The Synergistic Effect of the Dual Carbon Reduction Pilot on Corporate Carbon Performance: Empirical Evidence from Listed Manufacturing Companies

Abstract

1. Introduction

2. Policy Background, Literature Review, and Research Hypotheses

2.1. Policy Background

2.2. Literature Review

2.2.1. The Effect of Environmental Policy

2.2.2. Synergies of the Policy Mix

2.3. Research Hypotheses

2.3.1. The Impact of CETP on Corporate Carbon Performance

2.3.2. The Impact of LCCP on Corporate Carbon Performance

2.3.3. Analysis of the Synergistic Effect of DCRP

3. Materials and Methods

3.1. Model Specification

3.2. Variables

3.2.1. Dependent Variable

3.2.2. Independent Variables

3.2.3. Control Variables

3.3. Data

4. Results and Discussion

4.1. Descriptive Statistics

4.2. Univariate Difference Test

4.3. Benchmark Regression

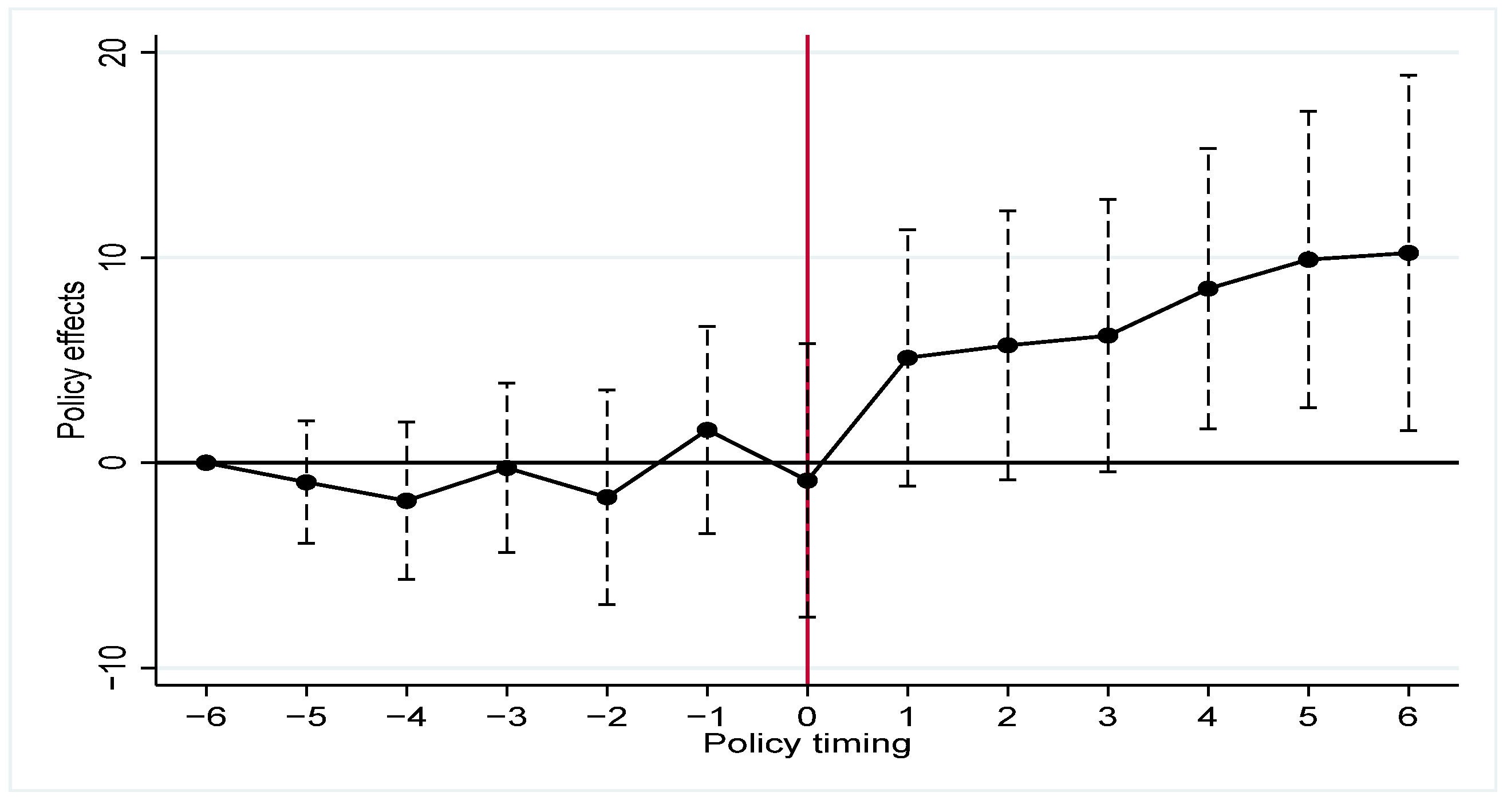

4.4. Parallel Trend Test

4.5. Robustness Test

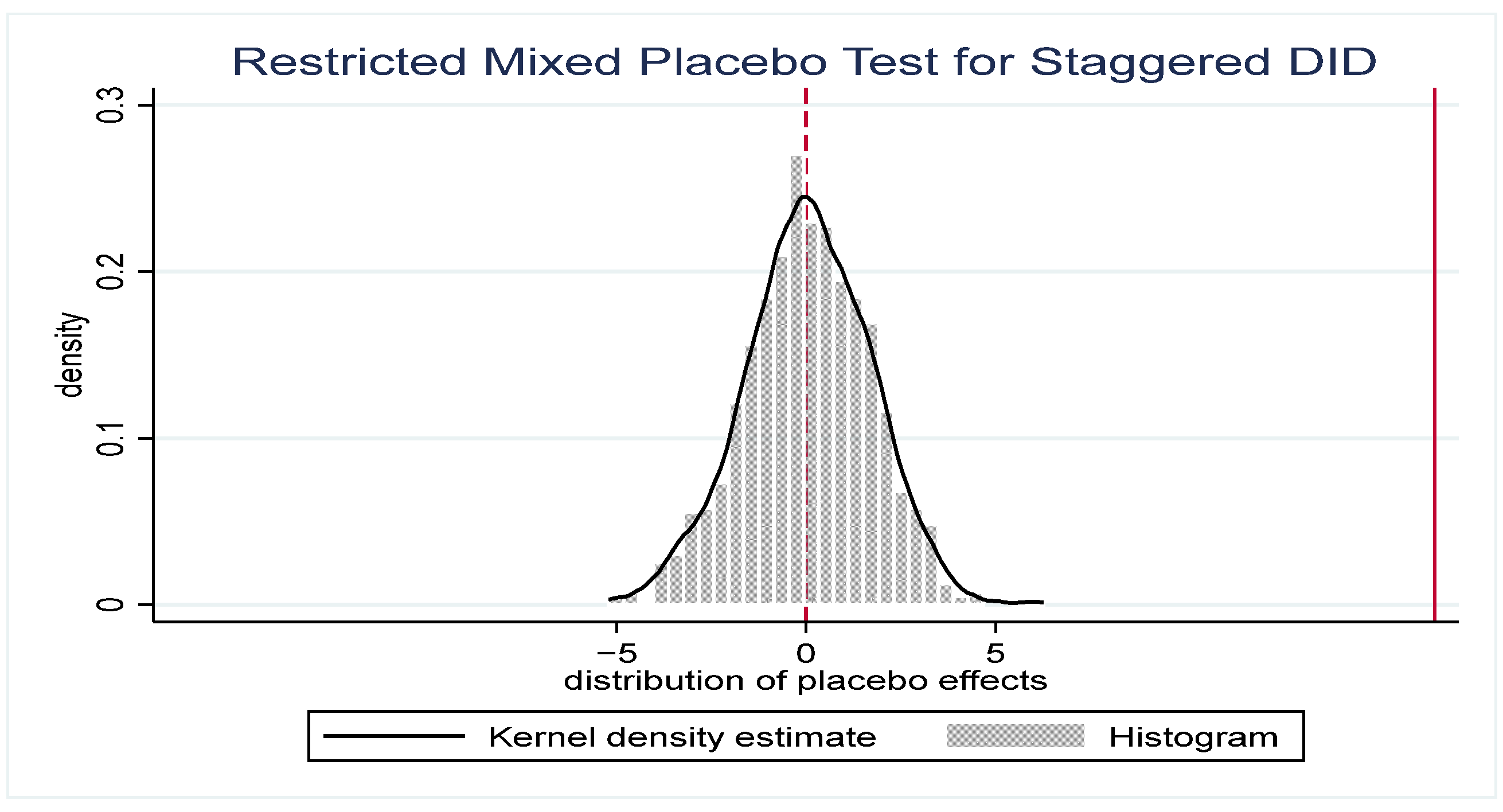

4.5.1. Placebo Test

4.5.2. Adjust the Sample Structure

4.5.3. Change the Clustering Level

4.5.4. Change the Test Method of Policy Synergistic Effect

4.6. Endogenous Analysis

4.6.1. PSM-DID

4.6.2. Eliminating Policy Factors

4.6.3. Lagged Independent Variable

4.6.4. IV Method

4.7. Mechanism Analysis

4.8. Heterogeneity Analysis

4.8.1. Enterprise Pollution Intensity Heterogeneity

4.8.2. Regional Heterogeneity

4.8.3. Heterogeneity in Enterprises’ Technological Attributes

5. Conclusions and Policy Recommendations

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Acknowledgments

Conflicts of Interest

Abbreviations

| WMO | The World Meteorological Organization |

| LCCP | Low-Carbon City Pilot |

| CETP | Carbon Emission Trading Pilot |

| DCRP | Dual carbon reduction pilot |

References

- World Meteorological Organization. World Meteorological Organization WMO Confirms 2024 as Warmest Year on Record at About 1.55 °C Above Pre-Industrial Level 2025; World Meteorological Organization: Geneva, Switzerland, 2025. [Google Scholar]

- Cole, M.A.; Elliott, R.J.; Okubo, T.; Zhou, Y. The Carbon Dioxide Emissions of Firms: A Spatial Analysis. J. Environ. Econ. Manag. 2013, 65, 290–309. [Google Scholar] [CrossRef]

- Jiang, W.; Wang, K.-L.; Jiang, N. 1+1 > 2? The Synergistic Effect of Carbon Emissions Reduction Policies: Empirical Evidence from China. Clim. Policy 2024, 1–14. [Google Scholar] [CrossRef]

- Jia, Z.; Wen, S. Interaction Effects of Market-Based and Incentive-Driven Low-Carbon Policies on Carbon Emissions. Energy Econ. 2024, 137, 107776. [Google Scholar] [CrossRef]

- Shi, B.; Li, N.; Gao, Q.; Li, G. Market Incentives, Carbon Quota Allocation and Carbon Emission Reduction: Evidence from China’s Carbon Trading Pilot Policy. J. Environ. Manag. 2022, 319, 115650. [Google Scholar] [CrossRef]

- Khanna, N.; Fridley, D.; Hong, L. China’s Pilot Low-Carbon City Initiative: A Comparative Assessment of National Goals and Local Plans. Sustain. Cities Soc. 2014, 12, 110–121. [Google Scholar] [CrossRef]

- Clarkson, P.; Li, Y.; Richardson, G.; Vasvari, F. Does It Really Pay to Be Green? Determinants and Consequences of Proactive Environmental Strategies. J. Account. Public Policy 2011, 30, 122–144. [Google Scholar] [CrossRef]

- Haque, F.; Ntim, C.G. Executive Compensation, Sustainable Compensation Policy, Carbon Performance and Market Value. Br. J. Manag. 2020, 31, 525–546. [Google Scholar] [CrossRef]

- Chen, S.; Mao, H.; Sun, J. Low-Carbon City Construction and Corporate Carbon Reduction Performance: Evidence from a Quasi-Natural Experiment in China. J. Bus. Ethics 2022, 180, 125–143. [Google Scholar] [CrossRef]

- Tan, X.; Choi, Y.; Wang, B.; Huang, X. Does China’s Carbon Regulatory Policy Improve Total Factor Carbon Efficiency? A Fixed-Effect Panel Stochastic Frontier Analysis. Technol. Forecast. Soc. Chang. 2020, 160, 120222. [Google Scholar] [CrossRef]

- Wang, X.; Gao, C. Does Green Finance Policy Help to Improve Carbon Reduction Welfare Performance? Evidence from China. Energy Econ. 2024, 132, 107452. [Google Scholar] [CrossRef]

- Li, N.; Zhang, H.; Zhang, X.; Xie, X. Does Market-Based Environmental Regulatory Policy Improve Corporate Environmental Performance? Evidence from Carbon Emission Trading in China. Sustainability 2025, 17, 623. [Google Scholar] [CrossRef]

- Yang, Z.; Shao, S.; Yang, L. Unintended Consequences of Carbon Regulation on the Performance of SOEs in China: The Role of Technical Efficiency. Energy Econ. 2021, 94, 105072. [Google Scholar] [CrossRef]

- Yang, L.; Li, Y.; Liu, H. Did Carbon Trade Improve Green Production Performance? Evidence from China. Energy Econ. 2021, 96, 105185. [Google Scholar] [CrossRef]

- Yang, Z.; Fan, M.; Shao, S.; Yang, L. Does Carbon Intensity Constraint Policy Improve Industrial Green Production Performance in China? A Quasi-DID Analysis. Energy Econ. 2017, 68, 271–282. [Google Scholar] [CrossRef]

- Zhang, K.; Xu, D.; Li, S.; Zhou, N.; Xiong, J. Has China’s Pilot Emissions Trading Scheme Influenced the Carbon Intensity of Output? Int. J. Environ. Res. Public Health 2019, 16, 1854. [Google Scholar] [CrossRef]

- Ge, X.; Li, Y.; Yang, H. The Green Paradox of Time Dimension: From Pilot to National Carbon Emission Trading System in China. Environ. Impact Assess. Rev. 2024, 109, 107642. [Google Scholar] [CrossRef]

- Yang, S. Carbon Emission Trading Policy and Firm’s Environmental Investment. Financ. Res. Lett. 2023, 54, 103695. [Google Scholar] [CrossRef]

- Li, H.; Wang, J.; Yang, X.; Wang, Y.; Wu, T. A Holistic Overview of the Progress of China’s Low-Carbon City Pilots. Sustain. Cities Soc. 2018, 42, 289–300. [Google Scholar] [CrossRef]

- Gustafsson, B. Scope and Limits of the Market Mechanism in Environmental Management. Ecol. Econ. 1998, 24, 259–274. [Google Scholar] [CrossRef]

- Zeng, S.; Jin, G.; Tan, K.; Liu, X. Can Low-Carbon City Construction Reduce Carbon Intensity? Empirical Evidence from Low-Carbon City Pilot Policy in China. J. Environ. Manag. 2023, 332, 117363. [Google Scholar] [CrossRef]

- Xu, R.; Pata, U.K.; Dai, J. Sustainable Growth through Green Electricity Transition and Environmental Regulations: Do Risks Associated with Corruption and Bureaucracy Matter? Politická Ekon. 2024, 72, 228–254. [Google Scholar] [CrossRef]

- Sinn, H. Public Policies against Global Warming: A Supply Side Approach. Int. Tax Public Financ. 2008, 15, 360–394. [Google Scholar] [CrossRef]

- Sepehri, A.; Sarrafzadeh, M.-H. Effect of Nitrifiers Community on Fouling Mitigation and Nitrification Efficiency in a Membrane Bioreactor. Chem. Eng. Process.-Process Intensif. 2018, 128, 10–18. [Google Scholar] [CrossRef]

- Yousefi, S.R.; Ghanbari, D.; Salavati-Niasari, M.; Hassanpour, M. Photo-Degradation of Organic Dyes: Simple Chemical Synthesis of Ni(OH)2 Nanoparticles, Ni/Ni(OH)2 and Ni/NiO Magnetic Nanocomposites. J. Mater. Sci. Mater. Electron. 2016, 27, 1244–1253. [Google Scholar] [CrossRef]

- Hong, Q.; Cui, L.; Hong, P. The Impact of Carbon Emissions Trading on Energy Efficiency: Evidence from Quasi-Experiment in China’s Carbon Emissions Trading Pilot. Energy Econ. 2022, 110, 106025. [Google Scholar] [CrossRef]

- Pan, A.; Zhang, W.; Shi, X.; Dai, L. Climate Policy and Low-Carbon Innovation: Evidence from Low-Carbon City Pilots in China. Energy Econ. 2022, 112, 106129. [Google Scholar] [CrossRef]

- Yu, Y.; Zhang, N. Low-Carbon City Pilot and Carbon Emission Efficiency: Quasi-Experimental Evidence from China. Energy Econ. 2021, 96, 105125. [Google Scholar] [CrossRef]

- Cao, Y.; Wu, Y.; Li, Z.; Wang, Q. Climate Policy and Carbon Leakage: Evidence from the Low-Carbon City Pilot Program in China. Environ. Impact Assess. Rev. 2025, 110, 107730. [Google Scholar] [CrossRef]

- Lyu, J.; Liu, T.; Cai, B.; Qi, Y.; Zhang, X. Heterogeneous Effects of China’s Low-Carbon City Pilots Policy. J. Environ. Manag. 2023, 344, 118329. [Google Scholar] [CrossRef]

- Feng, T.; Lin, Z.; Du, H.; Qiu, Y.; Zuo, J. Does Low-Carbon Pilot City Program Reduce Carbon Intensity? Evidence from Chinese Cities. Res. Int. Bus. Financ. 2021, 58, 101450. [Google Scholar] [CrossRef]

- Chen, X.; Lin, B. Towards Carbon Neutrality by Implementing Carbon Emissions Trading Scheme: Policy Evaluation in China. Energy Policy 2021, 157, 112510. [Google Scholar] [CrossRef]

- Zhuo, C.; Liu, Y.; Dai, L.; Deng, Y. Cultural, Economic, or Transport Link: Does Carbon Emissions Trading Promote “Good Neighbor” Carbon Emission Reduction? Land 2024, 13, 1762. [Google Scholar] [CrossRef]

- Reich, P.B.; Hobbie, S.E.; Lee, T.D.; Rich, R.; Pastore, M.A.; Worm, K. Synergistic Effects of Four Climate Change Drivers on Terrestrial Carbon Cycling. Nat. Geosci. 2020, 13, 787–793. [Google Scholar] [CrossRef]

- Wilts, H.; O’Brien, M. A Policy Mix for Resource Efficiency in the EU: Key Instruments, Challenges and Research Needs. Ecol. Econ. 2019, 155, 59–69. [Google Scholar] [CrossRef]

- Edmondson, D.L.; Kern, F.; Rogge, K.S. The Co-Evolution of Policy Mixes and Socio-Technical Systems: Towards a Conceptual Framework of Policy Mix Feedback in Sustainability Transitions. Res. Policy 2019, 48, 103555. [Google Scholar] [CrossRef]

- Zhang, P.; Zhou, D.; Guo, J. Policy Complementary or Policy Crowding-out? Effects of Cross-Instrumental Policy Mix on Green Innovation in China. Technol. Forecast. Soc. Change 2023, 192, 122530. [Google Scholar] [CrossRef]

- Montgomery, W. Markets in Licenses and Efficient Pollution Control Programs. J. Econ. Theory 1972, 5, 395–418. [Google Scholar] [CrossRef]

- Wang, J.; Liu, L.; Ou, Y. Low-Carbon City Pilot Policy and Corporate Environmental Violations: Evidence from Heavily Polluting Firms in China. Financ. Res. Lett. 2024, 65, 105548. [Google Scholar] [CrossRef]

- Hahn, R.; Stavins, R. Economic Incentives for Environmental-Protection—Integrating Theory and Practice. Am. Econ. Rev. 1992, 82, 464–468. [Google Scholar]

- Jaehn, F.; Letmathe, P. The Emissions Trading Paradox. Eur. J. Oper. Res. 2010, 202, 248–254. [Google Scholar] [CrossRef]

- Sorrell, S.; Sijm, J. Carbon Trading in the Policy Mix. Oxf. Rev. Econ. Policy 2003, 19, 420–437. [Google Scholar] [CrossRef]

- Busch, T.; Lewandowski, S. Corporate Carbon and Financial Performance: A Meta-Analysis. J. Ind. Ecol. 2018, 22, 745–759. [Google Scholar] [CrossRef]

- Siddique, M.A.; Akhtaruzzaman, M.; Rashid, A.; Hammami, H. Carbon Disclosure, Carbon Performance and Financial Performance: International Evidence. Int. Rev. Financ. Anal. 2021, 75, 101734. [Google Scholar] [CrossRef]

- Ren, X.; Li, Y.; Shahbaz, M.; Dong, K.; Lu, Z. Climate Risk and Corporate Environmental Performance: Empirical Evidence from China. Sustain. Prod. Consum. 2022, 30, 467–477. [Google Scholar] [CrossRef]

- Cheng, Z.; Meng, X. Can Carbon Emissions Trading Improve Corporate Total Factor Productivity? Technol. Forecast. Soc. Chang. 2023, 195, 122791. [Google Scholar] [CrossRef]

- Chen, S.; Wang, Y.; Albitar, K.; Huang, Z. Does Ownership Concentration Affect Corporate Environmental Responsibility Engagement? The Mediating Role of Corporate Leverage. Borsa Istanb. Rev. 2021, 21, S13–S24. [Google Scholar] [CrossRef]

- Akhtar, M.; Yusheng, K.; Haris, M.; Ain, Q.U.; Javaid, H.M. Impact of Financial Leverage on Sustainable Growth, Market Performance, and Profitability. Econ. Chang. Restruct. 2022, 55, 737–774. [Google Scholar] [CrossRef]

- Qian, L.; Xu, X.; Sun, Y.; Zhou, Y. Carbon Emission Reduction Effects of Eco-Industrial Park Policy in China. Energy 2022, 261, 125315. [Google Scholar] [CrossRef]

- Lei, X. Assessing the Effectiveness of Energy Transition Policies on Corporate ESG Performance: Insights from China’s NEDC Initiative. Int. J. Glob. Warm. 2024, 34, 291–299. [Google Scholar] [CrossRef]

- He, W.; Wang, X.; Miao, M. Network Infrastructure and Corporate Environmental Performance: Empirical Evidence from “Broadband China”. Energy Econ. 2024, 131, 107393. [Google Scholar] [CrossRef]

- Yang, S.; Jahanger, A.; Hossain, M.R. How Effective Has the Low-Carbon City Pilot Policy Been as an Environmental Intervention in Curbing Pollution? Evidence from Chinese Industrial Enterprises. Energy Econ. 2023, 118, 106523. [Google Scholar] [CrossRef]

- Hering, L.; Poncet, S. Environmental Policy and Exports: Evidence from Chinese Cities. J. Environ. Econ. Manag. 2014, 68, 296–318. [Google Scholar] [CrossRef]

- Ghanem, D.; Zhang, J. ‘Effortless Perfection’: Do Chinese Cities Manipulate Air Pollution Data? J. Environ. Econ. Manag. 2014, 68, 203–225. [Google Scholar] [CrossRef]

- Yu, Y.Z.; Sun, P.B.; Xuan, Y. Do Constraints on Local Governments’ Environmental Targets Affect Industrial Transformation and Upgrading? Econ. Res. J. 2020, 55, 57–72. (In Chinese) [Google Scholar]

- Huang, J.-W.; Li, Y.-H. Green Innovation and Performance: The View of Organizational Capability and Social Reciprocity. J. Bus. Ethics 2017, 145, 309–324. [Google Scholar] [CrossRef]

- Xu, R.; Farooq, U.; Alam, M.M.; Dai, J. How Does Cultural Diversity Determine Green Innovation? New Empirical Evidence from Asia Region. Environ. Impact Assess. Rev. 2024, 106, 107458. [Google Scholar] [CrossRef]

- Liu, S.; Li, Y. Exploration or Exploitation? Corporate Green Innovation Strategy for Carbon Emission Reduction-Evidence from Pilot Enterprises in China. Sustainability 2024, 16, 4486. [Google Scholar] [CrossRef]

- Porter, M.E.; van der Linde, C. Toward a New Conception of the Environment-Competitiveness Relationship. J. Econ. Perspect. 1995, 9, 97–118. [Google Scholar] [CrossRef]

- Krysiak, F. Environmental Regulation, Technological Diversity, and the Dynamics of Technological Change. J. Econ. Dyn. Control 2011, 35, 528–544. [Google Scholar] [CrossRef]

- Huang, J.; Meng, S.; Yu, J. The Effects of the Low-Carbon Pilot City Program on Green Innovation: Evidence from China. Land 2023, 12, 1639. [Google Scholar] [CrossRef]

- Baron, R.M.; Kenny, D.A. The Moderator-Mediator Variable Distinction in Social Psychological Research: Conceptual, Strategic, and Statistical Considerations. J. Personal. Soc. Psychol. 1986, 51, 1173–1182. [Google Scholar] [CrossRef] [PubMed]

- Grafton, R.; Kompas, T.; Long, N. Substitution between Biofuels and Fossil Fuels: Is There a Green Paradox? J. Environ. Econ. Manag. 2012, 64, 328–341. [Google Scholar] [CrossRef]

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Variables | Explanation |

|---|---|

| CP | The ratio of operating revenue to carbon emissions. |

| DID | The interaction term between LCCP and CETP. |

| CETP | A binary variable indicating whether a firm is located in a CETP city. The variable is assigned a value of 1 starting from the year the firm’s city was designated as a pilot city, and 0 otherwise. |

| LCCP | A binary variable indicating whether a firm is located in an LCCP city. The variable is assigned a value of 1 starting from the year the firm’s city was designated as a pilot city, and 0 otherwise. |

| lnSale | The logarithm of corporate sales. |

| ROA | Net profit after tax/total assets. |

| Top | The shareholding ratio of the largest shareholder. |

| Lev | Total liabilities/total assets. |

| Cash | Net cash flows from operating activities/current liabilities. |

| Boardsize | The logarithm of the number of board members. |

| Growth | Increase rate of main business revenue. |

| Variables | Count | Mean | SD | Min | Max |

|---|---|---|---|---|---|

| CP | 20,673 | 45.46 | 62.91 | 0.16 | 270.66 |

| DID | 20,673 | 0.26 | 0.44 | 0.00 | 1.00 |

| CETP | 20,673 | 0.27 | 0.44 | 0.00 | 1.00 |

| LCCP | 20,673 | 0.55 | 0.50 | 0.00 | 1.00 |

| lnSale | 20,673 | 21.37 | 1.39 | 18.47 | 25.25 |

| ROA | 20,673 | 0.04 | 0.06 | −0.24 | 0.21 |

| Top | 20,673 | 0.35 | 0.15 | 0.09 | 0.74 |

| Lev | 20,673 | 0.41 | 0.20 | 0.05 | 0.95 |

| Cash | 20,673 | 0.05 | 0.07 | −0.15 | 0.24 |

| Boardsize | 20,673 | 2.14 | 0.20 | 1.61 | 2.71 |

| Growth | 20,673 | 0.23 | 0.60 | −0.68 | 3.84 |

| Panel A: based on CETP | |||||

| Variables | Group1 | Mean1 | Group2 | Mean2 | MeanDiff |

| CP | 15,158 | 35.584 | 5515 | 72.592 | −37.008 *** |

| Panel B: based on LCCP | |||||

| Variables | Group1 | Mean1 | Group2 | Mean2 | MeanDiff |

| CP | 9344 | 26.890 | 11,329 | 60.770 | −33.880 *** |

| Panel C: based on DID | |||||

| Variables | Group1 | Mean1 | Group2 | Mean2 | MeanDiff |

| CP | 15,366 | 35.860 | 5307 | 73.244 | −37.384 *** |

| (1) | (2) | (3) | (4) | (5) | (6) | |

|---|---|---|---|---|---|---|

| Variables | CP | CP | CP | CP | CP | CP |

| DID | 16.510 *** (2.89) | 16.465 *** (2.70) | ||||

| CETP | 9.276 *** (2.77) | 8.622 *** (2.61) | −6.063 *** (2.03) | −6.683 *** (2.08) | ||

| LCCP | 3.187 (2.34) | 3.209 (2.38) | 2.017 (2.35) | 2.089 (2.37) | ||

| lnSale | 1.826 * (1.00) | 1.974 * (1.02) | 1.765 * (0.99) | |||

| ROA | 21.075 *** (7.55) | 21.904 *** (7.41) | 21.201 *** (7.63) | |||

| Top | −17.769 *** (6.56) | −17.987 *** (6.63) | −18.085 *** (6.50) | |||

| Lev | 15.555 *** (4.39) | 16.397 *** (4.33) | 15.767 *** (4.39) | |||

| Cash | 0.423 (5.23) | −0.057 (5.20) | 0.170 (5.24) | |||

| Boardsize | 5.156 (3.30) | 5.300 (3.32) | 5.279 (3.30) | |||

| Growth | 1.471 ** (0.71) | 1.406 ** (0.71) | 1.423 ** (0.71) | |||

| constant | 32.910 *** (1.30) | −16.857 (22.63) | 33.213 *** (1.36) | −20.196 (23.21) | 32.679 *** (1.35) | −16.043 (22.62) |

| Year | Yes | Yes | Yes | Yes | Yes | Yes |

| Id | Yes | Yes | Yes | Yes | Yes | Yes |

| N | 20,673 | 20,673 | 20,673 | 20,673 | 20,673 | 20,673 |

| R2 | 0.149 | 0.156 | 0.145 | 0.153 | 0.150 | 0.158 |

| F | 66.804 | 52.827 | 50.477 | 46.494 | 68.482 | 59.720 |

| (1) | (2) | (3) | (4) | (5) | (6) | |

|---|---|---|---|---|---|---|

| Variables | CP | CP | CP | CP | CP | CP |

| DID | 19.803 *** (2.75) | 16.416 *** (2.55) | 10.186 *** (2.49) | 8.037 ** (3.51) | 8.507 *** (2.38) | 8.028 ** (3.52) |

| CETP | −6.557 *** (2.07) | −6.603 *** (1.80) | ||||

| LCCP | 2.635 (2.60) | 2.124 (1.98) | ||||

| lnSale | 2.719 *** (0.97) | 1.751 * (0.88) | 1.781 * (0.99) | 0.421 (1.53) | −3.077 * (1.66) | 0.435 (1.54) |

| ROA | 16.355 ** (7.42) | 20.985 *** (6.47) | 21.020 *** (7.59) | 31.764 *** (11.70) | 45.009 ** (17.47) | 31.891 *** (11.87) |

| Top | −18.194 ** (7.08) | −17.985 ** (8.20) | −17.995 *** (6.52) | −19.662 ** (9.82) | 1.945 (21.32) | −19.869 ** (9.83) |

| Lev | 12.785 *** (3.96) | 15.797 *** (4.38) | 15.542 *** (4.39) | 15.118 * (7.89) | 12.881 (14.40) | 15.105 * (8.00) |

| Cash | −5.132 (4.46) | 0.068 (4.54) | 0.369 (5.23) | 2.367 (7.85) | 7.379 (15.62) | 2.004 (8.01) |

| Boardsize | 6.165 (3.76) | 5.327 * (2.87) | 5.206 (3.30) | 0.763 (5.77) | −5.273 (8.97) | 1.398 (5.80) |

| Growth | 1.634 ** (0.67) | 1.413 ** (0.63) | 1.459 ** (0.71) | 0.530 (1.19) | 0.799 (2.16) | 0.600 (1.20) |

| constant | −36.626 (22.54) | −15.924 (19.83) | −16.016 (22.52) | 15.794 (39.67) | 117.897 ** (47.71) | 14.315 (40.05) |

| Year | Yes | Yes | Yes | Yes | Yes | Yes |

| Id | Yes | Yes | Yes | Yes | Yes | Yes |

| N | 17,680 | 20,749 | 20,673 | 11,537 | 5515 | 11,329 |

| R2 | 0.160 | 0.157 | 0.156 | 0.148 | 0.092 | 0.149 |

| F | 48.805 | 51.320 | 52.440 | 74.255 | 74.344 | 74.650 |

| Variables | Unmatched Matched | Mean | %Bias | %Reduct |Bias| | t-Test | ||

|---|---|---|---|---|---|---|---|

| Treated | Control | T | p > |t| | ||||

| lnSale | U | 21.39 | 21.35 | 2.500 | 35.20 | 1.730 | 0.0830 |

| M | 21.39 | 21.37 | 1.600 | 0.960 | 0.339 | ||

| ROA | U | 0.0427 | 0.0393 | 5.500 | 64.80 | 3.730 | 0 |

| M | 0.0427 | 0.0415 | 1.900 | 1.120 | 0.262 | ||

| Top | U | 0.350 | 0.350 | 0.300 | −400.6 | 0.180 | 0.856 |

| M | 0.350 | 0.348 | 1.300 | 0.780 | 0.433 | ||

| Lev | U | 0.396 | 0.415 | −9.200 | 90.70 | −6.290 | 0 |

| M | 0.396 | 0.397 | −0.900 | −0.510 | 0.608 | ||

| Cash | U | 0.0511 | 0.0503 | 1.200 | 59.70 | 0.790 | 0.430 |

| M | 0.0511 | 0.0508 | 0.500 | 0.280 | 0.783 | ||

| Boardsize | U | 2.123 | 2.143 | −9.800 | 76.10 | −6.770 | 0 |

| M | 2.123 | 2.119 | 2.300 | 1.390 | 0.166 | ||

| Growth | U | 0.244 | 0.227 | 2.900 | 59.90 | 1.970 | 0.0490 |

| M | 0.244 | 0.251 | −1.200 | −0.670 | 0.506 | ||

| (1) | (2) | (3) | (4) | |

|---|---|---|---|---|

| Variables | CP | CP | CP | CP |

| DID | 20.817 *** (4.78) | 16.181 *** (2.53) | 16.122 *** (2.72) | 15.516 *** (4.23) |

| NEDCP | 1.803 (2.29) | |||

| BCP | 1.636 (1.74) | |||

| CETP | −10.169 ** (4.11) | −6.402 *** (2.17) | −6.791 *** (2.08) | −9.268 ** (3.97) |

| LCCP | 1.312 (2.64) | 2.164 (2.38) | 2.014 (2.38) | 2.992 (2.27) |

| lnSale | 0.910 (1.31) | 1.749 * (0.99) | 1.749 * (0.99) | 1.107 (1.06) |

| ROA | 15.476 (11.47) | 21.224 *** (7.61) | 21.270 *** (7.63) | −0.538 (7.13) |

| Top | −20.777 ** (8.64) | −17.930 *** (6.49) | −17.836 *** (6.49) | −13.400 * (8.09) |

| Lev | 15.228 ** (6.74) | 15.693 *** (4.44) | 15.800 *** (4.39) | 10.145 * (5.17) |

| Cash | 7.602 (8.02) | 0.157 (5.24) | 0.218 (5.24) | 6.428 (5.39) |

| Boardsize | 5.455 (5.67) | 5.303 (3.31) | 5.335 (3.31) | 3.116 (3.71) |

| Growth | 0.985 (1.00) | 1.422 ** (0.71) | 1.423 ** (0.71) | 1.043 * (0.62) |

| constant | 1.593 (24.80) | −9.706 (21.09) | −9.806 (21.06) | 5.038 (24.09) |

| Year | Yes | Yes | Yes | Yes |

| Id | Yes | Yes | Yes | Yes |

| N | 13,956 | 20,673 | 20,673 | 17,358 |

| R2 | 0.158 | 0.158 | 0.158 | 0.122 |

| F | 34.687 | 62.423 | 55.288 | 51.275 |

| (1) | (2) | |

|---|---|---|

| Variables | DID | CP |

| River | 0.063 *** | |

| (0.010) | ||

| Ventilation | −0.087 * | |

| (0.051) | ||

| DID | 30.351 *** | |

| (11.119) | ||

| ROA | 0.063 | 19.665 ** |

| (0.052) | (7.927) | |

| lnSale | 0.019 *** | 1.331 |

| (0.007) | (0.974) | |

| Top | 0.008 | −17.859 *** |

| (0.063) | (6.409) | |

| Lev | 0.040 | 14.227 *** |

| (0.042) | (4.785) | |

| Cash | −0.017 | 0.781 |

| (0.025) | (5.287) | |

| Boardsize | −0.001 | 5.213 |

| (0.028) | (3.334) | |

| Growth | −0.001 | 1.483 ** |

| (0.004) | (0.735) | |

| Year | Yes | Yes |

| Id | Yes | Yes |

| Kleibergen–Paap rk LM | 6.138 ** | |

| Kleibergen–Paap rk Wald F | 20.251 | |

| 10% maximal IV size | 19.93 | |

| Hansen J (p-value) | 1.541 (0.2145) | |

| Obs | 20,389 | 20,389 |

| (1) | (2) | (3) | |

|---|---|---|---|

| Variables | CP | GP | CP |

| DID | 11.493 *** (2.71) | 0.010 ** (0.00) | 11.434 *** (2.71) |

| GP | 5.901 ** (2.55) | ||

| lnSale | 2.587 ** (1.09) | −0.001 (0.00) | 2.595 ** (1.09) |

| ROA | 26.344 *** (9.62) | 0.011 (0.02) | 26.277 *** (9.62) |

| Top | −20.050 ** (8.31) | −0.001 (0.03) | −20.044 ** (8.30) |

| Lev | 16.665 *** (4.55) | 0.006 (0.01) | 16.630 *** (4.54) |

| Cash | −1.132 (7.33) | 0.021 (0.02) | −1.256 (7.30) |

| Boardsize | 4.153 (3.65) | −0.007 (0.01) | 4.193 (3.64) |

| Growth | 0.388 (0.63) | −0.006 *** (0.00) | 0.423 (0.63) |

| constant | −26.525 (22.30) | 0.065 (0.08) | −26.907 (22.23) |

| Year | Yes | Yes | Yes |

| Id | Yes | Yes | Yes |

| N | 14,467 | 14,467 | 14,467 |

| R2 | 0.177 | 0.003 | 0.177 |

| F | 51.520 | 4.140 | 49.359 |

| (1) | (2) | (3) | (4) | (5) | (6) | (7) | |

|---|---|---|---|---|---|---|---|

| Variables | CP | CP | CP | CP | CP | CP | CP |

| DID | 10.515 *** (2.62) | −1.461 ** (0.56) | 8.541 *** (2.77) | 11.654 * (6.10) | −3.454 * (1.75) | −0.713 (1.21) | 12.821 *** (3.05) |

| lnSale | 0.868 (1.17) | −0.364 (0.34) | 0.762 (1.30) | 3.960 ** (1.89) | 1.645 (1.99) | 0.455 (0.65) | 1.143 (1.32) |

| ROA | 27.368 *** (9.20) | 3.700 (2.47) | 36.928 *** (11.54) | −10.888 (11.79) | 6.109 (10.06) | 16.858 *** (4.32) | 21.734 ** (9.41) |

| Top | −17.584 ** (8.56) | −2.069 (2.70) | −31.297 *** (9.11) | −0.341 (9.98) | 12.814 (10.78) | −8.809 (5.48) | −12.843 (8.64) |

| Lev | 14.564 *** (5.26) | 1.802 (1.36) | 20.966 *** (6.09) | 11.710 (8.49) | 1.639 (8.35) | 8.075 *** (2.38) | 14.482 ** (5.65) |

| Cash | −1.942 (6.67) | 2.977 (1.98) | 1.559 (7.25) | −0.793 (8.06) | −4.533 (11.95) | −4.903 * (2.94) | 4.077 (6.77) |

| Boardsize | 4.244 (3.88) | −1.275 (1.40) | 3.077 (4.67) | 11.535 ** (5.20) | 3.191 (6.82) | −0.828 (2.42) | 5.878 (4.20) |

| Growth | 1.455 (0.89) | 0.565 * (0.32) | 1.444 (1.00) | 0.673 (1.27) | 2.175 (1.32) | −0.046 (0.34) | 1.750 * (0.92) |

| constant | 10.798 (26.55) | 13.980 ** (7.03) | 16.421 (30.41) | −85.104 ** (40.05) | −30.375 (44.78) | 1.983 (14.86) | 3.008 (29.43) |

| Year | Yes | Yes | Yes | Yes | Yes | Yes | Yes |

| Id | Yes | Yes | Yes | Yes | Yes | Yes | Yes |

| N | 16,965 | 3571 | 13,770 | 3678 | 2999 | 5449 | 15,095 |

| R2 | 0.183 | 0.094 | 0.172 | 0.160 | 0.108 | 0.105 | 0.192 |

| F | 59.678 | 8.447 | 75.949 | 8.344 | 9.465 | 11.922 | 67.196 |

| P | 0.000 | 0.017 | 0.002 | 0.640 | 0.000 | ||

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2025 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Wu, G.; Feng, C.; Ling, S. The Synergistic Effect of the Dual Carbon Reduction Pilot on Corporate Carbon Performance: Empirical Evidence from Listed Manufacturing Companies. Sustainability 2025, 17, 4409. https://doi.org/10.3390/su17104409

Wu G, Feng C, Ling S. The Synergistic Effect of the Dual Carbon Reduction Pilot on Corporate Carbon Performance: Empirical Evidence from Listed Manufacturing Companies. Sustainability. 2025; 17(10):4409. https://doi.org/10.3390/su17104409

Chicago/Turabian StyleWu, Guantai, Chaowei Feng, and Shixian Ling. 2025. "The Synergistic Effect of the Dual Carbon Reduction Pilot on Corporate Carbon Performance: Empirical Evidence from Listed Manufacturing Companies" Sustainability 17, no. 10: 4409. https://doi.org/10.3390/su17104409

APA StyleWu, G., Feng, C., & Ling, S. (2025). The Synergistic Effect of the Dual Carbon Reduction Pilot on Corporate Carbon Performance: Empirical Evidence from Listed Manufacturing Companies. Sustainability, 17(10), 4409. https://doi.org/10.3390/su17104409