Life Cycle Sustainability Assessment for Sustainability Improvements: A Case Study of High-Density Polyethylene Production in Alberta, Canada

Abstract

:1. Introduction

2. Goal and Scope Definition

3. Inventory Analysis

3.1. LCA Methodology

3.2. S-LCA Methodology

3.3. LCC Methodology

4. Impact Assessment

5. Interpretation

5.1. Results Presentation

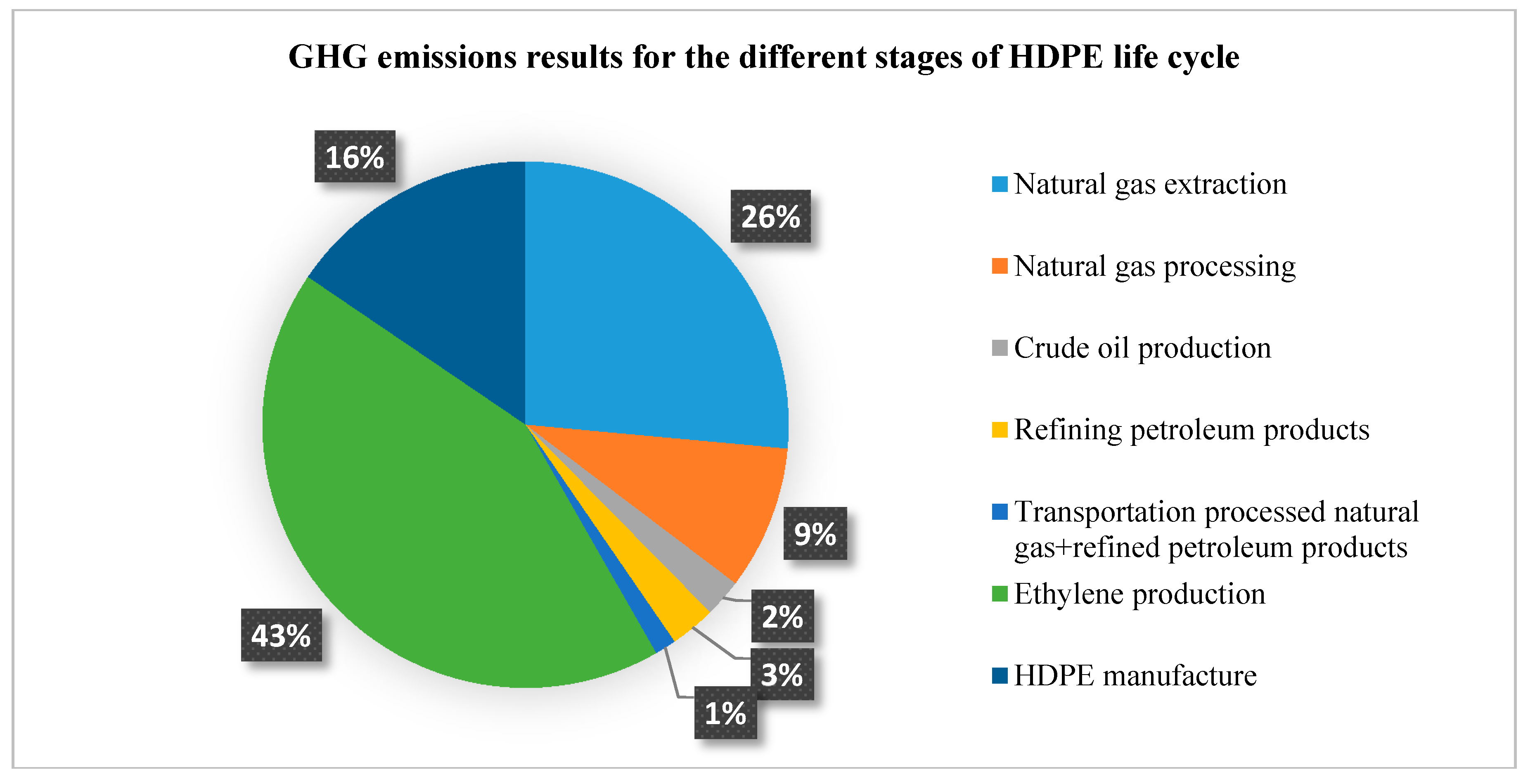

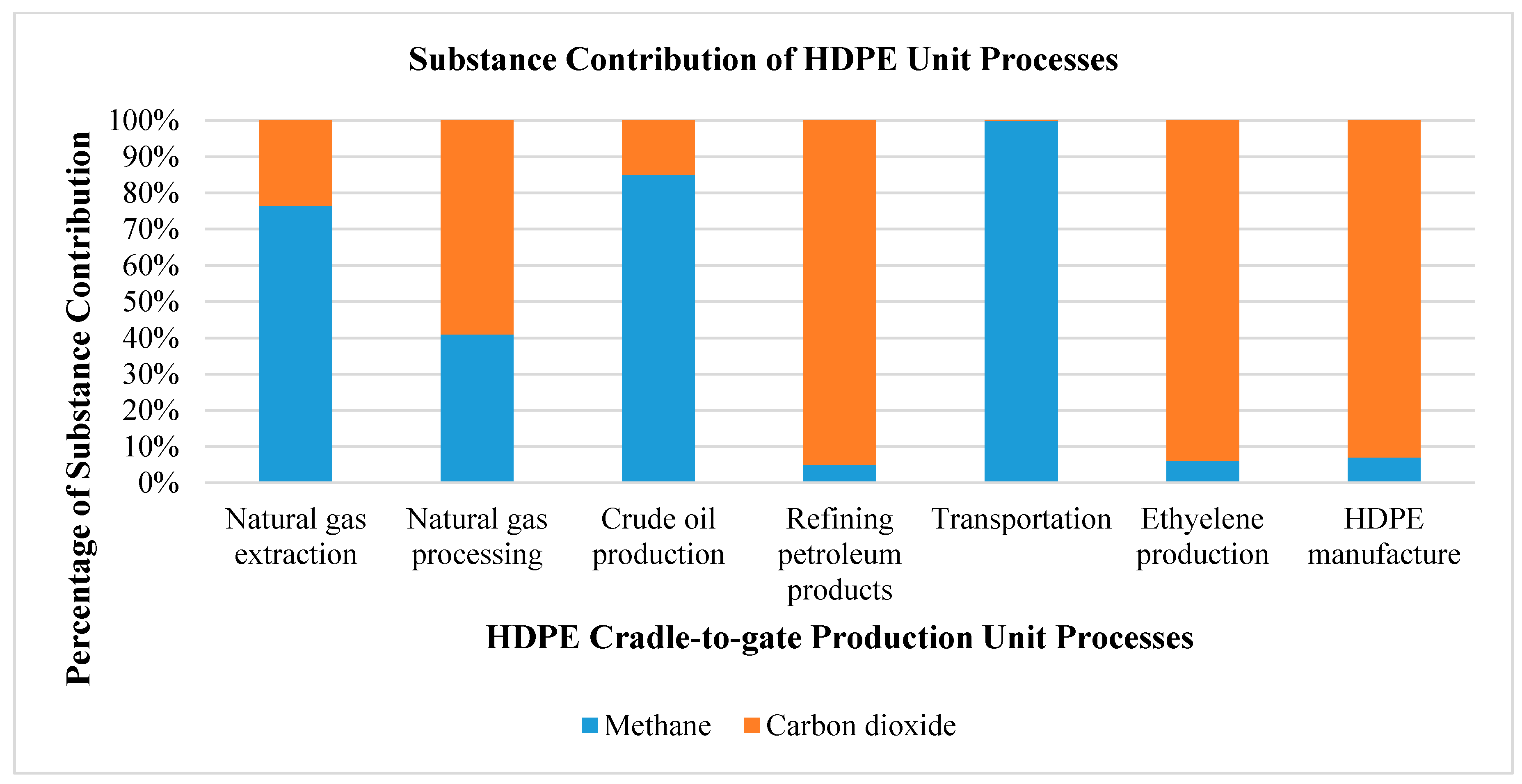

5.1.1. Environmental Dimension Results

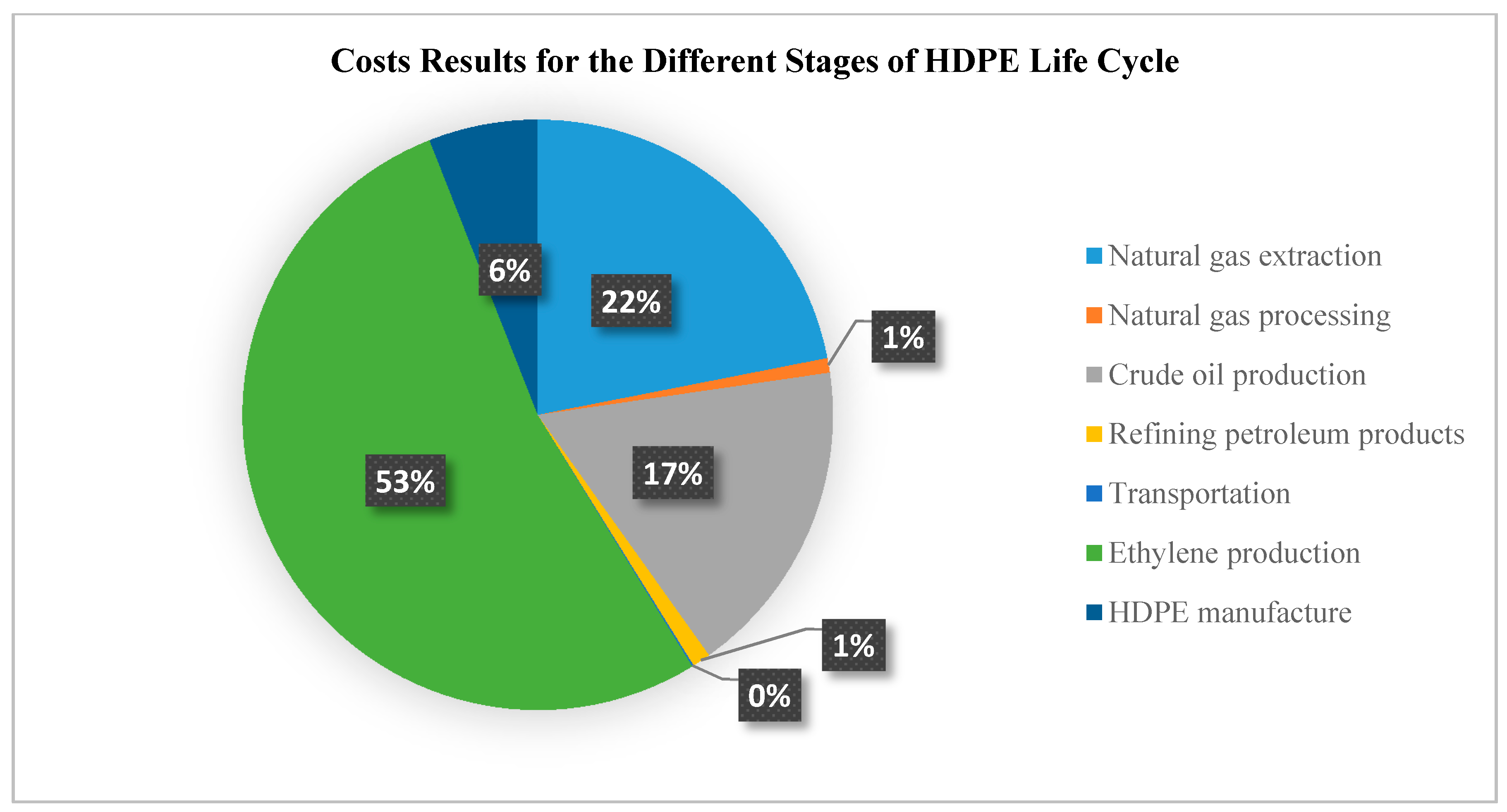

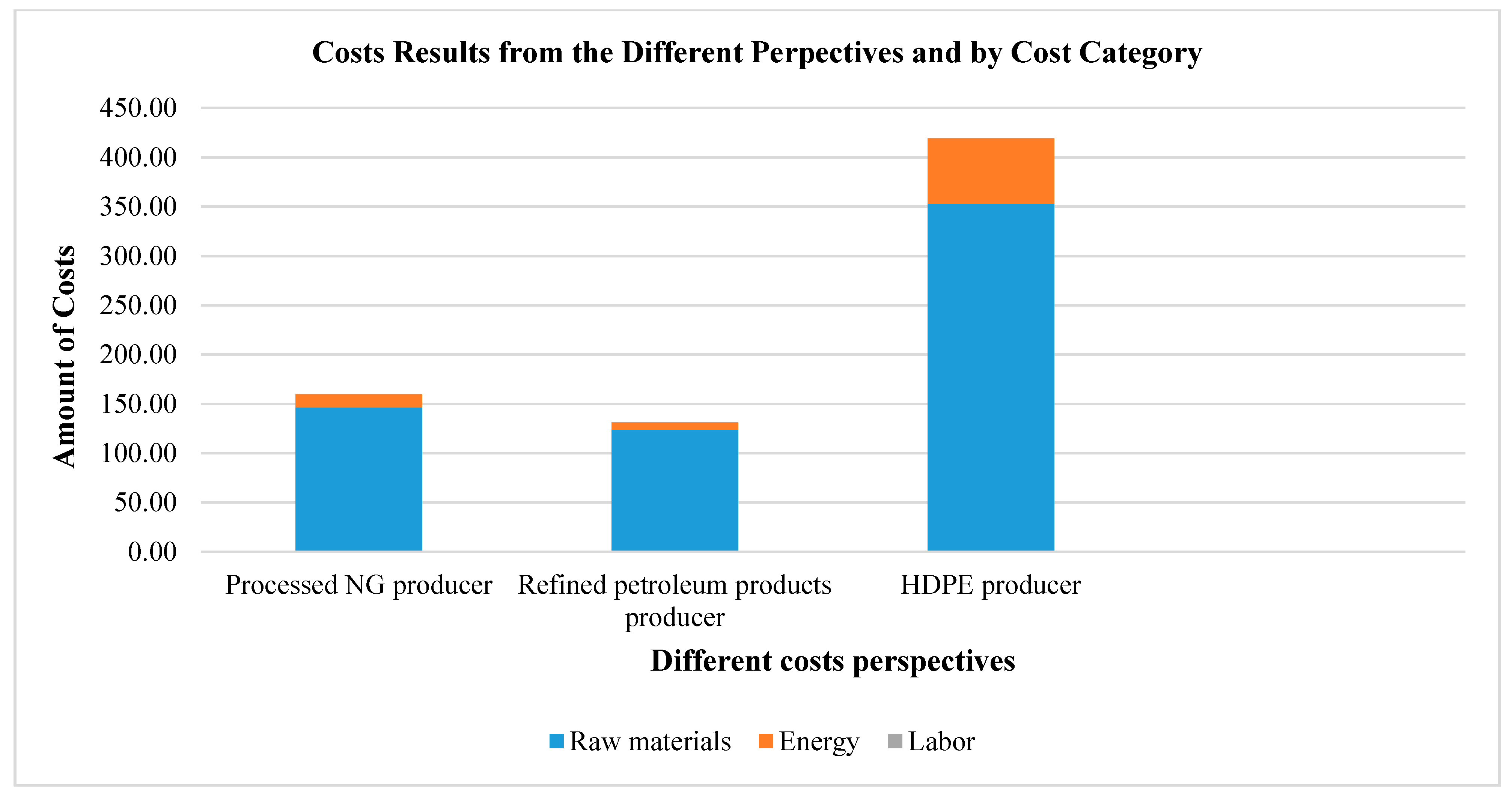

5.1.2. Economic Dimension Results

5.1.3. Social Dimension Results

5.2. Integrated Analysis of the Sustainability Results

5.2.1. Sustainability Concept

5.2.2. Integrated Solution-Oriented Approach

- -

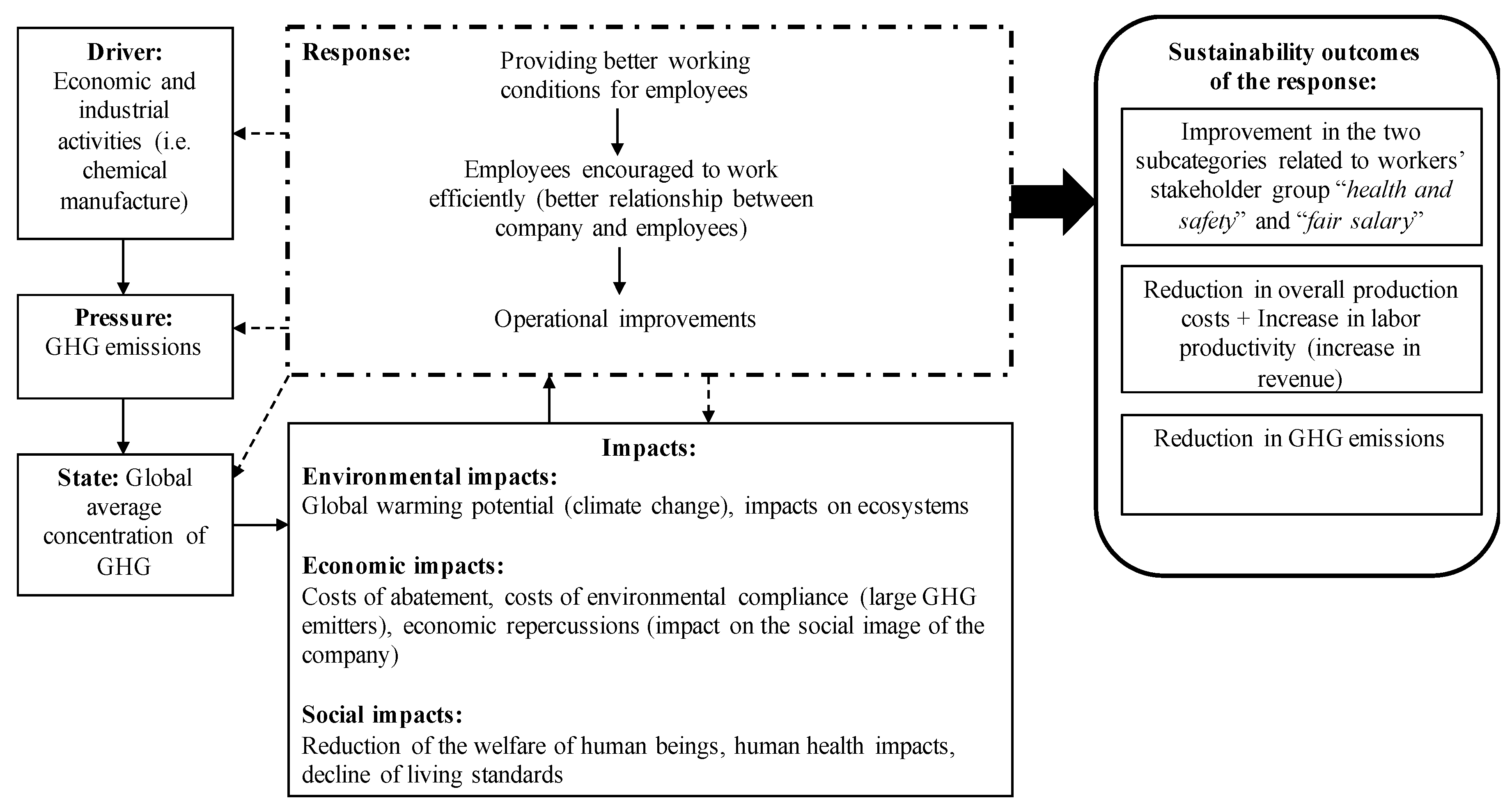

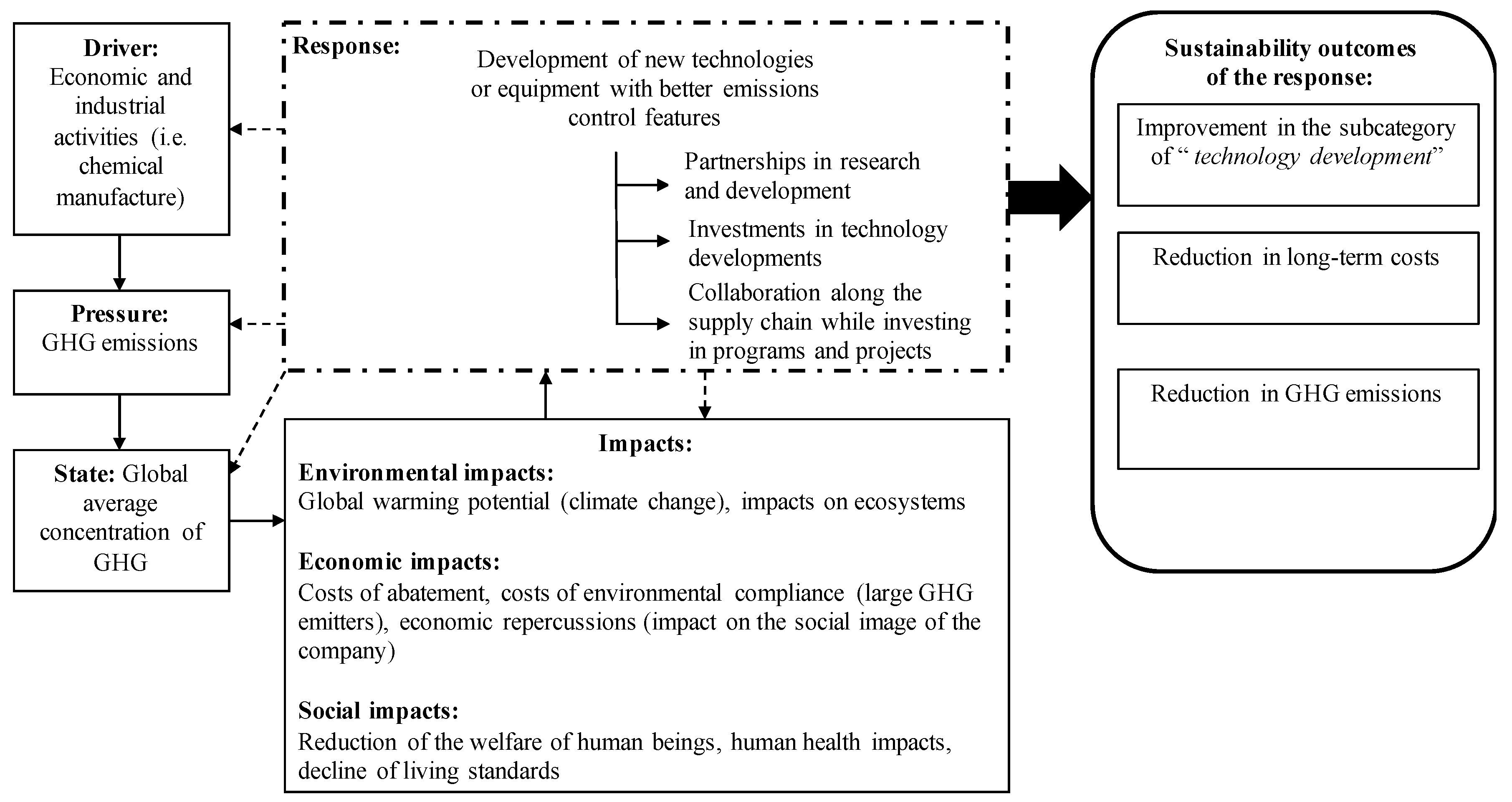

- A reduction of GHG emissions (approximately 0.05 kg CO2e per kg ethylene [30]) could be achieved by maintaining optimal operational conditions through for example process optimization that could be associated with an improvement in the working conditions for employees. For instance, providing better working conditions for employees could lead to an improvement in the subcategories related to worker’s stakeholders in S-LCA. Norris [33] has discussed the importance of information provided by S-LCA and has presented some of the benefits that companies can generate using this information. Among these advantages, Norris [33] has stated that an improvement in working conditions in the company can increase labor productivity. In addition, Nicolaescu et al. [34] have similarly argued that improving the social responsibility of companies increase the satisfaction of their employees and can ensure their long-term run.

- -

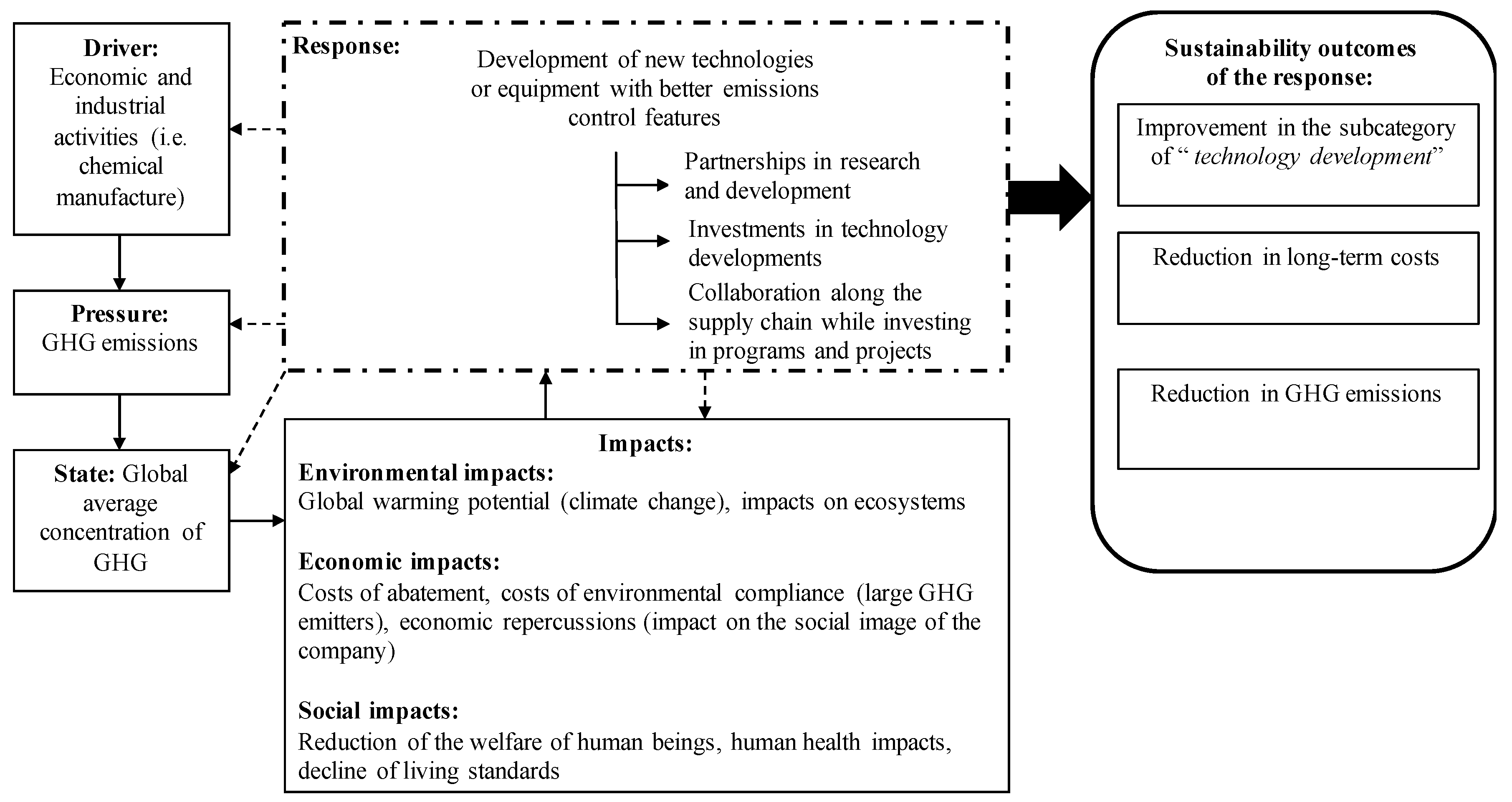

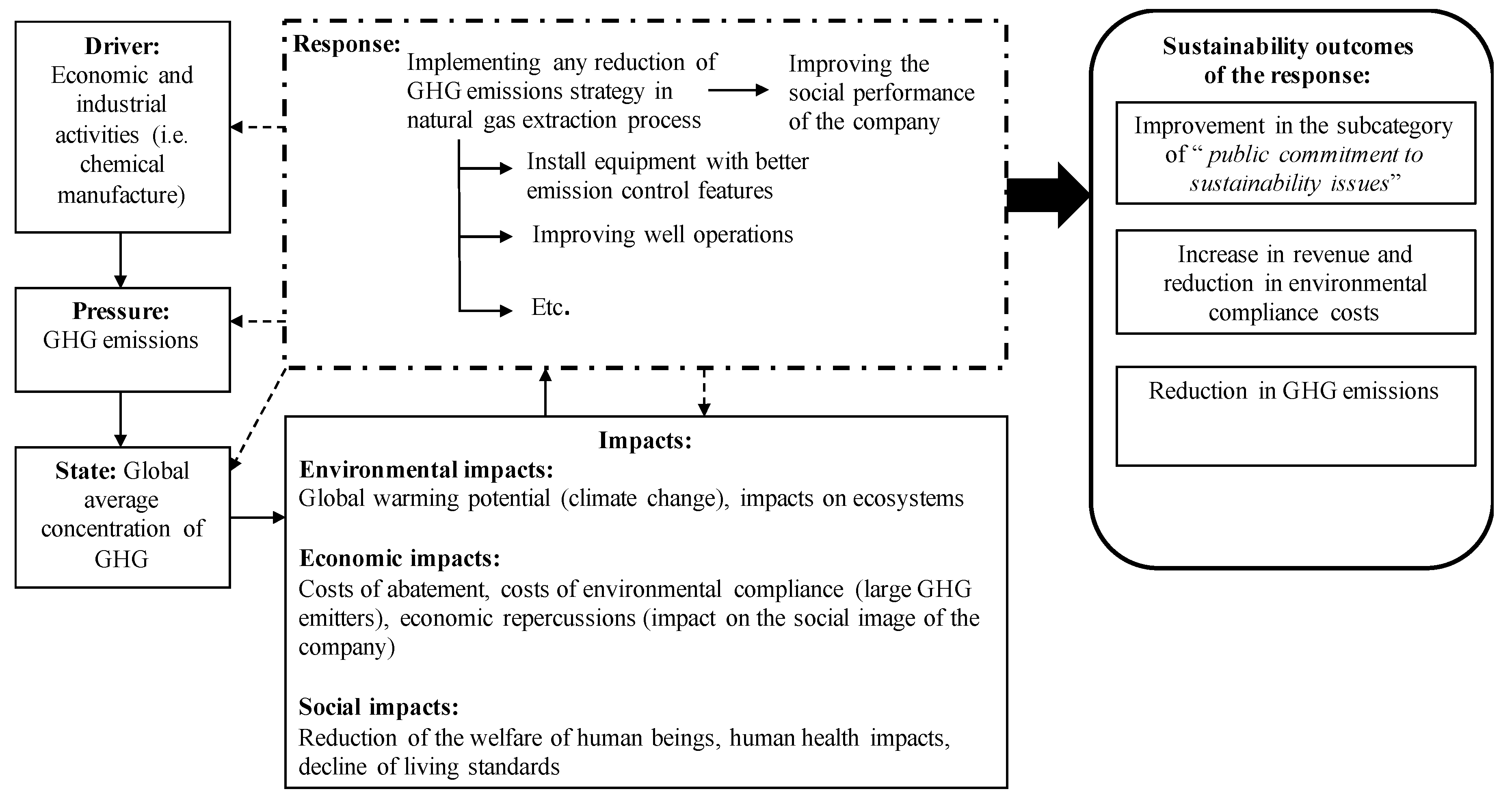

- A reduction of GHG emissions (approximately 0.2 to 0.6 kg CO2e per kg ethylene [30]) could be achieved by installing new equipment with better emission control features that could be associated with partnerships in research and development, investment in technology development and collaboration along the supply chain. For instance, these strategies could lead to an improvement in the technology development subcategory. Technology development subcategory is found to be one of the subcategories that require high level of improvements in natural gas extraction process. Therefore, we are arguing that companies need to frame developing new technologies or equipment with better emission control features through partnerships and investment in research and development as leading to a reduction in GHG emissions, and at the same time improvement in the technology development subcategory and reduction in long-term costs.

- -

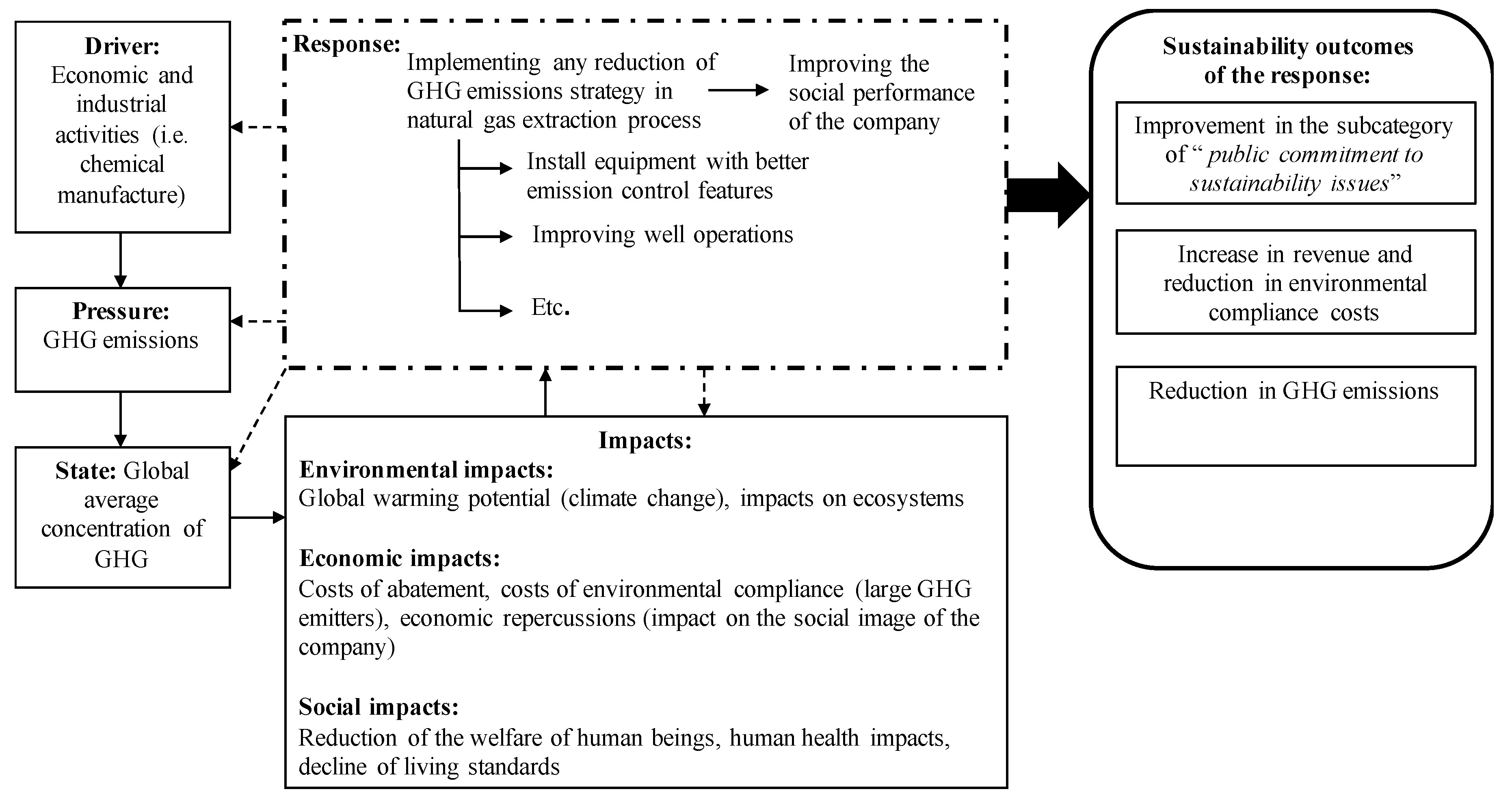

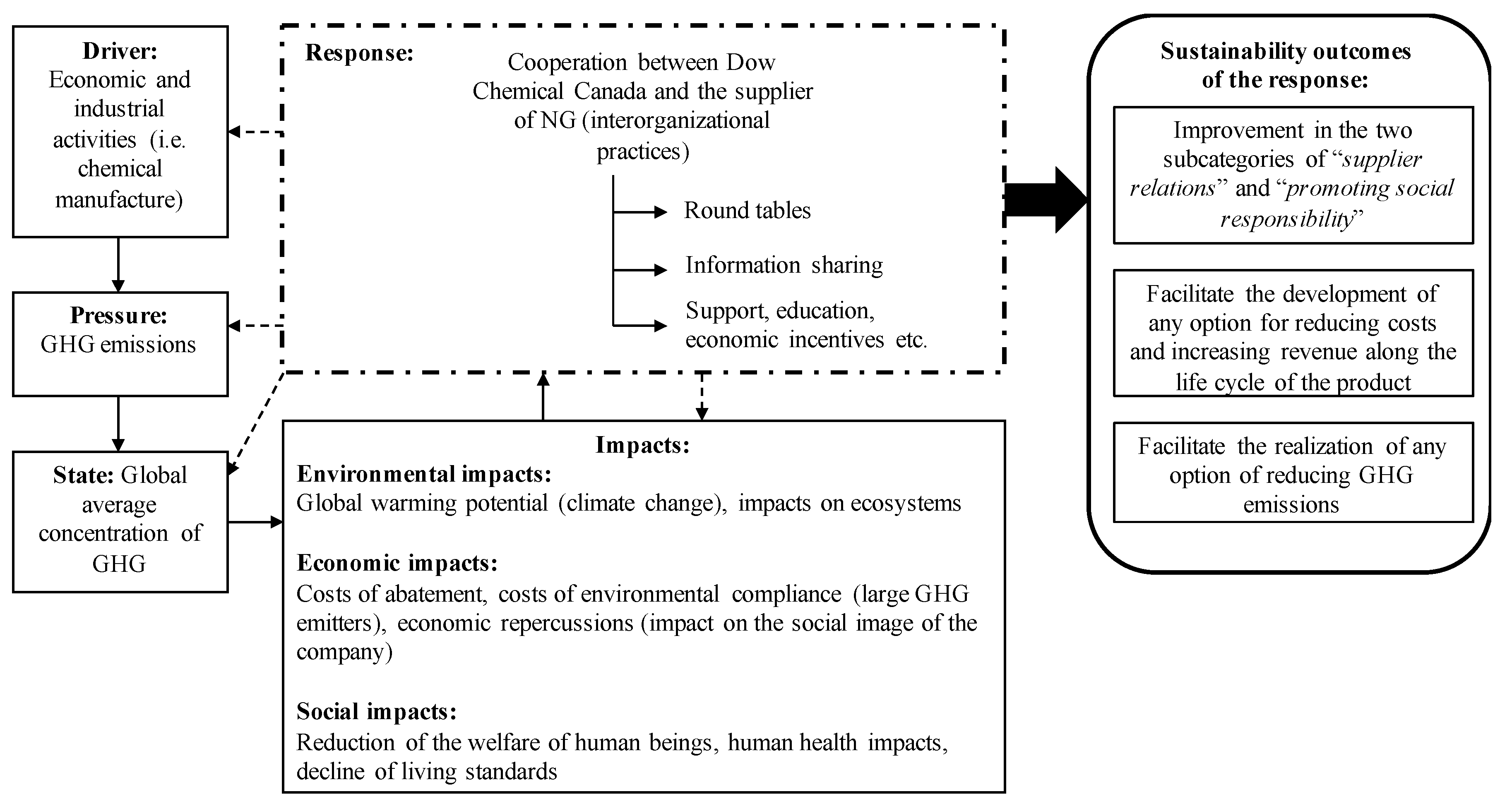

- On the other hand, any reduction of GHG emissions that could be achieved in background processes using any option mentioned in Table 2 or any other option is part of improving the social performance of the company and its social image in market. Therefore, this could lead to an improvement in the public commitment to sustainability issues subcategory which is found to be one of the subcategories that require high level of improvements in natural gas extraction process. One of the advantages that companies can gain while improving their social performance is to benefit from higher share in market and long-term profitability due to the increased demand for sustainable products [33,34]. Therefore, we are arguing that companies can successfully link any reduction in GHG emissions to lead to an improvement in the social performance of product systems and increase in the company’s revenues.

- -

- Similar to the example presented in Figure 5, a reduction in GHG emissions (approximately 0.05 kg CO2e per kg ethylene [30]) in natural gas extraction process could be achieved by improving well operations through as well process optimization that could be associated with an improvement in the working conditions for employees. As previously explained, providing better working conditions for employees could lead to an improvement in the subcategories related to worker’s stakeholders in S-LCA. Social benefits, freedom of association and discrimination subcategories are found here to be the three subcategories related to workers’ stakeholder group that need high or moderate level of improvements in natural gas extraction process. As the schematic example in this case is similar to the one presented in Figure 5, this won’t be repeated here again.

6. Discussion and Conclusions

- The interrelationships and linkages between the three groups of LCSA evaluation results in the context of achieving sustainability goals while adopting the strong sustainability perspective with a solution-oriented approach to sustainability.

- The connection between improving the social performance of the company toward increasing the well-being of its stakeholders which is the aim of S-LCA and increasing the environmental and economic performance at product system level.

- (1).

- While adopting a strong sustainability perspective, how sustainability goals on product system level could be addressed in interpreting the results of LCSA using a solution-oriented approach to sustainability problems?

- (2).

- How to use, link and interpret the LCSA results in decision-making to formulate sustainability improvement proposals in the context of strong sustainability model?

- (3).

- How improving the social well-being of companies’ stakeholders through the different subcategories presented in S-LCA is connected with improving the environmental and economic performance of product systems?

- (4).

- What type of decision-making approach is capable to handle and analyze the interdisciplinary, and different types of assessment results in LCSA and develop sustainability solutions for product systems?

- (5).

- Can a comprehensive theory about interpreting the three assessment results in an integrated approach to propose sustainability improvements in product systems be developed?

Supplementary Materials

Acknowledgments

Author Contributions

Conflicts of Interest

References

- World Commission on Environment and Development (WCED). Our Common Future; Oxford University Press: Oxford, UK, 1987. [Google Scholar]

- Zamagni, A. Life cycle sustainability assessment. Int. J. Life Cycle Assess. 2012, 17, 373–376. [Google Scholar] [CrossRef]

- Klöpffer, W. Life cycle sustainability assessment of products. Int. J. Life Cycle Assess. 2008, 13, 89–95. [Google Scholar] [CrossRef]

- UNEP; ETAC. Towards Life Cycle Sustainability Assessment: Making Informed Choices on Products. 2011. Available online: http://www.unep.org/pdf/UNEP_LifecycleInit_Dec_FINAL.pdf (accessed on 6 April 2016).

- International Organization for Standardization (ISO). Environmental Management—Life Cycle Assessment—Requirements and Guidelines; ISO 14044; ISO: Geneva, Switzerland, 2006. [Google Scholar]

- Lichtenvort, K.; Rebitzer, G.; Huppes, G.; Ciroth, A.; Seuring, S.; Schmidt, W.-P.; Günther, E.; Hoppe, H.; Swarr, T.; Hunkeler, D. Introduction—History of life cycle costing, its categorization, and its basic framework. In Environmental Life Cycle Costing; Hunkeler, D., Lichtenvort, K., Rebitzer, G., Eds.; CRC Press: Boca Raton, FL, USA; Society of Environmental Toxicology and Chemistry (SETAC): Pensacola, FL, USA, 2008; pp. 1–6. [Google Scholar]

- Hunkeler, D.; Lichtenvort, K.; Rebitzer, G. Environmental Life Cycle Costing; CRC Press: Boca Raton, FL, USA; Society of Environmental Toxicology and Chemistry (SETAC): Pensacola, FL, USA, 2008; ISBN 9781420054705. [Google Scholar]

- UNEP; SETAC. Guidelines for Social Life Cycle Assessment of Products, United Nations Environment Program, Paris SETAC Life Cycle Initiative. 2009. Available online: http://www.unep.fr/shared/publications/pdf/DTIx1164xPA-guidelines_sLCA.pdf (accessed on 4 June 2016).

- UNEP; SETAC. The Methodological Sheets for Sub-Categories in Social Life Cycle Assessment (S-LCA). 2013. Available online: http://www.lifecycleinitiative.org/wp-content/uploads/2013/11/S-LCA_methodological_sheets_11.11.13.pdf (accessed on 26 March 2016).

- Dong, Y.H.; Ng, S.T. A modeling framework to evaluate sustainability of building construction based on LCSA. Int. J. Life Cycle Assess. 2016, 21, 555–568. [Google Scholar] [CrossRef]

- Guinée, J. Life cycle sustainability assessment: What is it and what are its challenges? In Taking Stock of Industrial Ecology; Clift, R., Druckman, A., Eds.; Springer International Publishing: Cham, Switzerland, 2016; pp. 45–68. [Google Scholar]

- Sala, S.; Farioli, F.; Zamagni, A. Progress in sustainability science: Lessons learnt from current methodologies for sustainability assessment: Part 1. Int. J. Life Cycle Assess. 2013, 18, 1653–1672. [Google Scholar] [CrossRef]

- Sala, S.; Farioli, F.; Zamagni, A. Life cycle sustainability assessment in the context of sustainability science progress (Part 2). Int. J. Life Cycle Assess. 2013, 18, 1686–1697. [Google Scholar] [CrossRef]

- Basurko, O.C.; Mesbahi, E. Methodology for the sustainability assessment of marine technologies. J. Clean. Prod. 2014, 68, 155–164. [Google Scholar] [CrossRef]

- Foolmaun, R.K.; Ramjeawon, T. Life cycle sustainability assessments (LCSA) of four disposal scenarios for used polyethylene terephthalate (PET) bottles in Mauritius. Environ. Dev. Sustain. 2012, 15, 783–806. [Google Scholar] [CrossRef]

- Traverso, M.; Finkbeiner, M.; Jorgensen, A.; Schneider, L. Life cycle sustainability dashboard. J. Ind. Ecol. 2012, 16, 680–688. [Google Scholar] [CrossRef]

- Traverso, M.; Asdrubali, F.; Francia, A.; Finkbeiner, M. Toward life cycle sustainability assessment: An implementation to photovoltaic modules. Int. J. Life Cycle Assess. 2012, 17, 1068–1079. [Google Scholar] [CrossRef]

- Vinyes, E.; Oliver-Sola, J.; Ugaya, C.; Rieradeyall, J.; Gasol, C.M. Application of LCSA to used cooking oil waste management. Int. J. Life Cycle Assess. 2013, 18, 445–455. [Google Scholar] [CrossRef]

- Finkbeiner, M.; Schau, E.M.; Lehmann, A.; Traverso, M. Towards life cycle sustainability assessment. Sustainability 2010, 2, 3309–3322. [Google Scholar] [CrossRef]

- Zhang, H.; Haapala, K.R. Integrating sustainability manufacturing assessment into decision making for a production work cell. J. Clean. Prod. 2015, 105, 52–63. [Google Scholar] [CrossRef]

- CHEMINFO. Appendix B: Market Profiles for Chemicals. 2016. Available online: https://www.albertacanada.com/files/albertacanada/BioBased-Chemical-Import-Replacement-Report_8.Appendix-B-Market-Profiles-for-Chemicals.pdf (accessed on 19 May 2016).

- GIS Mapping and Data Services. Petrochemicals in Alberta. 2008. Available online: http://www.energy.alberta.ca/EnergyProcessing/pdfs/Petrochemicals_brochure_overview.pdf (accessed on 18 May 2016).

- Hannouf, M.; Assefa, G. Subcategory assessment method for social life cycle assessment: A case study of high-density polyethylene production in Alberta, Canada. Int. J. Life Cycle Assess. 2017, 1–17. [Google Scholar] [CrossRef]

- Swarr, T.E.; Hunkeler, D.; Klöpffer, W.; Pesonen, H.; Ciroth, A.; Brent, A.C.; Pagan, R. Environmental Life-Cycle Costing: A Code of Practice; Society of Environmental Toxicology and Chemistry (SETAC): New York, NY, USA, 2011. [Google Scholar]

- Klöpffer, W.; Ciroth, A. Is LCC relevant in a sustainability assessment? Answer to a letter to the editor. Int. J. Life Cycle Assess. 2011, 16, 99–101. [Google Scholar] [CrossRef]

- Daly, H.E. Ecological Economics and Sustainable Development, Selected Essays of Herman Daly; Edward Elgar Publishing Limited: Cheltenham, UK, 2007; ISBN 978-1-84720-101-0. [Google Scholar]

- Neumayer, E. Weak versus Strong Sustainability: Exploring the Limits of Two Opposing Paradigms; Edward Elgar Publishing Limited: Cheltenham, UK, 2013. [Google Scholar]

- Daly, H.E. Beyond Growth: The Economics of Sustainable Development; Beacon Press: Boston, MA, USA, 1996. [Google Scholar]

- Ott, K. The case for strong sustainability. In Greifswald’s Environmental Ethics; Ott, K., Thappa, P.P., Eds.; Steinbecker Verlag Ulrich Rose: Greifswald, Germany, 2003; pp. 59–64. [Google Scholar]

- Yao, Y.; Graziano, D.J.; Riddle, M.; Cresko, J.; Masanet, E. Understanding variability to reduce the energy and GHG footprints of U.S. ethylene production. Environ. Sci. Technol. 2015, 48, 14704–14716. [Google Scholar] [CrossRef] [PubMed]

- Ness, B.; Anderberg, S.; Olsson, L. Structuring problems in sustainability science: The multi-level DPSIR framework. Geoforum 2010, 41, 479–488. [Google Scholar] [CrossRef]

- Sun, S.; Wang, Y.; Liu, J.; Cai, H.; Wu, P.; Geng, Q.; Xu, L. Sustainability assessment of regional water resources under the DPSIR framework. J. Hydrol. 2016, 532, 140–148. [Google Scholar] [CrossRef]

- Norris, C.B. Social life cycle assessment: A technique providing a new wealth of information to inform sustainability-related decision making. In Life Cycle Assessment Handbook: A Guide for Environmentally Sustainable Products; Curran, M.A., Ed.; John Wiley and Sons: Hoboken, NJ, USA, 2012; pp. 433–452. [Google Scholar]

- Nicolaescu, E.; Alpopi, C.; Zaharia, C. Measuring corporate sustainability performance. Sustainability 2015, 7, 851–865. [Google Scholar] [CrossRef]

- Slagmulder, R. Managing costs across the supply chain. In Cost Management in Supply Chains; Seuring, S., Goldbach, M., Eds.; Physica-Verlag: Heidelberg, Germany; New York, NY, USA, 2002; pp. 75–88. [Google Scholar]

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Life Cycle Stages | |||||

|---|---|---|---|---|---|

| Foreground Processes | Background Processes | ||||

| Subcategories | Ethylene Production and HDPE Production | NG Extraction and Crude Oil Extraction | Refining Petroleum Products | NG Processing | Transportation |

| Freedom of association and collective bargaining | HI | MI | MI | HI | |

| Child labor | |||||

| Forced labor | |||||

| Equal opportunities/discrimination | MI | MI | MI | MI | |

| Health and safety (workers) | HI | HI | |||

| Social benefits/social security | MI | ||||

| Fair salary | HI | ||||

| Working hours | - | ||||

| Health and safety (consumers) | HI | ||||

| Feedback mechanism | - | - | - | - | - |

| Privacy | MI | MI | MI | MI | |

| Transparency | HI | ||||

| End of life responsibility | HI | ||||

| Supplier relations | - | - | - | - | - |

| Promoting social responsibility | - | - | - | - | - |

| Fair competition | MI | HI | |||

| Respect of intellectual property | HI | ||||

| Cultural heritage | HI | ||||

| Respect of indigenous rights | HI | HI | HI | HI | |

| Local employment | MI | MI | MI | MI | MI |

| Delocalization and migration | - | MI | MI | MI | MI |

| Access to immaterial resources | HI | HI | HI | HI | |

| Access to material resources | HI | HI | MI | ||

| Secure living conditions | HI | ||||

| Community engagement | |||||

| Safe and healthy living conditions | HI | ||||

| Public commitment to sustainability issues | HI | HI | HI | HI | |

| Contribution to economic development | |||||

| Technology development | HI | HI | HI | HI | |

| Prevention and mitigation of conflicts | HI | ||||

| Corruption | HI | HI | HI | HI | |

| GHG Emission Reduction Opportunities in Ethylene Production Process | GHG Emission Reduction Opportunities in Natural Gas Extraction Process |

|---|---|

|

|

| HDPE Production Processes | GHG Reduction Options—Approximate Amount of GHG Reduction in CO2e | Social Subcategories | Economic Opportunities |

|---|---|---|---|

| Foreground processes (i.e., ethylene production) |

|

|

|

| Background processes (i.e., NG extraction) |

|

| |

| Collaboration between foreground and background processes |

|

|

|

© 2017 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

Hannouf, M.; Assefa, G. Life Cycle Sustainability Assessment for Sustainability Improvements: A Case Study of High-Density Polyethylene Production in Alberta, Canada. Sustainability 2017, 9, 2332. https://doi.org/10.3390/su9122332

Hannouf M, Assefa G. Life Cycle Sustainability Assessment for Sustainability Improvements: A Case Study of High-Density Polyethylene Production in Alberta, Canada. Sustainability. 2017; 9(12):2332. https://doi.org/10.3390/su9122332

Chicago/Turabian StyleHannouf, Marwa, and Getachew Assefa. 2017. "Life Cycle Sustainability Assessment for Sustainability Improvements: A Case Study of High-Density Polyethylene Production in Alberta, Canada" Sustainability 9, no. 12: 2332. https://doi.org/10.3390/su9122332

APA StyleHannouf, M., & Assefa, G. (2017). Life Cycle Sustainability Assessment for Sustainability Improvements: A Case Study of High-Density Polyethylene Production in Alberta, Canada. Sustainability, 9(12), 2332. https://doi.org/10.3390/su9122332