Impact of Climate Policy Uncertainty, Clean Energy Index, and Carbon Emission Allowance Prices on Bitcoin Returns

Abstract

1. Introduction

2. Literature Review

3. Materials and Methods

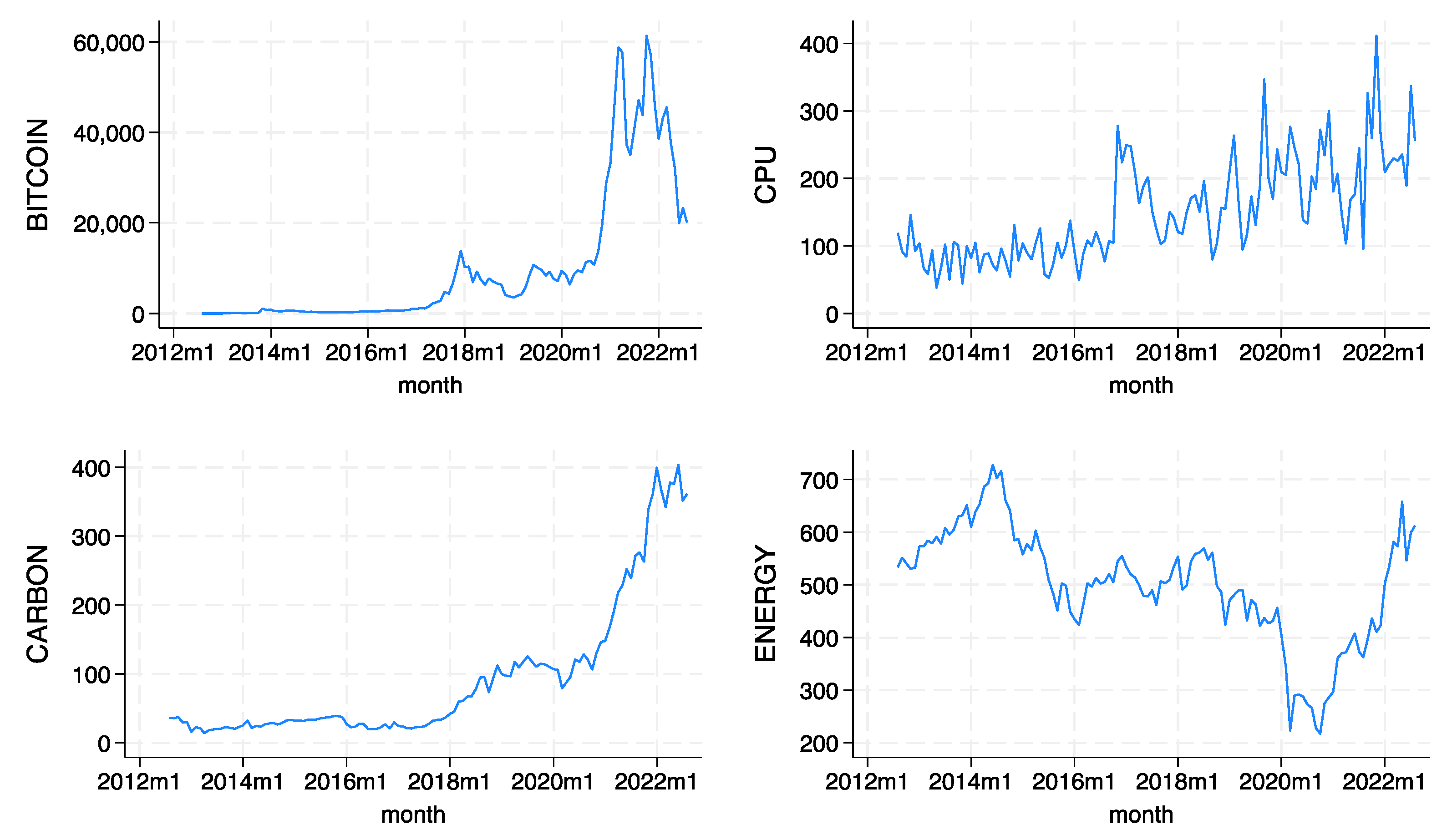

3.1. Materials

3.2. Methods

4. Results and Discussion

5. Conclusions and Policy Implications

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Conflicts of Interest

References

- IPCC. Summary for Policymakers. In Global Warming of 1.5 °C. An IPCC Special Report on the Impacts of Global Warming of 1.5 °C above Pre-Industrial Levels and Related Global Greenhouse Gas Emission Pathways, in the Context of Strengthening the Global Response to the Threat of Climate Change, Sustainable Development, and Efforts to Eradicate Poverty; Masson-Delmotte, V., Zhai, P., Pörtner, H.-O., Roberts, D., Skea, J., Shukla, P.R., Pirani, A., Moufouma-Okia, W., Péan, C., Pidcock, R., et al., Eds.; Cambridge University Press: Cambridge, UK; New York, NY, USA, 2018; pp. 3–24. [Google Scholar]

- IPCC. Climate Change 2022: Impacts, Adaptation, and Vulnerability. Contribution of Working Group II to the Sixth Assessment Report of the Intergovernmental Panel on Climate Change; Pörtner, H.-O., Roberts, D.C., Tignor, M., Poloczanska, E.S., Mintenbeck, K., Alegría, A., Craig, M., Langsdorf, S., Löschke, S., Möller, V., et al., Eds.; Cambridge University Press: Cambridge, UK, 2022. [Google Scholar]

- Tol, R.S.J. Poverty Traps and Climate Change. In ESRI Working Paper No. 413; The Economic and Social Research Institute: Dublin, Ireland, 2011. [Google Scholar]

- Bouri, E.; Iqbal, N.; Klein, T. Climate Policy Uncertainty and the Price Dynamics of Green and Brown Energy Stocks. Financ. Res. Lett. 2022, 47, 102740. [Google Scholar] [CrossRef]

- Ren, X.; Zhang, X.; Yan, C.; Gozgor, G. Climate Policy Uncertainty and Firm-Level Total Factor Productivity: Evidence from China. Energy Econ. 2022, 113, 106209. [Google Scholar] [CrossRef]

- Wu, Y.; Miao, C.; Fan, X.; Gou, J.; Zhang, Q.; Zheng, H. Quantifying the Uncertainty Sources of Future Climate Projections and Narrowing Uncertainties with Bias Correction Techniques. Earth’s Future 2022, 10, e2022EF002963. [Google Scholar] [CrossRef]

- Zhao, X. Do the Stock Returns of Clean Energy Corporations Respond to Oil Price Shocks and Policy Uncertainty? J. Econ. Struct. 2020, 9, 53. [Google Scholar] [CrossRef]

- Sarker, P.K.; Bouri, E.; Marco, C.K.L. Asymmetric Effects of Climate Policy Uncertainty, Geopolitical Risk, and Crude Oil Prices on Clean Energy Prices. Environ. Sci. Pollut. Res. 2023, 30, 15797–15807. [Google Scholar] [CrossRef] [PubMed]

- Xu, Y.; Li, M.; Yan, W.; Bai, J. Predictability of the Renewable Energy Market Returns: The Informational Gains from the Climate Policy Uncertainty. Resour. Polic. 2022, 79, 103141. [Google Scholar] [CrossRef]

- Lopez, J.M.R.; Sakhel, A.; Busch, T. Corporate Investments and Environmental Regulation: The Role of Regulatory Uncertainty, Regulation-Induced Uncertainty, and Investment History. Eur. Manag. J. 2017, 35, 91–101. [Google Scholar] [CrossRef]

- Liang, C.; Umar, M.; Ma, F.; Huynh, T.L.D. Climate Policy Uncertainty and World Renewable Energy Index Volatility Forecasting. Technol. Forecast. Soc. Chang. 2022, 182, 121810. [Google Scholar] [CrossRef]

- He, Y.; Zheng, H. Do Environmental Regulations Affect Firm Financial Distress in China? Evidence from Stock Markets. Appl. Econ. 2022, 54, 4384–4401. [Google Scholar] [CrossRef]

- Hsu, P.H.; Li, K.; Tsou, C.Y. The Pollution Premium. J. Financ. 2023, 78, 1343–1392. [Google Scholar] [CrossRef]

- Engle, R.F.; Giglio, S.; Kelly, B.; Lee, H.; Stroebel, J. Hedging Climate Change News. Rev. Financ. Stud. 2020, 33, 1184–1216. [Google Scholar] [CrossRef]

- Pástor, Ľ.; Stambaugh, R.F.; Taylor, L.A. Sustainable Investing in Equilibrium. J. Financ. Econ. 2021, 142, 550–571. [Google Scholar] [CrossRef]

- Jiang, S.; Li, Y.; Lu, Q.; Hong, Y.; Guan, D.; Xiong, Y.; Wang, S. Policy Assessments for the Carbon Emission Flows and Sustainability of Bitcoin Blockchain Operation in China. Nat. Commun. 2021, 12, 1938. [Google Scholar] [CrossRef] [PubMed]

- Xiao, Z.; Cui, S.; Xiang, L.; Liu, P.J.; Zhang, H. The Environmental Cost of Cryptocurrency: Assessing Carbon Emissions from Bitcoin Mining in China. J. Digit. Econ. 2023, 2, 119–136. [Google Scholar] [CrossRef]

- Kettner, C.; Kletzan-Slamanig, D. Is There Climate Policy Integration in European Union Energy Efficiency and Renewable Energy Policies? Yes, No, Maybe. Environ. Police Gov. 2020, 30, 141–150. [Google Scholar] [CrossRef]

- Le, T.-H.; Chang, Y.; Park, D. Renewable and Nonrenewable Energy Consumption, Economic Growth, and Emissions: International Evidence. Energy J. 2020, 41, 73–92. [Google Scholar] [CrossRef]

- Schlenker, W.; Taylor, C.A. Market Expectations of a Warming Climate. J. Financ. Econ. 2021, 142, 627–640. [Google Scholar] [CrossRef]

- Zhang, D.; Chen, X.H.; Lau, C.K.M.; Xu, B. Implications of Cryptocurrency Energy Usage on Climate Change. Technol. Forecast. Soc. Chang. 2023, 187, 122219. [Google Scholar] [CrossRef]

- Corbet, S.; Lucey, B.; Yarovaya, L. Bitcoin-Energy Markets Interrelationships—New Evidence. Resour. Police 2021, 70, 101916. [Google Scholar] [CrossRef]

- Gaies, B.; Nakhli, M.S.; Sahut, J.M.; Guesmi, K. Is Bitcoin Rooted in Confidence?—Unraveling the Determinants of Globalized Digital Currencies. Technol. Forecast. Soc. Chang. 2021, 172, 121038. [Google Scholar] [CrossRef]

- Baur, D.G.; Oll, J. Bitcoin Investments and Climate Change: A Financial and Carbon Intensity Perspective. Financ. Res. Lett. 2022, 47, 102575. [Google Scholar] [CrossRef]

- Yan, L.; Mirza, N.; Umar, M. The Cryptocurrency Uncertainties and Investment Transitions: Evidence from High and Low Carbon Energy Funds in China. Technol. Forecast. Soc. Chang. 2022, 175, 121326. [Google Scholar] [CrossRef]

- Gavriilidis, K. Measuring Climate Policy Uncertainty. SSRN Electron. J. 2021. [Google Scholar] [CrossRef]

- Baker, S.R.; Bloom, N.; Davis, S.J. Measuring Economic Policy Uncertainty*. Q. J. Econ. 2016, 131, 1593–1636. [Google Scholar] [CrossRef]

- Wenker, N. Online Currencies, Real-World Chaos: The Struggle to Regulate the Rise of Bitcoin. Tex. Rev. L. Pol. 2014, 19, 145. [Google Scholar]

- Grinberg, R. Bitcoin: An Innovative Alternative Digital Currency. Hastings Sci. Tech. L. J. 2012, 4, 159. [Google Scholar]

- Ciaian, P.; Rajcaniova, M.; Kancs, D. Virtual Relationships: Short- and Long-Run Evidence from BitCoin and Altcoin Markets. J. Int. Financ. Mark. Inst. Money 2018, 52, 173–195. [Google Scholar] [CrossRef]

- Przyłuska-Schmitt, J.; Jegorow, D.; Bučková, J. The Dynamics of Cryptocurrency Price Volatility in the Face of the Crisis on the Example of Bitcoin and Ethereum. Ann. Univ. Mariae Curie-Skłodowska Sect. H–Oeconomia 2023, 57, 101–113. [Google Scholar]

- Sehgal, S.; Pandey, P.; Diesting, F. Examining Dynamic Currency Linkages amongst South Asian Economies: An Empirical Study. Res. Int. Bus. Financ. 2017, 42, 173–190. [Google Scholar] [CrossRef]

- Corbet, S.; Lucey, B.; Urquhart, A.; Yarovaya, L. Cryptocurrencies as a Financial Asset: A Systematic Analysis. Int. Rev. Financ. Anal. 2019, 62, 182–199. [Google Scholar] [CrossRef]

- Elsayed, A.H.; Gozgor, G.; Lau, C.K.M. Causality and Dynamic Spillovers among Cryptocurrencies and Currency Markets. Int. J. Financ. Econ. 2022, 27, 2026–2040. [Google Scholar] [CrossRef]

- Paule-Vianez, J.; Prado-Román, C.; Gómez-Martínez, R. Economic Policy Uncertainty and Bitcoin. Is Bitcoin a Safe-Haven Asset? Eur. J. Manag. Bus. Econ. 2020, 29, 347–363. [Google Scholar] [CrossRef]

- Colon, F.; Kim, C.; Kim, H.; Kim, W. The Effect of Political and Economic Uncertainty on the Cryptocurrency Market. Financ. Res. Lett. 2021, 39, 101621. [Google Scholar] [CrossRef]

- Demir, E.; Gozgor, G.; Lau, C.K.M.; Vigne, S.A. Does Economic Policy Uncertainty Predict the Bitcoin Returns? An Empirical Investigation. Financ. Res. Lett. 2018, 26, 145–149. [Google Scholar] [CrossRef]

- Fang, L.; Bouri, E.; Gupta, R.; Roubaud, D. Does Global Economic Uncertainty Matter for the Volatility and Hedging Effectiveness of Bitcoin? Int. Rev. Financ. Anal. 2019, 61, 29–36. [Google Scholar] [CrossRef]

- Cai, Y.; Zhu, Z.; Xue, Q.; Song, X. Does Bitcoin Hedge against the Economic Policy Uncertainty: Based on the Continuous Wavelet Analysis. J. Appl. Econ. 2022, 25, 983–996. [Google Scholar] [CrossRef]

- Hung, N.T.; Huynh, T.L.D.; Nasir, M.A. Cryptocurrencies in an Uncertain World: Comprehensive Insights from a Wide Range of Uncertainty Indices. Int. J. Financ. Econ. 2023. [Google Scholar] [CrossRef]

- Lucey, B.M.; Vigne, S.A.; Yarovaya, L.; Wang, Y. The Cryptocurrency Uncertainty Index. Financ. Res. Lett. 2022, 45, 102147. [Google Scholar] [CrossRef]

- Wang, G.-J.; Xie, C.; Wen, D.; Zhao, L. When Bitcoin Meets Economic Policy Uncertainty (EPU): Measuring Risk Spillover Effect from EPU to Bitcoin. Financ. Res. Lett. 2019, 31. [Google Scholar] [CrossRef]

- de Vries, A. Bitcoin’s Growing Energy Problem. Joule 2018, 2, 801–805. [Google Scholar] [CrossRef]

- Browne, R. Bitcoin’s Wild Ride Renews Worries About Its Massive Carbon Footprint. CNBC Sustain. Energy Blog. 2021. Available online: https://www.cnbc.com/2021/02/05/bitcoin-btc-surge-renews-worries-about-its-massive-carbon-footprint.html (accessed on 3 February 2024).

- Mora, C.; Rollins, R.L.; Taladay, K.; Kantar, M.B.; Chock, M.K.; Shimada, M.; Franklin, E.C. Publisher Correction: Bitcoin Emissions Alone Could Push Global Warming above 2 °C. Nat. Clim. Chang. 2019, 9, 80. [Google Scholar] [CrossRef]

- Li, J.; Li, N.; Peng, J.; Cui, H.; Wu, Z. Energy Consumption of Cryptocurrency Mining: A Study of Electricity Consumption in Mining Cryptocurrencies. Energy 2019, 168, 160–168. [Google Scholar] [CrossRef]

- Wang, Y.; Lucey, B.; Vigne, S.A.; Yarovaya, L. An Index of Cryptocurrency Environmental Attention (ICEA). China Financ. Rev. Int. 2022, 12, 378–414. [Google Scholar] [CrossRef]

- Baur, D.G.; Oll, J. The (Un-)Sustainability of Bitcoin Investments. SSRN Electron. J. 2019. [Google Scholar] [CrossRef]

- Egiyi, M.A.; Ofoegbu, G.N. Cryptocurrency and Climate Change: An Overview. Int. J. Mech. Eng. Technol. 2020, 11, 15–22. [Google Scholar]

- Masanet, E.; Shehabi, A.; Lei, N.; Vranken, H.; Koomey, J.; Malmodin, J. Implausible Projections Overestimate Near-Term Bitcoin CO2 Emissions. Nat. Clim. Chang. 2019, 9, 653–654. [Google Scholar] [CrossRef]

- Huynh, T.L.D.; Ahmed, R.; Nasir, M.A.; Shahbaz, M.; Huynh, N.Q.A. The Nexus between Black and Digital Gold: Evidence from US Markets. Ann. Oper. Res. 2024, 334, 521–546. [Google Scholar] [CrossRef] [PubMed]

- Umar, M.; Ji, X.; Kirikkaleli, D.; Alola, A.A. The Imperativeness of Environmental Quality in the United States Transportation Sector amidst Biomass-Fossil Energy Consumption and Growth. J. Clean. Prod. 2021, 285, 124863. [Google Scholar] [CrossRef]

- Goodkind, A.L.; Jones, B.A.; Berrens, R.P. Cryptodamages: Monetary Value Estimates of the Air Pollution and Human Health Impacts of Cryptocurrency Mining. Energy Res. Soc. Sci. 2020, 59, 101281. [Google Scholar] [CrossRef]

- Yan, W.-L.; Cheung, A. The Dynamic Spillover Effects of Climate Policy Uncertainty and Coal Price on Carbon Price: Evidence from China. Financ. Res. Lett. 2023, 53, 103400. [Google Scholar] [CrossRef]

- Stoll, C.; Klaaßen, L.; Gallersdörfer, U. The Carbon Footprint of Bitcoin. Joule 2019, 3, 1647–1661. [Google Scholar] [CrossRef]

- Dogan, E.; Majeed, M.T.; Luni, T. Are Clean Energy and Carbon Emission Allowances Caused by Bitcoin? A Novel Time-Varying Method. J. Clean. Prod. 2022, 347, 131089. [Google Scholar] [CrossRef]

- Magazzino, C.; Bekun, F.V.; Etokakpan, M.U.; Uzuner, G. Modeling the Dynamic Nexus among Coal Consumption, Pollutant Emissions and Real Income: Empirical Evidence from South Africa. Environ. Sci. Pollut. Res. 2020, 27, 8772–8782. [Google Scholar] [CrossRef] [PubMed]

- Sailor, D.J.; Smith, M.; Hart, M. Climate Change Implications for Wind Power Resources in the Northwest United States. Renew. Energy 2008, 33, 2393–2406. [Google Scholar] [CrossRef]

- Venturini, A. Climate Change, Risk Factors and Stock Returns: A Review of the Literature. Int. Rev. Financ. Anal. 2022, 79, 101934. [Google Scholar] [CrossRef]

- Bartram, S.M.; Hou, K.; Kim, S. Real Effects of Climate Policy: Financial Constraints and Spillovers. J. Financ. Econ. 2022, 143, 668–696. [Google Scholar] [CrossRef]

- Diaz-Rainey, I.; Gehricke, S.A.; Roberts, H.; Zhang, R. Trump vs. Paris: The Impact of Climate Policy on US Listed Oil and Gas Firm Returns and Volatility. Int. Rev. Financ. Anal. 2021, 76, 101746. [Google Scholar] [CrossRef]

- Nam, K. Investigating the Effect of Climate Uncertainty on Global Commodity Markets. Energy Econ. 2021, 96, 105123. [Google Scholar] [CrossRef]

- Tian, H.; Long, S.; Li, Z. Asymmetric Effects of Climate Policy Uncertainty, Infectious Diseases-Related Uncertainty, Crude Oil Volatility, and Geopolitical Risks on Green Bond Prices. Financ. Res. Lett. 2022, 48, 103008. [Google Scholar] [CrossRef]

- Hoque, M.E.; Soo-Wah, L.; Bilgili, F.; Ali, M.H. Connectedness and Spillover Effects of US Climate Policy Uncertainty on Energy Stock, Alternative Energy Stock, and Carbon Future. Environ. Sci. Pollut. Res. 2023, 30, 18956–18972. [Google Scholar] [CrossRef] [PubMed]

- Febo, E.D.; Ortolano, A.; Foglia, M.; Leone, M.; Angelini, E. From Bitcoin to Carbon Allowances: An Asymmetric Extreme Risk Spillover. J. Environ. Manag. 2021, 298, 113384. [Google Scholar] [CrossRef]

- Cheng, Y.; Gu, B.; Tan, X.; Yan, H.; Sheng, Y. Allocation of Provincial Carbon Emission Allowances under China’s 2030 Carbon Peak Target: A Dynamic Multi-Criteria Decision Analysis Method. Sci. Total Environ. 2022, 837, 155798. [Google Scholar] [CrossRef] [PubMed]

- Enders, W.; Lee, J. The Flexible Fourier Form and Dickey–Fuller Type Unit Root Tests. Econ. Lett. 2012, 117, 196–199. [Google Scholar] [CrossRef]

- Enders, W.; Jones, P. Grain Prices, Oil Prices, and Multiple Smooth Breaks in a VAR. Stud. Nonlinear Dyn. Econ. 2016, 20, 399–419. [Google Scholar] [CrossRef]

- Toda, H.Y.; Yamamoto, T. Statistical Inference in Vector Autoregressions with Possibly Integrated Processes. J. Econ. 1995, 66, 225–250. [Google Scholar] [CrossRef]

- Pesaran, M.H.; Shin, Y.; Smith, R.J. Bounds Testing Approaches to the Analysis of Level Relationships. J. Appl. Econom. 2001, 16, 289–326. [Google Scholar] [CrossRef]

- McNown, R.; Sam, C.Y.; Goh, S.K. Bootstrapping the Autoregressive Distributed Lag Test for Cointegration. Appl. Econ. 2018, 50, 1509–1521. [Google Scholar] [CrossRef]

- Solarin, S.A. Modelling the Relationship between Financing by Islamic Banking System and Environmental Quality: Evidence from Bootstrap Autoregressive Distributive Lag with Fourier Terms. Qual. Quant. 2019, 53, 2867–2884. [Google Scholar] [CrossRef]

- Yilanci, V.; Bozoklu, S.; Gorus, M.S. Are BRICS Countries Pollution Havens? Evidence from a Bootstrap ARDL Bounds Testing Approach with a Fourier Function. Sustain. Cities Soc. 2020, 55, 102035. [Google Scholar] [CrossRef]

- Becker, R.; Enders, W.; Lee, J. A Stationarity Test in the Presence of an Unknown Number of Smooth Breaks. J. Time Ser. Anal. 2006, 27, 381–409. [Google Scholar] [CrossRef]

- Ludlow, J.; Enders, W. Estimating Non-Linear ARMA Models Using Fourier Coefficients. Int. J. Forecast. 2000, 16, 333–347. [Google Scholar] [CrossRef]

- Granger, C.W.J. Investigating Causal Relations by Econometric Models and Cross-Spectral Methods. Econometrica 1969, 37, 424. [Google Scholar] [CrossRef]

- Sims, C.A. Macroeconomics and Reality. Econometrica 1980, 48, 1. [Google Scholar] [CrossRef]

- Gallant, R. On the Basis in Flexible Functional Form and an Essentially Unbiased Form: The Flexible Fourier Form. J. Econom. 1981, 15, 211–245. [Google Scholar] [CrossRef]

- Nazlioglu, S.; Gormus, N.A.; Soytas, U. Oil Prices and Real Estate Investment Trusts (REITs): Gradual-Shift Causality and Volatility Transmission Analysis. Energy Econ. 2016, 60, 168–175. [Google Scholar] [CrossRef]

{kind=link}

| Var. | Abbr. | Srcs. | Samps. |

|---|---|---|---|

| Climate policy uncertainty | CPU | www.policyuncertainty.com (accessed on 3 February 2024) | [4,61,62,63] |

| S&P 500 Enegy Index | ENERGY | www.spglobal.com (accessed on 3 February 2024) | [9,13,57,59,60] |

| Carbon Emission Allowance | CARBON | www.spglobal.com (accessed on 3 February 2024) | [56,65,66] |

| Bitcoin | BITCOIN | www.investing.com (accessed on 1 February 2024) | [55,56] |

| BTC | CARBON | CPU | ENERGY | |

|---|---|---|---|---|

| Mean | 10,061.50 | 92.94 | 150.361 | 499.58 |

| Median | 3501.10 | 36.60 | 131.14 | 505.45 |

| Maximum | 61,330.00 | 403.40 | 411.29 | 727.63 |

| Minimum | 10.20 | 13.96 | 38.09 | 216.82 |

| Std. Dev. | 15,420.92 | 102.53 | 74.55 | 108.88 |

| Skewness | 1.86 | 1.73 | 0.87 | −0.54 |

| Kurtosis | 5.36 | 4.96 | 3.38 | 3.16 |

| Level | First Diff. | |

|---|---|---|

| BTC | −2.89 (3) | −8.61 (3) *** |

| CPU | −5.77 (4) *** | - |

| CARBON | −0.42 (3) | −13.07 (3) *** |

| ENERGY | −1.68 (2) | −12.56 (2) *** |

| Selected Model: FARDL (2, 1, 2, 2) k:3 | ||||

|---|---|---|---|---|

| Test Statistic | Bootstrap Critical Values | |||

| %10 | %5 | %1 | ||

| Fa | 6.509 *** | 3.375 | 3.843 | 5.581 |

| T | −2.819 * | −2.786 | −3.021 | −3.961 |

| Fb | 7.635 *** | 3.663 | 4.201 | 4.908 |

| Variable | Coefficient | Standard Error | p-Value |

|---|---|---|---|

| lnCARBON | 1.30 | 0.245 | 0.00 |

| lnCPU | 1.23 | 0.41 | 0.00 |

| lnENERGY | −0.61 | 0.23 | 0.01 |

| Method | Test Statistics | Asymptotic p-Value | Bootstrap p-Value | |

|---|---|---|---|---|

| lnBTC → lnCARBON | FGC | 8.287 | 0.406 | 0.411 |

| lnCarbon → lnBTC | FGC | 14.491 | 0.07 * | 0.087 * |

| lnBTC → lnCPU | FTY | 4.582 | 0.032 ** | 0.036 ** |

| lnCPU → lnBTC | FTY | 0.004 | 0.951 | 0.957 |

| lnBTC → lnENERGY | FGC | 3.319 | 0.068 * | 0.065 * |

| lnENERGY → lnBTC | FGC | 0.760 | 0.383 | 0.392 |

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2024 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Gürsoy, S.; Jóźwik, B.; Dogan, M.; Zeren, F.; Gulcan, N. Impact of Climate Policy Uncertainty, Clean Energy Index, and Carbon Emission Allowance Prices on Bitcoin Returns. Sustainability 2024, 16, 3822. https://doi.org/10.3390/su16093822

Gürsoy S, Jóźwik B, Dogan M, Zeren F, Gulcan N. Impact of Climate Policy Uncertainty, Clean Energy Index, and Carbon Emission Allowance Prices on Bitcoin Returns. Sustainability. 2024; 16(9):3822. https://doi.org/10.3390/su16093822

Chicago/Turabian StyleGürsoy, Samet, Bartosz Jóźwik, Mesut Dogan, Feyyaz Zeren, and Nazligul Gulcan. 2024. "Impact of Climate Policy Uncertainty, Clean Energy Index, and Carbon Emission Allowance Prices on Bitcoin Returns" Sustainability 16, no. 9: 3822. https://doi.org/10.3390/su16093822

APA StyleGürsoy, S., Jóźwik, B., Dogan, M., Zeren, F., & Gulcan, N. (2024). Impact of Climate Policy Uncertainty, Clean Energy Index, and Carbon Emission Allowance Prices on Bitcoin Returns. Sustainability, 16(9), 3822. https://doi.org/10.3390/su16093822