The Impact of Corporate Social Responsibility Implementation on Enterprises’ Financial Performance—Evidence from Chinese Listed Companies

Abstract

1. Introduction

2. Theoretical Foundations

2.1. Corporate Social Responsibility

2.2. The Relationship between CSR and CFP

2.2.1. The Social Impact Hypothesis

2.2.2. The Trade-Off Hypothesis

2.2.3. The Ambiguous Relationship

3. Research Methodology

3.1. Measures

3.1.1. Corporate Financial Performance

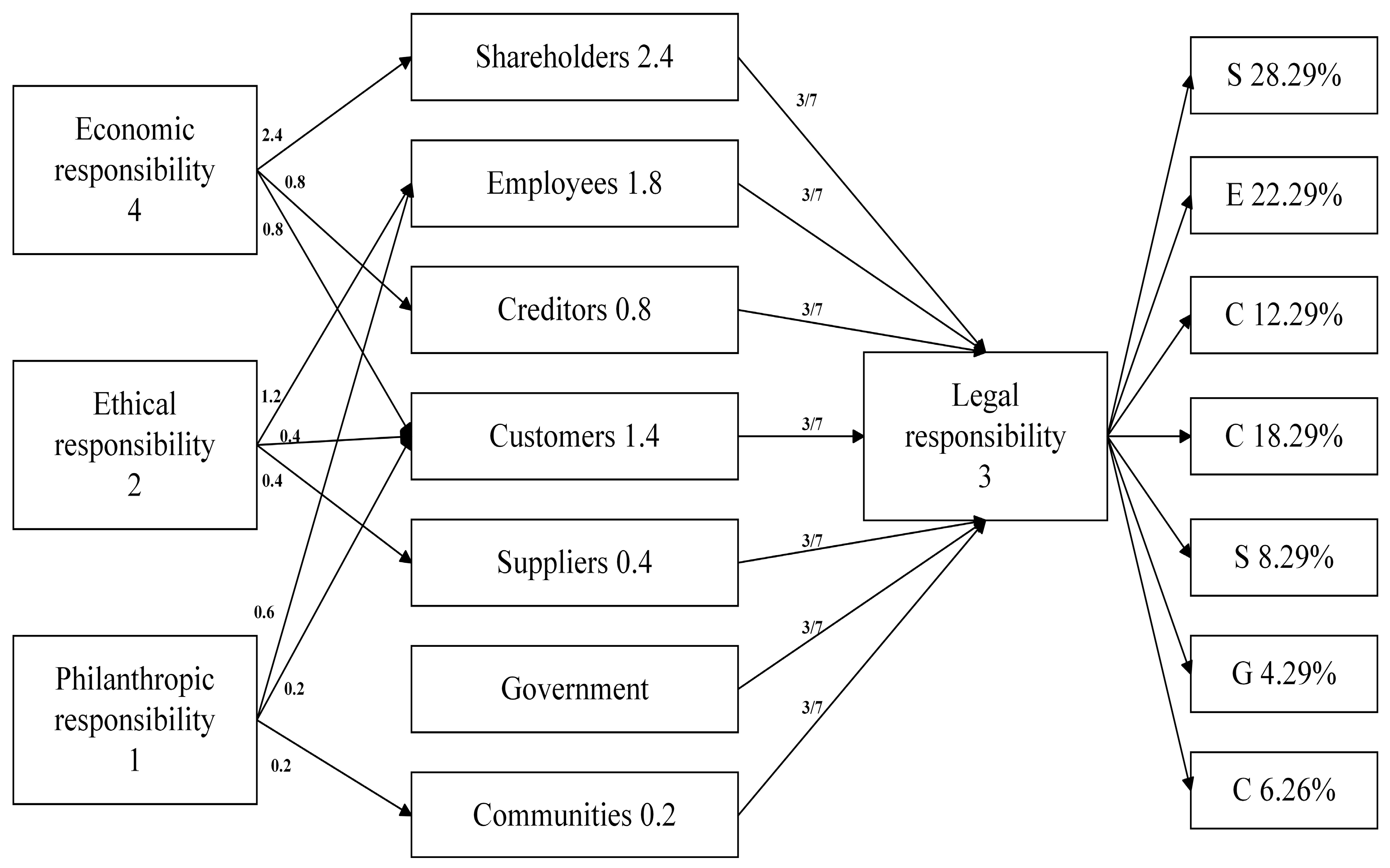

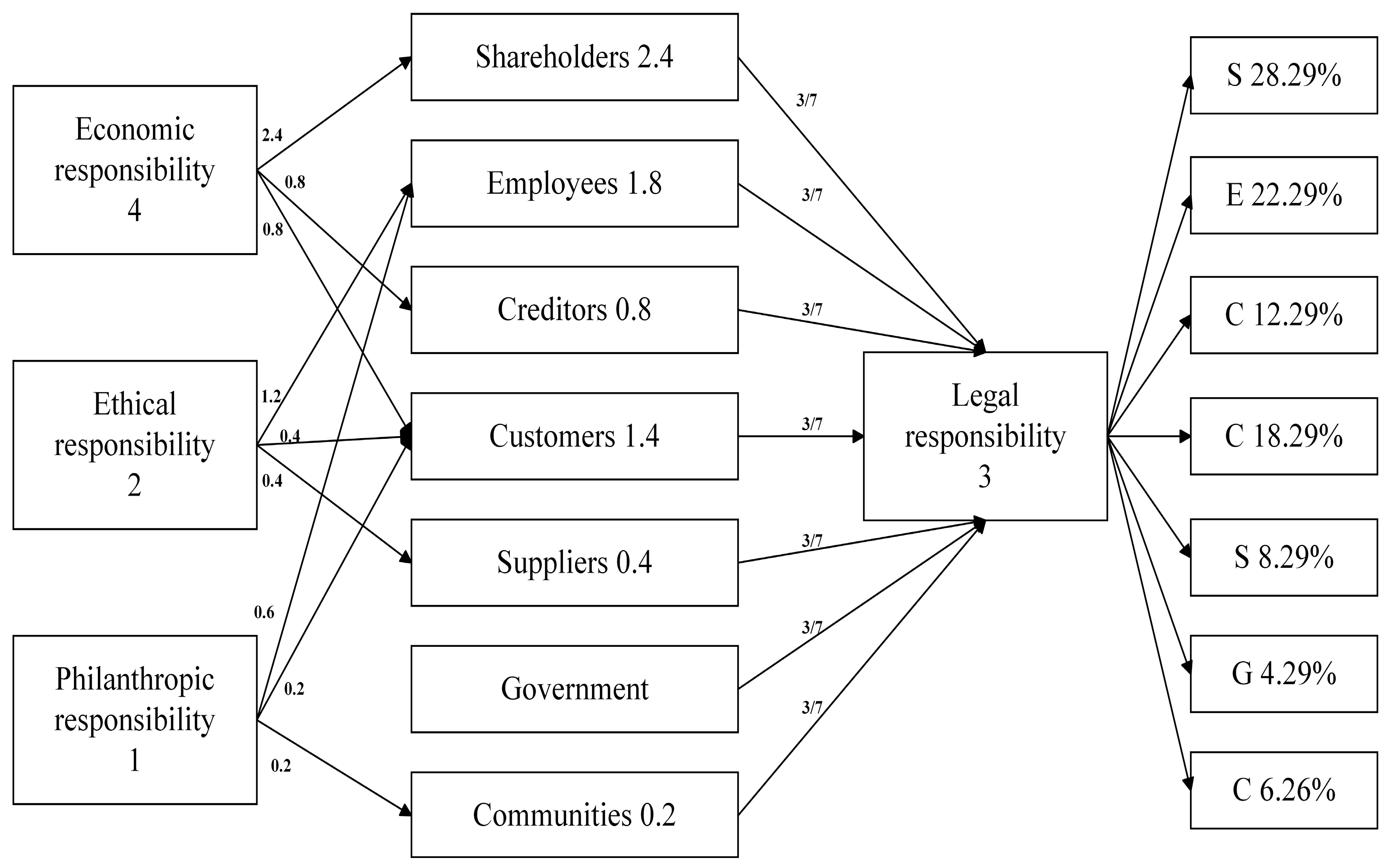

3.1.2. Corporate Social Responsibility

- (1)

- Responsibility to shareholders (SHR)

- (2)

- Responsibility to creditors (CRR)

- (3)

- Responsibility to customers (CUR)

- (4)

- Responsibility to suppliers (SUR)

- (5)

- Responsibility to employees (EMR)

- (6)

- Responsibility to government (GOR)

- (7)

- Responsibility to communities (CMR)

3.1.3. Mediating Variable and Overall CSR Gauge

3.1.4. Control Variables

3.2. Data Collection

4. Results

4.1. Descriptive Statistics

4.2. Testing of Hypotheses

4.3. Testing of Mediation Effect

4.4. Robustness Check

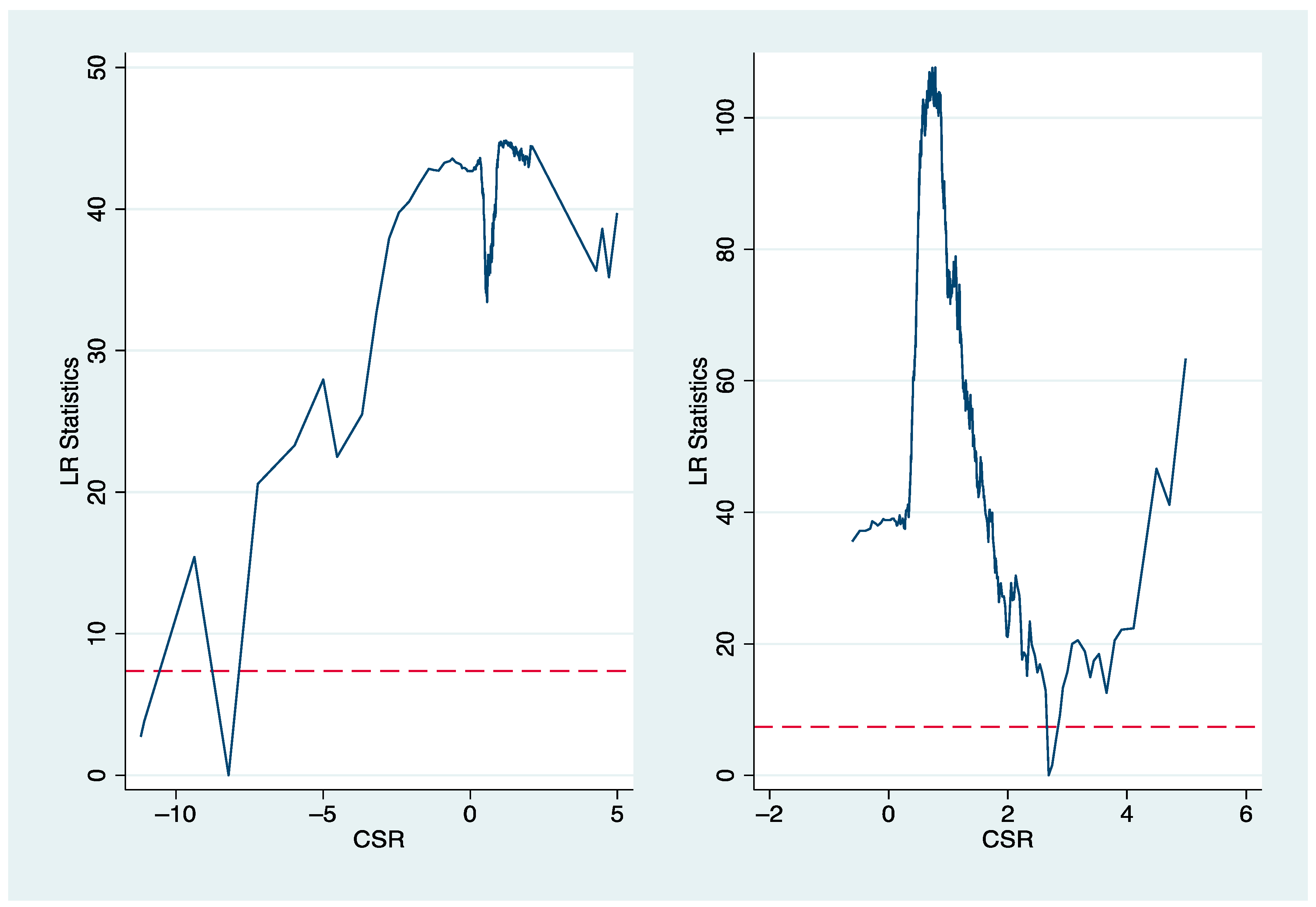

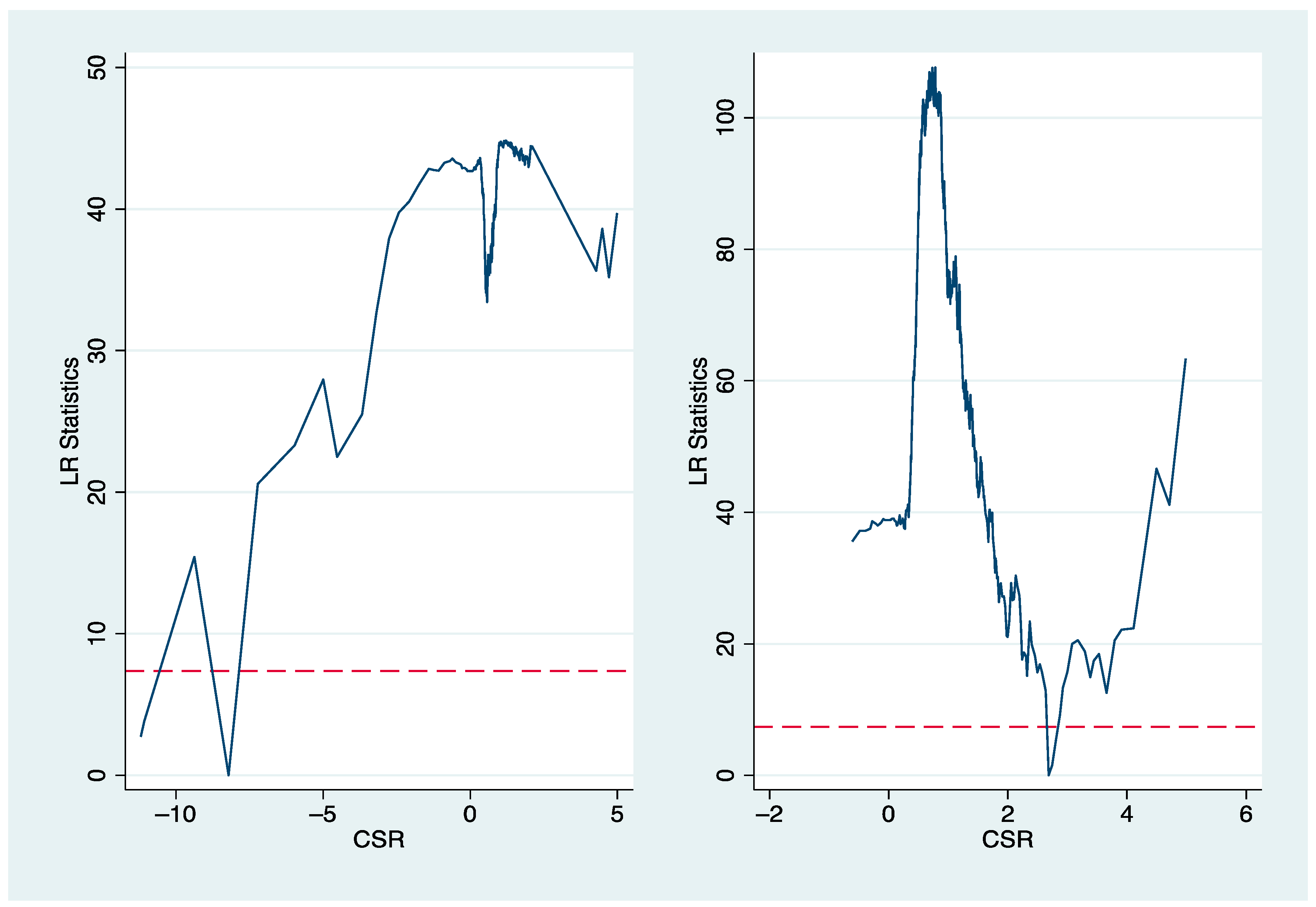

4.5. Testing of Threshold Effect

5. Discussion

5.1. Theoretical Implications

5.2. Managerial Implications

5.3. Limitations and Future Research

6. Conclusions

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Conflicts of Interest

References

- Lee, M.D.P. A review of the theories of corporate social responsibility: Its evolutionary path and the road ahead. Int. J. Manag. Rev. 2008, 10, 53–73. [Google Scholar] [CrossRef]

- McWilliams, A.; Siegel, D.S.; Wright, P.M. Corporate social responsibility: Strategic implications. J. Manag. Stud. 2006, 43, 1–18. [Google Scholar] [CrossRef]

- Coelho, R.; Jayantilal, S.; Ferreira, J.J. The impact of social responsibility on corporate financial performance: A systematic literature review. Corp. Soc. Responsib. Environ. Manag. 2023, 30, 1535–1560. [Google Scholar] [CrossRef]

- Kane, G. Three Secrets of Green Business: Unlocking Competitive Advantage in a Low Carbon Economy; Routledge: London, UK, 2009. [Google Scholar]

- Harjoto, M.; Laksmana, I. The impact of corporate social responsibility on risk taking and firm value. J. Bus. Ethics 2018, 151, 353–373. [Google Scholar] [CrossRef]

- Kao, E.H.; Yeh, C.C.; Wang, L.H.; Fung, H.G. The relationship between CSR and performance: Evidence in China. Pac.-Basin Financ. J. 2018, 51, 155–170. [Google Scholar] [CrossRef]

- Margolis, J.D.; Walsh, J.P. Misery loves companies: Rethinking social initiatives by business. Adm. Sci. Q. 2003, 48, 268–305. [Google Scholar] [CrossRef]

- Pava, M.L.; Krausz, J. The association between corporate social-responsibility and financial performance: The paradox of social cost. J. Bus. Ethics 1996, 15, 321–357. [Google Scholar] [CrossRef]

- Stanwick, P.A.; Stanwick, S.D. The relationship between corporate social performance, and organizational size, financial performance, and environmental performance: An empirical examination. J. Bus. Ethics 1998, 17, 195–204. [Google Scholar] [CrossRef]

- Campbell, D.; Moore, G.; Metzger, M. Corporate philanthropy in the UK 1985–2000 some empirical findings. J. Bus. Ethics 2002, 39, 29–41. [Google Scholar] [CrossRef]

- Wu, C.F. The relationship of ethical decision-making to business ethics and performance in Taiwan. J. Bus. Ethics 2002, 35, 163–176. [Google Scholar] [CrossRef]

- Benlemlih, M. Corporate social responsibility and firm financing decisions: A literature review. J. Multinatl. Financ. Manag. 2017, 42–43, 1–10. [Google Scholar] [CrossRef]

- Zhu, Q.; Liu, J.; Lai, K.H. Corporate social responsibility practices and performance improvement among Chinese national state-owned enterprises. Int. J. Prod. Econ. 2016, 171, 417–426. [Google Scholar] [CrossRef]

- Partalidou, X.; Zafeiriou, E.; Giannarakis, G.; Sariannidis, N. The effect of corporate social responsibility performance on financial performance: The case of food industry. Benchmarking Int. J. 2020, 27, 2701–2720. [Google Scholar] [CrossRef]

- Barnett, M.L.; Salomon, R.M. Does it pay to be really good? Addressing the shape of the relationship between social and financial performance. Strateg. Manag. J. 2012, 33, 1304–1320. [Google Scholar] [CrossRef]

- Nollet, J.; Filis, G.; Mitrokostas, E. Corporate social responsibility and financial performance: A non-linear and disaggregated approach. Econ. Model. 2016, 52, 400–407. [Google Scholar] [CrossRef]

- Deng, X.; Long, X.; Schuler, D.A.; Luo, H.; Zhao, X. External corporate social responsibility and labor productivity: AS-curve relationship and the moderating role of internal CSR and government subsidy. Corp. Soc. Responsib. Environ. Manag. 2020, 27, 393–408. [Google Scholar] [CrossRef]

- Long, W.; Li, S.; Wu, H.; Song, X. Corporate social responsibility and financial performance: The roles of government intervention and market competition. Corp. Soc. Responsib. Environ. Manag. 2020, 27, 525–541. [Google Scholar] [CrossRef]

- Kong, Y.; Antwi-Adjei, A.; Bawuah, J. A systematic review of the business case for corporate social responsibility and firm performance. Corp. Soc. Responsib. Environ. Manag. 2020, 27, 444–454. [Google Scholar] [CrossRef]

- Chen, L.; Feldmann, A.; Tang, O. The relationship between disclosures of corporate social performance and financial performance: Evidences from GRI reports in manufacturing industry. Int. J. Prod. Econ. 2015, 170, 445–456. [Google Scholar] [CrossRef]

- Soytas, M.A.; Denizel, M.; Usar, D.D. Addressing endogeneity in the causal relationship between sustainability and financial performance. Int. J. Prod. Econ. 2019, 210, 56–71. [Google Scholar] [CrossRef]

- Yang, Y.; Lau, A.K.; Lee, P.K.; Cheng, T.C.E. The performance implication of corporate social responsibility in matched Chinese small and medium-sized buyers and suppliers. Int. J. Prod. Econ. 2020, 230, 107796. [Google Scholar] [CrossRef]

- Okafor, A.; Adeleye, B.N.; Adusei, M. Corporate social responsibility and financial performance: Evidence from US tech firms. J. Clean. Prod. 2021, 292, 126078. [Google Scholar] [CrossRef]

- Eabrasu, M. Post hoc ergo propter hoc: Methodological limits of performance-oriented studies in CSR. Bus. Ethics A Eur. Rev. 2015, 24, S11–S23. [Google Scholar] [CrossRef]

- Cho, S.Y.; Lee, C. Managerial efficiency, corporate social performance, and corporate financial performance. J. Bus. Ethics 2019, 158, 467–486. [Google Scholar] [CrossRef]

- Jamali, D.; Safieddine, A.M.; Rabbath, M. Corporate governance and corporate social responsibility synergies and interrelationships. Corp. Gov. Int. Rev. 2008, 16, 443–459. [Google Scholar] [CrossRef]

- Ip, P.K. The challenge of developing a business ethics in China. J. Bus. Ethics 2009, 88, 211–224. [Google Scholar] [CrossRef]

- Kuo, T.C.; Chen, H.M.; Meng, H.M. Do corporate social responsibility practices improve financial performance? A case study of airline companies. J. Clean. Prod. 2021, 310, 127380. [Google Scholar] [CrossRef]

- Van Beurden, P.; Gössling, T. The worth of values–a literature review on the relation between corporate social and financial performance. J. Bus. Ethics 2008, 82, 407–424. [Google Scholar] [CrossRef]

- Bowen, H.R. Social Responsibilities of the Businessman; Harper & Row: New York, NY, USA, 1953. [Google Scholar]

- Friedman, M. Capitalism and Freedom; University of Chicago Press: Chicago, IL, USA, 1962. [Google Scholar]

- Carroll, A.B. A three-dimensional conceptual model of corporate performance. Acad. Manag. Rev. 1979, 4, 497–505. [Google Scholar] [CrossRef]

- Carroll, A.B. The pyramid of corporate social responsibility: Toward the moral management of organizational stakeholders. Bus. Horiz. 1991, 34, 39–48. [Google Scholar] [CrossRef]

- Kotler, P.; Lee, N. Corporate Social Responsibility: Doing the Most Good for Your Company and Your Cause; John Wiley & Sons: Hoboken, NJ, USA, 2005. [Google Scholar]

- Kramer, M.R.; Porter, M.E. Strategy and society: The link between competitive advantage and corporate social responsibility. Harv. Bus. Rev. 2006, 84, 78–92. [Google Scholar]

- Lindgreen, A.; Swaen, V. Corporate social responsibility. Int. J. Manag. Rev. 2010, 12, 1–7. [Google Scholar] [CrossRef]

- Vogel, D.J. Is there a market for virtue?: The business case for corporate social responsibility. Calif. Manag. Rev. 2005, 47, 19–45. [Google Scholar]

- Preston, L.E.; O’bannon, D.P. The corporate social-financial performance relationship: A typology and analysis. Bus. Soc. 1997, 36, 419–429. [Google Scholar] [CrossRef]

- Cornell, B.; Shapiro, A.C. Corporate stakeholders and corporate finance. Financ. Manag. 1987, 16, 5–14. [Google Scholar] [CrossRef]

- Waddock, S.A.; Graves, S.B. The corporate social performance–financial performance link. Strateg. Manag. J. 1997, 18, 303–319. [Google Scholar] [CrossRef]

- ISO26000; Social Responsibility. ISO: Geneva, Switzerland, 2010.

- Moon, J.; Shen, X. CSR in China research: Salience, focus and nature. J. Bus. Ethics 2010, 94, 613–629. [Google Scholar] [CrossRef]

- Marquis, C.; Qian, C. Corporate social responsibility reporting in China: Symbol or substance? Organ. Sci. 2014, 25, 127–148. [Google Scholar] [CrossRef]

- Shu, C.; Zhou, K.Z.; Xiao, Y.; Gao, S. How green management influences product innovation in China: The role of institutional benefits. J. Bus. Ethics 2016, 133, 471–485. [Google Scholar] [CrossRef]

- Peng, H.; Wei, F. An empirical study on the correlation between government subsidies and corporate social responsibility of manufacturing enterprises. Comm Financ Acc. 2013, 12, 68–70. [Google Scholar]

- Lee, E.; Walker, M.; Zeng, C.C. Do Chinese state subsidies affect voluntary corporate social responsibility disclosure? J. Account. Public Policy 2017, 36, 179–200. [Google Scholar] [CrossRef]

- Ji, H.; Miao, Z. Corporate social responsibility and collaborative innovation: The role of government support. J. Clean. Prod. 2020, 260, 121028. [Google Scholar] [CrossRef]

- Li, M.; Cao, G.; Cui, L.; Liu, X.; Dai, J. Examining how government subsidies influence firms’ circular supply chain management: The role of eco-innovation and top management team. Int. J. Prod. Econ. 2023, 261, 108893. [Google Scholar] [CrossRef]

- Li, W.; Zhang, R. Corporate social responsibility, ownership structure, and political interference: Evidence from China. J. Bus. Ethics 2010, 96, 631–645. [Google Scholar] [CrossRef]

- Sheng, S.; Zhou, K.Z.; Li, J.J. The effects of business and political ties on firm performance: Evidence from China. J. Mark. 2011, 75, 1–15. [Google Scholar] [CrossRef]

- Vance, S.C. Are socially responsible corporations good investment risks. Manag. Rev. 1975, 64, 19–24. [Google Scholar]

- Aupperle, K.E.; Carroll, A.B.; Hatfield, J.D. An empirical examination of the relationship between corporate social responsibility and profitability. Acad. Manag. J. 1985, 28, 446–463. [Google Scholar] [CrossRef]

- McGuire, J.B.; Sundgren, A.; Schneeweis, T. Corporate social responsibility and firm financial performance. Acad. Manag. J. 1988, 31, 854–872. [Google Scholar] [CrossRef]

- Makni, R.; Francoeur, C.; Bellavance, F. Causality between corporate social performance and financial performance: Evidence from Canadian firms. J. Bus. Ethics 2009, 89, 409–422. [Google Scholar] [CrossRef]

- Barnea, A.; Rubin, A. Corporate social responsibility as a conflict between shareholders. J. Bus. Ethics 2010, 97, 71–86. [Google Scholar] [CrossRef]

- Brammer, S.; Brooks, C.; Pavelin, S. Corporate social performance and stock returns: UK evidence from disaggregate measures. Financ. Manag. 2006, 35, 97–116. [Google Scholar] [CrossRef]

- McWilliams, A.; Siegel, D. Corporate social responsibility and financial performance: Correlation or misspecification? Strateg. Manag. J. 2000, 21, 603–609. [Google Scholar] [CrossRef]

- Surroca, J.; Tribó, J.A.; Waddock, S. Corporate responsibility and financial performance: The role of intangible resources. Strateg. Manag. J. 2010, 31, 463–490. [Google Scholar]

- McWilliams, A.; Siegel, D. Corporate social responsibility: A theory of the firm perspective. Acad. Manag. Rev. 2001, 26, 17–127. [Google Scholar] [CrossRef]

- Mahoney, L.; Roberts, R.W. Corporate social performance, financial performance and institutional ownership in Canadian firms. Account. Forum 2007, 31, 233–253. [Google Scholar] [CrossRef]

- Griffin, J.J.; Mahon, J.F. The corporate social performance and corporate financial performance debate: Twenty-five years of incomparable research. Bus. Soc. 1997, 36, 5–31. [Google Scholar] [CrossRef]

- Orlitzky, M.; Schmidt, F.L.; Rynes, S.L. Corporate social and financial performance: A meta-analysis. Organ. Stud. 2003, 24, 403–441. [Google Scholar] [CrossRef]

- Davidson, W.N.; Worrell, D.L. A comparison and test of the use of accounting and stock-market data in relating corporate social-responsibility and financial performance. Akron Bus. Econ. Rev. 1990, 21, 7–19. [Google Scholar]

- Cochran, P.L.; Wood, R.A. Corporate social responsibility and financial performance. Acad. Manag. J. 1984, 27, 42–56. [Google Scholar] [CrossRef]

- Zhao, Z.; Zhao, X.; Zuo, J. Corporate social responsibility construction system in construction enterprises. Constr. Econ. 2009, 10, 45–47. [Google Scholar]

- Ren, L.; Zhao, J. An Empirical Study of Relationship Between Corporate Social Responsibility and Financial Performance. J. Chongqing Jiaotong Univ. 2009, 9, 60–65. [Google Scholar]

- Zhao, Z.; Zhao, X.; Davidson, K.; Zuo, J. A corporate social responsibility indicator system for construction enterprises. J. Clean. Prod. 2012, 29, 277–289. [Google Scholar]

- Wen, S.; Fang, Y. An Empirical Research on Relationship between Corporate Social Responsibility and Financial Performance- Analysis Based on Stakeholder Theory and Panel Data. China Ind. Econ. 2008, 150–160. Available online: https://xueshu.baidu.com/usercenter/paper/show?paperid=5b3ddb7beaa947f1b5f8632def4ed8fa (accessed on 8 December 2023).

- Zhang, L.; Yuan, D.; Niu, D.; Jin, Y. An Empirical Research on the Effect of CSR on CFP- Based on Listed Companies in China. J. Northeast. Univ. (Nat. Sci.) 2011, 32, 292–296. [Google Scholar]

- Dou, X. The Lagging Effects of the Influence of Corporate Social Responsibility on Corporate Financial Performance- Empirical Analysis Based on the Panel Data of Chinese Listed Companies. Ind. Econ. Res. 2015, 3, 74–81. [Google Scholar]

- Pletnev, D.; Barkhatov, V. Business success of small and medium sized enterprises in Russia and social responsibility of managers. Procedia-Soc. Behav. Sci. 2016, 221, 185–193. [Google Scholar] [CrossRef]

- Xin, J. CSR performance evaluation indicators based on stakeholder perspective. Shandong Soc. Sci. 2008, 11, 83–86. [Google Scholar]

- Cramer, J. Experiences with structuring corporate social responsibility in Dutch industry. J. Clean. Prod. 2005, 13, 583–592. [Google Scholar] [CrossRef]

- Li, S.; Song, X.; Wu, H. Political connection, ownership structure, and corporate philanthropy in China: A strategic-political perspective. J. Bus. Ethics 2015, 129, 399–411. [Google Scholar] [CrossRef]

- Baltagi, B.H.; Bresson, G.; Pirotte, A. Fixed effects, random effects or Hausman–Taylor?: A pretest estimator. Econ. Lett. 2003, 79, 361–369. [Google Scholar] [CrossRef]

- Xu, Q.; Lu, Y.; Lin, H.; Li, B. Does corporate environmental responsibility (CER) affect corporate financial performance? Evidence from the global public construction firms. J. Clean. Prod. 2021, 315, 128131. [Google Scholar] [CrossRef]

- Hasan, I.; Kobeissi, N.; Liu, L.; Wang, H. Corporate social responsibility and firm financial performance: The mediating role of productivity. J. Bus. Ethics 2018, 149, 671–688. [Google Scholar] [CrossRef]

- Hansen, B.E. Threshold effects in non-dynamic panels: Estimation, testing, and inference. J. Econom. 1999, 93, 345–368. [Google Scholar] [CrossRef]

- Myers, R.H. Classical and Modern Regression with Applications; Duxbury Press: Belmont, CA, USA, 1990. [Google Scholar]

- Muller, D.; Judd, C.M.; Yzerbyt, V.Y. When moderation is mediated and mediation is moderated. J. Personal. Soc. Psychol. 2005, 89, 852. [Google Scholar] [CrossRef] [PubMed]

- Lucas, M.T.; Noordewier, T.G. Environmental management practices and firm financial performance: The moderating effect of industry pollution-related factors. Int. J. Prod. Econ. 2016, 175, 24–34. [Google Scholar] [CrossRef]

- Porter, M.E.; Kramer, M.R. Creating shared value: How to reinvent capitalism—And unleash a wave of innovation and growth. In Managing Sustainable Business: An Executive Education Case and Textbook; Springer: Dordrecht, The Netherlands, 2018; pp. 323–346. [Google Scholar]

- Zhao, Y.; Cao, J.; Lu, L. The Influence of Corporate Social Responsibility on the Green Innovation Performance- Empirical Analysis Based on Threshold Effect. Innov. Sci. Technol. 2022, 22, 71–83. [Google Scholar]

- Jo, H.; Harjoto, M.A. The causal effect of corporate governance on corporate social responsibility. J. Bus. Ethics 2012, 106, 53–72. [Google Scholar] [CrossRef]

- Centobelli, P.; Cerchione, R.; Esposito, E.; Passaro, R. Determinants of the transition towards circular economy in SMEs: A sustainable supply chain management perspective. Int. J. Prod. Econ. 2021, 242, 108297. [Google Scholar] [CrossRef]

- Yin, J.; Huang, G.; Xie, Y.; An, C.; Chen, X. An inexact two-stage multi-objective waste management planning model under considerations of subsidies and uncertainties: A case study of Baotou, China. J. Clean. Prod. 2021, 298, 126873. [Google Scholar] [CrossRef]

- Jones, T.M. Instrumental stakeholder theory: A synthesis of ethics and economics. Acad. Manag. Rev. 2016, 20, 404–437. [Google Scholar] [CrossRef]

- Le, T.T.; Huan, N.Q.; Hong, T.T.T.; Tran, D.K. The contribution of corporate social responsibility on SMEs performance in emerging country. J. Clean. Prod. 2021, 322, 129103. [Google Scholar]

- Burbano, V. The effect of corporate philanthropy on organizational citizenship behavior and employee performance. Acad. Manag. Proc. 2014, 2014, 13872. [Google Scholar] [CrossRef]

- Lee, Y.K.; Choi, J.; Moon, B.Y.; Babin, B.J. Codes of ethics, corporate philanthropy, and employee responses. Int. J. Hosp. Manag. 2014, 39, 97–106. [Google Scholar] [CrossRef]

- Duch, N.; Montolio, D.; Mediavilla, M. Evaluating the impact of public subsidies on a firm’s performance: A two-stage quasi-experimental approach. Investig. Reg.-J. Reg. Res. 2009, 39, 143–165. [Google Scholar]

- Lim, C.; Wang, J.; Zeng, C. China’s “mercantilist” government subsidies, the cost of debt and firm performance. J. Bank. Financ. 2018, 86, 37–52. [Google Scholar] [CrossRef]

- Allen, F.; Qian, J.; Qian, M. Law, finance, and economic growth in China. J. Financ. Econ. 2005, 77, 57–116. [Google Scholar] [CrossRef]

- Derwall, J.; Guenster, N.; Bauer, R.; Koedijk, K. The eco-efficiency premium puzzle. Financ. Anal. J. 2005, 61, 51–63. [Google Scholar] [CrossRef]

{kind=link}

{kind=link}

| Type | Code | Name | Indicator | Calculation Method |

|---|---|---|---|---|

| Dependent Variable | CFP | Corporate financial performance | Return on assets | Net income/Total assets |

| Independent Variables | SHR | Responsibility to shareholders | Earnings per share growth rate | (Earnings per share for current period-Earnings per share for last period)/Earnings per share for last period |

| CRR | Responsibility to creditors | Current ratio | Current assets/Current liabilities | |

| CUR | Responsibility to customers | Cost of main business ratio | Main business cost/Main business income | |

| SUR | Responsibility to suppliers | Accounts payable turnover ratio | Main business cost/Accounts payable | |

| EMR | Responsibility to employees | Employee profitability level | Employees’ salary/Net revenue | |

| GOR | Responsibility to government | Asset tax rate | Total taxes/Total assets | |

| CMR | Responsibility to communities | Social donation expenditure rate | Social donation expenditure/Main business income | |

| Mediating Variable | GS | Government subsidy | / | / |

| Threshold Variable | CSRCI | CSR comprehensive index | The weighted score of different stakeholders | / |

| Control Variables | SIZE | Firm size | / | Natural logarithm of total assets |

| RDI | Intensity of research and development | / | Expenditure on R&D/Main business income |

| N | SD | Mean | Min | Max | Median | |

|---|---|---|---|---|---|---|

| ROA | 27,684 | 0.089 | 0.0452 | −0.3961 | 0.2717 | 0.0463 |

| SHR | 27,683 | 5.3057 | −0.5303 | −40 | 14.129 | 0 |

| CRR | 27,685 | 2.4839 | 2.6013 | 0.3325 | 15.6897 | 1.7874 |

| CUR | 27,684 | 0.1872 | 0.6836 | 0.1169 | 1.0139 | 0.7164 |

| SUR | 27,664 | 10.8186 | 7.3111 | 0.4405 | 79.6351 | 4.2417 |

| EMR | 23,208 | 0.0146 | 0.0062 | −0.0282 | 0.0925 | 0.0023 |

| GOR | 23,217 | 0.0053 | 0.0050 | 0.0003 | 0.0386 | 0.0037 |

| CMR | 15,334 | 0.001 | 0.0005 | 0 | 0.0068 | 0.0001 |

| CSRCI | 15,331 | 2.0825 | 0.9231 | −11.1922 | 9.7152 | 0.7888 |

| GS | 23,045 | 5027.3255 | 1731.1160 | 0 | 37,836.891 | 202.71 |

| SIZE | 23,217 | 1.31 | 22.2550 | 19.8569 | 26.3729 | 22.0545 |

| RDI | 21,085 | 0.0564 | 0.0547 | 0.0002 | 0.3292 | 0.04 |

| ROA | SHR | CRR | CUR | SUR | EMR | GOR | CMR | CSRCI | GS1 | SIZE | RDI | |

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| ROA | 1 | 0.18 *** | 0.42 *** | −0.45 *** | 0.17 *** | 0.15 *** | 0.23 *** | 0.11 *** | 0.33 *** | 0.00 | −0.12 *** | 0.07 *** |

| SHR | 0.35 *** | 1 | 0.08 *** | −0.05 *** | −0.09 *** | 0.05 *** | −0.00 | −0.02 ** | 0.56 *** | 0.02 ** | −0.04 *** | 0.06 *** |

| CRR | 0.23 *** | 0.05 *** | 1 | −0.43 *** | 0.11 *** | 0.24 *** | 0.01 | 0.12 *** | 0.41 *** | −0.10 *** | −0.48 *** | 0.34 *** |

| CUR | −0.34 *** | −0.06 *** | −0.39 *** | 1 | 0.23 *** | −0.15 *** | −0.12 *** | −0.27 *** | 0.01 | 0.02 ** | 0.24 *** | −0.40 *** |

| SUR | 0.04 *** | −0.00 | 0.09 *** | 0.21 *** | 1 | 0.03 *** | 0.21 *** | −0.04 *** | 0.55 *** | −0.04 *** | −0.03 *** | −0.29 *** |

| EMR | 0.03 *** | 0.10 *** | 0.07 *** | −0.02 ** | −0.01 | 1 | −0.01 | 0.06 *** | 0.15 *** | −0.09 *** | −0.41 *** | 0.18 *** |

| GOR | 0.13 *** | 0.03 *** | −0.07 *** | −0.15 *** | 0.03 *** | −0.05 *** | 1 | 0.04 *** | 0.08 *** | −0.02 ** | −0.04 *** | −0.16 *** |

| CMR | 0.02 *** | −0.01 | 0.12 *** | −0.27 *** | −0.04 *** | 0.01 | 0.03 *** | 1 | −0.03 *** | 0.02 ** | −0.06 *** | 0.08 *** |

| CSRCI | 0.32 *** | 0.85 *** | 0.23 *** | −0.00 | 0.46 *** | 0.09 *** | 0.02 *** | −0.01 | 1 | −0.05 *** | −0.17 *** | −0.06 *** |

| GS | 0.03 *** | 0.02 *** | −0.11 *** | 0.06 *** | 0.00 | −0.09 *** | 0.07 *** | −0.02 ** | 0.00 | 1 | 0.28 *** | 0.04 *** |

| SIZE | −0.01 | 0.01 | −0.36 *** | 0.22 *** | 0.00 | −0.27 *** | 0.12 *** | −0.06 *** | −0.04 *** | 0.42 *** | 1 | −0.34 *** |

| RDI | −0.07 *** | −0.00 | 0.28 *** | −0.44 *** | −0.15 *** | 0.07 *** | −0.17 *** | 0.12 *** | −0.02 *** | 0.00 | −0.25 *** | 1 |

| (1) | (2) | (3) | (4) | |

|---|---|---|---|---|

| ROA | ROA | ROA | ROA | |

| SHR | 0.003 *** | 0.003 *** | 0.003 *** | |

| (36.063) | (36.256) | (35.691) | ||

| CRR | 0.002 *** | 0.003 *** | 0.002 *** | |

| (3.694) | (5.302) | (2.956) | ||

| CUR | −0.399 *** | −0.384 *** | −0.428 *** | |

| (−46.030) | (−44.369) | (−45.670) | ||

| SUR | 0.001 *** | 0.001 *** | 0.001 *** | |

| (12.634) | (12.568) | (9.704) | ||

| EMR | 0.326 *** | 0.343 *** | 0.316 *** | |

| (7.520) | (7.998) | (7.286) | ||

| GOR | 0.639 *** | 1.332 *** | 1.346 *** | |

| (2.654) | (5.471) | (4.649) | ||

| CMR | −3.995 *** | −3.797 *** | −3.423 *** | |

| (−5.719) | (−5.485) | (−4.843) | ||

| CSRCI | 0.011 *** | |||

| (34.486) | ||||

| SIZE | 0.030 *** | 0.023 *** | 0.028 *** | |

| (14.406) | (10.876) | (12.362) | ||

| RDI | −0.628 *** | −0.724 *** | ||

| (−22.139) | (−23.033) | |||

| _cons | 0.305 *** | −0.368 *** | −0.155 *** | −0.546 *** |

| (46.422) | (−7.806) | (−3.200) | (−10.789) | |

| Year fixed effects | Yes | Yes | Yes | Yes |

| Firm fixed effects | Yes | Yes | Yes | Yes |

| N | 15,331 | 15,331 | 14,057 | 14,057 |

| r2 | 0.282 | 0.295 | 0.349 | 0.186 |

| p | 0.000 | 0.000 | 0.000 | 0.000 |

| F | 367.680 | 361.593 | 390.522 | 292.175 |

| (1) | (2) | (3) | |

|---|---|---|---|

| ROA | GS | ROA | |

| CSRCI | 0.011 *** | 7.363 | 0.011 *** |

| (34.486) | (0.359) | (34.401) | |

| SIZE | 0.028 *** | 1316.413 *** | 0.028 *** |

| (12.362) | (8.952) | (12.218) | |

| RDI | −0.724 *** | 3272.657 | −0.725 *** |

| (−23.033) | (1.620) | (−23.006) | |

| GS | 0.000 | ||

| (0.837) | |||

| _cons | −0.546 *** | −2.81 × 104 *** | −0.543 *** |

| (−10.789) | (−8.619) | (−10.656) | |

| Year fixed effects | Yes | Yes | Yes |

| Firm fixed effects | Yes | Yes | Yes |

| N | 14,057 | 14,006 | 14,006 |

| r2 | 0.186 | 0.052 | 0.187 |

| p | 0.000 | 0.000 | 0.000 |

| F | 292.175 | 69.812 | 259.147 |

| (1) | (2) | (3) | |

|---|---|---|---|

| ROE | ROE | ROA-Base | |

| SHR | 0.007 *** | ||

| (28.927) | |||

| CRR | −0.001 | ||

| (−0.610) | |||

| CUR | −0.911 *** | ||

| (−38.645) | |||

| SUR | 0.002 *** | ||

| (6.638) | |||

| EMR | 0.934 *** | ||

| (8.564) | |||

| GOR | 2.100 *** | ||

| (2.884) | |||

| CMR | −9.229 *** | ||

| (−5.192) | |||

| CSRCI | 0.022 *** | 0.011 *** | |

| (28.846) | (34.486) | ||

| SIZE | 0.036 *** | 0.050 *** | 0.028 *** |

| (6.853) | (8.919) | (12.362) | |

| RDI | −1.268 *** | −1.460 *** | −0.724 *** |

| (−17.771) | (−19.017) | (−23.033) | |

| _cons | −0.071 | −0.968 *** | −0.546 *** |

| (−0.584) | (−7.830) | (−10.789) | |

| Year fixed effects | Yes | Yes | Yes |

| Firm fixed effects | Yes | Yes | Yes |

| N | 14,057 | 14,057 | 14,057 |

| r2 | 0.264 | 0.133 | 0.186 |

| p | 0.000 | 0.000 | 0.000 |

| F | 261.506 | 195.118 | 292.175 |

| Type of Threshold | Bootstrap Times | F-Value | p-Value | Critical Value | ||

|---|---|---|---|---|---|---|

| 10% | 5% | 1% | ||||

| Single | 300 | 158.23 | 0.000 | 7.416 | 9.624 | 13.377 |

| Double | 300 | 44.850 | 0.000 | 9.505 | 10.825 | 17.680 |

| Triple | 300 | 16.960 | 0.410 | 29.784 | 34.666 | 40.484 |

| Type of Threshold | Threshold Value | 95% Confidence Interval |

|---|---|---|

| First threshold | −8.208 | [−11.072, −7.210] |

| Second threshold | 2.687 | [2.637, 2.742] |

| (1) | |

|---|---|

| ROA | |

| SIZE | 0.015 *** |

| (6.422) | |

| RDI | −0.834 *** |

| (−21.905) | |

| CSRCI (CSRCI ≤ −8.208) | 0.012 *** |

| (24.753) | |

| CSRCI (−8.208 < CSRCI ≤ 2.687) | 0.018 *** |

| (22.697) | |

| CSRCI (CSRCI > 2.687) | 0.006 *** |

| (8.716) | |

| _cons | −0.263 *** |

| (−5.141) | |

| r2 | 0.200 |

| F | 374.200 |

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2024 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Li, X.; Esfahbodi, A.; Zhang, Y. The Impact of Corporate Social Responsibility Implementation on Enterprises’ Financial Performance—Evidence from Chinese Listed Companies. Sustainability 2024, 16, 1848. https://doi.org/10.3390/su16051848

Li X, Esfahbodi A, Zhang Y. The Impact of Corporate Social Responsibility Implementation on Enterprises’ Financial Performance—Evidence from Chinese Listed Companies. Sustainability. 2024; 16(5):1848. https://doi.org/10.3390/su16051848

Chicago/Turabian StyleLi, Xudong, Ali Esfahbodi, and Yufeng Zhang. 2024. "The Impact of Corporate Social Responsibility Implementation on Enterprises’ Financial Performance—Evidence from Chinese Listed Companies" Sustainability 16, no. 5: 1848. https://doi.org/10.3390/su16051848

APA StyleLi, X., Esfahbodi, A., & Zhang, Y. (2024). The Impact of Corporate Social Responsibility Implementation on Enterprises’ Financial Performance—Evidence from Chinese Listed Companies. Sustainability, 16(5), 1848. https://doi.org/10.3390/su16051848