2.1. Literature Review of Corporate Digital Transformation

In the 1990s, emerging technologies represented by internet technology began to be applied, driving the growth of the digital economy. This context gave rise to the development of enterprise digital transformation. Chun et al. [

21] argue that traditional U.S. industries with higher firm-specific stock returns began to adopt information technology more intensively in the late 20th century. Over the past decade, the concept of digitalization has evolved through contributions from various sectors, including academia, becoming a significant form of economic development that influences all aspects of society [

22]. Previous studies have found that enterprise digital transformation is a complex process of change driven by both external and internal factors. In terms of external factors, first, environmental elements such as socio-cultural shifts and technological advancements provide cognitive support and technological foundation for digital transformation. Chen and Tian [

23] argue that enterprise digital transformation depends on the interaction between environmental uncertainty and resource orchestration. Second, market elements such as market competition and consumer demand also put pressure on enterprises to decide whether to engage in digital transformation [

24]. Furthermore, policy incentives constitute an important external driver influencing enterprise digital transformation behavior. Governments can encourage such transformation through supportive policies and measures, such as financial assistance, tax incentives, and innovation inducements. Regarding internal factors, digital transformation is driven by managerial and organizational elements. Porfirio et al. [

25] argue that managerial characteristics significantly influence the digital transformation process, while managerial capabilities also impact a company’s strategic perception, organizational structure, and business model [

26]. The supportive attitudes held by executives and the organization’s technological capabilities also serve as prerequisites for advancing digital transformation [

27,

28].

2.2. Literature Review of ESG Rating Divergence

The existing studies primarily examine the negative effects of ESG rating divergence on capital market. Scholars have argued that divergence introduces uncertainty about corporate sustainability, signals a higher operational risk, increases risk premiums demanded by investors and creditors, as well as increases the volatility of stock return [

2,

4,

11,

29]. From the perspective of information, some scholars believe that ESG rating divergence aggravates market information asymmetry and weakens the predictive value of ESG disclosures, leading to the increase in bond issue spread, the decline of analyst forecast quality, and the rise in audit fees [

8,

9,

12,

15]. In addition, a limited number of studies explore corporate responses to ESG rating divergence, such as enhancing green investment or engaging in active earnings management [

6,

10].

Overall, while ESG research has a long history, the economic consequences of ESG rating divergence remain underexplored. Prior work focuses on equity and debt financing, but not yet on the impact of digital transformation. Additionally, studies that focus on the impact of corporate ESG performance on corporate digital transformation overlook the role of multiple ESG ratings and their inconsistencies.

2.3. Research Hypotheses

From an institutional theory perspective, ESG rating divergence generates complex and dynamic external institutional pressures for corporations [

8,

9]. This divergence fundamentally reflects the coexistence of multiple evaluation standards within the institutional environment, creating a legitimacy paradox for companies [

15,

29]. When rating agencies employ divergent methodologies and weighting systems, companies face significant challenges in simultaneously satisfying all evaluation criteria, resulting in their ESG practices being caught in a double bind [

6,

12].

This inherent contradiction activates institutional monitoring mechanisms [

2,

8]. Investors and regulators often adopt the most stringent rating standards as benchmarks, establishing binding constraints on corporate behavior [

11,

15]. Concurrently, rating divergence provides institutional actors with intervention opportunities. Through public scrutiny, shareholder proposals, and other means, these actors amplify the negative implications of the divergences, compelling firms to align with higher standards. Compounding these pressures, the divergence in ESG ratings among companies may ultimately drive greater emphasis on information transparency and disclosure practices [

30]. These companies may also focus more on managing environmental, social, and corporate governance risks to enhance their ESG performance and reduce inconsistencies in third-party ESG ratings, thereby increasing confidence among investors and stakeholders [

6].

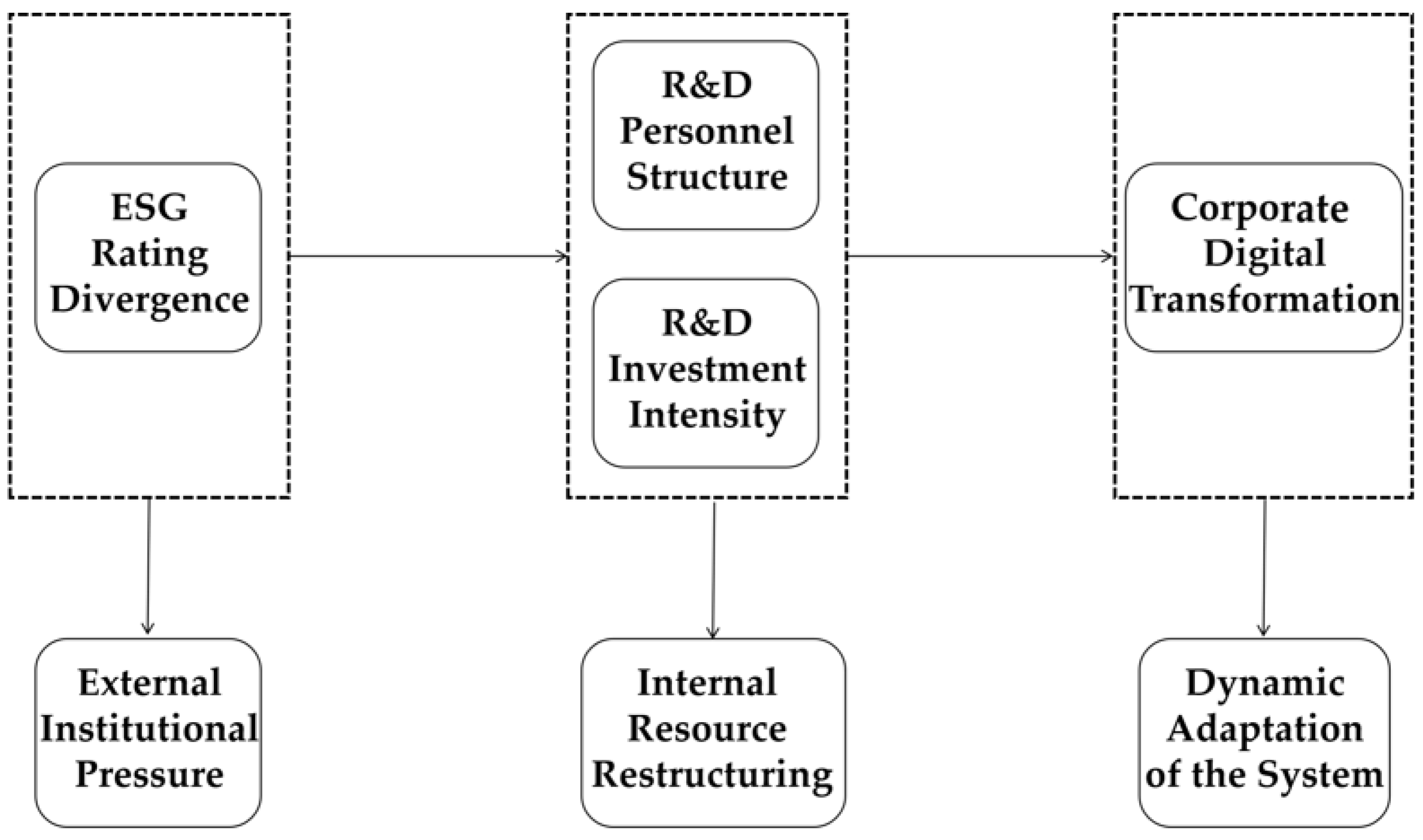

Against this backdrop, digital transformation may serve as a critical mechanism for companies seeking to enhance ESG performance [

23,

31]. From an institutional theory perspective, information asymmetry reflected in ESG rating divergence constitutes a significant “external pressure”, compelling firms to improve information disclosure quality through digital means to address legitimacy challenges. Under the resource dependence theory lens, corporations experiencing substantial rating divergence may engage in resource reconfiguration as an “internal response”. This manifests as strategic investments in digital technologies to establish more precise real-time data collection and analytical capabilities [

32,

33]. Such investments fundamentally represent strategic realignments in critical resource dependencies. Meanwhile, the dynamic capability theory elucidates how organizations achieve “dynamic adaptation” through digital tools—converting data-driven insights into organizational capacities for continuous ESG performance improvement [

34,

35]. This enables strategic agility within institutional environments characterized by evolving rating standards.

On one hand, digital technologies can enhance the transparency and credibility of companies’ ESG data [

35]. The transparency and credibility of ESG data have always been concerns for investors and stakeholders, as the collection and analysis processes are often subject to human factors [

36]. Through digital technologies, companies can disclose ESG-related data in a more transparent manner, enabling more precise ESG evaluations by rating agencies. Additionally, the improvement of digital technology ensures the security and credibility of companies’ ESG data [

37], reducing the difficulties faced by rating agencies in the investigation process and enabling them to issue more rigorous ESG rating reports [

34].

On the other hand, digital technologies can help companies better measure and improve their ESG performance [

34]. Digital technologies can assist companies in accurately assessing their own ESG performance and identifying and addressing relevant issues through data analysis. For example, companies can use big data analytics to identify and monitor potential risks in environmental protection, social responsibility, and corporate governance [

38,

39], and take timely measures to improve and mitigate negative outcomes, thereby enhancing their ESG performance [

34].

Based on the above analysis, companies with high ESG rating divergence may be more motivated to actively develop digital technologies to improve their ESG performance and reduce future inconsistencies in ESG-related issues raised by rating agencies. Therefore, we propose hypothesis H1, as follows:

Hypothesis 1. ESG rating divergence promotes corporate digital transformation.

However, large ESG rating divergence may also have adverse effects on corporate digital transformation. Companies with significant ESG rating divergence face greater information uncertainty, which may create difficulties in financing [

1,

17]. ESG ratings are important indicators considered by many financial institutions and investors. Due to the uncertainty caused by rating discrepancies, many financial institutions may be more cautious about providing financing to these companies. As a result, companies with high rating discrepancies may face restricted access to financing channels and increased financing costs, which could negatively impact their digital transformation.

In addition, digital transformation requires companies to obtain various resources, including technology, talent, and data [

33,

38,

39,

40]. Rating discrepancies by rating agencies regarding a company’s ESG performance may lead potential partners, suppliers, and customers to adopt a reserved attitude towards the company’s sustainability performance, reducing their willingness to collaborate [

41,

42,

43]. Furthermore, companies with significant ESG rating divergence may face challenges in talent recruitment and retention. Some talent may be more inclined to join or stay with companies with higher ESG ratings, putting companies with high rating discrepancies at a disadvantage in talent competition [

36,

44].

Moreover, companies with large ESG rating divergence may face trust and reputation risks in the market [

45,

46,

47,

48]. Investors and other stakeholders are increasingly concerned about ESG performance, and they often refer to rating results to assess a company’s sustainability capabilities [

4,

14,

15,

49]. Rating discrepancies may raise doubts among investors regarding a company’s sustainability capabilities, reducing their trust in the company. This could have a negative impact on the company’s brand image and market competitiveness, thereby affecting the progress and effectiveness of digital transformation. Based on this, we formulate a rival hypothesis H2.

Hypothesis 2. ESG rating divergence inhibits corporate digital transformation.

Therefore, whether ESG ratings promote or hinder corporate digital transformation is a question that requires empirical investigation.

{kind=link}