SERVQUAL to Determine Relationship Quality and Behavioral Intentions: An SEM Approach in Retail Banking Service

,

,  , ,

, ,  and

and

Abstract

1. Introduction

- (1)

- How do SQ dimensions under the SERVQUAL model influence REQ and BVI in retail banking?

- (2)

- How does REQ directly affect BVI and mediate the association between SQ and BVI?

2. Literature Review

2.1. Service Quality (SQ)

2.2. Relationship Quality (REQ)

2.3. Behavioral Intentions (BVI)

3. Hypothesis Development

4. Research Methodology

4.1. Survey Procedures and Data Collection

4.2. Data Analysis

4.3. Demographic Results

5. Empirical Results

5.1. Common Method Variance

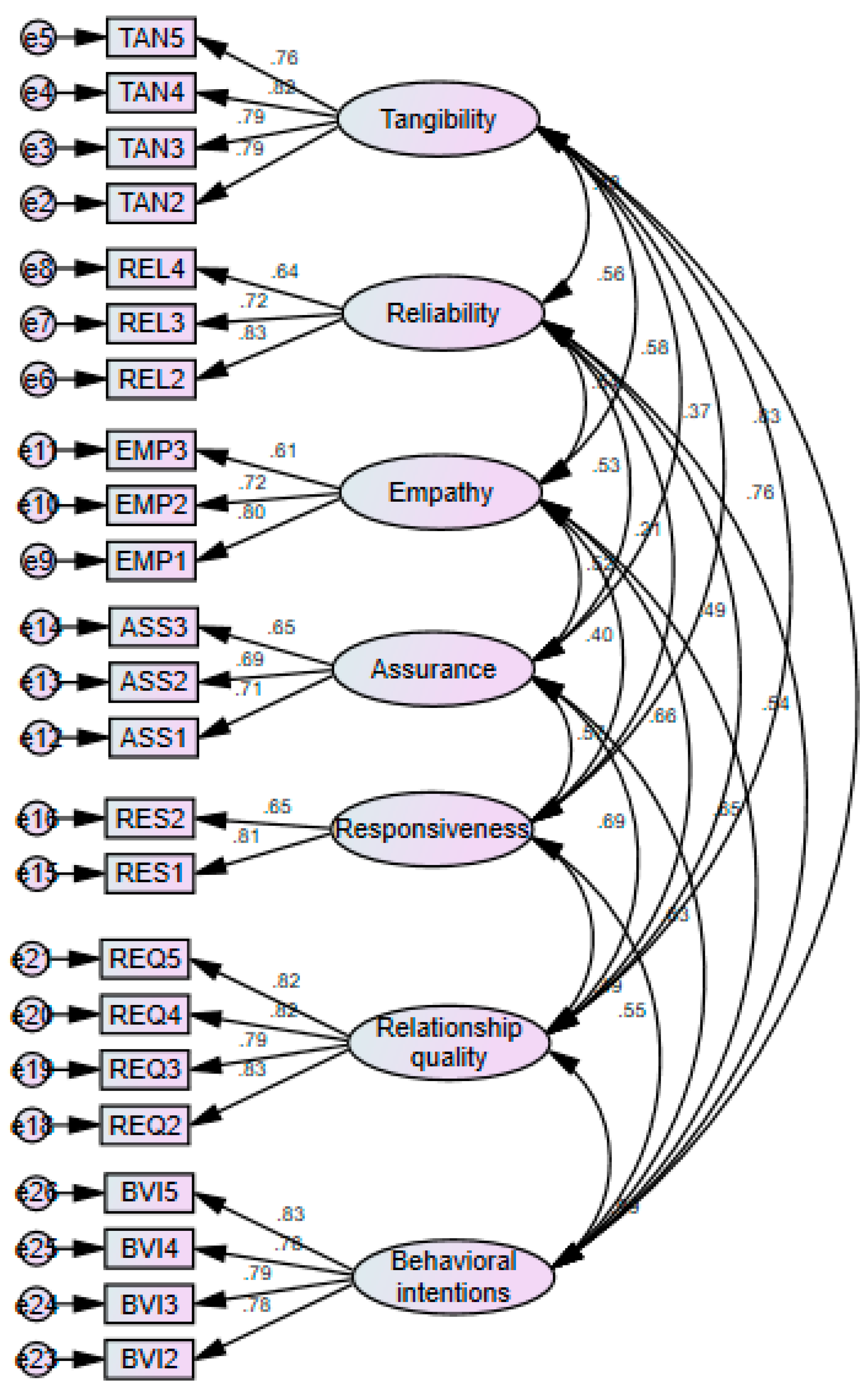

5.2. Testing of the Measurement Model: Construct Reliability and Validity

5.3. Model Fit Testing

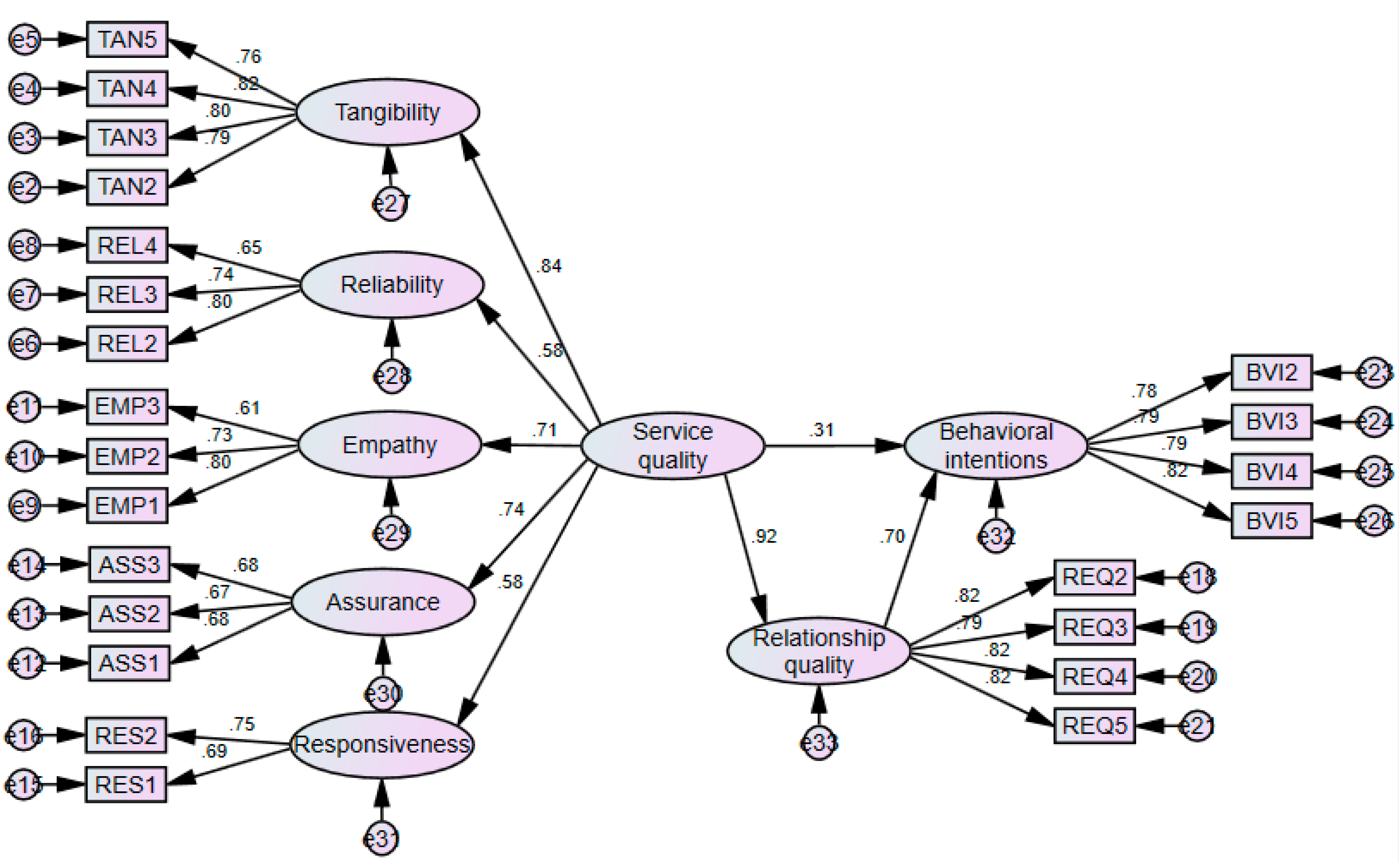

5.4. Hypothesis Testing

6. Discussion and Implications

6.1. Theoretical Implications

6.2. Managerial Implications

7. Conclusions

Limitations and Further Research

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Conflicts of Interest

References

- Uddin, M.J.; Rahman, M.M.; Rahaman, M.S. Convergent effect of work-family conflict on job satisfaction of commercial bank’s employees in Bangladesh: Does gender role moderate the effect? Indep. Bus. Rev. 2017, 10, 55–70. [Google Scholar]

- Hossain, M.U.; Asheq, A.A.; Arifuzzaman, S.M. The entrepreneurial intention of Bangladeshi students: The impact of individual and contextual factors. Probl. Perspect. Manag. 2019, 17, 493–503. [Google Scholar]

- Bangladesh Bank. Available online: https://www.bb.org.bd/fnansys/bankfi.php (accessed on 23 March 2020).

- Bakar, H.O.; Sulong, Z. The Role of Financial Sector on Economic Growth: Theoretical and Empirical Literature Reviews Analysis. J. Glob. Econ. 2018, 6, 309. [Google Scholar] [CrossRef]

- Bangladesh Bank. Banking Sector Performance, Regulation and Bank Supervision. Source: Department of Off-Site Supervision and Banking Regulation and Policy Department, Bangladesh Bank. 2020. Available online: https://www.bb.org.bd/pub/annual/anreport/ar2021/chap5.pdf (accessed on 30 June 2021).

- Cameran, M.; Moizer, P.; Pettinicchio, A. Customer satisfaction, corporate image, and service quality in professional services. Serv. Ind. J. 2010, 30, 421–435. [Google Scholar] [CrossRef]

- Parasuraman, A.; Zeithaml, V.A.; Berry, L.L. A conceptual model of service quality and its implications for future research. J. Mark. 1985, 49, 41–50. [Google Scholar] [CrossRef]

- Zeithaml, V.A. Service quality, profitability, and the economic worth of customers: What we know and what we need to learn. J. Acad. Mark. Sci. 2000, 28, 67–85. [Google Scholar] [CrossRef]

- Rahim, A.G. Perceived service quality and customer loyalty: The mediating effect of passenger satisfaction in the Nigerian Airline Industry. Int. J. Manag. Econ. 2016, 52, 94–117. [Google Scholar] [CrossRef]

- Chen, M.; Shen, C.W. The correlation analysis between the service quality of an intelligent library and the behavioral intention of users. Electron. Libr. 2019, 38, 95–112. [Google Scholar] [CrossRef]

- Grönroos, C. A service quality model and its marketing implications. Eur. J. Mark. 1984, 18, 836–844. [Google Scholar] [CrossRef]

- Amin, M.; Isa, Z.; Fontaine, R. Islamic banks: Contrasting the drivers of customer satisfaction on image, trust, and loyalty of Muslim and non-Muslim customers in Malaysia. Int. J. Bank Mark. 2013, 31, 79–97. [Google Scholar] [CrossRef]

- Clemes, M.D.; Shu, X.; Gan, C. Mobile communications: A comprehensive hierarchical modelling approach. Asia Pacific J. Mark. Logist. 2014, 26, 114–146. [Google Scholar] [CrossRef]

- De Matos, C.A.; Henrique, J.L.; de Rosa, F. The different roles of switching costs on the satisfaction loyalty relationship. Int. J. Bank Mark. 2009, 27, 506–523. [Google Scholar] [CrossRef]

- Kheng, L.L.; Mahamad, O.; Ramayah, T.M.; Mosahab, R. The impact of service quality on customer loyalty: A study of banks in Penang. Malaysia. Int. J. Mark. Stud. 2010, 2, 57–66. [Google Scholar] [CrossRef]

- Kumar, A. Effect of service quality on customer loyalty and the mediating role of customer satisfaction: An empirical investigation for the telecom service industry. J. Manag. Res. Anal. 2017, 4, 159–166. [Google Scholar]

- Pakurár, M.; Haddad, H.; Nagy, J.; Popp, J.; Oláh, J. The service quality dimensions that affect customer satisfaction in the Jordanian banking sector. Sustainability 2019, 11, 1113. [Google Scholar] [CrossRef]

- Cronin, J.; Taylor, S. Measuring service quality: A re-examination and extension. J. Mark. 1992, 56, 55. [Google Scholar] [CrossRef]

- Van Dyke, T.P.; Kappelman, L.A.; Prybutok, V.R. Measuring information systems service quality: Concerns on the use of the SERVQUAL questionnaire. MIS Q. 1997, 21, 195–208. [Google Scholar] [CrossRef]

- Ranasinghe, S. Service Quality and Customer Loyalty in the State Banks in Sri Lanka. Int. J. Innov. Res. Dev. 2021, 10, 7. [Google Scholar] [CrossRef]

- Dey, T.; Saha, T.; Salam, M.A.; Roy, S.K. Relationship between service quality and user satisfaction: An analysis of Ride-Sharing Services in Bangladesh based on SERVQUAL dimensions. J. Noakhali Sci. Technol. Univ. 2019, 3, 36–46. [Google Scholar]

- Schiffman, L.G.; Wisenblit, J.L. Consumer Behavior, Global Edition; Pearson Education Ltd.: London, UK, 2019. [Google Scholar]

- Dandis, A.O.; Wright, L.T.; Wallace-Williams, D.M.; Mukattash, I.; Al Haj Eid, M.; Cai, H. Enhancing consumers’ self-reported loyalty intentions in Islamic Banks: The relationship between service quality and the mediating role of customer satisfaction. Cogent Bus. Manag. 2021, 8, 1892256. [Google Scholar] [CrossRef]

- Narteh, B. Service quality and customer satisfaction in Ghanaian retail banks: The moderating role of price. Int. J. Bank Mark. 2018, 36, 68–88. [Google Scholar] [CrossRef]

- Yilmaz, V.; Ari, E.; Gürbüz, H. Investigating the relationship between service quality dimensions, customer satisfaction, and loyalty in the Turkish banking sector: An application of structural equation model. Int. J. Bank Mark. 2018, 36, 423–440. [Google Scholar] [CrossRef]

- Anouze, A.L.M.; Alamro, A.S.; Awwad, A.S. Customer satisfaction and its measurement in Islamic banking sector: A revisit and update. J. Islam. Mark. 2019, 10, 565–588. [Google Scholar] [CrossRef]

- Ryu, K.; Lee, H.R.; Kim, W.G. The influence of the quality of the physical environment, food, and service on restaurant image, customer perceived value, customer satisfaction, and behavioral intentions. Int. J. Contemp. Hosp. Manag. 2012, 24, 200–223. [Google Scholar] [CrossRef]

- Estrada, M.; Monferrer, D.; Moliner, M.A. Improving Relationship Quality during the Crisis. Serv. Ind. J. 2020, 40, 268–289. [Google Scholar] [CrossRef]

- Parasuraman, A.; Zeithaml, V.A.; Berry, L.L. Servqual: A multiple-item scale for measuring consumer perceptions of service quality. J. Retail. 1988, 64, 12–40. [Google Scholar]

- Rajaguru, R. Role of value for money and service quality on behavioral intention: A study of full service and low-cost airlines. J. Air Transp. Manag. 2016, 53, 114–122. [Google Scholar] [CrossRef]

- Zeithaml, V.; Berry, L.; Parasuraman, A. The Behavioral Consequences of Service Quality. J. Mark. 1996, 60, 31–46. [Google Scholar] [CrossRef]

- Kusumawardani, A.M.; Aruan, D.T.H. Comparing the effects of service quality and value-for-money on customer satisfaction, airline image, and behavioral intention between full-service and low-cost airlines: Evidence from Indonesia. Int. J. Tour. Policy 2019, 9, 27–49. [Google Scholar] [CrossRef]

- Paul, J.; Mittal, A.; Srivastav, G. Impact of service quality on customer satisfaction in private and public sector banks. Int. J. Bank Mark. 2016, 34, 606–622. [Google Scholar] [CrossRef]

- Aarhaug, J.; Olsen, S. Implications of ride-sourcing and self-driving vehicles on the need for regulation in unscheduled passenger transport. Res. Transp. Econ. 2018, 69, 573–582. [Google Scholar] [CrossRef]

- Li, F.; Lu, H.; Hou, M.; Cui, K.; Darbandi, M. Customer satisfaction with bank services: The role of cloud services, security, e-learning and service quality. Technol. Soc. 2021, 64, 101487. [Google Scholar] [CrossRef]

- Linares, M.P.; Barceló, J.; Carmona, C.; Montero, L. Analysis and operational challenges of dynamic ridesharing demand-responsive transportation models. Transp. Res. Procedia 2017, 21, 110–129. [Google Scholar] [CrossRef]

- Gupta, K.K.; Bansal, I. Development of an Instrument to measure Internet Banking Service Quality in India. Int. Ref. Res. J. 2012, 2, 11–25. [Google Scholar]

- Abdelghani, E. Applying SERVQUAL to banking services: An exploratory study in Morocco. Stud. Bus. Econ. 2012, 7, 62–72. [Google Scholar]

- Huntley, J.K. Conceptualization and measurement of relationship quality: Linking relationship quality to actual sales and recommendation intention. Ind. Mark. Manag. 2006, 35, 703–714. [Google Scholar] [CrossRef]

- Vesel, P.; Zabkar, V. Comprehension of relationship quality in the retail environment. Manag. Serv. Qual. 2010, 20, 213–235. [Google Scholar] [CrossRef]

- Palmatier, R.W.; Dant, R.P.; Grewal, D.; Evans, K.R. Factors influencing the effectiveness of relationship marketing: A meta-analysis. J. Mark. 2006, 70, 136–153. [Google Scholar] [CrossRef]

- Parasuraman, A.; Zeithaml, V.A.; Malhotra, A. E-SQUAL: A multiple-item scale for assessing electronic service quality. J. Serv. Res. 2005, 7, 213–234. [Google Scholar] [CrossRef]

- Bakar, J.A.; Clemes, M.D.; Bicknell, K.A. Comprehensive hierarchical model of retail banking. Int. J. Bank Mark. 2017, 35, 662–684. [Google Scholar] [CrossRef]

- Kim, Y.E.; Yang, H.C. The effects of perceived satisfaction level of high-involvement product choice attribute of the millennial generation on repurchase intention: Moderating effect of gender difference. J. Asian Financ. Econ. Bus. 2019, 7, 131–140. [Google Scholar] [CrossRef]

- Veloso, C.M.; Sousa, B.B. Drivers of customer behavioral intentions and the relationship with service quality in specific industry contexts. Int. Rev. Retail Distrib. Consum. Res. 2022, 32, 43–58. [Google Scholar] [CrossRef]

- Tran, V.D.; Le, N.M.T. Impact of service quality and perceived value on customer satisfaction and behavioral intentions: Evidence from convenience stores in Vietnam. J. Asian Financ. Econ. Bus. 2020, 7, 517–526. [Google Scholar] [CrossRef]

- Mpwanya, M.F.; Letsoalo, M.E. Relationship between service quality, customer satisfaction and behavioural intentions in South Africa’s mobile telecommunication industry. Afr. J. Bus. Econ. Res. 2019, 14, 67. [Google Scholar] [CrossRef]

- Boonlertvanich, K. Service quality, satisfaction, trust, and loyalty: The moderating role of main-bank and wealth status. Int. J. Bank Mark. 2019, 37, 278–302. [Google Scholar] [CrossRef]

- Bahia, K.; Nantel, J. A Reliable and Valid Measurement Scale for Perceived Service Quality of Banks. Int. J. Bank Mark. 2000, 18, 84–91. [Google Scholar] [CrossRef]

- Parasuraman, L.; Berry, L.; Zeithaml, V.A. Refinement and reassessment of the SERVQUAL scale. J. Retail. 1991, 67, 420–450. [Google Scholar]

- Hadid, K.I.; Soon, N.K.; Amreeghah, A.A.E. The effect of digital banking service quality on customer satisfaction: A case study on the Malaysian banks. Asian J. Appl. Sci. Technol. 2020, 4, 6–29. [Google Scholar] [CrossRef]

- Othman, B.A.; Harun, A.; Rashid, W.N.; Nazeer, S.; Kassim, W.M.; Kadhim, K.G. The influences of service marketing mix on customer loyalty towards Umrah travel agents: Evidence from Malaysia. Manag. Sci. Lett. 2019, 6, 865–876. [Google Scholar] [CrossRef]

- Boshoff, C.; Du Plessis, P.J. Services Marketing: A Contemporary Approach, 2nd ed.; Juta and Company Ltd.: Cape Town, South Africa, 2014. [Google Scholar]

- Kim, W.G.; Lee, Y.; Yoo, Y. Predictors of relationship quality and relationship outcomes in luxury restaurants. J. Hosp. Tour. Res. 2006, 30, 143–169. [Google Scholar] [CrossRef]

- Akintan, I.; Dabiri, M.; Jolaosho, S. Assessing Service Quality Dimensions on Customers Patronage of Islamic Banking in South-Western Nigeria. Int. J. Res. Commer. Manag. Stud. 2020, 2, 76–98. [Google Scholar]

- Rather, R.A.; Camilleri, M.A. The effects of service quality and consumer-brand value congruity on hospitality brand loyalty. Anatolia 2019, 30, 547–559. [Google Scholar] [CrossRef]

- Tran, V.D. Assessing the effects of service quality, experience value, relationship quality on behavioral intentions. J. Asian Financ. Econ. Bus. 2020, 7, 167–175. [Google Scholar] [CrossRef]

- Cronin, J.J.; Brady, M.K.; Hult, G.T. Assessing the effects of quality, value, and customer satisfaction on consumer behavioral intentions in service environments. J. Retail. 2000, 76, 193–218. [Google Scholar] [CrossRef]

- Roberts, K.; Varki, S.; Brodie, R. Measuring the quality of relationships in consumer services: An empirical study. Eur. J. Mark. 2003, 37, 169–196. [Google Scholar] [CrossRef]

- Lee, J.; Lee, J.E.; Breiter, D. Relationship marketing investment, relationship quality, and behavioral intention: In the context of the relationship between destination marketing organizations and meeting/convention planners. J. Conv. Event Tour. 2016, 17, 21–40. [Google Scholar] [CrossRef]

- Wu, H.C.; Li, T. An empirical study of the effects of service quality, visitor satisfaction, and emotions on behavioral intentions of visitors to the museums of Macau. J. Qual. Assur. Hosp. Tour. 2015, 16, 80–102. [Google Scholar] [CrossRef]

- Woodside, A.G.; Frey, L.L.; Daly, R.T. Linking service quality, customer satisfaction, and behavioral intention. J. Health Care Mark. 1989, 9, 5–17. [Google Scholar]

- Howat, G.; Assaker, G. The hierarchical effects of perceived quality on perceived value, satisfaction, and loyalty: Empirical results from public, outdoor aquatic centers in Australia. Sport Manag. Rev. 2013, 16, 268–284. [Google Scholar] [CrossRef]

- Das, S.; Jannat, F. Impact of Service Quality on Customers’ Satisfaction: An Empirical Study on State-Owned Commercial Banks in Bangladesh. J. Manag. 2018, 12, 31–48. [Google Scholar]

- Jahan, N.; Hossain, M.A.; Fang, Y. Multiple Mediating Effects on the Quality of and Loyalty to Banking Services. Asian Econ. Financ. Rev. 2020, 10, 1248–1258. [Google Scholar] [CrossRef]

- Morgan, R.M.; Hunt, S.D. The commitment-trust theory of relationship marketing. J. Mark. 1994, 58, 20–38. [Google Scholar] [CrossRef]

{kind=link}

{kind=link}

| Authors | Purpose | Country and Context | Dimensions | Essential Findings |

|---|---|---|---|---|

| Veloso and Sousa [45] | This paper determined customer satisfaction and loyalty, as well as the relationship with the perceived quality of service in traditional retail stores and proposed a conceptual model to analyze whether perceived SQ (five dimensions of SERVQUAL) directly contribute to customer satisfaction and customer-perceived value. | South and Island regions of Portugal | SQ, customer loyalty, Portugal, retail stores, consumer behavior | The findings show that SQ significantly influences corporate image, perceived value, and customer satisfaction. Furthermore, perceived value and quality of service are the main determinants of customer satisfaction. Additionally, customer satisfaction, corporate image, and perceived value significantly affect BVI towards the act of buying. |

| Ranasinghe [20] | The empirical research aimed to determine the relationship between SQ and customer loyalty with special reference to state banks. | Sri Lanka | Customer loyalty, SQ, reliable, empathy, accuracy, responsiveness | The results show the significant impact of the service tangibility dimension and customer loyalty; they also indicate that the service reliability dimension is the most effective connection to customer loyalty. |

| Tran and Le [46] | This research examines the association among product quality, SQ, perceived value, customer satisfaction, and BVI. | Vietnam | Product quality, SQ, perceived value, customer satisfaction, BVI | The findings illustrate the direct relationship between product quality and perceived value regarding customer satisfaction and BVI. For the indirect path, SQ has a positive influence on BVI through customer satisfaction. |

| Mpwanya and Letsoalo [47] | The study explores the relationship between SQ, customer satisfaction, and BVI in South Africa’s mobile telecommunications industry. | South Africa | SQ, customer satisfaction, and BVI | The results demonstrate that tangibles, customer relations, real network quality, and image quality, as well as customer satisfaction, are meaningfully correlated in the South African mobile telecommunications industry, additionally showing the connection between the constructs of SQ, reasonably influencing customer satisfaction. |

| Boonlertvanich [48] | This study aims to create a comprehensive model representing the connections among SQ, customer satisfaction, trust, and loyalty in retail banking service. | Thailand | Satisfaction, trust, SQ, loyalty, customer wealth, main-bank status | The results show that customer-perceived service quality directly and indirectly affects, via satisfaction and trust, attitudinal and behavioral loyalty. SQ influences customer loyalty less if the customer holds main-bank status. |

| Bakar et al. [43] | This paper uses comprehensive hierarchical modeling to synthesize the effects of SQ, customer satisfaction, perceived value, corporate image, and switching costs on the BVI of retail bank customers. | Malaysia | Retail banking, Structural equation modeling, BVI, comprehensive hierarchical modeling | The results explain that customer satisfaction is the most significant element of BVI, followed by switching costs, corporate image, and perceived value. SQ is indirectly related to BVI, and customer satisfaction mediates the relationship between the two constructs. |

| CR | AVE | Alpha | REQ | TAN | REL | EMP | ASS | RES | BVI | |

|---|---|---|---|---|---|---|---|---|---|---|

| REQ | 0.886 | 0.661 | 0.886 | 0.813 | ||||||

| TAN | 0.871 | 0.627 | 0.869 | 0.765 | 0.792 | |||||

| REL | 0.775 | 0.537 | 0.773 | 0.490 | 0.477 | 0.733 | ||||

| EMP | 0.758 | 0.514 | 0.755 | 0.665 | 0.557 | 0.535 | 0.717 | |||

| ASS | 0.724 | 0.467 | 0.720 | 0.691 | 0.585 | 0.529 | 0.515 | 0.683 | ||

| RES | 0.695 | 0.535 | 0.662 | 0.494 | 0.366 | 0.207 | 0.399 | 0.574 | 0.732 | |

| BVI | 0.874 | 0.634 | 0.873 | 0.296 | 0.633 | 0.542 | 0.648 | 0.627 | 0.552 | 0.796 |

| Indices | Recommended Value | Measurement Model | Structural Model |

|---|---|---|---|

| CMIN/DF | <3 | 1.848 | 1.928 |

| CFI | ≥0.90 | 0.940 | 0.930 |

| AGFI | ≥0.80 | 0.829 | 0.829 |

| TLI | ≥0.80 | 0.927 | 0.920 |

| RMSEA | ≤0.08 | 0.060 | 0.063 |

| Hypotheses | Paths | Std. Coefficient (t-Value) | Result | |||||

|---|---|---|---|---|---|---|---|---|

| H1a | Tangibility | ---> | Service quality | 0.84 (fixed) *** | Accepted | |||

| H1b | Reliability | ---> | Service quality | 0.58 (6.89) *** | Accepted | |||

| H1c | Empathy | ---> | Service quality | 0.705 (8.07) *** | Accepted | |||

| H1d | Assurance | ---> | Service quality | 0.736 (7.40) *** | Accepted | |||

| H1e | Responsiveness | ---> | Service quality | 0.579 (5.71) *** | Accepted | |||

| H2a | Service quality | ---> | Relationship quality | 0.919 (10.05) *** | Accepted | |||

| H2b | Service quality | ---> | Behavioral intentions | 0.313 (1.92) ** | Accepted | |||

| H3a | Relationship quality | ---> | Behavioral intentions | 0.698 (4.28) *** | Accepted | |||

| Mediating results (Bootstrapping bias-corrected model with 95% confidence interval) | ||||||||

| Indirect effect | Lower bound | Upper bound | p-value | |||||

| H3b | Service quality --->Relationship quality ---> Behavioral intentions | 0.64 | 0.05 | 0.17 | ** | Mediated | ||

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2023 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Yesmin, M.N.; Hoque, S.; Hossain, M.A.; Jahan, N.; Fang, Y.; Wu, R.; Alam, M.J. SERVQUAL to Determine Relationship Quality and Behavioral Intentions: An SEM Approach in Retail Banking Service. Sustainability 2023, 15, 6536. https://doi.org/10.3390/su15086536

Yesmin MN, Hoque S, Hossain MA, Jahan N, Fang Y, Wu R, Alam MJ. SERVQUAL to Determine Relationship Quality and Behavioral Intentions: An SEM Approach in Retail Banking Service. Sustainability. 2023; 15(8):6536. https://doi.org/10.3390/su15086536

Chicago/Turabian StyleYesmin, Most. Nirufer, Saiful Hoque, Md. Alamgir Hossain, Nusrat Jahan, Yuantao Fang, Renhong Wu, and Md. Jahangir Alam. 2023. "SERVQUAL to Determine Relationship Quality and Behavioral Intentions: An SEM Approach in Retail Banking Service" Sustainability 15, no. 8: 6536. https://doi.org/10.3390/su15086536

APA StyleYesmin, M. N., Hoque, S., Hossain, M. A., Jahan, N., Fang, Y., Wu, R., & Alam, M. J. (2023). SERVQUAL to Determine Relationship Quality and Behavioral Intentions: An SEM Approach in Retail Banking Service. Sustainability, 15(8), 6536. https://doi.org/10.3390/su15086536