The Impact of Educational Economic Factors on Institutional Sustainability Performance: The Mediating Role of Green Management Practices

Abstract

1. Introduction

2. Literature Review and Hypothesis

2.1. Educational Economic Factors in Higher Education Sustainability

2.2. Green Management Practices in Educational Institutions

2.3. Educational Economic Factors and Institutional Sustainability Performance

2.4. Educational Economic Factors and Green Management Practices

2.5. Green Management Practices Have a Mediating Effect on Institutional Sustainability Performance

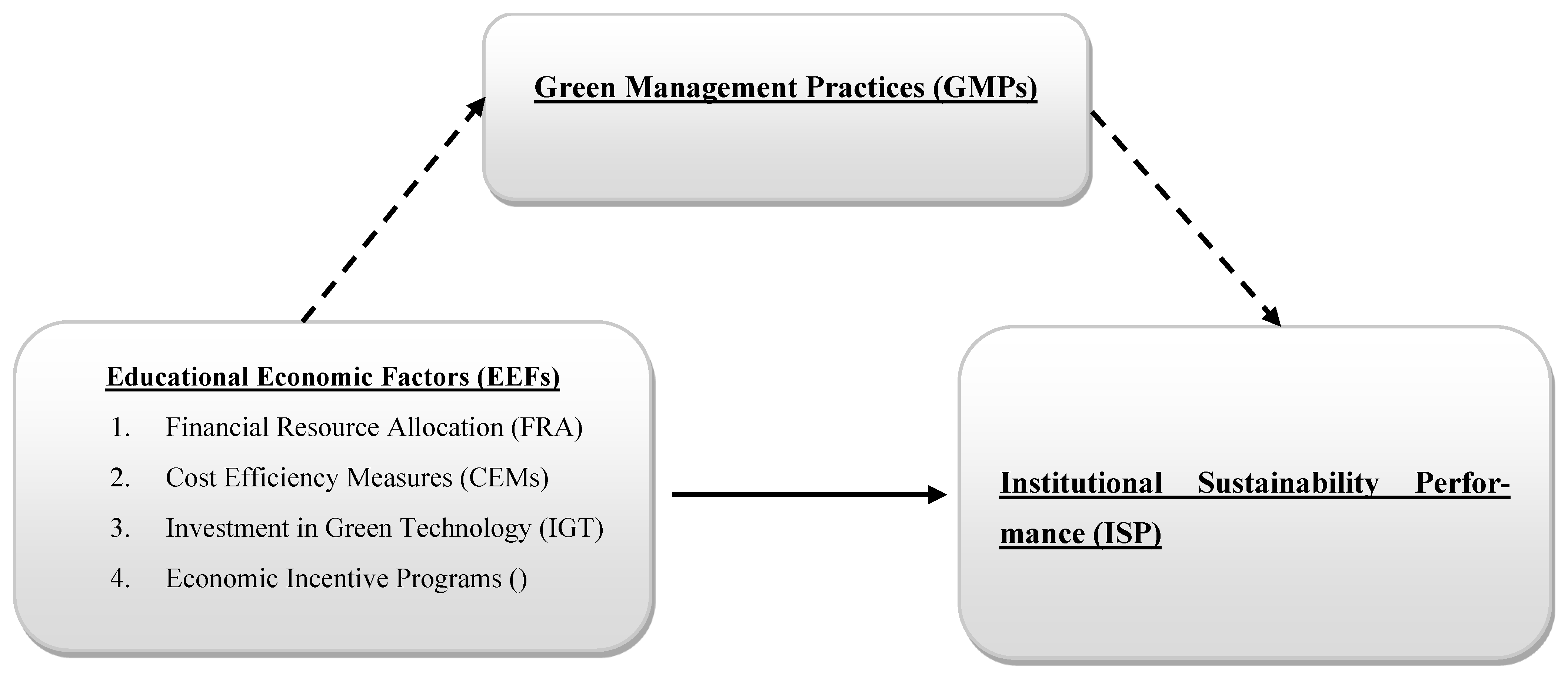

2.6. Research Framework

- The direct relationship between Educational Economic Factors (EEFs) and Institutional Sustainability Performance (ISP)

- The influence of EEFs on Green Management Practices (GMPs)

- The mediating role of GMPs in the relationship between EEFs and ISP

3. Materials and Methods

3.1. Subjects

3.2. Survey

4. Results

5. Discussion

6. Conclusions

7. Limitations and Suggestions for Future Studies

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Conflicts of Interest

References

- Bagire, V.; Arinaitwe, A.; Kakooza, J.; Aikiriza, F. Sustainable energy orientation in higher educational institutions: The effect of institutional pressures and organizational resources in a developing country context. Int. J. Energy Sect. Manag. 2024, 18, 999–1013. [Google Scholar] [CrossRef]

- Christou, O.; Manou, D.B.; Armenia, S.; Franco, E.; Blouchoutzi, A.; Papathanasiou, J. Fostering a Whole-Institution Approach to Sustainability through Systems Thinking: An Analysis of the State-of-the-Art in Sustainability Integration in Higher Education Institutions. Sustainability 2024, 16, 2508. [Google Scholar] [CrossRef]

- Abad-Segura, E.; González-Zamar, M.; Infante-Moro, J.C.; García, G.R. Sustainable Management of Digital Transformation in Higher Education: Global Research Trends. Sustainability 2020, 12, 2107. [Google Scholar] [CrossRef]

- Aleixo, A.M.; Azeiteiro, U.; Leal, S. The implementation of sustainability practices in Portuguese higher education institutions. Int. J. Sustain. High. Educ. 2018, 19, 146–178. [Google Scholar] [CrossRef]

- Almawishir, N.F.S.; Benlaria, H. Using the PLS-SEM Model to Measure the Impact of the Knowledge Economy on Sustainable Development in the Al-Jouf Region of Saudi Arabia. Sustainability 2023, 15, 6446. [Google Scholar] [CrossRef]

- Cáceres-Reche, M.P.; Tallón-Rosales, S.; Navas-Parejo, M.R.; De La Cruz-Campos, J.C. Influence of sociodemographic factors and knowledge in pedagogy on the labor market insertion of education science professionals. Educ. Sci. 2022, 12, 200. [Google Scholar] [CrossRef]

- Chen, T.; Kim, H.; Pan, S.; Tseng, P.; Lin, Y.; Chiang, P. Implementation of green chemistry principles in circular economy system towards sustainable development goals: Challenges and perspectives. Sci. Total Environ. 2020, 716, 136998. [Google Scholar] [CrossRef]

- Hameed, I.; Zaman, U.; Waris, I.; Shafique, O. A Serial-Mediation Model to Link Entrepreneurship Education and Green Entrepreneurial Behavior: Application of Resource-Based View and Flow Theory. Int. J. Environ. Res. Public Health 2021, 18, 550. [Google Scholar] [CrossRef]

- Alanazi, A.S.; Benlaria, H. Bridging Higher education outcomes and labour Market needs: A study of JOUF University graduates in the context of Vision 2030. Soc. Sci. 2023, 12, 360. [Google Scholar] [CrossRef]

- Amjad, F.; Abbas, W.; Zia-Ur-Rehman, M.; Baig, S.A.; Hashim, M.; Khan, A.; Rehman, H. Effect of green human resource management practices on organizational sustainability: The mediating role of environmental and employee performance. Environ. Sci. Pollut. Res. 2021, 28, 28191–28206. [Google Scholar] [CrossRef]

- Sančanin, B.; Penjišević, A.; Simjanović, D.J.; Ranđelović, B.M.; Vesić, N.O.; Mladenović, M. A fuzzy AHP and PCA approach to the role of media in improving education and the labor market in the 21st century. Mathematics 2024, 12, 3616. [Google Scholar] [CrossRef]

- Mian, S.H.; Salah, B.; Ameen, W.; Moiduddin, K.; Alkhalefah, H. Adapting universities for sustainability education in Industry 4.0: Channel of challenges and opportunities. Sustainability 2020, 12, 6100. [Google Scholar] [CrossRef]

- Nowotny, J.; Dodson, J.; Fiechter, S.; Gür, T.M.; Kennedy, B.; Macyk, W.; Bak, T.; Sigmund, W.; Yamawaki, M.; Rahman, K.A. Towards global sustainability: Education on environmentally clean energy technologies. Renew. Sustain. Energy Rev. 2018, 81, 2541–2551. [Google Scholar] [CrossRef]

- Filho, W.L.; Vargas, V.R.; Salvia, A.L.; Brandli, L.L.; Pallant, E.; Klavins, M.; Ray, S.; Moggi, S.; Maruna, M.; Conticelli, E.; et al. The role of higher education institutions in sustainability initiatives at the local level. J. Clean. Prod. 2019, 233, 1004–1015. [Google Scholar] [CrossRef]

- Patnaik, S.; Munjal, S.; Varma, A.; Sinha, S. Extending the resource-based view through the lens of the institution-based view: A longitudinal case study of an Indian higher educational institution. J. Bus. Res. 2022, 147, 124–141. [Google Scholar] [CrossRef]

- Tjahjadi, B.; Soewarno, N.; Mustikaningtiyas, F. Good corporate governance and corporate sustainability performance in Indonesia: A triple bottom line approach. Heliyon 2021, 7, e06453. [Google Scholar] [CrossRef] [PubMed]

- Al-Alawneh, R.; Othman, M.; Zaid, A.A. Green HRM impact on environmental performance in higher education with mediating roles of management support and green culture. Int. J. Organ. Anal. 2024, 32, 1141–1164. [Google Scholar] [CrossRef]

- Biancardi, A.; Colasante, A.; D’Adamo, I.; Daraio, C.; Gastaldi, M.; Uricchio, A.F. Strategies for developing sustainable communities in higher education institutions. Sci. Rep. 2023, 13. [Google Scholar] [CrossRef]

- Wang, M.; Li, Y.; Wang, Z. A nonlinear relationship between corporate environmental performance and economic performance of green technology innovation: Moderating effect of government market-based regulations. Bus. Strategy Environ. 2023, 32, 3119–3138. [Google Scholar] [CrossRef]

- Mansoor, A.; Jahan, S.; Riaz, M. Does green intellectual capital spur corporate environmental performance through green workforce? J. Intellect. Cap. 2021, 22, 823–839. [Google Scholar] [CrossRef]

- Ma, X.; Akhtar, R.; Akhtar, A.; Hashim, R.A.; Sibt-E-Ali, M. Mediation effect of environmental performance in the relationship between green supply chain management practices, institutional pressures, and financial performance. Front. Environ. Sci. 2022, 10. [Google Scholar] [CrossRef]

- Zhang, Q.; Ma, Y. The Impact of Environmental Management on Firm Economic Performance: The Mediating Effect of Green Innovation and the Moderating Effect of Environmental Leadership. J. Clean. Prod. 2021, 292, 126057. [Google Scholar] [CrossRef]

- Aleixo, A.M.; Leal, S.; Azeiteiro, U.M. Conceptualization of sustainable higher education institutions, roles, barriers, and challenges for sustainability: An exploratory study in Portugal. J. Clean. Prod. 2016, 172, 1664–1673. [Google Scholar] [CrossRef]

- Hsu, C.; Quang-Thanh, N.; Chien, F.; Li, L.; Mohsin, M. Evaluating green innovation and performance of financial development: Mediating concerns of environmental regulation. Environ. Sci. Pollut. Res. 2021, 28, 57386–57397. [Google Scholar] [CrossRef]

- Song, M.; Peng, L.; Shang, Y.; Zhao, X. Green technology progress and total factor productivity of resource-based enterprises: A perspective of technical compensation of environmental regulation. Technol. Forecast. Soc. Change 2022, 174, 121276. [Google Scholar] [CrossRef]

- Vasudevan, H. Resource-based view theory application on the educational service quality. Int. J. Eng. Appl. Sci. Technol. 2021, 6, 174–186. [Google Scholar] [CrossRef]

- Gupta, A.K.; Gupta, N. Environment Practices Mediating the Environmental Compliance and firm Performance: An Institutional Theory Perspective from Emerging Economies. Glob. J. Flex. Syst. Manag. 2021, 22, 157–178. [Google Scholar] [CrossRef]

- Khan, S.a.R.; Tabish, M.; Zhang, Y. Embracement of industry 4.0 and sustainable supply chain practices under the shadow of practice-based view theory: Ensuring environmental sustainability in corporate sector. J. Clean. Prod. 2023, 398, 136609. [Google Scholar] [CrossRef]

- Arda, O.A.; Montabon, F.; Tatoglu, E.; Golgeci, I.; Zaim, S. Toward a holistic understanding of sustainability in corporations: Resource-based view of sustainable supply chain management. Supply Chain Manag. 2021, 28, 193–208. [Google Scholar] [CrossRef]

- Makhloufi, L.; Laghouag, A.A.; Meirun, T.; Belaid, F. Impact of green entrepreneurship orientation on environmental performance: The natural resource-based view and environmental policy perspective. Bus. Strategy Environ. 2021, 31, 425–444. [Google Scholar] [CrossRef]

- Farrukh, A.; Mathrani, S.; Sajjad, A. A natural resource and institutional theory-based view of green-lean-six sigma drivers for environmental management. Bus. Strategy Environ. 2022, 31, 1074–1090. [Google Scholar] [CrossRef]

- Nandi, S.; Gonela, V.; Awudu, I. A resource-based and institutional theory-driven model of large-scale biomass-based bioethanol supply chains: An emerging economy policy perspective. Biomass Bioenergy 2023, 174, 106813. [Google Scholar] [CrossRef]

- Dahleez, K.A.; El-Saleh, A.A.; Al Alawi, A.M.; Abdel Fattah, F.A.M. Student Learning Outcomes and Online Engagement in Time of Crisis: The Role of E-Learning System Usability and Teacher Behavior. Int. J. Inf. Learn. Technol. 2021, 38, 473–492. [Google Scholar] [CrossRef]

- Budihardjo, M.A.; Ramadan, B.S.; Putri, S.A.; Wahyuningrum, I.F.S.; Muhammad, F.I. Towards Sustainability in Higher-Education Institutions: Analysis of Contributing Factors and Appropriate Strategies. Sustainability 2021, 13, 6562. [Google Scholar] [CrossRef]

- Zhang, S.; Wu, Z.; Wang, Y.; Hao, Y. Fostering Green Development with Green Finance: An Empirical Study on the Environmental Effect of Green Credit Policy in China. J. Environ. Manag. 2021, 296, 113159. [Google Scholar] [CrossRef]

- Ghardallou, W. Corporate Sustainability and Firm Performance: The Moderating Role of CEO Education and Tenure. Sustainability 2022, 14, 3513. [Google Scholar] [CrossRef]

- Ameer, F.; Khan, N.R. Green entrepreneurial orientation and corporate environmental performance: A systematic literature review. Eur. Manag. J. 2022, 41, 755–778. [Google Scholar] [CrossRef]

- Jamal, T.; Zahid, M.; Martins, J.M.; Mata, M.N.; Rahman, H.U.; Mata, P.N. Perceived Green Human Resource Management Practices and Corporate Sustainability: Multigroup Analysis and Major Industries Perspectives. Sustainability 2021, 13, 3045. [Google Scholar] [CrossRef]

- Habib, M.A.; Bao, Y.; Nabi, N.; Dulal, M.; Asha, A.A.; Islam, M. Impact of Strategic Orientations on the Implementation of Green Supply Chain Management Practices and Sustainable Firm Performance. Sustainability 2021, 13, 340. [Google Scholar] [CrossRef]

- Sahoo, S.; Vijayvargy, L. Green supply chain management practices and its impact on organizational performance: Evidence from Indian manufacturers. J. Manuf. Technol. Manag. 2021, 32, 862–886. [Google Scholar] [CrossRef]

- Asiaei, K.; Bontis, N.; Alizadeh, R.; Yaghoubi, M. Green intellectual capital and environmental management accounting: Natural resource orchestration in favor of environmental performance. Bus. Strategy Environ. 2021, 31, 76–93. [Google Scholar] [CrossRef]

- Ivascu, L.; Domil, A.; Sarfraz, M.; Bogdan, O.; Burca, V.; Pavel, C. New insights into corporate sustainability, environmental management and corporate financial performance in European Union: An application of VAR and Granger causality approach. Environ. Sci. Pollut. Res. 2022, 29, 82827–82843. [Google Scholar] [CrossRef] [PubMed]

- Chen, P. Curse or blessing? The relationship between sustainable development plans for resource cities and corporate sustainability—Evidence from China. J. Environ. Manag. 2023, 341, 117988. [Google Scholar] [CrossRef] [PubMed]

- Ali, Q.; Salman, A.; Parveen, S. Evaluating the effects of environmental management practices on environmental and financial performance of companies in Malaysia: The mediating role of ESG disclosure. Heliyon 2022, 8, e12486. [Google Scholar] [CrossRef]

- Hair, J.F.; Sarstedt, M.; Ringle, C.M. Rethinking some of the rethinking of partial least squares. Eur. J. Mark. 2019, 53, 566–584. [Google Scholar] [CrossRef]

- Hair, J.F.; Hult, G.T.M.; Ringle, C.M.; Sarstedt, M.; Danks, N.P.; Ray, S. Partial Least Squares Structural Equation Modeling (PLS-SEM) Using R; Classroom Companion: Business; Springer: Berlin/Heidelberg, Germany, 2021. [Google Scholar] [CrossRef]

- Henseler, J.; Hubona, G.; Ray, P.A. Using PLS path modeling in new technology research: Updated guidelines. Ind. Manag. Data Syst. 2016, 116, 2–20. [Google Scholar] [CrossRef]

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Characteristic | Category | N |

|---|---|---|

| Position | ||

| University Administrator | 45 | |

| Department Head | 42 | |

| Financial Manager | 35 | |

| Sustainability Officer | 24 | |

| Facility Manager | 22 | |

| University | ||

| Jouf University | 58 | |

| Hail University | 56 | |

| Northern Border University | 54 | |

| Years of Experience | ||

| <5 | 35 | |

| 5–10 | 72 | |

| >10 | 61 | |

| Department | ||

| Administration | 48 | |

| Finance | 42 | |

| Facilities | 38 | |

| Sustainability | 25 | |

| Other | 15 |

| Construct | Mean | SD |

|---|---|---|

| Educational Economic Factors (EEFs) | 4.215 | 0.682 |

| Financial Resource Allocation (FRA) | 4.386 | 0.712 |

| Cost Efficiency Measures (CEMs) | 3.892 | 0.845 |

| Investment in Green Technology (IGT) | 4.125 | 0.794 |

| Economic Incentive Programs (EIPs) | 4.158 | 0.756 |

| Green Management Practices (GMPs) | 4.076 | 0.823 |

| Institutional Sustainability Performance (ISP) | 4.142 | 0.768 |

| Items | Code | Loading | VIF | Cronbach’s Alpha | CR | AVE |

|---|---|---|---|---|---|---|

| Educational Economic Factors | ||||||

| ||||||

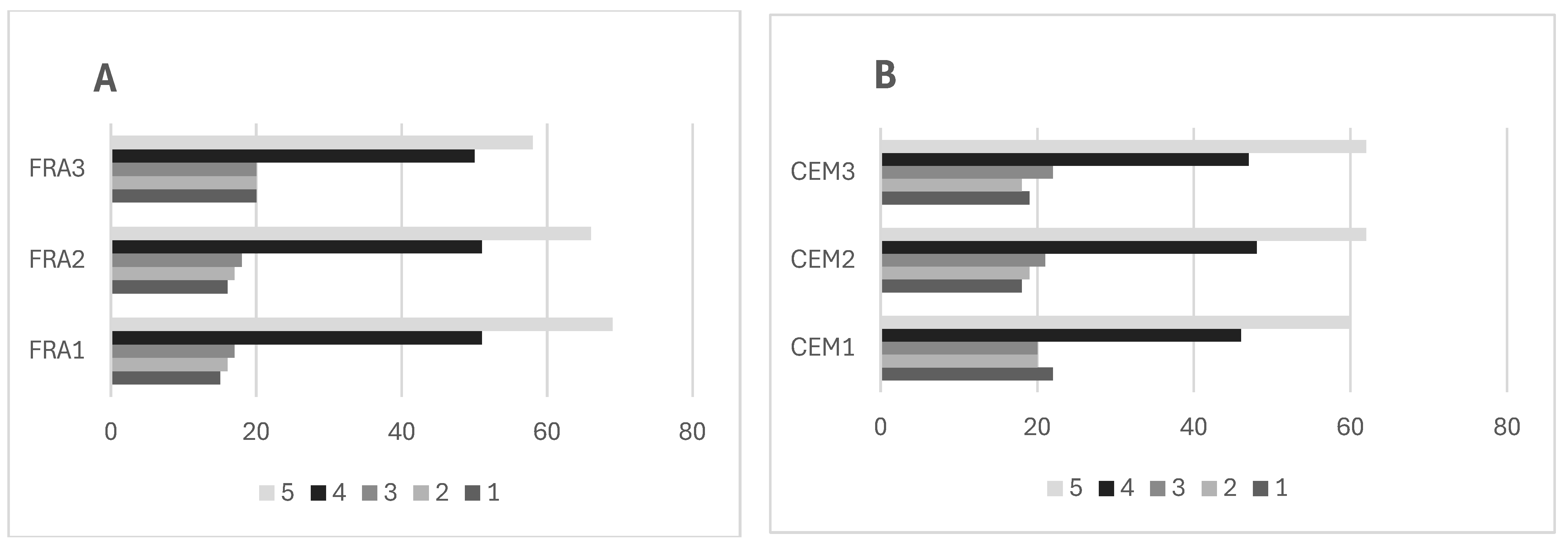

| Our university allocates adequate financial resources for implementing environmental sustainability initiatives. | FRA1 | 0.913 | 3.073 | 0.915 | 0.925 | 0.855 |

| Our institution’s budget planning process prioritizes funding for sustainability projects. | FRA2 | 0.937 | 3.392 | |||

| Financial resources are effectively distributed across different sustainability programs in our university. | FRA3 | 0.923 | 3.164 | |||

| ||||||

| Our university regularly implements cost-saving measures that support environmental sustainability. | CEM1 | 0.890 | 2.887 | 0.843 | 0.849 | 0.760 |

| We have effective systems in place to monitor and optimize resource consumption costs. | CEM2 | 0.886 | 2.852 | |||

| Our institution actively seeks ways to reduce operational costs through sustainable practices. | CEM3 | 0.840 | 1.555 | |||

| ||||||

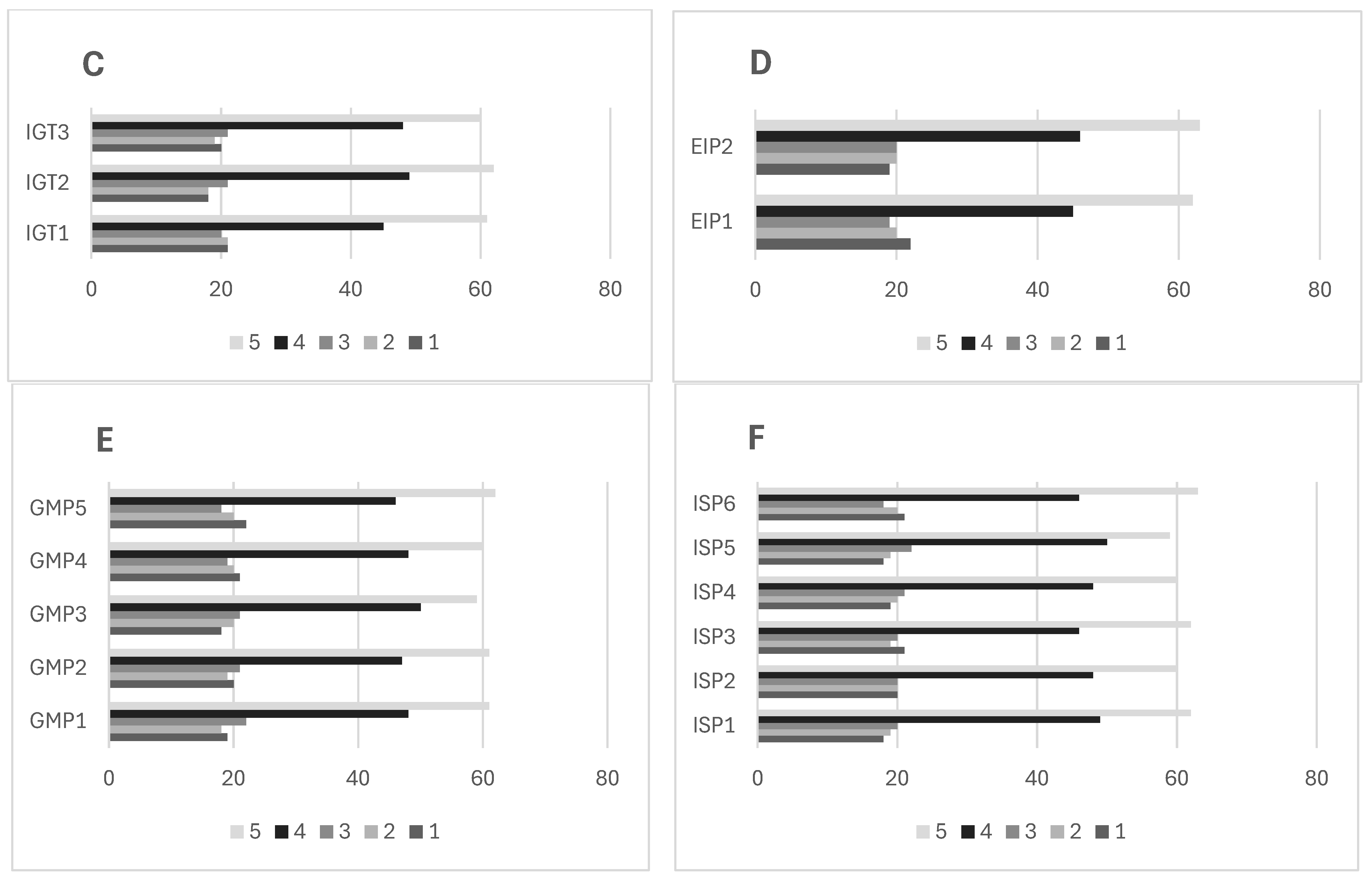

| Our university makes significant investments in environmentally friendly technologies. | IGT1 | 0.881 | 2.418 | 0.877 | 0.881 | 0.802 |

| We regularly upgrade our facilities with energy-efficient equipment and systems. | IGT2 | 0.920 | 2.932 | |||

| Our institution prioritizes investment in sustainable infrastructure development. | IGT3 | 0.886 | 2.169 | |||

| ||||||

| Our university offers financial incentives to departments that achieve sustainability targets. | EIP2 | 0.922 | 2.020 | 0.831 | 0.831 | 0.855 |

| We have established reward programs to encourage sustainable practices across the institution | EIP3 | 0.927 | 2.020 | |||

| Institutional Sustainability Performance (ISP) | ||||||

| Our university has achieved significant improvements in environmental performance. | ISP1 | 0.854 | 3.198 | 0.951 | 0.952 | 0.805 |

| We consistently meet our institutional sustainability targets. | ISP2 | 0.908 | 4.486 | |||

| Our environmental impact has notably decreased over time. | ISP3 | 0.891 | 4.070 | |||

| Our sustainability initiatives have produced measurable positive results. | ISP4 | 0.908 | 3.255 | |||

| Our university’s sustainability performance compares favorably with other institutions. | ISP5 | 0.925 | 3.393 | |||

| We have successfully implemented most of our planned sustainability projects. | ISP6 | 0.896 | 3.835 | |||

| Green Management Practices (GMPs) | ||||||

| Our university has comprehensive environmental management policies in place. | GMP1 | 0.729 | 1.530 | 0.828 | 0.848 | 0.594 |

| We actively implement waste reduction and recycling programs. | GMP2 | 0.633 | 1.475 | |||

| Environmental considerations are integrated into our operational decision-making. | GMP3 | 0.782 | 2.966 | |||

| Our green management practices are systematically monitored and evaluated. | GMP4 | 0.856 | 4.275 | |||

| We have effective environmental management systems across all university facilities. | GMP5 | 0.832 | 2.594 | |||

| ** Heterotrait–Monotrait Ratio (HTMT)—Matrix | * Fornell–Larcker Criterion | |||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| CEMs | EIPs | FRA | GMPs | IGT | ISP | CEMs | EIPs | FRA | GMPs | IGT | ISP | |

| CEMs | 0.872 | |||||||||||

| EIPs | 0.707 | 0.597 | 0.925 | |||||||||

| FRA | 0.760 | 0.579 | 0.732 | 0.505 | 0.924 | |||||||

| GMPs | 0.684 | 0.676 | 0.689 | 0.602 | 0.592 | 0.623 | 0.870 | |||||

| IGT | 0.821 | 0.814 | 0.656 | 0.761 | 0.719 | 0.697 | 0.591 | 0.676 | 0.896 | |||

| ISP | 0.595 | 0.803 | 0.384 | 0.507 | 0.754 | 0.547 | 0.717 | 0.363 | 0.475 | 0.694 | 0.897 | |

| Hypotheses | Relationships | Original Sample (O) | Standard Deviation (STDEV) | T Statistics (|O/STDEV|) | p Values | Decision |

|---|---|---|---|---|---|---|

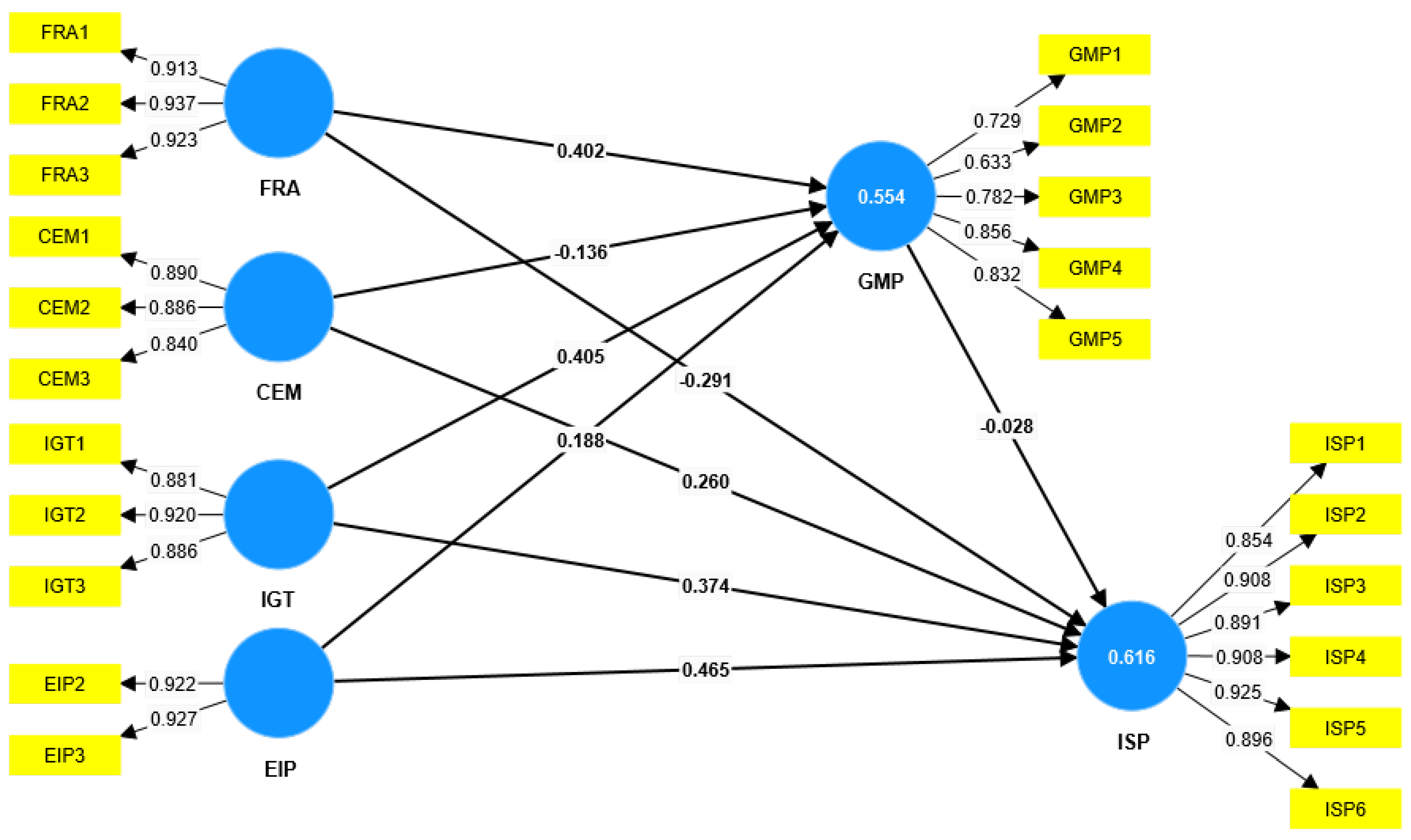

| H1a | FRA -> ISP | 0.291 | 0.087 | 3.344 | 0.001 | accept |

| H1b | CEMs -> ISP | 0.260 | 0.144 | 1.804 | 0.071 * | reject |

| H1c | IGT -> ISP | 0.374 | 0.099 | 3.776 | 0.000 ** | accept |

| H1d | EIPs -> ISP | 0.465 | 0.097 | 4.800 | 0.000 ** | accept |

| H2a | FRA -> GMPs | 0.402 | 0.122 | 3.288 | 0.001 ** | accept |

| H2b | CEMs -> GMPs | −0.136 | 0.148 | 0.916 | 0.360 | reject |

| H2c | IGT -> GMPs | 0.405 | 0.109 | 3.715 | 0.000 ** | accept |

| H2d | EIPs -> GMPs | 0.188 | 0.107 | 1.762 | 0.048 * | accept |

| Hypotheses | Relationships | Original Sample (O) | T Statistics (|O/STDEV|) | CI [2.5–97.5%] | p Values | Decision |

|---|---|---|---|---|---|---|

| H3a | FRA -> GMPs -> ISP | 0.191 | 4.248 | 0.085–0.266 | 0.001 ** | accept |

| H3b | CEMs -> GMPs -> ISP | 0.164 | 3.972 | 0.186–0.661 | 0.004 ** | accept |

| H3c | IGT -> GMPs -> ISP | 0.173 | 4.553 | 0.195–0.628 | 0.000 ** | accept |

| H3d | EIPs -> GMPs -> ISP | 0.145 | 3.919 | 0.269–0.647 | 0.041 * | accept |

| Path | Jouf (n = 58) β (t) | Hail (n = 56) β (t) | Northern (n = 54) β (t) | <5 Years (n = 35) β (p) | 5–10 Years (n = 72) β (p) | >10 Years (n = 61) β (p) | Jouf-Hail Diff (p) | Jouf-Northern Diff (p) | Hail-Northern Diff (p) |

|---|---|---|---|---|---|---|---|---|---|

| FRA -> ISP | 0.465 (4.82) ** | 0.323 (3.44) ** | 0.309 (3.28) ** | 0.312 (0.002) | 0.328 (0.001) | 0.342 (0.001) | 0.142 (0.042) * | 0.156 (0.038) * | 0.014 (0.428) |

| CEMs -> ISP | 0.260 (1.80) | 0.175 (1.54) | 0.136 (1.42) | 0.156 (0.084) | 0.168 (0.076) | 0.172 (0.068) | 0.085 (0.256) | 0.124 (0.186) | 0.039 (0.384) |

| IGT -> ISP | 0.374 (3.78) ** | 0.206 (2.24) * | 0.229 (2.36) * | 0.284 (0.004) | 0.296 (0.003) | 0.308 (0.002) | 0.168 (0.035) * | 0.145 (0.044) * | 0.023 (0.412) |

| EIPs -> ISP | 0.465 (4.80) ** | 0.293 (3.12) ** | 0.281 (3.02) ** | 0.326 (0.001) | 0.342 (0.001) | 0.356 (0.001) | 0.172 (0.008) ** | 0.184 (0.006) ** | 0.012 (0.445) |

| GMPs -> ISP | 0.402 (3.29) ** | 0.256 (2.86) ** | 0.244 (2.74) ** | 0.286 (0.003) | 0.298 (0.002) | 0.312 (0.002) | 0.146 (0.038) * | 0.158 (0.036) * | 0.012 (0.426) |

| R2 ISP | 0.616 | 0.584 | 0.572 | 0.584 | 0.596 | 0.608 | - | - | - |

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2025 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Benlaria, H.; Almawishir, N.F.S. The Impact of Educational Economic Factors on Institutional Sustainability Performance: The Mediating Role of Green Management Practices. Sustainability 2025, 17, 1260. https://doi.org/10.3390/su17031260

Benlaria H, Almawishir NFS. The Impact of Educational Economic Factors on Institutional Sustainability Performance: The Mediating Role of Green Management Practices. Sustainability. 2025; 17(3):1260. https://doi.org/10.3390/su17031260

Chicago/Turabian StyleBenlaria, Houcine, and Naeimah Fahad S. Almawishir. 2025. "The Impact of Educational Economic Factors on Institutional Sustainability Performance: The Mediating Role of Green Management Practices" Sustainability 17, no. 3: 1260. https://doi.org/10.3390/su17031260

APA StyleBenlaria, H., & Almawishir, N. F. S. (2025). The Impact of Educational Economic Factors on Institutional Sustainability Performance: The Mediating Role of Green Management Practices. Sustainability, 17(3), 1260. https://doi.org/10.3390/su17031260