Research Trends and Directions on Real Estate Investment Trusts’ Performance Risks

Abstract

1. Introduction

2. REITs Performance and Risks

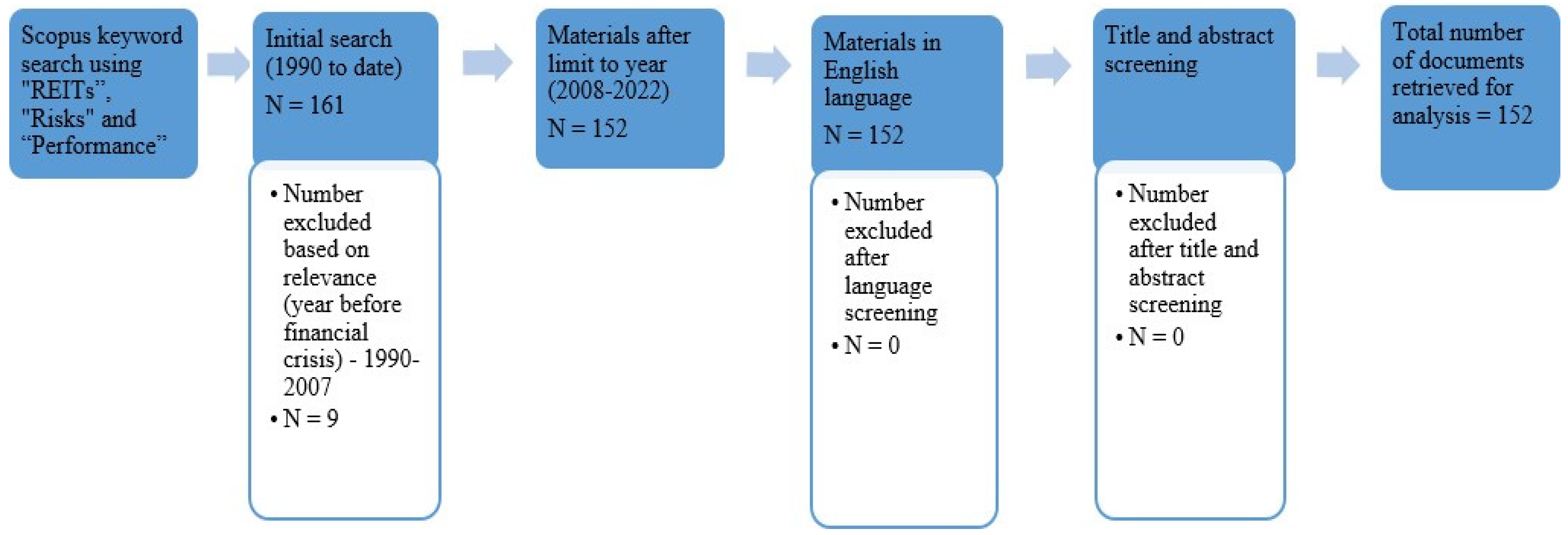

3. Materials and Methods

3.1. Database Selection

3.2. Search Strategy

3.3. Visualisation Techniques and Indicators

3.4. Content Analysis

- Sampling—identifying the materials based on a criterion (in this case, the most cited papers).

- Coding—this entailed assigning themes to the studies based on their content/findings.

- Identifying themes and findings (REITs performance volatility and factors contributing to it).

- Applying theory to explain findings (discussion of the findings in an integrative and consistent manner—aligning the findings from the most occurring keywords, clusters, and trends.

4. Results and Discussion

4.1. Bibliometric Analysis Findings

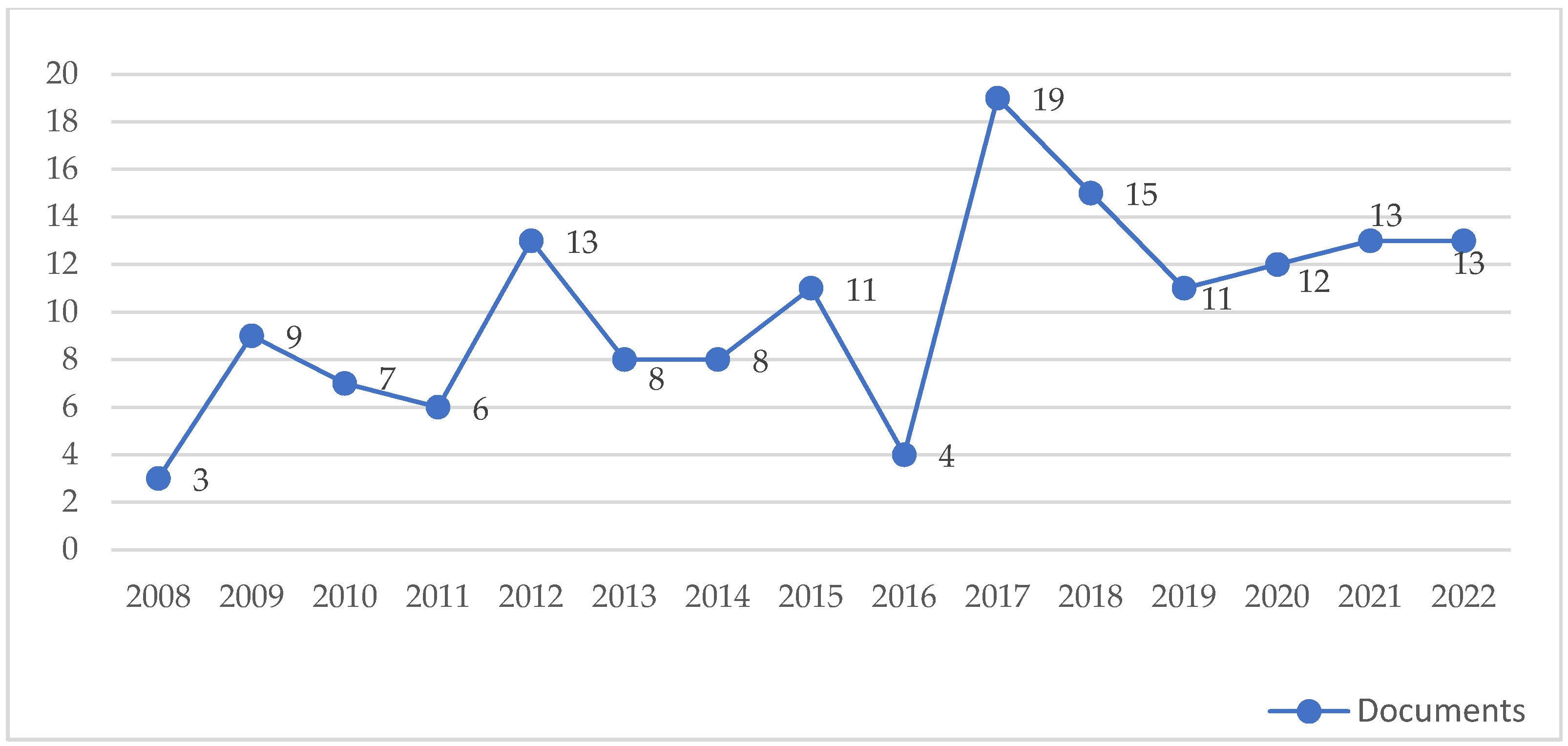

4.1.1. Publication Trend

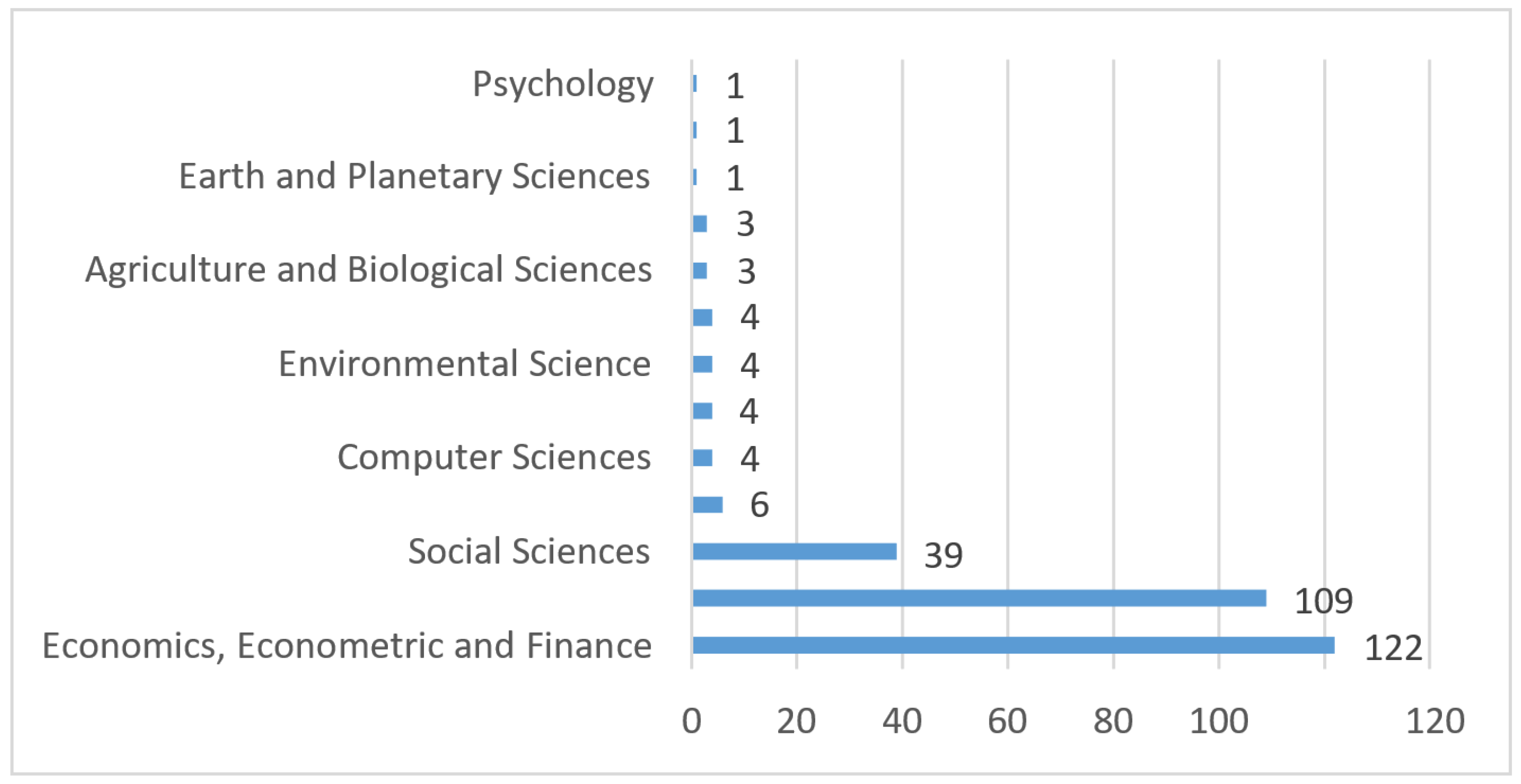

4.1.2. Publication Mapping by Subject Area

4.1.3. Top Sources by Bibliographic Coupling

4.1.4. Top Productive Countries

4.1.5. Co-Authorship Analysis

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Publications | Codes (Related Clusters) | Citation Count | Key Objective(s)/Focus | Methodology | Variables/Sample | Key Findings |

|---|---|---|---|---|---|---|

| Hartzell et al. [61] | Corporate governance | 61 | Impact of corporate governance structures on initial public offering (IPO) | Tobin’s Q as the valuation metric | IPOs of REITs from 1991–1998 Variables—REITs stock prices, returns, IPO dates, total assets, total book value of equity, number of shares outstanding, proportion of compensations tied to performance, incentives, monitoring, and rent extraction. | There is higher valuation for firms with stronger governance. Insider ownership beyond 32.3% reduces firm value. |

| Newell and Osmadi [62] | Risk management in diversified portfolios Portfolio risk assessment Portfolio construction and asset allocation strategies | 40 | Diversification benefits and risk-adjusted returns in a mixed-asset portfolio | Correlation analysis | Islamic Malaysian (IM) REITs total returns calculated using market cap-weighted M-REITs weekly returns estimates (August 2006 to December 2008). | Poor performance was due to the specialised nature, few listed numbers. Diversification benefits were more for Islamic REITs than the conventional counterpart. The smaller size was attributed to the diversification benefit; large assets co-movements were because of poor diversification benefits with the conventional assets. |

| Fei et al. [63] | REITs Portfolio measurement | 35 | Correlation and volatility dynamics of REITs, returns of direct real estate, and stock | Multivariate AD-DCC Multivariate GARCH | Financial time series; monthly data (January 1987 to May 2008); macro-economic variables | Inflation, unemployment rate, and credit spread explained time-varying conditional correlations in REIT returns. Weak correlations were noted between REITs returns and the S&P 500, indicating better future performance of REITs. |

| Nakano et al. [64] | Portfolio risk assessment Portfolio construction and asset allocation strategies | 33 | A new stochastic volatility model to test time-varying expected returns in financial markets. | Generalised exponential moving average model and Particle Filter model. | Total returns of bonds, and stocks; traditional strategies: minimum variance, equal-weighted, and risk parity portfolios; compound returns, Sharpe and Sortino ratios, and drawdowns for performance measures | A simple investment strategy using the proposed model produced superior REITs performance. |

| Zhou and Anderson [65] | Portfolio risk assessment | 33 | Performance of value at risk (VaR) and expected shortfall (ES) for major REITs markets. | VaR and ES | Daily return data from REITs and stock exchanges (January 1993 to December 2009). | No standard method for measuring extreme risks in the global market. Different methods may be required to estimate risks for stocks and REITs. |

| Brounen and De Koning [66] | REITs portfolio measurement | 28 | The evolution and performance of REITs since 1960. | Using asset pricing models | Firm size, property type specialisation, monthly total return data, and geographic portfolios across highly liquid REITs Index countries. | REIT stocks’ outperformance (highest in Europe in the past decade) was positively related to firm size, geographic portfolio focus, and the level of property type specialisation. Systematic REIT risk was highest among the Asian REITs. |

| Hebb et al. [67] | Corporate Governance | 28 | Responsible real estate investment using an integrated approach. | Semi-structured interviews | Real estate companies and REITs firms; variables include stock prices and ESG ratings. | An increasing number of ESG user adoption in many property firms and awareness among institutional investors. An increasing number of ESG ratings makes it an extra-financial determinant to boost REITs performance and value creation. Environmental and social factors impact REITs. |

| Jirasakuldech et al. [68] | Portfolio risk assessment | 23 | The dynamic behaviour of equity REITs (EREIT) volatility performance | GARCH model | Equity REIT from the National Association of Real Estate Investment Trusts (NAREIT). Monthly price indexes plus dividends (January 1972 to June 2006); Russell index price data from 1979. | The conditional volatility for Equity REITs is time-varying, predictable, and persistent. A positive relationship between expected risk and expected returns in the EREIT stocks pre-1993, but not after 1993. |

| Giacomini et al. [69] | Capital structure and REITs efficiency measurement | 21 | US REIT leverage decision-making and the associated impact on risk and returns | Finance literature and theory | Target leverage ratios; the speed estimates to which REITs adjust to any deviation from the targeted capital structure; capital structure decisions on REIT returns performance (conditioned and unconditioned). | Highly levered average REIT tends to underperform less levered REITs. REITs that are highly levered in relation to their target leverage show better performance on a risk-adjusted basis than REITs with less leverage. |

| Lecomte and Ooi [70] | Corporate Governance | 20 | To investigate links between the quality of corporate governance and corporate performance in Asia Pacific Real Estate Association (APREA). | The Ordinary least square regression model | Externally managed REITs companies listed on the Singapore Stock Exchange, financial data, performance data, and corporate governance scores; absolute differences in returns; equally weighted portfolio performance measures. | Evidence of a positive correlation between stock performances and corporate governance practices. S-REITs with good corporate governance tend to register better risk-adjusted returns; however, they do not outperform in terms of operations. |

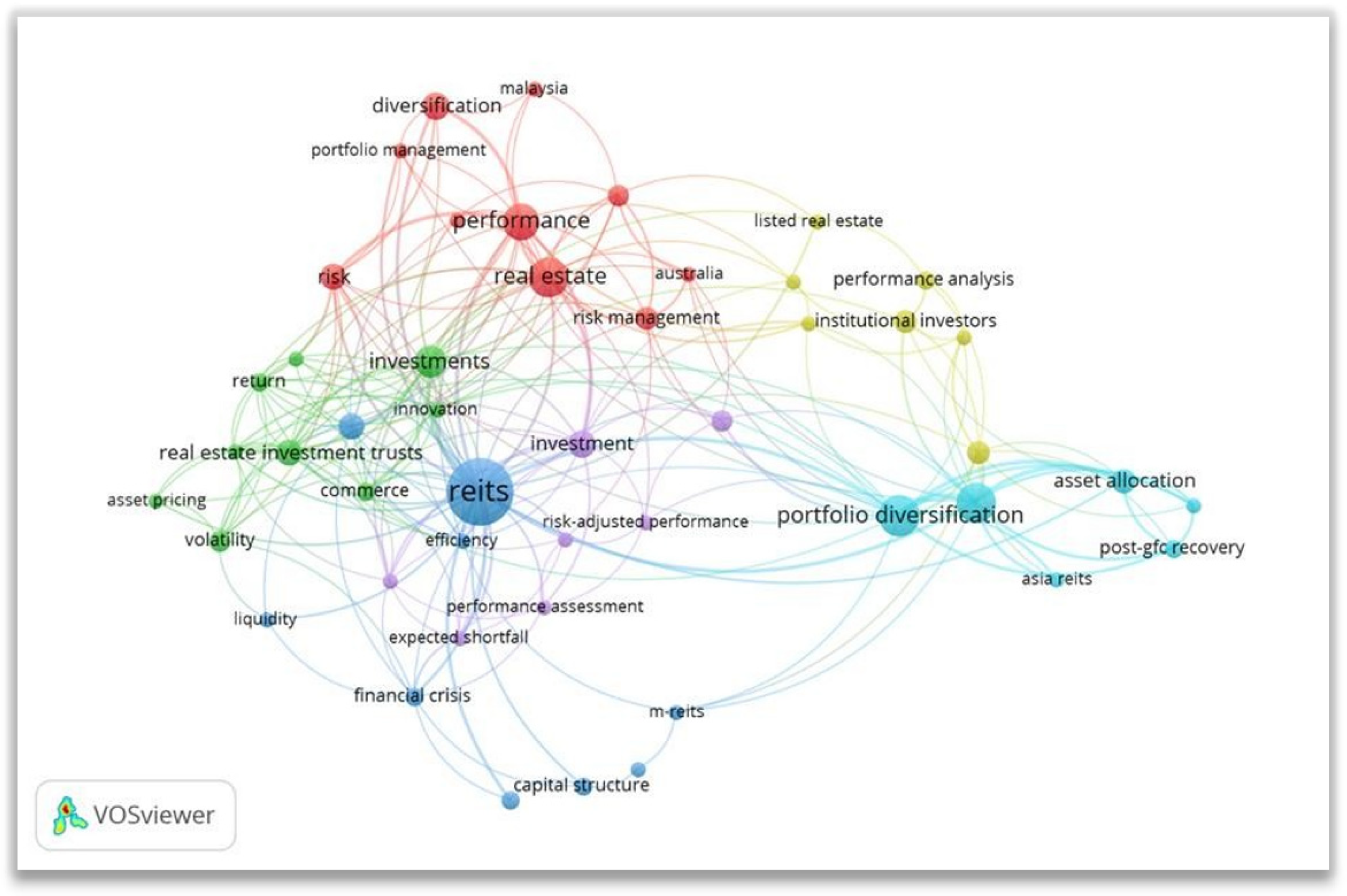

4.1.6. Keyword Analysis

- Cluster 1—Risk management in diversified portfolios (red, top)—Ten keywords were identified including Australia, diversification, Malaysia, performance, portfolio management, property, real estate, risk, risk management, and trusts.

- Cluster 2—REITs portfolio measurement (green, left)—Nine items including asset pricing, CAPM, commerce, economics, innovation, investments, real estate investment trust, return, and volatility were revealed.

- Cluster 3—Capital structure and REITs efficiency measurement (dark blue, middle/left)—Here, the items consisted of capital structure, efficiency, financial crisis, leverage, liquidity, M-REITs, REITs, and REITs performance.

- Cluster 4—Corporate governance (light green, top right)—Seven items were identified including corporate social responsibility, global financial crisis, institutional investors, listed real estate, performance analysis, and real estate investment trusts.

- Cluster 5—Portfolio risk assessment (purple, middle)—The items here included expected shortfall, investment, mixed-asset portfolio, performance assessment, risk assessment, risk-adjusted performance, and stock market.

- Cluster 6—Portfolio construction and asset allocation strategies (blue, right)—Six items were grouped in the sixth cluster. These were Asia REITs, asset allocation, portfolio diversification, portfolio investment, post-GFC, and risk-adjusted returns.

4.2. Content Analysis

- Hartzell et al. [61], with 61 citations, categorised as corporate governance-focused, found that there is higher value for firms with strong governance, but insider ownership reduces the value of firms. This suggests that external stakeholders may bring stronger confidence and size of investments.

- Newell and Osmadi [62] investigated diversification benefits and risk-adjusted returns in a mixed-asset portfolio. The study, with 40 citations, found that the size and extent of co-movements in REITS can be influenced by the diversification benefits. This study, however, has a cross-over link with at least three themes including Risk management in diversified portfolios, Portfolio risk assessment, and Portfolio construction and asset allocation strategies, suggesting a further potential link between diversification and other variables.

- Fei et al. [63]—With a focus on establishing the relationships between macro-economic variables and REITs, this article, cited 35 times, revealed that inflation, unemployment rate, and credit spread contribute to variations in REIT returns. This view was consistent with the second cluster (portfolio measurement), which contained items including economics, volatility, and returns, thus supporting the relationships between the variables investigated by [63].

- Nakano et al. [64] investigated the role of investment strategy and asset allocation in REITs performance and variations.

- Zhou and Anderson [65] focused on methods of portfolio risk assessment using VaR and ES. The study acknowledged that risks contribute to volatility in REITs performance.

- Brounen and De Koning’s [66] study among highly liquid REITs index countries, found that systematic REIT risk was highest among the Asian REITs, and REIT stocks’ outperformance was highest in Europe and correlated with firm size, level of specialised property, and geographic focus.

- Hebb et al. [67] focused on corporate social responsibility and found that environmental and social factors impact REITs. An increasing number of ESG ratings makes it an extra-financial determinant to boost REITs performance and value creation.

5. Discussion and Integration of the Emerging Clusters and Content Analysis Findings

6. Future Research Directions

7. Conclusions

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Conflicts of Interest

References

- Cai, Y.; Xu, K. Net impact of COVID-19 on REIT returns. J. Risk Financ. Manag. 2022, 15, 359. [Google Scholar] [CrossRef]

- Meng, W.; Shen, K.; An, Q. Visual analysis of real estate investment trusts research- A bibliometric analysis based on CiteSpace III. Am. J. Ind. Bus. Manag. 2015, 5, 794–805. [Google Scholar] [CrossRef]

- Alias, A.; Cy, S.T. Performance analysis of REITs: Comparison between M-REITS and UK-REITS. JSCP 2011, 2, 1–24. [Google Scholar] [CrossRef]

- Dabara, D.I. Evolution of REITs in the Nigerian real estate market. J. Prop. Invest. Financ. 2021, 40, 38–48. [Google Scholar] [CrossRef]

- Parker, D. Global Real Estate Investment Trusts: People, Process and Management, 1st ed.; John Wiley & Sons: Chichester, UK, 2012. [Google Scholar]

- Securities and Exchange Commission (SEC). Investor Bulletin: Real Estate Investment Trusts (REITs); Investor Bulletin: Washington, DC, USA, 2011; Volume 800, pp. 1–5. [Google Scholar]

- Sotelo, R.; McGreal, S. Real Estate Investment Trusts in Europe: Evolution, Regulation, and Opportunities for Growth; Springer: Berlin/Heidelberg, Germany, 2016. [Google Scholar] [CrossRef]

- Harrison, D.M.; Panasian, C.A.; Seiler, M.J. Further evidence on the capital structure of REITs. Real Estate Econ. 2011, 39, 133–166. [Google Scholar] [CrossRef]

- Modigliani, F.; Miller, M.H. The Cost of Capital, Corporation Finance, and the Theory of Investment. Am. Econ. Rev. 1958, 48, 261–297. [Google Scholar]

- Newell, G.; Peng, H. The impact of the global financial crisis on A-REITs. Pac. Rim Prop. Res. J. 2009, 15, 453–470. [Google Scholar] [CrossRef]

- Naidoo, N. The Introduction of REITs to the South African Property Market: Opportunities for Fund Managers. Unpublished Master’s Dissertation, University of the Witwatersrand, Johannesburg, South Africa, 2014. [Google Scholar]

- Olanrele, O.O.; Adegunle, T.O.; Fateye, O.B. Causal relationship of N-REITs dividend yield and money market indicators: A case study of Skye Shelter REITs. In Proceedings of the 18th African Real Estate Society (AFRES) Annual Conference, Abeokuta, Nigeria, 11–15 September 2018. [Google Scholar]

- Chiou, J.; Huang, G.; Liano, K.; Pan, M. Are REIT dividend changes a firm-specific or an industry-level signal? Evidence from the decomposition of stock returns. J. Real Estate Portf. Manag. 2022, 28, 139–152. [Google Scholar] [CrossRef]

- Newell, G. The effectiveness of A-REIT futures as a risk management strategy in the global financial crisis. Pac. Rim Prop. Res. J. 2010, 16, 339–357. [Google Scholar] [CrossRef]

- Marzuki, M.J.; Newell, G. The significance and performance of US commercial property in a post-GFC context. J. Prop. Investig. Financ. 2017, 35, 575–588. [Google Scholar] [CrossRef]

- Reddy, W.; Wong, W. Impact of interest rate movements on a-REITS performance before, during and after the global financial crises. In Proceedings of the 23rd Pacific Rim Real Estate Society Annual Conference, Sydney, Australia, 15–18 January 2017. [Google Scholar]

- Luo, Y.; Zhang, X.; Jin, P. Research hotspot and evolution trend of REITs since the new century-from the perspective of biblio-metrics. J. Innov. soc. Sci. Res. 2022, 9, 89–94. [Google Scholar] [CrossRef] [PubMed]

- Bosman, J.; van Mourik, I.; Rasch, M.; Sieverts, E.; Verhoeff, H. Scopus Reviewed and Compared: The Coverage and Functionality of the Citation Database Scopus, Including Comparisons with Web of Science and Google Scholar. 2006, pp. 1–63. Available online: https://www.ltu.se/cms_fs/1.25811!/scopus_reviewed.pdf (accessed on 18 July 2022).

- Akinsomi, O. Performance of Sector-Specific and Diversified REITs in South Africa. In Understanding African Real Estate Markets, 1st ed.; Routledge: London, UK, 2022; pp. 176–187. [Google Scholar]

- Akinsomi, O. How resilient are REITs to a pandemic? The COVID-19 effect. J. Prop. Invest. Financ. 2020, 39, 19–24. [Google Scholar] [CrossRef]

- Basse, T.; Friedrich, M.; Bea, E.V. REITs and the financial crisis: Empirical evidence from the US. J. Prop. Invest. Financ. 2009, 4, 3–10. [Google Scholar] [CrossRef]

- Akinbogun, S.; Jones, C.; Dunse, N. The property market maturity framework and its application to a developing country: The case of Nigeria. J. Real Estate Lit. 2014, 22, 217–232. [Google Scholar] [CrossRef]

- Kola, K.; Kodongo, O. Macroeconomic risks and REITs returns: A comparative analysis. Res. Int. Bus. Financ. 2017, 42, 1228–1243. [Google Scholar] [CrossRef]

- Ro, S.; Ziobrowski, A.J. Does focus really matter? Specialized vs. diversified REITs. J. Real Estate Financ. Econ. 2011, 42, 68–83. [Google Scholar] [CrossRef]

- Newell, G.; Yue, W.; Kwong Wing, C.; Sui Kei, W. The development and performance of REITs in Hong Kong. Pac. Rim Prop. Res. J. 2010, 16, 190–206. [Google Scholar] [CrossRef]

- Newell, G.; Adair, A.; Nguyen, T.K. The significance and performance of French REITs (SIICs) in a mixed-asset portfolio. J. Prop. Investig. Financ. 2013, 31, 575–588. [Google Scholar] [CrossRef]

- Marzuki, M.J.; Newell, G. The evolution of Belgium REITs. J. Prop. Investig. Financ. 2019, 37, 345–362. [Google Scholar] [CrossRef]

- Tsai, I.C.; Lee, C.F. The convergence behavior in REIT markets. J. Prop. Investig. Financ. 2012, 30, 42–57. [Google Scholar] [CrossRef]

- Lee, C.; Ting, K.H. The role of Malaysian securitised real estate in a mixed asset portfolio. J. Financ. Manag. Prop. Constr. 2009, 14, 208–230. [Google Scholar]

- Lee, S. The changing benefit of REITs to the mixed-asset portfolio. J. Real Estate Portf. Manag. 2010, 16, 201–215. [Google Scholar] [CrossRef]

- Ma, T.J.; Lee, G.G.; Liu, J.S.; Lan, R.; Weng, J.H. Bibliographic coupling: A main path analysis from 1963 to 2020. Inf. Syst. Res. 2022, 27. [Google Scholar] [CrossRef]

- Leong, Y.R.; Tajudeen, F.P.; Yeong, W.C. Bibliometric and content analysis of the internet of things research: A social science perspective. OIR 2021, 45, 1148–1166. [Google Scholar] [CrossRef]

- Mora, L.; Deakin, M. Revealing the Main Development Paths of Smart Cities- Untangling Smart Cities: From Utopian Dreams to Innovation Systems for a Technology- Enabled Urban Sustainability; Elsevier: Amsterdam, The Netherlands, 2019; pp. 89–133. [Google Scholar]

- Owojori, O.M.; Okoro, C.S.; Chileshe, N. Current status and emerging trends on the adaptive reuse of buildings: A bibliometric analysis. Sustainability 2021, 13, 11646. [Google Scholar] [CrossRef]

- Vaismoradi, M.; Turunen, H.; Bondas, T. Content analysis and thematic analysis: Implications for conducting a qualitative. Nurs. Health Sci. 2013, 15, 398–405. [Google Scholar] [CrossRef]

- Kumpulainen, M.; Seppänen, M. Combining web of science and scopus datasets in citation-based literature study. Scientometrics 2022, 127, 5613–5631. [Google Scholar] [CrossRef]

- Falagas, M.E.; Pitsouni, E.I.; Malietzis, G.A.; Pappas, G. Comparison of PubMed, Scopus, Web of Science, and Google Scholar: Strengths and weaknesses. FASEB J. 2008, 22, 338–342. [Google Scholar] [CrossRef]

- Hosseini, M.R.; Maghrebi, M.; Akbarnezhad, A.; Martek, I.; Arashpour, M. Analysis of citation networks in building information modeling research. J. Constr. Eng. Manag. 2018, 144, 04018064. [Google Scholar] [CrossRef]

- Bartol, T.; Budimir, G.; Dekleva-Smrekar, D.; Pusnik, M.; Juznic, P. Assessment of research fields in Scopus and Web of Science in the view of national research evaluation in Slovenia. Scientometrics 2014, 98, 1491–1504. [Google Scholar] [CrossRef]

- Sweileh, W.M. Bibliometric analysis of peer-reviewed literature on climate change and human health with an emphasis on infectious diseases. Glob. Health 2020, 16, 1–17. [Google Scholar] [CrossRef]

- Pham, M.T.; Rajic, A.; Greig, J.D.; Sargeant, J.M.; Papadopoulos, A.; McEwen, S.A. A scoping review of scoping reviews: Advancing the approach and enhancing the consistency. Res. Synth. Methods 2014, 5, 371–385. [Google Scholar] [CrossRef]

- Šūmakaris, P.; Sceulovs, D.; Korsakiene, R. Current research trends on interrelationships of eco-innovation and internationalisation: A bibliometric analysis. J. Risk Financ. Manag. 2020, 13, 85. [Google Scholar] [CrossRef]

- Van Eck, N.; Waltman, L. Software survey: Vosviewer, a computer program for bibliometricmapping. Scientometrics 2010, 84, 523–538. [Google Scholar] [CrossRef] [PubMed]

- Cobo, M.; Lopez-Herrera, A.; Herrera-Viedma, E.; Herrera, F. Science mapping software tools: Review, analysis, and cooperative study among tools. J. Am. Soc. Inf. Sci. Technol. 2011, 62, 1382–1402. [Google Scholar] [CrossRef]

- Maggon, M. A bibliometric analysis of the first 20 years of the Journal of Corporate Real Estate. J. Corp. Real Estate 2023, 25, 7–28. [Google Scholar] [CrossRef]

- Hudson, J. Trends in multi-authored papers in economics. J. Econ. Perspect. 1996, 10, 153–158. [Google Scholar] [CrossRef]

- Bernatovic, I.; Gomezel, A.S.; Cerne, M. Mapping the knowledge-hiding field and its future prospects: A bibliometric co-citation, co-word, and coupling analysis. Knowl. Manag. Res. Pract. 2022, 20, 394–409. [Google Scholar] [CrossRef]

- Van Eck, N.; Waltman, L. Text Mining and Visualization Using VOSviewer. 2011. Available online: https://arxiv.org/ftp/arxiv/papers/1109/1109.2058.pdf (accessed on 18 July 2022).

- Van Eck, N.; Waltman, L. Citation-based clustering of publications using CitNetExplorer and VOSviewer. Scientometrics 2017, 111, 1053–1070. [Google Scholar] [CrossRef]

- Walsh, I.; Rowe, F. BIBGT: Combining bibliometrics and grounded theory to conduct a literature review. Eur. J. Inf. Syst. 2022; in press. [Google Scholar]

- Bhandari. Design Thinking: From Bibliometric Analysis to Content Analysis, Current Research Trends, and Future Research Directions. Springer 2022. Available online: https://www.researchgate.net/publication/359298926_Design_Thinking_from_Bibliometric_Analysis_to_Content_Analysis_Current_Research_Trends_and_Future_Research_Directions (accessed on 9 February 2023).

- Okoro, C.S. Sustainable Facilities Management in the Built Environment: A Mixed-Method Review. Sustainability 2023, 15, 3174. [Google Scholar] [CrossRef]

- Stevens, J.A. Do changes in industry classification systems matter? Evidence from REITs. J. Real Estate Res. 2022, 44, 377–398. [Google Scholar] [CrossRef]

- BDO. BDO Risk Factor Report for REITs. United States. 2016. Available online: https://www.bdo.com/insights/industries/2016-bdo-riskfactor-report-for-reits (accessed on 3 January 2023).

- Morri, G.; Baccarin, A. European REITs NAV discount: Do investors believe in property appraisal? J. Prop. Invest. Financ. 2016, 34, 347–374. [Google Scholar] [CrossRef]

- Singh, V.K.; Singh, P.; Karmakar, M.; Leta, J.; Marr, P. The journal coverage of Web of Science, Scopus, and Dimensions: A comparative analysis. Scientometrics 2021, 126, 5113–5142. [Google Scholar] [CrossRef]

- Kessler, M.M. Bibliographic coupling between scientific papers. Am. Doc. 1963, 14, 10–25. [Google Scholar] [CrossRef]

- Cardoso, L.; Silva, R.; de Almeida, G.G.F.; Santos, L.L. A bibliometric model to analyze country research performance: SciVal Topic Prominence Approach in Tourism, Leisure and Hospitality. Sustainability 2020, 12, 9897. [Google Scholar] [CrossRef]

- Sampaio, R.B.; Fonseca, M.V.D.A.; Zicker, F. Co-authorship network analysis in health research: Method and potential use. Health Res. Policy Syst. 2016, 14, 1–10. [Google Scholar]

- Kelly, J.C.; Glynn, R.W.; O’Briain, D.E.; Felle, P.; McCabe, J.P. The 100 classic papers of orthopaedic surgery: A bibliometric analysis. J. Bone Jt. Surg. Br. 2010, 92, 1338–1343. [Google Scholar] [CrossRef]

- Hartzell, J.C.; Kallberg, J.G.; Liu, C.H. The role of corporate governance in initial public offerings: Evidence from real estate investment trusts. J. Law Econ. 2008, 51, 539–562. [Google Scholar] [CrossRef]

- Newell, G.; Osmadi, A. The development and preliminary performance analysis of Islamic REITs in Malaysia. J. Prop. Res. 2009, 26, 329–347. [Google Scholar] [CrossRef]

- Fei, P.; Ding, L.; Deng, Y. Correlation and volatility dynamics in REIT returns: Performance and portfolio consideration. J. Portf. Manag. Winter 2010, 36, 113–125. [Google Scholar] [CrossRef]

- Nakano, M.; Takahashi, A.; Takahashi, S. Generalized exponential moving average (EMA) model with particle filtering and anomaly detection. Expert Syst. Appl. 2017, 73, 187–200. [Google Scholar] [CrossRef]

- Zhou, J.; Anderson, R.I. Extreme risk measures for international REIT markets. J. Real Estate Financ. Econ. 2012, 45, 152–170. [Google Scholar] [CrossRef]

- Brounen, D.; De Koning, S. 50 years of real estate investment trusts: An international examination of the rise and performance of Reits. J. Real Estate Lit. 2012, 20, 197–223. [Google Scholar] [CrossRef]

- Hebb, T.; Hamilton, A.; Hachigian, H. Responsible property investing in Canada: Factoring both environmental and social impacts in the Canadian real estate market. J. Bus. 2010, 92 (Suppl. S1), 99–115. [Google Scholar] [CrossRef]

- Jirasakuldech, B.; Campbell, R.D.; Emekter, R. Conditional volatility of equity real estate investment trust returns: A pre- and post-1993 comparison. J. Real Estate Financ. Econ. 2009, 38, 137–154. [Google Scholar] [CrossRef]

- Giacomini, E.; Ling, D.C.; Naranjo, A. REIT Leverage and Return Performance: Keep Your Eye on the Target. Real Estate Econ. 2017, 45, 930–978. [Google Scholar] [CrossRef]

- Lecomte, P.; Ooi, J.T. Corporate governance and performance of externally managed Singapore REITs. J. Real Estate Financ. Econ. 2013, 46, 664–684. [Google Scholar] [CrossRef]

- Ntuli, M.; Akinsomi, O. An overview of the initial performance of the South African REIT market. J. Real Estate Lit. 2017, 25, 365–388. [Google Scholar] [CrossRef]

- Newell, G.; Marzuki, M.J.B. The significance and performance of UK-REITs in a mixed-asset portfolio. J. Eur. Real Estate Res. 2016, 9, 171–182. [Google Scholar] [CrossRef]

- Yat-Hung, C.; Joinkey, S.C.-K.; Bo-Sin, T. Time-varying performance of four Asia-Pacific REITs. J. Prop. Investig. Financ. 2008, 26, 210–231. [Google Scholar] [CrossRef]

- Coskun, Y.; Selcuk-Kestel, A.; Yilmaz, B. Diversification benefit and return performance of REITs using CAPM and Fama-French: Evidence from Turkey. Borsa Istanbul Rev. 2017, 17, 199–215. [Google Scholar] [CrossRef]

- Jackson, L.A. An application of the Fama-French three-factor model to lodging REITs: A 20-year analysis. Tour. Hosp. Res. 2020, 20, 31–40. [Google Scholar] [CrossRef]

- Morri, G.; Jostov, K. The effect of leverage on the performance of real estate companies: A pan-European post-crisis perspective of EPRA/NAREIT index. J. Eur. Real Estate Res. 2018, 11, 284–318. [Google Scholar] [CrossRef]

- Bao, H.; Gong, C. Reference-dependent analysis of capital structure and REIT performance. J. Behav. Exp. Econ. 2017, 69, 38–49. [Google Scholar] [CrossRef]

- Westermann, S.; Niblock, S.J.; Kortt, M.A. A review of corporate social responsibility and real estate investment trust studies: An Australian perspective. Econ. Pap. J. Appl. Econ. Policy 2018, 37, 92–110. [Google Scholar] [CrossRef]

- Zhou, J. Extreme risk measures for REITs: A comparison among alternative methods. Appl. Financ. Econ. 2012, 22, 113–126. [Google Scholar] [CrossRef]

- Stelk, S.J.; Zhou, J.; Anderson, R.I. REITs in a mixed-assets portfolio: An investigation of extreme risks. JAI Summer 2017, 20, 81–91. [Google Scholar]

- Coen, A.; Lecomte, P. Another look at Asian REITs performance after the global financial crisis. Handb. Asian Financ. REITs Trading Fund Perform. 2014, 2, 69–94. [Google Scholar]

- Schulte, K. Determinants of Risk-Adjusted REITs Performance-Evidence from US Equity REITs; European Real Estate Society: Istanbul, Turkey, 2009; p. 266. [Google Scholar]

- Milcheva, S. Volatility and the cross-section of real estate equity returns during COVID-19. J. Real Estate Financ. Econ. 2022, 65, 293–320. [Google Scholar] [CrossRef]

- Wasiuzzaman, S. Impact of COVID 19 on the Saudi stock market: Analysis of return, volatility and trading volume. J. Asset Manag. 2022, 23, 350–363. [Google Scholar] [CrossRef]

| Source | Documents | Citations | Total Link Strength |

|---|---|---|---|

| Journal of Property Investment and Finance | 29 | 182 | 720 |

| Journal of Real Estate Finance and Economics | 23 | 320 | 656 |

| Pacific Rim Property Research Journal | 10 | 135 | 270 |

| Journal of European Real Estate Research | 5 | 33 | 256 |

| Journal of Real Estate Literature | 5 | 45 | 245 |

| Journal of Real Estate Portfolio | 5 | 50 | 216 |

| Handbook of Asian Finance: REITs, Trading, and Fund Performance | 3 | 10 | 169 |

| Journal of Asset Management | 3 | 20 | 131 |

| Journal of Real Estate Research | 3 | 5 | 83 |

| Real Estate Economics | 3 | 30 | 70 |

| Country | Documents | Citations | Total Link Strength |

|---|---|---|---|

| Australia | 45 | 437 | 14 |

| United States | 44 | 492 | 14 |

| United Kingdom | 19 | 102 | 10 |

| Malaysia | 17 | 103 | 7 |

| Canada | 12 | 121 | 7 |

| Italy | 11 | 75 | 6 |

| Turkey | 6 | 16 | 1 |

| China | 5 | 20 | 3 |

| Singapore | 5 | 45 | 3 |

| Taiwan | 5 | 79 | 3 |

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2023 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Okoro, C.; Ayaba, M.M. Research Trends and Directions on Real Estate Investment Trusts’ Performance Risks. Sustainability 2023, 15, 5436. https://doi.org/10.3390/su15065436

Okoro C, Ayaba MM. Research Trends and Directions on Real Estate Investment Trusts’ Performance Risks. Sustainability. 2023; 15(6):5436. https://doi.org/10.3390/su15065436

Chicago/Turabian StyleOkoro, Chioma, and Marie Mangwi Ayaba. 2023. "Research Trends and Directions on Real Estate Investment Trusts’ Performance Risks" Sustainability 15, no. 6: 5436. https://doi.org/10.3390/su15065436

APA StyleOkoro, C., & Ayaba, M. M. (2023). Research Trends and Directions on Real Estate Investment Trusts’ Performance Risks. Sustainability, 15(6), 5436. https://doi.org/10.3390/su15065436