Integrated Evaluation Method-Based Technical and Economic Factors for International Oil Exploration Projects

Abstract

:

1. Introduction

2. Analysis of Influence Factors for International Oil Exploration Projects

2.1. The Technical Factors Affecting Investment Benefits

2.1.1. Geological Factors

2.1.2. Resource Quality

2.1.3. Geographic Conditions

2.2. The Economic Factors Affecting Investment Benefits

2.2.1. Contract Terms

2.2.2. Investment Environment

3. Approach

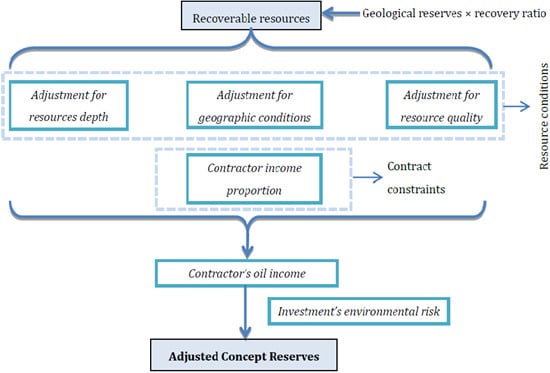

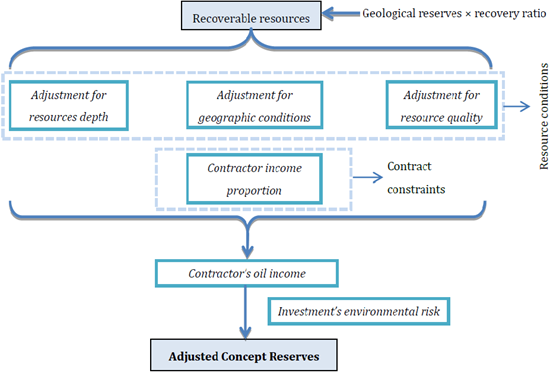

3.1. The Determination of Residual Recoverable Reserves

3.2. Adjustment for Different Resource Conditions

3.2.1. The Weight of the Influence of Resource Depth and the Adjustment of N2

3.2.2. The Weight of Influence of Geographic Conditions and the Adjustment of N2

3.2.3. Adjustment for Different Resource Quality

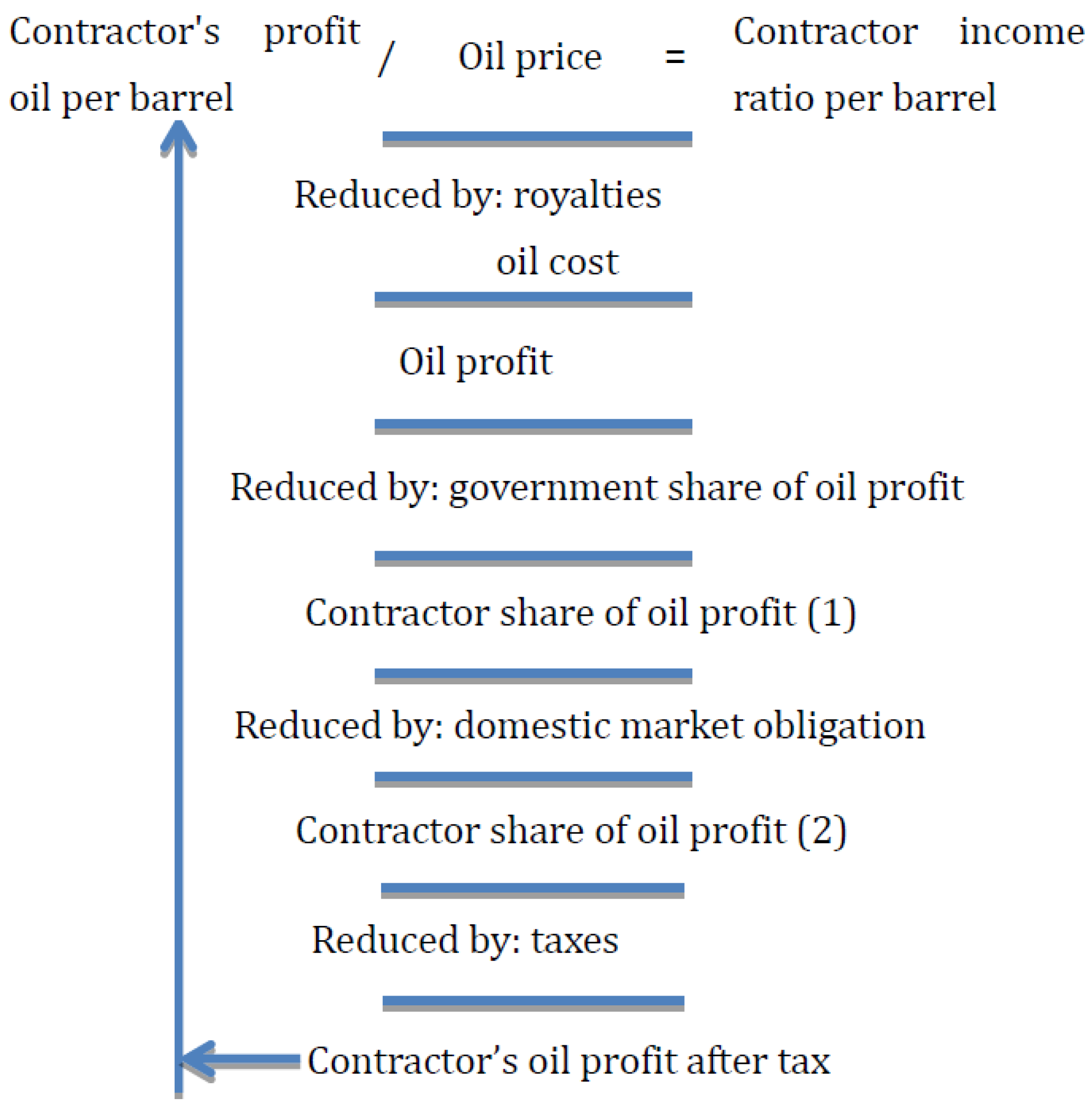

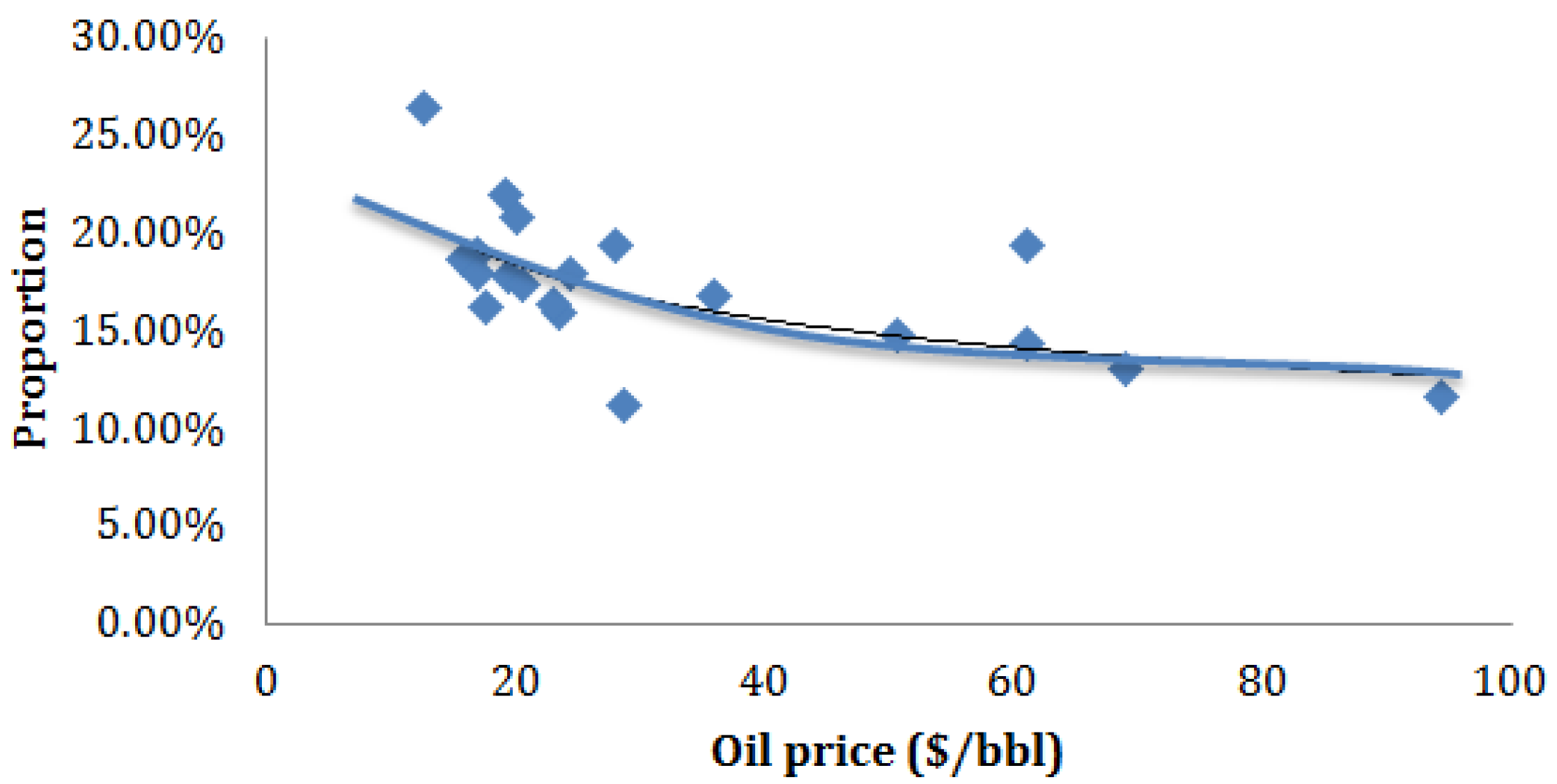

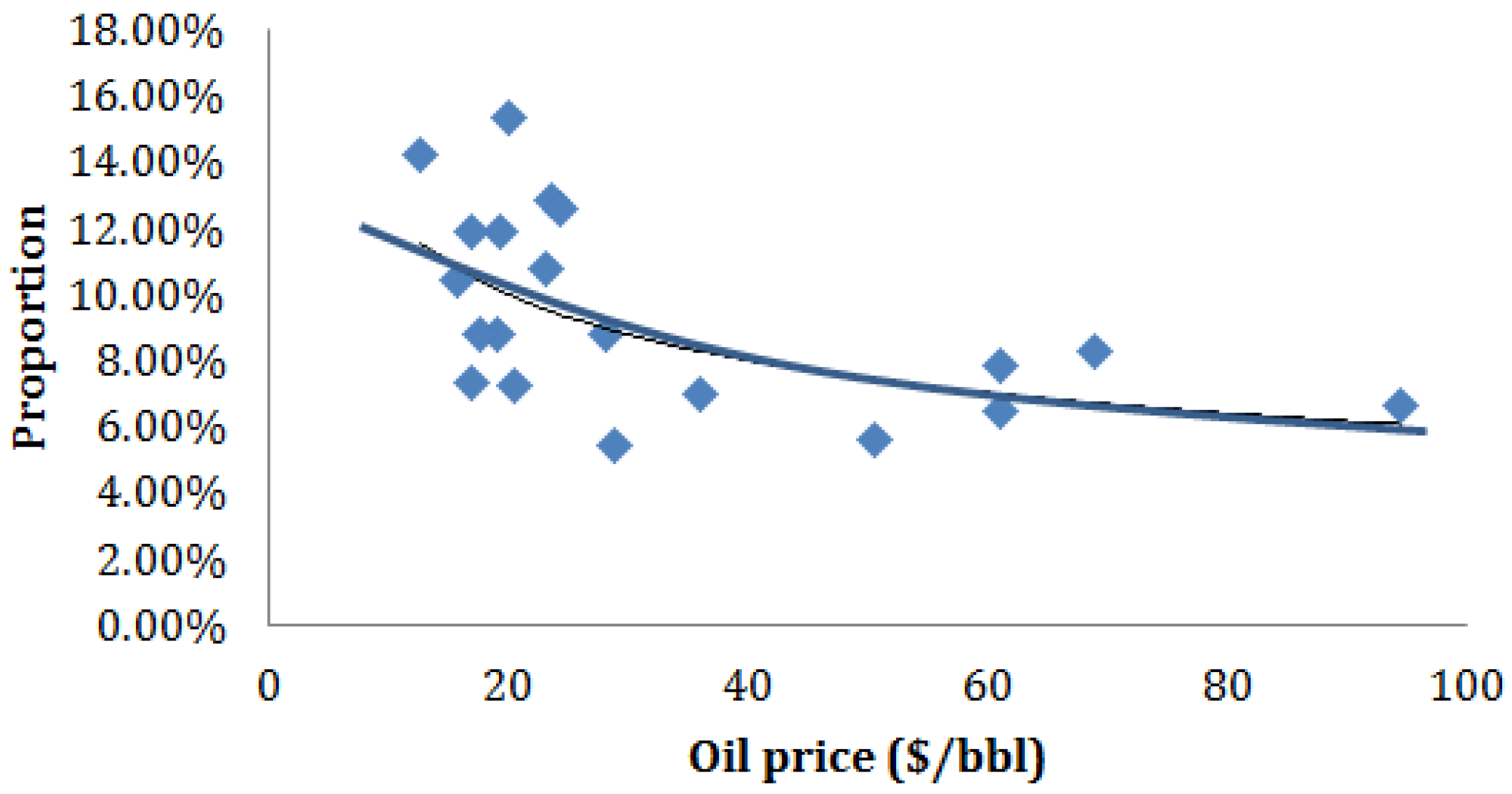

3.3. Calculation of the Contractor Income Ratio

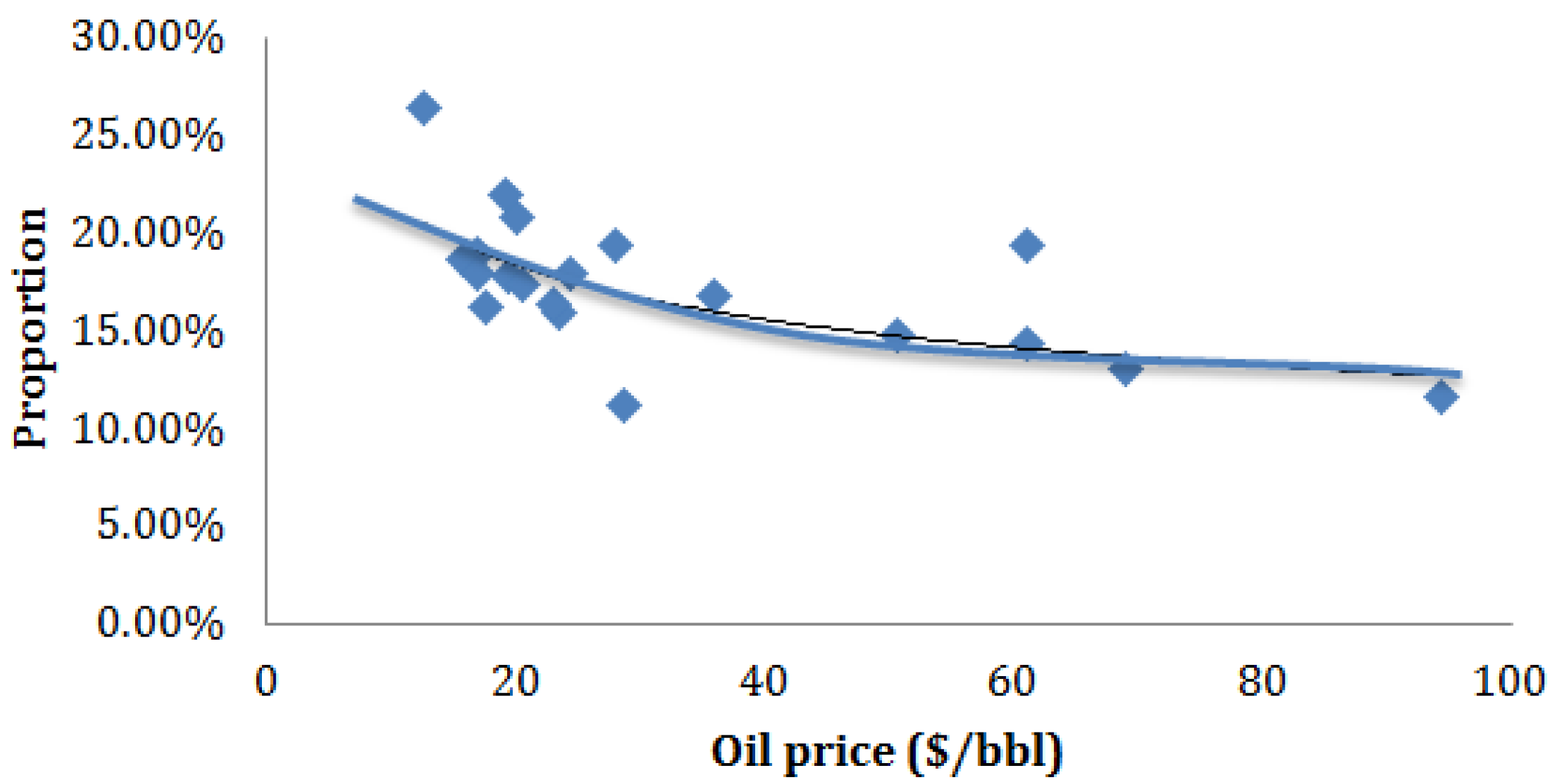

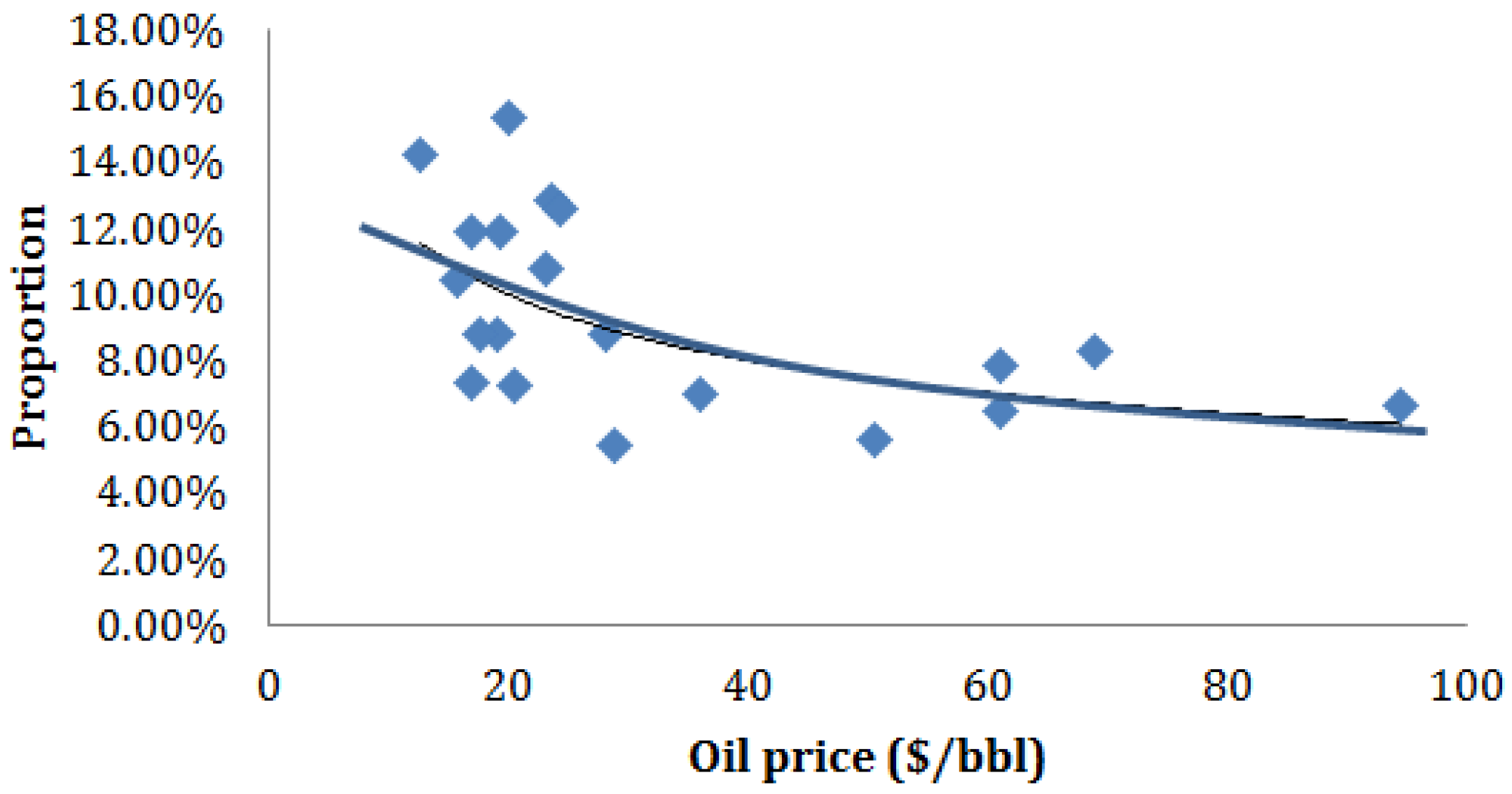

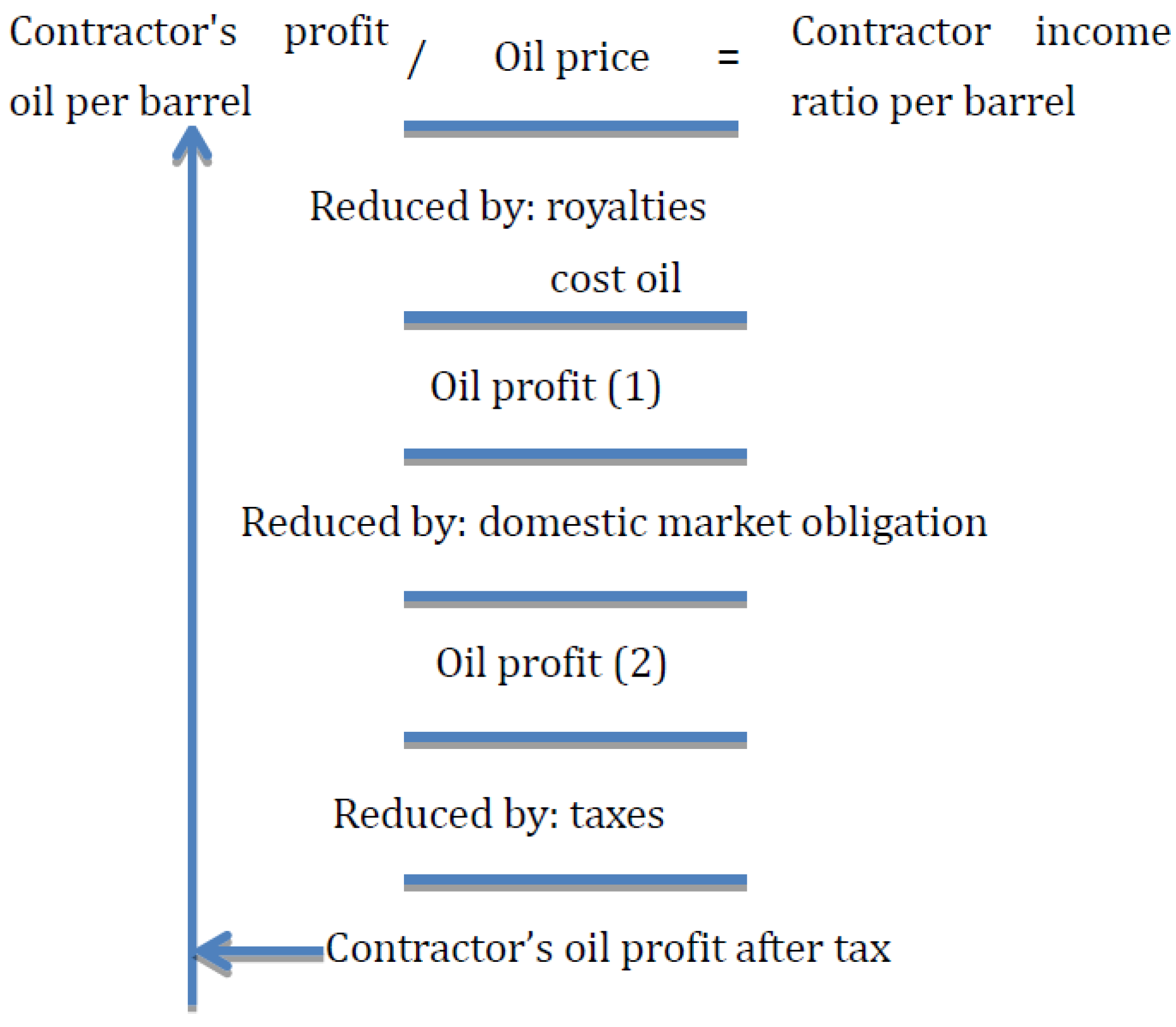

3.3.1. Royalty Contracts

- (1)

- Pay royalties to the government. Royalties should first be deducted from the total oil production revenue; royalty rates vary widely between countries.

- (2)

- The cost recovery of the contractor. This amount includes production costs, depreciation, depletion, amortization, and intangible capital costs. Some countries allow deduction of the deposit.

- (3)

- Pay taxes to the government. Oil production revenue less deductions for royalties and costs is taxable income. The types of taxes and tax rates vary widely between countries.

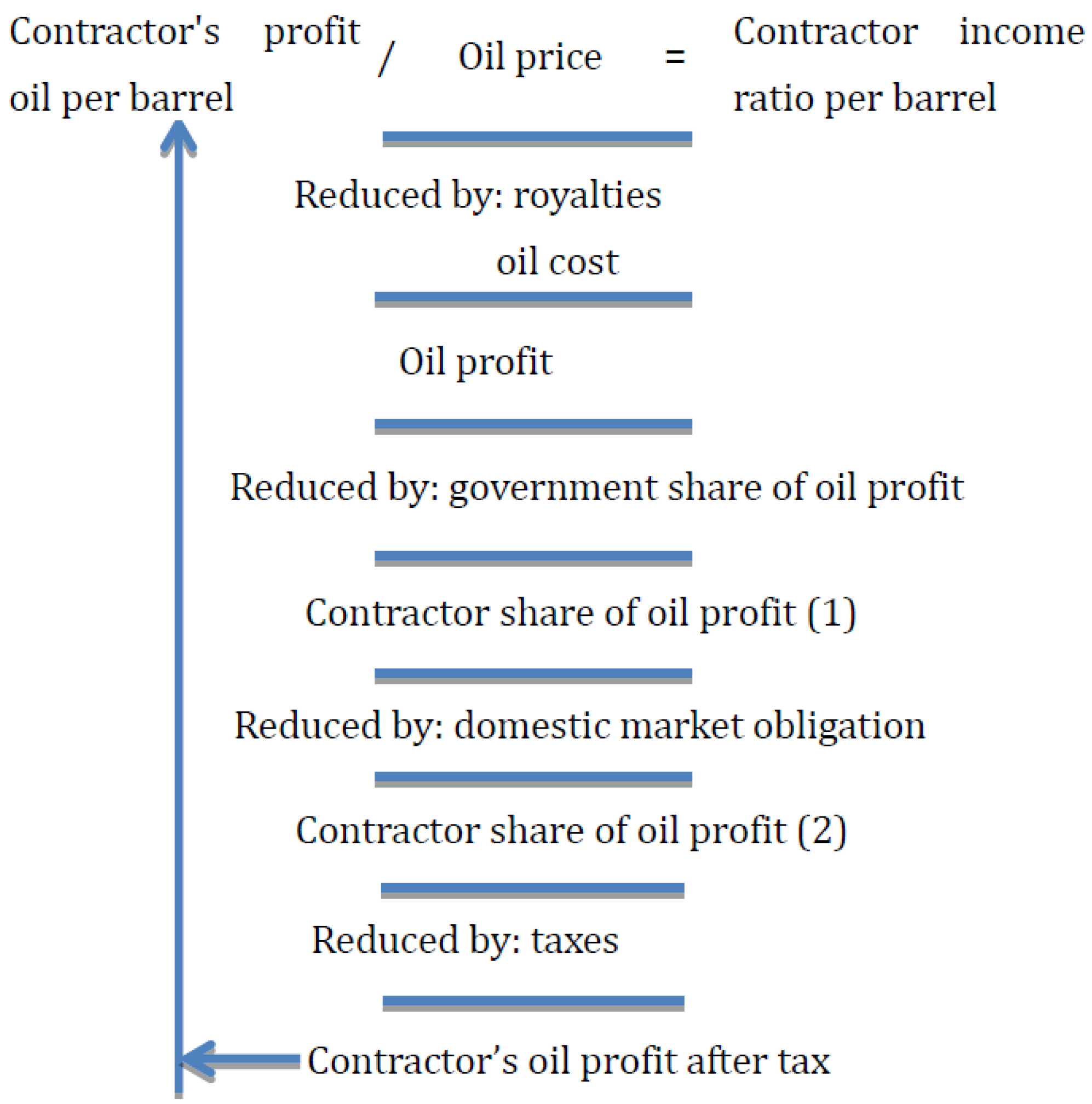

3.3.2. Production Sharing Contracts

- (1)

- Pay royalties to the government, like with royalty contract.

- (2)

- The cost recovery of the contractor. A production sharing contract sets a cost recovery limit. The unrecovered cost beyond the limit can be carried forward.

- (3)

- Oil profit-sharing. After removing the royalties paid to the government and the contractor’s oil recovery costs, the remainder is oil profit; this amount is divided based on the ratio stipulated in the contract between the host country and the contractors.

- (4)

- Tax. The contractor must pay taxes on its oil profits according to the provisions of the host country.

3.4. Adjustment for the Investment Environment Risk

3.5. The Evaluation Model of International Oil Projects

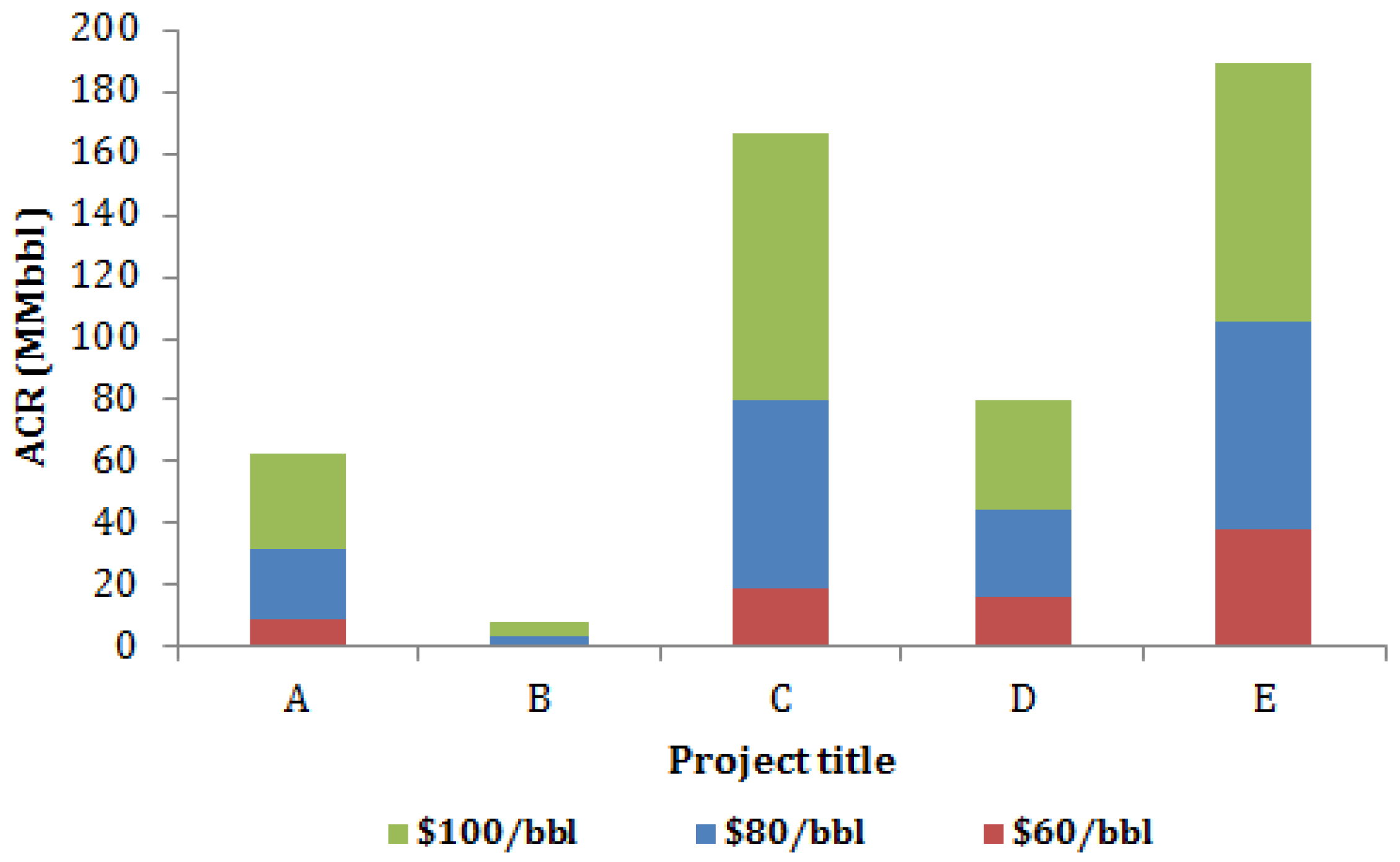

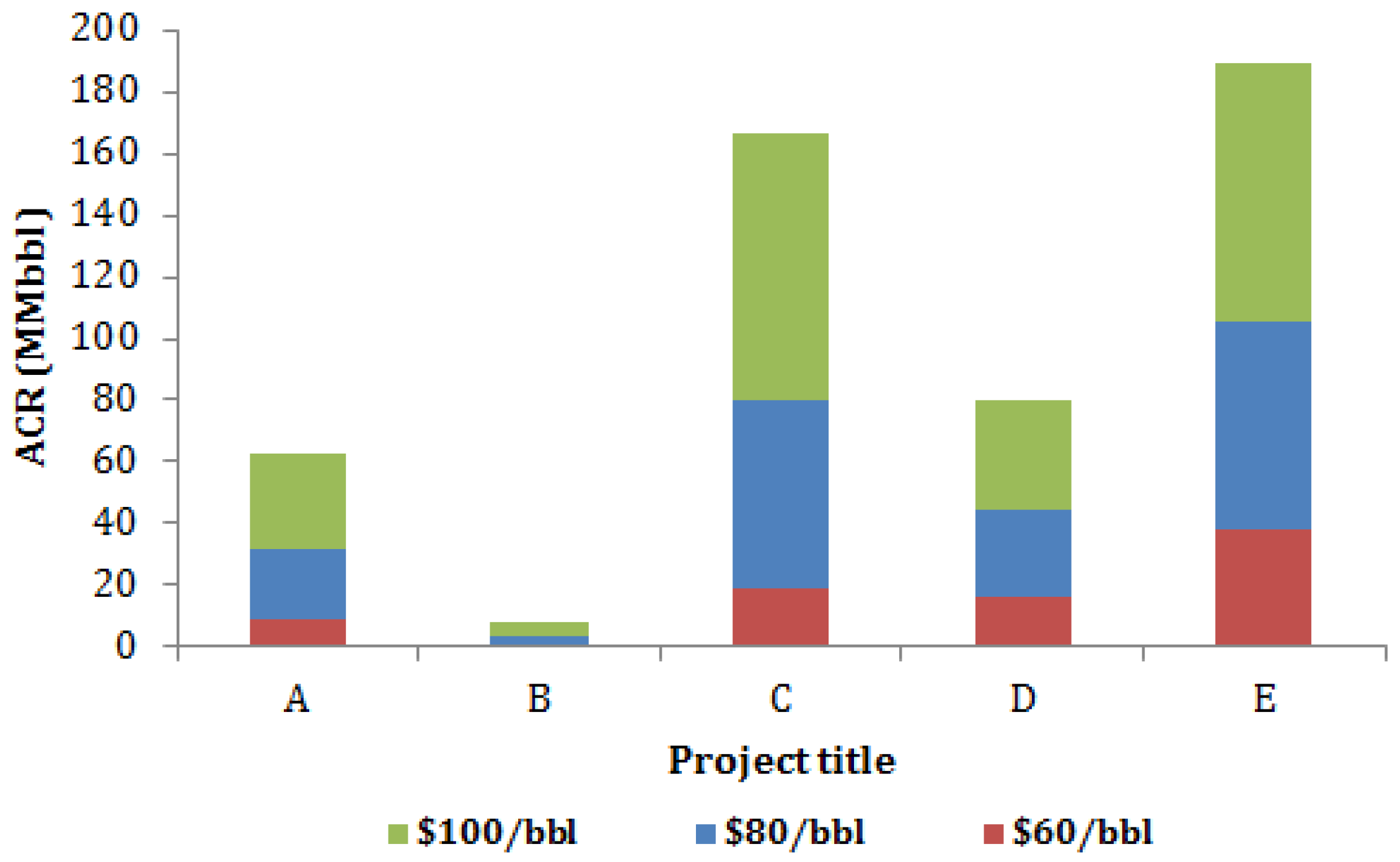

4. Example

5. Conclusions

Acknowledgments

Author Contributions

Conflicts of Interest

Nomenclature

| N0 | is geological reserves |

| N1 | is recoverable resources |

| N2 | is the remaining recoverable resources |

| f1 | denotes the recovery ratio for different types of reservoirs |

| f2 | denotes the recovery percentage of the reserves |

| Sdepth | represents the adjustment coefficient of different reservoir depths |

| m | is the proportion of the total costs associated with the resource depth (including drilling investment and the operating costs associated with well depth) in sales revenue |

| h | is the resource depth of the target project |

| h0 | is the average resource depth |

| Sg | represents the adjustment factor for different geographic conditions |

| e | is the proportion of ground construction investment over sales revenue |

| d | is the adjustment factor for ground construction investment for different landforms |

| f | is the adjustment factor for ground construction investment for different types of infrastructure |

| s | is a subjective adjustment factor. |

| IOC% | represents the contractor income ratio |

| Cr | is the recycling oil cost per barrel |

| p | is the oil price |

| ROY | is the royalties |

| DMO | is the domestic market obligation |

| TAX | is the amount of taxes in the contract |

| Rg | is the government’s share of the oil profit |

| fe | represents the risk adjustment factor of the investment environment |

| b | is the risk-adjusted weight of the investment environment |

| R | is the national competitiveness index |

| Rh | is the maximum of the competitiveness index |

| se | is the subjective adjustment factor |

| N* | represents the Adjusted Concept Reserves |

References

- BP. BP Statistical Review of World Energy 2014. Available online: http://www.bp.com/content/dam/bp-country/de_de/PDFs/brochures/BP-statistical-review-of-world-energy-2014-full-report.pdf (accessed on 17 February 2016).

- Charlez, P. Acceptability of New Oil & Gas Projects and Reputation Management. A Major Challenge for the International Oil Companies; Society of Petroleum Engineers: Richardson, TX, USA, 2012. [Google Scholar]

- Wang, Q.; Wang, J. The issues of overseas oil and gas exploration and new project development. China Pet. Explor. 2012, 4, 47–52. (In Chinese) [Google Scholar]

- Otillar, S.P. Risk Mitigation in International Oil & Gas Developments. In Proceedings of the Offshore Technology Conference, Houston, TX, USA, 3–6 May 2010.

- Walls, M.R.; Dyer, J.S. Risk Propensity and Firm Performance: A Study of the Petroleum Exploration Industry. Manag. Sci. 1996, 42, 1004–1021. [Google Scholar] [CrossRef]

- Clare, J.B.; Armstrong, L.J. Comprehensive Risk Evaluation Approaches for International E&P Operations; Society of Petroleum Engineers: Richardson, TX, USA, 2006. [Google Scholar]

- Emhjellen, M.; Alaouze, C.M. A comparison of discounted cashflow and modern asset pricing methods—Project selection and policy implications. Energy Policy 2003, 31, 1213–1220. [Google Scholar] [CrossRef]

- Emhjellen, M.; Alaouze, C.M. Project valuation when there are two cashflow streams. Energy Econ. 2002, 24, 455–467. [Google Scholar] [CrossRef]

- Brealey, R.A.; Myers, S.C. Principles of Corporate Finance; McGraw-Hill: New York, NY, USA, 1991. [Google Scholar]

- Frenette, C.T.; Saeedi, M.; Henke, J.L. Integrated Economic Model for Evaluation and Optimization of Cyclic Steam Stimulation Projects; Society of Petroleum Engineers: Richardson, TX, USA, 2016. [Google Scholar]

- Luo, D.K.; Dai, Y.J.; Xia, L.Y. Economic evaluation based policy analysis for coalbed methane industry in China. Energy 2011, 36, 360–368. [Google Scholar] [CrossRef]

- Dias, M.A.G. Valuation of exploration and production assets: An overview of real options models. J. Petrol. Sci. Eng. 2004, 44, 93–114. [Google Scholar] [CrossRef]

- Ho, S.-H.; Liao, S.-H. A fuzzy real option approach for investment project valuation. Expert. Syst. Appl. 2011, 38, 15296–15302. [Google Scholar] [CrossRef]

- Armstrong, M.; Galli, A.; Bailey, W.; Couët, B. Incorporating technical uncertainty in real option valuation of oil projects. J. Petrol. Sci. Eng. 2004, 44, 67–82. [Google Scholar] [CrossRef]

- Haque, M.A.; Topal, E.; Lilford, E. A numerical study for a mining project using real options valuation under commodity price uncertainty. Resour. Pol. 2014, 39, 115–123. [Google Scholar] [CrossRef]

- Amiri, M.P. Project selection for oil-fields development by using the AHP and fuzzy TOPSIS methods. Expert. Syst. Appl. 2010, 37, 6218–6224. [Google Scholar] [CrossRef]

- Liu, J.; Li, Q.; Wang, Y. Risk analysis in ultra deep scientific drilling project—A fuzzy synthetic evaluation approach. Int. J. Inform. Tech. Proj. Manag. 2013, 31, 449–458. [Google Scholar] [CrossRef]

- Shakhsi-Niaei, M.; Iranmanesh, S.H.; Torabi, S.A. Optimal planning of oil and gas development projects considering long-term production and transmission. Comput. Chem. Eng. 2014, 65, 67–80. [Google Scholar] [CrossRef]

- Dong, Z.; Zhen, W.; Lin, Z.; Ming-ming, L.I.U. Construction and application of risk rating and ranking model for international oil and gas exploration & production projects. J. China Univ. Petrol. Ed. Natrual Sci. 2010, 34, 164–169. [Google Scholar]

- Dey, P.K. Integrated project evaluation and selection using multiple-attribute decision-making technique. Int. J. Prod. Econ. 2006, 103, 90–103. [Google Scholar] [CrossRef]

- Di Somma, M.; Yan, B.; Bianco, N.; Graditi, G.; Luh, P.B.; Mongibello, L.; Naso, V. Operation optimization of a distributed energy system considering energy costs and exergy efficiency. Energ. Convers. Manag. 2015, 103, 739–751. [Google Scholar] [CrossRef]

- Castillo, L.; Dorao, C.A. Decision-making in the oil and gas projects based on game theory: Conceptual process design. Energ. Convers. Manag. 2013, 66, 48–55. [Google Scholar] [CrossRef]

- Rao, S.S. Game theory approach for multiobjective structural optimization. Comput. Struct. 1987, 25, 119–127. [Google Scholar] [CrossRef]

- Bhattacharya, A.; Kojima, S. Power sector investment risk and renewable energy: A Japanese case study using portfolio risk optimization method. Energy Policy 2012, 40, 69–80. [Google Scholar] [CrossRef]

- Arnesano, M.; Carlucci, A.P.; Laforgia, D. Extension of portfolio theory application to energy planning problem—The Italian case. Energy 2012, 39, 112–124. [Google Scholar] [CrossRef]

- Delarue, E.; De Jonghe, C.; Belmans, R.; D’Haeseleer, W. Applying portfolio theory to the electricity sector: Energy versus power. Energy Econ. 2011, 33, 12–23. [Google Scholar] [CrossRef]

- Dutra, C.C.; Ribeiro, J.L.D.; de Carvalho, M.M. An economic–probabilistic model for project selection and prioritization. Int. J. Prod. Econ. 2014, 32, 1042–1055. [Google Scholar] [CrossRef]

- Kemp, A.G.; Stephen, L. Price, cost and exploration sensitivities of prospective activity levels in the UKCS: An application of the Monte Carlo technique. Energy Policy 1999, 27, 801–810. [Google Scholar] [CrossRef]

- Terry, R.E.; Whitman, D.L.; Page, J.B. Monte Carlo Simulation of Heavy Oil Recovery Economics. In Energy Developments: New Forms, Renewables, Conservation; Curtis, F.A., Ed.; Pergamon Press, Ltd.: Oxford, UK, 1984; pp. 71–74. [Google Scholar]

- Wang, P.; Li, Z. The research of dynamic cost models for oil and gas reserves. J. Xi’an Petrol. Univ. 2004, 3, 35–39. (In Chinese) [Google Scholar]

- Ma, H. Differences analysis of economic evaluation methods for overseas oil and gas exploration project. Petrol. Petrochemical Today 2008, 7, 30–33. (In Chinese) [Google Scholar]

- Zuo, D.; Zhao, Y.-P.; Du, C. Average incremental cost method and its application in evaluation of undeveloped reserves. Fault-Block Oil Gas Field 2012, 2, 232–236. (In Chinese) [Google Scholar]

- Cheng, L.; Liu, B.; Rao, K. Economic Optimization Program and Risk Factors Analysis of Oil and Gas Cooperation; China Energy Strategy Research Center, China University of Petroleum: Beijing, China, 2009. (In Chinese) [Google Scholar]

- He, Y.; Zhao, H. An Introduction to the Oil Industry; Petroleum Industry Press: Beijing, China, 2006. (In Chinese) [Google Scholar]

- Lu, M.; Cheng, Y. Regulation of Petroleum Reserves Estimation; Ministry of Land and Resources of the People’s Republic of China: Beijing, China, 2005. (In Chinese)

- Luo, D.; Yan, N. Assessment of fiscal terms of international petroleum contracts. Petrol. Explor. Dev. 2010, 37, 756–762. [Google Scholar] [CrossRef]

- Feng, Z.; Zhang, S.-B.; Gao, Y. On oil investment and production: A comparison of production sharing contracts and buyback contracts. Energy Econ. 2014, 42, 395–402. [Google Scholar] [CrossRef]

- Zhao, X.; Luo, D.; Xia, L. Modelling optimal production rate with contract effects for international oil development projects. Energy 2012, 45, 662–668. [Google Scholar] [CrossRef]

- Ge, A.; Guo, P.; Xu, H. Theory & Practice of International Oil Cooperation; Petroleum Industry Press: Beijing, China, 2004. (In Chinese) [Google Scholar]

- China National Petroleum Corporation (CNPC). Long-Distance Pipeline Engineering Manual; CNPC: Beijing, China, 2010. (In Chinese) [Google Scholar]

- Forum, W.E. Global Competitiveness Report; World Economic Forum: Geneva, Switzerland, 2014. [Google Scholar]

- Creti, A.; Ftiti, Z.; Guesmi, K. Oil price and financial markets: Multivariate dynamic frequency analysis. Energy Policy 2014, 73, 245–258. [Google Scholar] [CrossRef]

- Katircioglu, S.T.; Sertoglu, K.; Candemir, M.; Mercan, M. Oil price movements and macroeconomic performance: Evidence from twenty-six OECD countries. Renew Sustain. Energ. Rev. 2015, 44, 257–270. [Google Scholar] [CrossRef]

- Reuters. Platts Price. Available online: http://www.platts.com/products/market-data-oil (accessed on 18 February 2016).

- Zheng, L.; Liang, H. World Oil Industry Statistics 2012; China National Petroleum Corporation (CNPC) Economic & Technical Research Institute: Beijing, China, 2012. (In Chinese) [Google Scholar]

- U.S. Energy Information Administration (EIA). Financial Report System. Available online: http://www.eia.gov/cfapps/frs/frstables.cfm (accessed on 18 February 2016).

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Main Factors | Basic Technical Factors | Merged Factors |

|---|---|---|

| Geological factors | Reservoir bed, trap types, sedimentary facies, resource abundance, oil-bearing area, average effective thickness, oil saturation, crude oil volume factor, etc. | Reserves scale |

| Reservoir type, porosity, permeability, natural energy, reservoir continuity, water saturation, reservoir wettability, oil viscosity, gas-oil ratio, bubble point pressure, reservoir heterogeneity, etc. | Recovery ratio | |

| Reservoir depth | Reservoir depth | |

| Resources quality | Chemical composition: hydrocarbons, non-hydrocarbon compounds Physical properties: specific gravity, viscosity | Price ratio |

| Geographic conditions | Transportation conditions, communication conditions, social services, location, topography, physioclimate, market conditions, etc. | Basic conditions |

| Contract terms | Contract type, contract period, signing bonus, minimum obligation workload, domestic market obligation, royalties, cost Recovery, profit distribution, government equity, taxes, etc. | Contractor income proportion |

| Investment environment | Legal soundness, political stability, foreign policy stability, economic system, GDP per capita, inflation rate, labor supply, industry competition, exchange rate, interest rate, religious culture, population quality | Investment’s environmental risk |

| Topography | Adjustment Coefficients (d) |

|---|---|

| Plain | 1 |

| Gobi | 0.92–0.96 |

| Desert | 1.05–1.08 |

| Marsh | 1.15–1.25 |

| Hills | 1.02–1.06 |

| Mountain | 1.2–1.3 |

| Level | Score (l) | Adjustment Coefficient (s) | |

|---|---|---|---|

| Excellent | 5 | 0.667 | 0.333 |

| Good | 4 | 0.333 | 0.667 |

| Fair | 3 | 0 | 1 |

| Poor | 2 | −0.333 | 1.333 |

| Very poor | 1 | −0.667 | 1.667 |

| Quality Grade | API ° | Viscosity (cP) | Sulfur Content (%) | Carbon Residue (%) | Value Coefficient |

|---|---|---|---|---|---|

| Excellent oil | 40–45 | ≤5 | ≤0.5 | ≤6 | 1.04 |

| high quality oil | >31.1 | 5–20 | ≤0.5 | ≤6 | 1.0 |

| customary quality oil | 22.3–31.1 | 20–50 | 0.5–1.0 | >8 | 0.88 |

| low quality oil | <22.3 | 50–150 | 1.0–2.0 | >8 | 0.70 |

| inferior oil | <10 | ≤10,000 | >2.0 | >8 | 0.68 |

| No. | Country | GCI | fe |

|---|---|---|---|

| 1 | Singapore | 5.67 | 1 |

| 2 | Qatar | 5.24 | 0.984832451 |

| 3 | United Arab Emirates | 4.92 | 0.973544974 |

| 4 | Indonesia | 4.53 | 0.95978836 |

| 5 | Kazakhstan | 4.41 | 0.955555556 |

| 6 | Brazil | 4.33 | 0.952733686 |

| 7 | Russia | 4.25 | 0.949911817 |

| 8 | Iran | 4.07 | 0.94356261 |

| 9 | Nigeria | 3.57 | 0.925925926 |

| 10 | Chad | 2.85 | 0.900529101 |

| Project Title | Block Area (km2) | Remaining Recoverable Reserves (MMbbl) | Resource Depths (m) | Topography | Resource Quality (API) |

|---|---|---|---|---|---|

| A | 27,516 | 658.837 | 2950–3400 | Desert | 30–35 |

| B | 29,000 | 345.8 | 2140–2379 | Plain | 26–44 |

| C | 25,694 | 610.189 | 2384–2510 | Plain | 35–45 |

| D | 17,747 | 504.112 | 1817–2081 | Tropical jungle | 21.6 |

| E | 45,876 | 930.604 | 1347–1688 | Plain | 13–34 |

| Project Title | Contract Type | Deposit a | Royalty Rates | Cost Recovery Limit | Profit Sharing Ratio (Contractor) | Income Tax |

|---|---|---|---|---|---|---|

| A | PSC | S | 12.50% | 70.00% | 20%–60% | 35% |

| B | PSC | S | 18.5% | 70.00% | 30% | 85% |

| C | Royalty | S,D,P | 16.50% | 100.00% | - | 50% |

| D | PSC | S,D,P | 0.00% | 60.00% | 20%–30% | 0% |

| E | PSC | S,D,P | 0.00% | 60.00% | 20%–30% | 0% |

| Project title | A | B | C | D | E | |||||

|---|---|---|---|---|---|---|---|---|---|---|

| Oil price (USD/bbl) | 99.08 | 99.08 | 99.08 | 99.08 | 99.08 | 99.08 | 99.08 | 99.08 | 99.08 | 99.08 |

| Royalties | 16.5% | 16.3482 | 18.50% | 18.3298 | 16.5% | 16.3482 | 0.00% | 0 | 0.00% | 0 |

| Recoverable costs * | 35.01 + 9.93 | 44.94 | 35.01 + 9.93 | 44.94 | 35.01 + 9.93 | 44.94 | 35.01 + 9.93 | 44.94 | 35.01 + 9.93 | 44.94 |

| Oil profit | - | 41.755 | - | 35.8102 | 37.7918 | - | 54.14 | - | 54.14 | |

| Contractor share of oil profit (1) | 25.0% | 10.43875 | 30.0% | 10.74306 | 25.0% | 13.535 | 25.0% | 13.535 | ||

| Domestic market obligation | - | - | - | - | - | - | - | - | ||

| Contractor share of oil profit (2) | - | 10.43875 | - | 10.74306 | - | 13.535 | - | 13.535 | ||

| Income tax | 35% | 3.6535625 | 85% | 9.131601 | 50% | 18.8959 | - | 0 | - | 0 |

| Oil profit after tax | - | 6.7851875 | - | 1.611459 | - | 18.8959 | - | 13.535 | - | 13.535 |

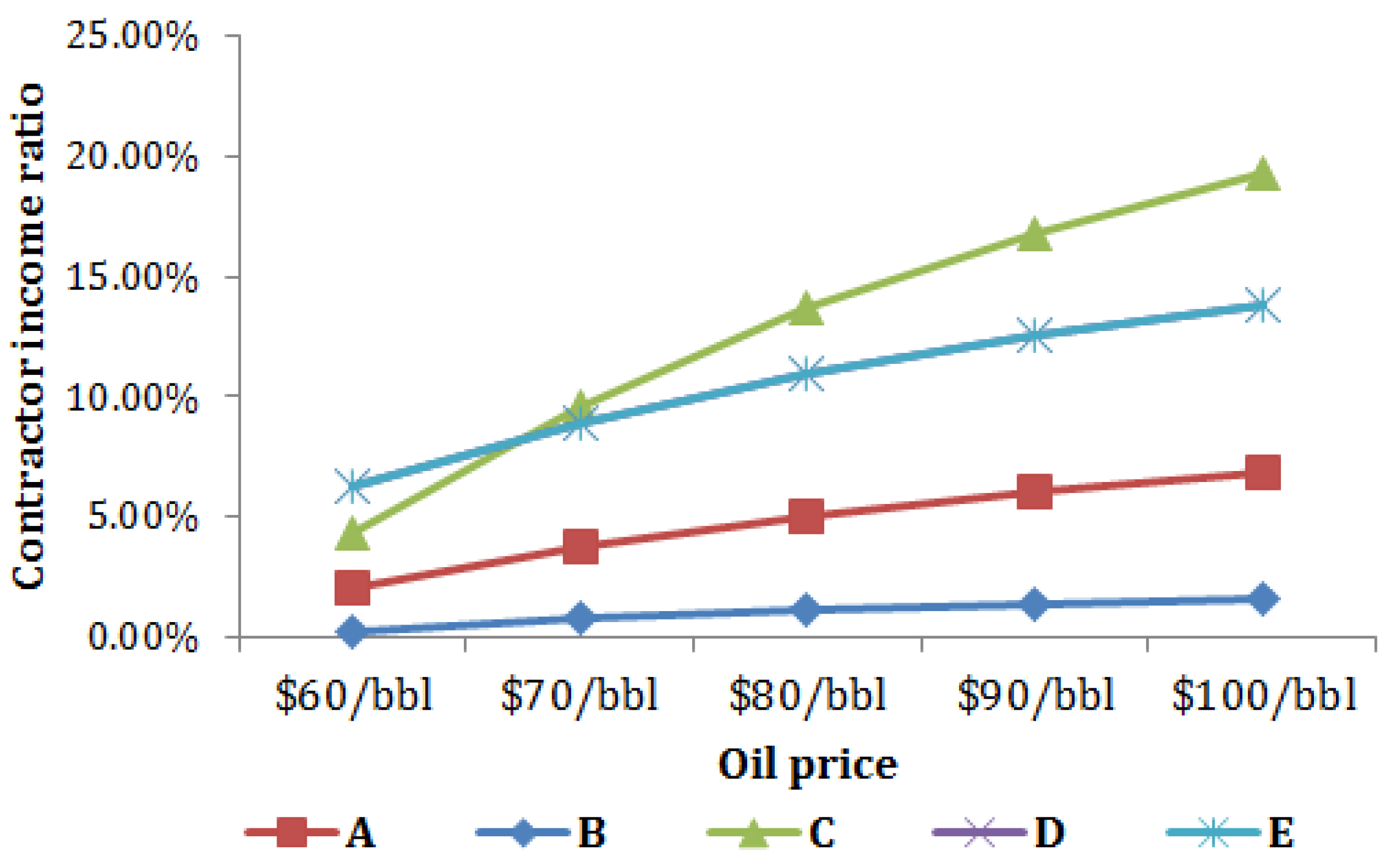

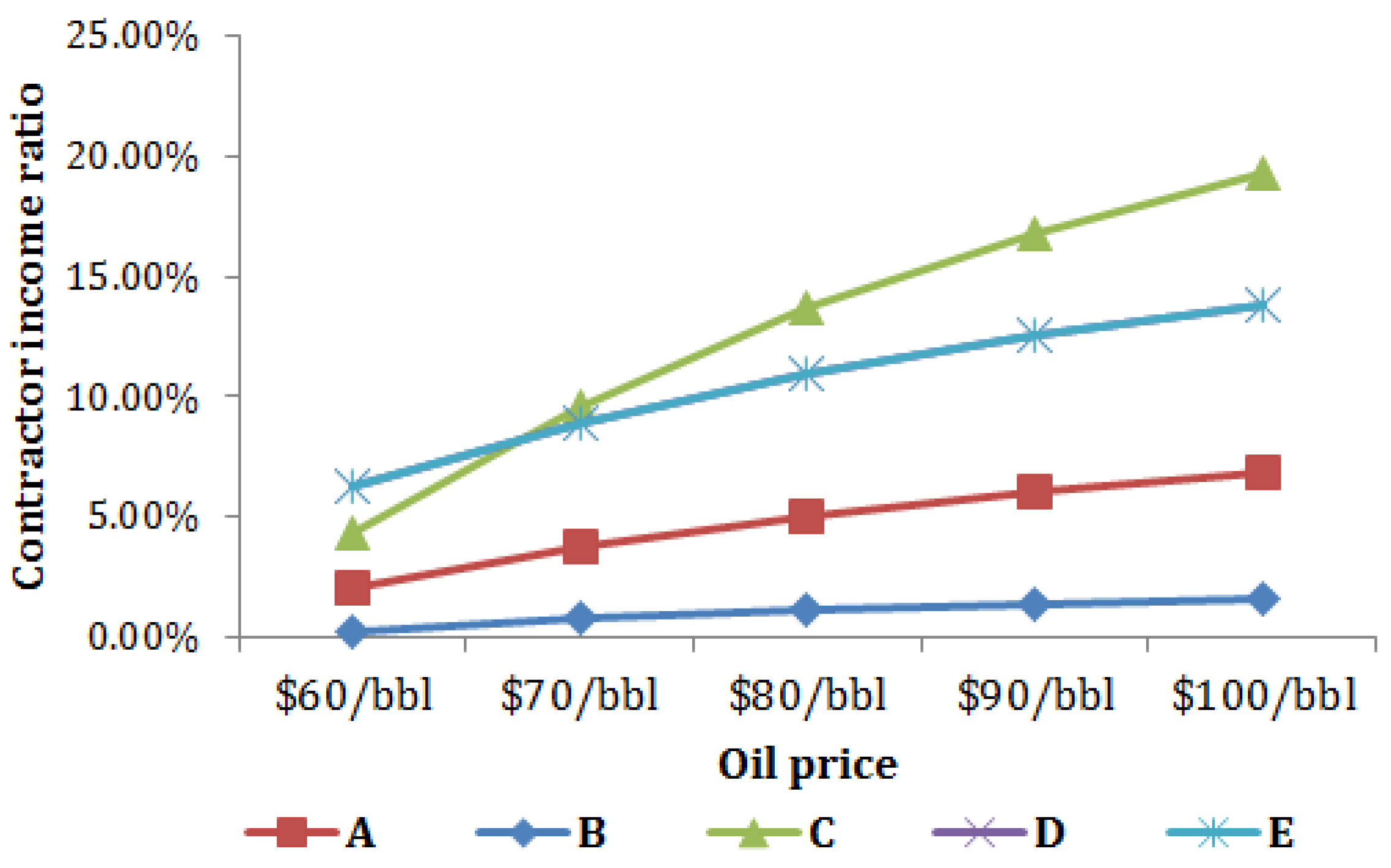

| Contractor income ratio | - | 6.85% | - | 1.63% | - | 19.07% | - | 13.66% | - | 13.66% |

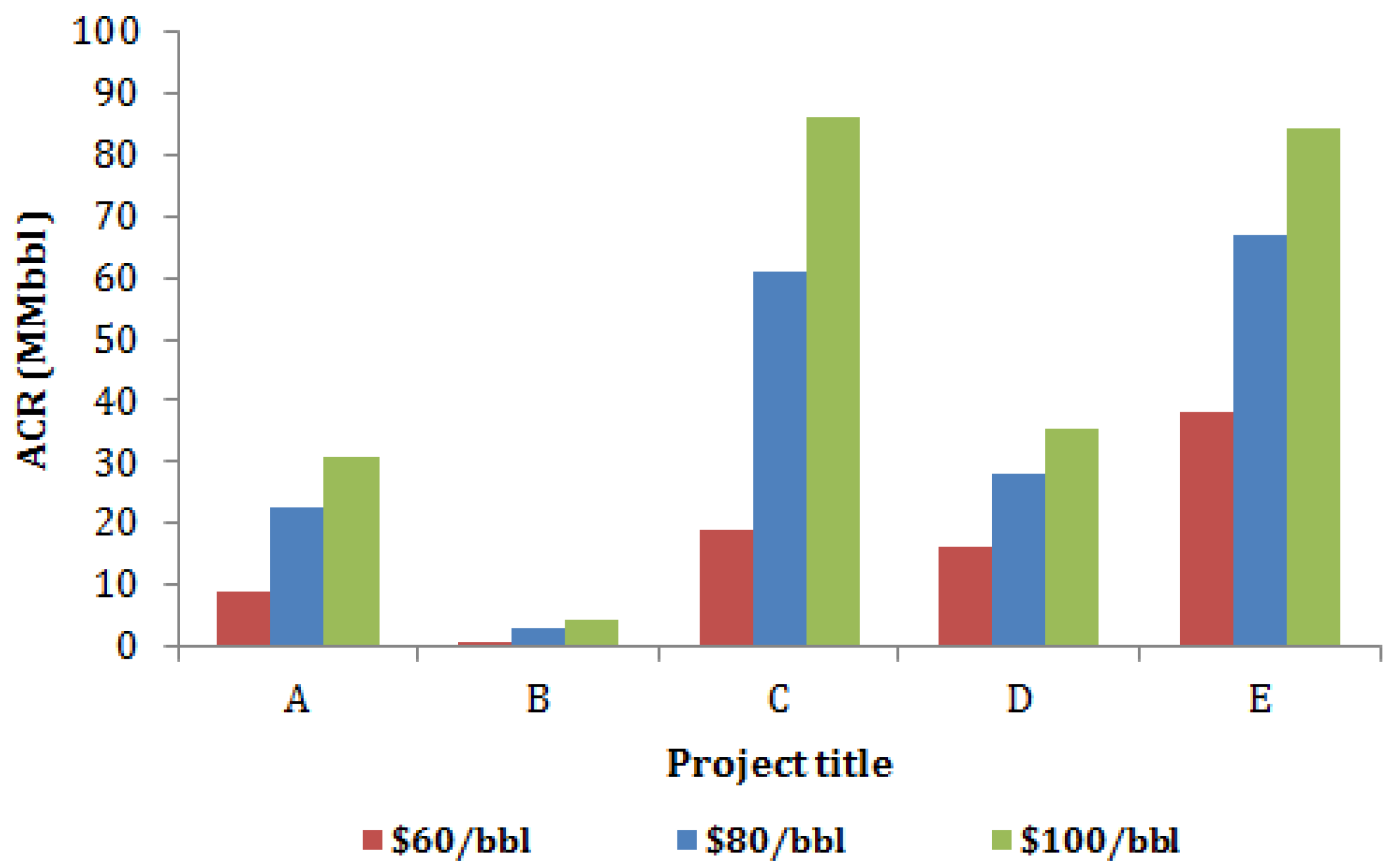

| Project Title | Remaining Recoverable Reserves (MMbbl) | Adjustment for Resource Depth | Adjustment for Geographic Conditions | Adjustment for Resource Quality | Contractor Income Ratio | Investment Environment Ristable9k | Adjusted Concept Reserves (MMbbl) |

|---|---|---|---|---|---|---|---|

| C | 610.189 | 0.12972973 | 0.058 | 1 | 19.07% | 0.900529101 | 85.12247995 |

| E | 930.604 | 0.084135135 | 0.058 | 0.88 | 13.66% | 0.870546737 | 83.54699279 |

| D | 504.112 | 0.113513514 | 0.063 | 0.7 | 13.66% | 0.888183422 | 35.25790288 |

| A | 658.837 | 0.202702703 | 0.058 | 1 | 6.85% | 0.913580247 | 30.47331183 |

| B | 345.8 | 0.116054054 | 0.058 | 1 | 1.63% | 0.925925926 | 4.301165184 |

© 2016 by the authors; licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons by Attribution (CC-BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

Guo, R.; Luo, D.; Zhao, X.; Wang, J. Integrated Evaluation Method-Based Technical and Economic Factors for International Oil Exploration Projects. Sustainability 2016, 8, 188. https://doi.org/10.3390/su8020188

Guo R, Luo D, Zhao X, Wang J. Integrated Evaluation Method-Based Technical and Economic Factors for International Oil Exploration Projects. Sustainability. 2016; 8(2):188. https://doi.org/10.3390/su8020188

Chicago/Turabian StyleGuo, Rui, Dongkun Luo, Xu Zhao, and Jianliang Wang. 2016. "Integrated Evaluation Method-Based Technical and Economic Factors for International Oil Exploration Projects" Sustainability 8, no. 2: 188. https://doi.org/10.3390/su8020188

APA StyleGuo, R., Luo, D., Zhao, X., & Wang, J. (2016). Integrated Evaluation Method-Based Technical and Economic Factors for International Oil Exploration Projects. Sustainability, 8(2), 188. https://doi.org/10.3390/su8020188