1. Introduction

The dynamics of economic globalization and integration increase the circulation of goods all over the world, affecting businesses and the overall economy. Among limited resources, laying a strategy and developing a business that is responsive to these changes effectively should be attended, especially the development of sustainable logistic facilities to support operation [

1]. Sustainable development (SD) is an action that balances social, environmental, and economic dimensions in sustainable development from three aspects [

2].

Sustainable green logistics can be evaluated through the long-term performance of a company, where green logistics encompasses the relationships among the economy, the environment, society, logistics, and transportation networks as well as information sharing. An analysis of the impact of green logistics on the entire logistics system and business operations is crucial when supporting an investment decision, selecting strategies in business development, and promoting environmentally and socially friendly development in the long run [

3]. The assessment and forecasting of the performance of 16 green logistics companies in the United States support investors and shareholders in the selection of the right logistics partners to improve business performance and reduce the impact on climate change. This action also helps decision-makers to select appropriate business partners that meet the requirements and achieve economic benefits from the aspect of sustainable development. The identification of appropriate and eco-friendly logistics operations [

4] significantly reduces the impacts caused by changes in social development, population, and climate. Designing a sustainable logistics business can accommodate the challenges to create a more flexible supply chain [

5].

Sustainable development, logistics, and supply chains are increasingly integrated into three interconnected and specific global research areas. To adapt and mitigate logistic issues in business operations [

6], the concept of sustainable supply chain management (SSCM) has emerged. SSCM involves manufacturing products and rendering services while considering the three dimensions of sustainability: society; environment; and economy, while including the needs and trusts of customers and stakeholders as well as corporate social responsibility and eco-friendly operations. This approach enables businesses to maintain sustainable growth and survive under the changes in external factors [

7]. SSCM can also identify the obstacles related to the major three aspects. Moreover, a lack of transparency in a supply chain may occur at the supplier or sub-supplier level in developing countries, where environmental, social, and regulatory impacts might be overlooked or not fully acknowledged as well as non-compliance with existing regulations [

8].

In addition to logistics businesses, sustainability also plays a part in strategic planning in the public sector to support and promote the growth of small and medium-sized enterprises [

9]. As supply chains are integral to business operations, SSCM can be applied when designing corporate strategy and creating practices that are environmentally and socially friendly for sustainable development.

This study is expected to provide understanding of the balance between society, the environment, and the economy for sustainable development. By assessing a company’s long-term performance, this study investigates the impact of SSCM on overall business, leading to the appropriate management and promotion of development that is environmentally and socially friendly.

While existing studies have examined various aspects of SSCM, there is still a lack of research from an institution and policy perspective. This perspective is crucial for business operations under SSCM, especially in developing countries where regulations are not fully or consistently enforced. This study aims to investigate the long-term performance of companies that implement SSCM and contribute valuable insights to investors, public authorities, and stakeholders. This study also identifies factors impacting the operation under SSCM.

In this research, the data were compiled from experts in businesses through a questionnaire structured on a 5-point Likert Scale. The experts were sampled under the snowball sampling method. After obtaining the answers, the scores were then analyzed using descriptive statistics and confirmatory analysis, exploratory factor analysis, factor analysis, and structural equation modeling (SEM).

To fill the academic gap, this research presents a model of sustainable supply chain management for business operations (SSCM-B). The model is expected to support the development of business towards sustainability in all relevant dimensions. For further details, this article is structured as follows: Part 1 introduces new in-depth knowledge about sustainable supply chain management, then Part 2 describes the literature review and hypotheses. Next, Part 3 describes the methodology and Part 4 presents the results of the study. Afterwards, Part 5 discusses the new perspectives and elaborates on the impact of this study. Finally, Part 6 summarizes the findings, limitations, and future work.

2. Literature Review

Supply Chain Management and Sustainability

One of the definitions of a supply chain is an arrangement in a company to provide goods in response to customer demands. This conventional definition is developed with a presumption that goods are transported from manufacturers to wholesalers, retailers, and consumers, respectively [

10].

In recent years, an increase and diversification in consumer demands has led to the integration of supply chain management (“SCM”) with business processes to enable a company to grow sustainably while maintaining integrity with ethical standards. This integration is highly important as it enables a business to deal with the changes in the environment and the market effectively and efficiently. In general, SCM expedites the time taken for supplier selection, allowing a company to work with a partner who strives for sustainable development [

11].

Moreover, SCM plays a crucial role in promoting sustainability by focusing on exploiting resources without harming the environment or the resource itself. The concept is important nowadays as environmental problems result in significant impacts to humans and the world [

12]. Practically, SCM balances cost, buyers, purchasers, and greenhouse gas emissions by implementing a policy on carbon credit and credit trading to control gas production [

13]. Nowadays, SSCM is widely recognized in academia and society. A discussion of SSCM is generally part of a strategy to create transparency from the aspects of society, the environment, and the economy for businesses to perform effectively and sustainably [

14]. Therefore, SSCM is gaining more and more recognition along with the need to audit and assess the work process of suppliers. This practice leads to a connection between supply chain management and business operations to support sustainability and reduce the impacts on the environment effectively. Furthermore, an efficient supply chain enables a business to grow sustainably while mitigating the risks to the environment and the economy that may occur in the future [

15]. From a social dimension, SD involves the social responsibility of an organization to communities concerning equality in education, access to resources in society, health, welfare, and improvements in quality of life. From an environmental dimension, SD relates to an environmental responsibility to communities and sustainability by monitoring the quality of air and water, energy usage, and the treatment of natural resources, disposals, hazardous wastes, and land utilization. From an economic dimension, SD leads to business accomplishments in response to shareholder expectations, leading to an increase in profits and stock value. To enable sustainable development from the three perspectives [

16], institution and policy has played a role through the enactment of laws and regulations for the effective use of resources [

17]. Sustainable development does not involve only an institution or a specific company, it also covers the collaboration between public and private sectors to create a guideline on policy and regulations for sustainable operation with a focus on long-term adjustment. Hence, the perspective of institution and policy is separately discussed to emphasize the significance of policy, regulation, and organizational structure that supports and stimulates sustainable development effectively. With a focus on responsibility in operations with achievable results in all perspectives of sustainable supply chain management for business operations (SSCM-B), the researcher has set the hypotheses as follows.

Hypothesis 1 (H1). The proposed SSCM-B model is consistent with the empirical data.

Hypothesis 2 (H2). The economic dimension correlates with the social dimension.

Hypothesis 3 (H3). The economic dimension correlates with the institution and policy dimension.

Hypothesis 4 (H4). The economic dimension correlates with the environmental dimension.

Hypothesis 5 (H5). The social dimension correlates with the institution and policy dimension.

Hypothesis 6 (H6). The social dimension perspective correlates with the environmental dimension.

Hypothesis 7 (H7). The institution and policy dimension correlates with the environmental dimension.

Based on the existing theory of SSCM that integrates sustainability with the practices in a supply chain to mitigate risks and gain trusts from customers, this research assesses the long-term performance of a company with contributions to investors, public authorities, and stakeholders. This research also identifies the factors that impact the operation under SSCM as shown in the literature reviews on

Table 1. The literature review was conducted on 30 articles on the new paradigm of sustainable supply chain management in various types of businesses to provide a comprehensive view and understanding for appropriate analysis.

3. Methodology

3.1. Index of Item–Objective Congruence

Index of Item–Objective Congruence (IOC) is a statistical method used to measure congruence between the items in the questionnaire and objectives or the preset indicators. The objectives were presented to three experts during data-assessment process to verify the quality of the questionnaire, which is the instrument deployed in this study. The verification focused on the validity of the content, where the IOC index should be greater than 0.5. In this study, the IOC value of all questions ranged between 0.67 and 1.00 as specified by Rovinelli and Hambleton [

45], hence it was considered valid. The organization committing to using eco-friendly equipment [

17] is one of the factors influencing sustainable supply chain management activities for business operations, as presented in

Table A1.

3.2. Inferential Statistics

Inferential statistics is another statistical method used in this research. It involves the analysis of SEM through exploratory factor analysis (EFA), an exploratory method to analyze data structure and group variables. It tests construct validity that is designed for unstructured data or data without predefined theory by grouping highly correlated variables into one factor. Then, the process moves to confirmatory factor analysis (CFA), which is designed to verify and confirm hypotheses and structural factors recommended by EFA or other theories. Afterwards, latent variables are considered to verify structure and correlation of the proposed variables. Thereafter, the hypothetical model is assessed of its fit with data through the Absolute Fit Index and Incremental Fit Index. The Absolute Fit Index includes CMIN/DF, RMSEA, GFI, AGFI, and RMR; where the Incremental Fit Index consists of NFI, TLI, CFI, and IFI. In this study, the data were gathered through the questionnaire from relevant samples comprising government agencies, entrepreneurs, and stakeholders. Under Cochran’s formula, as shown in formula [

46], the sample size was defined to be a minimum of 400 people.

where

n is a sample size; e is a margin error;

p is a fraction of population; and z is standard error at the chosen level of confidence of 95% or the level of significance at 0.05.

Next, SEM was analyzed by AMOS 26 software to examine validity and reliability, where the acceptable Composite Reliability (C.R.) should not be than 0.7. Moreover, convergent validity was considered from the Average Variance Extracted evaluation (AVE), which should not be less than 0.5. Furthermore, discriminant validity was conducted to assess whether the observed variables could be clearly distinguished from other latent variables. In detail, the variables in each factor were also examined for their correlation with factor loading, C.R., and AVE. When AVE was greater than the Maximum Shared Squared Variance (MSV) and the Cronbach’s Alpha, an indicator for internal consistency of related variables in a dataset, was greater than 0.7, the instrument was considered as highly reliable [

47,

48]. All statistical analyses were performed using SPSS Statistics 26.0.

4. Data Analysis and Results

4.1. Analysis of Descriptive Data

A demographic of the sample is shown in

Table 2. From the 400 participants, it was found that from the gender perspective, the majority of the participants were female at 71.75%. When considering age, the majority of the participants, or 38.50%, ranged between the ages of 31 and 40. Then, from the aspect of work experience, the majority of the participants, or 33.25%, had 5 to 7 years of experiences. Lastly, from the occupation aspect, the majority of the participants, or 38.00%, worked as an employee in the private sector.

4.2. Common Method Bias

Common Method Bias (CMB) is a measurement of variance that affects research accuracy. The measurement, assessed through Harman’s single-factor test, indicates the errors in the observed variables and the estimates [

49]. Since the data in this research are self-declared and varied by participants, the appropriate treatment of variances is necessary, as shown in the experiment by Harman (1976) in which the factors were tested in order and strictly. CMB is a widely accepted method to measure all the factors in EFA and to examine unrotation to define the number of factors that are necessary to calculate the variance. Among the number of variances, a correlation of variables is considered from the variance of one factor from factor analysis [

50]. This study shows that the variance of the first factor accounts for 43.38% of the total variance, which can be interpreted that common method variance (CMV) does not affect the result as it is less than 50% [

50].

4.3. Exploratory Factor Analysis

Exploratory factor analysis (EFA) in the proposed SSCM-B model found that the Kaiser–Meyer–Olkin (KMO) value was 0.891, indicating that the data were suitable for factor analysis. The Bartlett’s Test of Sphericity showed a value of 0.000, also indicating that the variables were correlated and suitable for factor analysis. The analysis was carried out using the Principal Component Analysis (PCA) with a Promax rotation that precisely categorizes factors with high correlations and explainability power [

51]. In this research, 15 factors were highly correlated. These results show appropriate factor grouping with communalities values greater than 1 considered acceptable. Also, when the Eigen value is greater than 1, the cumulative variance explained by the components is valid. Factor loading analysis showed all factors in one dimension had a value greater than 0.5, indicating that the indicators could be grouped into four dimensions with 15 factors, as shown in

Table 3.

4.4. Confirmatory Factor Analysis

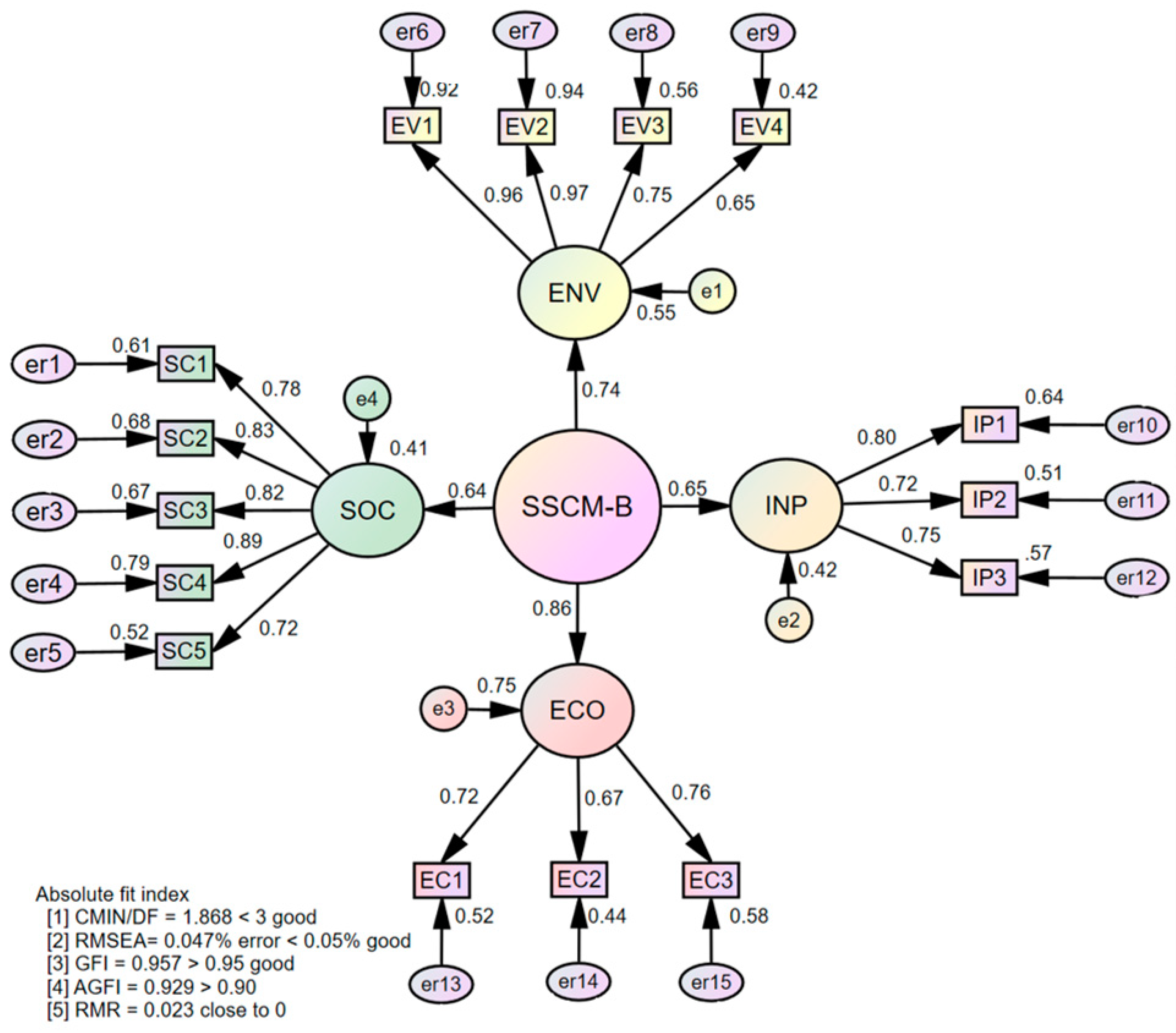

Confirmatory Factor Analysis (CFA) on the proposed SSCM-B model shows structural correlation among the observed variables within each latent variable related to Economy (EC1–EC3), Society (SC1–SC5), Environment (EV1–EV4), and Institution and Policy (IP1–IP3). The CFA results are found to be consistent with the empirical data. To test the model’s fit, the Absolute Fit Index, including CMIN/DF of 1.868 (where the value not over 3 was considered as good), indicated that the model fits well with statistical data. The Absolute Fit Index was also supported by an RMSEA of 0.047 (where the value not over 0.05 was considered as good), a GFI of 0.957 (where the value not less than 0.95 was considered as good), an AGFI of 0.929 (where the value not less than 0.90 was considered as good), and an RMR of 0.023 (where the value should be closed to 0). Furthermore, the Incremental Fit Index showed positive results. The Incremental Fit Index included an NFI of 0.965 (where the value not less than 0.95 was considered as good), a TLI of 0.976 (where the value not less than 0.95 was considered as good), a CFI of 0.983, and an IFI of 0.983 (where the value not less than 0.90 was considered as good). Therefore, the model was concluded to be suitable for statistical data. Despite the

p-value of the Chi-square being 0.000, it was considered as not statistically significant due to the characteristics of the Chi-square value being dependent on the sample size. As the Chi-square value may increase in a larger sample size, leading to the interpretation that the model is unfit for statistical data, the researcher deployed the concept proposed by Bollen [

48] where CMIN/DFs less than 3 were examined instead of the Chi-square value to test the model’s fit.

The validity test of the research instrument, the questionnaire, included the C.R. where the acceptable internal consistency of the questions or indicators within a factor should not be lower than 0.70. The convergent validity, observed from the AVE, should not be lower than 0.50. Additionally, the C.A. should not be lower than 0.7, as demonstrated in

Table 3 and the Structural Model shown in

Figure 1.

The hypotheses for testing the SEM of the proposed SSCM-B model are as follows.

H1: SSCM-B is congruent with empirical data due to the overall model fit. Every factor has components that are consistent with the empirical data, as shown in

Table 4. Therefore, H1 is accepted.

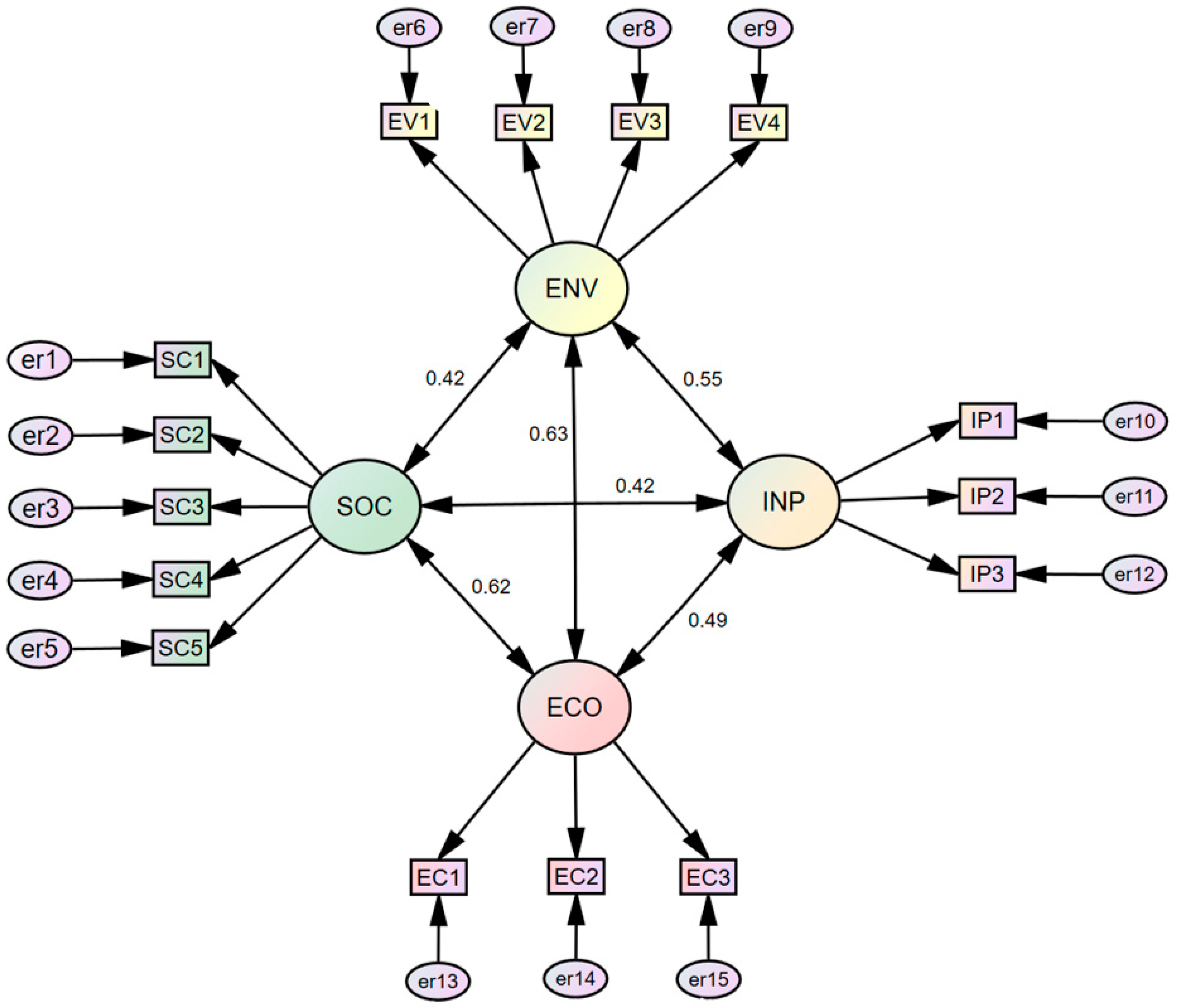

The analysis in discriminant validity was considered on the AVE. When the AVE is greater than MSV and

p-value is less than 0.01, it is considered valid. The test shows that all dimensions were correlated; therefore, all hypotheses were accepted, as shown in

Table 5 with the correlations among the four dimensions (economy, society, environment, institution and policy) are illustrated in

Figure 2.

Based on the test on correlations among each dimension, the researcher set hypotheses as shown in

Table 6.

The results indicate the acceptance of H1 to H7, which demonstrates significant correlations among the dimensions (economy, society, environment, and institution and policy) related to sustainable supply chain management in business operations. The acceptance of these hypotheses clearly shows the significance in considering sustainability from other aspects for efficient sustainable supply chain management in business operation.

5. Discussion and Implications

This research presents a model that considers sustainable supply chain management in business operations. Although previous research did not take into account the institution and policy dimension, our proposed model integrates this dimension with the other dimensions of sustainability (society, the environment, and the economy). The understanding of the complexity and correlation among these factors, provided by including the institution and policy dimension, enables businesses to operate sustainably and efficiently in the long term. The tool deployed in this study is derived from the consensus of the experts and factor analysis. The proposed model consists of 49 indicators, 15 factors, in four dimensions. The model fit, tested by SEM, shows that both the Absolute Fit Index and the Incremental Fit Index are consistent with empirical data. Subsequent checks on validity and reliability confirm that each factor in all dimensions meets the predefined criteria and aligns with the expert consensus. Finally, the correlations among the four dimensions are tested and it was found that all dimensions positively correlated to each other. Thus, a change in one dimension directly influences the other dimensions.

This study serves as a valuable resource for stakeholders, providing clarity on the complexities of sustainable supply chain management in business operations. It offers a detailed examination of influential factors across dimensions, presenting insights unexplored in the existing research. Business operators can leverage this in-depth information to tailor the indicators relevant to their organizations, and public and non-profit organizations can refer to the information to design supportive policies for private entities. For businesses, they can prioritize strategies and approaches in sustainable supply chain management in their operation.

The results have theoretical implications, significantly in three aspects of the concept of sustainable supply chain management in business. First, we propose a new model that includes the social perspective, the environmental perspective, the economic perspective, and the institutional and policy perspective for sustainable supply management in business operations. Second, this study focuses on complexities and correlations among factors in sustainable supply management with a study of the institution and policy perspective that positively enables a business to operate sustainably and efficiently. Lastly, this study shows integrity with expert consensus as it conducts factor analysis and SEM to examine model fit with real data.

Practically, these enhancements contribute to business operations and management in four aspects. First, a business can refer to this study to improve its practice or implement a concept of sustainable supply chain management from the perspectives of the economy, society, the environment, and institution and policy. Second, this study supports the development of policy and regulation for a business that is responsible to society and the environment to be innovative in using resources and reducing impacts on the environment. Third, a business can refer to this study to define or adjust its practices in supply chain management to become more sustainable. Lastly, this research serves as a resource for stakeholders in the public and private sectors to gain a better understanding of the complexities in supply chain management and sustainable practices in business operations.

6. Conclusions

Sustainable supply chain management in business operations is crucial for businesses to operate sustainably and reliably in the long term from the view of both the market and society. The ability of entrepreneurs to operate sustainably is vital for the long-term prosperity of a country and a positive influence on the economy and society. The results of this study provide valuable insights for both entrepreneurs and governments, highlighting the key factors that drive sustainable supply chain management in business operation with the following outcomes:

First, sustainable supply chain management in business operations significantly impacts economic dimensions as it helps businesses to achieve sustainability and financial stability, enhances market credibility, and builds positive images by reducing financial risks and uncertainties. It also develops trust and satisfaction from consumers towards products or services, leading to long-term valuable growth and sustainability for the business.

Second, sustainable supply chain management helps businesses survive and thrive in an era of intense environmental standards. It increases confidence in investment, allowing businesses to become more flexible to environmental challenges such as replacing materials or adjusting production processes to minimize environmental impact. As the changes decrease production costs, they enable businesses to survive in an increasingly competitive environment. Moreover, being a leader in eco-friendly supply chain management helps to gain a positive image and increases market trust as well as stakeholder engagement.

Third, these actions create social impacts in promoting corporate social responsibility by supporting projects that are beneficial to community and society, creating employment opportunities, reducing disparities between communities and businesses, and enhancing equality through the support of local activities and projects. Sustainable supply chain management fosters good relations between supporters and human rights activists from the compliance with social and environmental standards.

Lastly, sustainable supply chain management impacts institutions and policies as it promotes and supports businesses to be socially and environmentally responsible in sustainable operation. By implementing the concept of sustainability, the policies that support and promote those businesses are developed such as the use of clean energy and innovations that enhance resource efficiency and reduce environmental impacts. Public policies supporting such businesses include the promotion of eco-friendly materials.

The impacts on sustainable supply chain management in business operations, as mentioned above, aim to create sustainable and efficient businesses in the long term. They focus on the ability of a company to operate sustainably and continuously, which is crucial in building confidence and reliability. This involves a balance between impacts on the environment, society, the economy, and institution and policy, which finally create an opportunity for sustainability in business operations.

Limitations and Future Research Directions

While this study provides significant insights into sustainable supply chain management in business operations, the research still contains certain limitations.

First, the findings of this study are based on specific stakeholders in Thailand. Therefore, the ability to generalize may be limited as the business context can vary significantly between countries. Future research could aim at broadening the scope of exploring sustainable supply chain management in business operations across a diverse range of countries, to gain more comprehensive understanding. Moreover, future research can expand the scope of study to include areas with diversified geography, such as a comparison among different regions or countries for the better understanding of issues management under different conditions of local areas and regulations. Broadening the scope of study will lead to higher explainability with broader applications.

Second, further studies should utilize multi-criteria decision-making tools such as the Analytic Hierarchy Process (AHP), Fuzzy Analytic Hierarchy Process (FAHP), and Analytic Network Process (ANP) to support the strategic planning and decision-making of management to assess priority and correlation among options.

Lastly, the use of snowball sampling largely relies on personal references and experts, resulting in a controlling limitation over demographics. Future research should specify demographic data and address the expected composition of the sample to maintain research integrity while including varied aspects for comprehensive understanding in sustainable supply chain management for business operations from another effective and significant aspect.

{kind=link}

{kind=link}