Risks, Obstacles and Challenges of the Electrical Energy Transition in Europe: Greece as a Case Study

Abstract

1. Introduction

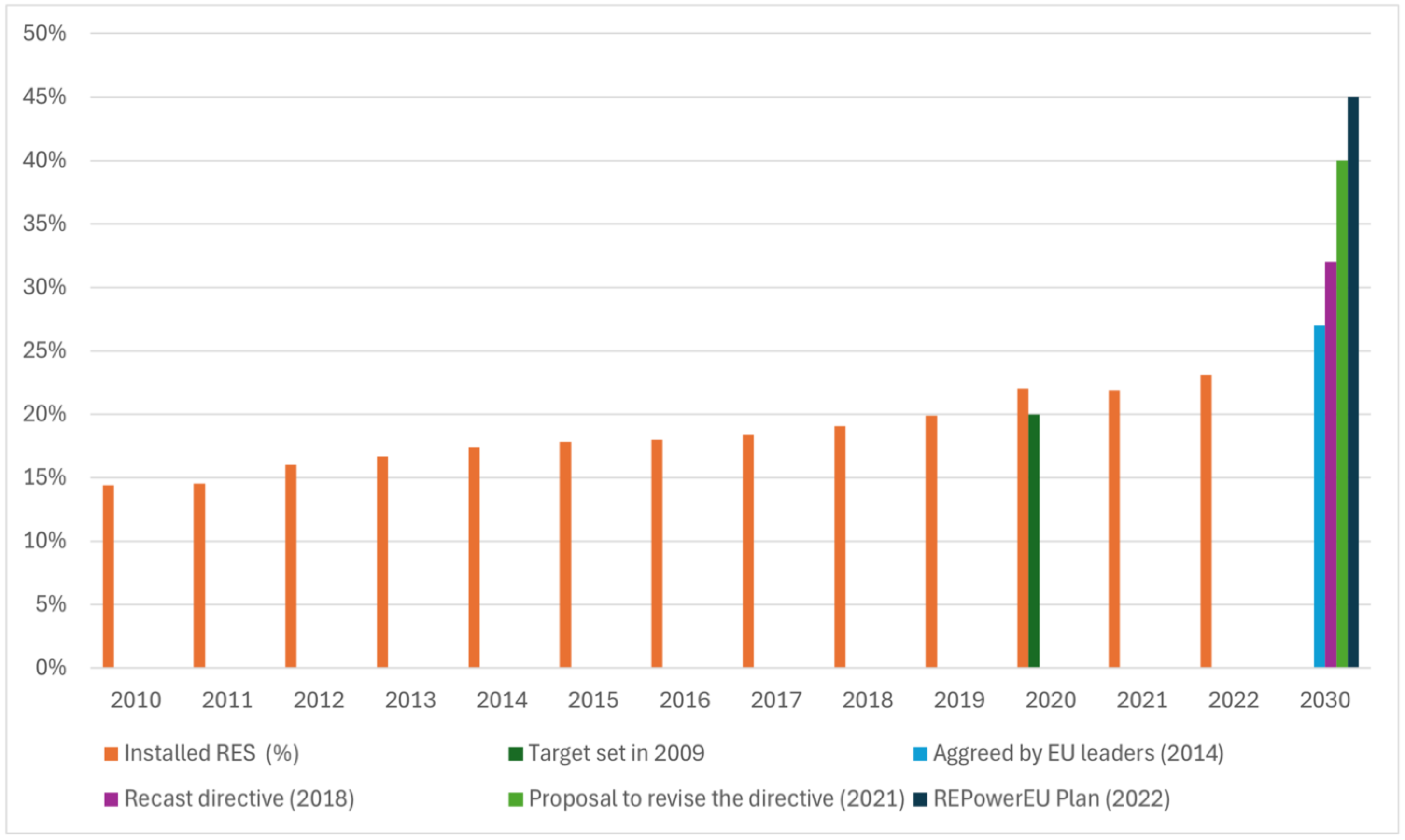

2. The Goals of the EU Energy Transition Until 2050

3. Barriers That Decelerate the European Energy Transition

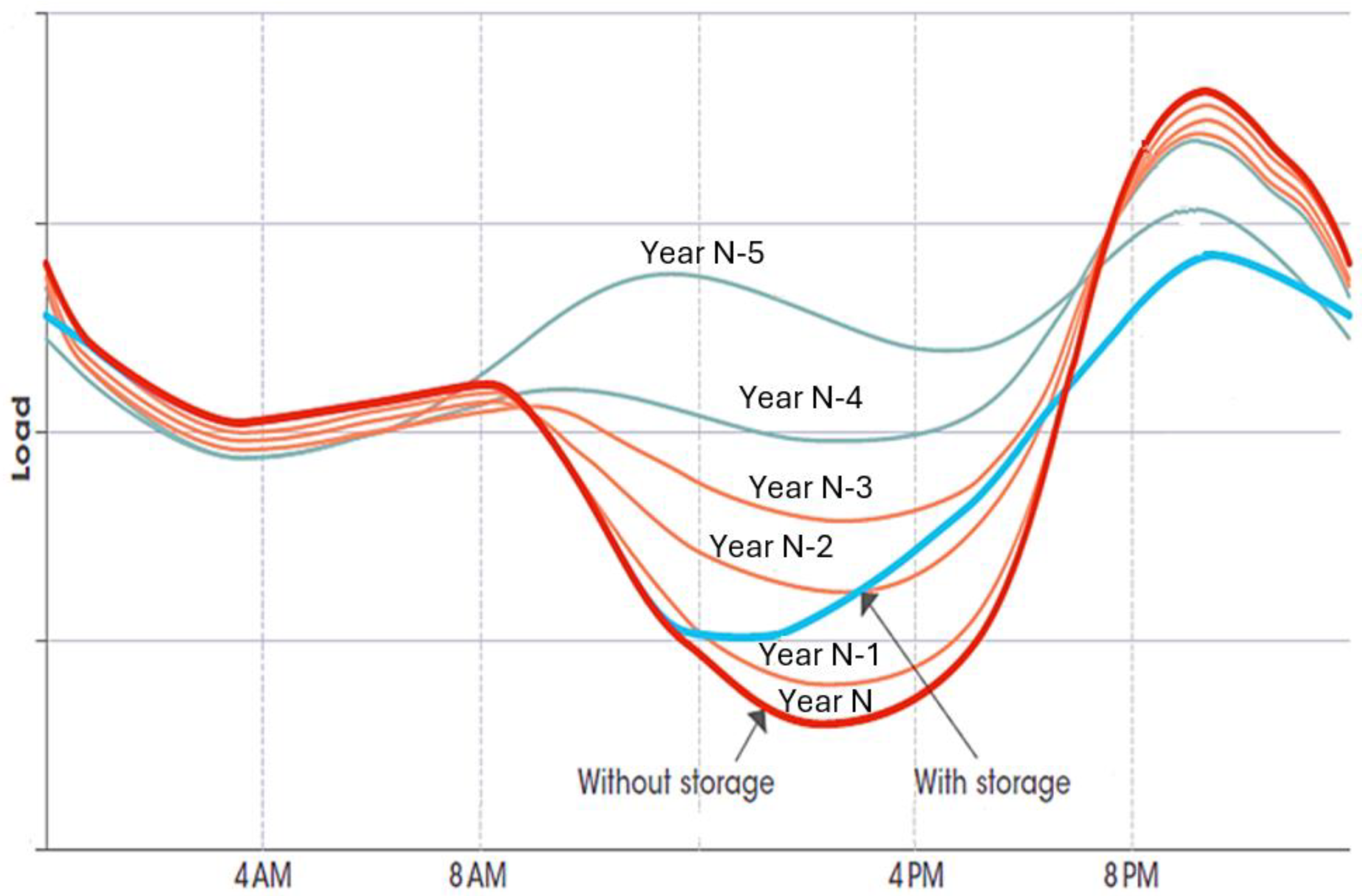

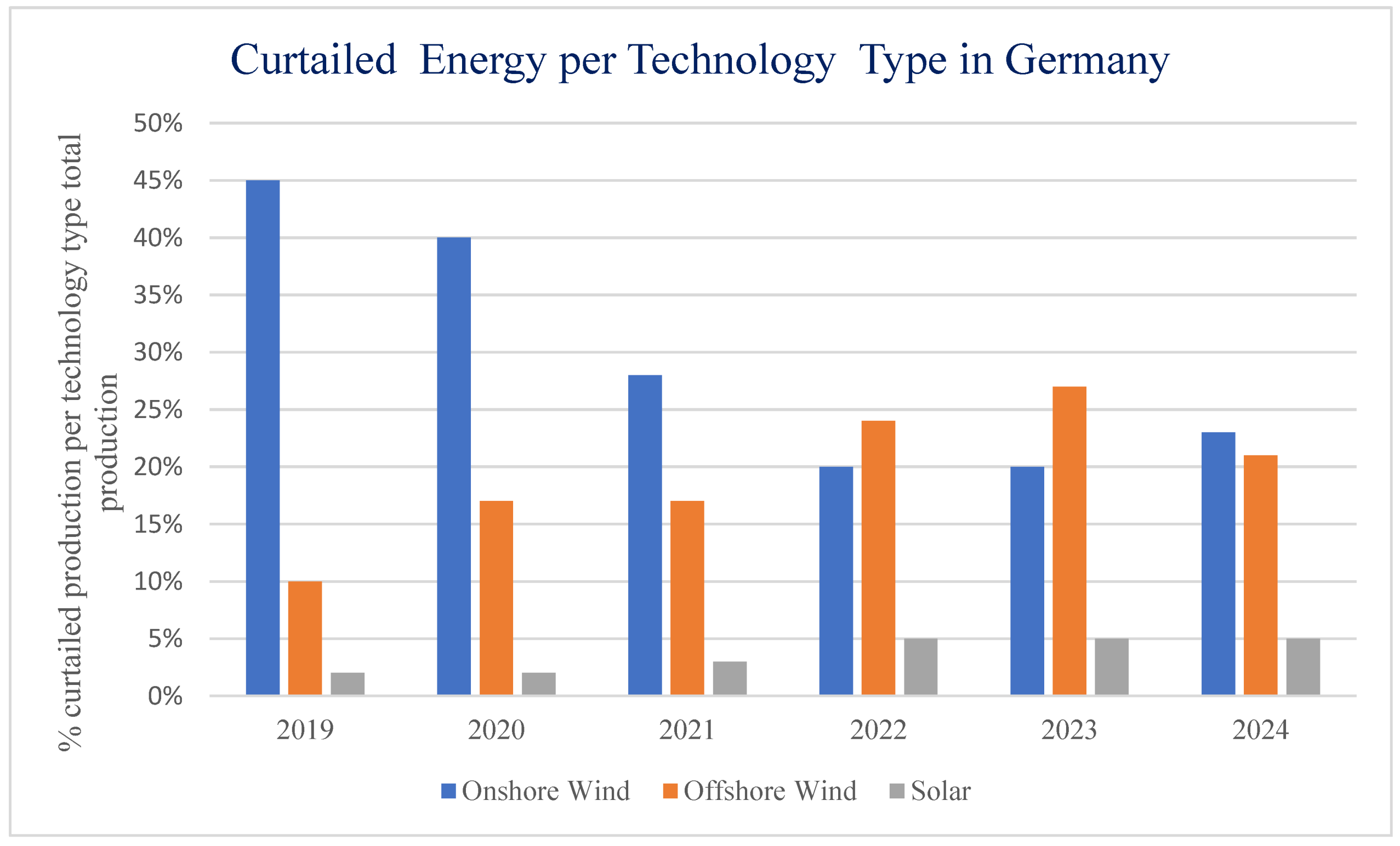

3.1. The Impact of Wind and Solar Generation to the Power System

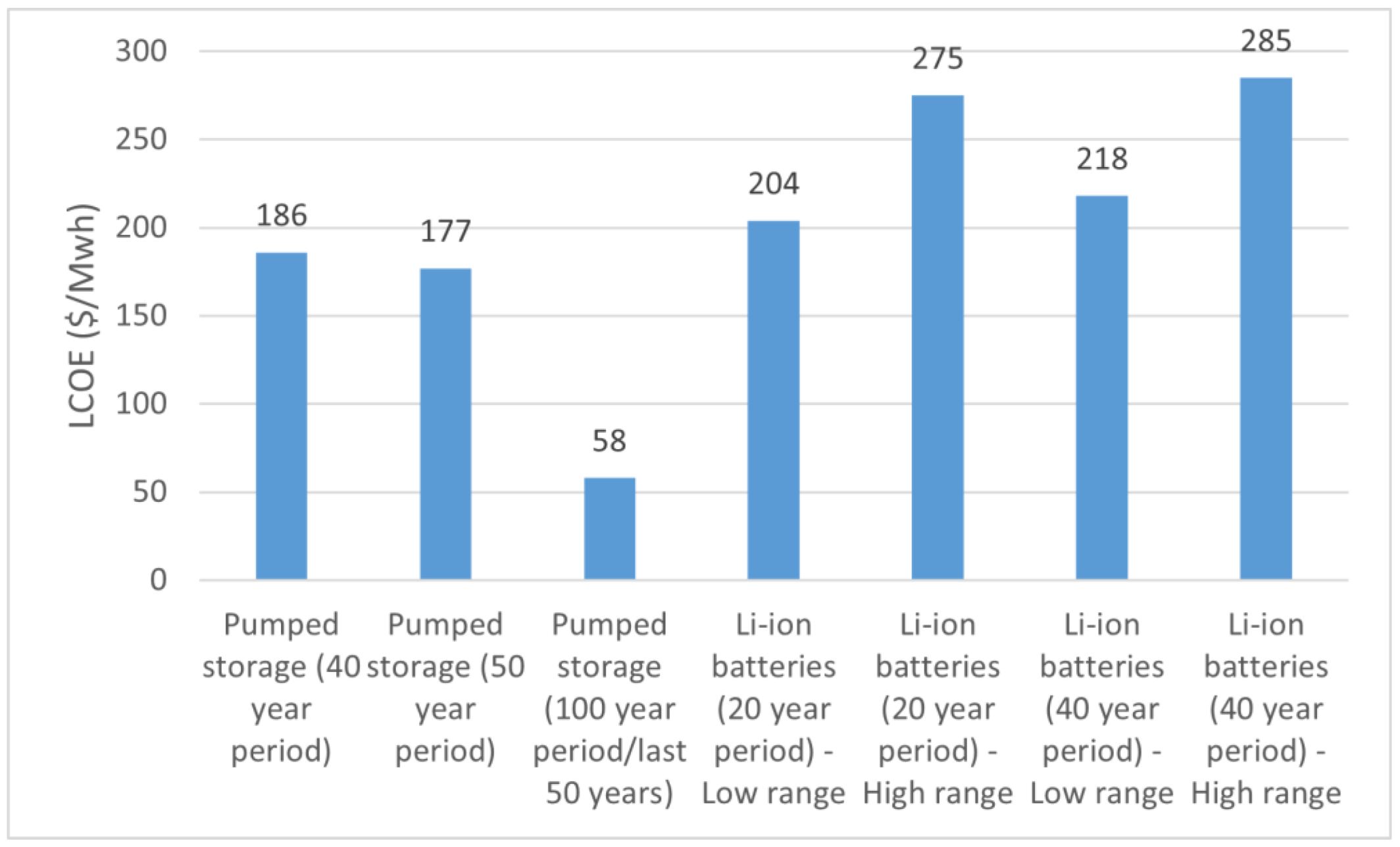

3.2. Lack of Energy Storage Capacity in Europe and High Costs

- Geographical, geological, and environmental limitations related to the design of reservoirs. Hydroelectric systems present difficulty finding topographically suitable areas that have sufficient water capacity and an appropriate elevation difference.

- The high cost of investment.

- The long implementation times (for licensing and construction).

3.3. Grid Infrastructure

3.4. Political Will and Market Design

- Recovering fixed investment costs for RESs and other assets at near-zero marginal cost, resulting in low average wholesale energy market prices.

- Encouraging investment in flexible technologies to ensure supply security when renewables are intermittent.

- Providing spatial price signals to reflect associated costs.

- To enable the transition to the energy and electrical system of the future, three areas demand more attention from governments than they have received thus far.

- Developing a new market architecture to provide decarbonized electricity supply.

- Avoiding government interventions that hinder the transition and increase costs; and

- Encouraging consumer participation in electricity markets.

3.5. Investment Risks

4. Case Study: The Energy Transition in Greece

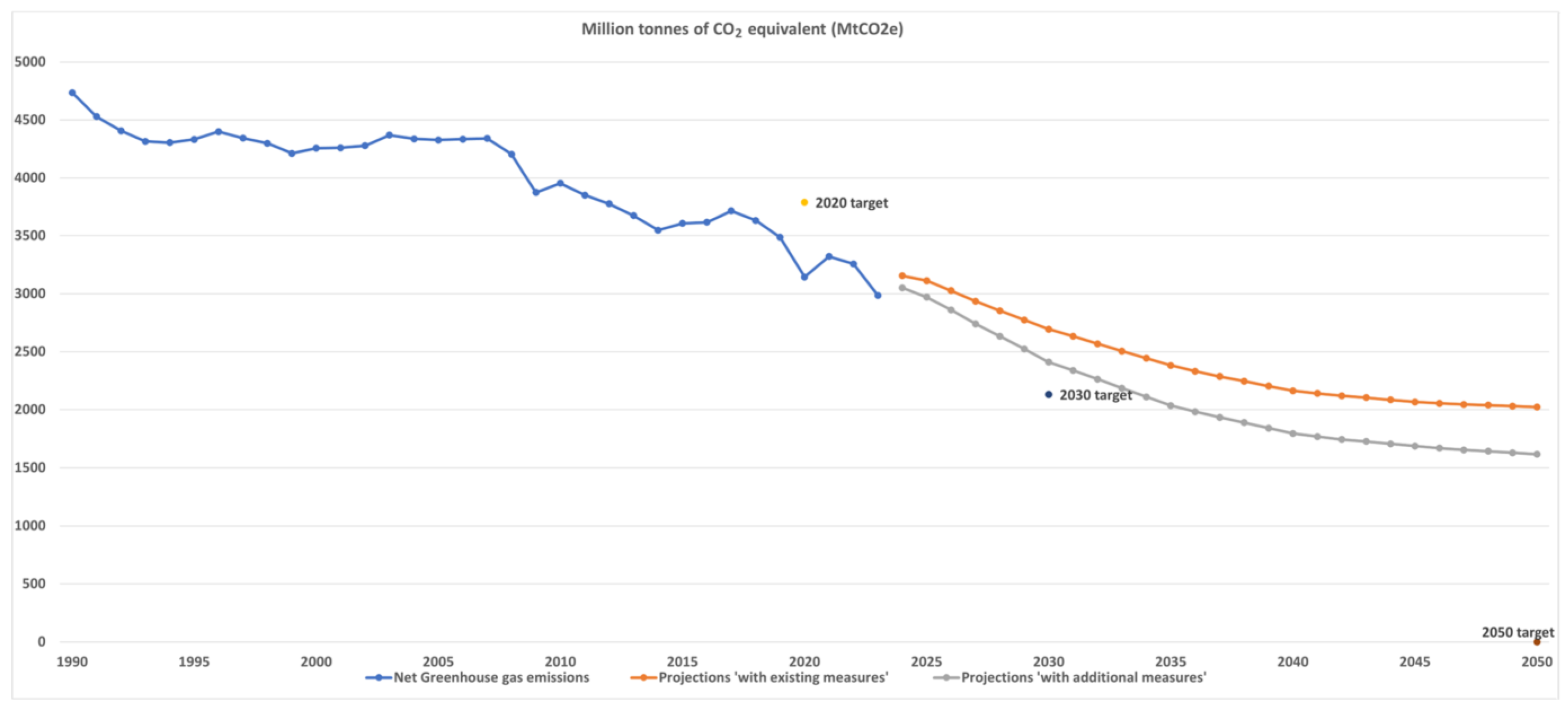

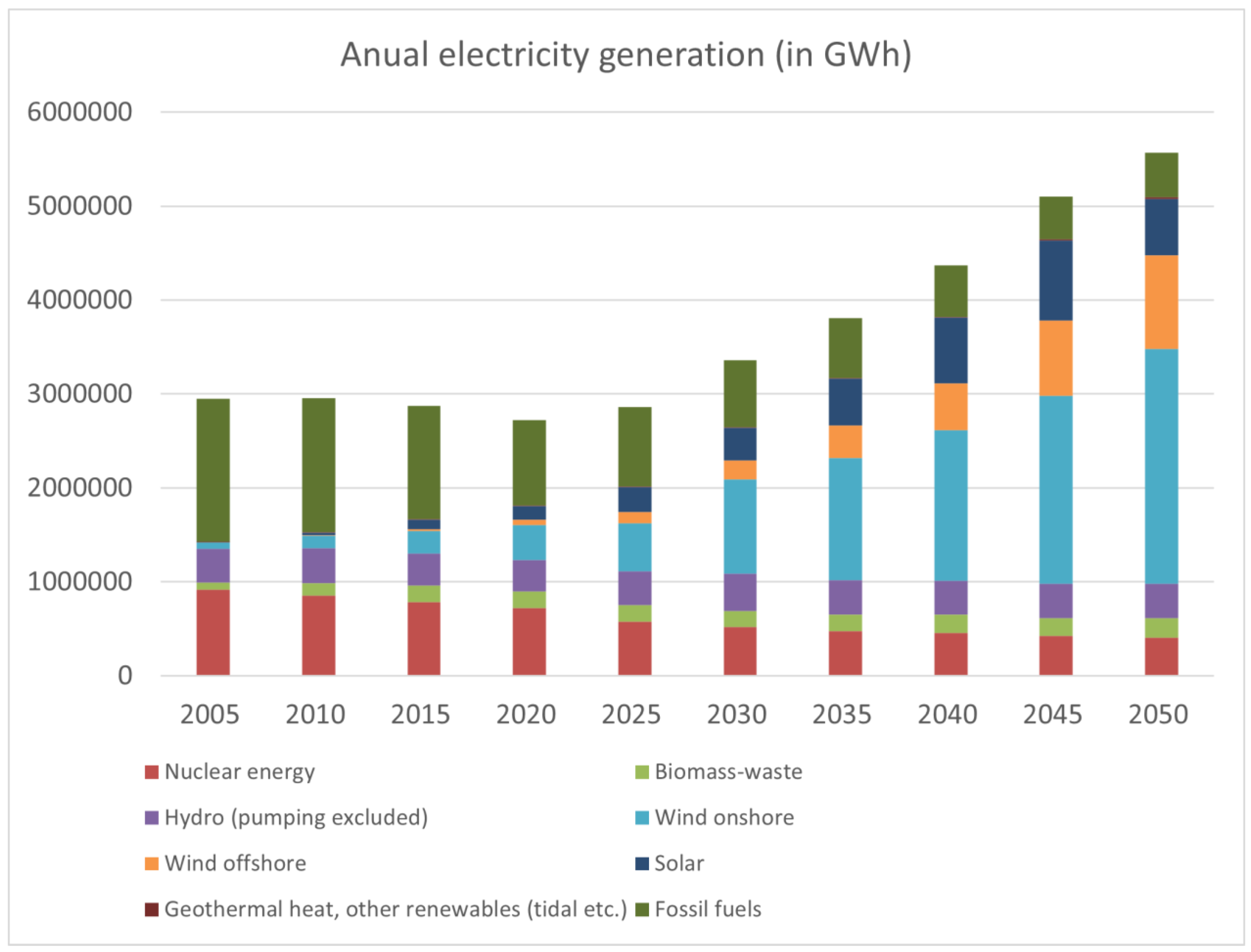

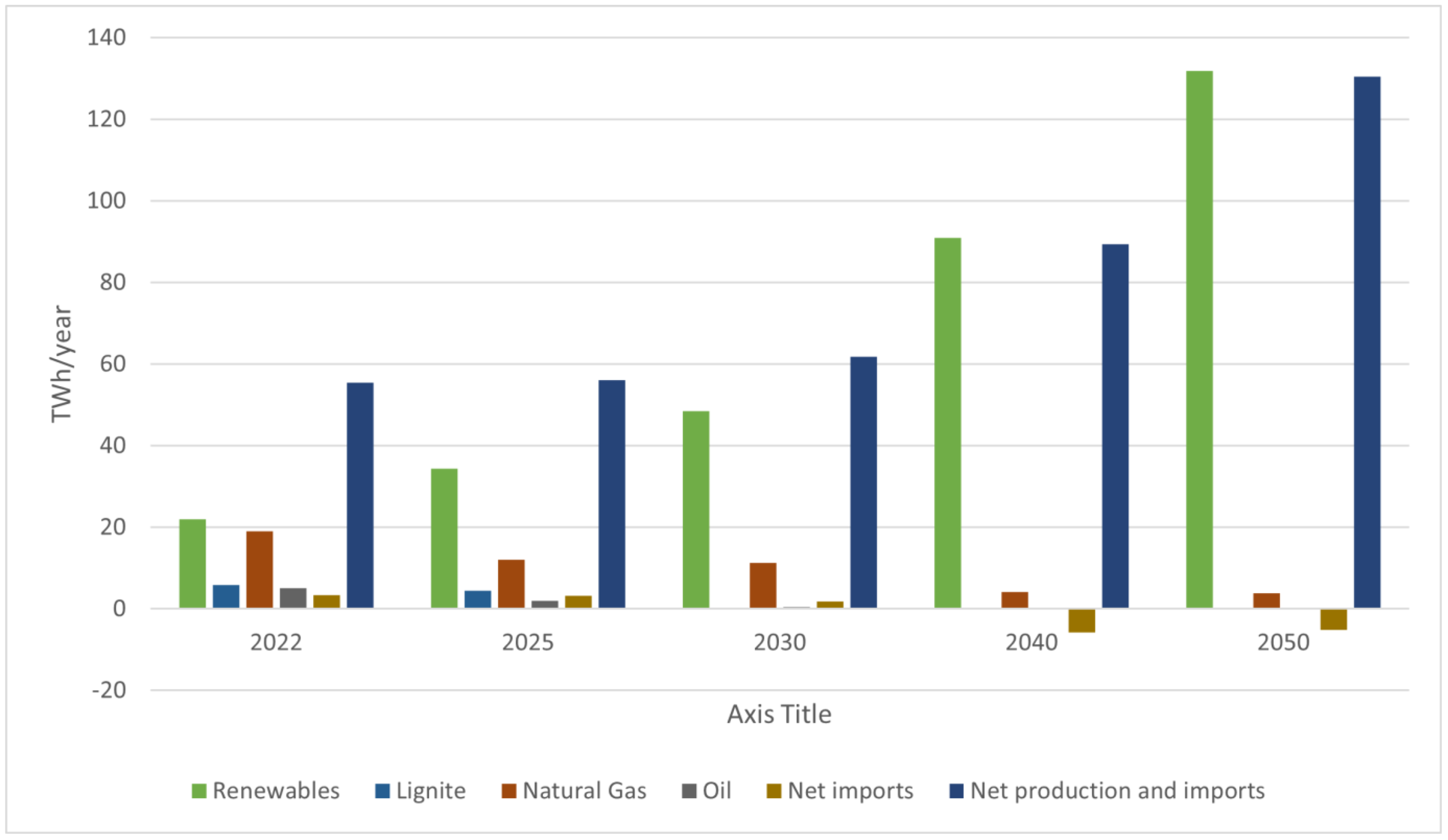

4.1. What Greece Has Achieved Until Now Regarding Its Green Transition

- Great freedom of movement of producers;

- Strong central control from the European Commission and the delays in the adoption of corrective changes;

- The blind trust in the competitive functioning and self-regulation of the market and the absence of control mechanisms.

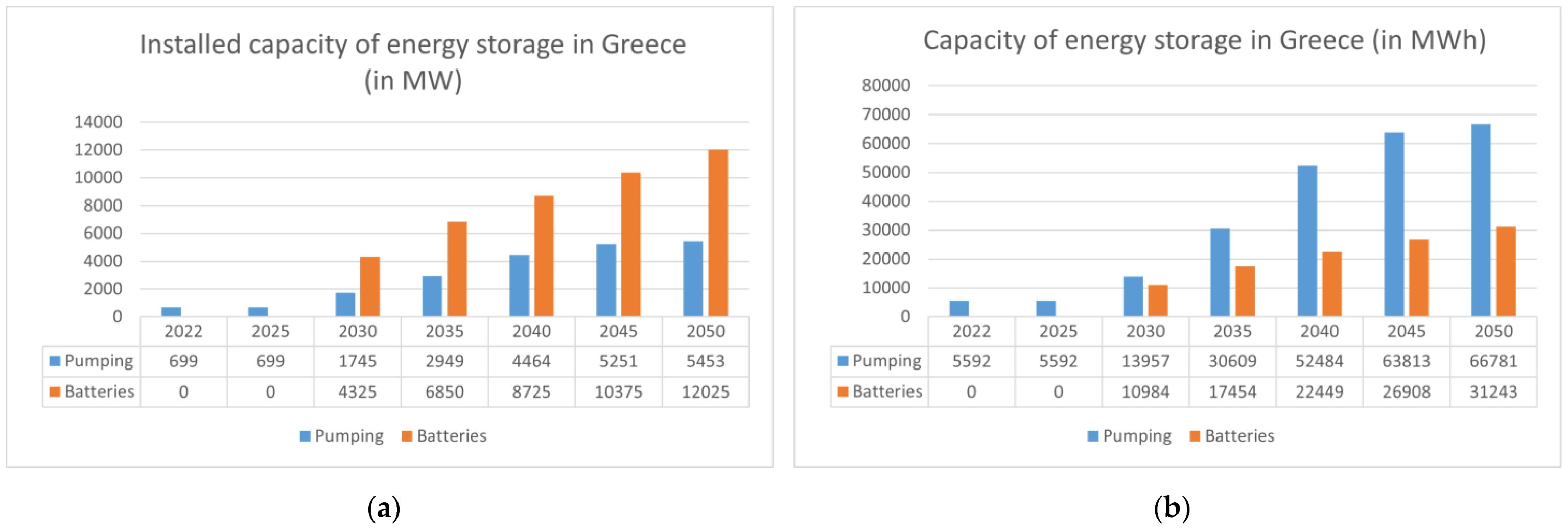

4.2. The Future of the Energy Transition in Greece: Risks, Challenges and Opportunities

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

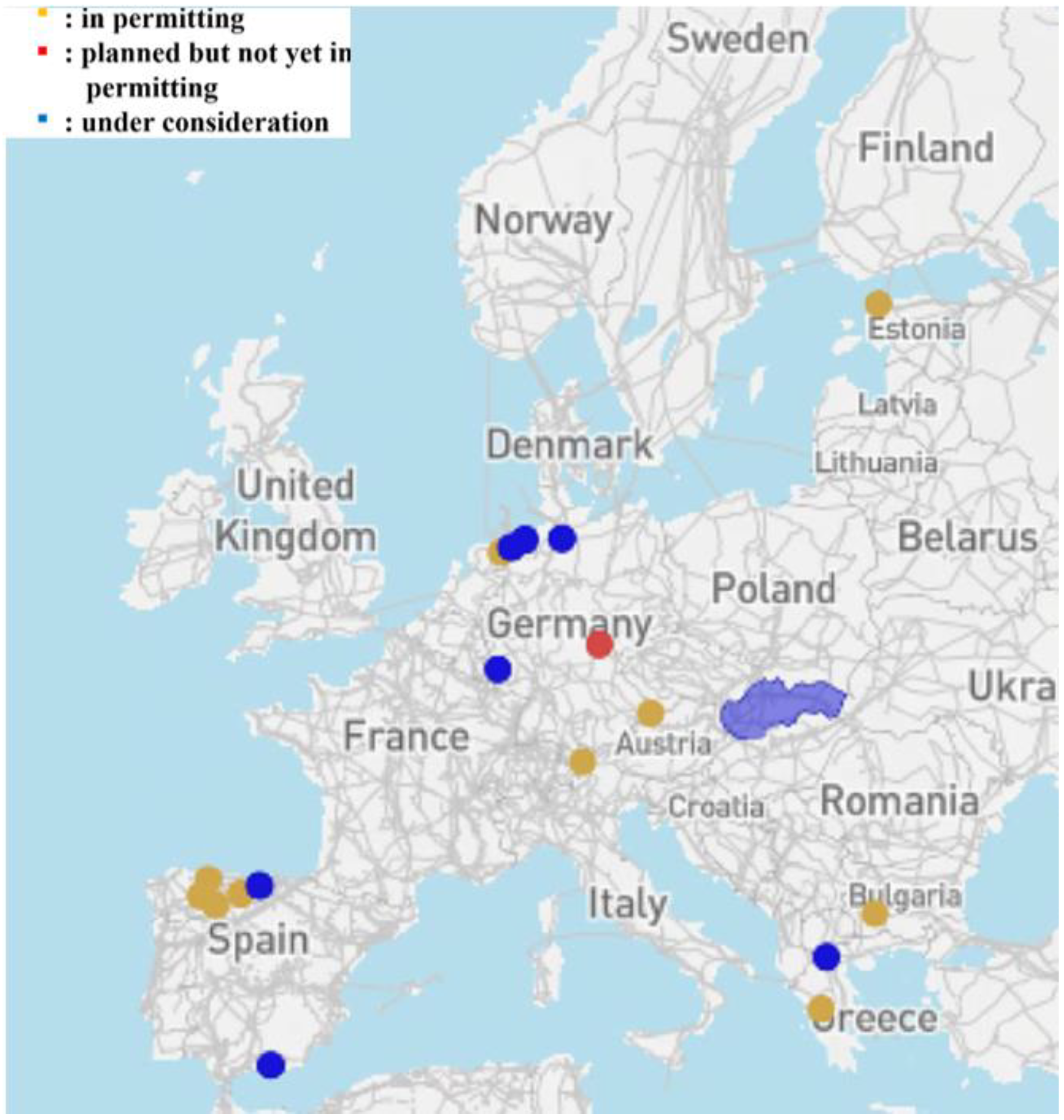

| Name of the Project | Interconnected Countries | Capacity [GW] | Budget (in EUR) | Estimated Completion Year | Included in the TYNDP of ENTSO-E |

|---|---|---|---|---|---|

| EuroAsia Interconnector [64] | Greece (Crete)–Cyprus–Israel | 1 | 3.5 billion | 2026 (Greece–Cyprus) 2028 (Cyprus–Israel) | Yes |

| GREGY interconnector [65] | Greece–Egypt | 3 | 4.2 billion | 2030 | Yes |

| Green Aegean Interconnection [66] | Greece–Austria–Slovenia | 3 | 8.1 billion | 2035 | Yes |

| Saudi Greek Interconnection [67] | Saudi Arabia–Greece | Not defined yet | Not defined yet | Not defined yet | No |

5. PESTEL Analysis for the Energy Sector in Greece for the Energy Transition

5.1. Introduction to PESTEL Analysis—Methodology

- (a)

- Possible opportunity for low impact;

- (b)

- Possible opportunity for medium impact;

- (c)

- Possible opportunity for high impact;

- (d)

- Possible opportunity with low urgency;

- (e)

- Possible opportunity with medium urgency;

- (f)

- Possible opportunity with high urgency.

5.2. PESTEL Analysis Results for the Greek Case Study

6. Conclusions

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Conflicts of Interest

References

- Potrc, S.; Cucek, L.; Martin, M.; Kravanja, Z. Sustainable renewable energy supply networks optimization—The gradual transition to a renewable energy system within the European Union by 2050. Renew. Sustain. Energy Rev. 2021, 146, 111186. [Google Scholar] [CrossRef]

- IPCC. Global Warming of 1.5 °C: An IPCC Special Report on the Impacts of global Warming of 1.5 °C Above Pre-Industrial Levels and Related Global Greenhouse Gas Emission Pathways, in the Context of Strengthening the Global Response to the Threat of Climate Change, Sustainable Development, and Efforts to Eradicate Poverty; Cambridge University Press: Cambridge, UK, 2018. [Google Scholar] [CrossRef]

- Dooley, K.; Kartha, S. Land-based negative emissions: Risks for climate mitigation and impacts on sustainable development. Int. Environ. Agreem. 2018, 18, 79–98. [Google Scholar] [CrossRef]

- Hassan, Q.; Algburi, S.; Sameen, A.Z.; Al-Musawi, T.J.; Al-Jiboory, A.K.; Salman, H.M.; Ali, B.M.; Jaszczur, M. A comprehensive review of international renewable energy growth. Energy Built Environ. 2024. [Google Scholar] [CrossRef]

- Skovgaard, J.; van Asselt, H. The politics of fossil fuel subsidies and their reform: Implications for climate change mitigation. Wiley Interdiscip. Rev. Clim. Change 2019, 10, e581. [Google Scholar] [CrossRef]

- IRENA. Renewable Capacity Statistics. 2023. Available online: https://www.irena.org/-/media/Files/IRENA/Agency/Publication/2024/Mar/IRENA_RE_Capacity_Statistics_2024.pdf (accessed on 13 April 2025).

- IRENA. World Energy Transitions Outlook 2023: 1.5°C Pathway. Available online: https://www.irena.org/-/media/Files/IRENA/Agency/Publication/2023/Jun/IRENA_World_energy_transitions_outlook_2023.pdf?rev=db3ca01ecb4a4ef8accb31d017934e97 (accessed on 20 April 2025).

- Palade, D.; Ioanid, A. Achieving Renewable Energy Targets in the Context of the RepowerEU Plan. Int. Conf. Manag. Ind. Eng. 2023, 11, 361–368. [Google Scholar] [CrossRef]

- European Commission. ‘Fit for 55’: Delivering the EU’s 2030 Climate Target on the Way to Climate Neutrality; Communication from the Commission to the European Parliament, the Council, the European Economic and Social Committee and the Committee of the Regions, COM (2021) 550 Final; European Commission: Brussels, Belgium, 2021. [Google Scholar]

- Manowska, A.; Bluszcz, A.; Chomiak-Orsa, I.; Wowra, R. Towards Energy Transformation: A Case Study of EU Countries. Energies 2024, 17, 1778. [Google Scholar] [CrossRef]

- European Commission: Commission Sets out Actions to Accelerate the Roll-Out of Electricity Grids. Available online: https://ec.europa.eu/commission/presscorner/detail/en/ip_23_6044 (accessed on 13 April 2025).

- Highlights—Future of our Grids: Accelerating Europe’s Energy Transition. Available online: https://www.entsoe.eu/eugridforum/ (accessed on 3 April 2025).

- Göke, L.; Weibezahn, J.; Kendziorski, M. How flexible electrification can integrate fluctuating renewables. Energy 2023, 278 Pt A, 127832. [Google Scholar] [CrossRef]

- Li, Q.; Qin, Z.; Zhang, L.; Yang, Y.; Deng, J.; Guo, J. Multi-objective optimization scheduling and flexibility margin study in integrated energy systems based on different strategies. J. Clean. Prod. 2024, 449, 141698. [Google Scholar] [CrossRef]

- Dash, S.; Chakravarty, S.; Giri, N.C.; Ghugar, U.; Fotis, G. Performance Assessment of Different Sustainable Energy Systems Using Multiple-Criteria Decision-Making Model and Self-Organizing Maps. Technologies 2024, 12, 42. [Google Scholar] [CrossRef]

- Koeva, D.; Kutkarska, R.; Zinoviev, V. High Penetration of Renewable Energy Sources and Power Market Formation for Countries in Energy Transition: Assessment via Price Analysis and Energy Forecasting. Energies 2023, 16, 7788. [Google Scholar] [CrossRef]

- Impram, S.; Nese, S.V.; Oral, B. Challenges of renewable energy penetration on power system flexibility: A survey. Energy Strategy Rev. 2020, 31, 100539. [Google Scholar] [CrossRef]

- Akrami, A.; Doostizadeh, M.; Aminafar, F. Power system flexibility: An overview of emergence to evolution. J. Mod. Power Syst. Clean Energy 2019, 7, 987–1007. [Google Scholar] [CrossRef]

- Alotaiq, A. Strategies to Achieving Deep Decarbonization in Power Generation: A Review. J. Econ. Technol. 2024, 3, 22–33. [Google Scholar] [CrossRef]

- IEA World Energy Outlook 2022. Available online: https://www.iea.org/reports/world-energy-outlook-2022 (accessed on 2 May 2025).

- Fotis, G.; Vita, V.; Maris, T.I. Risks in the European Transmission System and a Novel Restoration Strategy for a Power System after a Major Blackout. Appl. Sci. 2023, 13, 83. [Google Scholar] [CrossRef]

- Fotis, G.; Pavlatos, C.; Vita, V. Power system control centers and their role in the restoration process after a major blackout. WSEAS Trans. Power Syst. 2023, 18, 57–70. [Google Scholar] [CrossRef]

- Zafeiropoulou, M.; Sijakovic, N.; Zarkovic, M.; Ristic, V.; Terzic, A.; Makrygiorgou, D.; Zoulias, E.; Vita, V.; Maris, T.I.; Fotis, G. Development and Implementation of a Flexibility Platform for Active System Management at Both Transmission and Distribution Level in Greece. Appl. Sci. 2023, 13, 11248. [Google Scholar] [CrossRef]

- Zafeiropoulou, M.; Sijakovic, N.; Zarkovic, M.; Ristic, V.; Terzic, A.; Makrygiorgou, D.; Zoulias, E.; Vita, V.; Maris, T.I.; Fotis, G. A Flexibility Platform for Managing Outages and Ensuring the Power System’s Resilience during Extreme Weather Conditions. Processes 2023, 11, 3432. [Google Scholar] [CrossRef]

- Fotis, G.; Sijakovic, N.; Zarkovic, M.; Ristic, V.; Terzic, A.; Vita, V.; Zafeiropoulou, M.; Zoulias, E.; Maris, T.I. Forecasting Wind and Solar Energy Production in the Greek Power System using ANN Models. WSEAS Trans. Power Syst. 2023, 18, 373–391. [Google Scholar] [CrossRef]

- A European-Wide Vision for the Future of Our Power Network Energy Poverty in the EU. Available online: https://tyndp.entsoe.eu/explore (accessed on 13 May 2025).

- Bertsiou, M.M.; Baltas, E. Management of energy and water resources by minimizing the rejected renewable energy. Sustain. Energy Technol. Assess. 2022, 52 Pt A, 102002. [Google Scholar] [CrossRef]

- Gómez-Calvet, R.; Martínez-Duart, J.M.; Gómez-Calvet, A.R. The 2030 power sector transition in Spain: Too little storage for so many planned solar photovoltaics? Renew. Sustain. Energy Rev. 2023, 174, 113094. [Google Scholar] [CrossRef]

- Kashour, M.; Jaber, M.M. Revisiting energy poverty measurement for the European Union. Energy Res. Soc. Sci. 2024, 109, 103420. [Google Scholar] [CrossRef]

- Energy Poverty in the EU. Available online: https://www.europarl.europa.eu/RegData/etudes/BRIE/2022/733583/EPRS_BRI(2022)733583_EN.pdf (accessed on 3 May 2025).

- Kluskens, N.; Alkemade, F.; Höffken, J. Beyond a checklist for acceptance: Understanding the dynamic process of community acceptance. Sustain. Sci. 2024, 19, 831–846. [Google Scholar] [CrossRef]

- IPTO ISP Results. Available online: https://www.admie.gr/en/data-type/isp-results (accessed on 3 May 2025).

- Commission Regulation (EU) 2017/1485 (System Operational Guideline—SOGL). Available online: https://eur-lex.europa.eu/legal-content/EN/TXT/?uri=uriserv:OJ.L_.2017.220.01.0001.01.ENG&toc=OJ:L:2017:220:TOC (accessed on 13 May 2025).

- Regulation (EU) 2015/1222 Establishing a Guideline on Capacity Allocation and Congestion Management; European Union: Brussels, Belgium, 2015.

- European Union. Commission Regulation (EU) 2016/1388 of 17 August 2016 Establishing a Network Code on Demand Connection. Available online: https://eur-lex.europa.eu/legal-content/EN/TXT/?uri=uriserv%3AOJ.L_.2016.223.01.0010.01.ENG (accessed on 13 May 2025).

- European Union. Commission Regulation (EU) 2017/2195 Establishing a Guideline on Electricity Balancing; OJ L 312, 28.11.2017; European Union: Brussels, Belgium, 2017; pp. 6–53. Available online: https://eur-lex.europa.eu/legal-content/EN/TXT/PDF/?uri=CELEX:32017R2195&from=EN (accessed on 9 May 2025).

- ENTSO-E Summarizes the Key Actions Taken Against Long Lasting Frequency Deviations in Continental Europe. Available online: https://www.entsoe.eu/news/2021/04/27/entso-e-summarises-the-key-actions-taken-against-long-lasting-frequency-deviations-in-continental-europe/ (accessed on 3 May 2025).

- ENTSO-E Final Report on the Local Power Grid Incident in Rogowiec (Poland) Substation on 17 May 2021. Available online: https://www.entsoe.eu/news/2022/03/18/final-report-on-the-local-power-grid-incident-in-rogowiec-poland-substation-on-17-may-2021/ (accessed on 3 May 2025).

- Karapidakis, E.; Nikologiannis, M.; Mozakis, I.; Katsigiannis, Y.; Iliadis, I. Optimal Mitigation of Renewable Energy Curtailment in Greece through Energy Storage. In Proceedings of the 2024 5th International Conference on Communications, Information, Electronic and Energy Systems (CIEES), Veliko Tarnovo, Bulgaria, 20–22 November 2024; pp. 1–6. [Google Scholar] [CrossRef]

- European Union Clean Energy for All Europeans Package. Available online: https://energy.ec.europa.eu/topics/energy-strategy/clean-energy-all-europeans-package_en (accessed on 3 May 2025).

- Study on Energy Storage: Contribution to the Security of the Electricity Supply in Europe. Available online: https://op.europa.eu/en/publication-detail/-/publication/a6eba083-932e-11ea-aac4-01aa75ed71a1/language-en?WT.mc_id=Searchresult&WT.ria_c=37085&WT.ria_f=3608&WT.ria_ev=search (accessed on 3 May 2025).

- EASE. Energy Storage Targets 2030 and 2050—Ensuring Europe’s Energy Security in a Renewable Energy System. 2022. Available online: https://ease-storage.eu/wp-content/uploads/2022/06/Energy-Storage-Targets-2030-and-2050-Full-Report.pdf (accessed on 3 May 2025).

- High-Level Report TYNDP 2022 Final Version. May 2022. Available online: https://eepublicdownloads.blob.core.windows.net/public-cdn-container/tyndp-documents/TYNDP2022/public/high-level-report.pdf (accessed on 3 May 2025).

- IRENA: Global Energy Transformation. Available online: https://www.irena.org/-/media/Files/IRENA/Agency/Publication/2018/Apr/IRENA_Report_GET_2018.pdf (accessed on 3 May 2025).

- CNESA. Global Energy Storage Market Analysis 2020.Q1. 2020. Available online: https://en.cnesa.org/latest-news/2020/5/28/cnesa-global-energy-storage-market-analysis-2020q1-summary (accessed on 10 April 2024).

- Pumped Energy Storage: Vital to California’s Renewable Energy Future. Available online: https://www.sdcwa.org/sites/default/files/White%20Paper%20-%20Pumped%20Energy%20Storage%20V.16.pdf (accessed on 4 May 2025).

- Global Energy Perspective 2023. Available online: https://www.mckinsey.com/industries/oil-and-gas/our-insights/global-energy-perspective-2023 (accessed on 4 May 2025).

- ENTSO-E TYNDP 2020 Completing the Map Power System Needs in 2030 and 2040. Available online: https://eepublicdownloads.entsoe.eu/tyndp-documents/IoSN2020/200810_IoSN2020mainreport_beforeconsultation.pdf (accessed on 2 May 2025).

- Kuzemko, C.; Blondeel, M.; Dupont, C.; Brisbois, M.C. Russia’s war on Ukraine, European energy policy responses & implications for sustainable transformations. Energy Res. Soc. Sci. 2022, 93, 102842. [Google Scholar] [CrossRef]

- Yang, Y.; Xia, S.; Huang, P.; Qian, J. Energy transition: Connotations, mechanisms and effects. Energy Strategy Rev. 2024, 52, 101320. [Google Scholar] [CrossRef]

- Igliński, B.; Kiełkowska, U.; Mazurek, K.; Drużyński, S.; Pietrzak, M.B.; Kumar, G.; Veeramuthu, A.; Skrzatek, M.; Zinecker, M.; Piechota, G. Renewable energy transition in Europe in the context of renewable energy transition processes in the world. A review. Heliyon 2024, 10, e40997. [Google Scholar] [CrossRef]

- Gerlich, M. Brace for Impact: Facing the AI Revolution and Geopolitical Shifts in a Future Societal Scenario for 2025–2040. Societies 2024, 14, 180. [Google Scholar] [CrossRef]

- Ariadne Interconnection (Official Site). Available online: https://www.ariadne-interconnection.gr/en (accessed on 3 May 2025).

- Great Sea Interconnector. Available online: https://www.great-sea-interconnector.com/ (accessed on 3 May 2025).

- Keay, M. The EU “Target Model” for electricity markets: Fit for purpose? Oxford Energy Comment. 2013. Available online: https://www.oxfordenergy.org/publications/the-eu-target-model-for-electricity-markets-fit-for-purpose/ (accessed on 15 February 2022).

- Mini Monthly Report of the Special Account for RES, Heating and Storage. Available online: http://www.dapeep.gr/wp-content/uploads/2024/02/09_DEC_2023_min_DELTIO_ELAPE_v_1.0_06.02.2024.pdf (accessed on 10 May 2025).

- Greece’s National Energy and Climate Plan: Climate law (4936/2022 FEK 105 / A / 27-5 -2022). Available online: https://ypen.gov.gr/wp-content/uploads/2025/04/%CE%91%CE%BD%CE%B1%CE%B8%CE%B5%CF%89%CF%81%CE%B7%CE%BC%CE%AD%CE%BD%CE%BF-%CE%95%CE%A3%CE%95%CE%9A-2024-%CE%A6%CE%95%CE%9A-6983.pdf (accessed on 3 May 2025).

- IPTO Ten-year Network Development Plan. Available online: https://www.admie.gr/en/grid/development/ten-year-development-plan (accessed on 3 May 2025).

- IPTO Monthly Energy Report (December 2023). Available online: https://www.admie.gr/sites/default/files/attached-files/type-file/2024/02/Energy_Report_202312_v2_gr_0.pdf (accessed on 3 May 2025).

- Karystianos, M.E.; Pitas, C.N.; Efstathiou, S.P.; Tsili, M.A.; Mantzaris, J.C.; Leonidaki, E.A.; Voumvoulakis, E.M.; Sakellaridis, N.G. Planning of Aegean Archipelago Interconnections to the Continental Power System of Greece. Energies 2021, 14, 3818. [Google Scholar] [CrossRef]

- Yu, K.; van Son, P. Review of trans-Mediterranean power grid interconnection: A regional roadmap towards energy sector decarbonization. Glob. Energy Interconnect. 2023, 6, 115–126. [Google Scholar] [CrossRef]

- Sotiriou, S.A. Connecting security with sustainable development in the Eastern Mediterranean and generating pay-offs for the European Union. Mediterr. Politics 2023, 30, 208–217. [Google Scholar] [CrossRef]

- Moretti, A.; Pitas, C.; Christofi, G.; Bué, E.; Francescato, M.G. Grid Integration as a Strategy of Med-TSO in the Mediterranean Area in the Framework of Climate Change and Energy Transition. Energies 2020, 13, 5307. [Google Scholar] [CrossRef]

- TR 219—Great Sea Interconnector. Available online: https://tyndp2024.entsoe.eu/projects-map/transmission/219 (accessed on 3 May 2025).

- TR 1041—GREGY Green Energy Interconnector. Available online: https://tyndp2024.entsoe.eu/projects-map/transmission/1041 (accessed on 7 May 2025).

- TR 1231—Green Aegean Interconnector. Available online: https://tyndp2024.entsoe.eu/projects-map/transmission/1231 (accessed on 7 May 2025).

- IPTO Press Center “Saudi Greek Interconnection” Established by IPTO and National Grid. Available online: https://www.admie.gr/en/kentro-typoy/press-releases/saudi-greek-interconnection-established-ipto-and-national-grid (accessed on 7 May 2025).

- Fahey, L.; Narayanan, V.K. Macroenvironmental Analysis for Strategic Management; West Publishing: Eagan, MN, USA, 1986. [Google Scholar]

- Gibbs, D.; Deutz, P. Reflections on Implementing Industrial Ecology through Eco-Industrial Park Development. J. Clean. Prod. 2007, 15, 1683–1695. [Google Scholar] [CrossRef]

- Trapp, J.H.; Kerber, H.; Schramm, E. Implementation and diffusion of innovative water infrastructures: Obstacles, stakeholder networks and strategic opportunities for utilities. Environ. Earth Sci. 2017, 76, 15. [Google Scholar] [CrossRef]

- Hopkins, K.G.; Grimm, N.B.; York, A.M. Influence of governance structure on green stormwater infrastructure investment. Environ. Sci. Pol. 2018, 84, 124–133. [Google Scholar] [CrossRef]

| Energy Storage Technology | Power Capacity (GW) | |||

|---|---|---|---|---|

| 2021 | 2030 | 2050 | ||

| Power to X to Power | Vehicle to Grid (V2G) | - | 57 | 120 |

| Batteries | 7 | 57 | 50 | |

| Pumped Hydro Storage (PHS) | 40 | 53 | 65 | |

| Novel gravity storage, compressed air energy storage (CAES), liquid energy storage (LAES), thermal energy storage, electrochemical and chemical energy storage | - | 55 | 200 | |

| Power to X | P2X technologies | - | 22 | 165 |

| Total | 47 | 187 | 600 | |

| Number of Participants | Professional Specialization | Academic Degree | Years of Experience |

|---|---|---|---|

| 35 | Associate Professor or Full Professor | PhD in Electrical Engineering | 20–25 |

| 25 | Associate Professor or Full Professor | PhD in Mechanical Engineering | 20–25 |

| 18 | Associate Professor | PhD in Project Management | 18–28 |

| 14 | Full Professor | PhD in Economics | 27–32 |

| 18 | Associate Professor or Full Professor | PhD in Environmental Engineering | 20–30 |

| PESTEL Category |  | ||||

|---|---|---|---|---|---|

| Factors | Analysis | Type (Opportunity/Threat) | Impact (High/Medium/Low) | Urgency (High/Medium/Low) | |

| P1 | Infrastructure | RES share is expected to rise by 2050. | O | H | H |

| P2 | Moderate raw energy material reserves (oil, lignite). | O | M | L | |

| P3 | Trade/Tariffs | Energy security is dependent on foreign supplies, primarily gas. In a few years, lignite as a source will be totally phased out. | T | H | H |

| P4 | Low competition with neighboring countries as RES exporters. | T | H | H | |

| P5 | Policy | The scientific and research domain, including RES, benefits from the stability of the economic system. | O | L | M |

| P6 | Political structure | Regular changes to the central government. | T | H | H |

| P7 | Ineffective public administration. | T | H | H | |

| P8 | Regulation | Frequent modifications to the law. | T | H | H |

| P9 | Fiscal policy | Lack of a clear plan for attracting investors. | T | M | H |

| P10 | Defense/Wars | High geopolitical risk between Greece and Turkey may cause the planned HVDC interconnections with Saudi Arabia, Cyprus, and Israel to be delayed or even canceled. | T | H | H |

| P11 | Protectionism | Location on transmission routes is dependent on local societies and local administration, lengthening project delivery times. | T | M | M |

| PESTEL Category |  | ||||

|---|---|---|---|---|---|

| Factors | Analysis | Type (Opportunity/Threat) | Impact (High/Medium/Low) | Urgency (High/Medium/Low) | |

| E1 | Monetary Policy | The scientific and research domain, including RES, benefits from the stability of the economic system. | O | M | M |

| E2 | GDP Growth | Greece’s economic situation could abruptly alter because of a possible global economic crisis. | T | H | H |

| E12 | The Greek economy may enter a recession if the high cost HVDC are delayed or canceled for geopolitical reasons (such as with Turkey). | T | H | M | |

| E3 | Financial Markets | Greece is highly dependent on the economies of other counties for its imports. | T | H | H |

| E4 | Inflation | Electricity prices are rising, particularly after RES has become widely used. | T | H | H |

| E13 | High cost of electric cars. | T | H | M | |

| E5 | Investment | RES installation costs are still not very competitive, despite significantly lower operating costs. | T | M | M |

| E6 | Financing Accessibility | Aid funds for RES investments (grants, loans) are moderately available. | T | M | L |

| E7 | Business Cycles | Curtailment in RES production creates an investing environment of high uncertainty. | T | H | H |

| E8 | Unemployment | Significant employment in the lignite sector—abandonment of which will lead to mine closures and higher unemployment. | T | H | H |

| E11 | Favorable conditions for RES development in the most unemployed areas. | O | M | M | |

| E12 | While the growth of RESs will generate new jobs, it will also result in mine closures and job losses. | T | H | H | |

| E13 | Investment | Low investment rates in energy storage technologies. | T | H | H |

| E14 | Pressure to increase budget revenues. | T | M | M | |

| PESTEL Category |  | ||||

|---|---|---|---|---|---|

| Factors | Analysis | Type (Opportunity/Threat) | Impact (High/Medium/Low) | Urgency (High/Medium/Low) | |

| S1 | Population Growth | The Greek population’s fall has resulted in an unfavorable demographic position that limits their flexibility in responding to changes in the labor market and economy. | T | H | H |

| S2 | Education | Insufficient knowledge about RESs. There is a shortage of skilled workers for positions in numerous energy-related projects (such as energy storage projects and HVDC interconnections). | T | H | H |

| S3 | Cultural Dynamics | International organizations and local governments are not doing anything to increase public awareness of RES in Greece. | T | M | M |

| S5 | Behaviors | Although society views RESs as environmentally favorable, the phenomenon known as “NIMBY syndrome” (Not In My Back Yard) can occasionally be seen. | T | M | M |

| S6 | Attitudes | A widespread concern about rising energy costs because of more electricity coming from RESs. | T | H | H |

| S7 | Cultural Dynamics | A powerful political movement that publicly opposes the growth of RES in Greece is impeding its progress, particularly in the local municipalities. | T | H | H |

| S8 | The variety of communication channels helps to educate the public and advance RES. | O | H | H | |

| S9 | The potential for property owners to possess a RES. This method of obtaining energy (solar, wind, hydro energy) is essentially free. | O | H | M | |

| PESTEL Category |  | ||||

|---|---|---|---|---|---|

| Factors | Analysis | Type (Opportunity/Threat) | Impact (High/Medium/Low) | Urgency (High/Medium/Low) | |

| T1 | Infrastructure | Electricity transmission networks need to be modernized due to their aging and be further developed due to the goals of the energy transition. | T | H | H |

| T2 | The country’s energy security is seriously threatened by technical flaws and a lack of energy storage infrastructure. | T | H | H | |

| T3 | The establishment of a distributed energy market based on RES can contribute to energy stability by granting access to energy near RES installations. | O | H | H | |

| T11 | Insufficient infrastructure in the distribution system for the adoptation of electric mobility. | O | H | H | |

| T4 | Mobility | Most of the economy, including the private sector, depends on the central government, and strategic companies are unprepared for energy concerns. | T | H | H |

| T5 | Digitization | The systems for producing and supplying electricity are not well integrated. | T | M | M |

| T6 | Innovation | Utilizing RES to reduce emissions and achieve climate goals. | O | M | M |

| T7 | Relying mostly on non-waste RES (such as solar, wind, and water); and employing biomass to a limited degree. | O | L | L | |

| T10 | High-skilled jobs will be created by new HVDC connections with neighboring nations (such as the Aegean interconnection). | O | H | H | |

| S9 | Development of RES-focused university curricula. | O | M | M | |

| P4 | The growth of RES is made possible by Greece’s membership in the EU and involvement in European research areas (e.g., joint research programs, participation in research centers, etc.). | O | M | L | |

| PESTEL Category |  | ||||

|---|---|---|---|---|---|

| Factors | Analysis | Type (Opportunity/Threat) | Impact (High/Medium/Low) | Urgency (High/Medium/Low) | |

| E1 | Climate change | Utilizing RES to reduce emissions and meet climate goals | O | H | H |

| E2 | Pollution | Reducing the use of gas and oil throughout the chain—RESs reduce the use of transport fuels (reduced deterioration of roads, vehicles, etc.) because it does not require the transportation of fuels for energy production. | O | H | M |

| E3 | Diversifying the energy mix from oil and gas into sources that are healthier for humans and the environment. | O | M | M | |

| E4 | Natural resources | Reductions in fossil fuel exploitation, which results in the preservation of resources for future generations | O | M | M |

| E5 | Power units using conventional fuels will be phased out gradually. | T | H | H | |

| E6 | Sustainability | Reducing the amount of habitat and land loss caused by raw material extraction | T | H | H |

| E7 | Ecological Attitudes | Because RES plant manufacturers have a market, it is frequently essential to import parts or entire equipment, which increases the danger of importing outdated applicable technologies. | T | M | L |

| E8 | Port customs and shipbuilding, and as a result, adequate infrastructure for offshore wind farms | O | H | H | |

| E9 | Concerns on how RES installations may affect nearby ecosystems and residents (such as the effects of wind turbines on birds, animal migration, and noise emissions | T | H | H | |

| PESTEL Category |  | ||||

|---|---|---|---|---|---|

| Factors | Analysis | Type (Opportunity/Threat) | Impact (High/Medium/Low) | Urgency (High/Medium/Low) | |

| L1 | European Law | The signed climate aggreement resulted in a commitment to reduce GHGs and increase the share of RESs. | O | H | M |

| L2 | Risk | Nevertheless, unstable policies and frequent changes to legal restrictions raise doubts about whether the expected targets would be met. | T | H | H |

| L3 | Legal System | The government’s inability to fulfill its international commitments due to impractical national legislation; the difficulty in acquiring licenses. | T | H | H |

| L4 | The primary dangers to the field of science and research in RESs are overly complex laws and ineffective practical application of political goals. | T | M | L | |

| L5 | European Law | The creation of a new energy policy that takes into consideration the advancement of RESs and nuclear. | O | H | H |

| L6 | Investor Protection | Potential investors are deterred by the frequent changes to legal regulations, such as the RES Act. | T | H | H |

| L7 | The legal framework for the curtailment of the RES production is not well defined. | T | H | H | |

| L8 | The establishment of an auction system that enables the support of new RES installations. | O | M | L | |

| L9 | Liability | The system of support for RES development is inadequate and does not match recipient groups optimally. | T | M | M |

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2025 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Fotis, G.; Maris, T.I.; Mladenov, V. Risks, Obstacles and Challenges of the Electrical Energy Transition in Europe: Greece as a Case Study. Sustainability 2025, 17, 5325. https://doi.org/10.3390/su17125325

Fotis G, Maris TI, Mladenov V. Risks, Obstacles and Challenges of the Electrical Energy Transition in Europe: Greece as a Case Study. Sustainability. 2025; 17(12):5325. https://doi.org/10.3390/su17125325

Chicago/Turabian StyleFotis, Georgios, Theodoros I. Maris, and Valeri Mladenov. 2025. "Risks, Obstacles and Challenges of the Electrical Energy Transition in Europe: Greece as a Case Study" Sustainability 17, no. 12: 5325. https://doi.org/10.3390/su17125325

APA StyleFotis, G., Maris, T. I., & Mladenov, V. (2025). Risks, Obstacles and Challenges of the Electrical Energy Transition in Europe: Greece as a Case Study. Sustainability, 17(12), 5325. https://doi.org/10.3390/su17125325