Navigating the Future: Blockchain’s Impact on Accounting and Auditing Practices

Abstract

:1. Introduction

2. Literature Review

2.1. Blockchain Technology and Accounting

2.2. Blockchain Technology and Auditing

2.3. Blockchain Technology and Cryptocurrencies

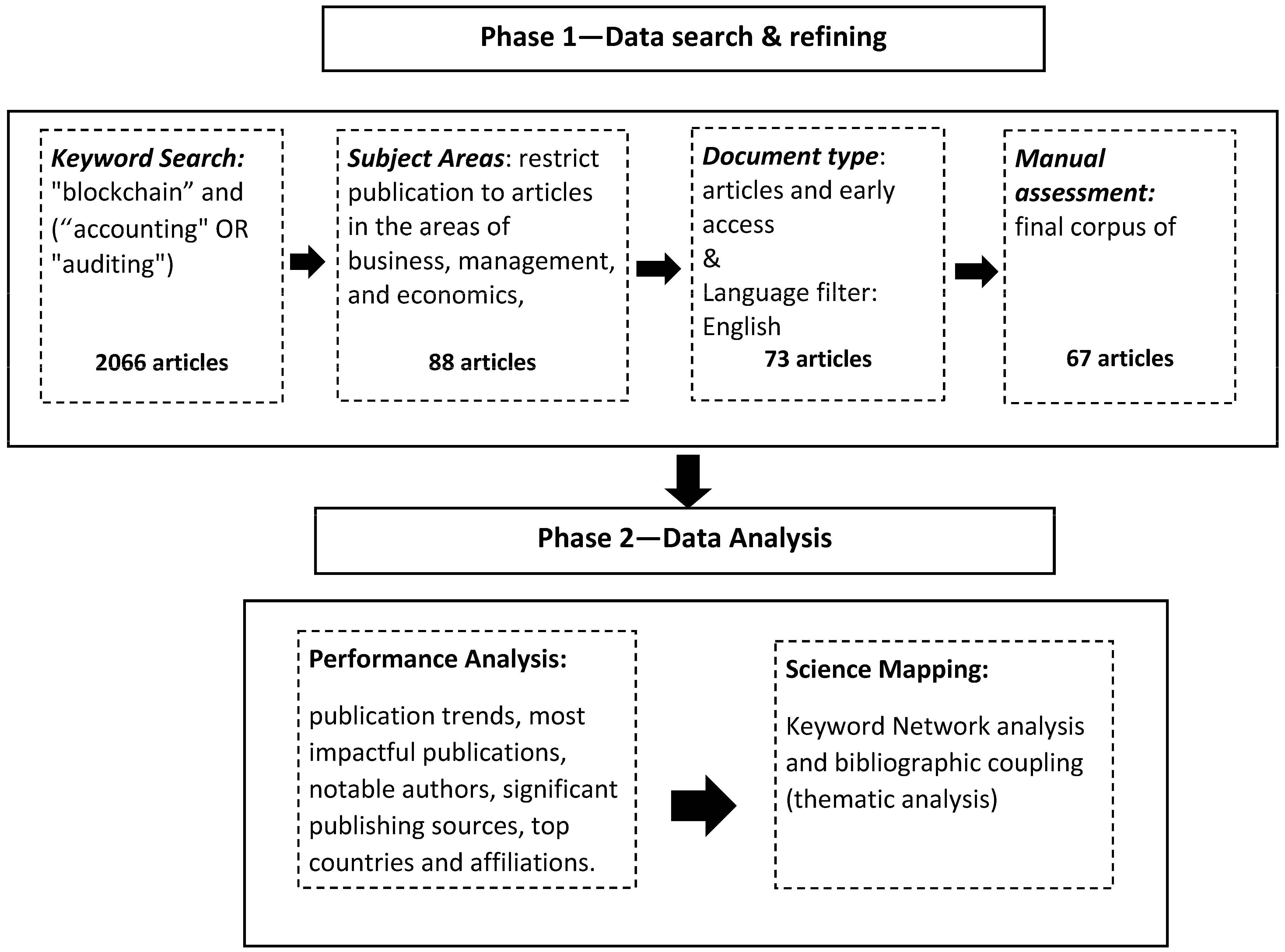

3. Materials and Methods

- RQ1:

- What are the trends in publications on blockchain technology within the realms of accounting and auditing?

- RQ2:

- Which are the major sources, documents, authors, institutions, and countries contributing toward blockchain technology within the realms of accounting and auditing?

- RQ3:

- What are the major themes of blockchain technology within the realms of accounting and auditing?

- RQ4:

- What are potential future areas of research on blockchain technology within the realms of accounting and auditing?

3.1. Data Extraction and Inclusion and Exclusion Criteria

3.2. Data Analysis

4. Results

4.1. Main Information

4.2. Publication Trend

4.3. Most Cited Document

4.4. Most Prolific Authors and Affiliations

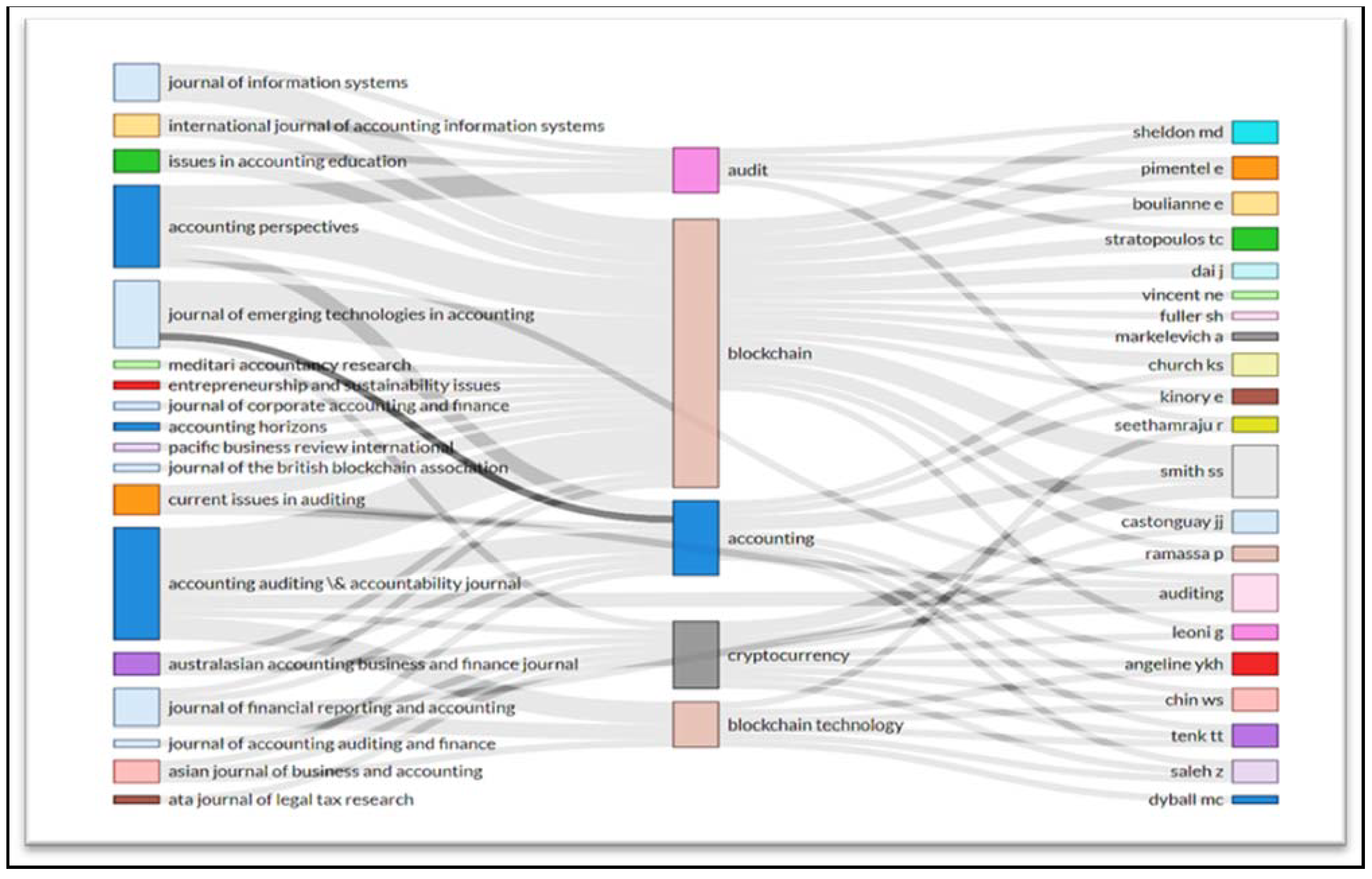

4.5. Most Cited Sources

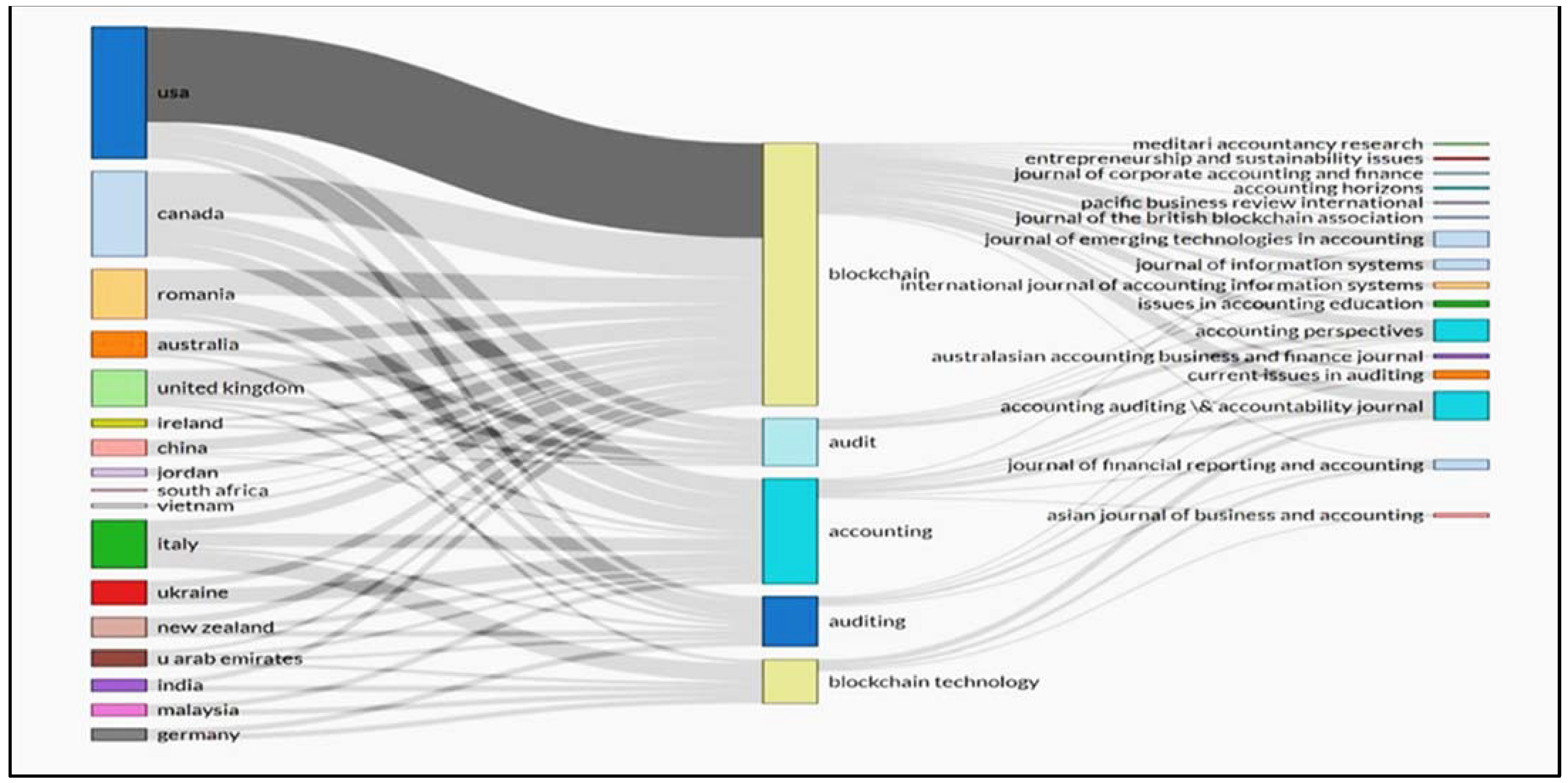

4.6. Countries with the Highest Scientific Production

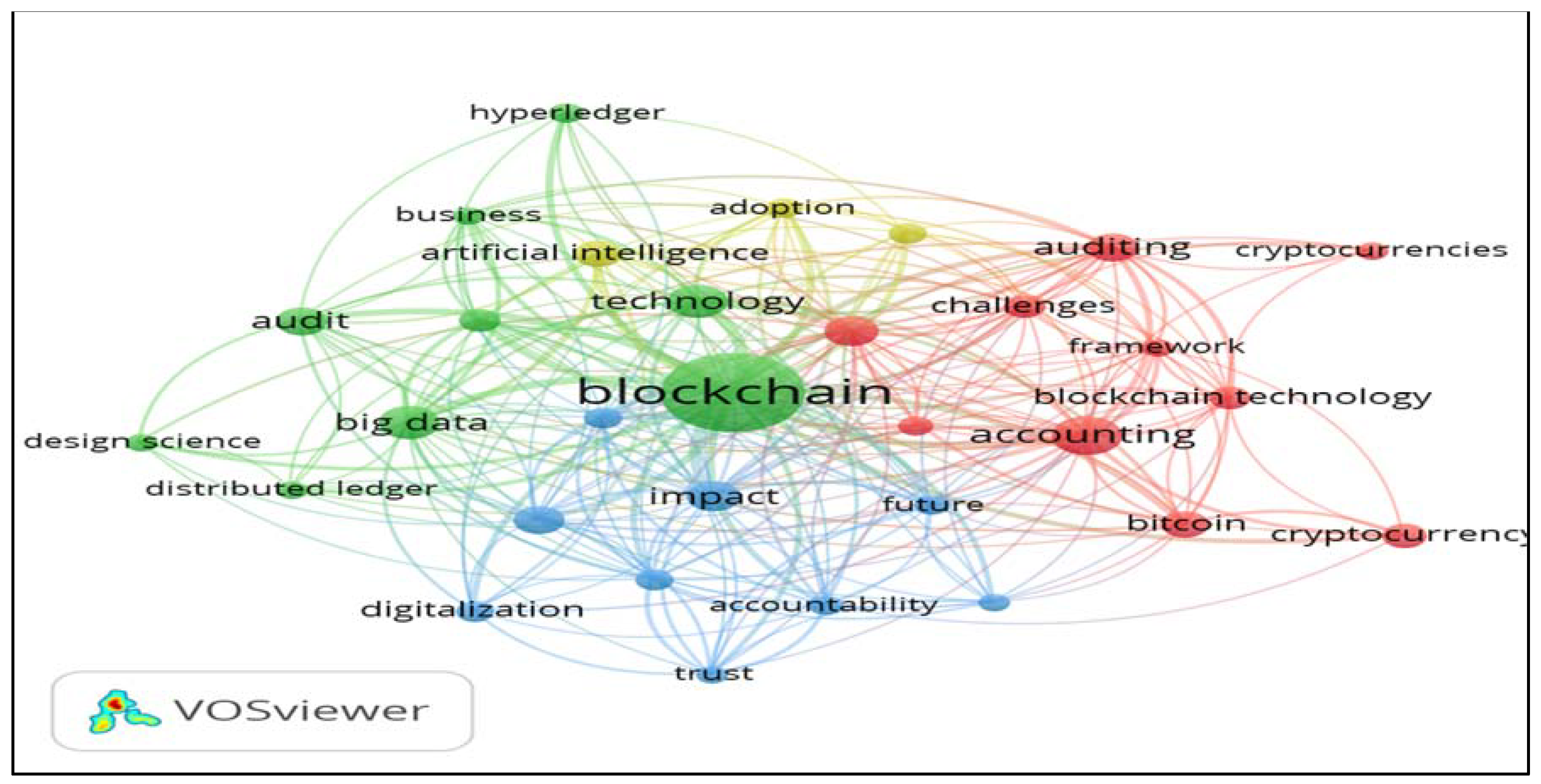

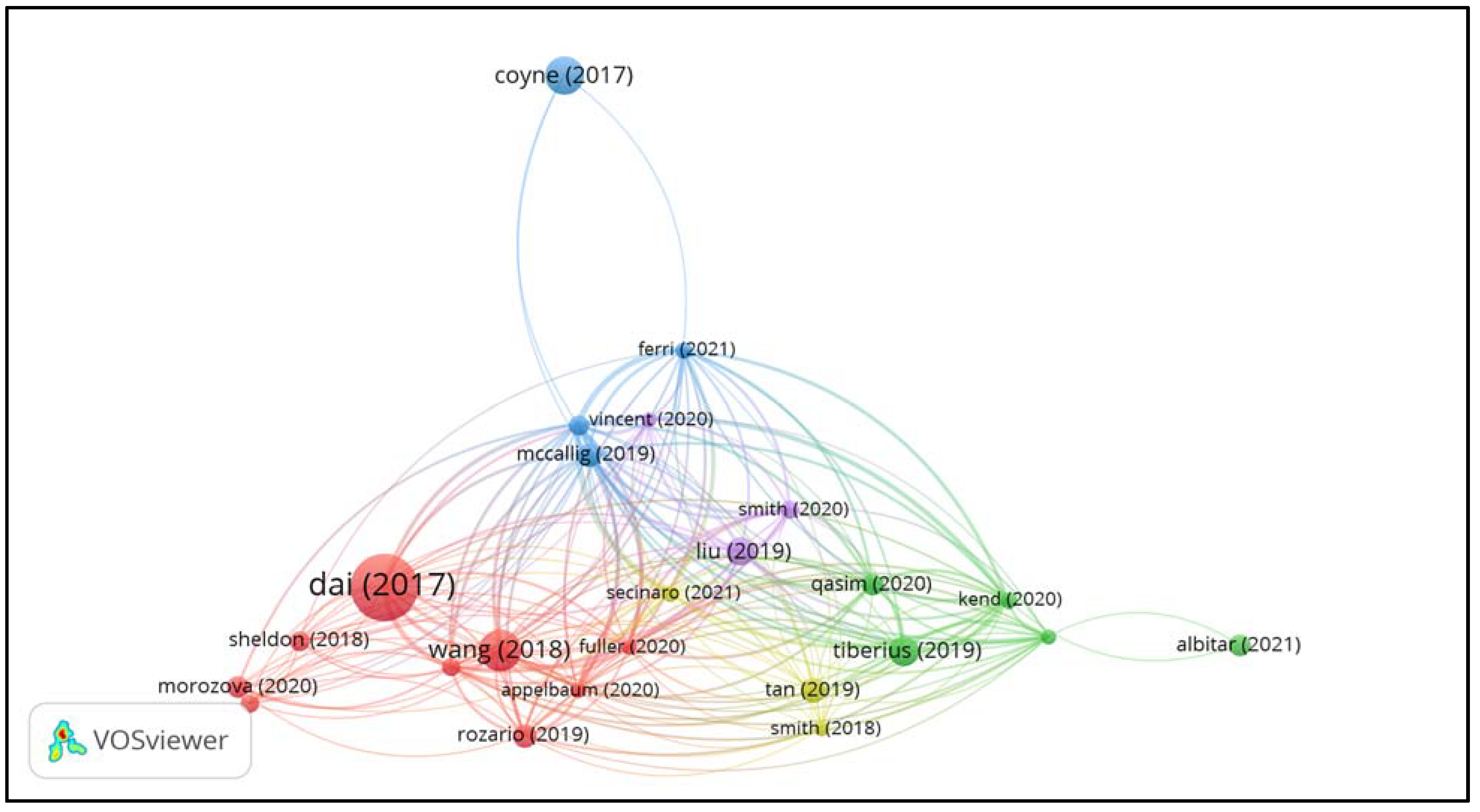

4.7. Co-Occurrence Network

4.8. Content Analysis

4.8.1. Theme 1: Blockchain Technology to Strengthen Financial Reporting Systems

4.8.2. Theme 2: Blockchain Technology and the Future of Auditing

4.9. Theme 3: Valuation of Cryptocurrencies

5. Conclusions

Author Contributions

Funding

Informed Consent Statement

Data Availability Statement

Acknowledgments

Conflicts of Interest

References

- Kokina, J.; Mancha, R.; Pachamanova, D. Blockchain: Emergent industry adoption and implications for accounting. J. Emerg. Technol. Account. 2017, 14, 91–100. [Google Scholar] [CrossRef]

- Pimentel, E.; Boulianne, E. Blockchain in accounting research and practice: Current trends and future opportunities. Account. Perspect. 2020, 19, 325–361. [Google Scholar] [CrossRef]

- Schmitz, J.; Leoni, G. Accounting and auditing at the time of blockchain technology: A research agenda. Aust. Account. Rev. 2019, 29, 331–342. [Google Scholar] [CrossRef]

- Secinaro, S.; Dal Mas, F.; Brescia, V.; Calandra, D. Blockchain in the accounting, auditing and accountability fields: A bibliometric and coding analysis. Account. Audit. Account. J. 2021, 35, 168–203. [Google Scholar] [CrossRef]

- Gietzmann, M.; Grossetti, F. Blockchain and other distributed ledger technologies: Where is the accounting? J. Account. Public Policy 2021, 40, 106881. [Google Scholar] [CrossRef]

- Kommunuri, J. Artificial intelligence and the changing landscape of accounting: A viewpoint. Pac. Account. Rev. 2022. ahead of print. [Google Scholar] [CrossRef]

- Lacurezeanu, R.; Tiron-Tudor, A.; Bresfelean, V.P. Robotic process automation in audit and accounting. Audit. Financ. 2020, 18, 752–770. [Google Scholar] [CrossRef]

- Bellucci, M.; Bianchi, D.C.; Manetti, G. Blockchain in accounting practice and research: Systematic literature review. Meditari Account. Res. 2022, 30, 121–146. [Google Scholar] [CrossRef]

- Garanina, T.; Ranta, M.; Dumay, J. Blockchain in accounting research: Current trends and emerging topics. Account. Audit. Account. J. 2021, 35, 1507–1533. [Google Scholar] [CrossRef]

- Spanò, R.; Massaro, M.; Ferri, L.; Dumay, J.; Schmitz, J. Blockchain in accounting, accountability and assurance: An overview. Account. Audit. Account. J. 2022, 35, 1493–1506. [Google Scholar] [CrossRef]

- Abdennadher, S.; Grassa, R.; Abdulla, H.; Alfalasi, A. The effects of blockchain technology on the accounting and assurance profession in the UAE: An exploratory study. J. Financ. Report. Account. 2022, 20, 53–71. [Google Scholar] [CrossRef]

- Marrone, M.; Hazelton, J. The disruptive and transformative potential of new technologies for accounting, accountants and accountability: A review of current literature and call for further research. Meditari Account. Res. 2019, 27, 677–694. [Google Scholar] [CrossRef]

- Bonsón, E.; Bednárová, M. Blockchain and its implications for accounting and auditing. Meditari Account. Res. 2019, 27, 725–740. [Google Scholar] [CrossRef]

- Dai, J.; Vasarhelyi, M.A. Toward blockchain-based accounting and assurance. J. Inf. Syst. 2017, 31, 5–21. [Google Scholar] [CrossRef]

- Benedetti, H.; Nikbakht, E. Returns and network growth of digital tokens after cross-listings. J. Corp. Financ. 2021, 66, 101853. [Google Scholar] [CrossRef]

- Yu, Y.; Li, Y.; Tian, J.; Liu, J. Blockchain-based solutions to security and privacy issues in the internet of things. IEEE Wirel. Commun. 2018, 25, 12–18. [Google Scholar] [CrossRef]

- Tang, X.; Zhu, L.; Shen, M.; Peng, J.; Kang, J.; Niyato, D.; Abd El-Latif, A.A. Secure and Trusted Collaborative Learning Based on Blockchain for Artificial Intelligence of Things. IEEE Wirel. Commun. 2022, 29, 14–22. [Google Scholar] [CrossRef]

- Iftikhar, Z.; Javed, Y.; Zaidi, S.Y.A.; Shah, M.A.; Iqbal Khan, Z.; Mussadiq, S.; Abbasi, K. Privacy Preservation in Resource-Constrained IoT Devices Using Blockchain—A Survey. Electronics 2021, 10, 1732. [Google Scholar] [CrossRef]

- Centobelli, P.; Cerchione, R.; del Vecchio, P.; Oropallo, E.; Secundo, G. Blockchain technology design in accounting: Game changer to tackle fraud or technological fairy tale? Account. Audit. Account. J. 2022, 35, 1566–1597. [Google Scholar] [CrossRef]

- Han, H.; Shiwakoti, R.K.; Jarvis, R.; Mordi, C.; Botchie, D. Accounting and auditing with blockchain technology and artificial Intelligence: A literature review. Int. J. Account. Inf. Syst. 2023, 48, 100598. [Google Scholar] [CrossRef]

- Demirkan, S.; Demirkan, I.; McKee, A. Blockchain technology in the future of business cyber security and accounting. J. Manag. Anal. 2020, 7, 189–208. [Google Scholar] [CrossRef]

- Liu, M.; Wu, K.; Xu, J.J. How will blockchain technology impact auditing and accounting: Permissionless versus permissioned blockchain. Curr. Issues Audit. 2019, 13, A19–A29. [Google Scholar] [CrossRef]

- Kolisnyk, O.; Hurina, N.; Druzhynska, N. Innovative Technologies in Accounting and Auditing: The Use of Blockchain Technology. Financ. Credit. Act. Probl. Theory Pract. 2023, 3, 24–41. [Google Scholar]

- Matskiv, H.; Smirnova, I.; Malikova, A. The Application of Blockchain Technology In Accounting and Auditing: Experience of Ukraine And Kazakhstan. Financ. Credit. Act. Probl. Theory Pract. 2023, 1, 180–191. [Google Scholar]

- Chowdhury, E.K.; Khan, I.I.; Dhar, B.K. Strategy for implementing blockchain technology in accounting: Perspectives of stakeholders in a developing nation. Bus. Strategy Dev. 2023, 6, 477–490. [Google Scholar] [CrossRef]

- Nordgren, A.; Weckström, E.; Martikainen, M.; Lehner, O. Blockchain in the Fields of Finance and Accounting: A Disruptive Technology or an Overhyped Phenomenon? ACRN J. Financ. Risk Perspect. 2019, 8, 47–58. Available online: https://www.acrn-journals.eu/resources/SI08_2019d.pdf (accessed on 17 October 2023).

- Tapscott, D.; Tapscott, A. How blockchain will change organizations. MIT Sloan Manag. Rev. 2017, 58, 10. [Google Scholar]

- Tijan, E.; Aksentijević, S.; Ivanić, K.; Jardas, M. Blockchain technology implementation in logistics. Sustainability 2019, 11, 1185. [Google Scholar] [CrossRef]

- Karajovic, M.; Kim, H.M.; Laskowski, M. Thinking outside the block: Projected phases of blockchain integration in the accounting industry. Aust. Account. Rev. 2019, 29, 319–330. [Google Scholar] [CrossRef]

- Villacreses Ponce, Á.G. Blockchain Application for the Supply Chain of the Ecuadorian oil Industry. Bachelor’s Thesis, Universidad de Investigación de Tecnología Experimental Yachay, San Miguel de Urcuquí, Ecuador, 2020. [Google Scholar]

- CPA Canada. 2017. Available online: https://us.aicpa.org/content/dam/aicpa/interestareas/frc/assuranceadvisoryservices/downloadabledocuments/blockchain-technology-and-its-potential-impact-on-the-audit-and-assurance-profession.pdf (accessed on 17 October 2023).

- Dyball, M.C.; Seethamraju, R. Client use of blockchain technology: Exploring its (potential) impact on financial statement audits of Australian accounting firms. Account. Audit. Account. J. 2022, 35, 1656–1684. [Google Scholar] [CrossRef]

- Javaid, M.; Haleem, A.; Singh, R.P.; Suman, R.; Khan, S. A review of Blockchain Technology applications for financial services. BenchCouncil Trans. Benchmarks Stand. Eval. 2022, 2, 100073. [Google Scholar] [CrossRef]

- Wang, T.; Wang, Y.; McLeod, A. Do health information technology investments impact hospital financial performance and productivity? Int. J. Account. Inf. Syst. 2018, 28, 1–13. [Google Scholar] [CrossRef]

- Deloitte. Impact of Blockchain on the Accounting Profession|Deloitte|Audit. Deloitte Bangladesh. 2022. Available online: https://www2.deloitte.com/bd/en/pages/audit/articles/gx-impact-of-blockchain-in-accounting.html (accessed on 17 October 2023).

- Abubakar, M.; McCarron, P.; Jaroucheh, Z.; Al Dubai, A.; Buchanan, B. Blockchain-based Platform for Secure Sharing and Validation of Vaccination Certificates. In Proceedings of the 2021 14th International Conference on Security of Information and Networks (SIN), Edinburgh, UK, 15–17 December 2021; pp. 1–8. [Google Scholar] [CrossRef]

- Karamitsos, I.; Papadaki, M.; Al Barghuthi, N.B. Design of the blockchain smart contract: A use case for real estate. J. Inf. Secur. 2018, 9, 177–190. [Google Scholar] [CrossRef]

- Peters, G.W.; Panayi, E. Understanding Modern Banking Ledgers through Blockchain Technologies: Future of Transaction Processing and Smart Contracts on the Internet of Money; Springer International Publishing: Berlin/Heidelberg, Germany, 2016; pp. 239–278. [Google Scholar]

- Smith, S.S.; Castonguay, J.J. Blockchain and accounting governance: Emerging issues and considerations for accounting and assurance professionals. J. Emerg. Technol. Account. 2020, 17, 119–131. [Google Scholar] [CrossRef]

- Zheng, P.; Zheng, Z.; Wu, J.; Dai, H.N. Xblock-eth: Extracting and exploring blockchain data from ethereum. IEEE Open J. Comput. Soc. 2020, 1, 95–106. [Google Scholar] [CrossRef]

- Dutta, P.; Choi, T.M.; Somani, S.; Butala, R. Blockchain technology in supply chain operations: Applications, challenges and research opportunities. Transp. Res. Part E Logist. Transp. Rev. 2020, 142, 102067. [Google Scholar] [CrossRef]

- Gamage, K.A.; Wijesuriya, D.I.; Ekanayake, S.Y.; Rennie, A.E.; Lambert, C.G.; Gunawardhana, N. Online delivery of teaching and laboratory practices: Continuity of university programmes during COVID-19 pandemic. Educ. Sci. 2020, 10, 291. [Google Scholar] [CrossRef]

- Qiao, L.; Dang, S.; Shihada, B.; Alouini, M.S.; Nowak, R.; Lv, Z. Can blockchain link the future? Digit. Commun. Netw. 2022, 8, 687–694. [Google Scholar] [CrossRef]

- Oh, J.; Shong, I. A case study on business model innovations using Blockchain: Focusing on financial institutions. Asia Pac. J. Innov. Entrep. 2017, 11, 335–344. [Google Scholar] [CrossRef]

- Peck, M.E. Blockchain world-Do you need a blockchain? This chart will tell you if the technology can solve your problem. IEEE Spectr. 2017, 54, 38–60. [Google Scholar] [CrossRef]

- Feng, Q.; He, D.; Zeadally, S.; Khan, M.K.; Kumar, N. A survey on privacy protection in blockchain system. J. Netw. Comput. Appl. 2019, 126, 45–58. [Google Scholar] [CrossRef]

- Khan, A.; Hassan, M.K.; Paltrinieri, A.; Dreassi, A.; Bahoo, S. A bibliometric review of takaful literature. Int. Rev. Econ. Financ. 2020, 69, 389–405. [Google Scholar] [CrossRef]

- Liu, L.; Zhou, S.; Huang, H.; Zheng, Z. From Technology to Society: An Overview of Blockchain-Based DAO. IEEE Open J. Comput. Soc. 2021, 2, 204–215. [Google Scholar] [CrossRef]

- Coyne, J.G.; McMickle, P.L. Can blockchains serve an accounting purpose? J. Emerg. Technol. Account. 2017, 14, 101–111. [Google Scholar] [CrossRef]

- Yermack, D.; Fingerhut, A. Blockchain technology’s potential in the financial system. In Proceedings of the 2019 Financial Market’s Conference, Amelia Island, FL, USA, 20 May 2019. [Google Scholar]

- Hoang, L.C.; Hoang, M.H.; Quang, H.T.; Hoang, T.H. Blockchain technology applications in retail branding: Insights from retailers in the developing world. Thunderbird Int. Bus. Rev. 2023. [Google Scholar] [CrossRef]

- Tušek, B.; Ježovita, A.; Halar, P. Critical Auditors’ expertise for Blockchain-Based business environment. Zagreb Int. Rev. Econ. Bus. 2021, 24, 49–61. [Google Scholar] [CrossRef]

- Wang, Y.; Han, J.W.; Beynon-Davies, P. Understanding blockchain technology for future supply chains: A systematic literature review and research agenda. Supply Chain. Manag. 2019, 24, 62–84. [Google Scholar] [CrossRef]

- Li, X.; Jiang, P.; Chen, T.; Luo, X.; Wen, Q. A survey on the security of blockchain systems. Future Gener. Comput. Syst. 2020, 107, 841–853. [Google Scholar] [CrossRef]

- Desplebin, O.; Lux, G.; Petit, N. To be or not to be: Blockchain and the future of accounting and auditing. Account. Perspect. 2021, 20, 743–769. [Google Scholar] [CrossRef]

- Abreu, P.W.; Aparicio, M.; Costa, C.J. Blockchain technology in the auditing environment. In Proceedings of the 2018 13th Iberian Conference on Information Systems and Technologies (CISTI), Caceres, Spain, 13–16 June 2018. [Google Scholar]

- Parmoodeh, A.M.; Ndiweni, E.; Barghathi, Y. An exploratory study of the perceptions of auditors on the impact on Blockchain technology in the United Arab Emirates. Int. J. Audit. 2023, 27, 24–44. [Google Scholar] [CrossRef]

- Brender, N.; Gauthier, M.; Morin, J.-H.; Salihi, A. The Potential Impact of Blockchain Technology on Audit Practice; University of Hawaii at Manoa: Honolulu, HI, USA, 2018. [Google Scholar]

- Alshurafat, H.; Al-Mawali, H.; Al Shbail, M.O. The influence of technostress on the intention to use blockchain technology: The perspectives of Jordanian auditors. Dev. Learn. Organ. Int. J. 2023, 37, 24–27. [Google Scholar] [CrossRef]

- Maffei, M.; Casciello, R.; Meucci, F. Blockchain technology: Uninvestigated issues emerging from an integrated view within accounting and auditing practices. J. Organ. Change Manag. 2021, 34, 462–476. [Google Scholar] [CrossRef]

- Hashem, R.; Mubarak, A.-R.I.; Abu-Musa, A. The impact of blockchain technology on audit process quality: An empirical study on the banking sector. Int. J. Audit. Account. Stud. 2023, 5, 87–118. [Google Scholar]

- Guo, H.; Yu, X. A survey on blockchain technology and its security. Blockchain Res. Appl. 2022, 3, 100067. [Google Scholar] [CrossRef]

- White, B.S.; King, C.G.; Holladay, J. Blockchain security risk assessment and the auditor. J. Corp. Account. Financ. 2020, 31, 47–53. [Google Scholar] [CrossRef]

- Li, X.; Zheng, Z.; Dai, H.-N. When services computing meets blockchain: Challenges and opportunities. J. Parallel Distrib. Comput. 2021, 150, 1–14. [Google Scholar] [CrossRef]

- Lu, H.; Huang, K.; Azimi, M.; Guo, L. Blockchain technology in the oil and gas industry: A review of applications, opportunities, challenges, and risks. IEEE Access 2019, 7, 41426–41444. [Google Scholar] [CrossRef]

- Monrat, A.A.; Schelén, O.; Andersson, K. A survey of blockchain from the perspectives of applications, challenges, and opportunities. IEEE Access 2019, 7, 117134–117151. [Google Scholar] [CrossRef]

- Popchev, I.; Radeva, I.; Velichkova, V. The impact of blockchain on internal audit. In Proceedings of the 2021 Big Data, Knowledge and Control Systems Engineering (BdKCSE), Sofia, Bulgaria, 28–29 October 2021. [Google Scholar]

- AlSobeh AM, R. OSM: Leveraging model checking for observing dynamic behaviors in aspect-oriented applications. Online J. Commun. Media Technol. 2023, 13, e202355. [Google Scholar] [CrossRef]

- AlSobeh, A.M.; Magableh, A.A. BlockASP: A Framework for AOP-based Model Checking Blockchain System. IEEE Access 2023, 11, 115062–115075. [Google Scholar] [CrossRef]

- Cui, W.; Paglialunga, S.; Kalant, D.; Lu, H.; Roy, C.; Laplante, M.; Deshaies, Y.; Cianflone, K. Acylation-stimulating protein/C5L2-neutralizing antibodies alter triglyceride metabolism in vitro and in vivo. Am. J. Physiol.-Endocrinol. Metab. 2007, 293, E1482–E1491. [Google Scholar] [CrossRef]

- Roine, H. Service Quality of ASPs (Application Service Providers): Case of an E-accounting Service. Bachelor’s Thesis, LUT University, Lappeenranta, Finland, 2008. [Google Scholar]

- Roslender, R. Accounting for Strategic Positioning: Responding to the Crisis in Management Accounting 1. Br. J. Manag. 1995, 6, 45–57. [Google Scholar] [CrossRef]

- Owusu, M.; Kuffer, M.; Belgiu, M.; Grippa, T.; Lennert, M.; Georganos, S.; Vanhuysse, S. Towards user-driven earth observation-based slum mapping. Comput. Environ. Urban Syst. 2021, 89, 101681. [Google Scholar] [CrossRef]

- Minghini, M.; Frassinelli, F. OpenStreetMap history for intrinsic quality assessment: Is OSM up-to-date? Open Geospat. Data Softw. Stand. 2019, 4, 9. [Google Scholar] [CrossRef]

- Mosley, B.; De Imus, C.; Friend, D.; Boiani, N.; Thoma, B.; Park, L.S.; Cosman, D. Dual oncostatin M (OSM) receptors: Cloning and characterization of an alternative signaling subunit conferring OSM-specific receptor activation. J. Biol. Chem. 1996, 271, 32635–32643. [Google Scholar] [CrossRef]

- Vujičić, D.; Jagodic, D.; Ranđić, S. Blockchain technology, bitcoin, and Ethereum: A brief overview. In Proceedings of the 17th International Symposium Infoteh-Jahorina (INFOTEH), East Sarajevo, Bosnia and Herzegovina, 21–23 March 2018. [Google Scholar] [CrossRef]

- Miraz, M.H.; Ali, M. Applications of Blockchain Technology beyond Cryptocurrency. Ann. Emerg. Technol. Comput. 2018, 2, 1–6. [Google Scholar] [CrossRef]

- Albayati, H.; Kim, S.K.; Rho, J.J. Accepting financial transactions using blockchain technology and cryptocurrency: A customer perspective approach. Technol. Soc. 2020, 62, 101320. [Google Scholar] [CrossRef]

- Liu, F.; Fan, H.; Qi, J. Blockchain Technology, Cryptocurrency: Entropy-Based Perspective. Entropy 2022, 24, 557. [Google Scholar] [CrossRef] [PubMed]

- Astuti, I.N.; Rajab, S.; Setiyouji, D. Cryptocurrency Blockchain technology in the Digital revolution era. Aptisi Trans. Technopreneurship (ATT) 2022, 4, 9–16. [Google Scholar] [CrossRef]

- Eyal, I. Blockchain Technology: Transforming libertarian cryptocurrency dreams to finance and banking realities. IEEE Comput. 2017, 50, 38–49. [Google Scholar] [CrossRef]

- Babkin, A.V.; Burkaltseva, D.D.; Pshenichnikov, V.V.; Tyulin, A.S. Cryptocurrency and blockchain technology in digital economy: Development genesis, St. Petersburg State Polytechnical University Journal. π-Economics 2017, 10, 9–22. [Google Scholar] [CrossRef]

- Ghosh, A.; Gupta, S.; Dua, A.; Kumar, N. Security of Cryptocurrencies in blockchain technology: State-of-art, challenges and future prospects. J. Netw. Comput. Appl. 2020, 163, 102635. [Google Scholar] [CrossRef]

- Ghaemi Asl, M.; Rashidi, M.M.; Hosseini Ebrahim Abad, S.A. Emerging digital economy companies and leading cryptocurrencies: Insights from blockchain-based technology companies. J. Enterp. Inf. Manag. 2021, 34, 1506–1550. [Google Scholar] [CrossRef]

- Joo, M.H.; Nishikawa, Y.; Dandapani, K. Cryptocurrency, a successful application of blockchain technology. Manag. Financ. 2019, 46, 715–733. [Google Scholar] [CrossRef]

- Scott, B.; Loonam, J.; Kumar, V. Exploring the rise of blockchain technology: Towards distributed collaborative organizations. Strateg. Change 2017, 26, 423–428. [Google Scholar] [CrossRef]

- Kshetri, N. Blockchain-Based Financial Technologies and Cryptocurrencies for Low-Income People: Technical Potential versus Practical Reality. IEEE Comput. 2020, 53, 18–29. [Google Scholar] [CrossRef]

- Bogusz, C.I.; Laurell, C.; Sandström, C. Tracking the digital evolution of entrepreneurial finance: The interplay between crowdfunding, blockchain technologies, cryptocurrencies, and initial coin offerings. IEEE Trans. Eng. Manag. 2020, 67, 1099–1108. [Google Scholar] [CrossRef]

- Liu, J.; Liu, Z. A survey on Security Verification of blockchain smart contracts. IEEE Access 2019, 7, 77894–77904. [Google Scholar] [CrossRef]

- Sabri-Laghaie, K.; Ghoushchi, S.J.; Elhambakhsh, F.; Mardani, A. Monitoring blockchain cryptocurrency transactions to improve the trustworthiness of the Fourth Industrial Revolution (Industry 4.0). Algorithms 2020, 13, 312. [Google Scholar] [CrossRef]

- Baker, H.K.; Pandey, N.; Kumar, S.; Haldar, A. A bibliometric analysis of board diversity: Current status, development, and future research directions. J. Bus. Res. 2020, 108, 232–246. [Google Scholar] [CrossRef]

- Baker, H.K.; Kumar, S.; Pandey, N. A bibliometric analysis of managerial finance: A retrospective. Manag. Financ. 2020, 46, 1495–1517. [Google Scholar] [CrossRef]

- Lardo, A.; Corsi, K.; Varma, A.; Mancini, D. Exploring blockchain in the accounting domain: A bibliometric analysis. Account. Audit. Account. 2022, 35, 204–233. [Google Scholar] [CrossRef]

- Van Eck, N.J.; Waltman, L. Software survey: VOSviewer, a computer program for bibliometric mapping. Scientometrics 2009, 84, 523–538. [Google Scholar] [CrossRef] [PubMed]

- Rumpenhorst, F.; Industry 4.0 Building Your Digital Enterprise April 2016. PWC. 2016. Available online: https://www.pwc.com/gx/en/industries/industries-4.0/landing-page/industry-4.0-building-your-digital-enterprise-april-2016.pdf (accessed on 17 October 2023).

- Tiberius, V.; Hirth, S. Impacts of digitization on auditing: A Delphi study for Germany. J. Int. Account. Audit. Tax. 2019, 37, 100288. [Google Scholar] [CrossRef]

- Tan, B.S.; Low, K.Y. Blockchain as the database engine in the accounting system. Aust. Account. Rev. 2019, 29, 312–318. [Google Scholar] [CrossRef]

- Marques, M.; Pinho, C.; Montenegro, T.M. The effect of international income shifting on the link between real investment and corporate taxation. J. Int. Account. Audit. Account. 2019, 36, 100268. [Google Scholar] [CrossRef]

- McCallig, J.; Robb, A.; Rohde, F. Establishing the representational faithfulness of financial accounting information using multiparty security, network analysis and a blockchain. Int. J. Account. Inf. Syst. 2019, 33, 47–58. [Google Scholar] [CrossRef]

- Albitar, K.; Gerged, A.M.; Kikhia, H.; Hussainey, K. Auditing in times of social distancing: The effect of COVID-19 on auditing quality. Int. J. Account. Inf. Manag. 2020, 29, 169–178. [Google Scholar] [CrossRef]

- Morozova, T.; Akhmadeev, R.; Lehoux, L.; Yumashev, A.V.; Meshkova, G.V.; Lukiyanova, M. Crypto asset assessment models in financial reporting content typologies. Entrep. Sustain. Issues 2020, 7, 2196. [Google Scholar] [CrossRef]

- Moll, J.; Yigitbasioglu, O. The role of internet-related technologies in shaping the work of accountants: New directions for accounting research. Br. Account. Rev. 2019, 51, 100833. [Google Scholar] [CrossRef]

- Pascual Pedreño, E.; Gelashvili, V.; Pascual Nebreda, L. Blockchain and its application to accounting. Intang. Cap. 2021, 17, 1–16. [Google Scholar] [CrossRef]

- Appelbaum, D.; Nehmer, R.A. Auditing cloud-based blockchain accounting systems. J. Inf. Syst. 2020, 34, 5–21. [Google Scholar] [CrossRef]

- Ferri, L.; Spanò, R.; Ginesti, G.; Theodosopoulos, G. Ascertaining auditors’ intentions to use blockchain technology: Evidence from the Big 4 accountancy firms in Italy. Meditari Account. Res. 2020, 29, 1063–1087. [Google Scholar] [CrossRef]

- Fuller, S.H.; Markelevich, A. Should accountants care about blockchain? J. Corp. Account. Financ. 2020, 31, 34–46. [Google Scholar] [CrossRef]

- Kend, M.; Nguyen, L.A. Big data analytics and other emerging technologies: The impact on the Australian audit and assurance profession. Aust. Account. Rev. 2020, 30, 269–282. [Google Scholar] [CrossRef]

- Qasim, A.; Kharbat, F.F. Blockchain technology, business data analytics, and artificial intelligence: Use in the accounting profession and ideas for inclusion into the accounting curriculum. J. Emerg. Technol. Account. 2020, 17, 107–117. [Google Scholar] [CrossRef]

- Rozario, A.M.; Thomas, C. Reengineering the audit with blockchain and smart contracts. J. Emerg. Technol. Account. 2019, 16, 21–35. [Google Scholar] [CrossRef]

- Sheldon, M.D. Using blockchain to aggregate and share misconduct issues across the accounting profession. Curr. Issues Audit. 2018, 12, A27–A35. [Google Scholar] [CrossRef]

- Vincent, N.E.; Skjellum, A.; Medury, S. Blockchain architecture: A design that helps CPA firms leverage the technology. Int. J. Account. Inf. Syst. 2020, 38, 100466. [Google Scholar] [CrossRef]

- Kozlowski, S. An audit ecosystem to support blockchain-based accounting and assurance. In Continuous Auditing; Emerald Publishing Limited: Bingley, UK, 2018. [Google Scholar]

- Mosteanu, N.R.; Faccia, A.; Ansari, A.; Shamout, M.D.; Capitanio, F. Sustainability integration in supply chain management through systematic literature review. Qual. -Access Success 2020, 21, 117–123. [Google Scholar]

- Fullana, O.; Ruíz, J. Accounting information systems in the blockchain era. Int. J. Intellect. Prop. Manag. 2021, 11, 63. [Google Scholar] [CrossRef]

- O’Leary, D.E. Configuring blockchain architectures for transaction information in blockchain consortiums: The case of accounting and supply chain systems. Intell. Syst. Account. Financ. Manag. 2017, 24, 138–147. [Google Scholar] [CrossRef]

- Yermack, D. Corporate governance and blockchains. Rev. Financ. 2017, 21, 7–31. [Google Scholar] [CrossRef]

- Cai, Y.J.; Choi, T.M.; Zhang, J. Platform supported supply chain operations in the blockchain era: Supply contracting and moral hazards. Decis. Sci. 2021, 52, 866–892. [Google Scholar] [CrossRef]

- Carlin, T. Blockchain and the journey beyond double entry. Aust. Account. Rev. 2019, 29, 305–311. [Google Scholar] [CrossRef]

- Al-Zaqeba MA, A.; Jarah BA, F.; Ineizeh, N.I.; Almatarneh, Z.; Jarrah, M.A.A. The effect of management accounting and blockchain technology characteristics on supply chains efficiency. Uncertain Supply Chain. Manag. 2022, 10, 973–982. [Google Scholar] [CrossRef]

- Cai, W.; Wang, Z.; Ernst, J.B.; Hong, Z.; Feng, C.; Leung, V.C. Decentralized applications: The blockchain-empowered software system. IEEE Access 2018, 6, 53019–53033. [Google Scholar] [CrossRef]

- Kitsantas, T.; Chytis, E. Blockchain technology as an ecosystem: Trends and perspectives in accounting and management. J. Theor. Appl. Electron. Commer. Res. 2020, 17, 1143–1161. [Google Scholar] [CrossRef]

- Chan, S.; Chu, J.; Zhang, Y.; Nadarajah, S. Blockchain and cryptocurrencies. J. Risk Financ. Manag. 2020, 13, 227. [Google Scholar] [CrossRef]

- Dai, J.; He, N.; Yu, H. Utilizing blockchain and smart contracts to enable audit 4.0: From the perspective of accountability audit of air pollution control in China. J. Emerg. Technol. Account. 2019, 16, 23–41. [Google Scholar] [CrossRef]

- KPMG Audit Technology Evoluti on Content Series: Blockchai n Blockchain-What Does It Mean for the Audit? (n.d.). Available online: https://assets.kpmg/content/dam/kpmg/za/pdf/2021/blockchain-what-does-it%20mean-for-the-audit.pdf (accessed on 17 October 2023).

- pwc. In Depth a Look at Current Financial Reporting Issues Cryptographic Assets and Related Transactions: Accounting Considerations under IFRS at a Glance. 2019. Available online: https://www.pwc.com/gx/en/audit-services/ifrs/publications/ifrs-16/cryptographic-assets-related-transactions-accounting-considerations-ifrs-pwc-in-depth.pdf (accessed on 17 October 2023).

- How Blockchain Could Introduce Real-Time Auditing. (n.d.). Available online: https://www.ey.com/en_my/assurance/how-blockchain-could-introduce-real-time-auditing (accessed on 16 November 2023).

- Farahani, B.; Firouzi, F.; Luecking, M. The convergence of IoT and distributed ledger technologies (DLT): Opportunities, challenges, and solutions. J. Netw. Comput. Appl. 2021, 177, 102936. [Google Scholar] [CrossRef]

- Roszkowska, P. Fintech in financial reporting and audit for fraud prevention and safeguarding equity investments. J. Account. Organ. Change 2020, 17, 164–196. [Google Scholar] [CrossRef]

- Hsieh, S.; Brennan, G. Issues, risks, and challenges for auditing crypto asset transactions. Int. J. Account. Inf. Syst. 2022, 46, 100569. [Google Scholar] [CrossRef]

- Tiron-Tudor, A.; Deliu, D. Reflections on the human-algorithm complex duality perspectives in the auditing process. Qual. Res. Account. Manag. 2022, 19, 255–285. [Google Scholar]

- Sheldon, M.D. Auditing the blockchain oracle problem. J. Inf. Syst. 2021, 35, 121–133. [Google Scholar] [CrossRef]

- Gauthier, M.P.; Brender, N. How do the current auditing standards fit the emergent use of blockchain? Manag. Audit. J. 2021, 293, E1482–E1491. [Google Scholar] [CrossRef]

- Ram, A.; Maroun, W.; Garnett, R. Accounting for the Bitcoin: Accountability, neoliberalism and a correspondence analysis. Meditari Account. Res. 2016, 24, 2–35. [Google Scholar] [CrossRef]

- IFRS. IFRS Accounting Standards Navigator. (n.d.). Available online: https://www.ifrs.org/issued-standards/list-of-standards/ (accessed on 17 October 2023).

- TeamMate. (2 December 2022). Internal Audit Introductory Guide to Cryptocurrency and Blockchain Auditing. Wolters Kluwer. Available online: https://www.wolterskluwer.com/en/expert-insights/internal-audit-introductory-guide-to-cryptocurrency-and-blockchain (accessed on 17 October 2023).

- Tapscott, D.; Tapscott, A. Blockchain revolution: How the technology behind bitcoin is changing money, business, and the world. Qual. Manag. J. 2016, 25, 64–65. [Google Scholar]

- Ashfaq, T.; Khalid, R.; Yahaya, A.S.; Aslam, S.; Azar, A.T.; Alsafari, S.; Hameed, I.A. A Machine Learning and Blockchain Based Efficient Fraud Detection Mechanism. Sensors 2022, 22, 7162. [Google Scholar] [CrossRef]

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Description | Results |

|---|---|

| Documents | 67 |

| Sources | 32 |

| KeyWords Plus (ID) | 121 |

| Author’s keywords (DE) | 211 |

| period | 2016–2022 |

| Average citations per document | 12.72 |

| Authors | 170 |

| Author appearances | 183 |

| Authors of single-authored documents | 5 |

| Authors of multi-authored documents | 165 |

| Single-authored documents | 5 |

| Documents per author | 0.382 |

| Authors per document | 2.62 |

| Co-Authors per documents | 2.82 |

| Collaboration index | 2.75 |

| Authors | Document | Publication Year | Source | Total Citations | TC per Year |

|---|---|---|---|---|---|

| Jun Dai and Miklos A. Vasarhelyi [14] | “Toward Blockchain-Based Accounting and Assurance” | 2017 | Journal of Information Systems | 205 | 34.167 |

| Tiankai Wang, Yangmei Wang and Alexander McLead [34] | “Do health information technology investments impact hospital financial performance and productivity?” | 2018 | International Journal of Accounting Information Systems | 78 | 15.6 |

| Joshua G. Coyne and Peter L. McMickle [49] | “Can blockchains serve an accounting purpose?” | 2017 | Journal of Emerging Technologies in Accounting | 68 | 11.333 |

| Victor Tiberius and Stefanie Hirth [96] | “Impacts of digitization on auditing: A Delphi study for Germany” | 2019 | Journal of International Accounting, Auditing and Taxation | 43 | 10.75 |

| Manlu Liu, Kean Wu, Jennifer Jie Xu [22] | “How will blockchain technology impact auditing and accounting: Permissionless versus permissioned blockchain” | 2019 | Current issues in auditing | 36 | 9 |

| Boon Seng Tan and Kin Yew Low [97] | “Blockchain as the Database Engine in the Accounting System” | 2019 | Australian Accounting Review | 29 | 7.25 |

| Mário Marques, Carlos Pinho, and Tânia Menezes Montenegro [98] | “Reengineering the audit with blockchain and smart contracts” | 2019 | Journal of emerging technologies in Accounting | 27 | 6.75 |

| John McCallig, Alastair Robb, and Fiona Rohde [99] | “Establishing the representational faithfulness of financial accounting information using multiparty security, network analysis, and a blockchain” | 2019 | International Journal of Accounting Information Systems | 26 | 6.5 |

| Khaldoon Albitar, Ali Meftah Gerged, Hassan Kikhia, and Khaled Hussainey [100] | “Auditing in times of social distancing: the effect of COVID-19 on Auditing quality” | 2021 | International Journal of Accounting & Information Management | 24 | 12 |

| Tatiana Morozova, Ravil Akhmadeev, Liubov Lehoux, Alexei Yumashev, Galina Meshkova, and Marina Lukiyanova [101] | “Crypto asset assessment models in financial reporting content typologies” | 2020 | Entrepreneurship and Sustainability Issues | 23 | 7.667 |

| Author | h-Index | Citations | Affiliation |

|---|---|---|---|

| Miklos A. Vasarhelyi | 60 | 14,764 | Rutgers University |

| Jun Dai | 10 | 1696 | Michigan Technology University |

| Kin-Yew Low | 10 | 1229 | Nanyang Technological University |

| Boon-Seng Tan | 7 | 437 | Nanyang Technological University |

| Mark Sheldon | 8 | 278 | John Carroll University |

| Emilio Boulianne | 11 | 808 | Concordia University |

| Erica Pimentel | 4 | 145 | Queen’s University |

| Alexander Kogan | 41 | 7552 | Rutgers Business School |

| Sources | Citations | ABDC Ranking | ABS Ranking | SJR | Publisher |

|---|---|---|---|---|---|

| Journal of Emerging Technology in Accounting | 127 | B | 1 | Q2 | American Accounting Association, Lakewood Ranch, FL, USA |

| Accounting Organization and Society | 82 | A * | 4 * | Q1 | Elsevier, Amsterdam, The Netherlands, |

| Journal of Information System | 80 | A | 1 | Q1 | American Accounting Association, Lakewood Ranch, FL, USA |

| Accounting Auditing and Accountability Journal | 48 | A * | 3 | Q1 | Emerald Group Publishing Ltd., Bradford, UK |

| Australian Accounting Review | 47 | B | 2 | Q2 | Wiley-Blackwell Publishing Ltd., Hoboken, NJ, USA |

| Accounting Horizon | 45 | A | 3 | Q1 | American Accounting Association, Lakewood Ranch, FL, USA |

| Journal of Corporate Accounting and Finance | 42 | B | - | Q2 | Wiley-Blackwell, Hoboken, NJ, USA |

| MIS Quarterly | 32 | A * | 4 * | Q1 | Management Information Systems Research Center, Minneapolis, MN, USA |

| Current Issues in Auditing | 31 | B | 2 | Q2 | American Accounting Association, Lakewood Ranch, FL, USA |

| Meditari Accountancy Research | 27 | A | 1 | Q1 | Emerald Group Publishing Ltd., Bradford, UK |

| Critical Perspectives in Accounting | 26 | A | 3 | Q1 | Academic Press Inc., Cambridge, MA, USA |

| Accounting Review | 25 | A * | 4 * | Q1 | American Accounting Association, Lakewood Ranch, FL, USA |

| AUDITING: A Journal of Practice & Theory | 25 | A * | 3 | Q1 | Emerald Group Publishing Ltd., Bradford, UK |

| International Journal of Information Management | 25 | A * | 2 | Q1 | Elsevier Ltd., Amsterdam, The Netherlands |

| Technological Forecasting and Social Change | 25 | A | 3 | Q1 | Elsevier Ltd., Amsterdam, The Netherlands |

| Region | Number of Publications | Total Citation | Region | Number of Publications | Total Citation |

|---|---|---|---|---|---|

| United States of America | 61 | 512 | Czech Republic | 4 | 2 |

| Canada | 20 | 31 | Jordan | 4 | 3 |

| Australia | 16 | 19 | New Zealand | 4 | 0 |

| Romania | 16 | 9 | Germany | 3 | 43 |

| Italy | 15 | 37 | Malaysia | 3 | 0 |

| United Kingdom | 13 | 35 | South Africa | 3 | 16 |

| Ukraine | 11 | 2 | Croatia | 2 | 0 |

| China | 9 | 15 | Ireland | 2 | 26 |

| India | 6 | 0 | Poland | 2 | 0 |

| Russia | 5 | 23 | Singapore | 2 | 21 |

| Domain | Potential Future Research |

|---|---|

| Governance and regulatory obstacles | The utilization of blockchain technology in a decentralized setting poses governance and regulatory obstacles that require careful consideration. Future research could examine the existing governance structures and propose governance frameworks and regulatory guidelines that are tailored to the application of blockchain technology in the fields of accounting and auditing. Through a comparative analysis, the study could evaluate existing governance structures to ascertain their alignment with the decentralized nature of blockchain. The study could also investigate stakeholder perspectives, including regulators, industry professionals, and users, through surveys and interviews. This approach ensures a comprehensive understanding of the challenges and expectations related to regulatory compliance, providing valuable insights for the successful implementation of blockchain in the accounting and auditing domains. |

| Constant technical development | As blockchain technology continues to improve, future studies should concentrate on examining new developments and advances in the area. Potential research questions are (1) how can blockchain technology be integrated with emerging technologies like AI, IoT, or quantum computing to enhance accounting and auditing practices? (2) What are the potential synergies and challenges in the simultaneous development of blockchain technology alongside other disruptive technologies? (3) How can the continuous evolution of blockchain impact the scalability and security of accounting and auditing processes? A multi- disciplinary study exploring the integration of blockchain with AI, IoT, or quantum computing in accounting might provide insightful information about possible future opportunities and challenges. |

| Impact of blockchain on financial reporting | Potential research questions are (1) what are the specific technological aspects of blockchain that can enhance the reliability of financial reporting? (2) How can blockchain improve transparency in financial reporting, and what challenges may arise in the implementation process? Further research could examine the advantages and challenges of utilizing blockchain technology in financial reporting, considering technological, operational, and regulatory aspects, investigate the technological features of blockchain that contribute to the reliability of financial reporting, and assess the impact of blockchain on transparency in financial reporting. The research should aim to establish rules and best practices for leveraging blockchain to enhance the reliability, transparency, and efficiency of financial reporting procedures. |

| Blockchain-based triple- entry bookkeeping | The potential research questions are (1) how does the integration of a decentralized blockchain ledger impact the verification process in triple-entry bookkeeping? (2) What challenges may arise in reconciling traditional double-entry bookkeeping with blockchain-based triple-entry systems? (3) In what ways can triple-entry bookkeeping enhance the reliability and transparency of financial transactions? Future research could investigate the implications and challenges of integrating a decentralized and immutable blockchain ledger as a supplementary element to the traditional double-entry bookkeeping system. Additionally, research could evaluate the performance of triple-entry bookkeeping in terms of reliability and transparency. |

| Domain | Potential Future Research |

|---|---|

| Regulatory and legal considerations | Potential research questions are (1) how do existing legal frameworks align with blockchain technology in auditing, especially considering compliance, data protection, and privacy laws? (2) What are the challenges and opportunities in using blockchain-based evidence for regulatory compliance in auditing? Future research could engage with stakeholders, including regulators, and conduct an in-depth analysis of existing legal frameworks to identify gaps and areas of alignment with blockchain in auditing. This includes focusing on compliance, data protection, audit regulations, privacy laws, confidentiality, and the use of blockchain-based evidence for regulatory compliance. Addressing these challenges will help navigate the legal and regulatory considerations of blockchain auditing. |

| Integration with existing audit practices | Potential research questions are (1) what are the key areas of synergy between blockchain technology and traditional audit practices? (2) How can practical guidelines be developed to facilitate the seamless integration of blockchain into existing audit processes? Using the case study methodology, future research could analyze successful integrations of blockchain technology with traditional audit practices and ultimately determine areas of synergy that could improve the effectiveness and efficiency of audits and identify practical guidelines and recommendations. |

| Data reliability and accuracy | Research question: What methods can be developed to enhance data integrity verification and fraud detection in blockchain-based auditing? To fully utilize blockchain technology in auditing, future research could collaborate with technologists to develop tools or algorithms for identifying deceptive practices or erroneous data on the blockchain. Research could also focus on identifying challenges, validating and ensuring the accuracy of data stored on the blockchain. A case methodology could be utilized to identify and rectify deceptive practices or erroneous data, ensuring data integrity verification and fraud detection to uphold audit integrity and trust. |

| Risk assessment and control considerations | Potential research questions: (1) What are the specific risks associated with auditing blockchain-based systems, and how can they be categorized and assessed? (2) How do blockchain-based systems impact internal controls, audit trails, and access management in auditing processes? (3) What frameworks can be developed to enhance internal controls, transparency, data integrity, fraud prevention, and access management in auditing blockchain-based systems? Future research could investigate and categorize risks associated with auditing blockchain-based systems and develop risk assessment frameworks tailored to the unique features of blockchain, investigate the impact of blockchain application on internal controls, audit trails, and access management in auditing processes, and develop guidelines for adapting and enhancing these elements to address new challenges. This could be achieved by collaborating with auditors, technology providers, and regulators to develop comprehensive frameworks for internal controls, transparency, data integrity, fraud prevention, and access management in blockchain-based auditing. |

| Blockchain-based audit evidence | Potential Research Questions: (1) How reliable is audit evidence derived from blockchain technology, to what extent is the audit evidence adequate in meeting the requirements of a thorough audit process, and what factors contribute to its reliability or lack thereof? (2) What frameworks can be developed to systematically assess the reliability and adequacy of audit evidence generated from blockchain transactions? (3) What challenges do auditors face in interpreting blockchain-based audit evidence, and how can these challenges be addressed to ensure accurate conclusions? Future research could analyze real-world cases to identify patterns and factors influencing reliability. Researchers could also collaborate with auditors, industry, and blockchain experts to design comprehensive frameworks for systematically assessing the reliability and adequacy of blockchain-based audit evidence. Additionally, survey-based research could be conducted with auditors to understand the challenges they face in interpreting blockchain-based audit evidence and identify areas of improvement. |

| Domain | Potential Future Research |

|---|---|

| Regulatory Frameworks | Potential research questions: (1) How effective are current valuation methods in accurately determining the fair value of cryptocurrencies, and what are their limitations in capturing the volatile nature of these assets? (2) What variations exist in cryptocurrency reporting practices across different jurisdictions, and how can a comparative analysis identify opportunities for harmonization? (3) How can the alignment between international and national standards in cryptocurrency reporting enhance compliance and simplify the reporting and auditing processes for entities dealing with cryptocurrencies? Future research could evaluate the effectiveness and limitations of current valuation methods for cryptocurrencies and investigate the alignment between international accounting standards (IFRS) and national frameworks for cryptocurrency reporting. A comparative analysis across jurisdictions can identify opportunities for harmonization, ensuring compliance and simplifying cryptocurrency reporting and auditing processes. |

| Auditing and Assurance | Potential Research Questions: (1) To what extent are the existing auditing frameworks, standards, and processes tailored to cryptocurrencies relevant, and what are the primary challenges associated with their application in the dynamic cryptocurrency landscape? (2) How effective are the internal controls, security measures, exchange platform reliability assessments, the sufficiency of cryptographic keys and wallets, and testing methodologies for blockchain transaction integrity in ensuring accurate financial reporting, risk mitigation, and stakeholder confidence in the cryptocurrency ecosystem? Future research could conduct a comprehensive analysis of existing cryptocurrency auditing frameworks, standards, and processes specific to cryptocurrencies and identify their relevance and challenges. A case study could be undertaken to assess the effectiveness, challenges faced by auditors, and emerging best practices of key auditing components specific to cryptocurrencies, such as internal controls, security measures, exchange platform reliability assessments, and cryptographic key and wallet sufficiency. Research could also evaluate their adaptability to the rapidly evolving nature of the cryptocurrency landscape, identifying gaps and areas for improvement. |

| Taxation Implications | Potential Research Questions: (1) What are the optimal tax treatments and regulations for the taxation of cryptocurrencies, taking into consideration the volatile nature of these assets and their implications for individual and business tax liabilities? (2) What are the primary challenges associated with ensuring tax compliance in the context of cryptocurrencies, and what innovative solutions can be proposed to address these challenges and promote fair and transparent taxation? Future research could concentrate on developing clear and comprehensive tax regulations for cryptocurrencies. This includes addressing challenges related to gains and losses treatment, tax reporting requirements, and ensuring tax compliance. This will enable individuals and businesses to fulfill their tax obligations accurately and promote fairness and transparency in the taxation of cryptocurrencies. |

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2023 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Sheela, S.; Alsmady, A.A.; Tanaraj, K.; Izani, I. Navigating the Future: Blockchain’s Impact on Accounting and Auditing Practices. Sustainability 2023, 15, 16887. https://doi.org/10.3390/su152416887

Sheela S, Alsmady AA, Tanaraj K, Izani I. Navigating the Future: Blockchain’s Impact on Accounting and Auditing Practices. Sustainability. 2023; 15(24):16887. https://doi.org/10.3390/su152416887

Chicago/Turabian StyleSheela, Sundarasen, Ahnaf Ali Alsmady, K. Tanaraj, and Ibrahim Izani. 2023. "Navigating the Future: Blockchain’s Impact on Accounting and Auditing Practices" Sustainability 15, no. 24: 16887. https://doi.org/10.3390/su152416887

APA StyleSheela, S., Alsmady, A. A., Tanaraj, K., & Izani, I. (2023). Navigating the Future: Blockchain’s Impact on Accounting and Auditing Practices. Sustainability, 15(24), 16887. https://doi.org/10.3390/su152416887