1. Introduction

Nowadays, the integration of the global economy is accelerated, techno-logical innovation is accelerated, geopolitical and macroeconomic fluctuations are more intensive, and more grave sustainability concerns like global warming, resource deficiencies, and expanding social responsibility severely impact enterprise survival and sustainable development [

1]. Although integration trends persist, anti-globalization views and growing trade tensions have resulted in the spectacular growth in world trade significantly decelerating. As per a UNCTAD report, global trade volume declined by approximately USD 1.5 trillion during 2023, falling 5% year-on-year. Amidst the external drags, enhancing and sustaining firm performance has become a core necessity for all organizations worldwide, including Chinese companies, to survive and thrive amidst turmoil. Company performance is not only a simple measure of a company’s health and management effectiveness but also critical to its adaptability, creativity, and competitiveness in a complex and dynamic environment. In-depth examination of company performance can allow companies to know their strengths and weaknesses precisely, optimize resource allocation and decision-making effectiveness, and thus formulate more promising and sustainable strategies to achieve long-term value creation and sustainable competitive advantages under a tougher competitive market and an uncertain external world. Therefore, enhancing company performance in a complicated and dynamic setting has become an unavoidable mission for scholars and practitioners.

In such a scenario, executive cognitive flexibility becomes increasingly vital, becoming a key requirement for firms to achieve greater performance under turbulent conditions. Cognitive flexibility, as a core cognitive style, refers to the executive’s ability to use diverse problem-solving strategies in a versatile way when encountering complex changes in the internal and external environment in order to effectively synthesize heterogeneous information, break through fixed cognition patterns, and dynamically adjust decision-making procedures [

2]. This capacity compels businesses to quickly respond to trends in the marketplace, streamline internal operational effectiveness, and encourage ongoing innovation and expansion through impact on organizational culture and allocation of resources [

3]. A timeless illustration is how, during the 1980s, General Electric’s legendary CEO, Jack Welch, precisely exemplified Upper Echelons Theory’s fundamental premise by utilizing his cognitive flexibility in the face of a rapidly developing market and internal inefficiency. It holds that corporate strategy and performance are significantly influenced by the CEO’s personal and cognitive styles. As a principal member of GE’s “upper echelon,” Welch’s unique “cognitive filter” allowed him to move beyond traditional thinking and intensely feel the new paradigm of globalization and efficiency supremacy. Based on high cognitive flexibility, he dropped the traditional “big and overarching” idea and introduced the “Be Number One or Number Two” business philosophy. He aggressively sold or closed over 200 money-losing businesses and rolled more than 40 business units into fewer than 20. All these restructuring actions were difficult decisions that Welch made based on his own cognition and values. These adaptive strategies, triggered by Welch’s cognitive flexibility, ultimately drove GE to radical restructuring and consistent growth. This supports the argument of Upper Echelons Theory: a top executive’s profound cognition influences the foundation for formulating adaptive strategies so that a company can attain consistent competitive advantage and growth in dynamic environments. However, existing literature is still lacking in an extensive and systematic examination of the inherent mechanisms through which executive cognitive flexibility acts, particularly on firm performance, particularly its dynamic impact channels in complex and unpredictable environments.

In the scenario of an increasingly complex and unstable global business landscape, traditional market rivalry is increasing, forcing companies to seek differentiated advantages and strategic resources through non-market channels [

4]. This is the trend of business today. As pursuing economic benefits, non-market forces such as regulations and policies, social tendencies, popular opinion, and increasingly intense environmental problems are progressively supporting their power over corporate operational sustainability and long-term stability. Particularly in China’s unique socialist market economy system, its ever-improving legal and regulative environment, complex social ecology, and emphasis on ecological civilization construction and high-quality development make non-market forces profoundly affect corporate operations and performance. Executive cognitive flexibility here not only influences their keen insight into market opportunities but also has a considerable influence on their perception, interpretation, and response to non-market opportunities and challenges. More importantly, Corporate Social Responsibility (CSR) and Corporate Political Activity (CPA), being two of the key components of non-market strategy, largely rely upon the strategic ability and flexibility of executives in order to be effectively implemented. Executive cognitive flexibility enables them to more sensitively respond to potential environmental threats, social norms, and government opportunities in the non-market environment and nimbly change CSR investments and CPA strategies to better accommodate the specific needs of the Chinese market. This versatility not only creates new strategic space for enhancing the performance of companies but, above all, allows companies to build sustainable, environmentally friendly, socially responsible, and well-governed competitive powers, thereby propelling long-term sustainable value creation. Therefore, with non-market strategy as a key mediating variable between executive cognitive flexibility and firm performance, there can be a more comprehensive and detailed explication of the complex mechanisms through which executive cognitive flexibility influences enterprise sustainable development, giving birth to richer theoretical implications and practical recommendations on grasping the determinants of firm performance in China.

Despite existing research having focused on the impact of executives on firm performance, it has primarily concentrated on entrepreneurial identity [

5], executive heterogeneity [

6], and executive compensation [

7] on firm performance. Furthermore, only a small number of studies have examined the impact of executive cognition on firm performance [

8], but these have been conducted in static environments, lacking an exploration of the mechanisms through which executive cognition, particularly executive cognitive flexibility, influences firm performance in dynamic environments.

In brief, to address the research gap on the mechanisms by which executive cognitive flexibility influences firm performance, this paper, using data of Chinese A-share listed firms for 2016–2022, develops an executive cognitive flexibility index via text analysis and tests its effect on firm performance empirically. Meanwhile, under the “cognition–behavior–performance” paradigm, non-market strategy is proposed as a mediating variable. The paper proves that executive cognitive flexibility has a positive effect on firm performance, and non-market strategy mediates between them. Particularly, executive cognitive flexibility improves firm performance by decreasing the taking of social responsibility and escalating corporate political activity.

In comparison to current literature, the research findings of this paper can be primarily illustrated as below: Firstly, there is limited current research on executive cognitive flexibility. Based on an empirical study, the paper identifies that executive cognitive flexibility has a positive impact on business performance, and, at the same time, non-market strategy would take an intermediary variable, namely, operating under the mechanism of two modes: corporate social responsibility and political activity. Secondly, there is an imperative guide value for the management practice of corporations. This study stresses that there is great significance for executive cognitive flexibility development, which could help executives achieve an integrated and future-visionary vision of the market, as well as the non-market environment, making corporations grasp strategic opportunities. Meanwhile, there is an introduction and explanation of non-market strategic channels, which have an advantage for corporations to explore and capitalize benefits of non-market opportunities, achieving differentiation advantages based on building a non-market strategic system for core business.

The research paper is as below: The literature of executive cognitive flexibility and firm performance is elaborated, and defects of the theory of existing research are mentioned in the second part, based on upper echelon theory and stakeholder theory, etc. In the third part, based on existing research, a research framework is established based on upper echelon theory and stakeholder theory, etc. Executive cognitive flexibility impacts on firm performance are elaborated, and the mechanistic channels of non-market strategies, i.e., the above-mentioned two channels of corporate social responsibility and corporate political activities, are examined. The research approach of sample selection and variable measurement is elaborated in the fourth part. Empirical results analysis of descriptive statistics, correlation analysis, multiple linear regression analysis, robust checking, and heterogeneity analysis of sample data is provided in the fifth part. Directions for future research and recommendations for companies to strengthen executive cognitive flexibility to promote development are provided in the abstract of the sixth part of the paper.

4. Research Design

4.1. Data Sources and Sample Selection

This paper uses a panel dataset of Chinese A-share listed firms between 2016 and 2022 to test our hypotheses empirically. Data for our major variables were collected from a number of authoritative databases. Data for the construction of the executive cognitive flexibility index were retrieved from the Management Discussion and Analysis (MD&A) section of firm annual reports, which were collected from the WIND database, the official websites of the Shanghai and Shenzhen Stock Exchanges, and Juchao Information Network (

www.cninfo.com.cn). Data on corporate social responsibility (CSR) were collected from the dedicated CSR module in the CSMAR database. Data for corporate political activity and all the other firm-level financial and governance variables were also collected from the CSMAR database.

To construct the final sample, we applied the following screening criteria:

- (1)

Exclusion of Financial and Public Utility Firms: We removed companies from the financial and public utility sectors. These sectors operate under unique business models, distinct accounting standards, and highly specific regulatory environments. Their differing competitive dynamics and governance structures could potentially obscure the true relationship between executive cognition, non-market strategies, and firm performance.

- (2)

Exclusion of ST and *ST Designated Firms: We excluded firms that were labeled as ST (Special Treatment) or *ST (Particular Transfer), i.e., under the threat of being delisted. The purpose of this exclusion was to rid our analysis of the confounding effects of severe financial distress.

- (3)

Exclusion of Firms with Significant Missing Data: Any observations with missing values for executive cognitive flexibility, firm performance, non-market strategies (CSR and CPA), or any control variables were excluded from the analysis. This ensures the robustness of our results across all observed variables.

Despite these necessary sample exclusions, our final dataset comprises 13,586 unbalanced panel data samples, which is still broad and broadly representative. By removing some industries like finance and public utilities, the remaining sample still covers a broad distribution of Chinese A-share listed companies over various core sectors, including manufacturing, information technology, real estate, and wholesale and retail. This broad coverage ensures that our research results represent typical patterns found in the majority of companies. The large sample size in this way leaves us with sufficient statistical power for this study to easily identify significant relationships among variables.

4.2. Model Specification and Variable Definition

To test our hypotheses, we follow the causal steps approach and specify a series of Ordinary Least Squares (OLS) regression models with industry and year fixed effects.

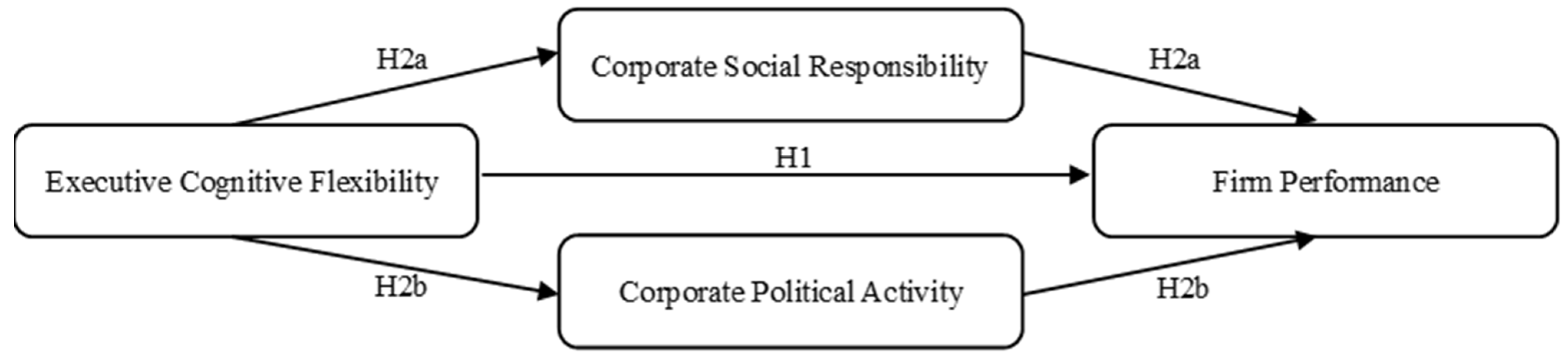

First, to test the direct effect of executive cognitive flexibility on firm performance (H1), we estimate the following model:

In Model (1), TobinQ represents firm performance, CF represents executive cognitive flexibility, Control represents the selected control variables, Year represents year fixed effects, and Ind represents industry fixed effects. Through OLS regression of Model (1), the primary focus is on the coefficient α1.

Next, to test the mediating role of non-market strategies (H2a and H2b), we construct the following models:

These models define CSR as corporate social responsibility and CPB as corporate political behavior; all other variables remain consistent with Model (1). Using OLS regression, Model (2) primarily focuses on coefficient β1, while Model (3) centers on coefficient β4. For Model (4), we examine coefficients γ1 and γ2, and for Model (5), we look at coefficients γ5 and γ6. Models (2) and (4) are designed to verify the mediating role of corporate social responsibility, whereas Models (3) and (5) aim to verify the mediating effect of corporate political behavior. Specifically, if β1, γ1, and γ2 are all significant in Models (2) and (4), this indicates that CSR acts as a mechanism through which executive cognitive flexibility enhances firm performance, though it may not be the sole mechanism. The same logic applies to the mediating effect of CPB in Models (3) and (5).

4.2.1. Dependent Variable

Firm Performance (Tobin’s Q): Tobin’s Q is defined as the ratio of a company’s stock market value to the replacement cost of its capital. It is more than just an indicator that measures a firm’s current asset value and its ability to generate sufficient returns from new investments. More importantly, it can transcend short-term accounting data to comprehensively capture the market’s holistic expectations and assessment of a firm’s future growth potential, innovation capabilities, brand reputation, and unique intangible assets. This includes, for instance, government relations and social capital accumulated through its non-market strategies [

44].

4.2.2. Independent Variable

Executive Cognitive Flexibility (CF): Following the research of Deng [

15], textual analysis is conducted on the Management Discussion and Analysis (MD&A) section of listed companies’ annual reports. The MD&A describes the company’s operating performance during the reporting period and its outlook for future development, directly or indirectly reflecting the direction and focus of managers’ attention. Since cognitive flexibility is the ability of managers to capture changes in the external environment and promptly adjust cognitive strategies, it is reflected by capturing keywords related to the perception of the external environment. Python 3.11 is used to count the frequency of keywords related to external environment perception, and this count is divided by the total number of characters in the annual report text (in thousands of characters). To ensure consistent dimensionality, the resulting ratio is multiplied by 100.

4.2.3. Mediating Variables: Non-Market Strategies

Corporate Social Responsibility (CSR): Following Hu and Li [

45], we measure the quality and credibility of CSR reporting, rather than just its existence. CSR is an index calculated as the average of two binary indicators: (1) a value of 1 if the firm’s CSR report has been independently audited by a third party, and 0 otherwise; and (2) a value of 1 if the report explicitly references the Global Reporting Initiative (GRI) Sustainability Reporting Guidelines, and 0 otherwise. This measure captures the firm’s commitment to standardized and verifiable CSR practices.

Corporate Political Activity (CPA): In China’s distinctive market environment, a company’s ability to forge and maintain strong ties with the government is paramount for its survival and growth. These connections often become crucial conduits for acquiring vital resources. Charitable donations, in this context, transcend mere fulfillment of social responsibility; they are a strategic non-market investment. Their purpose is to cultivate positive interactions with the government, thereby securing essential resources and competitive advantages for the enterprise [

46]. Consequently, this study quantifies corporate political behavior by using the ratio of charitable donations to total assets, a methodology adopted from Cheng and Geng [

47]. To ensure consistent dimensionality, the resulting ratio is multiplied by 1000.

4.2.4. Control Variables

This paper introduces six control variables: Asset Growth, Gross Profit, Liquid Ratio, TOP1 (shareholding ratio of the largest shareholder), Der (debt-to-equity ratio), and Board (executive team size).

All models include Year and Industry fixed effects to account for unobserved factors that vary over time and across industries.

The main variables and their definitions are shown in

Table 1.

5. Empirical Results and Analysis

5.1. Descriptive Statistics and Correlation Analysis

Table 2 presents the descriptive statistics for the key variables. For executive cognitive flexibility, the values range from 0.000 to 1.030, with a mean of 0.240 and a standard deviation of 0.070, indicating a notable degree of variation across the sample firms. Corporate social responsibility (CSR) exhibits even greater dispersion, with a range of 0 to 2 and a standard deviation of 0.345. This suggests significant heterogeneity in the level of social responsibility engagement among firms. The range of values for corporate political behavior is between 0.000 and 16.090, indicating a certain gap in corporate political actions.

Table 3 presents the variable correlation coefficient matrix. The results show that all correlation coefficients between variables in the matrix are less than 0.7. Simultaneously, TobinQ is significantly positively correlated with executive cognitive flexibility (CF) and corporate political activity (CPA), and significantly negatively correlated with corporate social responsibility (CSR). Executive cognitive flexibility (CF) is significantly negatively correlated with corporate social responsibility (CSR) and significantly positively correlated with corporate political activity (CPA). These results are consistent with our expectations.

5.2. Baseline Regression

Table 4 shows the findings of the OLS regression analysis examining the impact of executive cognitive flexibility on firm performance. We report the findings stepwise to illustrate the stability of our results.

Column (1) presents a parsimonious specification featuring just our independent variable, executive cognitive flexibility (CF), but no control variables. The coefficient for CF is positive and statistically significant (α = 1.0357, p < 0.01), offering initial support for a positive link between executive cognitive flexibility and firm performance.

Column (2) reports the results for our complete specification as outlined in Model (1), with the complete set of control variables and year and industry fixed effects. The coefficient on executive cognitive flexibility (CF) is still positive and highly significant (α1 = 0.8486, p < 0.01). This offers strong empirical confirmation of Hypothesis 1 in that executives with higher cognitive flexibility are indeed linked to better firm performance.

This implies that executive cognitive flexibility not only indicates managers’ profound awareness of the external environment’s complexity and uncertainty but also their capacity for effective decision-making, strategy adjustment, and resource allocation optimization in the face of changing circumstances. In dynamic environments, executives with cognitive flexibility have the capacity to promptly detect and respond to external changes, flexibly combine information and insights from different sources, and then make decisions that favor the company’s growth and firm performance.

The findings for our control variables are generally in line with previous literature. Both Gross Profit and Liquidity Ratio are positively and significantly related to firm performance, which supports the expectation that greater profitability and higher short-term solvency lead to better firm valuation. In contrast, Ownership Concentration (TOP1) and Board Size are negatively and significantly related to firm performance. The negative coefficient on TOP1 is possibly due to the entrenchment effect, in that a dominant, largest shareholder might make decisions that benefit private interests at the cost of firm value. The negative impact of board size supports theories of group dynamics, which argue that larger boards tend to have slower decision-making processes, coordination problems, and diffusion of responsibility, all of which are harmful to firm performance.

5.3. Endogeneity and Robustness Tests

To accommodate consideration of establishing baseline validity of estimates, as for criticism of endogeneity, various robustness checks were executed.

Table 4 presents the findings.

(1) Addressing Endogeneity with Instrumental Variables (IV)

One of our main endogeneity issues is reverse causality, for which good-performing companies have resources to spare for hiring or building more cognitively flexible executives. To account for that, we use an IV 2SLS (two-stage least squares) regression. As the classical method used in the literature of strategic management and corporate finance, such as that of Dong et al. [

48], including us, we use the one-period lag of the independent variable (CF

t−1) of an instrument of the current executive cognitive flexibility (CF

t). It is worth using a lag of a variable as an instrument because, by definition, they are correlated with their own current value (relevance) but have smaller chances of being correlated with the error term of the current period (exclusion restriction) because historical cognitive flexibility is impossible to be driven by future performance shocks.

Column (1) of

Table 5 reports the 2SLS regression. Our first-stage results affirm the validity of the instrument. While the null hypothesis of underidentification of the model is rejected by the Kleibergen-Paap rk LM underidentification statistic of 0.000 (

p = 0.000), its corresponding F-statistic, 194.07, is strongly bigger than the Stock-Yogo critical value for 10% maximal IV size, suggesting that our instrument is far, very far indeed, from being weak. In the second stage, the instrumented executive cognitive flexibility remains positive and significant. This means that even adjusting for its possible endogeneity, its positive effect of executive cognitive flexibility on firm performance still persists, and as such, makes us even convinced of Hypothesis 1.

(2) Heckman Test

To address potential sample selection bias in the testing of the effect of executive cognitive flexibility on the performance of firms, we use the Heckman two-stage model. We estimate the inverse Mills ratio (IMR) in the first stage in a Probit model. In the second stage, we incorporate the IMR as a control variable into the conventional regression equation, which we use in the testing of the effect of executive cognitive flexibility on firm performance. By incorporating the IMR into the model, we can remove potential selective bias that can hamper our research results. Regression outcome with the incorporation of the IMR is presented in

Table 5, column (2). We notice that the regression coefficient of executive cognitive flexibility on firm performance continues to be significantly positive, as is the situation without correcting for selection bias. This provides stronger assurance for the validity of our study results.

(3) Propensity Score Matching (PSM)

To overcome possible endogeneity due to self-selection bias, we adapted the method of Propensity Score Matching (PSM). For that, our sample is split into the group of high executive cognitive flexibility (the treatment group) and the group of low executive cognitive flexibility (the control group) along the executive cognitive flexibility median line. Then, propensity scores have been estimated based on Asset Growth, Gross Profit, Li-uid, TOP1, Der, and Board as controls and did 1:1 nearest-neighbor matching. Column (3) of

Table 5 reports regression outcomes on the matched sample, where the regression coefficient of executive cognitive flexibility is still astonishingly positive at 1%, as is also for the regression results of the present study.

(4) Alternative Measure of the Dependent Variable

To ensure that our findings are not being pulled by a single measure of firm performance, we also conduct a robustness check based on an alternative measure. Instead of Tobin’s Q, based on market measures, which is an accounting-based measure commonly used, we employ Return on Assets (ROA) as an alternative accounting-based measure. Whereas Tobin’s Q reflects market perceptions, as well as future prospects, ROA reflects the firm’s historical operational efficiency of generating profit out of its asset base. By re-estimating our baseline model where ROA is being viewed as the dependent variable, we can study the generalizability of our findings. As can be seen from Column (4) of

Table 5, the executive cognitive flexibility variable still has a positive and significant impact, and our main finding is also robust across different measures of performance.

(5) Controlling for Industry-by-Year Fixed Effects

Our baseline regression includes separate fixed effects for industries and for each year. To take into consideration potentially relevant, but otherwise unknown, time-varying shocks that might have extremely different effects across industries, however, an even stronger fixed-effects definition is used. We exclude the separate fixed effects for industries and for each year and include fixed effects for interactions of industries by years. This technique accounts for whatever otherwise unidentified heterogeneity is shared across all those firms belonging to each given pair of industry and year. Column (5),

Table 5 reports results that show that the executive cognitive flexibility is still significant and unchanged, thereby affirming the robustness of our main result.

(6) Using a Lagged Dependent Variable

It is plausible that the effects of executive cognition on firm performance are not instantaneous and may manifest over time. To account for this possibility and to mitigate concerns about dynamic endogeneity, we re-estimate our model with the dependent variable (Tobin’s Q) lagged by one period. As reported in Column (6) of

Table 5, the positive and significant association between executive cognitive flexibility and future firm performance persists. This result not only demonstrates the robustness of our findings but also suggests that the influence of executive cognition on performance is enduring.

5.4. Mechanism Test

We now test the mediating roles of corporate social responsibility (CSR) and corporate political activity (CPA) in the relationship between executive cognitive flexibility and firm performance. The results are presented in

Table 5.

5.4.1. The Mediating Role of Corporate Social Responsibility (CSR)

Table 6, columns (1) and (3), reveals that in Model (2), executive cognitive flexibility significantly reduces the undertaking of corporate social responsibility (CSR) (β

1 = −0.4993,

p < 0.01). This finding likely stems from the current Chinese context, where CSR requirements are often ambiguous, and ESG information disclosure is largely encouraged rather than mandated. Faced with limited resources and a volatile external environment, cognitively flexible executives, upon recognizing the importance of short-term financial returns, strategically choose to reduce the adoption of non-mandatory CSR initiatives. This allows them to reallocate finite resources toward core business activities that yield quicker economic benefits. In Model (4), cognitive flexibility remains significantly positively related to firm performance (γ

1 = 0.7715,

p < 0.01), while interestingly, CSR is significantly negatively related to firm performance (γ

2 = −0.1543,

p < 0.01). This combination of results further supports Hypothesis 2a. It indicates that executives, through their cognitive flexibility, influence the “behavioral” choice regarding CSR, which ultimately leads to an improvement in firm performance. This robustly validates the proposed “cognition–behavior–performance” logical chain.

5.4.2. The Mediating Role of Corporate Political Activity (CPA)

Table 6, columns (2) and (4), reveals that in Model (3), executive cognitive flexibility significantly enhances the implementation of corporate political behavior (CPB) (β

4 = 0.2316,

p < 0.01). This suggests that when cognitively flexible executives “perceive” the bottlenecks arising from a rapidly changing external environment and the necessity of resource acquisition, their “behavior” involves actively identifying and leveraging various social resources. These resources include interpersonal networks, industry alliances, and government relationships, leading to swift political action. In Model (5), cognitive flexibility is significantly positively related to firm performance (γ

5 = 0.7827,

p < 0.01), and simultaneously, political behavior is also significantly positively related to firm performance (γ

6 = 0.2845,

p < 0.01). This dual significance provides strong support for Hypothesis 2b. It further clarifies that executives, through their cognitive flexibility, drive strategic political “behavior,” which in turn helps firms secure more external resources, gain a competitive edge, and ultimately improve firm performance. This thoroughly validates the “cognition–behavior–performance” logical framework.

5.5. Heterogeneity Test

In order to explore the boundary conditions of our main findings, we investigated whether the impact of executive cognitive flexibility on firm performance varies depending on the internal and external environment of the company.

5.5.1. Differences in Internal Firm Environment

(1) Differences in CEO Overseas Background

As representatives of top management, CEOs’ international experience may shape their cognitive structures, information processing styles, and strategic choice preferences [

49], thereby influencing the mechanism through which executive cognitive flexibility affects firm performance. CEOs without an overseas background are often more adapted to the local business environment and have a deeper understanding of the domestic market compared to those with overseas backgrounds. Consequently, their cognitive flexibility may allow them to more swiftly perceive and grasp local market information and make quicker decisions and judgments. Based on this, this study examines whether the CEO has an overseas background (Oversea) as a contextual variable for heterogeneity analysis, assigning a value of 1 to firms where the CEO has an overseas background, and 0 otherwise. The regression results are presented in

Table 7, columns (1) and (2). When the CEO has no overseas background, the impact of executive cognitive flexibility on firm performance is significantly positive. However, for firms where the CEO has an overseas background, the impact of executive cognitive flexibility on firm performance is not significant.

(2) Differences in Firm Size

Firm size, being an organizational structural characteristic of utmost significance, may influence the channel by which executive cognitive flexibility influences firm performance via fluctuation in resources, organisational complexity, and market influence. Large firms, due to their enormous organisational breadth and multifaceted operations, need higher levels of macro-strategic direction and complex information processing capability from their top executives [

50]. In these firms, cognitive flexibility might be of greater strategic value. Conversely, small firms, with their limited resources and flatter organizational structures, will be highly reliant on direct action and velocity of market response as drivers of performance and, therefore, can potentially have divergent paths to executive cognitive flexibility. Firm size is thus introduced into this paper as a factor to be examined. Based on Shen and Yin’s [

51] work, the firm size is calculated by the natural logarithm of total assets. Large firms whose size is greater than the mean are assigned the value of 1; the rest are assigned 0. Columns (3) and (4) of

Table 7 report the results. The impact of executive cognitive flexibility on firm performance is positive and significant in big firms. However, in small businesses, this effect is minimal. This implies that bigger companies require executives to demonstrate more macro-level regulation, as well as complex problem-solving abilities, where cognitive flexibility is the core element.

(3) Differences in Executive Concurrent Positions

Considering that high-level managers’ external relationships and potential conflicts of interest may significantly influence the application of their cognitive flexibility and its impact on firm performance, this paper introduces a context variable: whether DSSE simultaneously occupies offices in shareholder units for heterogeneity analysis. Where DSSE simultaneously occupies offices in shareholder units, it is threatened with dual agency relationships and multiple objective conflicts [

52]. This dual commitment may lead to a diversion of executives’ strategic attention and cognitive effort in the process of strategic decision-making. That is, their decisions would be more obviously influenced by the specific interests of the shareholder unit, rather than by a sole motivation to maximize the aggregate interest of the firm. This potential entanglement of interests and mental bias could compromise the independence and effectiveness of executive cognitive flexibility in improving overall firm performance, essentially transforming the direct impact mechanism of cognitive flexibility on firm performance. We included Executive Concurrent Positions (IsCocurP) in further analysis in compliance with the research of Yan et al. [

53]. This variable equals 1 if and only if any DSSE holds a position in a shareholder unit at the same time, and 0 otherwise. The estimated regression results presented in Columns (5) and (6) of

Table 7 indicate that the net effect of executive cognitive flexibility on firm performance is significant when DSSE is not holding a concurrent position in shareholder units. Conversely, when DSSE holds positions in shareholder units at the same time, the main effect of executive cognitive flexibility on firm performance vanishes. This implies that in those firms where DSSE do not hold simultaneous positions in shareholder units, executives are in a better position to apply their cognitive flexibility independently, concentrating on the shared interests of the firm.

5.5.2. Differences in External Firm Environment

(1) Differences in Market Status

Since a firm’s position in its industry is likely to influence its strategy and the latitude available for executive cognitive flexibility to operate, dominant market position firms tend to have more power, more valuable strategic assets, and better access to information [

54]. This imbalance in resource endowment and power could provide executives with greater resource allocation discretion and greater strategic adjustment latitude and, hence, lead to a greater impact of executive cognitive flexibility on firm performance. After the affirmation of the significant positive main effect of executive cognitive flexibility on firm performance, this study also investigates the differentiating effect of market status. Following Meng et al. [

55], we measured industry status as a percentage of the operating revenue of the firm to total operating revenue in the whole industry. We divided the sample into high and low industry status subgroups according to the median industry status for the purpose of regression analysis. The evidence, with

Table 8, Columns (1) and (2), shows that for the group with high industry status, executive cognitive flexibility has a significant positive impact on firm performance at the 1% level. For the group with low industry status, however, this impact is insignificant. This suggests that firms with high industry status are able to reap more information resource benefits, so this executive cognitive flexibility can impact firm performance more directly.

(2) Differences in Industry Pollution Attributes

Because the degree of industry pollution for a company is directly related to the environmental regulatory pressure, public scrutiny, and sustainability demands it faces [

56], such external non-market influences may have a considerable influence on how executive cognitive flexibility leads to firm performance, especially sustainable performance. Therefore, this research introduces industry pollution level as a heterogeneity analysis contextual variable. Polluting industries tend to face stricter environmental controls, higher social obligations requirements, and stronger public scrutiny. Strategic choices and how well they perform in their non-market activities (e.g., corporate social responsibility expenditures and lobbying) place higher expectations on executives’ mental skills and adaptability. We speculate that in situations of stricter environmental limits, the process by which executive cognitive flexibility influences firm performance could be of a higher order or subject to some constraints. We split the sample between non-heavily polluting and heavily polluting sectors, according to the study by Guo Ye et al. [

57]. The regression estimates are provided in

Table 8, Columns (3) and (4). We found that the positive correlation between cognitive flexibility and firm performance is significant in non-heavily polluting sectors but not significant in heavily polluting sectors. This indicates that the positive correlation between cognitive flexibility and firm performance mostly occurs in non-heavily polluting sectors.

(3) Differences in Production Factors

Industries vary in their production factor input structures, especially their labor intensity. In non-labor-intensive firms, strategic adjustments and rapid responses to the external environment may be more critical, and executive cognitive flexibility could play a more direct strategic role. In contrast, labor-intensive firms might focus more on standardized processes, human resource management, and cost control in their production and management [

58]. For these firms, the demand for executive cognitive flexibility might manifest more in adapting employee management and improving efficiency. This study introduces industry labor intensity as a contextual variable. Following the research by Yin et al. [

59], sample firms are categorized into labor-intensive and non-labor-intensive based on their industry sub-codes. The regression results are shown in

Table 8, columns (5) and (6). The results indicate that in non-labor-intensive industries, the impact of executive cognitive flexibility on firm performance is significantly positive. However, in labor-intensive firms, the effect of executive cognitive flexibility on firm performance is not significant. This suggests that executives in non-labor-intensive firms can flexibly adjust their cognitive frameworks, quickly absorb new information, and promptly reconfigure strategies to adapt to the external environment. Meanwhile, the standardized production and management in labor-intensive firms weaken the role of executive cognitive flexibility in firm performance.

6. Discussion and Conclusions

6.1. General Conclusions and Recommendations

When juxtaposed against the conditions of rising competition worldwide, growing uncertainty, and China’s dizzying economic evolution with an enhanced interest in sustainable development, companies are brought face-to-face with challenges far more complex than those of traditional market competition. Under such conditions, CEOs’ decision-making capability is brought into focus as the focal point of companies’ survival and development challenges. CEOs under such complex conditions would need to exhibit immense cognitive flexibility on their part to excel in rapidly fluctuating business conditions, complex multinational operational project undertakings, and ever-increasingly prominent environmental and social responsibility challenges. This study has drawn upon two basic theories: Upper Echelons Theory and non-market strategy literature. Upper Echelons Theory is concerned with executive individual characteristics that define a company’s strategic choices and performance. Non-market strategy literature, on the other hand, provides explanations of why companies must develop competitive advantages under political, social, and other non-market conditions. Based on an enormous panel database of Chinese A-share listed companies between 2016 and 2022, the present piece of work methodically and exhaustively examines the way executive cognitive flexibility influences firm performance along the root mediator of non-market strategies. It also makes efforts to delineate the boundary conditions of such an effect.

Our empirical analysis yields several key conclusions:

To begin with, executive cognitive flexibility is a positive predictor of firm performance. This result supports the key proposition of upper echelon theory, stressing that the psychological attributes of an executive are a key determinant of organizational performance. Executives who possess greater cognitive flexibility are more capable of dealing with environmental uncertainty, recognizing opportunities, and making successful strategic choices, which is reflected in increased corporate value.

Second, non-market strategies are an essential mediating mechanism in this link, but they do so through different and counterintuitive channels. In particular, we identify that cognitive flexibility improves firm performance by (a) strategically decreasing investment in expensive, high-quality corporate social responsibility (CSR) activities, and (b) concurrently elevating participation in corporate political activity (CPA). This reveals a subtle dynamic of strategic resource allocation, with cognitively flexible executives seemingly making pragmatic compromises by diverting resources away from discretionary social expenditures towards political actions with more immediate and concrete returns.

Especially, the differences in the internal and external environments of a firm moderate the influence of executive cognitive flexibility on firm performance. When viewed from the internal environmental level, the positive influence of executive cognitive flexibility on firm performance is stronger in firms with CEOs who do not have overseas backgrounds, implying that an in-depth knowledge of the local market aids cognitive flexibility to be effective. At the same time, this influence is also stronger in large firms, highlighting the fundamental role of macroeconomic strategic control and complicated information processing abilities in large firms. In addition, when executives do not hold concurrent positions in shareholder units, their cognitive flexibility has a more apparent positive influence on firm performance, suggesting the role of independence for cognitive flexibility to be effective. From the external environmental level, the positive influence of executive cognitive flexibility on firm performance is stronger in firms with greater market status, enjoying the advantages of superior information resources. In non-heavily polluting industries, the positive function of cognitive flexibility is also fully realized, implying that environments with lighter environmental regulations and public supervision are more favorable for its effectiveness. Lastly, in non-labor-intensive firms, executive cognitive flexibility’s facilitative influence on firm performance is also stronger because such firms depend more on strategic adaptation and quick reactions to the external environment.

Based on the above research findings, businesses should establish systematic mechanisms for executive cognitive flexibility development and utilization in order to promote sustainable corporate development. At the talent selection and team building level, organizations need to actively select and cultivate executives with high cognitive flexibility and build an organizational climate that encourages multidimensional thinking and balances short-term and long-term interests to address increasingly complex sustainability issues. At the strategic resource allocation level, firms need to deeply integrate market and non-market strategies. That is, they should invest resources in Corporate Social Responsibility (CSR) initiatives directly serving core business operations, namely, highlighting CSR projects with material, sustainable value. In doing so, they prevent the long-term damage resulting from the over-reduction of CSR initiatives. Meanwhile, companies should actively leverage political actions to access differentiated resources and policy support, facilitating green development, innovation, and sustainable transformation. This dual strategy enables dynamic optimization of resource allocation, so when firms pursue economic benefits, they simultaneously generate positive impacts on the environment and society. Moreover, firms should develop differentiated strategic implementation trajectories based on their executive team characteristics, firm size, market status, industry characteristics, production factors, and governance structures to achieve more vigorous and sustainable development: firms should attempt to build an executive team endowed with cognitive diversity and complementary experience to solve sustainable development issues from an integrated perspective; for large firms, investment in executive cognitive flexibility improvement should be made to effectively tackle complex sustainable development programs; firms with a superior market status should fully utilize their resource advantages to opportunistically grasp emerging green market opportunities; firms in high-polluting industries need to leverage executive cognitive flexibility to accelerate green transformation and circular economy conduct and ensure compliance; and firms with non-labor-intensive industries need to invest additional resources in strategic tasks supporting the effectiveness of executive cognitive flexibility, including sustainable technology R&D and innovation. Meanwhile, firms where executives hold concurrent positions need to build more rigorous conflict-of-interest screening and decision-making oversight mechanisms to ensure that executive cognitive flexibility can actually be transformed into long-term firm-level performance improvement and sustainable value creation.

Academically, this study makes the following two contributions: First, this study innovatively introduces executive cognitive flexibility to the field of corporate strategic management to address the shortage of current literature in examining the mechanisms between executive CF and firm performance. We are the first to construct and empirically test the “cognition–behavior–performance” theoretical model, revealing the indirect manner by which executive CF affects firm performance through its influence on non-market strategies (by making optimal investment in Corporate Social Responsibility (CSR) in a strategic way and utilizing Corporate Political Activity (CPA) efficiently). This finding improves our understanding of how executive cognitive traits propel corporate non-market behaviors and their economic consequences for sustainable development. Second, this study meticulously explores the dual mediating mechanisms of corporate political activity and corporate social responsibility in non-market strategies. We not only validate the mediating role of non-market strategy between CF and firm performance, but, more importantly, reveal how, under the condition of resource scarcity and pursuing long-term sustainable development, executive CF drives firms to make strategic, rational reaction to CSR (rather than blind expansion of it, for avoiding resource wastage and enhancing efficiency), and how to effectively utilize CPA to attain policy favor and scarce resources, thereby creating integrated economic, social, and environmental value for the firm. This offers new knowledge on the complexity of non-market strategies and their contextual dependence in supporting corporate sustainable operations. Finally, the study also investigates internal and external environments’ differential moderating influences on the executive CF–firm performance link, providing finer-grained theoretical insight into the boundary conditions under which executive cognitive traits become operative in diverse contexts, particularly when confronting sustainable development issues and opportunities, thus enhancing the application of contextual factors in strategic management research.

6.2. Limitations and Future Research

Despite having made general contributions, the present study has some limitations that still need to be explored further. Firstly, as the present study is mainly based upon Chinese A-share listed companies, cross-national generalizability of results needs to be evidenced further. This is because national cultural differences potentially might have unique influences upon executive cognitive flexibility and firm strategic actions, and thus their bearing upon firm performance is unknown. Secondly, due to the limitation of the availability of data, the measurement of the present study mainly depends on textual analysis. While all efforts have been undertaken to employ rigor, textual sentiment or semantic analysis might not be capable of capturing the rich cognitive patterns embedded into executive decision-making behaviors appropriately. Hence, future research is advisable to conduct more integrated comparison analysis of firms across various countries and regions to determine the universality of results. Meanwhile, the measuring approach of the executive cognitive flexibility indicator is capable of being further developed, for instance, facilitated by big data models for better capturing executive dynamism or by using a qualitative–quantitative mixed methodology to reduce inaccuracies and poverty of the indicator.

{kind=link}