Does the Carbon Emission Trading Pilot Policy Enhance Carbon Reduction Efficiency?

Abstract

1. Introduction

2. Literature Review

3. Theoretical Analysis and Research Hypothesis

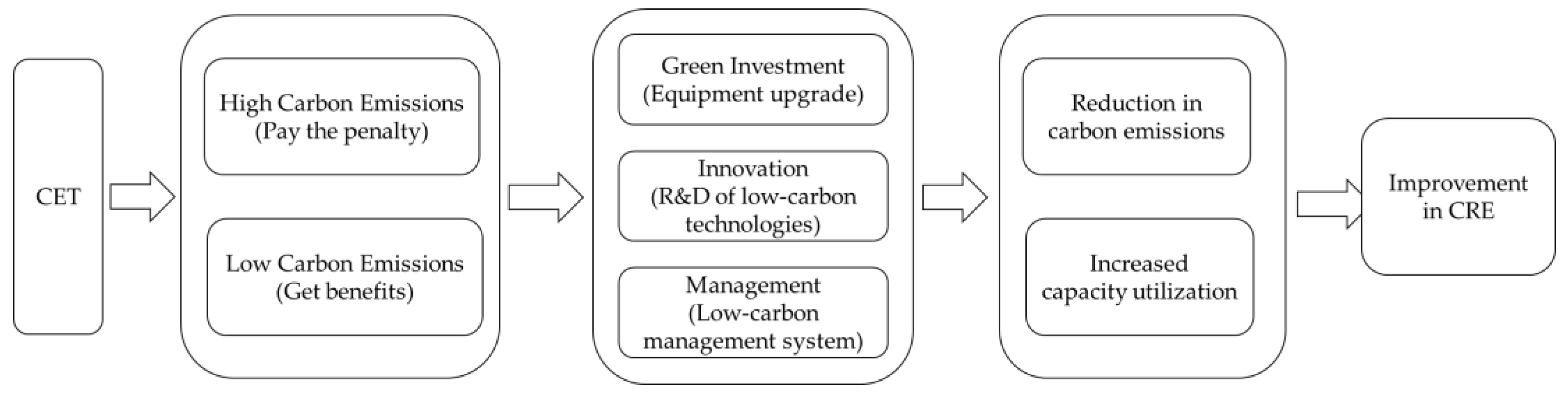

3.1. Impact of Carbon Trading Pilots on CRE

3.2. Mechanisms of CET Pilots to Promote the CRE of Enterprises

4. Empirical Strategy and Data Sources

4.1. Impact of Carbon Trading Pilots on CRE

4.1.1. Data Source

- Excluding enterprises with “ST” and “*ST” in their stock abbreviations, which may face specific financial difficulties and accounting treatment problems;

- Excluding enterprises with a large number of missing financial values;

- Excluding outliers, including missing values and unreasonable values, and shrinking all continuous variables at the 1% level.

4.1.2. The Impact of CET on the CRE of Enterprises

4.1.3. The Impact of CET on Corporate CEs and CU

4.2. Variable Declarations

4.2.1. Dependent Variable and Explained Variable

4.2.2. Control Variables

5. Analysis of Empirical Results

5.1. The Impact of CET on the CRE of Enterprises

5.2. The Impact of CET on CEs and CU

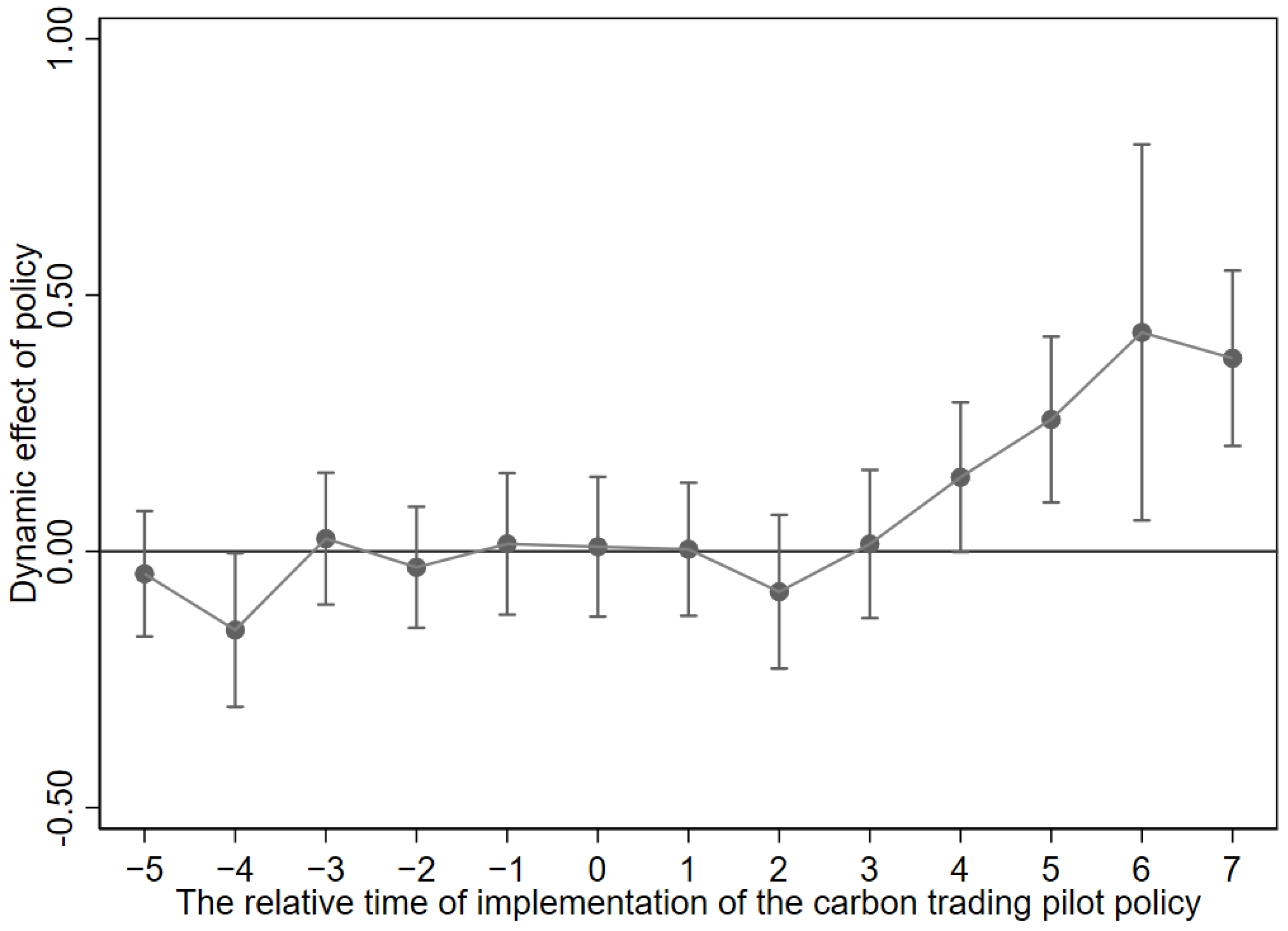

5.3. Parallel Trends Test

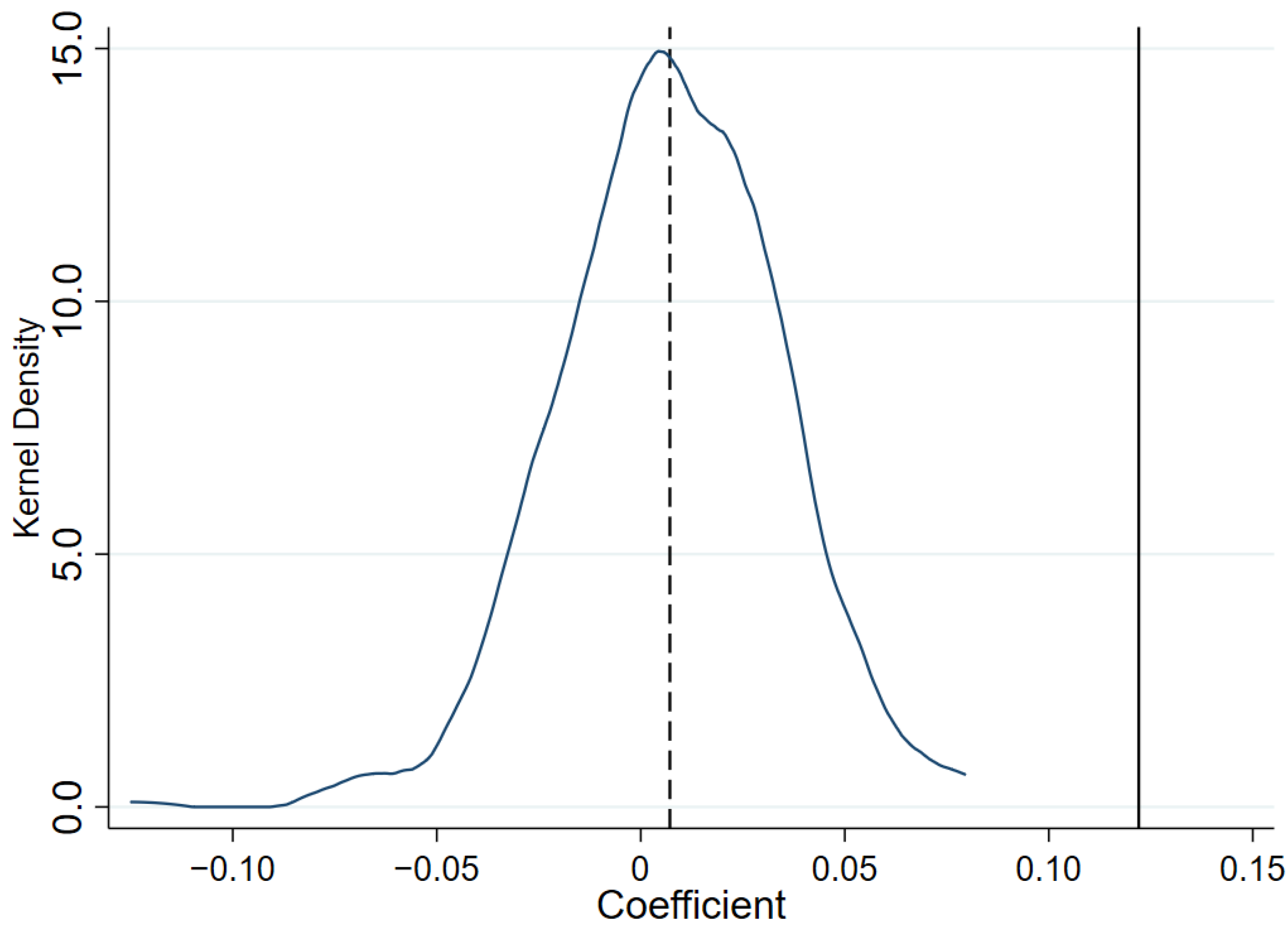

5.4. Placebo Test

5.5. Robustness Test

5.5.1. Alternative CU Metrics

5.5.2. Alternative CE Measurement

5.5.3. Propensity Score Matching Difference-in-Differences

5.5.4. Exclusion of Other Policy Interferences

5.6. Mechanism Test

5.6.1. Green Investment

5.6.2. Innovation Performance

5.6.3. Management Capability

6. Heterogeneity Test

7. Conclusions and Policy Implications

7.1. Conclusions

7.2. Policy Implications

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Acknowledgments

Conflicts of Interest

Abbreviations

| DID | Difference-in-differences |

| CRE | Carbon reduction efficiency |

| CU | Capacity utilization |

| CEs | Carbon emissions |

| CET | Carbon emission trading |

References

- Tang, E.; Peng, C.; Xu, Y. Changes of energy consumption with economic development when an economy becomes more productive. J. Clean. Prod. 2018, 196, 788–795. [Google Scholar] [CrossRef]

- Jiang, P.; Chen, Y.; Geng, Y.; Dong, W.; Xue, B.; Li, W. Analysis of the co-benefits of climate change mitigation and air pollution reduction in China. J. Clean. Prod. 2013, 58, 130–137. [Google Scholar] [CrossRef]

- Fernando, Y.; Hor, W.L. Impacts of energy management practices on energy efficiency and carbon emissions reduction: A survey of Malaysian manufacturing firms. Resour. Conserv. Recycl. 2017, 126, 62–73. [Google Scholar] [CrossRef]

- Shan, P.; Zhang, L.; Jiang, S.; Hou, A.; Huang, Z. Which coal-fired power units in China should be prioritized for decommissioning? Energy 2024, 308, 133059. [Google Scholar] [CrossRef]

- Acemoglu, D.; Aghion, P.; Bursztyn, L.; Hemous, D. The environment and directed technical change. Am. Econ. Rev. 2012, 102, 131–166. [Google Scholar] [CrossRef]

- Yang, L.; Li, Z. Technology advance and the carbon dioxide emission in China—Empirical research based on the rebound effect. Energy Policy 2017, 101, 150–161. [Google Scholar] [CrossRef]

- Dong, F.; Long, R.; Yu, B.; Wang, Y.; Li, J.; Wang, Y.; Dai, Y.; Yang, Q.; Chen, H. How can China allocate CO2 reduction targets at the provincial level considering both equity and efficiency? Evidence from its Copenhagen Accord pledge. Resour. Conserv. Recycl. 2018, 130, 31–43. [Google Scholar] [CrossRef]

- Chen, X.; Chen, Y.E.; Chang, C.P. The effects of environmental regulation and industrial structure on carbon dioxide emission: A non-linear investigation. Environ. Sci. Pollut. Res. 2019, 26, 30252–30267. [Google Scholar] [CrossRef]

- Chen, S.; Shi, A.; Wang, X. Carbon emission curbing effects and influencing mechanisms of China’s emission trading scheme: The mediating roles of technique effect, composition effect and allocation effect. J. Clean. Prod. 2020, 264, 121700. [Google Scholar] [CrossRef]

- Sovacool, K.; Brown, M.A. Scaling the policy response to climate change. Policy Soc. 2009, 27, 317–328. [Google Scholar] [CrossRef]

- Han, Y. Impact of environmental regulation policy on environmental regulation level: A quasi-natural experiment based on carbon emission trading pilot. Environ. Sci. Pollut. Res. 2020, 27, 23602–23615. [Google Scholar] [CrossRef] [PubMed]

- Li, X. How digital finance affect rural household carbon emissions from energy expenditures: Evidence from rural China. Energy Sources 2025, 20, 2505179. [Google Scholar] [CrossRef]

- Yin, Z.; Chang, N. The carbon characteristics of digital economy: A case study in China. Appl. Econ. 2025, 1–16. [Google Scholar] [CrossRef]

- Hu, R.; Song, K. Carbon reduction effects of government digital attention. Front. Environ. 2025, 13, 1539223. [Google Scholar] [CrossRef]

- Yuan, X.; Dong, Y.; Liang, L.; Wei, Y. The impact of carbon emission trading scheme policy on information asymmetry in the stock market: Evidence from China. Energy Policy 2025, 198, 114502. [Google Scholar] [CrossRef]

- Tu, Z.; Cao, Y.; Kong, J. The Impacts of Low-Carbon City Pilot Projects on Carbon Emissions in China. Atmosphere 2022, 13, 1269. [Google Scholar] [CrossRef]

- Hansol, M.; Juchul, J. Impact of Compact City on Carbon Emission Reduction Based on Urban Size: A Spatial Analysis Using Satellite Imagery, Sustainable Cities and Society. Sustain. City Soc. 2025, 126, 106326. [Google Scholar]

- Zhou, D.; Chen, G.; Xie, D. Can green financial pilot policy reduce firms’ carbon emissions? Evidence from Chinese manufacturing firms. Econ. Change Restruct. 2025, 58, 16. [Google Scholar] [CrossRef]

- Huang, J.; Zheng, B.; Du, M. How digital economy mitigates urban carbon emissions: The green facilitative power of industrial coagglomeration. Appl. Econ. 2025, 1–19. [Google Scholar] [CrossRef]

- Liu, C. The impact of green technological innovation on carbon emissions—A perspective based on nonlinear effects, moderating effects and spatial spillover effects. Technol. Anal. Strateg. Manag. 2025, 1–18. [Google Scholar] [CrossRef]

- Zhang, X.; Qiu, F.; Liu, J. Digital Economy’s Impact on Carbon Emission Performance: Evidence from the Yangtze River Delta, China. Chin. Geogr. Sci. 2025, 35, 217–233. [Google Scholar] [CrossRef]

- Liu, Z.; Li, L.; Hou, J.; Li, B. Does digital innovation improve carbon productivity? A new perspective based on industrial upgrading. Appl. Econ. 2025, 1–19. [Google Scholar] [CrossRef]

- Yang, Z.; Huang, S.; Ma, J.; Song, C.; Xu, S. The impact of digital infrastructure on urban total factor carbon emission performance: Evidence from enterprise production and household consumption in China. Front. Environ. 2025, 13, 1506012. [Google Scholar]

- Wu, J.; Yu, Z.; Wang, B.; Ma, C. Environmental regulations and carbon intensity: Assessing the impact of command-and-control, market-incentive, and public-participation approaches. Carbon Manag. 2025, 16, 2499091. [Google Scholar] [CrossRef]

- Yu, B.; Shen, C. Environmental regulation and industrial capacity utilization: An empirical study of China. J. Clean. Prod. 2020, 246, 118986. [Google Scholar] [CrossRef]

- Zhu, B.; Su, B.; Li, Y.; Ng, Y.S. Embodied energy and intensity in China’s (normal and processing) exports and their driving forces, 2005-2015. Energy Econ. 2020, 91, 104911. [Google Scholar] [CrossRef]

- Li, M.; Du, W. Opening the black box of capacity governance: Environmental regulation and capacity utilization of microcosmic firms in China. Econ. Model. 2022, 108, 105766. [Google Scholar] [CrossRef]

- Xie, B.; Yang, C.; Song, W.; Song, L.; Wang, A. The impact of environmental regulation on capacity utilization of China’s manufacturing industry: An empirical research based on the sector level. Ecol. Indic. 2023, 148, 110085. [Google Scholar] [CrossRef]

- Xu, X.; Xu, X.; Chen, Q.; Che, Y. The impacts on CO2 emission reduction and haze by coal resource tax reform based on dynamic CGE model. Resour. Policy 2018, 58, 268–276. [Google Scholar] [CrossRef]

- Du, W.; Wang, F.; Li, M. Effects of environmental regulation on capacity utilization: Evidence from energy enterprises in China. Ecol. Indic. 2020, 113, 106217. [Google Scholar] [CrossRef]

- Liu, C.; Xin, L.; Li, J. Environmental regulation and manufacturing carbon emissions in China: A new perspective on local government competition. Environ. Sci. Pollut. Res. 2022, 29, 36351–36375. [Google Scholar] [CrossRef] [PubMed]

- Yang, X.; Yang, X.; Zhu, J.; Jiang, P.; Lin, H.; Cai, Z.; Huang, H.; Long, J. Synergic emissions reduction effect of China’s “Air Pollution Prevention and Control Action Plan”: Benefits and efficiency. Sci. Total Environ. 2022, 847, 157564. [Google Scholar] [CrossRef] [PubMed]

- Huang, X.; Tian, P. How does heterogeneous environmental regulation affect net carbon emissions: Spatial and threshold analysis for China. J. Environ. Manag. 2023, 330, 117161. [Google Scholar] [CrossRef]

- Ouyang, W.; Zhou, Y.; Wang, Y. Can command-and-control regulation reduce carbon emissions? Evidence from China. Environ. Impact Assess. Rev. 2025, 112, 107802. [Google Scholar] [CrossRef]

- Sinn, H.W. Public policies against global warming: A supply side approach. Int. Tax Public Financ. 2008, 15, 360–394. [Google Scholar] [CrossRef]

- Albulescu, C.T.; Artene, A.E.; Luminosu, C.T.; Tămășilă, M. CO2 emissions, renewable energy, and environmental regulations in the EU countries. Environ. Sci. Pollut. Res. 2020, 27, 33615–33635. [Google Scholar] [CrossRef]

- Chen, J.; Huang, S.; Shen, Z.; Song, M.; Zhu, Z. Impact of sulfur dioxide emissions trading pilot scheme on pollution emissions intensity: A study based on the synthetic control method. Energy Policy 2022, 161, 112730. [Google Scholar] [CrossRef]

- Wang, K.; Wei, Y.M.; Huang, Z. Potential gains from carbon emissions trading in China: A DEA based estimation on abatement cost savings. Omega 2016, 63, 48–59. [Google Scholar] [CrossRef]

- Zhou, D.; Liang, X.; Zhou, Y.; Tang, K. Does emission trading boost carbon productivity? Evidence from China’s Pilot Emission Trading Scheme. Int. J. Environ. Res. Public Health 2020, 17, 5522. [Google Scholar] [CrossRef]

- Yang, X.; Zhang, J.; Bi, L.; Jiang, Y. Does China’s carbon trading pilot policy reduce carbon emissions? Empirical analysis from 285 cities. Int. J. Environ. Res. Public Health 2023, 20, 4421. [Google Scholar] [CrossRef]

- Zhang, K.; Xu, D.; Li, S.; Zhou, N.; Xiong, J. Has China’s pilot emissions trading scheme influenced the carbon intensity of output? Int. J. Environ. Res. Public Health 2019, 16, 1854. [Google Scholar] [CrossRef] [PubMed]

- Ren, F.; Liu, X. Evaluation of carbon emission reduction effect and porter effect of China’s carbon trading policy. Environ. Sci. Pollut. Res. 2023, 30, 46527–46546. [Google Scholar] [CrossRef] [PubMed]

- Lv, M.; Bai, M. Evaluation of China’s carbon emission trading policy from corporate innovation. Financ. Res. Lett. 2021, 39, 1544–6123. [Google Scholar] [CrossRef]

- Zhang, W.; Li, G.; Guo, F. Does carbon emissions trading promote green technology innovation in China? Appl. Energy 2022, 315, 119012. [Google Scholar] [CrossRef]

- Porter, M.E.; van der Linde, C. Toward a new conception of the environment-competitiveness relationship. J. Econ. Perspect. 1995, 9, 97–118. [Google Scholar] [CrossRef]

- Jorgenson, D.W.; Wilcoxen, P.J. Environmental regulation and U.S. economic growth. RAND J. Econ. 1990, 21, 314–340. [Google Scholar] [CrossRef]

- Barney, J. Firm resources and sustained competitive advantage. J. Manag. 1991, 17, 99–120. [Google Scholar] [CrossRef]

- Wu, Y.; Qi, J.; Xian, Q.; Chen, J. The carbon emission reduction effect of China’s carbon market: From the perspective of the coordination between market mechanism and administrative intervention. China Ind. Econ. 2021, 114–132. (In Chinese) [Google Scholar]

- Feng, X.; Zhao, Y.; Yan, R. Does carbon emission trading policy has emission reduction effect?—An empirical study based on quasi-natural experiment method. J. Environ. Manag. 2024, 351, 119791. [Google Scholar] [CrossRef]

- Xu, W.; Sun, L. Market-Incentive Environmental Regulation and Energy Consumption Structure Transformation. J. Quant. Technol. Econ. 2023, 40, 133–155. (In Chinese) [Google Scholar]

- Chung, Y.H.; Färe, R.; Grosskopf, S. Productivity and Undesirable Outputs: A Directional Distance Function Approach. J. Environ. Manag. 1997, 51, 229–240. [Google Scholar] [CrossRef]

- Morrison, C.J. Primal and dual capacity utilization: An application to productivity measurement in the U.S. automobile industry. J. Bus. Econ. Stat. 1985, 3, 312–324. [Google Scholar] [CrossRef]

- Olley, G.S.; Pakes, A. The Dynamics of Productivity in the Telecommunications Equipment Industry. Econometrica 1996, 64, 1263–1297. [Google Scholar] [CrossRef]

- Han, Z.; Wang, L.; Zhao, F. Can emission trading system improve capacity utilization? A quasi-natural experiment in Chinese listed firms. J. Clean. Prod. 2023, 385, 135719. [Google Scholar] [CrossRef]

- Svensson, L.; Fare, R. Congestion of Production Factors. Econometrica 1980, 48, 1745–1753. [Google Scholar]

- Wang, Z.; Yu, X.; Zhang, W. Chinese-style carbon emission reduction: Micro mechanisms of state-owned enterprises. Int. Rev. Econ. Financ. 2024, 96, 103527. [Google Scholar] [CrossRef]

- Zhao, L.; Li, Z.; Cheng, L. The impact of China’s carbon emissions trading policy on corporate investment expenditures: Evidence from carbon-intensive industries. J. Environ. Manag. 2024, 366, 121743. [Google Scholar] [CrossRef]

- Ji, H.; Yu, Z.; Tian, G.; Wang, D.; Wen, Y. Market competition, environmental, social and corporate governance investment, and enterprise green innovation performance. Financ. Res. Lett. 2025, 77, 107057. [Google Scholar] [CrossRef]

- Li, Q.; Tian, S. Can Environmental Regulation Promote Corporate Environmental Investment—Considering the Influence of Market Competition. J. Beijing Inst. Technol. 2016, 18, 1–8. (In Chinese) [Google Scholar]

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Variables | N | Mean | SD | Min | Max |

|---|---|---|---|---|---|

| CRE | 12,672 | −4.493 | 1.959 | −9.628 | 0.303 |

| CE | 12,672 | 45.380 | 147.114 | 0.093 | 1023.210 |

| CU | 12,672 | 0.793 | 0.677 | 0.043 | 2.997 |

| did | 12,672 | 0.021 | 0.143 | 0 | 1 |

| Cap | 12,672 | 1.912 | 1.143 | 0.453 | 8.243 |

| ROA | 12,672 | 0.045 | 0.059 | −0.219 | 0.208 |

| Emp | 12,672 | 7.863 | 1.081 | 5.288 | 10.81 |

| Tax | 12,672 | 17.07 | 1.476 | 13.260 | 21.020 |

| Size | 12,672 | 22.11 | 1.154 | 19.920 | 25.510 |

| TFP | 12,672 | 3.044 | 0.781 | 0.169 | 6.799 |

| HHI | 12,672 | 0.068 | 0.057 | 0.013 | 0.278 |

| Mshare | 12,672 | 13.43 | 20.02 | 0 | 69.83 |

| City | 12,672 | 0.704 | 0.456 | 0 | 1 |

| Regular | 12,672 | 0.256 | 0.436 | 0 | 1 |

| Gov | 12,672 | 0.144 | 0.053 | 0.044 | 1.699 |

| Price | 12,672 | 0.693 | 1.886 | 0 | 18.23 |

| Type | α | β | γ | δ |

|---|---|---|---|---|

| low-pollution | 0.053561 | 0.04676 | 0.717975 | 0.212395 |

| medium-pollution | 0.021886 | 0.049416 | 0.792614 | 0.15082 |

| high-pollution | 0.063167 | 0.035407 | 0.839682 | 0.060593 |

| (1) | (2) | (3) | (4) | |

|---|---|---|---|---|

| VARIABLES | CRE | CRE | CE | CU |

| did | 0.158 *** | 0.113 ** | ||

| (0.024) | (0.046) | |||

| did_short | −0.042 * | 0.011 | ||

| (0.022) | (0.035) | |||

| did_long | −0.088 *** | 0.190 *** | ||

| (0.023) | (0.070) | |||

| L.CRE | 0.933 *** | 0.664 *** | ||

| (0.005) | (0.015) | |||

| L.CE | 0.625 *** | |||

| (0.018) | ||||

| L.CU | 0.650 *** | |||

| (0.013) | ||||

| Cap | −0.024 *** | −0.010 | −0.129 *** | −0.191 *** |

| (0.005) | (0.009) | (0.008) | (0.011) | |

| ROA | −0.282 *** | −0.010 | 0.109 * | 0.235 *** |

| (0.067) | (0.091) | (0.056) | (0.086) | |

| Emp | −0.016 ** | −0.053 *** | 0.006 | −0.048 *** |

| (0.008) | (0.018) | (0.009) | (0.017) | |

| Scale | −0.085 *** | −0.412 *** | 0.350 *** | 0.015 |

| (0.008) | (0.027) | (0.019) | (0.020) | |

| TFP | −0.019 ** | 0.319 *** | −0.055 *** | 0.209 *** |

| (0.007) | (0.038) | (0.015) | (0.035) | |

| HHI | 0.139 *** | −0.062 | −0.029 | −0.140 ** |

| (0.033) | (0.067) | (0.035) | (0.059) | |

| Mshare | −0.003 *** | −0.002 *** | 0.000 | −0.002 *** |

| (0.000) | (0.001) | (0.000) | (0.001) | |

| City | 0.016 | 0.212 ** | −0.024 | 0.118 * |

| (0.010) | (0.083) | (0.054) | (0.065) | |

| Regular | −0.158 *** | −0.113 * | 0.146 *** | −0.003 |

| (0.014) | (0.059) | (0.041) | (0.045) | |

| Gov | −0.099 | −0.174 | 0.039 | −0.187 |

| (0.077) | (0.194) | (0.117) | (0.194) | |

| Price | −0.005 ** | −0.003 | 0.004 *** | 0.001 |

| (0.002) | (0.003) | (0.001) | (0.003) | |

| Tax | 0.016 *** | 0.013 ** | 0.005 * | 0.021 *** |

| (0.005) | (0.006) | (0.003) | (0.005) | |

| Constant | 1.518 *** | 6.722 *** | −6.658 *** | −1.564 *** |

| (0.125) | (0.471) | (0.339) | (0.353) | |

| N | 12,672 | 12,672 | 12,672 | 12,672 |

| R2 | 0.959 | 0.974 | 0.993 | 0.939 |

| Year | NO | YES | YES | YES |

| Ind | NO | YES | YES | YES |

| (1) | (2) | |

|---|---|---|

| Variables | CU | CE |

| did | 0.063 ** | 0.125 ** |

| (0.031) | (0.057) | |

| Controls | YES | YES |

| Constants | 8.634 *** | 2.868 *** |

| (0.359) | (0.414) | |

| N | 12,672 | 12,672 |

| R2 | 0.991 | 0.947 |

| Year | YES | YES |

| Ind | YES | YES |

| (1) | (2) | (3) | |

|---|---|---|---|

| Variables | Nearest Neighbor Matching | Radius Matching | Kernel Matching |

| did | 0.127 ** | 0.112 ** | 0.105 ** |

| (0.052) | (0.046) | (0.046) | |

| Controls | YES | YES | YES |

| Constants | 5.632 *** | 6.690 *** | 6.448 *** |

| (1.287) | (0.472) | (0.480) | |

| N | 952 | 12,619 | 11,030 |

| R2 | 0.983 | 0.974 | 0.975 |

| Year | YES | YES | YES |

| Ind | YES | YES | YES |

| (1) | (2) | (3) | (4) | |

|---|---|---|---|---|

| did | 0.1538 ** | 0.1259 ** | 0.1639 * | 0.1116 * |

| (0.069) | (0.061) | (0.099) | (0.065) | |

| Smart City | −0.0164 | |||

| (0.025) | ||||

| Low Carbon | −0.0080 | |||

| (0.018) | ||||

| Provincially Designated | 0.0307 ** | |||

| (0.013) | ||||

| Nationally Designated | −0.0056 | |||

| (0.013) | ||||

| did × Smart City | −0.0891 | |||

| (0.086) | ||||

| did × Low Carbon | −0.0088 | |||

| (0.079) | ||||

| did × Provincially | −0.0674 | |||

| (0.112) | ||||

| did × Nationally | 0.0427 | |||

| (0.081) | ||||

| Controls | YES | YES | YES | YES |

| Constant | 6.7459 *** | 6.7509 *** | 6.7033 *** | 6.7185 *** |

| (0.473) | (0.475) | (0.470) | (0.471) | |

| N | 12,654 | 12,602 | 12,654 | 12,644 |

| R2 | 0.974 | 0.974 | 0.974 | 0.974 |

| Year | YES | YES | YES | YES |

| Ind | YES | YES | YES | YES |

| (1) | (2) | (3) | (4) | (5) | (6) | |

|---|---|---|---|---|---|---|

| Variables | Innovation | CRE | Investment | CRE | Management | CRE |

| did | 0.2929 ** | 0.0789 ** | 0.0940 ** | 0.0866 * | 0.0064 ** | 0.0765 ** |

| (0.140) | (0.037) | (0.039) | (0.052) | (0.003) | (0.034) | |

| Innovation | 0.0112 *** | |||||

| (0.003) | ||||||

| Investment | 0.0365 ** | |||||

| (0.019) | ||||||

| Management | 0.3798 * | |||||

| (0.211) | ||||||

| Constant | −12.2124 *** | 6.9157 *** | 5.9498 *** | 6.3281 *** | 0.5224 *** | 6.4171 *** |

| (2.128) | (0.465) | (0.353) | (0.514) | (0.026) | (0.484) | |

| Controls | YES | YES | YES | YES | YES | YES |

| N | 14,474 | 12,672 | 13,374 | 12,672 | 14,474 | 12,672 |

| R2 | 0.979 | 0.974 | 0.956 | 0.977 | 0.834 | 0.975 |

| Year | YES | YES | YES | YES | YES | YES |

| Ind | YES | YES | YES | YES | YES | YES |

| (1) | (2) | (3) | (4) | (5) | (6) | (7) | (8) | |

|---|---|---|---|---|---|---|---|---|

| Variables | SOEs | CIEs | EEs | HHI | ||||

| Y | N | Y | N | Y | N | Low | High | |

| did | 0.104 * | 0.118 | 0.144 ** | 0.026 | 0.118 ** | 0.053 | 0.203 *** | 0.000 |

| (0.057) | (0.083) | (0.057) | (0.074) | (0.055) | (0.066) | (0.073) | (0.050) | |

| Controls | YES | YES | YES | YES | YES | YES | YES | YES |

| Constants | 6.463 *** | 7.213 *** | 6.805 *** | 6.378 *** | 6.501 *** | 6.401 *** | 5.879 *** | 7.408 *** |

| (0.751) | (0.613) | (0.527) | (0.951) | (0.530) | (0.813) | (0.586) | (0.718) | |

| N | 4244 | 8352 | 10,044 | 2610 | 8909 | 3720 | 5858 | 6796 |

| R2 | 0.977 | 0.969 | 0.970 | 0.981 | 0.972 | 0.975 | 0.967 | 0.979 |

| Year | YES | YES | YES | YES | YES | YES | YES | YES |

| Ind | YES | YES | YES | YES | YES | YES | YES | YES |

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2025 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Wang, Y.; Wu, W. Does the Carbon Emission Trading Pilot Policy Enhance Carbon Reduction Efficiency? Sustainability 2025, 17, 5076. https://doi.org/10.3390/su17115076

Wang Y, Wu W. Does the Carbon Emission Trading Pilot Policy Enhance Carbon Reduction Efficiency? Sustainability. 2025; 17(11):5076. https://doi.org/10.3390/su17115076

Chicago/Turabian StyleWang, Yin, and Wanzong Wu. 2025. "Does the Carbon Emission Trading Pilot Policy Enhance Carbon Reduction Efficiency?" Sustainability 17, no. 11: 5076. https://doi.org/10.3390/su17115076

APA StyleWang, Y., & Wu, W. (2025). Does the Carbon Emission Trading Pilot Policy Enhance Carbon Reduction Efficiency? Sustainability, 17(11), 5076. https://doi.org/10.3390/su17115076