Do Carbon Emission Trading Schemes Promote the Green Transition of Enterprises? Evidence from China

Abstract

1. Introduction

2. Literature Review

2.1. Environmental Regulations and Green Transition of Enterprises

2.2. Research Related to Carbon Emission Trading Schemes

2.3. Research related to the Evaluation of Green Transition

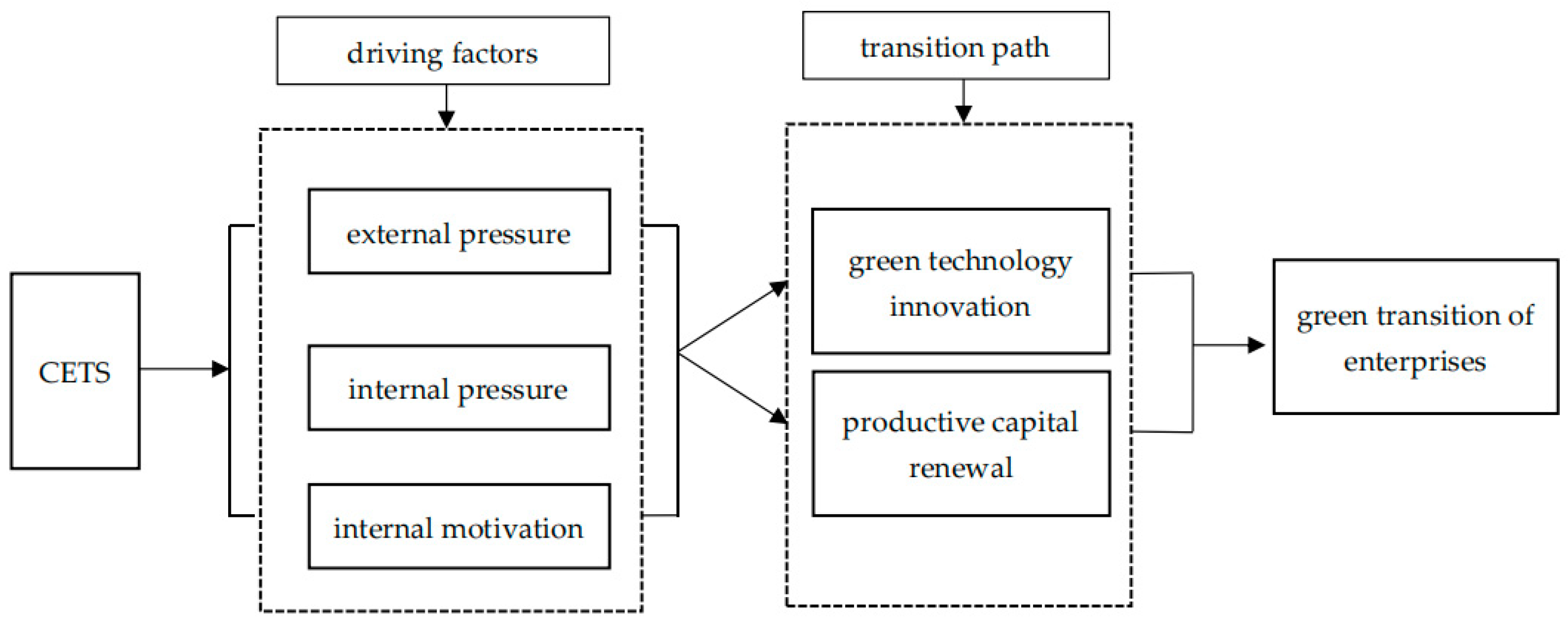

3. Theoretical Mechanism and Hypotheses

3.1. CETS and Green Transition of Heavy-Polluting Enterprises

3.2. Analysis of the Impact Mechanism of CETS to Promote the Green Transition of Heavy-Polluting Enterprises

3.3. Heterogeneity Analysis of CETS Promoting the Green Transformation of Heavy-Polluting Enterprises

4. Methodology

4.1. Data Source and Processing

4.2. Research Model

4.2.1. Propensity Score Matching (PSM)

4.2.2. A Staggered Difference-in-Difference Model

4.3. Variable and Definition

4.3.1. Green Transition of Enterprises (GT)

4.3.2. Carbon Emission Trading Schemes (CETS)

4.3.3. Mechanism Variables

- (1)

- Green technological innovation. Referring to the definition and classification of green technological innovation by existing scholars [93], the number of green patent applications was applied to measure green technological innovation (Patent_gre), which was the sum of the number of green invention patent applications and green utility model patent applications. In addition, the numbers of green invention patent applications and green utility model patent applications were used to measure the substantial green technological innovation (Green_inv) and strategic green technological innovation (Green_uti) in this paper, respectively.

- (2)

4.3.4. Control Variables

5. Empirical Results

5.1. Propensity Score Matching

5.2. Benchmark Regression Results

5.3. Robustness Test

- Change the matching method of PSM

- 2.

- Use one-period lagged control variables

- 3.

- Counterfactual analysis

- 4.

- Eliminate interference from other environmental policies

- 5.

- Considering the heterogeneous treatment effects of staggered DID

6. Further Discussion

6.1. Mechanism Analysis

6.1.1. Green Technological Innovation

6.1.2. Productive Capital Renewal

6.2. Heterogeneity Analysis

6.2.1. Heterogeneity Effect of Different Cost Transfer Abilities

6.2.2. Heterogeneity Effect of Different Levels of Financing Constraints

6.2.3. Heterogeneity Effect of Different Internal Control Systems

6.2.4. Heterogeneity Effect of Different Environmental Enforcement Intensities

7. Conclusions

8. Recommendations

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Conflicts of Interest

Appendix A

{kind=link}

| Variable | Unmatched | Mean | %bias | %Reduct | t Test | ||

|---|---|---|---|---|---|---|---|

| Matched | Treatment Group | Control Group | |bias| | t | p > |t| | ||

| size | U | 22.065 | 22.487 | −32.8 | 76.8 | −1.20 | 0.231 |

| M | 22.091 | 22.189 | −7.6 | −0.19 | 0.848 | ||

| lev | U | 0.5375 | 0.5107 | 12.1 | 68.7 | 0.46 | 0.078 |

| M | 0.5459 | 0.5375 | 3.8 | 0.09 | 0.645 | ||

| roa | U | 0.0349 | 0.0284 | 12.4 | 25.6 | 0.42 | 0.672 |

| M | 0.0280 | 0.0328 | −9.2 | −0.24 | 0.814 | ||

| indep | U | 0.3618 | 0.3676 | −12.2 | 67.3 | −0.44 | 0.664 |

| M | 0.3608 | 0.3627 | −4.0 | −0.10 | 0.921 | ||

| board | U | 2.2201 | 2.215 | 3.1 | −16.9 | 0.10 | 0.922 |

| M | 2.2309 | 2.225 | 3.6 | −0.10 | 0.925 | ||

| growth | U | 0.1728 | 0.0987 | 26.2 | 73.2 | 0.77 | 0.442 |

| M | 0.1620 | 0.1422 | 7.0 | 0.16 | 0.874 | ||

| bm | U | 1.5758 | 1.866 | −18.2 | 66.2 | −0.61 | 0.541 |

| M | 1.647 | 1.7451 | −6.1 | −0.15 | 0.879 | ||

| listage | U | 2.5318 | 2.3902 | 26.6 | 90.5 | 1.03 | 0.303 |

| M | 2.4923 | 2.4789 | 2.5 | 0.07 | 0.948 | ||

| tobinq | U | 1.7776 | 1.5036 | 36.5 | 48.9 | 1.28 | 0.201 |

| M | 1.7241 | 1.584 | 18.7 | 0.48 | 0.637 | ||

| cashflow | U | 0.0757 | 0.0518 | 33.3 | 53.5 | 1.32 | 0.189 |

| M | 0.0624 | 0.0735 | −15.5 | −0.43 | 0.671 | ||

| Variable | Unmatched | Mean | %bias | %Reduct | t Test | ||

|---|---|---|---|---|---|---|---|

| Matched | Treatment Group | Control Group | |bias| | t | Matched | ||

| size | U | 22.549 | 22.609 | −4.8 | −80.8 | −1.20 | 0.231 |

| M | 22.549 | 22.441 | 8.6 | −0.19 | 0.848 | ||

| lev | U | 0.4843 | 0.4882 | −2.1 | 96.8 | −0.07 | 0.948 |

| M | 0.4843 | 0.4844 | −0.1 | −0.00 | 0.999 | ||

| roa | U | 0.0050 | 0.0161 | −17.3 | 26.3 | −0.63 | 0.528 |

| M | 0.0050 | −0.0032 | 12.7 | 0.30 | 0.770 | ||

| indep | U | 0.3694 | 0.3674 | 4.4 | 95.3 | 0.16 | 0.872 |

| M | 0.3694 | 0.3693 | 0.2 | 0.01 | 0.996 | ||

| board | U | 2.163 | 2.1876 | −14.8 | 98.5 | −0.49 | 0.622 |

| M | 2.163 | 2.1627 | 0.2 | 0.01 | 0.995 | ||

| growth | U | 0.0138 | −0.0341 | 15.1 | −2.2 | 0.60 | 0.552 |

| M | 0.0138 | −0.0351 | 15.4 | 0.38 | 0.706 | ||

| bm | U | 0.7795 | 1.1121 | −36.7 | 94.8 | −1.04 | 0.300 |

| M | 0.7795 | 0.7622 | 1.9 | 0.09 | 0.926 | ||

| listage | U | 2.6317 | 2.576 | 14.6 | 72.9 | 0.51 | 0.613 |

| M | 2.6317 | 2.6167 | 4.0 | 0.11 | 0.915 | ||

| tobinq | U | 2.1673 | 2.2857 | −9.2 | 59.8 | −0.30 | 0.762 |

| M | 2.1673 | 2.2149 | −3.7 | −0.11 | 0.912 | ||

| cashflow | U | 0.0523 | 0.0554 | −4.3 | −53.4 | −0.17 | 0.867 |

| M | 0.0523 | 0.0571 | −6.7 | −017 | 0.868 | ||

Super-Efficiency SBM Model and Global Malmquist-Luenberger (GML) Productivity Index

References

- Yang, X.; Jiang, P.; Pan, Y. Does China’s carbon emission trading policy have an employment double dividend and a Porter effect? Energy Policy 2020, 142, 111492. [Google Scholar] [CrossRef]

- Fang, K.; Zhang, Q.; Long, Y.; Yoshida, Y.; Sun, L.; Zhang, H.; Dou, Y.; Li, S. How can China achieve its Intended Nationally Determined Contributions by 2030? A multi-criteria allocation of China’s carbon emission allowance. Appl. Energy 2019, 241, 380–389. [Google Scholar] [CrossRef]

- Mallapaty, S. How China could be carbon neutral by mid-century. Nature 2020, 586, 482–484. [Google Scholar] [CrossRef]

- Wang, K.; Li, S.Y. China’s Carbon Market: Reviews and Prospects (2022). J. Bejing Inst. Technol. (Soc. Sci. Ed.) 2022, 24, 33–42. [Google Scholar]

- Ortega-Gras, J.J.; Bueno-Delgado, M.V.; Cañavate-Cruzado, G.; Garrido-Lova, J. Twin Transition through the Implementation of Industry 4.0 Technologies: Desk-Research Analysis and Practical Use Cases in Europe. Sustainability 2021, 13, 13601. [Google Scholar] [CrossRef]

- Chatzistamoulou, N.; Tyllianakis, E. Commitment of European SMEs to resource efficiency actions to achieve sustainability transition. A feasible reality or an elusive goal? J. Environ. Manag. 2022, 321, 115937. [Google Scholar] [CrossRef]

- Niu, H.; Zhao, X.; Luo, Z.; Gong, Y.; Zhang, X. Green credit and enterprise green operation: Based on the perspective of enterprise green transformation. Front. Psychol. 2022, 13, 1041798. [Google Scholar] [CrossRef] [PubMed]

- Pan, A.; Liu, X.; Qiu, J.; Shen, Y. Can green M&A of heavy polluting enterprises achieve substantial transformation under the pressure of media. China Ind. Econ. 2019, 2, 174–192. [Google Scholar]

- Zhang, J.J.; Yu, L.; Bi, Q.; Pan, J. Media supervision, environmental regulation and firm green investment. J. Shanghai Univ. Financ. Econ. 2016, 185, 91–103. [Google Scholar]

- Qian, B.I.; Hong-yuan, L.I. Can Green Tax Incentives Promote Green Transformation of Enterprises. J. Guizhou Univ. Financ. Econ. 2019, 37, 89. [Google Scholar]

- Dang, D. Can environmental subsidies promote the green investment of enterprises? Mod. Econ. 2020, 11, 109. [Google Scholar] [CrossRef]

- Wan, P.B.; Yang, M.; Chen, L. How do environmental technology standards affect the green transition of China’s manufacturing industry—A perspective from technological transformation. China Ind. Econ. 2021, 9, 118–136. [Google Scholar]

- Yu, L.C.; Zhang, W.G.; Bi, Q. Can the reform of environmental protection fee-to-tax promote the green transformation of high-polluting enterprises. China Popul. Resour. Environ. 2021, 31, 109–118. [Google Scholar]

- Wang, X.Q.; Ning, J.H. Can mandatory social responsibility disclosure drive corporate green transformation?—Evidence based on green patent data of listed companies in China. J. Audit Econ. 2020, 35, 69–77. [Google Scholar]

- Hu, G.; Wang, X.; Wang, Y. Can the green credit policy stimulate green innovation in heavily polluting enterprises? Evidence from a quasi-natural experiment in China. Energy Econ. 2021, 98, 105134. [Google Scholar] [CrossRef]

- Martin, R.; Muûls, M.; Wagner, U.J. The impact of the European Union Emissions Trading Scheme on regulated firms: What is the evidence after ten years? Rev. Environ. Econ. Policy 2016, 10, 129–148. [Google Scholar] [CrossRef]

- Zhang, X.; Zhang, D.; Yu, R. Theory and Practice of China’s National Carbon Emissions Trading System. Manag. World 2021, 37, 80–95. [Google Scholar]

- Porter, M.E.; Van der Linde, C. Toward a new conception of the environment-competitiveness relationship. J. Econ. Perspect. 1995, 9, 97–118. [Google Scholar] [CrossRef]

- Liu, Y.; Li, Z.; Yin, X. Environmental regulation, technological innovation and energy consumption—A cross-region analysis in China. J. Clean Prod. 2018, 203, 885–897. [Google Scholar] [CrossRef]

- Gans, J.S. Innovation and climate change policy. American Economic Journal. Econ. Policy 2012, 4, 125–145. [Google Scholar]

- Rassier, D.G.; Earnhart, D. Does the porter hypothesis explain expected future financial performance? The effect of clean water regulation on chemical manufacturing firms. Environ. Resour. Econ. 2010, 45, 353–377. [Google Scholar] [CrossRef]

- Li, S.B.; Guo, Y.L. The Economic Impact and Policy Instrument Choice of Envronmental Regulaton: A Literature Review. Ind. Organ. Rev. 2021, 1, 200–219. [Google Scholar]

- He, L.Y.; Qi, X.F. Environmental Regulation and Green Total Factor Productivity: Evidence from China’s Marine Economy. Pol. J. Environ. Stud. 2021, 30, 5117–5131. [Google Scholar]

- Zhu, X.; He, M.; Li, H. Environmental regulation, governance transformation and the green development of Chinese iron and steel enterprises. J. Clean Prod. 2021, 328, 129557. [Google Scholar] [CrossRef]

- Tvinnereim, E.; Mehling, M. Carbon pricing and deep decarbonisation. Energy Policy 2018, 121, 185–189. [Google Scholar] [CrossRef]

- Bayer, P.; Aklin, M. The European Union emissions trading system reduced CO2 emissions despite low prices. Proc. Natl. Acad. Sci. USA 2020, 117, 8804–8812. [Google Scholar] [CrossRef]

- Bakam, I.; Balana, B.B.; Matthews, R. Cost-effectiveness analysis of policy instruments for greenhouse gas emission mitigation in the agricultural sector. J. Environ. Manag. 2012, 112, 33–44. [Google Scholar] [CrossRef]

- Qi, X.; Han, Y. The design of the intertemporal trading ratio of carbon quotas. J. Clean Prod. 2022, 370, 133481. [Google Scholar] [CrossRef]

- He, W.; Zhang, B.; Li, Y.; Chen, H. A performance analysis framework for carbon emission quota allocation schemes in China: Perspectives from economics and energy conservation. J. Environ. Manag. 2021, 296, 113165. [Google Scholar] [CrossRef]

- Chen, S.; Shi, A.; Wang, X. Carbon emission curbing effects and influencing mechanisms of China’s Emission Trading Scheme: The mediating roles of technique effect, composition effect and allocation effect. J. Clean Prod. 2020, 264, 121700. [Google Scholar] [CrossRef]

- Wu, Y.; Qi, J.; Xian, Q.; Wu, J.D. The carbon emission reduction effect of China’s carbon market—The perspective of the coordination between market mechanism and administrative intervention. China Ind. Econ. 2021, 8, 114–132. [Google Scholar]

- Zhu, B.; Zhang, M.; Huang, L.; Wang, P.; Su, B.; Wei, Y.M. Exploring the effect of carbon trading mechanism on China’s green development efficiency: A novel integrated approach. Energy Econ. 2020, 85, 104601. [Google Scholar] [CrossRef]

- Zhang, S.; Wang, Y.; Hao, Y.; Liu, Z. Shooting two hawks with one arrow: Could China’s emission trading scheme promote green development efficiency and regional carbon equality? Energy Econ. 2021, 101, 105412. [Google Scholar] [CrossRef]

- Zhou, Z.; Ma, Z.; Lin, X. Carbon Emissions Trading Policy and Green Transformation of China’s Manufacturing Industry: Mechanism Assessment and Policy Implications. Front. Environ. Sci. 2022, 10, 1543. [Google Scholar] [CrossRef]

- Lei, Y.; Zhang, X.; Peng, W. Can China’s Policy of Carbon Emissions Trading Optimize Manufacturing Structure? Evidence from Guangdong Based on a Synthetic Control Approach. Sustainability 2022, 14, 3302. [Google Scholar] [CrossRef]

- García, A.; García-Álvarez, M.T.; Moreno, B. The impact of EU allowance prices on the stock market indices of the European power industries: Evidence from the ongoing EU ETS phase III. Organ. Environ. 2021, 34, 459–478. [Google Scholar] [CrossRef]

- Mo, J.Y. Environmental policy and R&D productivity: A case study from the Korean Emissions Trading Scheme. Sci. Public Policy 2022, 50, 120–128. [Google Scholar]

- Li, X.; Shu, Y.; Jin, X. Environmental regulation, carbon emissions and green total factor productivity: A case study of China. Environ. Dev. Sustain. 2022, 24, 2577–2597. [Google Scholar] [CrossRef]

- Li, X.; Guo, D.; Feng, C. The Carbon Emissions Trading Policy of China: Does It Really Promote the Enterprises’ Green Technology Innovations? Int. J. Environ. Res. Public Health 2022, 19, 14325. [Google Scholar] [CrossRef]

- Calel, R.; Dechezleprêtre, A. Environmental policy and directed technological change: Evidence from the European carbon market. Rev. Econ. Stat. 2016, 98, 173–191. [Google Scholar] [CrossRef]

- Bel, G.; Joseph, S. Policy stringency under the European Union Emission trading system and its impact on technological change in the energy sector. Energy Policy 2018, 117, 434–444. [Google Scholar] [CrossRef]

- Xiao, J.; Li, G.; Zhu, B.; Xie, L.; Hu, Y.; Huang, J. Evaluating the impact of carbon emissions trading scheme on Chinese firms’ total factor productivity. J. Clean Prod. 2021, 306, 127104. [Google Scholar] [CrossRef]

- Koch, N.; Themann, M. Catching up and falling behind: Cross-country evidence on the impact of the EU ETS on firm productivity. Resour. Energy Econ. 2022, 69, 101315. [Google Scholar] [CrossRef]

- Yu, D.J.; Li, J. Evaluating the employment effect of China’s carbon emission trading policy: Based on the perspective of spatial spillover. J. Clean Prod. 2021, 292, 126052. [Google Scholar] [CrossRef]

- Marin, G.; Marino, M.; Pellegrin, C. The impact of the European Emission Trading Scheme on multiple measures of economic performance. Environ. Resour. Econ. 2018, 71, 551–582. [Google Scholar] [CrossRef]

- Makridou, G.; Doumpos, M.; Galariotis, E. The financial performance of firms participating in the EU emissions trading scheme. Energy Policy 2019, 129, 250–259. [Google Scholar] [CrossRef]

- Ferrara, A.R.; Giua, L. Indirect cost compensation under the EU ETS: A firm-level analysis. Energy Policy 2022, 165, 112989. [Google Scholar] [CrossRef]

- Dai, Y.; Li, N.; Gu, R.; Zhu, X. Can China’s carbon emissions trading rights mechanism transform its manufacturing industry? Based on the perspective of enterprise behavior. Sustainability 2018, 10, 2421. [Google Scholar] [CrossRef]

- Tang, M.; Cheng, S.; Guo, W.; Ma, W.; Hu, F. Relationship between carbon emission trading schemes and companies’ total factor productivity: Evidence from listed companies in China. Environ. Dev. Sustain. 2022, 1–33. [Google Scholar] [CrossRef]

- Chen, Z.; Zhang, X.; Chen, F. Do carbon emission trading schemes stimulate green innovation in enterprises? Evidence from China. Technol. Forecast. Soc. Chang. 2021, 168, 120744. [Google Scholar] [CrossRef]

- Luo, Y.; Li, X.; Qi, X.; Zhao, D. The impact of emission trading schemes on firm competitiveness: Evidence of the mediating effects of firm behaviors from the guangdong ETS. J. Environ. Manag. 2021, 290, 112633. [Google Scholar] [CrossRef] [PubMed]

- Zhai, X.; An, Y. Analyzing influencing factors of green transformation in China’s manufacturing industry under environmental regulation: A structural equation model. J. Clean Prod. 2020, 251, 119760. [Google Scholar] [CrossRef]

- Gong, M.; You, Z.; Wang, L.; Cheng, J. Environmental regulation, trade comparative advantage, and the manufacturing industry’s green transformation and upgrading. Int. J. Environ. Res. Public Health 2020, 17, 2823. [Google Scholar] [CrossRef] [PubMed]

- Cheng, Z.; Li, L.; Liu, J. Natural resource abundance, resource industry dependence and economic green growth in China. Resour. Policy 2020, 68, 101734. [Google Scholar] [CrossRef]

- Zhang, F.; Yao, S.; Wang, F. The role of high-speed rail on green total factor productivity: Evidence from Chinese cities. Environ. Sci. Pollut. Res. 2022, 30, 15044–15058. [Google Scholar] [CrossRef]

- Kumbhakar, S.C.; Wang, H.; Horncastle, A.P. A Practitioner’s Guide to Stochastic Frontier Analysis Using Stata; Cambridge University Press: Cambridge, UK, 2015. [Google Scholar]

- Zhong, S.; Li, Y.; Li, J.; Yang, H. Measurement of total factor productivity of green agriculture in China: Analysis of the regional differences based on China. PLoS ONE 2021, 16, e0257239. [Google Scholar] [CrossRef]

- Wang, L.; Liu, B.; He, Y.; Dong, Z.; Wang, S. Have public environmental appeals inspired green total factor productivity? empirical evidence from Baidu Environmental Search Index. Environ. Sci. Pollut. Res. 2022, 30, 30237–30252. [Google Scholar] [CrossRef]

- Liu, D.; Zhu, X.; Wang, Y. China’s agricultural green total factor productivity based on carbon emission: An analysis of evolution trend and influencing factors. J. Clean Prod. 2021, 278, 123692. [Google Scholar] [CrossRef]

- Zhang, X.; Chen, X.; Lu, C.C.; Cheng, F.Y. A comparative analysis of slack-based green total factor productivity in China: A directional distance function. Water Air Soil Pollut. 2021, 232, 466. [Google Scholar] [CrossRef]

- Ma, Y.; Lin, T.; Xiao, Q. The Relationship between Environmental Regulation, Green-Technology Innovation and Green Total-Factor Productivity—Evidence from 279 Cities in China. Int. J. Environ. Res. Public Health 2022, 19, 16290. [Google Scholar] [CrossRef]

- Bao, B.; Jin, S.; Li, L.; Duan, K.; Gong, X. Analysis of green total factor productivity of grain and its dynamic distribution: Evidence from Poyang Lake Basin, China. Agriculture 2022, 12, 8. [Google Scholar] [CrossRef]

- Li, Y.; Chen, Y. Development of an SBM-ML model for the measurement of green total factor productivity: The case of pearl river delta urban agglomeration. Renew. Sustain. Energy Rev. 2021, 145, 111131. [Google Scholar] [CrossRef]

- Oh, D. A global Malmquist-Luenberger productivity index. J. Prod. Anal. 2010, 34, 183–197. [Google Scholar] [CrossRef]

- Qiu, S.; Wang, Z.; Geng, S. How do environmental regulation and foreign investment behavior affect green productivity growth in the industrial sector? An empirical test based on Chinese provincial panel data. J. Environ. Manag. 2021, 287, 112282. [Google Scholar] [CrossRef] [PubMed]

- Suchman, M.C. Managing legitimacy: Strategic and institutional approaches. Acad. Manag. Rev. 1995, 20, 571–610. [Google Scholar] [CrossRef]

- Johnsen, T.; Phillips, W.; Caldwell, N.; Lewis, M. Centrality of customer and supplier interaction in innovation. J. Bus. Res. 2006, 59, 671–678. [Google Scholar] [CrossRef]

- Grossman, G.M.; Helpman, E. Growth, trade, and inequality. Econometrica 2018, 86, 37–83. [Google Scholar] [CrossRef]

- Ambec, S.; Barla, P. A theoretical foundation of the Porter hypothesis. Econ. Lett. 2002, 75, 355–360. [Google Scholar] [CrossRef]

- Barney, J. Firm resources and sustained competitive advantage. J. Manag. 1991, 17, 99–120. [Google Scholar] [CrossRef]

- Schumpeter, J.A. The Theory of Economic Development: An Inquiry into Profits, Capital, Credit, Interest, and the Business Cycle (1912/1934); Trans. Publishers: Victoria, BC, Canada, 1982; Volume 1, p. 244. [Google Scholar]

- Borghesi, S.; Cainelli, G.; Mazzanti, M. Linking emission trading to environmental innovation: Evidence from the Italian manufacturing industry. Res. Policy 2015, 44, 669–683. [Google Scholar] [CrossRef]

- Goulder, L.H.; Parry, I.W. Instrument choice in environmental policy. Rev. Environ. Econ. Policy 2008, 2, 152–174. [Google Scholar] [CrossRef]

- King, A.A.; Lenox, M.J. Does it really pay to be green? An empirical study of firm environmental and financial performance: An empirical study of firm environmental and financial performance. J. Ind. Ecol. 2001, 5, 105–116. [Google Scholar] [CrossRef]

- Fan, Y. Top-level design of China’s carbon market: Policy objectives and economic impacts. J. Environ. Econ. 2018, 3, 1–7. [Google Scholar]

- Shi, D.; Li, P. Quality evolution and assessment of China’s industry over the past seven decades. China Ind. Econ. 2019, 35, 5–23. [Google Scholar]

- Perino, G.; Requate, T. Does more stringent environmental regulation induce or reduce technology adoption? When the rate of technology adoption is inverted U-shaped. J. Environ. Econ. Manag. 2012, 64, 456–467. [Google Scholar] [CrossRef]

- Shao, S.; Hu, Z.; Cao, J.; Yang, L.; Guan, D. Environmental regulation and enterprise innovation: A review. Bus. Strateg. Environ. 2020, 29, 1465–1478. [Google Scholar] [CrossRef]

- Kerr, S.; Newell, R.G. Policy-induced technology adoption: Evidence from the US lead phasedown. J. Indust. Econ. 2003, 51, 317–343. [Google Scholar] [CrossRef]

- Zhang, C.Y.; Lv, Y. Green production regulation and enterprise R&D innovation: Impact and mechanism research. Bus. Manag. J. 2018, 1, 71–89. [Google Scholar]

- Fabra, N.; Reguant, M. Pass-through of emissions costs in electricity markets. Am. Econ. Rev. 2014, 104, 2872–2899. [Google Scholar] [CrossRef]

- Liu, Q.; Luo, L.; Zhang, Y.; Chen, H. Concentration of managerial power, internal control, and accounting information quality. Nankai Bus. Rev. 2013, 16, 15–23. [Google Scholar]

- Zhang, W.; Li, G.; Guo, F. Does carbon emissions trading promote green technology innovation in China? Appl. Energy 2022, 315, 119012. [Google Scholar] [CrossRef]

- Lin, C.; Shao, S.; Sun, W.; Yin, H. Can the electricity price subsidy policy curb NOX emissions from China’s coal-fired power industry? A difference-in-differences approach. J. Environ. Manag. 2021, 290, 112367. [Google Scholar] [CrossRef]

- Li, B.; Han, Y.; Wang, C.; Sun, W. Did civilized city policy improve energy efficiency of resource-based cities? Prefecture-level evidence from China. Energy Policy 2022, 167, 113081. [Google Scholar] [CrossRef]

- Bertrand, M.; Duflo, E.; Mullainathan, S. How Much should We Trust Differences-in-Differences Estimates? Q. J. Econ. 2004, 119, 249–275. [Google Scholar] [CrossRef]

- Rosenbaum, P.R.; Rubin, D.B. The central role of the propensity score in observational studies for causal effects. Biometrika 1983, 70, 41–55. [Google Scholar] [CrossRef]

- Zhang, J.P.; Chen, S.Y. Financial Development, Environmental Regulations and Green Economic Transition. J. Financ. Econ. 2021, 47, 78–93. [Google Scholar]

- Tone, K. A slacks-based measure of efficiency in data envelopment analysis. Eur. J. Oper. Res. 2001, 130, 498–509. [Google Scholar] [CrossRef]

- Tone, K. A slacks-based measure of super-efficiency in data envelopment analysis. Eur. J. Oper. Res. 2002, 143, 32–41. [Google Scholar] [CrossRef]

- Wang, Y.; Yao, Y.D. Sources of China’s economic growth 1952–1999: Incorporating human capital accumulation. China Econ. Rev. 2003, 14, 32–52. [Google Scholar] [CrossRef]

- Wu, J.; Xia, Q.; Li, Z. Green innovation and enterprise green total factor productivity at a micro level: A perspective of technical distance. J. Clean Prod. 2022, 344, 131070. [Google Scholar] [CrossRef]

- Li, W.J.; Zheng, M. Is it substantive innovation or strategic innovation? Impact of macroeconomic policies on micro-enterprises’ innovation. Econ. Res. J. 2016, 4, 60–73. [Google Scholar]

- Blundell, R.; Costa Dias, M. Evaluation methods for non-experimental data. Fisc. Stud. 2000, 21, 427–468. [Google Scholar] [CrossRef]

- De Chaisemartin, C.; D’Haultfoeuille, X. Two-way fixed effects estimators with heterogeneous treatment effects. Am. Econ. Rev. 2020, 110, 2964–2996. [Google Scholar] [CrossRef]

- Whited, T.M.; Wu, G. Financial constraints risk. Rev. Financ. Stud. 2006, 19, 531–559. [Google Scholar] [CrossRef]

| Variable Type | Variable | Variable Symbol | Variable Description |

|---|---|---|---|

| Dependent variable | green transition | GT | expressed by the green total factor productivity (GTFP) |

| Independent variable | carbon emission trading scheme | Carbon_policy | equals 1 in the years after the district in which heavy-polluting enterprises are located has carried out carbon emission trading policies, and 0 otherwise. |

| Mechanism Variables | green technological innovation | Patent_gre | ln(number of green patent applications + 1) |

| substantial green technological innovation | Green_inv | ln(number of green invention patent applications + 1) | |

| strategic green technological innovation | Green_uti | ln(number of green utility model patent applications + 1) | |

| fixed asset investment | Inv | ln(cash paid to acquire fixed assets, intangible assets, and other long-term assets) | |

| depreciation | Depre | ln(depreciation) | |

| depreciation rate | Depre_rate | depreciation/fixed asset investment | |

| Control variables | enterprise size | size | ln(total assets) |

| asset-liability ratio | lev | year-end total debt divided by year-end total assets. | |

| return on total assets | roa | net profit/average balance of total assets | |

| independent director ratio | indep | number of independent directors/total number of directors | |

| board size | board | ln(number of board members) | |

| revenue growth rate | growth | (operating income in yeart+1 − operating income in yeart)/(operating income in yeart) | |

| book to market ratio | bm | book value/total market value | |

| age of listing | listage | ln(current year − year of launch + 1) | |

| Tobin’s Q | tobinq | ratio of enterprise market value to asset replacement cost; | |

| operating cash flow | cashflow | net cash flow/total assets | |

| the regional GDP | lngdp | ln(gdp) | |

| industrial structure | industry | percentage of secondary industry |

| Variable | Obs | Mean | SD | Min | Max |

|---|---|---|---|---|---|

| GTFP | 3740 | 1.3618 | 0.8303 | 0.2553 | 5.0971 |

| size | 3740 | 22.6383 | 1.4215 | 20.0217 | 26.4580 |

| lev | 3740 | 0.4829 | 0.2032 | 0.0574 | 0.9411 |

| roa | 3740 | 0.0379 | 0.0598 | −0.1697 | 0.2414 |

| indep | 3740 | 0.3691 | 0.0507 | 0.3077 | 0.5714 |

| board | 3740 | 2.2001 | 0.1998 | 1.6094 | 2.7080 |

| growth | 3740 | 0.1434 | 0.3410 | −0.4689 | 2.1079 |

| bm | 3740 | 1.4408 | 1.4054 | 0.1408 | 7.5598 |

| tobinq | 3740 | 1.7794 | 1.0798 | 0.8462 | 6.8636 |

| listage | 3740 | 2.4739 | 0.6007 | 0 | 3.2581 |

| cashflow | 3740 | 0.0613 | 0.0668 | −0.1215 | 0.2489 |

| lngdp | 3740 | 17.4960 | 1.0845 | 15.2166 | 19.6049 |

| industry | 3740 | 0.4631 | 0.1083 | 0.1863 | 0.6865 |

| Patent_gre | 3740 | 0.5044 | 0.9702 | 0 | 7.3421 |

| Green_inv | 3740 | 0.3569 | 0.8195 | 0 | 7.2277 |

| Green_uti | 3740 | 0.2966 | 0.7194 | 0 | 5.1240 |

| Inv | 3740 | 12.4347 | 1.9024 | 4.0304 | 19.6172 |

| Depre | 3740 | 19.0487 | 1.6614 | 14.31 | 26.07 |

| Depre_rata | 3740 | 0.0557 | 0.0200 | 0.0209 | 0.1597 |

| Variable | Unmatched | Mean | %bias | %Reduct | t Test | ||

|---|---|---|---|---|---|---|---|

| Matched | Treatment Group | Control Group | |bias| | t | p > |t| | ||

| size | U | 22.806 | 22.38 | 27.6 | 86.1 | 2.30 | 0.022 |

| M | 22.558 | 22.617 | −3.8 | −0.23 | 0.816 | ||

| lev | U | 0.4626 | 0.5100 | −24.1 | 81.2 | −1.77 | 0.078 |

| M | 0.4702 | 0.4791 | −4.5 | −0.25 | 0.801 | ||

| roa | U | 0.0391 | 0.0353 | 7.0 | 46.8 | 0.51 | 0.614 |

| M | 0.0354 | 0.0334 | 3.7 | 0.21 | 0.836 | ||

| indep | U | 0.3760 | 0.3653 | 19.3 | 98.7 | 1.56 | 0.119 |

| M | 0.3703 | 0.3701 | 0.3 | 0.02 | 0.988 | ||

| board | U | 2.2377 | 2.2139 | 11.4 | 69.9 | 0.88 | 0.381 |

| M | 2.2214 | 2.2286 | −3.4 | −0.19 | 0.848 | ||

| growth | U | 0.1291 | 0.0796 | 12.6 | 83.3 | 1.03 | 0.305 |

| M | 0.1297 | 0.1214 | 2.1 | 0.11 | 0.914 | ||

| bm | U | 1.5577 | 1.6067 | −3.5 | 81.3 | −0.26 | 0.796 |

| M | 1.564 | 1.5548 | 0.6 | 0.04 | 0.970 | ||

| listage | U | 2.145 | 2.2767 | −20.6 | 83.0 | −1.66 | 0.097 |

| M | 2.1842 | 2.1617 | 3.5 | 0.19 | 0.847 | ||

| tobinq | U | 1.4565 | 1.582 | −15.6 | 99.4 | −1.10 | 0.273 |

| M | 1.4859 | 1.4867 | −0.1 | −0.01 | 0.966 | ||

| cashflow | U | 0.0755 | 0.0582 | 26.1 | 70.8 | 1.99 | 0.047 |

| M | 0.24 | 0.0673 | 7.6 | 0.45 | 0.655 | ||

| Variable | GT | ||

|---|---|---|---|

| (1) | (2) | (3) | |

| Carbon_policy | 0.2481 *** (5.2586) | 0.2270 *** (4.8556) | 0.1415 *** (3.0961) |

| size | 0.2570 *** (4.0978) | 0.2198 *** (3.5248) | |

| lev | 0.0624 (0.4423) | 0.1131 (0.8355) | |

| roa | 0.7191 ** (2.1727) | 0.7419 ** (2.3466) | |

| indep | 0.4936 (1.2207) | 0.6093 (1.5917) | |

| board | −0.2830 ** (−2.0596) | −0.2580 * (−1.9309) | |

| growth | 0.1709 *** (2.9804) | 0.1855 *** (3.3018) | |

| bm | −0.0041 (−0.1842) | −0.0053 (−0.2504) | |

| listage | −0.1578 ** (−2.5466) | −0.1649 *** (−2.7228) | |

| tobinq | 0.0315 (1.4174) | 0.0234 (1.1262) | |

| cashflow | −0.0294 (−0.1207) | −0.0360 (−0.1505) | |

| lngdp | 1.2495 *** (10.4228) | ||

| industry | 0.6550 (1.3395) | ||

| enterprise fixed effect | Yes | Yes | Yes |

| year fixed effect | Yes | Yes | Yes |

| Observations | 3010 | 3010 | 3010 |

| Adjusted R2 | 0.4929 | 0.5137 | 0.5414 |

| Variable | GT | |

|---|---|---|

| (1) | (2) | |

| Carbon_policy | 0.1537 *** (3.3497) | 0.1704 *** (3.2015) |

| control | Yes | No |

| L. control | No | Yes |

| enterprise fixed effect | Yes | Yes |

| year fixed effect | Yes | Yes |

| Observations | 3020 | 2709 |

| Adjusted R2 | 0.5466 | 0.5690 |

| Variable | GT | |

|---|---|---|

| (1) | (2) | |

| Carbon_policy-1 | 0.0679 (1.2562) | |

| Carbon_policy-2 | −0.0147 (−0.2006) | |

| control | Yes | Yes |

| enterprise fixed effect | Yes | Yes |

| year fixed effect | Yes | Yes |

| Observations | 3010 | 3010 |

| Adjusted R2 | 0.5400 | 0.5397 |

| Variable | GT | |||

|---|---|---|---|---|

| (1) | (2) | (3) | (4) | |

| Carbon_policy | 0.0835 * (1.6669) | 0.1893 *** (3.0295) | 0.1348 ** (2.1355) | 0.1336 ** (2.24) |

| control | Yes | Yes | Yes | Yes |

| enterprise fixed effect | Yes | Yes | Yes | Yes |

| year fixed effect | Yes | Yes | Yes | Yes |

| Treat*Year2010 | −0.0365 (−0.4080) | |||

| Treat*Year2012 | 0.0909 (0.8201) | |||

| Treat*Year2017 | 0.1414 ** (1.9938) | |||

| Observations | 1505 | 2250 | 3010 | 2650 |

| Adjusted R2 | 0.4083 | 0.5505 | 0.5418 | 0.5001 |

| Variable | Pantent_gre (1) | Green_inv (2) | Green_uti (3) |

|---|---|---|---|

| Carbon_policy | 0.0500 (1.1906) | 0.0688 ** (1.9690) | 0.0117 (0.3720) |

| control | Yes | Yes | Yes |

| enterprise fixed effect | Yes | Yes | Yes |

| year fixed effect | Yes | Yes | Yes |

| Observations | 3010 | 3010 | 3010 |

| Adjusted R2 | 0.6283 | 0.6221 | 0.5343 |

| Variable | Inv (1) | Depre (2) | Depre_rate (3) |

|---|---|---|---|

| Carbon_policy | 0.1452 ** (2.5217) | 0.0430 * (1.7982) | 0.1890 * (1.8275) |

| control | Yes | Yes | Yes |

| enterprise fixed effect | Yes | Yes | Yes |

| year fixed effect | Yes | Yes | Yes |

| Observations | 3010 | 3010 | 3010 |

| Adjusted R2 | 0.8197 | 0.9634 | 0.5955 |

| Variable | Cost Transfer Ability | Financing Constraints (3) | Internal Control (4) | Environmental Enforcement (5) | |

|---|---|---|---|---|---|

| (1) | (2) | ||||

| Carbon_policy | 0.1883 *** (3.3100) | 0.2564 *** (3.7723) | 0.2410 *** (3.9186) | 0.0918 * (1.6948) | 0.1756 *** (3.6711) |

| Carbon_policy*PMCD | −0.1075 * (−1.6680) | ||||

| Carbon_policy*BP | −0.1750 ** (−2.2305) | ||||

| Carbon_policy*FC | −0.2428 *** (−3.0990) | ||||

| Carbon_policy*IC | 0.0932 * (1.7851) | ||||

| Carbon_policy*EEI | 0.3181 ** (2.3484) | ||||

| control | Yes | Yes | Yes | Yes | Yes |

| enterprise fixed effect | Yes | Yes | Yes | Yes | Yes |

| Year fixed effect | Yes | Yes | Yes | Yes | Yes |

| Observations | 3010 | 2790 | 2743 | 2792 | 3010 |

| Adjusted R2 | 0.5359 | 0.5459 | 0.5537 | 0.5388 | 0.5200 |

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2023 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Xu, S.; Pan, W.; Wen, D. Do Carbon Emission Trading Schemes Promote the Green Transition of Enterprises? Evidence from China. Sustainability 2023, 15, 6333. https://doi.org/10.3390/su15086333

Xu S, Pan W, Wen D. Do Carbon Emission Trading Schemes Promote the Green Transition of Enterprises? Evidence from China. Sustainability. 2023; 15(8):6333. https://doi.org/10.3390/su15086333

Chicago/Turabian StyleXu, Sheng, Wenran Pan, and Demei Wen. 2023. "Do Carbon Emission Trading Schemes Promote the Green Transition of Enterprises? Evidence from China" Sustainability 15, no. 8: 6333. https://doi.org/10.3390/su15086333

APA StyleXu, S., Pan, W., & Wen, D. (2023). Do Carbon Emission Trading Schemes Promote the Green Transition of Enterprises? Evidence from China. Sustainability, 15(8), 6333. https://doi.org/10.3390/su15086333