Abstract

Green finance—including bilateral and multilateral development aid and concessional loans—has emerged as a critical tool in supporting the transition to a low-carbon economy, particularly in emerging economies. Türkiye, since the early 2000s, has increasingly relied on climate-related official development flows in alignment with its sustainability and emissions reduction targets. This study examines the impact of green finance and financial globalization on environmental sustainability in Türkiye over the period 2001–2021. It specifically tests the load capacity curve (LCC) hypothesis, which posits a non-linear (U-shaped) relationship between financial drivers and ecological outcomes. The study employs the load capacity factor (LCF) as an environmental pressure indicator and uses ARDL, FMOLS, DOLS, and CCR estimation methods to ensure robustness. The results indicate that green finance has a long-term positive effect on Türkiye’s environmental sustainability, whereas financial globalization shows mixed effects. The findings confirm the presence of a U-shaped relationship between green finance and environmental pressure, supporting the LCC hypothesis. These results contribute to the limited empirical literature on green finance in emerging economies and suggest that policy frameworks should emphasize the sequencing and institutional alignment of green financial flows. Policymakers in Türkiye and similar economies may benefit from integrating green finance strategies with targeted regulatory reforms to maximize ecological benefits.

1. Introduction

Since the Industrial Revolution, the growing use of fossil fuels has played a key role in increasing waste from human production and consumption activities, contributing to environmental pollution and global warming. Climate change caused by global warming and the intensification of extreme weather events has now become a major threat to life on Earth. The ongoing exploitation of natural resources is further accelerated by technological progress, population growth, globalization, and the pursuit of political influence. Each year, nearly 30% of natural resources are turned into waste, and the lack of effective waste management systems continues to endanger ecosystems [1] (p. 626). Roughly 75% of global greenhouse gas emissions are still linked to fossil fuel-based energy production.

Fossil fuels, a major contributor to environmental pollution, are associated with approximately 8.7 million premature deaths globally each year [2]. The Global Resources Outlook 2024 by the United Nations Environment Programme (UNEP) shows that demand for natural resources has more than tripled in the last 50 years and continues to grow at an annual rate of over 2.3%. Without urgent and coordinated action to change how we use these resources, global extraction could rise by 60% by 2060, reaching 160 billion tons compared to 100 billion tons in 2020. This would significantly surpass the global temperature rise limit set by the 2015 Paris Agreement as cited in the UNEP report [3]. The European Investment Bank (EIB) estimates that if carbon emissions stay at current levels, average global temperatures could rise by 4 °C by the end of this century [4] (p. 15). Such a development would undermine climate targets, harm ecosystems, and negatively impact public health and economic well-being [3].

The sustainability of ecosystems is strongly tied to how we define and manage environmental carrying capacity. This concept refers to the highest level of use that a natural environment can support without triggering irreversible damage or severe ecological degradation [5]. As a key element of sustainable development, environmental carrying capacity serves as a quantitative tool to assess environmental sustainability [6]. By supporting the optimal and sustainable use of energy resources, carrying capacity helps prevent resource depletion, strengthens long-term energy security, lowers costs, and aids in the fight against climate change through reduced carbon emissions. When carrying capacity is exceeded, ecosystems can suffer lasting and potentially irreversible damage. For this reason, identifying and regulating carrying capacity is vital for achieving both environmental and economic sustainability. A sustainable future depends on respecting the planet’s ecological boundaries.

Growing global concern about climate change has brought renewed focus to reducing greenhouse gas emissions, ensuring a sustainable planet for future generations, and supporting greener economic growth. In response to the ecological crisis caused by rising emissions, many countries have begun to adopt proactive climate policies. These efforts gained structure through the 1994 United Nations Framework Convention on Climate Change (UNFCCC) and were later formalized in the 2015 Paris Agreement, which sets key targets: limiting global temperature rise to 1.5–2 °C, cutting emissions by 50% by 2030, and achieving net-zero emissions by 2050 [7]. As a result, countries now commit to national emission reduction goals that shape their economic strategies. Meeting these goals requires a transition to clean and renewable energy sources. Given the environmental risks and limited availability of fossil fuels, renewables are becoming increasingly important for protecting ecosystems, reducing carbon footprints, and aligning with global sustainability trends. Increasing the share of renewables in energy production supports cleaner environments, stronger economies, and more secure energy systems. Without such a transition, population growth and rising per capita Gross Domestic Product (GDP) are expected to drive further increases in CO2 emissions [8] (p. 10). As electricity consumption rises, and with nearly two-thirds of global CO2 emissions coming from the energy sector, the demand for clean energy alternatives like renewables is growing [9] (p. 709).

BloombergNEF’s Power Transition Trends 2024 and Renewable Energy Investment Tracker 2024 reports [10] highlight the growing momentum in clean energy investments. In 2023, zero-carbon sources provided over 40% of global electricity, with hydropower accounting for 14.7%, wind and solar for 13.9%, and nuclear energy for 9.4%. Wind and solar made up around 91% of new power capacity, while fossil fuels accounted for just 6%. This trend continued in the first half of 2024, with USD 313 billion invested globally—matching the level seen in the first half of 2023. The IRENA notes that to keep global warming within 1.5 °C, the world must add more than 1000 GW of renewable capacity annually until 2050 [11] (p. 2). BloombergNEF projects that renewable capacity must triple in the next decade to achieve net zero by 2050, raising the share of renewables in electricity to over 50% [12]. The IRENA’s Planned Energy Scenario suggests that if planned targets are met, CO2 emissions could drop 6% by 2030 and 56% by 2050 compared to 2022. Reaching the 1.5 °C goal will require USD 47 trillion in cumulative investments in clean energy by 2050 [13] (p. 4). The IMF estimates that annual global spending will need to reach between USD 3 and 6 trillion to meet the Paris Agreement’s temperature and adaptation targets [14].

Achieving sustainability goals will require stronger policy action and significantly more financial support. This means that strategies must be developed and implemented quickly at both national and global levels, backed by effective regulations and adequate funding [13] (p. 4). A key question in this context is how and where the necessary capital can be mobilized. The growing need to diversify funding sources and manage risks has given rise to green finance as a key solution [15]. Expanding infrastructure and improving technology for renewable energy investments are central to building a sustainable economy. Although many countries are turning to renewables for electricity generation, current levels still fall short. One of the main barriers remains access to financing. At this point, green finance is gaining attention as a mechanism that supports climate goals, prevents environmental overuse, and aligns with the principles of sustainable development. It promotes environmental sustainability while helping manage the use of natural resources more responsibly.

Lowering the cost of sustainable development in developing countries is a key challenge in the global economy. One of the central themes in climate justice debates is the need for developed countries to help fund decarbonization efforts in less developed economies. Since the early 2000s, such policy initiatives have increasingly been implemented through official development frameworks, where bilateral and multilateral channels deliver climate-related development aid and investment-related financial flows (IFCF) to developing countries.

In response to this gap, the study provides a structured contribution by integrating green finance, environmental sustainability, and international financial dynamics into a single empirical framework. While there is a growing body of research on green finance and its role in promoting sustainability, empirical studies focusing on the interaction between international financial flows and environmental sustainability in developing countries remain limited. Moreover, few studies have examined this relationship through the lens of LCC hypothesis, particularly in the context of Türkiye. Given the increasing relevance of the LCC hypothesis in recent environmental economics research, this study addresses a critical gap by providing a quantitative analysis of climate-related development finance (YEF) and financial globalization, using the LCF as a comprehensive indicator of environmental sustainability.

In doing so, it contributes to the literature by offering new insights into the nonlinear dynamics of finance–sustainability linkages in emerging economies. Additionally, the study advances the understanding of sustainable development finance by directly supporting the achievement of Sustainable Development Goals (SDGs), particularly SDG 13 (Climate Action) and SDG 7 (Affordable and Clean Energy). The findings are intended to guide policymakers in designing effective green finance strategies that align with long-term sustainability objectives in developing and emerging economies.

In the case of Türkiye, rapid urbanization, fossil fuel dependency, and a growing need for external financing pose significant challenges for achieving environmental sustainability. Despite committing to net-zero emissions by 2053, Türkiye continues to face structural and macroeconomic constraints in implementing its green transition agenda. These dynamics highlight the importance of analyzing Türkiye’s experience within the broader discourse on sustainable finance and globalization. These challenges are further compounded by Türkiye’s vulnerability to global economic fluctuations, similar to other emerging economies, which reduces its resilience to macroeconomic instability and may undermine the stability and efficacy of long-term green finance mechanisms, thereby weakening the country’s adaptive capacity and resilience as captured by environmental indicators such as the LCF.

Building upon the existing LCC framework, this study extends its empirical application to Türkiye, an emerging economy, thereby addressing the gap in sustainability research on developing countries. This study contributes to multiple areas of the sustainability and finance literature. First, it expands the application of the LCC framework by testing it within the context of a developing economy, Türkiye. Second, it introduces green finance as a positive scale driver, conceptualizing its role in structural transformation toward sustainability. Third, it integrates financial globalization dynamics via the KOF Financial Globalization Index, highlighting the macro-financial environment as a critical enabler of green finance effectiveness. These contributions offer theoretical, empirical, and policy insights into sustainable development transitions in emerging economies. Notably, this study is the first to empirically examine the positive scale effects of green finance within the LCC framework by using the YEF variable, while simultaneously integrating financial globalization as a contextual factor, thereby offering a novel approach to analyzing sustainability transitions in emerging economies.

This study addresses the following research question: Does green finance enhance environmental sustainability in Türkiye, and does this relationship exhibit a U-shaped pattern as proposed by the LCC hypothesis? Additionally, what is the role of financial globalization in shaping environmental sustainability outcomes? To answer this question, the following hypotheses are tested:

H1.

Green finance has a statistically significant impact on environmental sustainability in Türkiye.

H2.

Financial globalization has a statistically significant impact on environmental sustainability in Türkiye.

H3.

The relationship between green finance and environmental sustainability follows a U-shaped curve, consistent with the LCC hypothesis. Following this framework, the subsequent sections first introduce the conceptual foundations of green finance and its role in sustainable development, followed by a detailed examination of Türkiye’s green finance landscape. Subsequently, the study presents the econometric model, empirical findings, and policy implications, offering a comprehensive analysis of the relationshisp among green finance, financial globalization, and environmental sustainability in the context of an emerging economy.

2. Green Finance: Conceptual Framework

Green finance emerged in the 2010s as a forward-looking financial approach designed to support the development of the financial sector, enhance environmental outcomes, and foster economic growth. Institutions such as the World Bank (WB) and the United Nations consider it a new paradigm that promotes the realization of economic, social, and environmental sustainability—the three pillars of sustainable development [16].

In contrast to traditional finance, green finance aims to steer capital toward projects that protect the environment, conserve natural resources, and support sustainability objectives [17] (p. 672). It seeks to incorporate environmental and social considerations into financial decision-making and channel resources toward initiatives aligned with the SDGs, particularly in areas such as renewable energy, sustainable infrastructure, and climate change mitigation.

Green finance plays a crucial role in promoting sustainable economic growth by reducing environmental pollution and enhancing the efficient use of natural resources. It primarily supports renewable energy investments, energy efficiency improvements, and climate change adaptation projects [18]. Numerous studies confirm a strong positive relationship between green finance and renewable energy investments, highlighting the facilitative role of green finance in channeling resources to sustainability-oriented projects in both developed and developing economies [19]. The global advancement of green finance strengthens efforts to mitigate the negative impacts of climate change. As an emerging financial instrument, green finance not only provides funding for environmentally friendly projects but also fosters technological innovation, supporting green economic growth and enhancing environmental sustainability [20]. In this regard, green finance plays a crucial role in facilitating the transition to a green economy and maintaining ecological balance.

Green finance has gained increasing interest from banks, institutional investors, and international financial institutions due to its alignment with the principles of sustainability. Governments define the regulatory framework, while central banks ensure operational stability. Among the key green finance instruments, international green loans and green bonds have emerged as prominent mechanisms, particularly in facilitating investments in renewable energy and energy efficiency [21].

International green loans and official development assistance (ODA) are key financial instruments supporting projects that directly contribute to environmental sustainability [22]. Since the early 2000s, the global expansion of green loans has facilitated investments in renewable energy, energy efficiency, and environmental protection initiatives. Unlike traditional loans, green loans are evaluated based on environmental performance criteria, ensuring that financial flows are aligned with long-term sustainability objectives [23]. By channeling financial resources into green initiatives, green loans help drive investment in sustainability-focused projects and support the achievement of environmental goals. International financial institutions particularly target developing countries to promote renewable energy, environmental protection, and energy efficiency. Eligible projects must comply with specific environmental criteria and align with both national and international sustainability frameworks. Climate finance in the form of development assistance has become a key policy instrument in efforts to meet the targets set under the Paris Agreement. Within the framework of the 17th Sustainable Development Goal (SDG 17) titled Partnerships for the Goals, target 17.2 outlines specific objectives related to ODA from developed countries to developing and least developed countries. SDG 7.a also calls for enhanced international cooperation to facilitate access to clean energy and improvements in energy efficiency in developing countries, specifically encouraging investment in energy infrastructure and clean energy technologies. Furthermore, SDG 13 (Climate Action) emphasizes the urgent need for mobilizing financial resources to mitigate and adapt to climate change impacts, directly linking YEF to global sustainability targets. The Organisation for Economic Co-operation and Development (OECD) plays a leading role in monitoring these flows through its Development Assistance Committee (DAC). In parallel, Multilateral Development Banks (MDBs) are among the major institutional actors supporting YEF. Key MDB members include the European Bank for Reconstruction and Development (EBRD), the Islamic Development Bank (IsDB), the WB, and EIB, which are among the most prominent providers of climate finance to developing countries [24].

Green bonds have rapidly emerged as key instruments within sustainable finance. The first green bond was issued in 2007 by the WB in response to a Swedish pension fund group’s interest in global warming mitigation efforts. Green bonds, like conventional bonds, are low-cost, long-term, fixed-income securities; however, unlike traditional bonds, their proceeds are exclusively allocated to projects with verifiable environmental benefits [25,26]. According to the International Capital Market Association [27], green bonds align investor capital with the SDGs by financing new or existing green projects.

Given their heightened vulnerability to climate change and limited access to traditional capital markets, developing countries face significant challenges in financing sustainable development. In this context, green finance emerges as a critical mechanism, offering targeted financial support to bridge investment gaps and facilitate the transition toward resilient and environmentally sustainable economies.

3. Green Finance Applications in Türkiye

In the case of Türkiye, the need for financial resources to support investments that enhance energy efficiency has become increasingly critical in the country’s transition toward a low-carbon economy. Since the 1970s, with the rapid integration of the global economy, Türkiye has experienced substantial economic growth. This growth has significantly increased energy consumption and, in turn, electricity demand. Over the past two decades, electricity demand has tripled, growing at an average annual rate of approximately 4.7%. To achieve its target of net-zero carbon emissions by 2053, Türkiye must undergo a major transformation in its energy sector, addressing the challenges of growing energy demand and high dependence on imported energy. According to the most recent data released by the Turkish Statistical Institute, energy-related emissions accounted for 71.8% of total greenhouse gas emissions in 2022. Moreover, emissions from the energy sector increased by 179.8% in 2022 compared to 1990 levels [28].

The increasing use of fossil fuels and rising dependency on energy imports in Türkiye have significantly contributed to the surge in greenhouse gas emissions. Approximately 70% of the country’s trade deficit is attributed to energy imports, underscoring the strategic importance of renewable energy development. Türkiye possesses substantial potential in various renewable energy sources such as wind, solar, and geothermal energy, which are critical for enhancing economic performance, climate resilience, and environmental sustainability [29]. In this context, the expansion of green finance emerges as a pivotal mechanism to support the transition toward a sustainable energy sector. However, limited financial resources, low public awareness, and regulatory barriers continue to hinder progress. Strengthening the green finance ecosystem, with support from international financial institutions and targeted government incentives, could accelerate Türkiye’s transition to a low-carbon economy.

Türkiye has taken important regulatory and institutional steps to support sustainability and combat climate change as part of the global green transition process. The country joined the UNFCCC in May 2004, signaling its entry into international cooperation on environmental issues. In 2021, the Ministry of Trade released the Green Deal Action Plan to align national policies with the European Green Deal, and later that year, Türkiye ratified the Paris Climate Agreement, committing to achieve net-zero carbon emissions by 2053. Following these commitments, policy platforms focusing on carbon pricing mechanisms, renewable energy development, and climate adaptation strategies were initiated to accelerate the reduction of greenhouse gas emissions [30].

On 22 February 2022, the Capital Markets Board of Türkiye (CMB) published the “Guidelines on Green Debt Instruments, Sustainable Debt Instruments, Green Lease Certificates, and Sustainable Lease Certificates,” developed based on the Green Bond Principles updated by the International Capital Market Association in 2021. These guidelines aim to enhance transparency, integrity, and comparability in the financing of sustainability-focused investments. In Türkiye, the issuance of green bonds is regulated by the CMB, and regulatory incentives have been introduced to facilitate market development [31]. Furthermore, the 12th Development Plan (2024–2028) emphasizes the strategic use of green bonds to finance renewable energy and energy efficiency projects [32].

Green finance has gained increasing significance in Türkiye’s efforts to achieve its sustainability goals, with both international financial institutions and domestic banks playing crucial roles in developing the national green finance ecosystem. Among the available instruments, international loans remain the most widely utilized for financing green projects, particularly renewable energy investments. Türkiye’s green bond market has also shown notable progress in recent years. Financial globalization, which gained momentum globally in the 1970s, accelerated in Türkiye during the 1980s with the liberalization of capital flows, leading to the rapid integration of Türkiye’s financial sector into global markets. This integration facilitated greater access to international credit and enhanced the country’s ability to borrow from global financial institutions [33] (p. 129). Given Türkiye’s significant savings-investment gap, green projects are predominantly financed through green loans provided by international financial institutions. These loans, offering favorable terms such as lower interest rates and extended maturities, are primarily directed toward investments in renewable energy and energy efficiency.

In Türkiye, green aid and loan mechanisms provided by international institutions are primarily used to finance renewable energy, energy efficiency, and environmentally friendly infrastructure projects. Key multilateral organizations involved in this process include the OECD DAC, MDBs, the EBRD, the WB, and EIB. Among DAC member countries, Türkiye receives significant bilateral aid and green loans from major donors such as Germany, the United Kingdom, and Japan. In 2022, green finance was provided by institutions including the EBRD, the International Bank for Reconstruction and Development, the European Commission, and the Asian Infrastructure Investment Bank [24]. The Türkiye Sustainable Energy Financing Facility (TurSEFF), launched by the EBRD in 2010, has significantly contributed to financing renewable energy and energy efficiency investments [34].

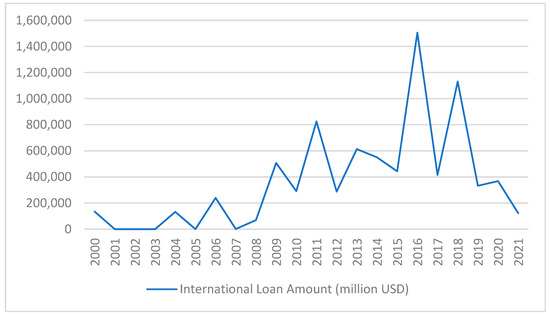

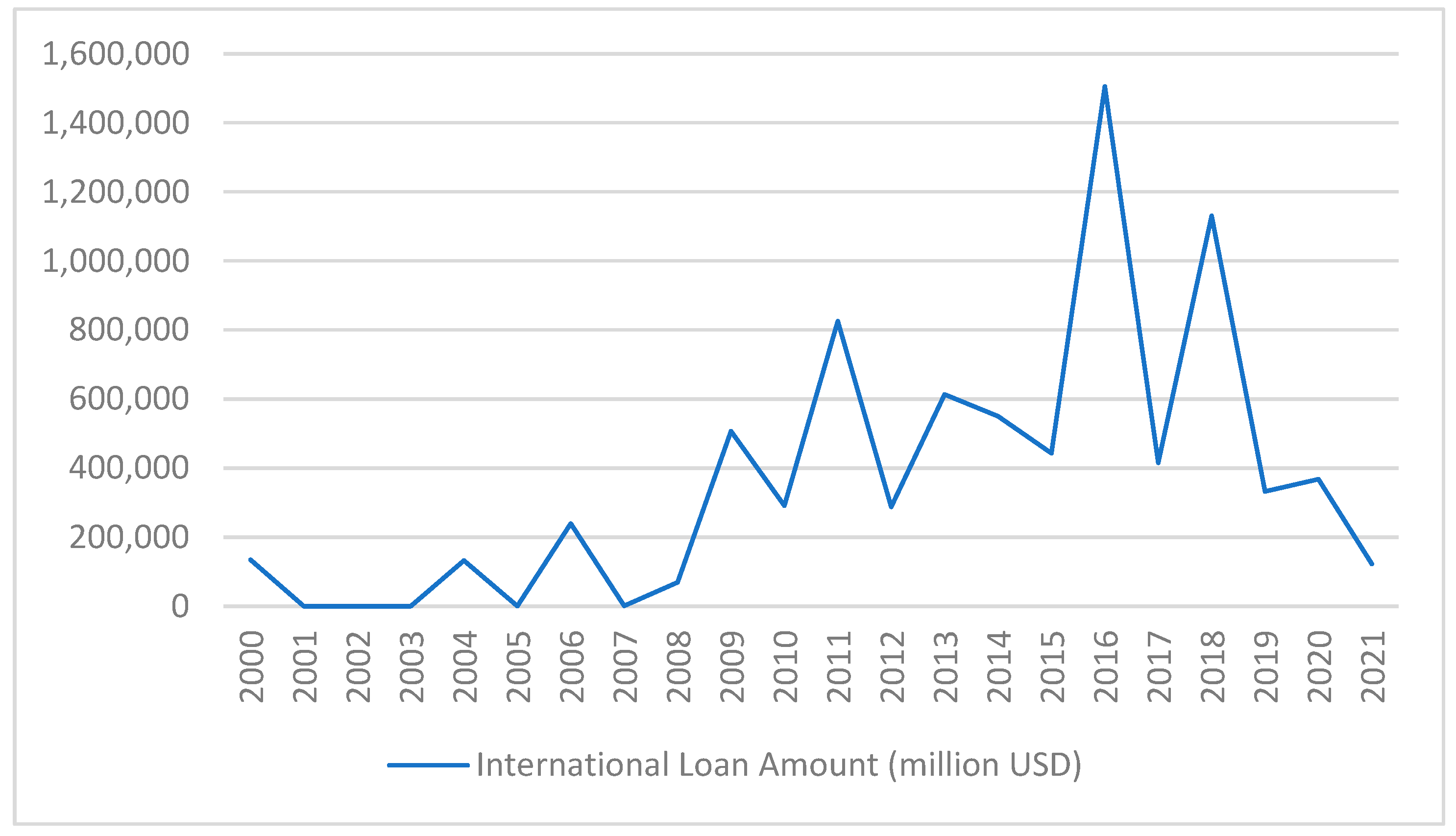

Figure 1 presents the international loans obtained for renewable energy production in Türkiye under IFCF between 2000 and 2021 [35]. As shown, the total amount of green loans received by Türkiye for renewable energy investments has exhibited considerable volatility over the years. In 2000, the loan volume stood at USD 134.70 million. No new green loans were recorded in 2002 and 2003. Beginning in 2004, green financing resumed and peaked in 2016 at USD 1.51 billion. Although loan volumes declined in 2017, they rebounded in 2018 to reach USD 1.13 billion. However, since 2020, a downward trend has been observed, with the total loan volume falling to USD 122.82 million. This downward trend may reflect broader market uncertainties, changes in global financing conditions, or shifting policy priorities. This fluctuating pattern in green loan inflows reflects the dynamic interaction between international financing conditions and domestic policy initiatives, consistent with the theoretical framework of financial globalization and its implications for sustainable development pathways in emerging economies.

Figure 1.

International loans for renewable energy in Türkiye (2000–2021). Note: Data compiled from Ritchie et al. [35]; authors’ calculations.

Complementing international loan inflows, Türkiye’s green finance ecosystem has gradually diversified to include market-based instruments such as green bonds and green sukuk. Green bond issuance in Türkiye began in 2016, initially dominated by banks and concentrated largely in the financial sector. Although the total number of issuances remains relatively low, the market has developed rapidly in recent years and has attracted strong investor interest, leading to successful placements. The first sovereign green bond issuance was carried out by the Ministry of Treasury and Finance on 5 April 2023. In Türkiye, green bonds are primarily issued in international markets and mostly denominated in U.S. dollars. However, there are no comprehensive data available on the proportion of these bonds allocated specifically to renewable energy investments. This is because green bond proceeds have been used not only to finance renewable energy but also for investments in clean transportation, green buildings, and green technologies. The Industrial Development Bank of Türkiye was the first institution to issue a green bond, which financed a total of 19 green projects. These included renewable energy, energy and resource efficiency, electricity distribution, port infrastructure, and healthcare facilities. Of these, seven projects—representing 42.6% of the total—were in the field of renewable energy [36] (p. 280). While green bond issuance in Türkiye is increasing, it still remains modest compared to global growth trends. Türkiye’s first green sukuk was issued in 2021, with 50% of the proceeds allocated to clean transportation, 29% to waste management, and 22% to renewable energy projects [37] (p. 20).

Overall, while Türkiye has made notable progress in developing green finance instruments such as green bonds and sukuk, the sector remains nascent compared to global trends. The country’s green finance landscape continues to rely predominantly on international financial flows rather than fully matured domestic market-based instruments. This pattern reflects broader structural challenges common to emerging economies, where green finance initiatives are advancing yet still constrained by market depth and macroeconomic volatility. Addressing these limitations will be essential for aligning Türkiye’s green finance ecosystem more closely with the SDGs and for enhancing its resilience in the global transition toward a low-carbon economy.

4. Econometric Analysis on Türkiye

4.1. Theoretical and Empirical Literature

The relationship between economic development and environmental quality has been extensively analyzed through the Environmental Kuznets Curve (EKC) hypothesis. Originally developed by Kuznets [38], the EKC posits an inverted U-shaped relationship, suggesting that environmental degradation initially intensifies with rising income but eventually declines as economies transition to cleaner technologies and sustainable practices. Grossman and Krueger [39,40] extended this framework by analyzing the environmental impacts of trade liberalization under the North American Free Trade Agreement (NAFTA), while Panayotou [41] further emphasized the importance of structural economic changes and regulatory policies in driving the turning point of environmental improvements.

While the EKC hypothesis traditionally links rising income to environmental improvements, recent studies suggest that income alone may not fully capture the structural dynamics underlying sustainable development. Consequently, alternative indicators such as the Economic Complexity Index (ECI) have gained prominence in the literature. The ECI measures a country’s productive capabilities through the diversification and sophistication of its production and export structures, serving as a proxy for structural economic transformation. Pata [42] and Balsalobre-Lorente et al. [43] demonstrate that ECI is significantly associated with environmental outcomes, suggesting that economies with higher complexity levels tend to adopt cleaner technologies and resource-efficient practices more rapidly than less diversified economies.

Green finance policies, particularly those grounded in strong sustainability approaches, are increasingly recognized as critical drivers of environmental improvement and long-term sustainability outcomes. Recent studies demonstrate that green finance, when combined with technological innovation and institutional quality, significantly enhances environmental performance in developing economies [44]. Vardar et al. [45] provide further evidence that green finance initiatives are effective in reducing ecological footprints (EF) and supporting structural transformation.

The financing of climate change mitigation, widely regarded as a global public good, is considered particularly important for lowering transitional costs in emerging markets. Prior research emphasizes that climate finance facilitates the decarbonization of energy structures and supports positive long-term environmental outcomes [46]. The role of climate funds in substituting fossil fuels and promoting sustainable growth trajectories has also been widely acknowledged in the literature [47]. Within environmental and ecological economics frameworks, indicators such as per capita carbon emissions and EF are widely utilized for sustainability assessments. Previous research highlights that, although green finance flows are associated with positive long-term effects, short-run transitional inefficiencies may arise due to limitations in absorptive capacities and national policy frameworks [48,49]. Building on these insights, robust green finance strategies are considered essential for achieving environmental sustainability, particularly in regions such as Association of Southeast Asian Nations (ASEAN) and Belt and Road Initiative (BRI) [50,51]. These findings reinforce the broader understanding that the strategic and context-specific deployment of climate finance mechanisms is crucial for facilitating sustainable development trajectories across diverse economic settings.

Beyond the choice of explanatory variables, selecting an appropriate and comprehensive indicator for environmental sustainability has become a central concern in recent empirical studies investigating the relationship between economic activity and environmental outcomes. In particular, the LCF—defined as the ratio of biocapacity to EF—has emerged as a key metric capturing both the environmental burden and regenerative capacity of ecosystems [52,53]. Unlike conventional pollutant-based measures, the LCF offers a dual-lens assessment by integrating both resource consumption and renewal dynamics, capturing the underlying structural regenerative capacity of ecosystems, thereby making it a theoretically robust indicator of environmental sustainability, particularly for emerging economies.

Extending the EKC framework, the LCC hypothesis posits a U-shaped relationship between economic or financial factors and ecological outcomes [54]. According to this hypothesis, financial globalization and green finance may initially exacerbate environmental stress due to transitional inefficiencies or uncoordinated financial flows. However, as absorptive capacities and institutional structures improve, these financial dynamics are expected to enhance environmental sustainability. This study empirically investigates whether such non-linear dynamics hold in the case of Türkiye, directly testing the LCC hypothesis with respect to green finance and financial globalization.

Unlike conventional indicators such as CO2 emissions per capita, which focus solely on pollutant outputs, the LCF offers a dual-lens assessment of sustainability by accounting for both environmental burdens and the regenerative capacity of ecosystems. Rather than serving as a static measurement of environmental pressure, the LCF provides a dynamic indicator of how natural systems absorb and adapt over time. Unlike the entropic and unidirectional nature of traditional EF measures, the LCF incorporates biophysical renewal processes, offering a more comprehensive view of sustainability dynamics.

This supply-side framing aligns the LCF closely with the concept of adaptive capacity, an essential dimension for emerging economies like Türkiye, where institutional readiness, fossil fuel dependency, and resource pressures vary widely. In such contexts, the LCF serves as a policy-relevant lens for evaluating environmental sustainability. The Global Footprint Network’s provision of LCF data facilitates robust empirical modeling to inform sustainable development policies. Extending the traditional EKC, the LCC hypothesis posits a U-shaped relationship among development, structural transformation, and the LCF [54], offering a more dynamic perspective on the nexus between finance, growth, and sustainability.

Traditionally, the EKC models the relationship between economic growth and environmental degradation, suggesting an inverted U-shaped pattern where environmental pressure initially rises with GDP growth and declines after reaching a certain income threshold due to technological innovation and structural transformation effects. In contrast, the LCC hypothesis reframes this relationship by focusing on environmental carrying capacity, proposing a U-shaped trajectory where initial development stresses ecological limits, but subsequent advancements enhance environmental resilience.

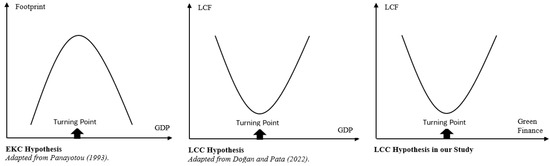

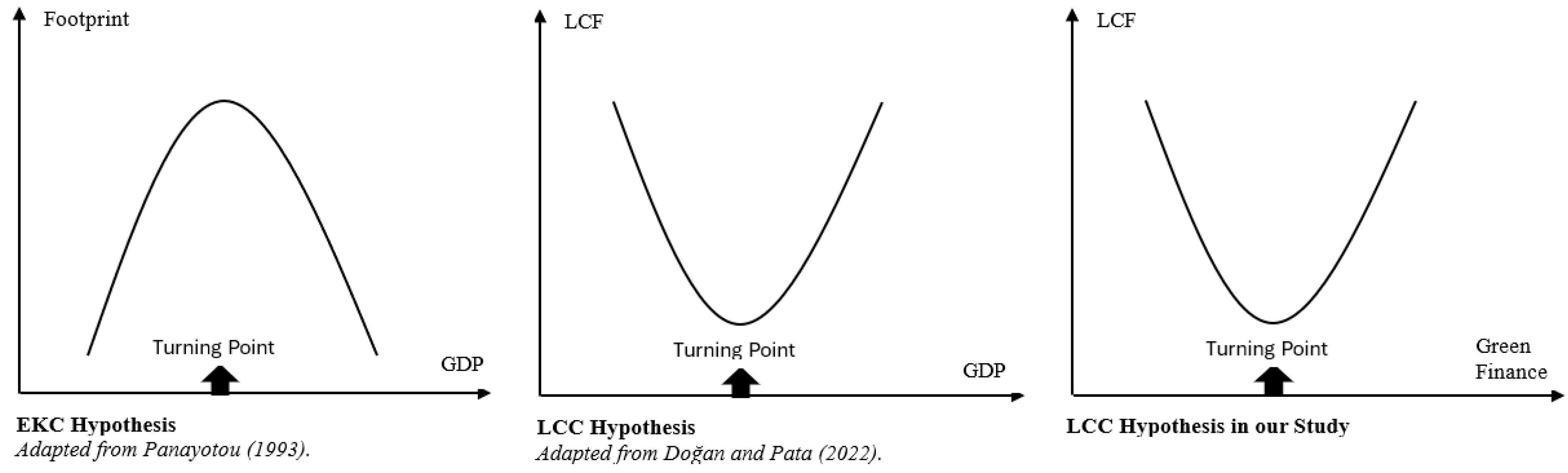

Figure 2 illustrates the conceptual adaptation of the LCC hypothesis as employed in this study. The vertical axis denotes the LCF, capturing the balance between ecological pressure and regenerative capacity, while the horizontal axis represents the level of green finance mobilization. According to the LCC framework, green finance inflows—particularly those channeled into sustainable, project-based investments—initially improve environmental carrying capacity by facilitating structural transformation and innovation. However, beyond a critical threshold, additional inflows may yield diminishing marginal returns on the LCF, primarily due to institutional absorptive capacity constraints and potential inefficiencies in capital allocation.

Figure 2.

Comparative Illustration of EKC and LCC Frameworks. This comparative figure provides an intuitive understanding of how the LCC hypothesis developed in this study diverges from the classical EKC approach by focusing on green finance as the structural transformation driver rather than GDP [41,54].

This comparative figure provides an intuitive understanding of how the LCC hypothesis developed in this study diverges from the classical EKC approach by focusing on green finance as the driver of structural transformation, rather than GDP.

Extending the LCC framework, this study replaces the traditional explanatory variable, GDP, with green finance to better capture the financial dynamics that underpin sustainable development transitions. Recent empirical studies have increasingly recognized that GDP alone may not sufficiently account for the structural transformations required for environmental sustainability, particularly in emerging economies. By focusing on climate-related capital flows, this research aligns with contemporary perspectives emphasizing the role of sustainable finance in advancing environmental outcomes.

Substantial empirical support for the LCC hypothesis can be found in the recent literature. For instance, Pata and Ertugrul [55] and Erdogan [56] confirmed the U-shaped relationship between economic activities and environmental carrying capacity, indicating that improvements in institutional frameworks and financial mobilization can reverse initial environmental degradation. Similarly, Yurtkuran and Güneysu [57] and Güneysu [58] demonstrated that in Türkiye, financial development and globalization processes, when aligned with green finance strategies, positively affect the LCF, thereby enhancing ecological sustainability.

Moreover, broader evidence from emerging economies supports the integration of green finance into LCC models. Dai et al. [59] emphasized that human capital and renewable energy investments significantly improve the LCF, while Ximei et al. [60] underlined the role of information and communication technology and globalization factors in shaping environmental outcomes consistent with the LCC hypothesis.

However, the literature also presents some contradictory findings. Pata et al. [61] and Ulussever et al. [62] reported cases where economic and financial globalization did not necessarily translate into improvements in environmental carrying capacity. These studies highlight that the relationship may be context-dependent, influenced by variations in governance quality, absorptive capacity, and structural economic factors. Thus, while a substantial body of research supports the extended LCC framework incorporating green finance, inconsistencies in empirical findings underscore the need for context-specific analysis, such as that conducted for Türkiye in this study.

In the context of EKC and LCC analyses, the relationships among development level, globalization, and environmental outcomes have been widely studied. Increasing global economic and social integration has significant implications for sustainable development. For instance, the seminal work by Grossman and Krueger [40] analyzed the environmental effects of the NAFTA. Since the 1990s, the EKC hypothesis has become a central framework in discussions on globalization and sustainability, with particular emphasis on the environmental impacts of trade and financial liberalization under economic globalization. When accompanied by green finance opportunities, globalization can have positive effects on environmental quality [46,62]. However, negative outcomes, such as pollution leakage, may occur when foreign direct investments shift toward developing or least developed countries with weaker environmental regulations. These dynamics highlight the growing importance of international coordination and policy alignment in sustainable development strategies [63,64].

Therefore, a clear connection exists between globalization policies and international capital flows (ICF) from developed to developing countries. Within this framework, economic globalization—particularly financial liberalization—can facilitate access to global green finance resources. In sustainable development financing, it is often recommended that developing countries prioritize capital flows such as ICF rather than financing options that exacerbate debt burdens [65,66]. Furthermore, for developing economies facing trade-offs among human development, inequality, and environmental degradation, increased access to development assistance is seen as beneficial [67]. The effective integration of ODA within national public policy frameworks is also considered essential to maximize developmental outcomes.

Despite the growing interest in green finance and environmental sustainability in developing economies, empirical studies exploring their relationship through the LCC framework remain limited. Addressing this gap, the present study provides new evidence from Türkiye.

4.2. Theoretical Justification of the Model

In conventional environmental economics, scale effects are typically associated with production expansion that intensifies environmental stress—especially when driven by traditional industrial or GDP-based growth. However, this study conceptualizes green finance not as a neutral capital inflow, but as a development-oriented financial instrument that initiates positive scale dynamics in the context of sustainability [44,47]. In particular, climate-related ODA flows are viewed as catalytic financial mechanisms that bridge the transition from development-driven growth to sustainability-oriented, climate-resilient transformations.

Unlike undirected financial expansion or GDP-driven growth, which may initially degrade environmental quality, green finance channels capital directly into projects that enhance environmental performance—such as renewable energy, energy efficiency, and adaptive infrastructure [68,69]. This distinction allows green finance to generate a scale effect with positive externalities, in contrast to the negative scale pressures traditionally emphasized in EKC-type models.

Within the LCC framework, green finance acts as a transformative financial mechanism, initially limited by institutional capacity and sectoral absorption constraints. As this capacity improves, the environmental benefits of green finance intensify, leading to a U-shaped relationship between green finance intensity and environmental sustainability—where environmental quality first declines, then improves after a threshold. Thus, instead of treating scale as an exogenous burden on the environment, our model highlights green finance as an endogenous enabler of structural change. This theoretical framing allows reinterpretation of the scale effect as a function of the quality and direction of financial flows, rather than their volume alone.

Based on the LCC framework and drawing from the scale, composition, and technique effects initially conceptualized by Grossman and Krueger [39] and Panayotou [41], this study hypothesizes a U-shaped relationship between green finance and environmental carrying capacity. In the early stages, limited and uncoordinated green finance flows may generate a negative scale effect, exacerbating environmental stress due to transitional inefficiencies and weak absorptive capacity. However, as green finance inflows grow and are increasingly channeled into renewable energy, sustainable infrastructure, and clean technologies, composition and technique effects become dominant. These effects lead to structural transformations and technological advancements that enhance environmental regenerative capacity. This theoretical framework underpins the expected non-linear dynamics observed in the empirical analysis.

In addition to green finance, this study incorporates the KOF Financial Globalization Index (KOFFI) to account for the structural macro-financial environment that conditions the effectiveness of climate-related capital flows. Unlike traditional growth-based models that control for income or GDP, we argue that financial globalization constitutes a more policy-relevant dimension, especially in emerging economies, where the ability to absorb and allocate green finance depends significantly on global financial integration [63]. KOFFI, as a composite index of both de facto (e.g., FDI, portfolio flows, external debt) and de jure (e.g., capital account openness, investment agreements) elements, captures the institutional and market-based linkages between a country and the global financial system [70]. This is critical in the context of green finance, which often originates from international development banks and multilateral institutions.

In line with the recent literature, our inclusion of the KOFFI reflects the recognition that financial globalization can both enable and constrain environmental sustainability, depending on the regulatory and absorptive capacities of the recipient country [50,63]. Evidence from emerging economies suggests that while global financial integration facilitates access to green finance, institutional weaknesses and governance deficits can undermine its environmental benefits. This modelling approach represents a novel contribution to the literature by replacing GDP controls with a more functional macro-financial variable, thereby aligning the empirical specification with the global institutional mechanisms that shape climate finance effectiveness.

While we acknowledge that disaggregating financial globalization into its components (e.g., FDI, portfolio flows) could offer nuanced insights, we retain the composite KOFFI variable for both theoretical and empirical reasons. First, as Rodrik [71] emphasized, de facto financial flows—such as private capital movements—are highly cyclical and vulnerable to global financial volatility, posing risks to sustainability transitions in emerging economies. Complementary evidence from Boujedra [66] highlights how volatility and governance effectiveness jointly condition the environmental impacts of financial flows in developing countries. At the same time, financial openness and liberalization policies (de jure aspects) play a critical role in enhancing access to green finance resources and fostering institutional resilience. Given that green finance flows—particularly ODA and multilateral loans—cut across both private and public channels, the composite KOFFI index provides a more comprehensive reflection of a country’s macro-financial integration and capacity to absorb climate finance. Therefore, using the KOFFI aligns with our systemic approach to analyzing the enabling environment for sustainability financing and ensures model stability given the single-country context and limited sample size.

4.3. Data

This study rigorously investigates the impact of green finance and financial globalization on environmental sustainability in Türkiye, utilizing annual data spanning the 2001–2021 period. The analysis is situated within the conceptual framework of the LCC hypothesis, which posits a U-shaped relationship between economic or financial drivers and ecological outcomes.

Environmental sustainability is proxied by the LCF, capturing the ratio of biocapacity to EF and serving as a comprehensive measure of an ecosystem’s regenerative capacity. Green finance is measured through YEF, reflecting targeted capital flows into sustainability-oriented projects. Financial globalization is represented by the KOFFI, developed by the KOF Swiss Economic Institute, capturing both de facto and de jure aspects of a country’s integration into global financial markets. Detailed information on the variables and their data sources is provided in Table 1.

Table 1.

Descriptive information on the variables used in the analysis created by the authors.

All variables are transformed into their natural logarithmic forms to facilitate elasticity interpretation and to mitigate potential heteroskedasticity concerns, thereby ensuring statistical robustness. The empirical analysis was performed using EViews 10 (IHS Global Inc., Irvine, CA, USA).

Descriptive statistics of the variables are summarized in Table 2. The results of the Jarque–Bera normality test indicate that all variables follow a normal distribution, with p-values exceeding the 5% significance threshold.

Table 2.

Descriptive statistics. Created by the authors.

As shown in Table 2, all variables are expressed in their natural logarithmic forms. The Jarque–Bera test statistics confirm that none of the variables deviate significantly from a normal distribution, thereby validating the suitability of the dataset for econometric analysis.

4.4. Model Specification

The econometric model analyzed in this study is constructed to empirically test the predictions of the LCC hypothesis, which posits a U-shaped relationship between financial drivers and environmental sustainability. Following recent empirical applications, the model is specified as follows [45,54,69]:

where

- L denotes the natural logarithmic transformation of the variables;

- LLCF is the logarithm of the LCF, representing environmental sustainability;

- LYEF is the logarithm of YEF (green finance);

- LYEF2 is the squared term of green finance, included to capture potential non-linear (U-shaped) effects;

- LKOFFI is the logarithm of the KOF Financial Globalization Index;

- μt is the error term.

All variables are transformed into their natural logarithmic forms to allow for elasticity interpretation and to mitigate potential heteroskedasticity issues, ensuring statistical robustness.

The inclusion of the squared term (LYEF2) is particularly critical, as it enables the detection of a non-linear relationship between green finance and environmental sustainability, as suggested by the LCC hypothesis. A positive and significant coefficient for LYEF2 would confirm the U-shaped relationship, indicating that while initial increases in green finance might degrade environmental quality, higher levels of green finance contribute to improving the LCF after a certain threshold.

4.5. Methodology

This study employs the autoregressive distributed lag (ARDL) bounds testing approach to examine the long-run and short-run relationships among green finance, financial globalization, and environmental sustainability. The ARDL method, developed by Pesaran, Shin, and Smith [74] is particularly advantageous when variables exhibit mixed orders of integration, i.e., I(0) and I(1), and it provides consistent and efficient estimates even with relatively small sample sizes [75].

Before determining the appropriate econometric method, the stationarity properties of the time series must be analyzed. For this purpose, two widely used unit root tests are employed: the ADF test [76] and the PP test [77]. Given that the PP test is considered to produce more robust results, particularly in cases of small sample sizes, it is utilized alongside the ADF test in this study [78]. The results of the unit root tests are presented in Table 3.

Table 3.

Unit root test results. Created by the authors.

According to the results presented in Table 3, all variables contain unit roots at their levels but become stationary after first differencing. Moreover, none of the series are found to be integrated of order two, I(2). Therefore, the ARDL bounds testing approach developed by Pesaran, Shin, and Smith [74] is deemed suitable for analyzing the long-run relationships among the variables. The ARDL model is particularly advantageous as it allows for the inclusion of variables with different integration orders (i.e., I(0) and I(1)) and performs well even with small sample sizes [79].

Within the ARDL bounds testing framework, the analysis begins by constructing a conditional error correction model (ECM) as specified below:

where

- Δ refers to the first-difference operator;

- p, m, n, and r represent the optimal lag lengths;

- μt denotes the error term.

After determining the optimal lag structure, the presence of a long-run cointegration relationship is tested using the following null and alternative hypotheses:

If cointegration is confirmed, both short-run and long-run coefficients are estimated in the subsequent stages.

To further enhance the robustness and validity of the long-run estimations, alternative cointegration estimators are employed:

- FMOLS (Fully Modified OLS): adjusts for endogeneity and serial correlation, yielding unbiased long-run parameter estimates.

- DOLS (Dynamic OLS): incorporates leads and lags of differenced regressors, thereby correcting for simultaneity bias.

- CCR (Canonical Cointegrating Regression): minimizes bias and standard errors through adjustments for long-run endogeneity.

This multi-method strategy addresses various econometric limitations such as endogeneity, autocorrelation, and simultaneity bias, thereby ensuring the credibility and consistency of the empirical findings.

In addition to its methodological rigor, this study employs the empirical framework to test a specific theoretical proposition—the LCC hypothesis. The LCC hypothesis posits that economic development and structural transformation initially exert a negative impact on environmental carrying capacity, but over time, as economies mature, this effect reverses, leading to environmental improvement. Recent empirical studies, including those by Dogan and Pata [54] and Ximei et al. [60], have provided support for this non-linear relationship. By applying this framework to the context of Türkiye, the study not only tests the LCC hypothesis in a developing economy setting but also contributes new insights to the broader discourse on environmental sustainability.

Overall, this comprehensive methodological framework enables a nuanced examination of both short-run and long-run dynamics. The incorporation of multiple robustness checks ensures the credibility of the results, thereby enhancing the validity of the empirical analysis.

4.6. Empirical Results

The optimal lag length for the ARDL model was selected as ARDL(1,1,0,1) based on the Akaike Information Criterion (AIC). According to the results presented in Table 4, the calculated F-statistic for the joint significance of the lagged level variables [75] is greater than the 1% critical value (6.50 > 5.33). Additionally, the t-statistic for the lagged dependent variable [74] exceeds the 1% critical threshold in absolute terms (4.79 > 4.37).

Table 4.

Cointegration test results of the ARDL(1,1,0,1) model. Created by the authors.

These findings confirm the existence of a long-run cointegration relationship among the variables. Furthermore, the diagnostic tests indicate that the model does not suffer from structural problems at the 1% level of significance.

As shown in Table 4, the calculated F-statistic (6.50) exceeds the 1% upper bound critical value of 7.06 in [75], while the t-statistic (−4.79) also exceeds the corresponding 1% critical value of −4.37 based on Pesaran, Shin, and Smith [74]. These results confirm the existence of a long-run cointegration relationship. In addition, all diagnostic tests support the adequacy of the model, indicating no misspecification, no autocorrelation, and homoscedastic residuals at the 1% significance level.

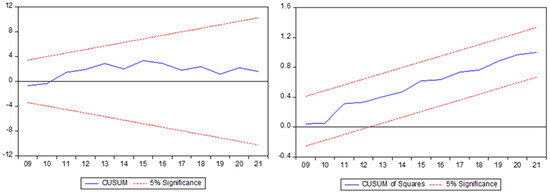

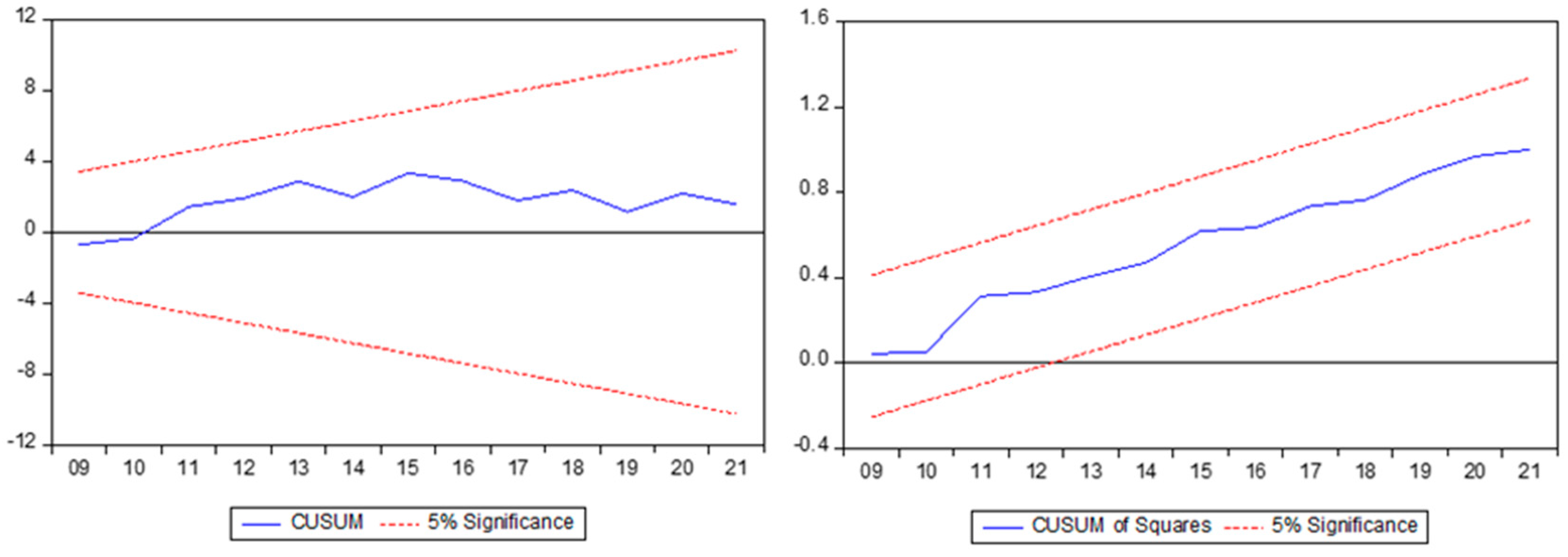

Figure 3 presents the CUSUM and CUSUMQ plots for the ARDL model used in the analysis. The results indicate that the estimated model remains stable over the sample period. Therefore, the estimated coefficients are expected to yield reliable results within the 95% confidence interval. While the CUSUM and CUSUMQ tests confirm parameter stability, it is important to acknowledge that model misspecification—such as omitted variable bias or measurement errors—can still affect the consistency and explanatory power of coefficient estimates. However, the use of robust estimation techniques (ARDL with FMOLS, DOLS, and CCR) mitigates these risks and enhances the credibility of the results.

Figure 3.

CUSUM and CUSUMQ Plots. Created by the authors.

Table 5 reports the short-run and long-run coefficient estimates for the ARDL model. All long-run coefficients are statistically significant at the 1% level and align with theoretical expectations. Specifically, a 1% increase in LYEF is associated with a 0.291% decrease in the LLCF, indicating a short-term negative environmental impact. In contrast, the squared term LYEF2 and the LKOFFI exert positive effects of 0.008% and 0.183%, respectively.

Table 5.

Short- and long-run coefficient estimates for the dependent variable (LLCF). Created by the authors.

However, the p-value for LKOFFI (0.100) suggests that this coefficient is not statistically significant. Overall, the findings provide empirical support for a U-shaped relationship between green finance and environmental quality in Türkiye during the study period. The turning point of this U-shaped relationship is calculated as LYEF ≈ 16.68, which corresponds to approximately USD 17.5 million

In the analysis of short-run coefficients, particular attention must be paid to the error correction term of the cointegration model. The estimated coefficient of the error correction term, ECM (HDM(−1)), is negative as expected, and its corresponding t-statistic is statistically significant at the 1% level. Specifically, the absolute value of the t-statistic (−5.66) exceeds both the lower and upper critical bounds (I(0) = 3.43; I(1) = 4.37), confirming the validity of the short-run dynamics.

Accordingly, the short-run coefficients are consistent with the long-run equilibrium, and deviations from equilibrium are corrected within approximately one year (1/0.96 ≈ 1.04). Notably, the coefficient of the LKOFFI variable is statistically significant at the 1% level and higher in the short run, indicating that the impact of financial globalization on environmental quality is stronger in the short term but weakens over the long run.

As shown in Table 6, the long-run coefficient estimates obtained from FMOLS, DOLS, and CCR estimators support the short-run findings derived from the ARDL model. Across all three estimation techniques, the LKOFFI variable is found to be statistically significant. Specifically, a 1% increase in financial globalization is associated with improvements in environmental quality by approximately 0.18% in FMOLS, 33% in DOLS, and 0.16% in CCR models. These findings indicate that, when considered alongside climate-focused capital flows, financial globalization plays a critical role as a policy-relevant variable in achieving environmental sustainability [46,67,68].

Table 6.

Long-run estimates using FMOLS, DOLS, and CCR methods. Created by the authors.

The findings of this study are consistent with a growing body of empirical research indicating that green finance has a positive impact on environmental sustainability [44,45,46,47,49]. Furthermore, when interpreted through the lens of the LCC hypothesis, the results support prior studies that confirm the existence of a U-shaped relationship between economic-financial variables and environmental quality [55,56,57,59,60].

Overall, the empirical findings of this study are in line with the growing body of literature that highlights the critical role of green finance and financial globalization in fostering environmental sustainability and structural economic transformation. Aligned with the LCC framework, these results demonstrate how sustainable financing flows contribute to resilience-building efforts in emerging economies, particularly in the case of Türkiye.

5. Discussion and Comparative Analysis

5.1. Comparative Analysis of Empirical Findings

The empirical findings confirm that green finance and financial globalization positively influence environmental sustainability in Türkiye, consistent with the theoretical expectations of the LCC hypothesis. Specifically, the study identifies a U-shaped relationship between green finance and environmental quality, indicating that while initial financial flows may impose environmental stress, subsequent increases contribute to ecological improvements as institutional absorptive capacity strengthens. Furthermore, a 1% increase in financial globalization is associated with improvements in environmental sustainability across all estimation techniques, reinforcing the significance of macro-financial integration in sustainability transitions.

These results are consistent with previous studies [46,68], which highlight the pivotal role of climate-related capital flows and renewable energy investments in improving environmental performance in developing economies. However, this study extends the literature by providing empirical evidence specific to Türkiye, an emerging economy characterized by structural vulnerabilities like currency volatility and external financing dependency, which condition the effectiveness of green finance initiatives.

Furthermore, the confirmation of a U-shaped relationship between financial variables and environmental sustainability parallels the findings in previous studies [51,55], which demonstrate that the initial adverse effects of financial globalization on ecological outcomes can be reversed as institutional absorptive capacity and governance frameworks strengthen over time. In a broader comparative context, similar dynamics have been observed among BRICS-T economies [63], where improvements in governance quality significantly enhance the environmental benefits of financial globalization. These comparative insights underscore the critical role of complementary institutional reforms in maximizing the positive externalities of global financial integration for environmental sustainability.

5.2. Green Finance, Adaptive Capacity, and Sustainability in Developing Economies

Compared to other emerging economies, Türkiye’s experience reveals both notable similarities and important distinctions. Similar to ASEAN countries analyzed [51], Türkiye demonstrates that targeted financial policies and green financing strategies can effectively accelerate sustainability transitions. However, Türkiye’s heightened exposure to geopolitical volatility, currency fluctuations, and external financing pressures, as highlighted [56], introduces additional macroeconomic risks. These structural vulnerabilities necessitate cautious policy design when integrating global green finance flows into national development strategies to ensure long-term environmental and economic resilience.

In terms of policy implications, the findings advocate for a more strategic alignment between financial globalization policies and national sustainability objectives. Specifically, financial instruments such as green sukuk—successfully implemented in countries like Malaysia and Indonesia, as discussed [66]—could be tailored to Türkiye’s financial ecosystem to diversify funding sources and enhance financial resilience. Moreover, strengthening the data infrastructure for climate finance, as in [69], is critical for ensuring transparency, enabling effective monitoring, and facilitating comprehensive impact assessments. Improving data quality would also support the integration of climate-related financial flows into broader national development strategies, enhancing both accountability and policy effectiveness.

Furthermore, recent evidence [80] demonstrates that green finance significantly promotes energy transition by facilitating technological innovation and industrial restructuring, although its effectiveness may be moderated by climate-related risks. While their study focuses on regional heterogeneities within China, the mechanisms they identify—particularly the importance of robust green finance systems and adaptive policy frameworks—are highly relevant for emerging economies, including Türkiye. These insights reinforce the necessity of designing context-specific strategies to manage green finance effectively and to ensure a successful sustainability transition aligned with national development objectives.

5.3. Role of ODA in Sustainable Development Transitions

In light of these findings, it becomes evident that while domestic policy alignment and financial innovation are essential prerequisites for sustainable transitions, external financing mechanisms must also be critically evaluated. Financial globalization, as captured through composite indices such as the KOFFI index, plays a pivotal role in facilitating cross-border capital flows that support sustainable development trajectories in emerging economies [63,70]. These mechanisms are intrinsically linked to the achievement of global targets, particularly SDG 13 and SDG 17, which underscore the importance of mobilizing international finance and fostering robust international partnerships. Within this framework, ODA emerges as a vital component of green finance strategies in developing economies. A critical assessment of both the advantages and inherent risks of ODA-based financing is, therefore, essential for understanding how external capital flows can effectively complement national efforts toward achieving environmental sustainability in Türkiye and other comparable emerging markets.

ODA continues to serve as a significant conduit for facilitating sustainable development transitions by providing concessional financial flows that support climate adaptation and institutional resilience in developing countries [81]. Empirical evidence suggests that adaptation-focused ODA has contributed to capacity-building efforts and infrastructure development, particularly in regions characterized by high vulnerability [81]. Nevertheless, the effectiveness of ODA remains heterogeneous, heavily influenced by governance quality, institutional readiness, and local economic structures [82]. Furthermore, the transparency, predictability, and conditionality of ODA flows continue to be critical factors affecting their developmental impact [83]. Therefore, aligning ODA interventions with national development priorities and integrating them into broader green finance and sustainability frameworks is crucial for enhancing their effectiveness and ensuring resilient and inclusive transitions in Türkiye and other emerging economies.

For developing economies, including Türkiye, optimizing the role of ODA requires strategic alignment with national development plans, the strengthening of institutional absorptive capacities, and the integration of ODA flows into comprehensive green finance and sustainability frameworks to maximize their developmental impact.

5.4. Türkiye-Specific Policy Implications

While the broader advantages and limitations of ODA-based green finance offer valuable insights for developing economies, a more context-specific analysis is essential to capture the unique structural and macroeconomic dynamics of Türkiye. In this regard, the empirical findings of this study, confirming a U-shaped relationship between green finance, financial globalization, and environmental sustainability in Türkiye, highlight several country-specific risks and strategic policy priorities.

First, despite the recognized long-run benefits of green finance, Türkiye’s green financial market remains underdeveloped and insufficiently diversified, with a heavy reliance on conventional credit mechanisms; similar structural limitations have been documented across other emerging economies [45].

Second, the absence of stringent and enforceable environmental regulations may undermine the environmental returns of green financial flows, a challenge emphasized and mirrored in Türkiye’s current regulatory practices [58].

Third, Türkiye’s economic dependency on carbon-intensive industries exacerbates the difficulty of achieving green structural transformation, necessitating significant investments in technological innovation and renewable energy infrastructure, consistent with the findings [59].

Fourth, limited institutional capacity—particularly within local financial systems—and low levels of private sector engagement present additional barriers to the effective absorption of international climate finance, a constraint also noted in the contexts of ASEAN and BRICS-T economies [51,63].

Fifth, the lack of a robust and transparent green finance data infrastructure continues to impede the monitoring, verification, and reporting of sustainability outcomes, a gap repeatedly emphasized in the literature on emerging economies [66].

To mitigate these risks, Türkiye should prioritize expanding and diversifying its green finance portfolio, enhancing the stringency and enforcement of environmental regulations, supporting technological innovation and renewable energy investments, strengthening institutional capacities alongside private sector engagement, and establishing comprehensive data systems to monitor green financial flows and sustainability impacts. Such a holistic and multi-dimensional policy strategy would not only align Türkiye with international best practices observed in other developing economies but also reinforce its capacity to integrate financial globalization dynamics into a resilient and sustainable development pathway.

5.5. Summary of Findings and Theoretical Contributions

In summary, the findings of this study directly address the research questions posed at the outset. The positive and statistically significant impact of green finance and financial globalization on environmental quality confirms the first and second hypotheses (H1 and H2), while the observed U-shaped relationship between financial variables and environmental sustainability empirically validates the LCC hypothesis (H3) in the context of Türkiye. Beyond hypothesis validation, this study advances the LCC framework by demonstrating how sustainable financial flows and global financial integration—captured through the KOFFI—jointly enhance environmental resilience.

These results are consistent with recent empirical evidence underscoring the critical role of financial globalization in shaping sustainable development trajectories in emerging economies [63,70]. Moreover, by explicitly linking national sustainability efforts to broader global frameworks, this study provides practical guidance for aligning green finance strategies with the SDG 13 and SDG 17. In doing so, it delivers both theoretical enrichment and actionable insights for policymakers in Türkiye and comparable developing economies seeking to balance financial integration with long-term environmental sustainability objectives.

Building on the preceding discussion, the next section synthesizes the key conclusions and presents targeted policy recommendations derived from the Turkish experience, with broader implications for emerging markets globally.

6. Conclusions and Evaluation

This study aimed to examine the role of green finance policies in improving environmental quality during Türkiye’s transition to a low-carbon economy. In the analysis, the LCF was employed as a comprehensive proxy for environmental quality and sustainability. The variable representing climate-related capital flows from developed to developing countries was used as a measure of international green finance, while the KOF Financial Globalization Index was included to capture the influence of economic integration policies in this process.

Based on theoretical expectations, it was hypothesized that green finance might have a negative effect on environmental sustainability in the short run, but as financing levels increase over time, economic activity and financial liberalization could contribute positively to environmental capacity in the long run. These hypotheses were tested using the ARDL bounds testing approach along with alternative cointegration estimators including FMOLS, DOLS, and CCR.

This study highlights key gaps in the literature in terms of theoretical model design and variable selection. It underscores the need to evaluate financial development not only in aggregate terms, but also in relation to sectoral resource use and access to green financial instruments. The fact that sustainability-centered finance frameworks gained momentum globally only after the 2000s—and that Türkiye’s green finance initiatives began later than those of developed countries—has contributed to a lack of comprehensive, climate-targeted financial data. This data scarcity presents challenges for conducting ex-post analyses aimed at generating country-level policy implications. Therefore, there is a pressing need to establish institutional structures at the national level that can classify sustainability-oriented financial activities and ensure their alignment with international reporting frameworks and databases. Doing so would enhance both the effectiveness of resource allocation in green finance and the predictive capacity of impact assessments linked to sustainability goals.

Based on the empirical findings, this study concludes that there exists a long-run relationship between environmental quality—measured through the LCF—and both green finance and financial globalization in Türkiye during the 2001–2021 period. The results suggest that increases in green finance contribute positively to environmental quality over time. In line with the LCC hypothesis, the combined effect of green finance and financial globalization appears to support environmental sustainability in the long run, and the policies adopted during this period have contributed positively to this trajectory. These findings have broader implications for emerging economies undergoing financial liberalization and seeking to integrate green finance flows into their sustainable development strategies.

Given the national sustainability targets and evolving global financial landscape, context-specific strategies are necessary to maximize benefits while minimizing potential risks. To reduce the financial burden of its sustainability agenda and meet its carbon targets, Türkiye should continue to leverage global climate finance. However, future research should carefully assess the macroeconomic implications of receiving such financial flows—whether in the form of aid, debt, or investment finance—particularly for developing countries, where external funding may entail trade-offs and long-term fiscal consequences. Given Türkiye’s structural constraints such as geopolitical volatility and currency instability, the interpretation of our findings should consider these macro-institutional realities, which remain outside the empirical model but are critical for policy implementation.

The findings of this study suggest that long-term access to YEF plays a crucial role in strengthening environmental sustainability in emerging economies. Based on the results, three policy recommendations can be proposed:

- (i)

- Financial globalization policies should be accompanied by green finance strategies to enhance environmental carrying capacity.

- (ii)

- Climate-related ODA flows should prioritize investments that simultaneously promote structural economic transformation and ecological regeneration.

- (iii)

- National development plans should integrate green finance mechanisms with sustainable development strategies to maximize the environmental benefits of globalization.

This study contributes to the literature by integrating ecological sustainability and macro-financial structure within a unified empirical framework. By employing the LCF as a supply-side sustainability indicator and the KOFFI as a composite measure of financial integration, the analysis captures both the environmental resilience of ecosystems and the enabling role of financial openness in facilitating green finance flows. This dual focus offers a novel perspective on the structural conditions underpinning sustainable development transitions in emerging economies.

Despite these contributions, this study has several limitations that should be acknowledged. First, the analysis is limited to Türkiye and relies on annual data covering the period 2001–2021, which may constrain the generalizability of the findings to other emerging economies. Second, the scope of green finance in this study is restricted to climate-related development flows, without considering broader green financial instruments such as green bonds or sustainability-linked loans. Future research could extend this framework by conducting cross-country analyses across different income groups and regions, and by incorporating disaggregated green finance indicators to better understand sector-specific impacts on environmental sustainability.

Author Contributions

Conceptualization, methodology, writing—original draft preparation, writing—review and editing: P.Y. and C.O.; formal analysis, econometric modeling, investigation, visualization: P.Y.; supervision: C.O. All authors have read and agreed to the published version of the manuscript.

Funding

This research received no external funding.

Institutional Review Board Statement

Not applicable.

Informed Consent Statement

Not applicable.

Data Availability Statement

The data used in this study are publicly available from the Global Footprint Network (https://data.footprintnetwork.org/, accessed on 21 October 2024), OECD Climate Finance Database (https://www.oecd.org/, accessed on 21 October 2024), and KOF Swiss Economic Institute (https://kof.ethz.ch/, 21 October 2024).

Conflicts of Interest

The authors declare no conflicts of interest.

References

- Ye, X.; Rasoulinezhad, E. Assessment of Impacts of Green Bonds on Renewable Energy Utilization Efficiency. Renew. Energy 2023, 202, 626–633. [Google Scholar] [CrossRef]

- Vohra, K.; Vodonos, A.; Schwartz, J.; Marais, E.A.; Sulprizio, M.P.; Mickley, L.J. Global Mortality from Outdoor Fine Particle Pollution Generated by Fossil Fuel Combustion: Results from GEOS-Chem. Environ. Res. 2021, 195, 110754. [Google Scholar] [CrossRef] [PubMed]

- United Nations Environment Programme (UNEP). Global Resources Outlook 2024: Pathways to Sustainable Resource Use. 2024. Available online: https://www.resourcepanel.org/reports/global-resources-outlook-2024 (accessed on 15 November 2024).

- Bhutta, U.S.; Tariq, A.; Farrukh, M.; Raza, A.; Iqbal, M.K. Green Bonds for Sustainable Development: Review of Literature on Development and Impact of Green Bonds. Technol. Forecast. Soc. Change 2022, 175, 121378. [Google Scholar] [CrossRef]