | 0.00449 |

| - | (0.00189) | - | (0.00439) | - | (0.00505) | |

| Debt*CPI | 0.000558 | 0.00259 | 0.00678 ** | 0.00322 | 0.0101 ** | 0.00783 |

| (0.00206) | (0.00276) | (0.00317) | (0.00384) | (0.00474) | (0.00541) | |

| Constant | 0.167 *** | 0.171 *** | 0.796 *** | 0.759 *** | 1.067 *** | 1.044 *** |

| (0.0297) | (0.0299) | (0.0823) | (0.0850) | (0.118) | (0.122) | |

| Observations | 258 | 258 | 258 | 258 | 144 | 144 |

| R-squared | 0.133 | 0.137 | 0.468 | 0.476 | ||

| AR(1) | 0.4113 | 0.3754 | ||||

| Sargan Test | 0.3542 | 0.4326 |

| Variables | Model (1) | Model (2) | Model (3) | Model (4) | Model (5) | Model (6) |

|---|---|---|---|---|---|---|

| OLS | OLS | Fixed Effect | Fixed Effect | GMM | GMM | |

| Initial GDP | −0.0214 *** | −0.0188 *** | −0.0740 *** | −0.0734 *** | −0.0993 *** | −0.0921 *** |

| (0.00478) | (0.00523) | (0.0146) | (0.0148) | (0.0220) | (0.0222) | |

| Human Capital | 0.0107 | 0.00995 | 0.0994 *** | 0.0990 *** | 0.135 *** | 0.132 *** |

| (0.00649) | (0.00650) | (0.0271) | (0.0272) | (0.0331) | (0.0329) | |

| Inflation | −0.0438 | −0.0470 | −0.115 ** | −0.117 ** | −0.0811 | −0.101 * |

| (0.0413) | (0.0413) | (0.0448) | (0.0455) | (0.0566) | (0.0575) | |

| Government Size | −0.00341 | −0.0142 | −0.393 *** | −0.393 *** | −0.248 ** | −0.249 ** |

| (0.0417) | (0.0425) | (0.0819) | (0.0823) | (0.107) | (0.106) | |

| Trade Openness | −0.00270 | −0.00215 | 0.00209 | 0.00219 | 0.0120 | 0.00814 |

| (0.00401) | (0.00403) | (0.0116) | (0.0116) | (0.0151) | (0.0150) | |

| Deficit | 0.0841 | 0.0892 | 0.139 ** | 0.137 ** | −0.0271 | −0.0354 |

| (0.0612) | (0.0612) | (0.0643) | (0.0649) | (0.0924) | (0.0926) | |

| Debt | −0.0226 | −0.0415 * | −0.0449 * | −0.0501 | −0.0786 * | −0.105 ** |

| (0.0148) | (0.0213) | (0.0269) | (0.0326) | (0.0403) | (0.0432) | |

| CPI | - | −0.00282 | - | −0.00150 | - | −0.00805 |

| - | (0.00228) | - | (0.00531) | - | (0.00621) | |

| Debt*CPI | 0.00168 | 0.00464 | 0.00627 * | 0.00719 | 0.00957 * | 0.0148 ** |

| (0.00212) | (0.00319) | (0.00341) | (0.00473) | (0.00573) | (0.00658) | |

| Constant | 0.214 *** | 0.209 *** | 0.534 *** | 0.539 *** | 0.660 *** | 0.647 *** |

| (0.0375) | (0.0377) | (0.101) | (0.103) | (0.173) | (0.171) | |

| Observations | 137 | 137 | 137 | 137 | 73 | 73 |

| R-squared | 0.281 | 0.289 | 0.384 | 0.384 | ||

| AR(1) | 0.0593 | 0.0535 | ||||

| Sargan Test | 0.2940 | 0.2810 |

© 2017 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license ( http://creativecommons.org/licenses/by/4.0/).

Share and Cite

Kim, E.; Ha, Y.; Kim, S. Public Debt, Corruption and Sustainable Economic Growth. Sustainability 2017, 9, 433. https://doi.org/10.3390/su9030433

Kim E, Ha Y, Kim S. Public Debt, Corruption and Sustainable Economic Growth. Sustainability. 2017; 9(3):433. https://doi.org/10.3390/su9030433

Chicago/Turabian StyleKim, Eunji, Yoonhee Ha, and Sangheon Kim. 2017. "Public Debt, Corruption and Sustainable Economic Growth" Sustainability 9, no. 3: 433. https://doi.org/10.3390/su9030433

APA StyleKim, E., Ha, Y., & Kim, S. (2017). Public Debt, Corruption and Sustainable Economic Growth. Sustainability, 9(3), 433. https://doi.org/10.3390/su9030433