Key Corporate Sustainability Assessment Methods for Coal Companies

Abstract

1. Introduction

- Designing an effective system for short- and long-term corporate management that factors in both economic and non-economic consequences of the company’s activity;

- Expanding the scope of the company’s financial reporting and, consequently, increasing the value of its business results;

- Creating a communication environment through interacting with interested participants (stakeholders);

- Strengthening the company’s financial performance and sustainability and, as a result, its market position [19].

- (1)

- (2)

- Composite-index approach (for example, the DJSI index, etc.).

- Growth in the company’s shareholder value and profits often serves as a CS indicator in the economic domain;

- The environmental domain is assessed through various ecological indicators with economic or natural units of measurement;

- The social domain is not always included in the assessment due to the complexity of measuring the company’s impact on social processes at various levels.

- Studies where the significant difference between the coal industry and other industries is not taken into account, with CS in the coal sector being viewed through the lens of general CS assessment principles;

- Studies that take into consideration the fact that the coal industry has specific features and a significant impact on the ecological, economic, and social aspects of the environment where the company operates.

- Analyzing different CS assessment methods and determining the principles on which a methodology for assessing the corporate sustainability of coal companies can be based;

- Substantiating a classification of factors for assessing corporate sustainability in the coal sector and identifying the most influential factors in light of current trends in the coal industry and institutional regulation.

2. Materials and Methods

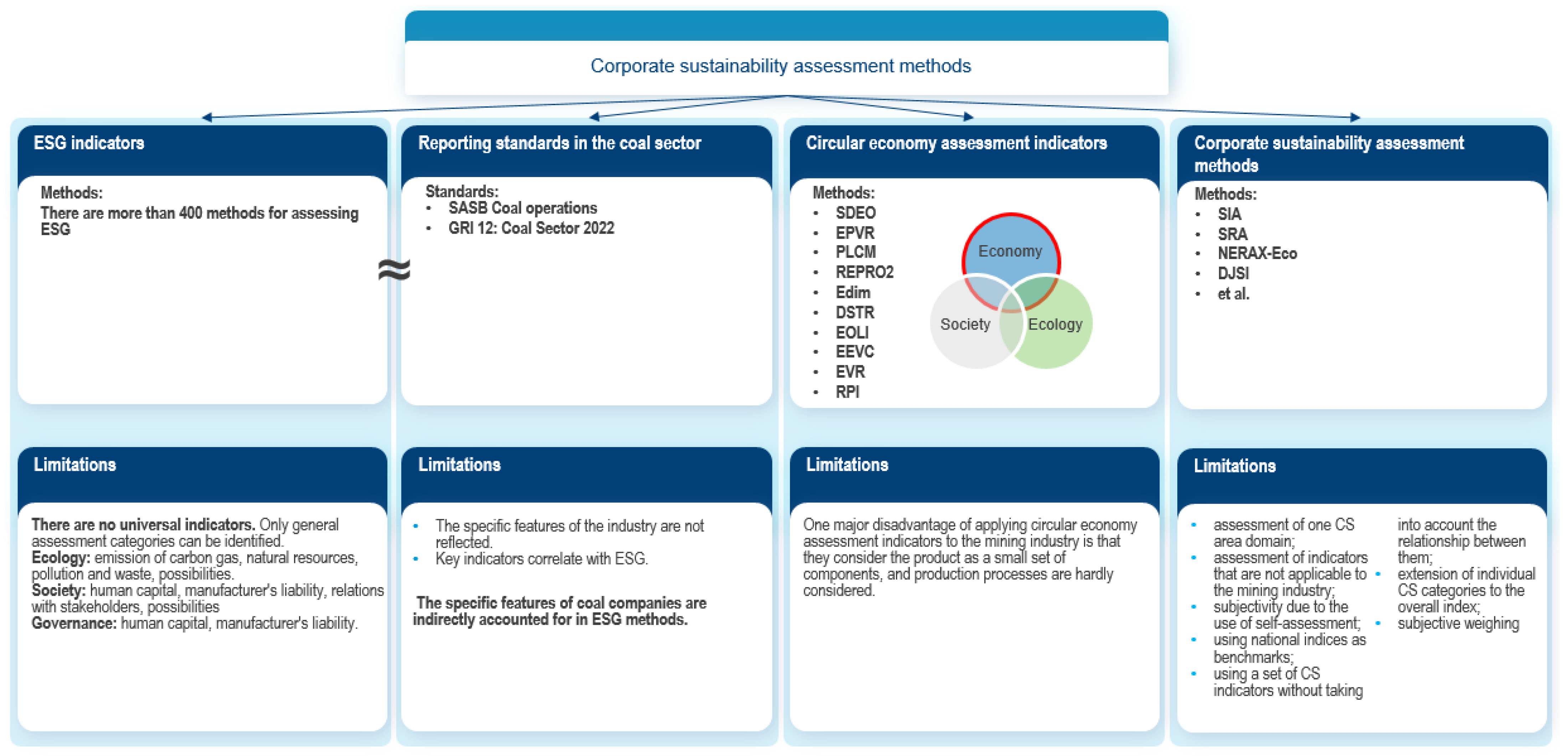

- Analyzing CS assessment methods, which includes a study of assessment methods used in related areas (ESG, circular economy, sustainable development) [34]. The search for scientific publications was carried out using Science Direct and Scopus for the period from 2002 to 2022 by the keywords ”assessment of corporate sustainability”, ”measuring corporate sustainability“. Twenty-seven methods were assessed that are described in scientific publications, reports by research institutes (National Research Institute of Finance of the Ministry of Finance of the Russian Federation), and corporate reporting standards (SASB (Coal Operations) and GRI (GRI 12: Coal Sector 2022));

- Comparing assessment indicators used in different CS assessment methods and their consolidation;

- Analyzing CS factors and identifying those most significant for CS assessment. The analysis was carried out in order to identify factors affecting the resulting indicator of the CS assessment and to assess the significance and applicability of factors considered in the scientific literature for coal companies;

- Analyzing trends in the coal industry in order to assess their impact and identify CS factors specific to coal companies;

- Assessment of the institutional regulation impact on coal companies as the most important factor in determining the ability to provide CS.

3. Results and Discussion

3.1. An Analysis of Corporate Sustainability Assessment Methods for Coal Companies

- Most of them assess only one individual CS domain (society, economy, or ecology). Examples include the Social Impact Assessment (SIA), Social Return Assessment (SRA), and NERAX-Eco environmental indicators;

- They analyze industrial indicators that are not applicable to the mining industry (agroecosystem efficiency indicators, tourism sustainability assessment maps, etc.);

- Some of them are subjective due to the use of self-assessment methods (for example, DJSI);

- Using national indices as benchmarks (Figge et al. [36]);

- Using a set of CS assessment indicators without factoring in their relationships (for example, Labuschagne et al. [37]);

- Lack of well-defined indicators (the method proposed by Rahdari and Rostamy [25]).

- Indicators covering not only economic but also other factors for improving social and environmental development at the company or product level (for example, PR-MCDT) [59].

- Coal mining companies have a major impact on the environmental, economic, and social development of mining regions and countries with resource-based economies;

- They actively support and increase mineral assets;

- They efficiently and rationally use natural capital, including mineral assets, as well as soil, land, water, and forest resources;

- They develop and implement CSR strategies based on a combination of the balanced interests of stakeholders;

- They are associated with high environmental risks;

- The majority of social and environmental consequences of the coal companies’ activities are long-term and are resolved by government involvement for a long time;

- The efficiency of the economic activity of a coal company depends on the mining and geological conditions of the fields and the physical and chemical properties of the minerals, as well as the economic and geographical location of the coal enterprise.

- 1.

- Factors affecting CS. Academic studies discuss factors that can affect CS. Therefore, in CS assessment, it is necessary to take into account, among other things, how the company manages these factors;

- 2.

- Industrial factors. The functioning of the company is influenced by industry trends [61]. In our opinion, if there is a crisis in the industry, individual companies cannot maintain their sustainability. In addition, favorable factors in the development of the industry can stimulate CS. This means that the state of the industry affects the sustainability of its companies.

3.2. Factors Affecting Corporate Sustainability: Identification and Analysis

- Group 1: government regulation and the regulatory framework as the factors that are most often mentioned;

- Group 2: imperfect management, interaction with stakeholders, corporate self-regulation, and self-reflection as factors manageable within the company.

3.2.1. Corporate Sustainability Factors: Group 1

- Implementation of regulatory measures (taxes, levies, etc.) that promote environmental innovation [70];

- Information disclosure initiatives (in the form of corresponding legislation or banning public funds from investing in companies that do not disclose their information);

- Assisting businesses in the development and use of SD tools and instruments (preferential tax policies, co-financing, and other incentives for the design and implementation of new technologies) aimed at gaining environmental and financial benefits.

- 1.

- In 2025: A decrease in energy consumption of 13.5% and carbon emissions of 18% from the 2020 level; the share of non-fossil energy consumption reaching 20%; the forest stock volume growing to 18 billion cubic meters;

- 2.

- In 2030: A 65% reduction in carbon emissions from the 2005 level; the share of non-fossil energy consumption reaching 25%; the forest stock volume growing to 19 billion cubic meters;

- 3.

- In 2060: With the share of non-fossil energy consumption exceeding 80%; the country will have become carbon-neutral.

3.2.2. Corporate Sustainability Factors: Group 2

3.3. Trends in Russia’s Coal Industry

- (1)

- Factors affecting the resilience (sustainability) of the industry. This group of factors includes industry trends and the degree of state regulation and determines the ability of the industry to recover and adapt after the impact of external factors. Government regulation ensures the resilience of the industry, as the regulatory framework can create a “loop” of resilience. Taking into account the identified trends that negatively affect the coal industry in modern conditions (change in market structure, falling sales, demand and price volatility), a reasonable level of government support can become an industry recovery driver in various countries, including Russia;

- (2)

- Factors affecting the CS of coal companies. This group of factors is determined by the peculiarities of conducting activities in accordance with the three-type classification of coal companies. These factors include organizational features, for example, the presence of organizational barriers, the level of business diversification, etc.

4. Conclusions

- This literature review showed that corporate sustainability assessment methods differ in the number and composition of indicators, the degree of aggregation, the method of calculating the resulting value, weighting factors, and CS progress assessment, while not taking into account the specific features of the coal industry;

- Due to significant differences between CS assessment methods, it is impossible to identify universal CS assessment indicators. The problem lies in choosing a limited set of indicators that will ensure a comprehensive and detailed CS assessment;

- Twenty-seven CS assessment methods were analyzed that can be classified into traditional corporate sustainability assessment methods, circular economy assessment methods, ESG assessment methods, and non-financial performance indicators. None of the analyzed methods can be used to assess the CS of coal companies due to the lack of the coal companies’ specific consideration;

- Current CS assessment methods have a number of limitations. Most of them are based on ESG principles or TBL principles. The lack of methods for assessing CS without restrictions shows the shortage of corporate sustainability management tools. In our opinion, CS assessment should factor in the environment in which coal companies operate. ESG principles rather than indicators should serve as the core of the methodology as the latter have a large number of shortcomings;

- Most researchers identify five major factors that can affect the process of implementing a CS policy: government regulation, imperfect management, interaction with stakeholders, corporate self-regulation and self-reflection, and the regulatory framework. In our opinion, these factors can be consolidated into two groups, with one focused on government regulation and the other connected with management barriers. Our literature review shows that government regulation is the most influential factor;

- Factors affecting CS can be considered in the CS assessment. For the mining industry (coal industry), the main factors are industry factors and government regulation factors. Both groups of factors affect the resilience of the coal industry, which can ensure the CS of a particular coal company, depending on their strength and degree of influence;

- Russian coal companies can be divided into three types depending on their business models: metal manufacturers, energy companies, and companies engaged in the extraction and sale of coal. Factors influencing the coal industry (changes in the supply structure, decarbonization trends, the role of the primary local employer) affect different types of companies to varying degrees, so companies of each type should be assessed using different sets of CS indicators;

- CS assessment in the coal sector should include two stages: the assessment of an individual coal company depending on its type and the assessment of trends in the industry, as they largely affect the functioning of companies.

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Conflicts of Interest

References

- Ala-Uddin, M. ‘Sustainable’ Discourse: A Critical Analysis of the 2030 Agenda for Sustainable Development. Asia Pac. Media Educ. 2019, 29, 214–224. [Google Scholar] [CrossRef]

- Bobylev, S.N. Sustainable Development for Future Generations: Economic Priorities. World New Econ. 2017, 3, 90–96. (In Russian) [Google Scholar]

- Nordén, B.; Avery, H. Global Learning for Sustainable Development: A Historical Review. Sustainability 2021, 13, 3451. [Google Scholar] [CrossRef]

- United Nations. Voluntary National Review of the Implementation of the 2030 Agenda for Sustainable Development. Available online: https://sustainabledevelopment.un.org/content/documents/26421VNR_2020_Russia_Report_Russian.pdf (accessed on 16 January 2023). (In Russian).

- Agence Francaise de Development. The Sustainable Development Analysis. Available online: https://www.afd.fr/en/ressources/sustainable-development-analysis (accessed on 16 January 2023).

- Accenture. The Course Towards Sustainability as Russian Business Becomes Responsible. Sustainability Research. Available online: https://www.accenture.com/_acnmedia/PDF-162/Accenture-Sustainability-Survey-2021-RUSSIA.pdf (accessed on 16 January 2023). (In Russian).

- Deioitte. Sustainable Development and Corporate Social Responsibility. Available online: https://www2.deloitte.com/ru/ru/pages/risk/solutions/sustainability-and-csr.html (accessed on 16 January 2023). (In Russian).

- Investinfa. Recommendations for Sustainable Development and Green Investment. Available online: https://investinfra.ru/frontend/images/PDF/rekomendatsii-nakdi-v-oblasti-ustoichivogo-razvitiya-i-zelenyh-investitsii-230318.pdf (accessed on 16 January 2023). (In Russian).

- United Nations. The UN Global Compact. Available online: http://www.globalcompact.org (accessed on 16 January 2023).

- United Nations. The Global Reporting Initiative. Available online: http://www.globalreporting.org (accessed on 16 January 2023).

- Yurak, V.V.; Dushin, A.V.; Mochalova, L.A. Vs sustainable development: Scenarios for the future. J. Min. Inst. 2020, 242, 242–247. [Google Scholar] [CrossRef]

- Litvinenko, V.; Bowbrick, I.; Naumov, I.; Zaitseva, Z. Global guidelines and requirements for professional competencies of natural resource extraction engineers: Implications for ESG principles and sustainable development goals. J. Clean. Prod. 2022, 338, 130530. [Google Scholar] [CrossRef]

- Golovina, E.; Pasternak, S.; Tsiglianu, P.; Tselischev, N. Sustainable Management of Transboundary Groundwater Resources: Past and Future. Sustainability 2021, 13, 12102. [Google Scholar] [CrossRef]

- Litvinenko, V.S.; Tsvetkov, P.S.; Dvoynikov, M.V.; Buslaev, G.V. Barriers to implementation of hydrogen initiatives in the context of global energy sustainable development. J. Min. Inst. 2020, 244, 428–438. [Google Scholar] [CrossRef]

- Ahmed, M.; Mubarik, M.S.; Shahbaz, M. Factors affecting the outcome of corporate sustainability policy: A review paper. Env. Sci. Pollut. Res. 2021, 28, 10335–10356. [Google Scholar] [CrossRef]

- Baumgartner, R.J. Managing Corporate Sustainability and CSR: A Conceptual Framework Combining Values, Strategies and Instruments Contributing to Sustainable Development. Corp. Soc. Responsib. Environ. Manag. 2014, 21, 258–271. [Google Scholar] [CrossRef]

- Cherepovitsyn, A.; Rutenko, E. Strategic Planning of Oil and Gas Companies: The Decarbonization Transition. Energies 2022, 15, 6163. [Google Scholar] [CrossRef]

- Dmitrieva, D.; Cherepovitsyna, A.; Stroykov, G.; Solovyova, V. Strategic Sustainability of Offshore Arctic Oil and Gas Projects: Definition, Principles, and Conceptual Framework. J. Mar. Sci. Eng. 2022, 10, 23. [Google Scholar] [CrossRef]

- Stroykov, G.; Vasilev, Y.N.; Zhukov, O.V. Basic Principles (Indicators) for Assessing the Technical and Economic Potential of Developing Arctic Offshore Oil and Gas Fields. J. Mar. Sci. Eng. 2021, 9, 1400. [Google Scholar] [CrossRef]

- Pranugrahaning, A.; Donovan, J.D.; Topple, C.; Masli, E.K. Corporate sustainability assessments: A systematic literature review and conceptual framework. J. Clean. Prod. 2021, 295, 126385. [Google Scholar] [CrossRef]

- Silva, S.; Nuzum, A.-K.; Schaltegger, S. Stakeholder expectations on sustainability performance measurement and assessment. A systematic literature review. J. Clean. Prod. 2019, 217, 204–215. [Google Scholar] [CrossRef]

- Schneider, A.; Meins, E. Two Dimensions of Corporate Sustainability Assessment: Towards a Comprehensive Framework. Bus. Strategy Environ. 2011, 21, 211–222. [Google Scholar] [CrossRef]

- Cherepovitsyn, A.E.; Tsvetkov, P.S.; Evseeva, O.O. Critical analysis of methodological approaches to assessing sustainability of arctic oil and gas projects. J. Min. Inst. 2021, 249, 463–478. [Google Scholar] [CrossRef]

- Nikolaou, I.E.; Tsalis, T.A.; Evangelinos, K.I. A framework to measure corporate sustainability performance: A strong sustainability-based view of firm. Sustain. Prod. Consum. 2018, 18, 1–18. [Google Scholar] [CrossRef]

- Rahdari, A.H.; Rostamy, A.A.A. Designing a general set of sustainability indicators at the corporate level. J. Clean. Prod. 2015, 108, 757–771. [Google Scholar] [CrossRef]

- Figge, F.; Hahn, T.; Schaltegger, S.; Wagner, M. The sustainability balanced scorecard—Linking sustainability management to business strategy. Bus. Strategy Environ. 2002, 11, 269–284. [Google Scholar] [CrossRef]

- Gomez-Limon, J.; Sanchez-Fernandez, G. Empirical evaluation of agricultural sustainability using composite indicators. Ecol. Econ. 2010, 69, 1062–1075. [Google Scholar] [CrossRef]

- Vayssieres, J.; Guerrin, F.; Paillat, J.; Lecomte, P. GAMEDE: A global activity model for evaluating the sustainability of dairy enterprises Part I—Whole-farm dynamic model. Agric. Syst. 2009, 101, 128–138. [Google Scholar] [CrossRef]

- Van Passel, S.; Nevens, F.; Mathijs, E.; Van Huylenbroeck, G. Measuring farm sustainability and explaining differences in sustainable efficiency. Ecol. Econ. 2007, 62, 149–161. [Google Scholar] [CrossRef]

- Van Cauwenbergh, N.; Bielders, C.; Reijnders, J.; Vanclooster, M.; Biala, K.; Brouckaert, V.; Garcia, C.V.; Sauvenier, X.; Peeters, A.; Franchois, L.; et al. SAFE—A hierarchical framework for assessing the sustainability of agricultural systems. Agr. Ecosyst. Environ. 2007, 120, 229–242. [Google Scholar] [CrossRef]

- Caporali, F.; Tellarini, V. An input/output methodology to evaluate farms as sustainable agroecosystems: An application of indicators to farms in central Italy. Agr. Ecosyst. Environ. 2000, 77, 111–123. [Google Scholar] [CrossRef]

- Lozano, R. A tool for a Graphical Assessment of Sustainability in Universities (GASU). J. Clean. Prod. 2006, 14, 963–972. [Google Scholar] [CrossRef]

- Ko, T.G. Development of tourism sustainability assessment procedure: A conceptual approach. Tour. Manag. 2005, 26, 431–455. [Google Scholar] [CrossRef]

- Blinova, E.; Ponomarenko, T.; Knysh, V. Analyzing the Concept of Corporate Sustainability in the Context of Sustainable Business Development in the Mining Sector with Elements of Circular Economy. Sustainability 2022, 14, 8163. [Google Scholar] [CrossRef]

- Kocmanová, A.; Pavláková Dočekalová, M.; Škapa, S.; Smolíková, L. Measuring Corporate Sustainability and Environmental, Social, and Corporate Governance Value Added. Sustainability 2016, 8, 945. [Google Scholar] [CrossRef]

- Figge, F.; Hahn, T. The Cost of Sustainability Capital and the Creation of Sustainable Value by Companies. J. Ind. Ecol. 2005, 9, 47–58. [Google Scholar] [CrossRef]

- Labuschagne, C.; Brent, A.; van Erck, R. Assessing the sustainability performances of industries. J. Clean. Prod. 2005, 13, 373–385. [Google Scholar] [CrossRef]

- Phillis, Y.A.; Kouikoglou, V.S.; Manousiouthakis, V. A Review of Sustainability Assessment Models as System of Systems. IEEE Syst. J. 2010, 4, 15–25. [Google Scholar] [CrossRef]

- Munoz, M.; Rivera, J.; Moneva, J. Evaluating sustainability in organisations with a fuzzy logic approach. Ind. Manag. Data Syst. 2008, 108, 829–841. [Google Scholar] [CrossRef]

- RBK. ESG Principles: What They Are and Why Companies Should Follow Them. Available online: https://trends.rbc.ru/trends/green/614b224f9a7947699655a435 (accessed on 16 January 2023). (In Russian).

- National Research Institute of Finance of the Ministry of Finance of the Russian Federation. Evolution, Basic Concepts and Experience of ESG Regulation. Available online: https://www.nifi.ru/images/FILES/Reports/%D0%9D%D0%98%D0%A4%D0%98_%D0%AD%D0%BA%D0%BE%D0%BB%D0%BE%D0%B3%D0%B8%D1%87%D0%B5%D1%81%D0%BA%D0%B8%D0%B5_%D1%81%D0%BE%D1%86%D0%B8%D0%B0%D0%BB%D1%8C%D0%BD%D1%8B%D0%B5_%D1%83%D0%BF%D1%80%D0%B0%D0%B2%D0%BB%D0%B5%D0%BD%D1%87%D0%B5%D1%81%D0%BA%D0%B8%D0%B5_%D1%84%D0%B0%D0%BA%D1%82%D0%BE%D1%80%D1%8B_ESG.pdf (accessed on 16 January 2023). (In Russian).

- Gendler, S.G.; Prokhorova, E.A. Assessment of the cumulative impact of occupational injuries and diseases on the state of labor protection in the coal industry. MIAB Mining Inf. Anal. Bull. 2022, 10-2, 105–116. [Google Scholar] [CrossRef]

- SASB. Coal Operations Sustainability Accounting Standard. Available online: https://www.sasb.org/standards/download (accessed on 16 January 2023).

- GRI. GRI 12: Coal Sector 2022. Available online: https://www.globalreporting.org/standards/standards-development/sector-standard-for-coal/ (accessed on 16 January 2023).

- Atkinson, G. Measuring Corporate Sustainability. J. Environ. Plan. Manag. 2010, 43, 235–252. [Google Scholar] [CrossRef]

- Kristensen, H.S.; Mosgaard, M.A. A review of micro level indicators for a circular economy—Moving away from the three dimensions of sustainability. J. Clean. Prod. 2020, 243, 118531. [Google Scholar] [CrossRef]

- De Oliveira, C.T.; Dantas, T.E.T.; Soares, S.R. Nano and micro level circular economy indicators: Assisting decision-makers in circularity assessments. Sustain. Prod. Consum. 2021, 26, 455–468. [Google Scholar] [CrossRef]

- Janik, A.; Ryszko, A. Circular economy in companies: An analysis of selected indicators from a managerial perspective. Multidiscip. Asp. Prod. Eng. 2019, 2, 523–535. [Google Scholar] [CrossRef]

- Ameli, M.; Mansour, S.; Ahmadi-Javid, A. A simulation-optimization model for sustainable product design and efficient end-of-life management based on individual producer responsibility. Resour. Conserv. Recycl. 2019, 140, 246–258. [Google Scholar] [CrossRef]

- Cong, L.; Zhao, F.; Sutherland, J.W. A design method to improve end-of-use product value recovery for circular economy. J. Mech. Des. 2018, 141, 044502. [Google Scholar] [CrossRef]

- Linder, M.; Sarasini, S.; van Loon, P. A metric for quantifying product-level circularity. J. Ind. Ecol. 2017, 21, 545–558. [Google Scholar] [CrossRef]

- Zwolinski, P.; Lopez-Ontiveros, M.-A.; Brissaud, D. Integrated design of remanufacturable products based on product profiles. J. Clean. Prod. 2006, 14, 1333–1345. [Google Scholar] [CrossRef]

- Vanegas, P.; Peeters, J.R.; Cattrysse, D.; Tecchio, P.; Ardente, F.; Mathieux, F.; Dewulf, W.; Duflou, J.R. Ease of disassembly of products to support circular economy strategies. Resour. Conserv. Recycl. 2018, 135, 323–334. [Google Scholar] [CrossRef] [PubMed]

- van Loon, P.; Van Wassenhove, L.N. Assessing the economic and environmental impact of remanufacturing: A decision support tool for OEM suppliers. Int. J. Prod. Res. 2018, 56, 1662–1674. [Google Scholar] [CrossRef]

- Lee, H.M.; Lu, W.F.; Song, B. A framework for assessing product End-Of-Life performance: Reviewing the state of the art and proposing an innovative approach using an End-of-Life Index. J. Clean. Prod. 2014, 66, 355–371. [Google Scholar] [CrossRef]

- Favi, C.; Germani, M.; Luzi, A.; Mandolini, M.; Marconi, M. A design for EoL approach and metrics to favour closed-loop scenarios for products. Int. J. Sustain. Eng. 2017, 10, 136–146. [Google Scholar] [CrossRef]

- Vogtlander, J.G.; Scheepens, A.E.; Bocken, N.M.P.; Peck, D. Combined analyses of costs, market value and eco-costs in circular business models: Eco-efficient value creation in remanufacturing. J. Remanuf. 2017, 7, 1–17. [Google Scholar] [CrossRef]

- Scheepens, A.E.; Vogtlander, J.G.; Brezet, J.C. Two life cycle assessment (LCA) based methods to analyse and design complex (regional) circular economy systems. Case: Making water tourism more sustainable. J. Clean. Prod. 2016, 114, 257–268. [Google Scholar] [CrossRef]

- Alamerew, Y.A.; Brissaud, D. Circular economy assessment tool for end of life product recovery strategies. J. Remanuf. 2018, 9, 169–185. [Google Scholar] [CrossRef]

- Park, J.Y.; Chertow, M.R. Establishing and testing the “reuse potential” indicator for managing wastes as resources. J. Environ. Manag. 2014, 137, 45–53. [Google Scholar] [CrossRef]

- Gendler, S.G.; Fazylov, I.R.; Abashin, A.N. The results of experimental studies of the thermal regime of oil mines in the thermal method of oil production. MIAB. Min. Inf. Anal. Bull. 2022, 6-1, 248–262. [Google Scholar] [CrossRef]

- Nedosekin, A.O.; Rejshahrit, E.I.; Kozlovskij, A.N. Strategic approach to assessing economic sustainability objects of mineral resources sector of Russia. J. Min. Inst. 2019, 237, 354–360. [Google Scholar] [CrossRef]

- Zhu, Q. Institutional pressures and support from industrial zones for motivating sustainable production among Chinese manufacturers. Int. J. Prod. Econ. 2016, 181, 402–409. [Google Scholar] [CrossRef]

- Yu, Y.; Chen, Z.; Wei, L.; Wang, B. The low-carbon technology characteristics of China‘s ferrous metal industry. J. Clean. Prod. 2017, 140, 1739–1748. [Google Scholar] [CrossRef]

- Feng, C.; Huang, J.B.; Wang, M. Analysis of green total-factor productivity in China‘s regional metal industry: A meta-frontier approach. Resour. Policy 2018, 58, 219–229. [Google Scholar] [CrossRef]

- Luan, C.; Tien, C.; Wu, P. Strategizing environmental policy and compliance for firm economic sustainability: Evidence from Taiwanese electronics firms. Bus. Strategy Environ. 2013, 22, 517–546. [Google Scholar] [CrossRef]

- Van Hemel, C.; Cramer, J. Barriers and stimuli for ecodesign in SMEs. J. Clean. Prod. 2002, 10, 439–453. [Google Scholar] [CrossRef]

- Que, C.T.; Nevskaya, M.; Marinina, O. Coal Mines in Vietnam: Geological Conditions and Their Influence on Production Sustainability Indicators. Sustainability 2021, 13, 11800. [Google Scholar] [CrossRef]

- Khoroshavin, A.V. New Generation of Business Sustainable Development Management Instruments and Their Implementation in Russian Oil and Gaz Companies. Ph.D. Thesis, St. Petersburg State University, St Petersburg, Russia, 28 May 2018. (In Russian). [Google Scholar]

- Xanthos, D.; Walker, T.R. International policies to reduce plastic marine pollution from single-use plastics (plastic bags and microbeads): A review. Mar. Pollut. Bull. 2017, 118, 17–26. [Google Scholar] [CrossRef] [PubMed]

- Gardner, J.S.; Sinclair, A.J. Evaluation of capacity and policy development for environmental sustainability: A case from Himachal Pradesh, India. Can. J. Dev. Stud. 2003, 24, 137–153. [Google Scholar] [CrossRef]

- Fairbrass, J. Exploring corporate social responsibility policy in the European Union: A discursive institutionalist analysis. JCMS: J. Common Mark. Stud. 2011, 49, 949–970. [Google Scholar] [CrossRef]

- Deakin, S.; Hobbs, R. False dawn for CSR? Shifts in regulatory policy and the response of the corporate and financial sectors in Britain. Corp. Gov. Int. Rev. 2007, 15, 68–76. [Google Scholar] [CrossRef]

- Driessen, P.P.J.; Dieperink, C.; Laerhoven, F.V.; Runhaar, H.A.C.; Vermeulen, W.J.V. Towards a conceptual framework for the study of shifts in modes of environmental governance–experiences from the Netherlands. Environ. Policy Gov. 2012, 22, 143–160. [Google Scholar] [CrossRef]

- Lange, P.; Bornemann, B.; Burger, P. Sustainability impacts of governance modes: Insights from Swiss energy policy. J. Environ. Policy Plan. 2019, 21, 174–187. [Google Scholar] [CrossRef]

- Pankov, D.A.; Afanasiev, V.Y.; Baykova, O.V.; Tregubova, E.A. Global coal market review and Russian export trends. Ugol’ 2021, 3, 23–26. [Google Scholar] [CrossRef]

- Timofeev, O.A.; Sharipov, F.F.; Petrenko, B.V. COVID-19 pandemic impact on China’s coal market. Ugol’ 2021, 1, 63–67. [Google Scholar] [CrossRef]

- Russian International Affairs Council. China’s Energy Crisis. Available online: https://russiancouncil.ru/analytics-and-comments/analytics/energeticheskiy-krizis-v-kitae/ (accessed on 11 January 2023).

- Environmentalism Ltd. (E3G). Analytical Center on Climate Change. Coal in 2022: China’s Coal Power Industry in the Spotlight. Available online: https://www.e3g.org/news/coal-in-2022-china-s-coal-power-in-the-spotlight/ (accessed on 12 January 2023).

- Forbes. Coal To Power China’s Energy Transition. Available online: https://www.forbes.com/sites/thebakersinstitute/2022/04/26/coal-to-power-chinas-energy-transition/?sh=421bc51f1b9e (accessed on 13 January 2023).

- International Energy Agency. Global Coal Demand is Forecast to Remain Flat in 2023, but Uncertainty is Rising. Available online: https://www.iea.org/reports/coal-market-update-july-2022/demand (accessed on 12 January 2023).

- S&P Global. China «Needs a Future Coal Industry, not a Future without Coal». Available online: https://www.spglobal.com/commodityinsights/en/market-insights/latest-news/coal/062321-china-needs-a-future-coal-industry-not-a-future-without-coal (accessed on 13 January 2023).

- National Development and Reform Commission (NDRC) People´s Republic of China. Working Guidance for Carbon Dioxide Peaking and Carbon Neutrality in Full and Faithful Implementation of the New Development Philosophy. Available online: https://en.ndrc.gov.cn/policies/202110/t20211024_1300725.html (accessed on 13 January 2023).

- Hepburn, C.; Qi, Y.; Stern, N.; Ward, B.; Xie, C.; Zenghelis, D. Towards carbon neutrality and China’s 14th Five-Year Plan: Clean energy transition, sustainable urban development, and investment priorities. Environ. Sci. Ecotechnol. 2021, 8, 100130. [Google Scholar] [CrossRef]

- Reyshakhrit, E.I.; Nevskaya, M.A.; Chu, T.Q. Analysis of the state, prospects and problems the coal industry in Vietnam. Eurasian Sci. J. 2021, 1, 16ECVN121. (In Russian) [Google Scholar]

- Dezan Shira & Associates. Vietnam’s Power Development Plan Draft Incorporates Renewables, Reduces Coal. Available online: https://www.vietnam-briefing.com/news/vietnams-power-development-plan-draft-incorporates-renewables-reduces-coal.html/ (accessed on 13 January 2023).

- VietnamPlus. Vietnam to Increase Coal Imports in 2025–2035 Period: Ministry. Available online: https://en.vietnamplus.vn/vietnam-to-increase-coal-imports-in-20252035-period-ministry/235325.vnp (accessed on 13 January 2023).

- Watson Farley & Williams LLP. Vietnam’s Draft Master Plan VIII and the Energy Transition. Available online: https://www.wfw.com/articles/vietnams-draft-master-plan-viii-and-the-energy-transition/ (accessed on 13 January 2023).

- Reuters International News Agency. G7 Makes New $15 Billion Offer to Vietnam to Reduce Coal Consumption. Available online: https://www.reuters.com/business/energy/g7-makes-new-15-billion-offer-vietnam-cut-coal-use-sources-2022-12-07/ (accessed on 13 January 2023).

- Orji, I.J. Examining barriers to organizational change for sustainability and drivers of sustainable performance in the metal manufacturing industry. Resour. Conserv. Recycl. 2019, 140, 102–114. [Google Scholar] [CrossRef]

- Klewitz, J.; Zeyen, A.; Hansen, E.G. Intermediaries driving eco-innovation in SMEs: A qualitative investigation. Eur. J. Innov. Manag. 2012, 15, 442–467. [Google Scholar] [CrossRef]

- Nykvist, B.; Nilsson, M. Are impact assessment procedures actually promoting sustainable development? Institutional perspectives on barriers and opportunities found in the Swedish committee system. Environ. Impact Assess. Rev. 2009, 29, 15–24. [Google Scholar] [CrossRef]

- Moore, J. Barriers and pathways to creating sustainability education programs: Policy, rhetoric and reality. Environ. Educ. Res. 2005, 11, 537–555. [Google Scholar] [CrossRef]

- Trianni, A.; Cagno, E.; Neri, A. Modelling barriers to the adoption of industrial sustainability measures. J. Clean. Prod. 2017, 168, 1482–1504. [Google Scholar] [CrossRef]

- Clarke, S.; Roome, N. Sustainable business: Learning–action networks as organizational assets. Bus. Strategy Environ. 1999, 8, 296–310. [Google Scholar] [CrossRef]

- Morgan, G.; Ryu, K.; Mirvis, P. Leading corporate citizenship: Governance, structure, systems. Corp. Gov. Int. J. Bus. Soc. 2009, 9, 39–49. [Google Scholar] [CrossRef]

- Mathis, A. Corporate social responsibility and policy making: What role does communication play? Bus. Strategy Environ. 2007, 16, 366–385. [Google Scholar] [CrossRef]

- Neftegaz.RU. SUEK Partially Compensated for the Reduction of Coal Supplies to Europe at the Expense of Asian and African Countries. Available online: https://neftegaz.ru/news/coal/749914-suek-chastichno-kompensiroval-sokrashchenie-postavok-uglya-v-evropu-za-schet-stran-azii-i-afriki/ (accessed on 13 January 2023).

- Russian News Agency TASS. Head of SUEK: Reduction of Supplies to Europe is Compensated by Africa and Asia. Available online: https://tass.ru/interviews/15673009 (accessed on 13 January 2023).

- EADaily. It’s Not Sanctions That Spoil Russian Coal Exports: 70% of Kuzbass Coal Warehouses are Crammed. Available online: https://eadaily.com/ru/news/2022/09/15/ne-sankcii-rossiyskomu-uglyu-eksport-portyat-70-skladov-uglya-kuzbassa-zabity (accessed on 13 January 2023).

- International Energy Agency. Coal 2022. Available online: https://www.iea.org/reports/coal-2022 (accessed on 13 January 2023).

- CDU TEK, a Branch of the Federal State Budgetary Institution of the Russian Ministry of Energy. The Carbon Chemistry of the Future. Available online: https://www.cdu.ru/tek_russia/articles/5/884/ (accessed on 13 January 2023).

- Kommersant. Coal Needs Determined Polymers. Available online: https://www.kommersant.ru/doc/5077388 (accessed on 13 January 2023).

- Ministry of Energy of the Russian Federation. Report on the Status of Thermal Power and District Heat Supply in the Russian Federation in 2020. Available online: https://minenergo.gov.ru/system/download-pdf/22832/181259 (accessed on 30 January 2023).

- Pisarenko, M.V.; Shaklein, S.V. Production and consumption of coal in the world and Russia. Min. Ind. 2015, 2, 24–27. (In Russian) [Google Scholar]

{kind=link}

| ESG Component | Indicator Group | Examples of Indicators |

|---|---|---|

| Environmental indicators | Climate change (emission of carbon gas) | Release of carbon gas |

| Carbon footprint | ||

| Funding for environmental impact mitigation | ||

| Company/product vulnerability to climate change | ||

| Natural resources | Water scarcity | |

| Biodiversity | ||

| Land use | ||

| Sources of natural raw materials | ||

| Pollution and Waste | Toxic emissions and waste | |

| Packaging materials and waste | ||

| Electronic waste | ||

| Possibilities | Clean technologies | |

| Green environment | ||

| Energy transition | ||

| Social indicators | Human capital | Personnel Management |

| Health and Safety | ||

| Development of human capital | ||

| Labor standards in the supply chain | ||

| Manufacturer’s liability | Product quality and safety | |

| Chemical safety | ||

| Reliability of financial instruments | ||

| Data privacy and security | ||

| Responsible investment | ||

| Security and demographic risks | ||

| Relations with Stakeholders | Opposing interests and conflicts | |

| Public relations | ||

| Possibilities | Availability of communication | |

| Financial accessibility | ||

| Access to healthcare | ||

| Nutrition and health | ||

| Government indicators | Human capital | Diversity on the Board of Directors |

| Manager Compensation | ||

| Responsibility | ||

| Accountability | ||

| Manufacturer’s liability | Business ethics | |

| Anti-corruption measures | ||

| Stability of the financial environment | ||

| Tax transparency |

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2023 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Blinova, E.; Ponomarenko, T.; Tesovskaya, S. Key Corporate Sustainability Assessment Methods for Coal Companies. Sustainability 2023, 15, 5763. https://doi.org/10.3390/su15075763

Blinova E, Ponomarenko T, Tesovskaya S. Key Corporate Sustainability Assessment Methods for Coal Companies. Sustainability. 2023; 15(7):5763. https://doi.org/10.3390/su15075763

Chicago/Turabian StyleBlinova, Ekaterina, Tatyana Ponomarenko, and Sofiya Tesovskaya. 2023. "Key Corporate Sustainability Assessment Methods for Coal Companies" Sustainability 15, no. 7: 5763. https://doi.org/10.3390/su15075763

APA StyleBlinova, E., Ponomarenko, T., & Tesovskaya, S. (2023). Key Corporate Sustainability Assessment Methods for Coal Companies. Sustainability, 15(7), 5763. https://doi.org/10.3390/su15075763