Effects of Green Innovation on Environmental and Corporate Performance: A Stakeholder Perspective

Abstract

:1. Introduction

2. Literature Review

2.1. Stakeholder Theory

2.2. Green Innovation

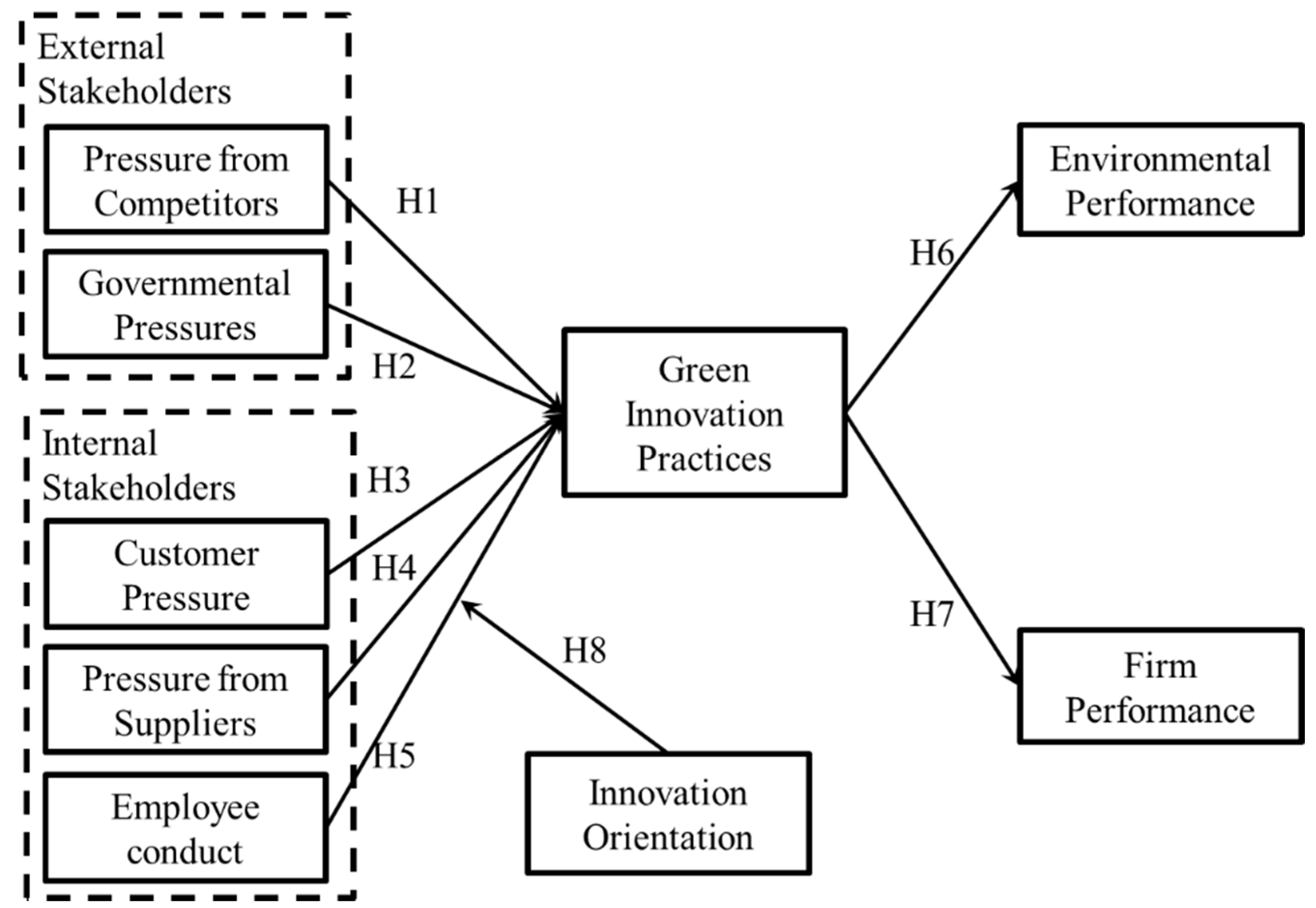

3. Green Innovation Model

3.1. External and Internal Stakeholders

3.1.1. Pressure from Competitors

3.1.2. Governmental Pressures

3.1.3. Customer Pressure

3.1.4. Pressure from Suppliers

3.1.5. Employee Conduct

3.2. Performance

3.2.1. Environmental Performance

3.2.2. Firm Performance

3.3. Innovation Orientation

4. Research Methodology

4.1. Instrument Design

4.2. Operationalization of Constructs

4.2.1. Pressure from Competitors (COM)

4.2.2. Governmental Pressure (GOV)

4.2.3. Customer Pressure (CUS)

4.2.4. Pressure from Suppliers (SU)

4.2.5. Employee Conduct (EM)

4.2.6. Green Innovation Practices (GI)

4.2.7. Environmental Performance (EP)

4.2.8. Firm Performance (FP)

4.2.9. Innovation Orientation (IO)

4.2.10. Control Variables

4.3. Sampling

4.4. Data Collection

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Construct | Mean | T-test for the equality of means | |||

|---|---|---|---|---|---|

| Early response (n = 127) | Late response (n = 75) | Mean difference | t-value | p-value (2-tailed) | |

| YE | 4.850 | 4.720 | 0.130 | 0.663 | 0.508 |

| FC | 3.803 | 3.787 | 0.016 | 0.130 | 0.897 |

| NE | 3.158 | 3.160 | −0.003 | −0.013 | 0.990 |

| TW | 3.677 | 3.627 | 0.050 | 0.238 | 0.812 |

| Construct | Mean | T-test for the equality of means | |||

|---|---|---|---|---|---|

| SI (n = 112) | MI (n = 90) | Mean difference | t-value | p-value (2-tailed) | |

| COM | 3.833 | 3.917 | −0.084 | −0.906 | 0.366 |

| CUS | 3.938 | 4.106 | −0.168 | −1.856 | 0.065 |

| SU | 3.813 | 3.978 | −0.165 | −1.540 | 0.125 |

| GOV | 3.864 | 3.778 | 0.086 | 0.815 | 0.416 |

| EM | 3.721 | 3.842 | −0.121 | −1.303 | 0.195 |

| GIa | 4.009 | 3.975 | 0.034 | 0.423 | 0.673 |

| GIb | 3.929 | 3.885 | 0.043 | 0.492 | 0.624 |

| IO | 3.973 | 4.065 | −0.092 | −1.022 | 0.308 |

| EP | 3.987 | 3.950 | 0.037 | 0.452 | 0.652 |

| FP | 3.757 | 3.689 | 0.068 | 0.769 | 0.443 |

5. Data Analysis and Results

5.1. Sample Demographics

| Variable | Category | N | Rate (%) |

|---|---|---|---|

| Years of firm established in Taiwan | 3 years and fewer | 5 | 2.5 |

| Over 3 years to 5 years | 5 | 2.5 | |

| Over 5 years to 10 years | 28 | 13.8 | |

| Over 10 years to 15 years | 43 | 21.3 | |

| Over 15 years to 20 years | 27 | 13.4 | |

| Over 20 years | 94 | 46.5 | |

| Firm capital (1 US dolla ≈ 30 NT dollars) | Less than USD 0.33 million | 5 | 2.5 |

| USD 0.33 million to 1.6 million | 17 | 8.4 | |

| USD 1.6 million to 3.3 million | 14 | 6.8 | |

| USD 3.3 million to 170 million | 150 | 74.3 | |

| USD 170 million to 330 million | 10 | 5.0 | |

| Over USD 330 million | 6 | 3.0 | |

| Number of employees (people) | 50 and fewer | 25 | 12.4 |

| 51 to 100 | 19 | 9.4 | |

| 101 to 500 | 107 | 53.0 | |

| 501 to 1000 | 20 | 9.9 | |

| 1001 to 2000 | 12 | 5.9 | |

| Over 2000 | 19 | 9.4 | |

| Industry | Hotel | 35 | 17.3 |

| Logistics | 37 | 18.3 | |

| Contractors | 33 | 16.3 | |

| Photoelectric | 31 | 15.4 | |

| Computer Peripherals | 30 | 14.9 | |

| Automobile Manufacturing | 22 | 10.9 | |

| Others | 14 | 6.9 | |

| Tenures of informants | 3 years and fewer | 14 | 6.9 |

| Over 3 years to 5 years | 26 | 12.9 | |

| Over 5 years to 10 years | 63 | 31.2 | |

| Over 10 years to 15 years | 45 | 22.3 | |

| Over 15 years to 20 years | 20 | 9.9 | |

| Over 20 years | 34 | 16.8 |

5.2. The Measurement Model

| Item | Factor | ||||

|---|---|---|---|---|---|

| 1 | 2 | 3 | 4 | 5 | |

| EM1 | 0.690 | 0.256 | 0.180 | 0.248 | 0.172 |

| EM2 | 0.847 | 0.092 | 0.058 | 0.144 | 0.209 |

| EM3 | 0.745 | 0.120 | 0.156 | 0.195 | 0.248 |

| EM4 | 0.515 | 0.257 | 0.116 | 0.256 | −0.059 |

| EM5 | 0.694 | 0.130 | 0.124 | 0.297 | 0.121 |

| GOV1 | −0.018 | 0.807 | 0.159 | 0.291 | 0.156 |

| GOV2 | 0.167 | 0.880 | 0.175 | 0.103 | 0.109 |

| GOV3 | 0.322 | 0.832 | 0.185 | 0.050 | 0.230 |

| GOV4 | 0.279 | 0.767 | 0.043 | −0.036 | 0.226 |

| CUS1 | −0.023 | 0.196 | 0.807 | 0.258 | 0.145 |

| CUS2 | 0.187 | 0.170 | 0.831 | 0.185 | 0.194 |

| CUS3 | 0.164 | 0.075 | 0.790 | 0.157 | 0.309 |

| CUS4 | 0.279 | 0.126 | 0.763 | 0.121 | 0.260 |

| COM1 | 0.388 | 0.072 | 0.245 | 0.733 | 0.142 |

| COM2 | 0.335 | 0.085 | 0.100 | 0.736 | 0.160 |

| COM3 | 0.183 | 0.138 | 0.201 | 0.797 | 0.226 |

| COM4 | 0.241 | 0.104 | 0.245 | 0.752 | 0.240 |

| SU1 | 0.045 | 0.239 | 0.277 | 0.245 | 0.698 |

| SU2 | 0.154 | 0.258 | 0.292 | 0.245 | 0.769 |

| SU3 | 0.192 | 0.169 | 0.290 | 0.257 | 0.777 |

| SU4 | 0.286 | 0.133 | 0.153 | 0.078 | 0.757 |

| Construct | Construct identifier | Items | Factor loading | Cronbach’s alpha | Composite reliability |

|---|---|---|---|---|---|

| Pressures from competitors | COM | COM1 | 0.838 | 0.888 | 0.922 |

| COM2 | 0.777 | ||||

| COM3 | 0.820 | ||||

| COM4 | 0.828 | ||||

| Customer pressure | CUS | CUS1 | 0.793 | 0.898 | 0.930 |

| CUS2 | 0.885 | ||||

| CUS3 | 0.838 | ||||

| CUS4 | 0.804 | ||||

| Pressure from suppliers | SU | SU1 | 0.752 | 0.887 | 0.922 |

| SU2 | 0.906 | ||||

| SU3 | 0.907 | ||||

| SU4 | 0.701 | ||||

| Governmental pressures | GOV | GOV1 | 0.721 | 0.904 | 0.933 |

| GOV2 | 0.884 | ||||

| GOV3 | 0.967 | ||||

| GOV4 | 0.774 | ||||

| Employee conduct | EM | EM1 | 0.789 | 0.845 | 0.890 |

| EM2 | 0.814 | ||||

| EM3 | 0.765 | ||||

| EM4 | 0.542 | ||||

| EM5 | 0.727 | ||||

| Green product innovation practices | GIa | GI1 | 0.757 | 0.845 | 0.889 |

| GI2 | 0.720 | ||||

| GI3 | 0.705 | ||||

| GI4 | 0.683 | ||||

| GI5 | 0.742 | ||||

| Green process innovation practices | GIb | GI6 | 0.673 | 0.891 | 0.914 |

| GI7 | 0.702 | ||||

| GI8 | 0.784 | ||||

| GI9 | 0.750 | ||||

| GI10 | 0.696 | ||||

| GI11 | 0.729 | ||||

| GI12 | 0.784 | ||||

| Innovation orientation | IO | IO1 | 0.775 | 0.924 | 0.939 |

| IO2 | 0.851 | ||||

| IO3 | 0.899 | ||||

| IO4 | 0.669 | ||||

| IO5 | 0.839 | ||||

| IO6 | 0.827 | ||||

| IO7 | 0.727 | ||||

| Environmental performance | EP | EP1 | 0.776 | 0.892 | 0.918 |

| EP2 | 0.828 | ||||

| EP3 | 0.812 | ||||

| EP4 | 0.795 | ||||

| EP5 | 0.721 | ||||

| Firm performance | FP | FP1 | 0.776 | 0.945 | 0.954 |

| FP2 | 0.856 | ||||

| FP3 | 0.876 | ||||

| FP4 | 0.867 | ||||

| FP5 | 0.888 | ||||

| FP6 | 0.746 | ||||

| FP7 | 0.781 | ||||

| FP8 | 0.815 |

5.3. The Structural Model

| Mean | SD | AVE | (a) | (b) | (c) | (d) | (e) | (f) | (g) | (h) | (i) | (j) | ||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| COM | (a) | 3.870 | 0.655 | 0.747 | 0.864 | |||||||||

| CUS | (b) | 4.002 | 0.638 | 0.766 | 0.527 ** | 0.875 | ||||||||

| SU | (c) | 3.765 | 0.684 | 0.747 | 0.549 ** | 0.608 ** | 0.864 | |||||||

| GOV | (d) | 3.825 | 0.726 | 0.645 | 0.364 ** | 0.409 ** | 0.500 ** | 0.803 | ||||||

| EM | (e) | 3.775 | 0.634 | 0.619 | 0.629 ** | 0.439 ** | 0.502 ** | 0.479 ** | 0.787 | |||||

| GIa | (f) | 4.034 | 0.519 | 0.617 | 0.550 ** | 0.457 ** | 0.492 ** | 0.451 ** | 0.550 ** | 0.785 | ||||

| GIb | (g) | 3.946 | 0.550 | 0.603 | 0.503 ** | 0.362 ** | 0.346 ** | 0.395 ** | 0.572 ** | 0.674 ** | 0.777 | |||

| IO | (h) | 4.014 | 0.635 | 0.689 | 0.539 ** | 0.401 ** | 0.393 ** | 0.395 ** | 0.583 ** | 0.540 ** | 0.413 ** | 0.830 | ||

| EP | (i) | 3.970 | 0.556 | 0.651 | 0.677 ** | 0.456 ** | 0.453 ** | 0.411 ** | 0.682 ** | 0.684 ** | 0.697 ** | 0.515 ** | 0.807 | |

| FP | (j) | 3.726 | 0.623 | 0.722 | 0.666 ** | 0.505 ** | 0.529 ** | 0.426 ** | 0.574 ** | 0.525 ** | 0.497 ** | 0.546 ** | 0.637 ** | 0.850 |

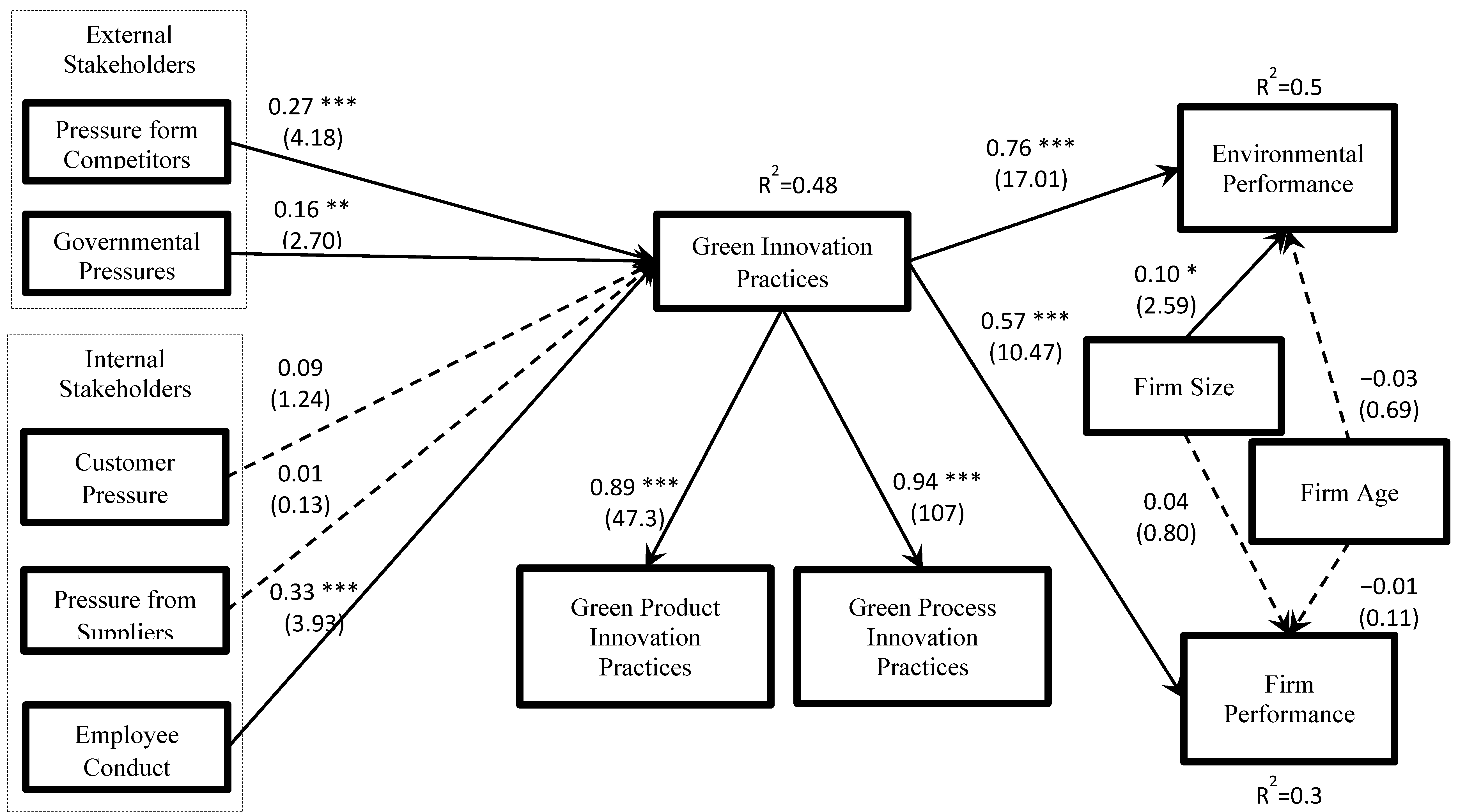

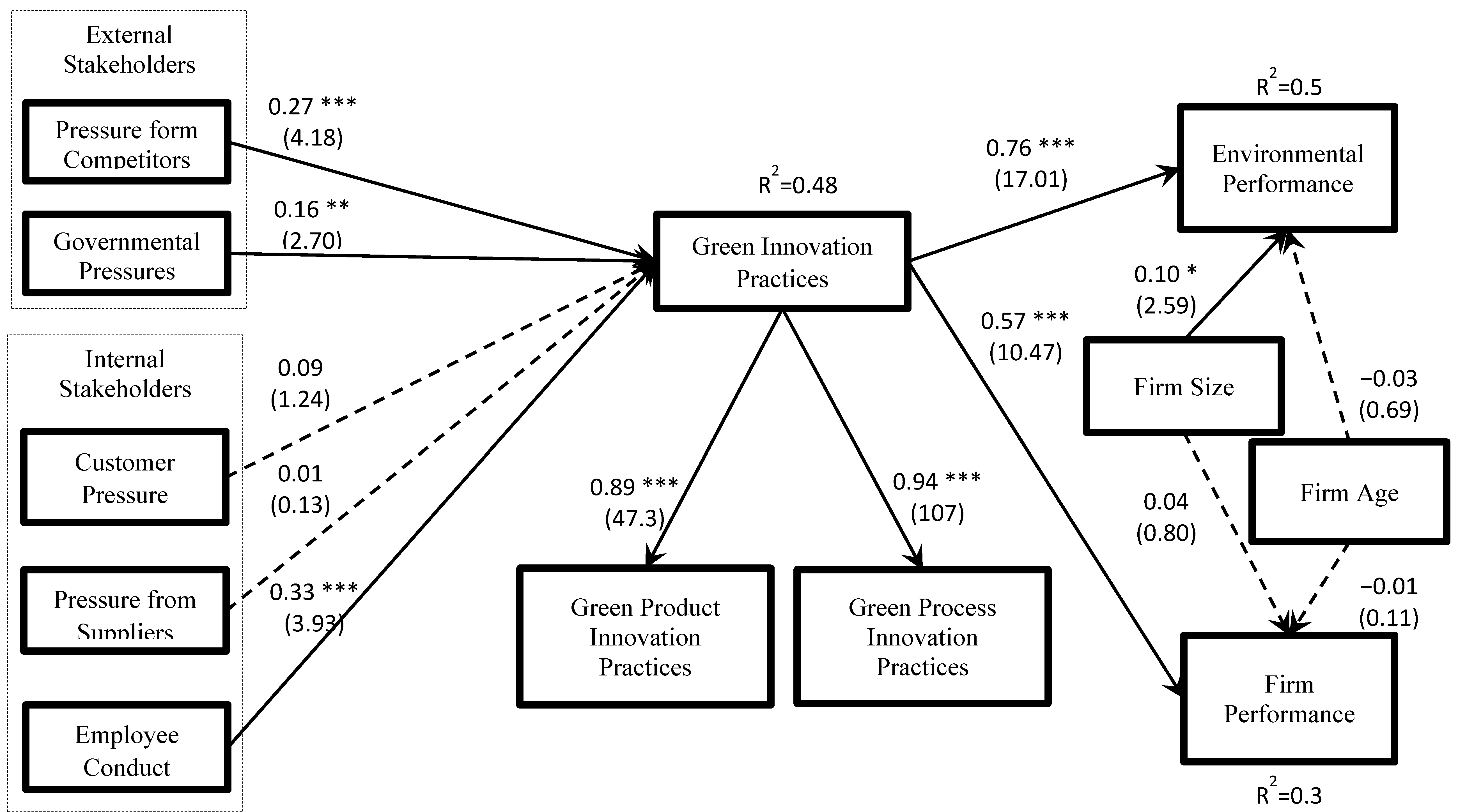

Results for the Direct and Moderating Effects

| Path/hypothesis | Path coefficient | t-value | Results | |||

|---|---|---|---|---|---|---|

| Hypothesized relationships | ||||||

| Pressure from Competitors | ➔ | Green innovation practices | H1 | 0.27 *** | 4.18 | Supported |

| Governmental pressures | ➔ | Green innovation practices | H2 | 0.16 ** | 2.70 | Supported |

| Customer pressure | ➔ | Green innovation practices | H3 | 0.09 | 1.24 | Not Supported |

| Pressure from Suppliers | ➔ | Green innovation practices | H4 | 0.01 | 0.13 | Not Supported |

| Employee conduct | ➔ | Green innovation practices | H5 | 0.33 *** | 3.93 | Supported |

| Green innovation practices | ➔ | Environmental performance | H6 | 0.76 *** | 17.01 | Supported |

| Green innovation practices | ➔ | Firm performance | H7 | 0.57 *** | 10.47 | Supported |

| Firm size | ➔ | Environmental Performance | 0.10* | 2.59 | ||

| Firm size | ➔ | Firm performance | 0.04 | 0.80 | ||

| Firm age | ➔ | Environmental performance | −0.03 | 0.69 | ||

| Firm age | ➔ | Firm performance | −0.01 | 0.11 | ||

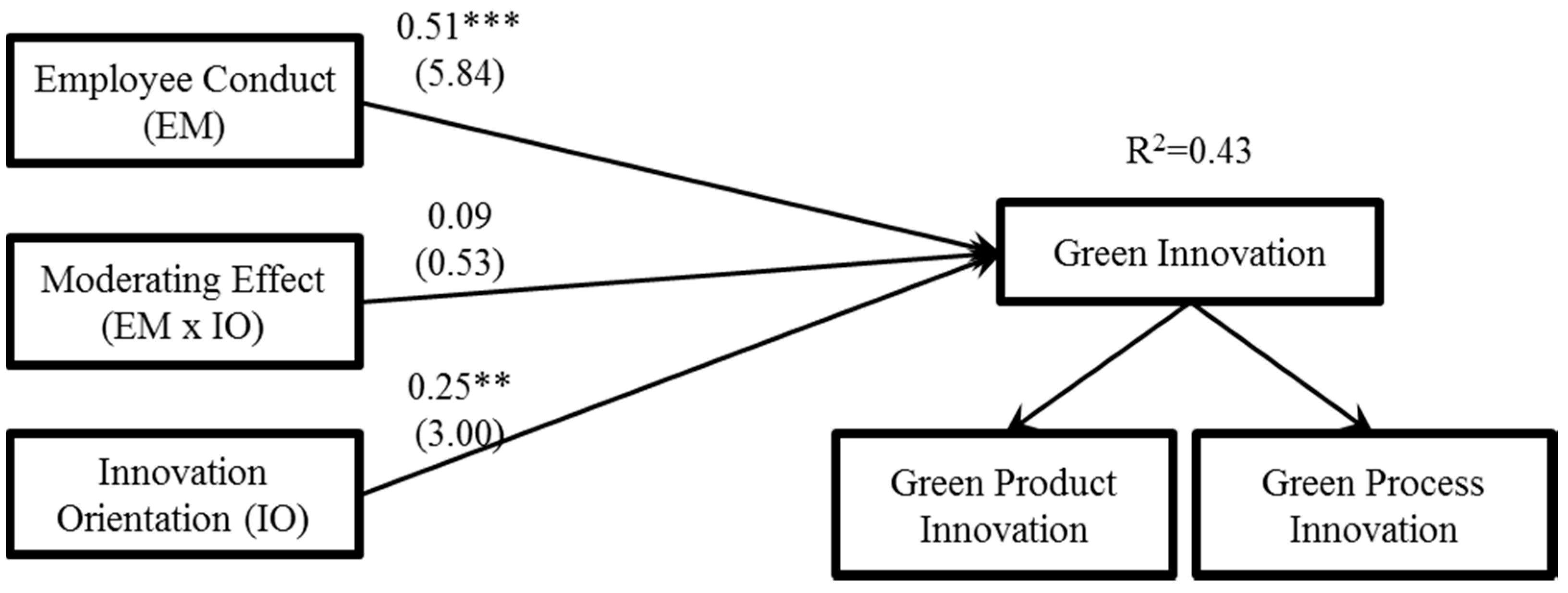

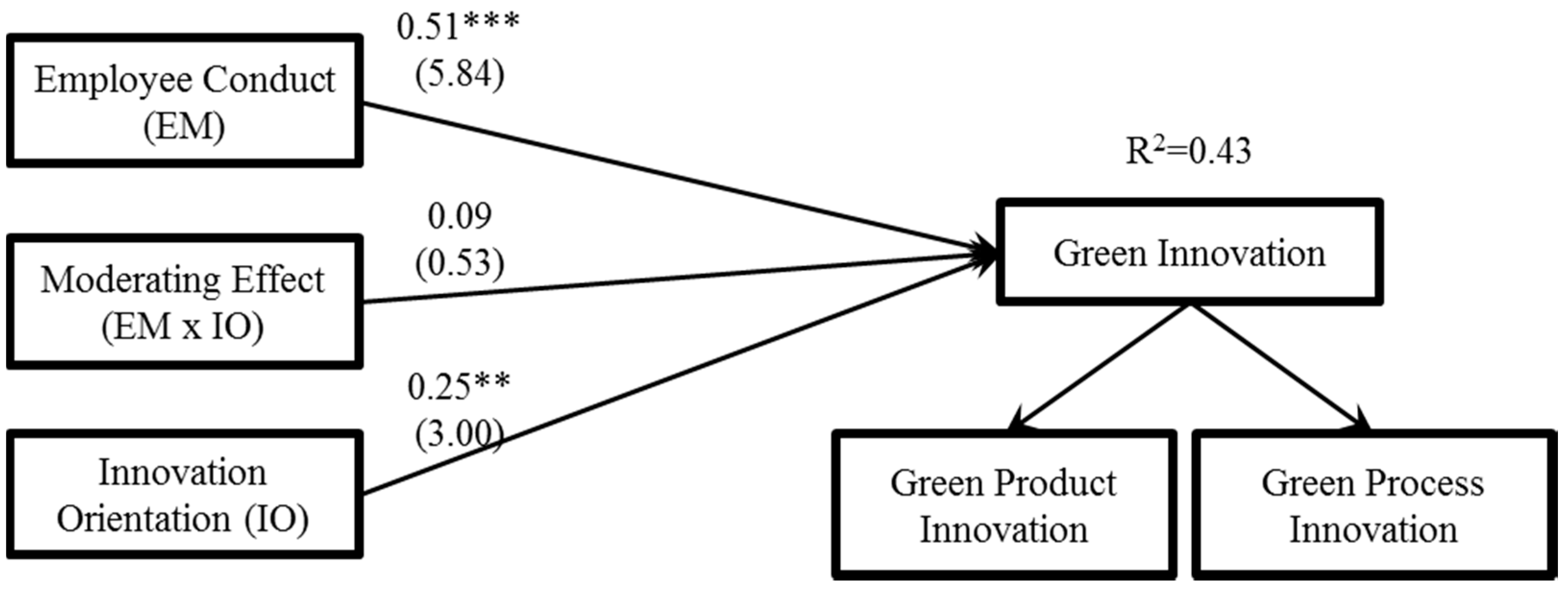

| Variable(s) entered | Dependent variable: second order green innovation practices | |||

|---|---|---|---|---|

| Hypothesis | Main effects | Interaction | Result | |

| Innovation orientation | 0.244 ** | 0.247 ** | ||

| Employee conduct | 0.474 *** | 0.508 *** | ||

| Innovation orientation × Employee conduct | H8 | 0.085 | Not supported | |

| R² | 0.42 | 0.43 | ||

6. Discussion

6.1. Stakeholders and Green Innovation Practices

6.2. Green Innovation Practices and Performance

6.3. The Moderating Effect of Innovation Orientation

| Variable(s) Entered | Dependent variable: green product innovation practices | |||

|---|---|---|---|---|

| Hypothesis | Main effects | Interaction | Result | |

| Innovation orientation | 0.341 *** | 0.371 *** | ||

| Employee conduct | 0.366 *** | 0.412 *** | ||

| Innovation orientation × Employee conduct | H8a | 0.343 * | Supported | |

| R2 | 0.40 | 0.50 | ||

| Variable(s) entered | Dependent variable: green process innovation practices | |||

|---|---|---|---|---|

| Hypothesis | Main effects | Interaction | Result | |

| Innovation orientation | 0.143 | 0.145 | ||

| Employee conduct | 0.498 *** | 0.513 *** | ||

| Innovation orientation × Employee conduct | H8b | 0.041 | Not Supported | |

| R2 | 0.35 | 0.35 | ||

6.4. Comparison of Manufacturing and Service Industries

6.5. Control Variables

7. Conclusions

8. Limitations and Further Research

Acknowledgments

Author Contributions

Conflicts of Interest

References

- Qi, G.Y.; Shen, L.Y.; Zeng, S.X.; Jorge, O.J. The drivers for contractors’ green innovation: An industry perspective. J. Clean. Prod. 2010, 18, 1358–1365. [Google Scholar] [CrossRef]

- Panwar, N.; Kaushik, S.; Kothari, S. Role of renewable energy sources in environmental protection: A review. Renew. Sustain. Energy Rev. 2011, 15, 1513–1524. [Google Scholar] [CrossRef]

- Zhu, Q.; Sarkis, J. Relationships between operational practices and performance among early adopters of green supply chain management practices in chinese manufacturing enterprises. J. Oper. Manag. 2004, 22, 265–289. [Google Scholar] [CrossRef]

- Claver, E.; López, M.D.; Molina, J.F.; Tarí, J.J. Environmental management and firm performance: A case study. J. Environ. Manag. 2007, 84, 606–619. [Google Scholar] [CrossRef]

- Porter, M.E.; van der Linde, C. Green and competitive: Ending the stalemate. Harv. Bus. Rev. 1995, 73, 120–134. [Google Scholar]

- Chen, Y.-S. The driver of green innovation and green image—Green core competence. J. Bus. Ethics 2008, 81, 531–543. [Google Scholar] [CrossRef]

- Hillestad, T.; Chunyan, X.; Haugland, S.A. Innovative corporate social responsibility: The founder’s role in creating a trustworthy corporate brand through “green innovation”. J. Prod. Brand Manag. 2010, 19, 440–451. [Google Scholar] [CrossRef]

- Rusinko, C.A. Green manufacturing: An evaluation of environmentally sustainable manufacturing practices and their impact on competitive outcomes. IEEE Trans. Eng. Manag. 2007, 54, 445–454. [Google Scholar] [CrossRef]

- Davis, C.H. The earth summit and the promotion of environmentally sound industrial innovation in developing countries. Knowl. Policy 1995, 8, 26–52. [Google Scholar] [CrossRef]

- Schiederig, T.; Tietze, F.; Herstatt, C. Green innovation in technology and innovation management—An exploratory literature review. R&D Manag. 2012, 42, 180–192. [Google Scholar] [CrossRef]

- Routroy, S. Antecedents and drivers for green supply chain management implementation in manufacturing environment. ICFAI J. Supply Chain Manag. 2009, 6, 20–35. [Google Scholar]

- Thøgersen, J.; Zhou, Y. Chinese consumers’ adoption of a ‘green’ innovation—The case of organic food. J. Mark. Manag. 2012, 28, 313–333. [Google Scholar] [CrossRef]

- Huang, Y.-C.; Ding, H.-B.; Kao, M.-R. Salient stakeholder voices: Family business and green innovation adoption. J. Manag. Organ. 2009, 15, 309–326. [Google Scholar] [CrossRef]

- Chiou, T.-Y.; Chan, H.K.; Lettice, F.; Chung, S.H. The influence of greening the suppliers and green innovation on environmental performance and competitive advantage in taiwan. Transp. Res. Part E 2011, 47, 822–836. [Google Scholar] [CrossRef]

- Kammerer, D. The effects of customer benefit and regulation on environmental product innovation: Empirical evidence from appliance manufacturers in germany. Ecol. Econ. 2009, 68, 2285–2295. [Google Scholar] [CrossRef]

- Lin, C.-Y.; Ho, Y.-H. Determinants of green practice adoption for logistics companies in China. J. Bus. Ethics 2011, 98, 67–83. [Google Scholar] [CrossRef]

- Chang, C.-H. The Influence of Corporate Environmental Ethics on Competitive Advantage: The Mediation role of Green Innovation; Springer Science & Business Media B.V.: Berlin, Germany, 2011; pp. 361–370. [Google Scholar]

- Chen, Y.-S. The positive effect of green intellectual capital on competitive advantages of firms. J. Bus. Ethics 2008, 77, 271–286. [Google Scholar] [CrossRef]

- Cordano, M.; Marshall, R.; Silverman, M. How do small and medium enterprises go “green”? A study of environmental management programs in the u.S. Wine industry. J. Bus. Ethics 2010, 92, 463–478. [Google Scholar] [CrossRef]

- Freeman, R.E. Strategic Management: A stakeholder Approach; Cambridge University Press: New York, NY, USA, 2010. [Google Scholar]

- Harrison, J.S.; Bosse, D.A.; Phillips, R.A. Managing for stakeholders, stakeholder utility functions, and competitive advantage. Strateg. Manag. J. 2010, 31, 58–74. [Google Scholar] [CrossRef]

- Friedman, A.L.; Miles, S. Stakeholders: Theory and Practice; Oxford University Press Inc.: New York, NY, USA, 2006; p. 330. [Google Scholar]

- Donaldson, T.; Preston, L.E. The stakeholder theory of the corporation: Concepts, evidence, and implications. Acad. Manag. Rev. 1995, 20, 65–91. [Google Scholar]

- Mitchell, R.K.; Agle, B.R.; Wood, D.J. Toward a theory of stakeholder identification and salience: Defining the principle of who and what really counts. Acad. Manag. Rev. 1997, 22, 853–886. [Google Scholar]

- Mainardes, E.W.; Alves, H.; Raposo, M. Stakeholder theory: Issues to resolve. Manag. Decis. 2011, 49, 226–252. [Google Scholar] [CrossRef]

- Jones, T.M.; Wicks, A.C. Convergent stakeholder theory. Acad. Manag. Rev. 1999, 24, 206–221. [Google Scholar]

- Laplume, A.O.; Sonpar, K.; Litz, R.A. Stakeholder theory: Reviewing a theory that moves us. J. Manag. 2008, 34, 1152–1189. [Google Scholar]

- Co, H.C.; Barro, F. Stakeholder theory and dynamics in supply chain collaboration. Int. J. Oper. Prod. Manag. 2009, 29, 591–611. [Google Scholar] [CrossRef]

- Clarkson, M.E. A stakeholder framework for analyzing and evaluating corporate social performance. Acad. Manag. Rev. 1995, 20, 92–117. [Google Scholar]

- Bansal, P.; Roth, K. Why companies go green: A model of ecological responsiveness. Acad. Manag. J. 2000, 43, 717–736. [Google Scholar] [CrossRef]

- Neu, D.; Warsame, H.; Pedwell, K. Managing public impressions: Environmental disclosures in annual reports. Account. Organ. Soc. 1998, 23, 265–282. [Google Scholar] [CrossRef]

- Buysse, K.; Verbeke, A. Proactive environmental strategies: A stakeholder management perspective. Strateg. Manag. J. 2003, 24, 453–470. [Google Scholar] [CrossRef]

- Kassinis, G.; Vafeas, N. Corporate boards and outside stakeholders as determinants of environmental litigation. Strateg. Manag. J. 2002, 23, 399–415. [Google Scholar] [CrossRef]

- Murillo-Luna, J.L.; Garcés-Ayerbe, C.; Rivera-Torres, P. Why do patterns of environmental response differ? A stakeholders' pressure approach. Strateg. Manag. J. 2008, 29, 1225–1240. [Google Scholar] [CrossRef]

- Wagner, M. On the relationship between environmental management, environmental innovation and patenting: Evidence from german manufacturing firms. Res. Policy 2007, 36, 1587–1602. [Google Scholar] [CrossRef]

- Gluch, P.; Gustafsson, M.; Thuvander, L. An absorptive capacity model for green innovation and performance in the construction industry. Constr. Manag. Econ. 2009, 27, 451–464. [Google Scholar] [CrossRef]

- Lin, C.-Y.; Ho, Y.-H.; Chiang, S.-H. Organizational determinants of green innovation implementation in the logistics industry. Int. J. Organ. Innov. 2009, 2, 3–12. [Google Scholar]

- Lin, C.-Y.; Ho, Y.-H. An empirical study on logistics service providers’ intention to adopt green innovations. J. Tech. Manag. Innov. 2008, 3, 18–26. [Google Scholar]

- Chen, Y.-S.; Lai, S.-B.; Wen, C.-T. The influence of green innovation performance on corporate advantage in taiwan. J. Bus. Ethics 2006, 67, 331–339. [Google Scholar] [CrossRef]

- Rennings, K. Redefining innovation—Eco-innovation research and the contribution from ecological economics. Ecol. Econ. 2000, 32, 319. [Google Scholar] [CrossRef]

- Oltra, V.; Saint Jean, M. Sectoral systems of environmental innovation: An application to the french automotive industry. Technol. Forecast. Social Chang. 2009, 76, 567–583. [Google Scholar] [CrossRef]

- Bernauer, T.; Engel, S.; Kammerer, D.; Sejas Nogareda, J. Explaining green innovation: Ten years after Porter’s win-win proposition: How to study the effects of regulation on corporate environmental innovation? Politische Vieteljahresschrift 2007, 39, 323–341. [Google Scholar]

- Christmann, P. Multinational companies and the natural environment: Determinants of global environmental policy standardization. Acad. Manag. J. 2004, 47, 747–760. [Google Scholar] [CrossRef]

- Hsu, C.-C.; Tan, K.C.; Zailani, S.H.M.; Jayaraman, V. Supply chain drivers that foster the development of green initiatives in an emerging economy. Int. J. Oper. Prod. Manag. 2013, 33, 656–688. [Google Scholar] [CrossRef]

- Abrahamson, E.; Rosenkopf, L. Institutional and competitive bandwagons: Using mathematical modeling as a tool to explore innovation diffusion. Acad. Manag. Rev. 1993, 18, 487–517. [Google Scholar]

- Backer, L. Engaging stakeholders in corporate environmental governance. Bus. Soc. Rev. 2007, 112, 29–54. [Google Scholar] [CrossRef]

- Zhu, Q.; Sarkis, J. The moderating effects of institutional pressures on emergent green supply chain practices and performance. Int. J. Prod. Res. 2007, 45, 4333–4355. [Google Scholar] [CrossRef]

- Lindell, M.; Karagozoglu, N. Corporate environmental behaviour—A comparison between nordic and us firms. Bus. Strategy Environ. 2001, 10, 38–52. [Google Scholar] [CrossRef]

- Zeng, S.X.; Meng, X.H.; Zeng, R.C.; Tam, C.M.; Tam, V.W.Y.; Jin, T. How environmental management driving forces affect environmental and economic performance of smes: A study in the northern China district. J. Clean. Prod. 2011, 19, 1426–1437. [Google Scholar] [CrossRef]

- Sarkis, J.; Gonzalez-Torre, P.; Adenso-Diaz, B. Stakeholder pressure and the adoption of environmental practices: The mediating effect of training. J. Oper. Manag. 2010, 28, 163–176. [Google Scholar] [CrossRef]

- Lee, S.-Y.; Klassen, R.D. Drivers and enablers that foster environmental management capabilities in small- and medium-sized suppliers in supply chains. Prod. Oper. Manag. 2008, 17, 573–586. [Google Scholar] [CrossRef]

- Liu, X.; Yang, J.; Qu, S.; Wang, L.; Shishime, T.; Bao, C. Sustainable production: Practices and determinant factors of green supply chain management of chinese companies. Bus. Strategy Environ. 2012, 21, 1–16. [Google Scholar] [CrossRef]

- Doonan, J.; Lanoie, P.; Laplante, B. Determinants of environmental performance in the Canadian pulp and paper industry: An assessment from inside the industry. Ecol. Econ. 2005, 55, 73–84. [Google Scholar] [CrossRef]

- Khanna, M.; Anton, W.R.Q. Corporate environmental management: Regulatory and market-based incentives. Land Econ. 2002, 78, 539–558. [Google Scholar] [CrossRef]

- Christmann, P.; Taylor, G. Globalization and the environment: Determinants of firm self-regulation in China. J. Int. Bus. Stud. 2001, 32, 439–458. [Google Scholar] [CrossRef]

- Henriques, I.; Sadorsky, P. The determinants of an environmentally responsive firm: An empirical approach. J. Environ. Econ. Manag. 1996, 30, 381–395. [Google Scholar] [CrossRef]

- Varnäs, A.; Balfors, B.; Faith-Ell, C. Environmental consideration in procurement of construction contracts: Current practice, problems and opportunities in green procurement in the Swedish construction industry. J. Clean. Prod. 2009, 17, 1214–1222. [Google Scholar] [CrossRef]

- Hult, G.; Swan, S.K. A research agenda for the nexus of product development and supply chain management processes. J. Prod. Innov. Manag. 2003, 20, 333–336. [Google Scholar] [CrossRef]

- Pujari, D. Eco-innovation and new product development: Understanding the influences on market performance. Technovation 2006, 26, 76–85. [Google Scholar] [CrossRef]

- Geffen, C.A.; Rothenberg, S. Suppliers and environmental innovation. Int. J. Oper. Prod. Manag. 2000, 20, 166–186. [Google Scholar] [CrossRef]

- Fergusson, H.; Langford, D.A. Strategies for managing environmental issues in construction organizations. Eng. Constr. Archit. Manag. 2006, 13, 171–185. [Google Scholar] [CrossRef]

- Daily, B.F.; Huang, S.-C. Achieving sustainability through attention to human resource factors in environmental management. Int. J. Oper. Prod. Manag. 2001, 21, 1539–1552. [Google Scholar] [CrossRef]

- Zhu, Q.; Sarkis, J.; Cordeiro, J.J.; Lai, K.-H. Firm-level correlates of emergent green supply chain management practices in the Chinese context. Omega 2008, 36, 577–591. [Google Scholar] [CrossRef]

- Reinhardt, F.L. Bringing the environment down to earth. Harv. Bus. Rev. 1999, 77, 149–158. [Google Scholar] [PubMed]

- Klassen, R.D.; Whybark, D.C. The impact of environmental technologies on manufacturing performance. Acad. Manag. J. 1999, 42, 599–615. [Google Scholar] [CrossRef]

- Venkatraman, N.; Ramanujam, V. Measurement of business performance in strategy research: A comparison of approaches. Acad. Manag. Rev. 1986, 11, 801–814. [Google Scholar]

- Chen, J.-S.; Tsou, H.-T.; Huang, A.Y.-H. Service delivery innovation. J. Serv. Res. 2009, 12, 36–55. [Google Scholar] [CrossRef]

- Zhu, Q.; Geng, Y.; Fujita, T.; Hashimoto, S. Green supply chain management in leading manufacturers: Case studies in Japanese large companies. Manag. Res. Rev. 2010, 33, 380–392. [Google Scholar] [CrossRef]

- Sarkis, J.; Cordeiro, J.J. An empirical evaluation of environmental efficiencies and firm performance: Pollution prevention versus end-of-pipe practice. Eur. J. Oper. Res. 2001, 135, 102–113. [Google Scholar] [CrossRef]

- De Giovanni, P. Do internal and external environmental management contribute to the triple bottom line? Int. J. Oper. Prod. Manag. 2012, 32, 265–290. [Google Scholar] [CrossRef]

- Montabon, F.; Sroufe, R.; Narasimhan, R. An examination of corporate reporting, environmental management practices and firm performance. J. Oper. Manag. 2007, 25, 998–1014. [Google Scholar] [CrossRef]

- Gounaris, S.P.; Papastathopoulou, P.G.; Avlonitis, G.J. Assessing the importance of the development activities for successful new services: Does innovativeness matter? Int. J. Bank Mark. 2003, 21, 266–279. [Google Scholar] [CrossRef]

- de Burgos-Jiménez, J.; Vázquez-Brust, D.; Plaza-Úbeda, J.A.; Dijkshoorn, J. Environmental protection and financial performance: An empirical analysis in Wales. Int. J. Oper. Prod. Manag. 2013, 33, 981–1018. [Google Scholar] [CrossRef]

- Berry, M.A.; Rondinelli, D.A. Proactive corporate environmental management: A new industrial revolution. Acad. Manag. Exec. 1998, 12, 38–50. [Google Scholar]

- Blazevic, V.; Lievens, A. Learning during the new financial service innovation process: Antecedents and performance effects. J. Bus. Res. 2004, 57, 374–391. [Google Scholar] [CrossRef]

- Chen, J.-S.; Tsou, H.-T.; Ching, R.K.H. Co-production and its effects on service innovation. Ind. Mark. Manag. 2011, 40, 1331–1346. [Google Scholar] [CrossRef]

- Stock, R.; Zacharias, N. Patterns and performance outcomes of innovation orientation. J. Acad. Mark. Sci. 2011, 39, 870–888. [Google Scholar] [CrossRef]

- Zhou, K.Z.; Gao, G.Y.; Yang, Z.; Zhou, N. Developing strategic orientation in china: Antecedents and consequences of market and innovation orientations. J. Bus. Res. 2005, 58, 1049–1058. [Google Scholar] [CrossRef]

- Siguaw, J.A.; Simpson, P.M.; Enz, C.A. Conceptualizing innovation orientation: A framework for study and integration of innovation research. J. Prod. Innov. Manag. 2006, 23, 556–574. [Google Scholar] [CrossRef]

- Oke, A. Innovation types and innovation management practices in service companies. Int. J. Oper. Prod. Manag. 2007, 27, 564–587. [Google Scholar] [CrossRef]

- Kinnear, T.C.; Taylor, J.R.; Ahmed, S.A. Ecologically concerned consumers: Who are they? J. Mark. 1974, 38, 20–24. [Google Scholar] [CrossRef]

- López-Gamero, M.; Claver-Cortés, E.; Molina-Azorín, J. Complementary resources and capabilities for an ethical and environmental management: A qual/quan study. J. Bus. Ethics 2008, 82, 701–732. [Google Scholar] [CrossRef]

- Papadopoulos, A.M.; Giama, E. Rating systems for counting buildings’ environmental performance. Int. J. Sustain. Energy 2009, 28, 29–43. [Google Scholar] [CrossRef]

- Avlonitis, G.J.; Papastathopoulou, P.G.; Gounaris, S.P. An empirically-based typology of product innovativeness for new financial services: Success and failure scenarios. J. Prod. Innov. Manag. 2001, 18, 324–342. [Google Scholar] [CrossRef]

- Hurley, R.F.; Hult, G.T.M. Innovation, market orientation, and organizational learning: An integration and empirical examination. J. Mark. 1998, 62, 42–54. [Google Scholar] [CrossRef]

- Ziegler, A.; Seijas Nogareda, J. Environmental management systems and technological environmental innovations: Exploring the causal relationship. Res. Policy 2009, 38, 885–893. [Google Scholar] [CrossRef]

- Egri, C.P.; Herman, S. Leadership in the north american environmental sector: Values, leadership styles, and contexts of environmental leaders and their organizations. Acad. Manag. J. 2000, 43, 571–604. [Google Scholar] [CrossRef]

- Armstrong, J.S.; Overton, T.S. Estimating nonresponse bias in mail surveys. J. Mark. Res. (JMR) 1977, 14, 396–402. [Google Scholar] [CrossRef]

- Podsakoff, P.M.; MacKenzie, S.B.; Lee, J.-Y.; Podsakoff, N.P. Common method biases in behavioral research: A critical review of the literature and recommended remedies. J. Appl. Psychol. 2003, 88, 879–903. [Google Scholar] [CrossRef] [PubMed]

- Lindell, M.K.; Whitney, D.J. Accounting for common method variance in cross-sectional research designs. J. Appl. Psychol. 2001, 86, 114–121. [Google Scholar] [CrossRef] [PubMed]

- Chin, W.W.; Marcolin, B.L.; Newsted, P.R. A partial least squares latent variable modeling approach for measuring interaction effects: Results from a monte carlo simulation study and an electronic-mail emotion/adoption study. Inf. Syst. Res. 2003, 14, 189–217. [Google Scholar] [CrossRef]

- Lohmoller, J.-B. The pls program system: Latent variables path analysis with partial least squares estimation. Multivar. Behav. Res. 1988, 23, 125–127. [Google Scholar] [CrossRef]

- Smith, J.B.; Barclay, D.W. The effects of organizational differences and trust on the effectiveness of selling partner relationships. J. Mark. 1997, 61, 3–21. [Google Scholar] [CrossRef]

- Hair, J.F., Jr.; Black, W.C.; Babin, B.J.; Anderson, R.E.; Tatham, R.L. Multivariate Data Analysis, 6th ed.; Pearson Education, Inc.: Upper Saddle River, NJ, USA, 2006; p. 899. [Google Scholar]

- Nunnally, J.; Bernstein, I. Psychometric Theory, 3rd ed.; McGraw-Hill Humanities: New York, NY, USA, 1994; p. 736. [Google Scholar]

- Fornell, C.; Larcker, D.F. Evaluating structural equation models with unobservable variables and measurement error. J. Mark. Res. (JMR) 1981, 18, 39–50. [Google Scholar] [CrossRef]

- Pavlou, P.A.; Sawy, O.A.E. From it leveraging competence to competitive advantage in turbulent environments: The case of new product development. Inf. Syst. Res. 2006, 17, 198–227. [Google Scholar] [CrossRef]

- Karimi, J.; Somers, T.M.; Bhattacherjee, A. The role of erp implementation in enabling digital options: A theoretical and empirical analysis. Int. J. Electron. Commer. 2009, 13, 7–42. [Google Scholar] [CrossRef]

© 2015 by the authors; licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

Weng, H.-H.; Chen, J.-S.; Chen, P.-C. Effects of Green Innovation on Environmental and Corporate Performance: A Stakeholder Perspective. Sustainability 2015, 7, 4997-5026. https://doi.org/10.3390/su7054997

Weng H-H, Chen J-S, Chen P-C. Effects of Green Innovation on Environmental and Corporate Performance: A Stakeholder Perspective. Sustainability. 2015; 7(5):4997-5026. https://doi.org/10.3390/su7054997

Chicago/Turabian StyleWeng, Hua-Hung (Robin), Ja-Shen Chen, and Pei-Ching Chen. 2015. "Effects of Green Innovation on Environmental and Corporate Performance: A Stakeholder Perspective" Sustainability 7, no. 5: 4997-5026. https://doi.org/10.3390/su7054997

APA StyleWeng, H.-H., Chen, J.-S., & Chen, P.-C. (2015). Effects of Green Innovation on Environmental and Corporate Performance: A Stakeholder Perspective. Sustainability, 7(5), 4997-5026. https://doi.org/10.3390/su7054997