Readability of Sustainability Reports: A Bibliometric Analysis and Systematic Literature Review

Abstract

:1. Introduction

2. Readability of Sustainability Reports

3. Organizational Legitimacy Theory

4. Methodology

4.1. Relevance of the Methodologies Applied

4.2. Objectives and Research Questions

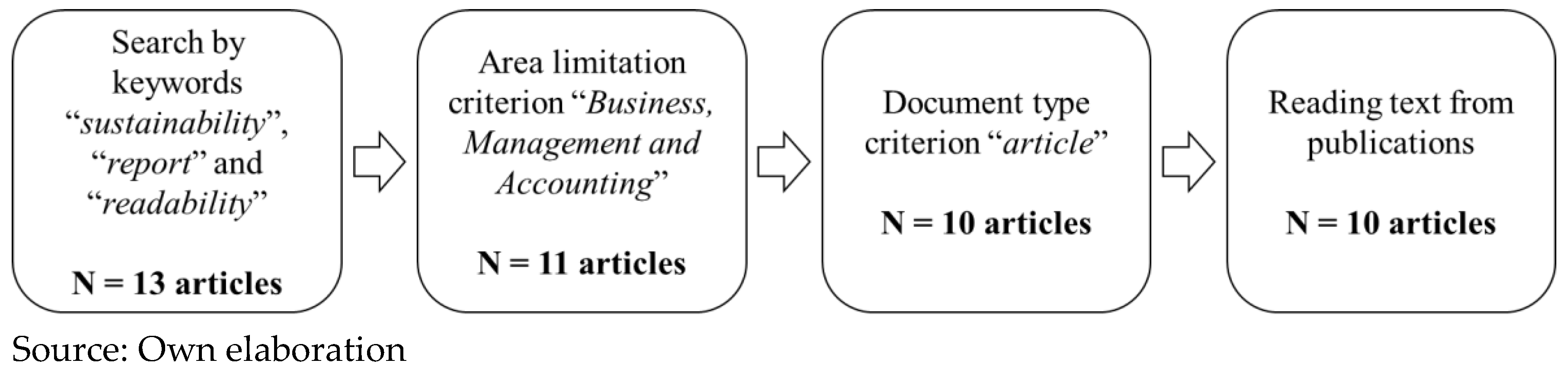

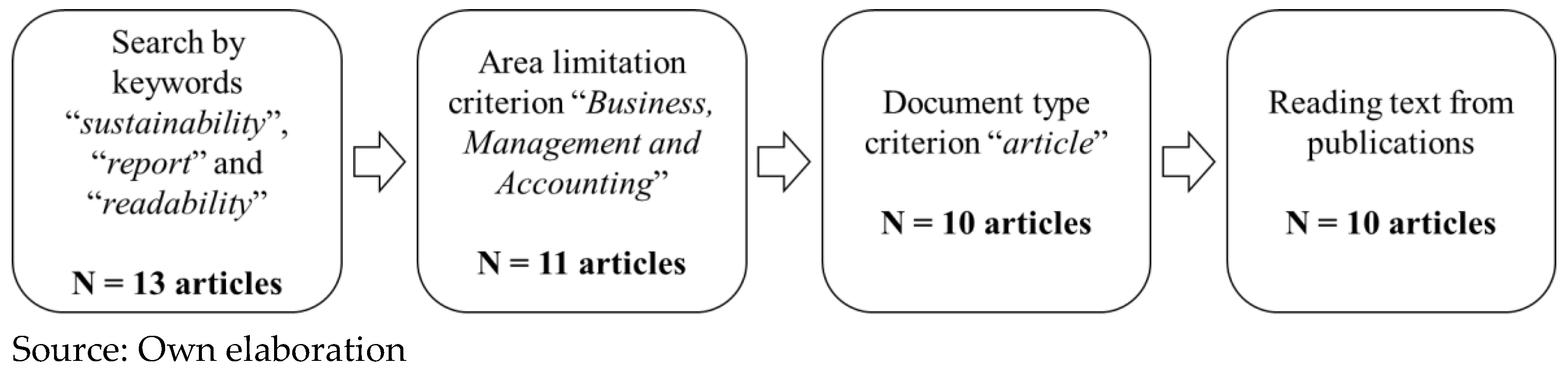

4.3. Data Collection, Filtering, and Analysis

5. Results and Discussion

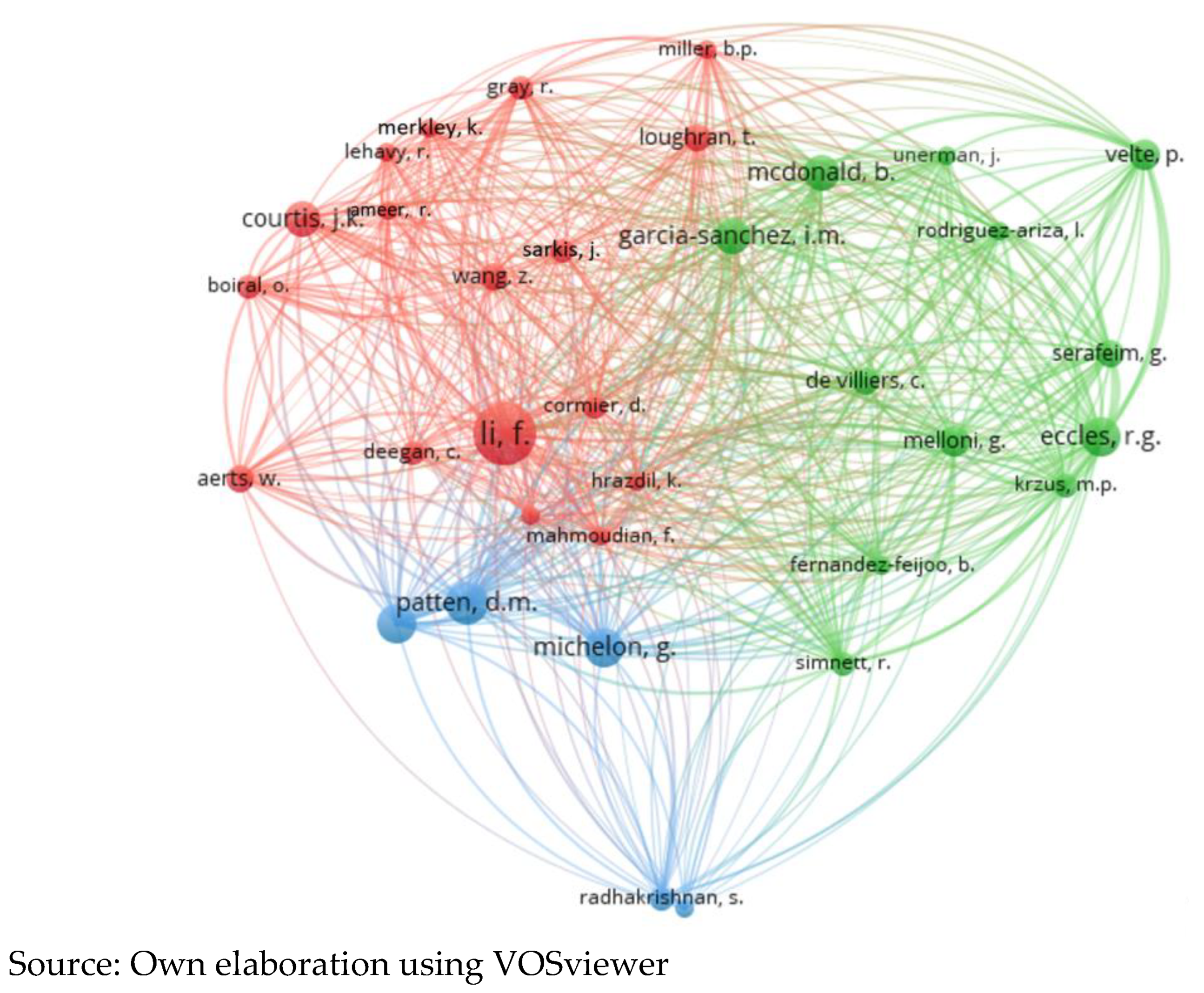

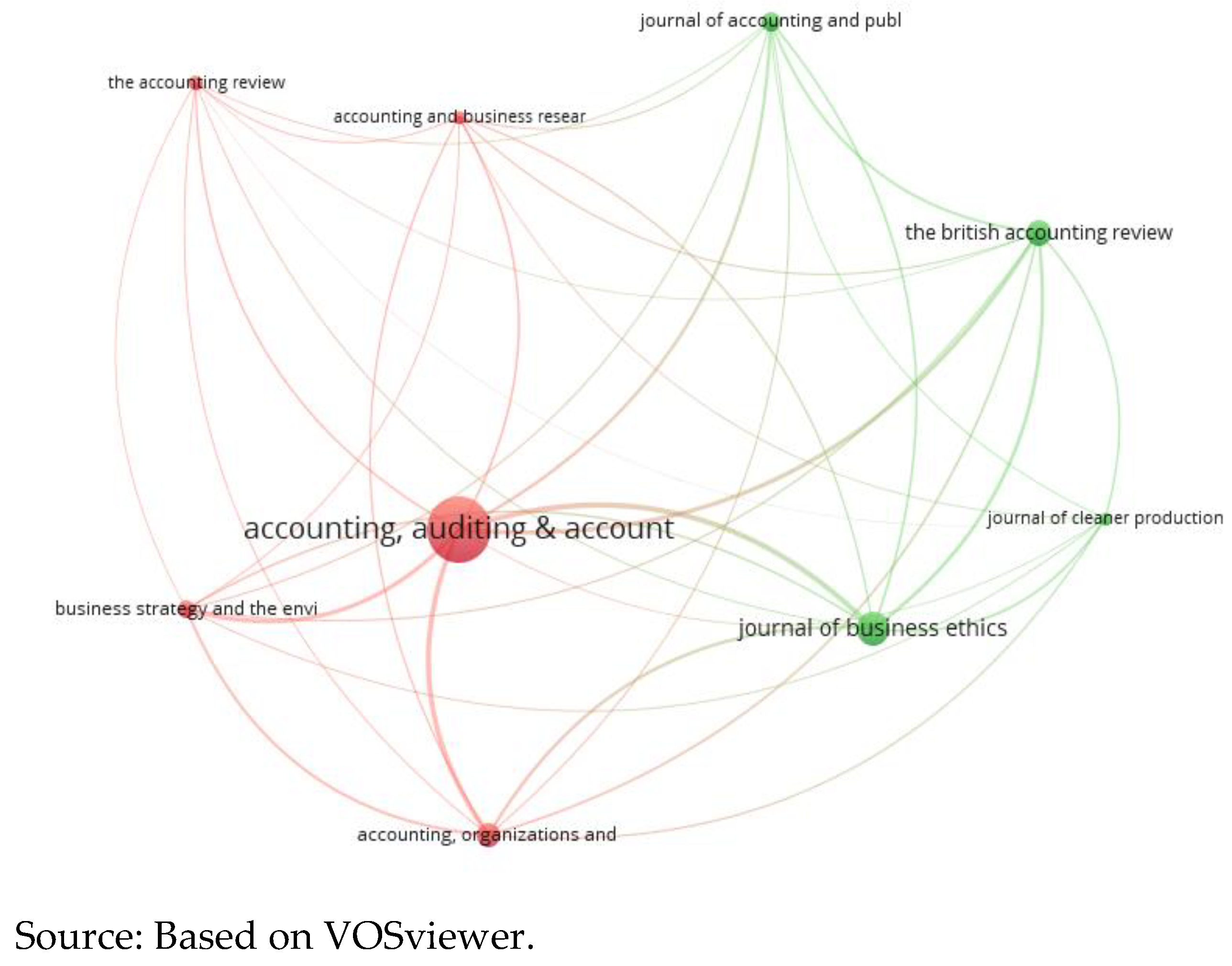

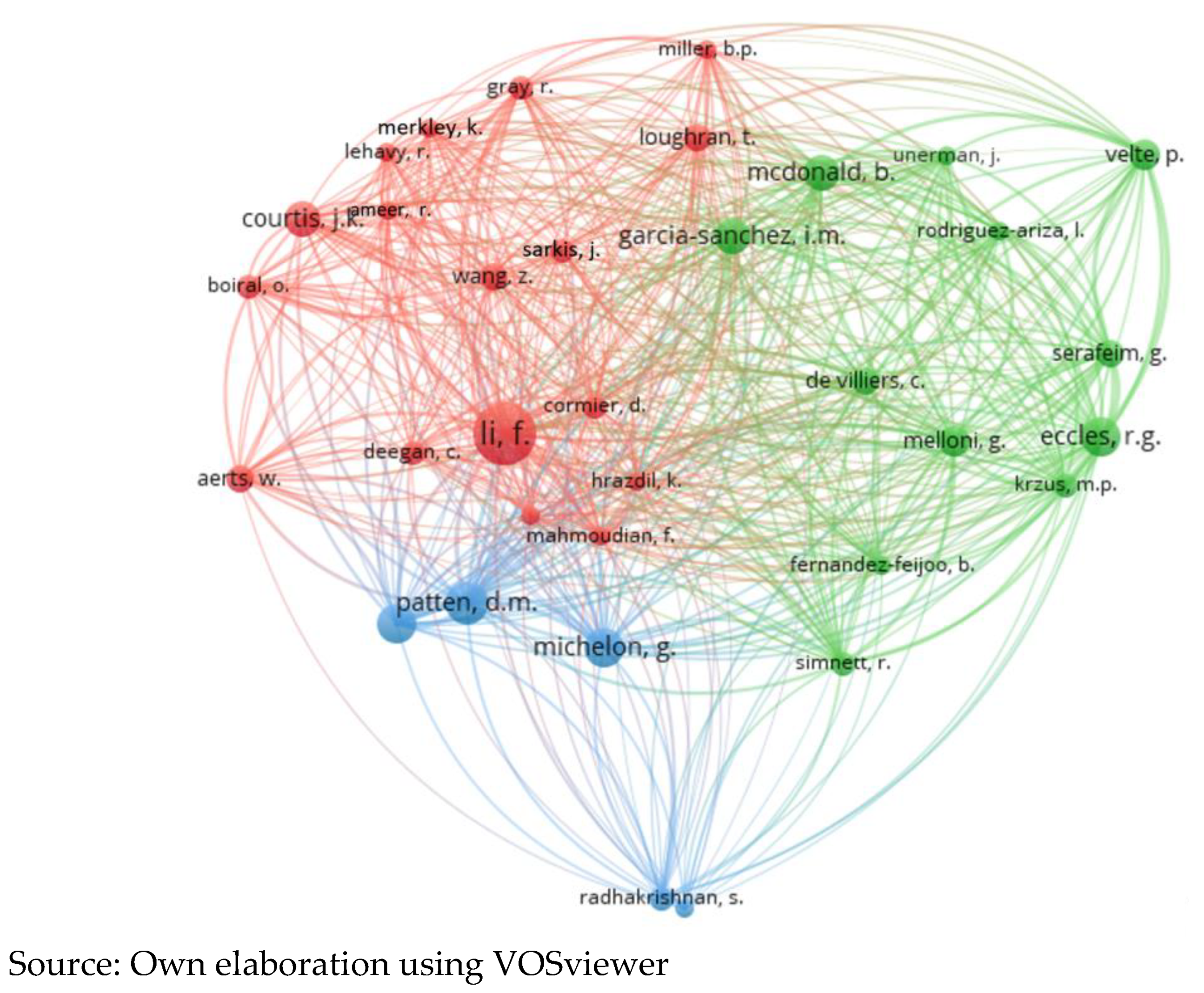

5.1. Bibliometric Mapping

{kind=link}

{kind=link}

{kind=link}

| Author(s) and Year of Publication | Geographical Origin | Journal Title | Number Cited | AJG (2021) | SQJ (2022) | SNIP (2022) | H-Index (Average) |

|---|---|---|---|---|---|---|---|

| Uddin & Chakraborty (2022) [1] | United States | Journal of Emerging Technologies in Accounting | 0 | ABS1 | Q2 | 0.825 | 2.5 |

| Phang et al. (2022) [92] | Australia | Managerial Auditing Journal | 0 | ABS2 | Q2 | 1.323 | 7 |

| Zhang et al. (2021) [56] | Australia | Journal of Business Ethics | 22 | ABS3 | Q1 | 2.976 | 9 |

| Mnif & Kchaou (2021) [93] | Tunisia | Meditari Accountancy Research | 1 | ABS1 | Q2 | 1.337 | 4 |

| Adhariani & du Toit (2020) [55] | Indonesia | Journal of Accounting in Emerging Economies | 10 | ABS2 | Q2 | 1.177 | 7.5 |

| Nilipour et al. (2020) [27] | New Zealand | Australasian Accounting, Business and Finance Journal | 5 | ABS1 | Q2 | 1.024 | 5 |

| Smeuninx et al. (2020) [9] | Belgium | International Journal of Business Communication | 15 | - | Q1 | 1.306 | 9 |

| Saber & Weber (2019) [94] | Germany | International Journal of Retail and Distribution Management | 13 | ABS2 | Q1 | 1.359 | 4.5 |

| Gerwanski et al. (2019) [91] | Germany | Business Strategy and the Environment | 58 | ABS3 | Q1 | 2.790 | 13.5 |

| Velte (2018) [90] | Germany | Problems and Perspectives in Management | 23 | ABS1 | Q3 | 0.586 | 23 |

5.2. Bibliometric Citation Networks

5.3. Systematic Literature Review

5.4. Theoretical and Pratical Implications

6. Conclusions

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Conflicts of Interest

Appendix A

References

- Uddin, N.; Chakraborty, V. An Investigation of the Readability of Sustainability Reports. J. Emerg. Technol. Account. 2022, 19, 69–78. [Google Scholar] [CrossRef]

- Bebbington, J.; Kirk, E.A.; Larrinaga, C. The production of normativity: A comparison of reporting regimes in Spain and the UK. Account. Organ. Soc. 2012, 37, 78–94. [Google Scholar] [CrossRef]

- Cho, C.H.; Freedman, M.; Patten, D.M. Corporate disclosure of environmental capital expenditures: A test of alternative theories. Account. Audit. Account. J. 2012, 25, 486–507. [Google Scholar] [CrossRef]

- Senn, J.; Giordano-Spring, S. The limits of environmental accounting disclosure: Enforcement of regulations, standards and interpretative strategies. Account. Audit. Account. J. 2020, 33, 1367–1393. [Google Scholar] [CrossRef]

- De Villiers, C.; Van Staden, C.J. Can less environmental disclosure have a legitimising effect? Evidence from Africa. Account. Organ. Soc. 2006, 31, 763–781. [Google Scholar] [CrossRef]

- Hackston, D.; Milne, M.J. Some determinants of social and environmental disclosures in New Zealand companies. Account. Audit. Account. J. 1996, 9, 77–108. [Google Scholar] [CrossRef]

- Solomon, A.; Lewis, L. Incentives and disincentives for corporate environmental disclosure. Bus. Strategy Environ. 2002, 11, 154–169. [Google Scholar] [CrossRef]

- Martins, A.; Gomes, D.; Branco, M.C. Managing corporate social and environmental disclosure: An accountability vs. impression management framework. Sustainability 2020, 13, 296. [Google Scholar] [CrossRef]

- Smeuninx, N.; De Clerck, B.; Aerts, W. Measuring the readability of sustainability reports: A corpus-based analysis through standard formulae and NLP. Int. J. Bus. Commun. 2020, 57, 52–85. [Google Scholar] [CrossRef]

- Dowling, J.; Pfeffer, J. Organizational legitimacy: Social values and organizational behavior. Pac. Sociol. Rev. 1975, 18, 122–136. [Google Scholar] [CrossRef]

- Cüre, T.; Esen, E.; Özsözgün Çalışkan, A. Impression management in graphical representation of economic, social, and environmental issues: An empirical study. Sustainability 2020, 12, 379. [Google Scholar] [CrossRef]

- García-Sánchez, I.M.; Amor-Esteban, V.; Galindo-Álvarez, D. Communication strategies for the 2030 agenda commitments: A multivariate approach. Sustainability 2020, 12, 10554. [Google Scholar] [CrossRef]

- Neu, D.; Warsame, H.; Pedwell, K. Managing public impressions: Environmental disclosures in annual reports. Account. Organ. Soc. 1998, 23, 265–282. [Google Scholar] [CrossRef]

- Chiu, T.K.; Wang, Y.H. Determinants of social disclosure quality in Taiwan: An application of stakeholder theory. J. Bus. Ethics 2015, 129, 379–398. [Google Scholar] [CrossRef]

- Schaltegger, S.; Burritt, R. Contemporary Environmental Accounting: Issues, Concepts and Practice; Greenleaf Publishing: Austin, TX, USA; Routledge: London, UK, 2017. [Google Scholar]

- Lu, Y.; Abeysekera, I. What do stakeholders care about? Investigating corporate social and environmental disclosure in China. J. Bus. Ethics 2017, 144, 169–184. [Google Scholar] [CrossRef]

- Patten, D.M. The relation between environmental performance and environmental disclosure: A research note. Account. Organ. Soc. 2002, 27, 763–773. [Google Scholar] [CrossRef]

- Beretta, V.; Demartini, M.C.; Lico, L.; Trucco, S. A tone analysis of the non-financial disclosure in the automotive industry. Sustainability 2021, 13, 2132. [Google Scholar] [CrossRef]

- Parker, L.D. Twenty-one years of social and environmental accountability research: A coming of age. Account. Forum 2011, 35, 1–10. [Google Scholar] [CrossRef]

- Deegan, C. Introduction: The legitimising effect of social and environmental disclosures–a theoretical foundation. Account. Audit. Account. J. 2002, 15, 282–311. [Google Scholar] [CrossRef]

- Mahadeo, J.D.; Oogarah-Hanuman, V.; Soobaroyen, T. Changes in social and environmental reporting practices in an emerging economy (2004–2007): Exploring the relevance of stakeholder and legitimacy theories. Account. Forum 2011, 35, 158–175. [Google Scholar] [CrossRef]

- Gray, R.; Kouhy, R.; Lavers, S. Corporate social and environmental reporting: A review of the literature and a longitudinal study of UK disclosure. Account. Audit. Account. J. 1995, 8, 47–77. [Google Scholar] [CrossRef]

- Lindblom, C. The implications of organizational legitimacy for corporate social performance and disclosure. In Proceedings of the Critical Perspectives on Accounting Conference, New York, NY, USA, 17 April 1993. [Google Scholar]

- Milne, M.J.; Patten, D.M. Securing organizational legitimacy: An experimental decision case examining the impact of environmental disclosures. Account. Audit. Account. J. 2002, 15, 372–405. [Google Scholar] [CrossRef]

- Wang, Z.; Hsieh, T.S.; Sarkis, J. CSR performance and the readability of CSR reports: Too good to be true? Corp. Soc. Responsib. Environ. Manag. 2018, 25, 66–79. [Google Scholar] [CrossRef]

- Stubbs, W.; Higgins, C.; Milne, M. Why do companies not produce sustainability reports? Bus. Strategy Environ. 2013, 22, 456–470. [Google Scholar] [CrossRef]

- Nilipour, A.; De Silva, T.A.; Li, X. The readability of sustainability reporting in New Zealand over time. Australas. Account. Bus. Financ. J. 2020, 14, 86–107. [Google Scholar] [CrossRef]

- Merkl-Davies, D.M.; Brennan, N.M. Discretionary disclosure strategies in corporate narratives: Incremental information or impression management? J. Account. Lit. 2007, 27, 116–196. [Google Scholar]

- Rosenfeld, P.; Giacalone, R.A.; Riordan, C.A. Impression management theory and diversity: Lessons for organizational behavior. Am. Behav. Sci. 1994, 37, 601–604. [Google Scholar] [CrossRef]

- Bozeman, D.P.; Kacmar, K.M. A cybernetic model of impression management processes in organizations. Organ. Behav. Hum. Decis. Process. 1997, 69, 9–30. [Google Scholar] [CrossRef]

- Rosenfeld, P. Impression management, fairness, and the employment interview. J. Bus. Ethics 1997, 16, 801–808. [Google Scholar] [CrossRef]

- Godfrey, J.; Mather, P.; Ramsay, A. Earnings and impression management in financial reports: The case of CEO changes. Abacus 2003, 39, 95–123. [Google Scholar] [CrossRef]

- Jones, M.J. A longitudinal study of the readability of the chairman’s narratives in the corporate reports of a UK company. Account. Bus. Res. 1988, 18, 297–305. [Google Scholar] [CrossRef]

- Courtis, J.K. Annual report readability variability: Tests of the obfuscation hypothesis. Account. Audit. Account. J. 1998, 11, 459–472. [Google Scholar] [CrossRef]

- Clatworthy, M.; Jones, M.J. The effect of thematic structure on the variability of annual report readability. Account. Audit. Account. J. 2001, 14, 311–326. [Google Scholar] [CrossRef]

- Rutherford, B.A. Genre analysis of corporate annual report narratives: A corpus linguistics–based approach. J. Bus. Commun. 2005, 42, 349–378. [Google Scholar] [CrossRef]

- Diouf, D.; Boiral, O. The quality of sustainability reports and impression management: A stakeholder perspective. Account. Audit. Account. J. 2017, 30, 643–667. [Google Scholar] [CrossRef]

- Brennan, N.M.; Merkl-Davies, D.M. Accounting narratives and impression management. In The Routledge Companion to Accounting Communication; Routledge: London, UK, 2013; pp. 123–146. [Google Scholar]

- Li, F. Annual report readability, current earnings, and earnings persistence. J. Account. Econ. 2008, 45, 221–247. [Google Scholar] [CrossRef]

- Courtis, J.K. Readability of annual reports: Western versus Asian evidence. Account. Audit. Account. J. 1995, 8, 4–17. [Google Scholar] [CrossRef]

- Li, F. Textual analysis of corporate disclosures: A survey of the literature. J. Account. Lit. 2010, 29, 143–165. [Google Scholar]

- Courtis, J.K. An investigation into annual report readability and corporate risk-return relationships. Account. Bus. Res. 1986, 16, 285–294. [Google Scholar] [CrossRef]

- Subramanian, R.; Insley, R.G.; Blackwell, R.D. Performance and readability: A comparison of annual reports of profitable and unprofitable corporations. J. Bus. Commun. 1993, 30, 49–61. [Google Scholar] [CrossRef]

- Madasu, P. Longitudinal Readability Analysis of Letter-to-shareholders published by Indian listed banking companies. Glob. Manag. Rev. 2020, 14, 1–18. [Google Scholar]

- Balsells, M. La Carta del Presidente Como Medio de Legitimación: Análisis Longitudinal de Legibilidad y Contenido de Cepsa (1930–2004) y Repsol-YPF (1987–2004). Ph.D. Thesis, Departamento de Dirección de Empresas, Universidad Pablo de Olavide, Sevilla, Spain, 2007. [Google Scholar]

- Soper, F.J.; Dolphin, R. Readability and corporate annual reports. Account. Rev. 1964, 39, 358. [Google Scholar]

- Poshalian, S.; Crissy, W.J. Corporate annual reports are difficult, dull reading, human interest value low, survey shows. J. Account. 1952, 94, 215. [Google Scholar]

- Smith, J.E.; Smith, N.P. Readability: A measure of the performance of the communication function of financial reporting. Account. Rev. 1971, 46, 552–561. [Google Scholar]

- Haried, A.A. The semantic dimensions of financial statements. J. Account. Res. 1972, 10, 376–391. [Google Scholar] [CrossRef]

- Still, M.D. The Readability of Chairmen’s Statements. Account. Bus. Res. 1972, 3, 36–39. [Google Scholar] [CrossRef]

- Haried, A.A. Measurement of meaning in financial reports. J. Account. Res. 1973, 11, 117–145. [Google Scholar] [CrossRef]

- Morton, J.R. Qualitative objectives of financial accounting: A comment on relevance and understandability. J. Account. Res. 1974, 12, 288–298. [Google Scholar] [CrossRef]

- Beattie, V. Accounting narratives and the narrative turn in accounting research: Issues, theory, methodology, methods and a research framework. Br. Account. Rev. 2014, 46, 111–134. [Google Scholar] [CrossRef]

- Eugene Baker III, H.; Kare, D.D. Relationship between annual report readability and corporate financial performance. Manag. Res. News 1992, 15, 1–4. [Google Scholar] [CrossRef]

- Adhariani, D.; Du Toit, E. Readability of sustainability reports: Evidence from Indonesia. J. Account. Emerg. Econ. 2020, 10, 621–636. [Google Scholar] [CrossRef]

- Zhang, L.; Shan, Y.G.; Chang, M. Can CSR disclosure protect firm reputation during financial restatements? J. Bus. Ethics 2021, 173, 157–184. [Google Scholar] [CrossRef]

- Alexander, D.; Jermakowicz, E. A true and fair view of the principles/rules debate. Abacus 2006, 42, 132–164. [Google Scholar] [CrossRef]

- Yongvanich, K.; Guthrie, J. An extended performance reporting framework for social and environmental accounting. Bus. Strategy Environ. 2006, 15, 309–321. [Google Scholar] [CrossRef]

- Roman, A.G.; Mocanu, M.; Hoinaru, R. Disclosure style and its determinants in integrated reports. Sustainability 2019, 11, 1960. [Google Scholar] [CrossRef]

- Shauki, E.R.; Oktavini, E. Earnings Management and Annual Report Readability: The Moderating Effect of Female Directors. Int. J. Financ. Stud. 2022, 10, 73. [Google Scholar] [CrossRef]

- Al-Shaer, H.; Albitar, K.; Hussainey, K. Creating sustainability reports that matter: An investigation of factors behind the narratives. J. Appl. Account. Res. 2022, 23, 738–763. [Google Scholar] [CrossRef]

- Cormier, D.; Gordon, I.M.; Magnan, M. Corporate environmental disclosure: Contrasting management’s perceptions with reality. J. Bus. Ethics 2004, 49, 143–165. [Google Scholar] [CrossRef]

- Van Der Ploeg, L.; Vanclay, F. Credible claim or corporate spin? A checklist to evaluate corporate sustainability reports. J. Environ. Assess. Policy Manag. 2013, 15, 1350012. [Google Scholar] [CrossRef]

- Demuijnck, G.; Ngnodjom, H. Responsibility and informal CSR in formal Cameroonian SMEs. J. Bus. Ethics 2013, 112, 653–665. [Google Scholar] [CrossRef]

- Cong, Y.; Freedman, M.; Park, J.D. Tone at the top: CEO environmental rhetoric and environmental performance. Adv. Account. 2014, 30, 322–327. [Google Scholar] [CrossRef]

- Suchman, M.C. Managing legitimacy: Strategic and institutional approaches. Acad. Manag. Rev. 1995, 20, 571–610. [Google Scholar] [CrossRef]

- Patten, D.M. Exposure, legitimacy and social disclosure. J. Account. Public Policy 1991, 10, 297–308. [Google Scholar] [CrossRef]

- Patten, D.M. Intra-industry environmental disclosures in response to the Alaskan oil spill: A note on legitimacy theory. Account. Organ. Soc. 1992, 17, 471–475. [Google Scholar] [CrossRef]

- Aerts, W.; Cormier, D. Media legitimacy and corporate environmental communication. Account. Organ. Soc. 2009, 34, 1–27. [Google Scholar] [CrossRef]

- Fanelli, A.; Misangyi, V.F. Bringing out charisma: CEO charisma and external stakeholders. Acad. Manag. Rev. 2006, 31, 1049–1061. [Google Scholar] [CrossRef]

- Elsbach, K.D.; Sutton, R. Acquiring organizational legitimacy through illegitimate actions: A marriage of institutional and impression management theories. Acad. Manag. J. 1992, 35, 699–739. [Google Scholar] [CrossRef]

- O’Donovan, G. Environmental disclosures in the annual report: Extending the applicability and predictive power of legitimacy theory. Account. Audit. Account. J. 2002, 15, 344–371. [Google Scholar] [CrossRef]

- Clarkson, P.M.; Li, Y.; Richardson, G.D.; Vasvari, F.P. Revisiting the relation between environmental performance and environmental disclosure: An empirical analysis. Account. Organ. Soc. 2008, 33, 303–327. [Google Scholar] [CrossRef]

- Bolino, M.; Long, D.; Turnley, W. Impression management in organizations: Critical questions, answers, and areas for future research. Annu. Rev. Organ. Psychol. Organ. Behav. 2016, 3, 377–406. [Google Scholar] [CrossRef]

- Hrasky, S.; Smith, B. Concise corporate reporting: Communication or symbolism? Corp. Commun. Int. J. 2008, 13, 418–432. [Google Scholar] [CrossRef]

- Hooghiemstra, R. Corporate communication and impression management—New perspectives why companies engage in corporate social reporting. J. Bus. Ethics 2000, 27, 55–68. [Google Scholar] [CrossRef]

- Ogden, S.; Clarke, J. Customer disclosures, impression management and the construction of legitimacy: Corporate reports in the UK privatised water industry. Account. Audit. Account. J. 2005, 18, 313–345. [Google Scholar] [CrossRef]

- Talbot, D.; Boiral, O. GHG reporting and impression management: An assessment of sustainability reports from the energy sector. J. Bus. Ethics 2018, 147, 367–383. [Google Scholar] [CrossRef]

- Castriotta, M.; Loi, M.; Marku, E.; Naitana, L. What’s in a name? Exploring the conceptual structure of emerging organizations. Scientometrics 2019, 118, 407–437. [Google Scholar] [CrossRef]

- Kumar, S.; Sureka, R.; Colombage, S. Capital structure of SMEs: A systematic literature review and bibliometric analysis. Manag. Rev. Q. 2020, 70, 535–565. [Google Scholar] [CrossRef]

- Donthu, N.; Kumar, S.; Mukherjee, D.; Pandey, N.; Lim, W.M. How to conduct a bibliometric analysis: An overview and guidelines. J. Bus. Res. 2021, 133, 285–296. [Google Scholar] [CrossRef]

- Brown, T.; Park, A.; Pitt, L. A 60-year bibliographic review of the Journal of Advertising Research: Perspectives on trends in authorship, influences, and research impact. J. Advert. Res. 2020, 60, 353–360. [Google Scholar] [CrossRef]

- Li, Z.; Chen, Z.; Yang, N.; Wei, K.; Ling, Z.; Liu, Q.; Chen, G.; Ye, B.H. Trends in research on the carbon footprint of higher education: A bibliometric analysis (2010–2019). J. Clean. Prod. 2021, 289, 125642. [Google Scholar] [CrossRef]

- Khan, M.A.; Pattnaik, D.; Ashraf, R.; Ali, I.; Kumar, S.; Donthu, N. Value of special issues in the journal of business research: A bibliometric analysis. J. Bus. Res. 2021, 125, 295–313. [Google Scholar] [CrossRef]

- Fink, A. Conducting Research Literature Reviews: From the Internet to Paper, 5th ed.; Sage Publications: Thousand Oaks, CA, USA, 2019. [Google Scholar]

- Okoli, C.; Schabram, K. A guide to conducting a systematic literature review of information systems research. Soc. Sci. Res. Netw. 2010, 10, 1–49. [Google Scholar] [CrossRef]

- Paré, G.; Trudel, M.C.; Jaana, M.; Kitsiou, S. Synthesizing information systems knowledge: A typology of literature reviews. Inf. Manag. 2015, 52, 183–199. [Google Scholar] [CrossRef]

- Xiao, Y.; Watson, M. Guidance on conducting a systematic literature review. J. Plan. Educ. Res. 2019, 39, 93–112. [Google Scholar] [CrossRef]

- Tranfield, D.; Denyer, D.; Smart, P. Towards a methodology for developing evidence-informed management knowledge by means of systematic review. Br. J. Manag. 2003, 14, 207–222. [Google Scholar] [CrossRef]

- Velte, P. Is audit committee expertise connected with increased readability of integrated reports: Evidence from EU companies. Probl. Perspect. Manag. 2018, 16, 23–41. [Google Scholar] [CrossRef]

- Gerwanski, J.; Kordsachia, O.; Velte, P. Determinants of materiality disclosure quality in integrated reporting: Empirical evidence from an international setting. Bus. Strategy Environ. 2019, 28, 750–770. [Google Scholar] [CrossRef]

- Phang, S.-Y.; Adrian, C.; Garg, M.; Pham, A.V.; Truong, C. COVID-19 pandemic resilience: An analysis of firm valuation and disclosure of sustainability practices of listed firms. Manag. Audit. J. 2023, 38, 85–128. [Google Scholar] [CrossRef]

- Mnif, Y.; Kchaou, J. Through the rhetoric art: CEO incentives in sustainability sensitive industries. Meditari Account. Res. 2023, 31, 576–601. [Google Scholar] [CrossRef]

- Saber, M.; Weber, A. How do supermarkets and discounters communicate about sustainability? A comparative analysis of sustainability reports and in-store communication. Int. J. Retail Distrib. Manag. 2019, 47, 1181–1202. [Google Scholar]

- Peters, V.; Wester, F. How qualitative data analysis software may support the qualitative analysis process. Qual. Quant. 2007, 41, 635–659. [Google Scholar] [CrossRef]

- Carungu, J.; Di Pietra, R.; Molinari, M. Mandatory vs. voluntary exercise on non-financial reporting: Does a normative/coercive isomorphism facilitate an increase in quality? Meditari Account. Res. 2020, 29, 449–476. [Google Scholar] [CrossRef]

- Krasodomska, J.; Michalak, J.; Świetla, K. Directive 2014/95/EU: Accountants’ under-standing and attitude towards mandatory non-financial disclosures in corporate reporting. Meditari Account. Res. 2020, 28, 751–779. [Google Scholar] [CrossRef]

- Adnan, S.M.; Hay, D.; van Staden, C.J. The influence of culture and corporate governance on corporate social responsibility disclosure: A cross country analysis. J. Clean. Prod. 2018, 198, 820–832. [Google Scholar] [CrossRef]

- Arena, C.; Bozzolan, S.; Michelon, G. Environmental reporting: Transparency to stakeholders or stakeholder manipulation? An analysis of disclosure tone and the role of the board of directors. Corp. Soc. Responsib. Environ. Manag. 2015, 22, 346–361. [Google Scholar] [CrossRef]

- De Silva, T.A.; Nilipour, A.; Mansouri, N. Sustainability Reporting by New Zealand Wineries. In Social Sustainability in the Global Wine Industry: Concepts and Cases; Palgrave Pivot: Cham, Switzerland, 2020; pp. 169–184. [Google Scholar]

| Objectives | Research Questions | Methodology |

|---|---|---|

| 1. Investigate the latest scientific developments on the readability of sustainability reports. | 1.1. Which authors have published work on the readability of sustainability reports? 1.2. What is the geographical origin of the authors identified? 1.3. Which journals published them? 1.4. What is the impact of the journals where the papers were published? | Bibliometric analysis with Scopus database metrics and AJG classification. |

| 2. Identify research networks and topics in the field of readability of corporate sustainability disclosures. | 2.1. What are the main research topics in this area? 2.2. What methodologies used? 2.3. What samples are analyzed? 2.4. What is the bibliometric relationship between our sample and the literature? | Construction and visualization of bibliometric maps with VOSviewer software, version 1.6.18. |

| 3. Critical analysis of the gaps in the literature and proposals for developing future research work in sustainability reporting readability. | 3.1. What are the main results of the literature review? 3.2. What are the main contributions of the work? 3.3. What are the main gaps in the literature and opportunities for future research? | Systematic literature review of the sample of articles collected. |

| Research Topic | Methodology | Sample/Research Period | Author(s) and Year of Publication |

|---|---|---|---|

| Quality and effectiveness of sustainability reporting (blue cluster) | Content analysis. Gunning fog index. Multiple linear regression model. | 99 companies listed on the S&P 300 and S&P Global 300 between 2016 and 2017. | Uddin & Chakraborty (2022) [1] |

| Content analysis. Gunning fog and Bog index. Multiple linear regression model. | 518 companies from 45 countries operating in environmentally sensitive sectors during 2016–2018. | Mnif & Kchaou (2021) [93] | |

| Content analysis. Flesch reading ease, Flesch–Kincaid, and Gunning fog. | 25 companies listed on Indonesia’s stock exchange from 2015 to 2017. | Adhariani & du Toit (2020) [55] | |

| Content analysis. Flesch–Kincaid grade level, Gunning fog, Coleman–Liau, SMOG and Automated readability. | 37 companies listed on the New Zealand stock exchange from 2007 to 2016. | Nilipour et al. (2020) [27] | |

| Content analysis. Flesch–Kincaid grade level and Gunning fog. | 470 companies from the United States, United Kingdom, Europe, Australia, and India. | Smeuninx et al. (2020) [9] | |

| Content analysis. Gunning fog index. Multiple linear regression model. | 359 European and South African companies between 2013 and 2016. | Gerwanski et al. (2019) [91] | |

| Content analysis. German modified SMOG index, Modified Amdahl index and WSTF index. | Two supermarket chains and six German outlet chains in 2016. | Saber & Weber (2019) [94] | |

| Relationship between sustainability disclosure and financial performance of companies and auditing issues (green cluster) | Content analysis. Dale–Chall index, Flesch–Kincaid index and Gunning fog index. Logistic regression analysis model. | 48 Australian listed companies between 2011 and 2021. | Phang et al. (2022) [82] |

| Content analysis. SMOG and tone at the top Logistic regression analysis model. | 130 companies in financial restatements processes from the Audit Analytics database between 2000 and 2017. | Zhang et al. (2021) [56] | |

| Content analysis. Flesch reading ease and Gunning fog. Multiple linear regression model. | 215 European companies, between 2014 and 2016. | Velte (2018) [90] |

| Research Subject | Results and Discussion | Future Perspectives | Author(s) and Year of Publication |

|---|---|---|---|

| Quality and effectiveness of sustainability reporting (blue cluster) | Reports from companies in regulated industries are less readable than reports from other companies. Less complex companies have more readable sustainability reports. | Analyze linguistic manipulation of sustainability reports as an obfuscation technique. Examine differences by country or region, especially about the new EU environmental, social, and climate reporting requirements. | Uddin & Chakraborty (2022) [1] |

| CEO’s monetary and non-monetary incentives negatively influence the readability of sustainability reports (greater reading complexity). The complementary relationship between these incentives. Other CEO characteristics have no significant effect on the readability of sustainability reports. | Investigate the readability of sustainability reports written in a language other than English. Use other readability indices like the plain English index and the Flesch reading ease score. Analyze the role of the sustainability director in reporting and explore the relationship between director incentives and sustainability assurance practices. | Mnif & Kchaou (2021) [93] | |

| The reports had a low level of readability. Companies in the same industry implemented the same format and language in disclosing their sustainability information. Companies may deliberately use more complex language for some purposes, such as creating a good impression and supporting the legitimacy of the company. CSR disclosure practices are considered symbolic to establish a company’s positive image and are not substantive in nature. | Construct more accurate measures of readability in the Indonesian context. Investigate possible determinants and the economic consequences of readability in Indonesia. Analyze the relationship between sustainability reporting readability and company financial performance. | Adhariani & Toit (2020) [55] | |

| Readability improved by only 6.5 percent. Substantial increase in the number of companies reporting sustainability information. Statistically significant negative correlation between average readability index and number of reports. Longer sustainability reports have lower readability indices. Environmentally sensitive companies published more readable information. | Examine the readability of other communication channels, such as sustainability information published on web pages and in social media. Investigate other determinants (company characteristics) of readability. | Nilipour et al. (2020) [27] | |

| Sustainability reports are still a very difficult document to read, sometimes more difficult than financial reports. Region proved to be an important variable. Results highlight the impact of legislative contexts and linguistic variety as an underexplored variable. Association between better economic performance and lower syntactic complexity, supporting the syntactic obfuscation hypothesis. | Analyze the relationship between nonfinancial performance and readability of financial and nonfinancial reports. Quantitatively investigate language variety and the impact of industry on readability. | Smeuninx et al. (2020) [9] | |

| Readability is positively associated with learning effects, gender diversity, and the assurance of non-financial information in the integrated report. The amount of information in the integrated reports and earnings management does not affect the quality of readability. | Analyze the impact of senior management characteristics on sustainability disclosure. Investigate and compare the alignment of materiality disclosure quality with different theoretical frameworks. Analyze whether a company’s disclosure is truly geared towards providing valuable information or to what extent it is used for impression management. | Gerwanski et al. (2019) [91] | |

| The results reveal no major differences between supermarkets and discounters regarding the readability of sustainability reports. Supermarkets perform significantly better in sustainability readability than discounters. Poor quality in readability analysis is reflected in less concrete data. | Analyze differences in the readability of different retail formats for different countries and for different industry sectors. Investigate the readability of different forms of communication. | Saber & Weber (2019) [94] | |

| Relationship between sustainability disclosure and financial performance of companies and auditing issues (green cluster) | Companies that disclose sustainability practices exhibit higher market valuations relative to other companies. Sustainable practices help loss-making companies remain resilient during the pandemic. The negative association between sustainability practices and asset profitability. The positive relationship between sustainability disclosure and firm value is stronger in firms with higher readability ratings. | Analyze the investment and degree of disclosure of sustainable practices during the COVID-19 pandemic. | Phang et al. (2022) [92] |

| Companies change their reports to a more conservative tone, increasing the readability and length of reports, despite strategically disclosing sustainability-related content. Companies that reaffirm CSR disclosure suffer smaller losses in value. Disclosure of CSR practices alleviates reputational damage and plays a protective role during periods of crisis. | Examine other disclosure characteristics of CSR reports, such as strategic framing and presentation style. Investigate how possible sustainability items can be integrated into integrated reports. | Zhang et al. (2021) [56] | |

| Financial and sustainability auditing has a positive impact on the readability of reports. Combined auditing has a stronger effect. To combine financial and sustainability information into integrated reports, audit committees need to have more diversified expertise. | Analyze the effects of regulatory changes that increased stakeholder management incentives after the 2008–2009 financial crisis. Examine other variables of board composition on the quality of integrated reporting. Use other methodologies such as interviews and questionnaires to overcome the limitations of readability indices. | Velte (2018) [90] |

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2023 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Pombinho, M.; Fialho, A.; Novas, J. Readability of Sustainability Reports: A Bibliometric Analysis and Systematic Literature Review. Sustainability 2024, 16, 260. https://doi.org/10.3390/su16010260

Pombinho M, Fialho A, Novas J. Readability of Sustainability Reports: A Bibliometric Analysis and Systematic Literature Review. Sustainability. 2024; 16(1):260. https://doi.org/10.3390/su16010260

Chicago/Turabian StylePombinho, Miguel, Ana Fialho, and Jorge Novas. 2024. "Readability of Sustainability Reports: A Bibliometric Analysis and Systematic Literature Review" Sustainability 16, no. 1: 260. https://doi.org/10.3390/su16010260

APA StylePombinho, M., Fialho, A., & Novas, J. (2024). Readability of Sustainability Reports: A Bibliometric Analysis and Systematic Literature Review. Sustainability, 16(1), 260. https://doi.org/10.3390/su16010260