Social and Environmental Responsibility Manager on the Example of Companies from Poland and Germany

,

,  ,

,

Abstract

:1. Introduction

2. Materials and Methods

2.1. Review of the Literature

2.2. The Role of the Manager in Creating a Sustainable and Socially Responsible Business: The Perspective of Poland and Germany

2.3. The Importance of the Manager’s Role in CSR Strategies in Poland and Germany

2.4. Conflict between Short-Term Financial Goals and Long-Term CSR Goals

2.5. Balancing the Interests of Various Stakeholders

3. Examples of CSR Activities

Benefits of Integrating CSR with Business Practices Based on Poland and Germany

4. Results

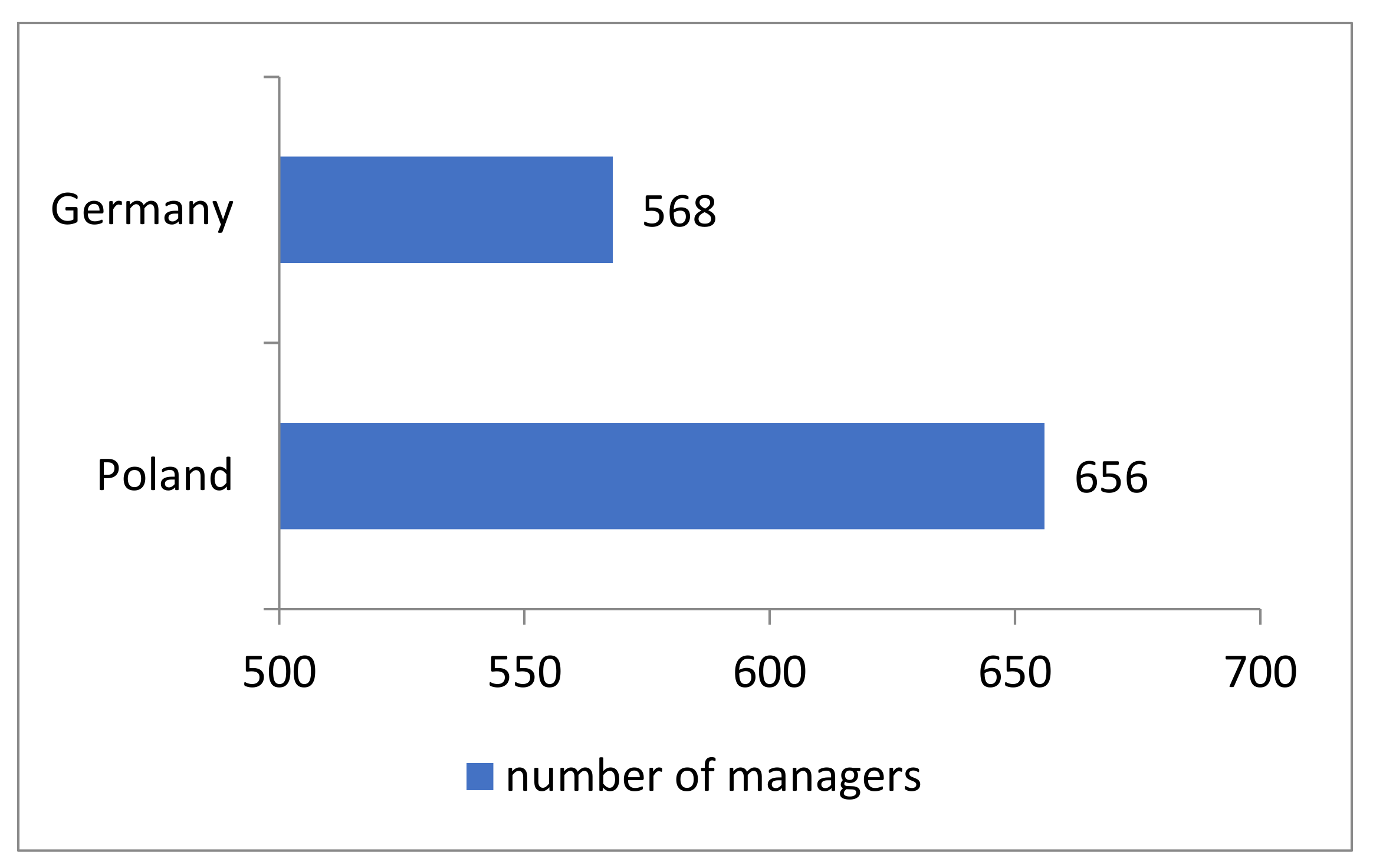

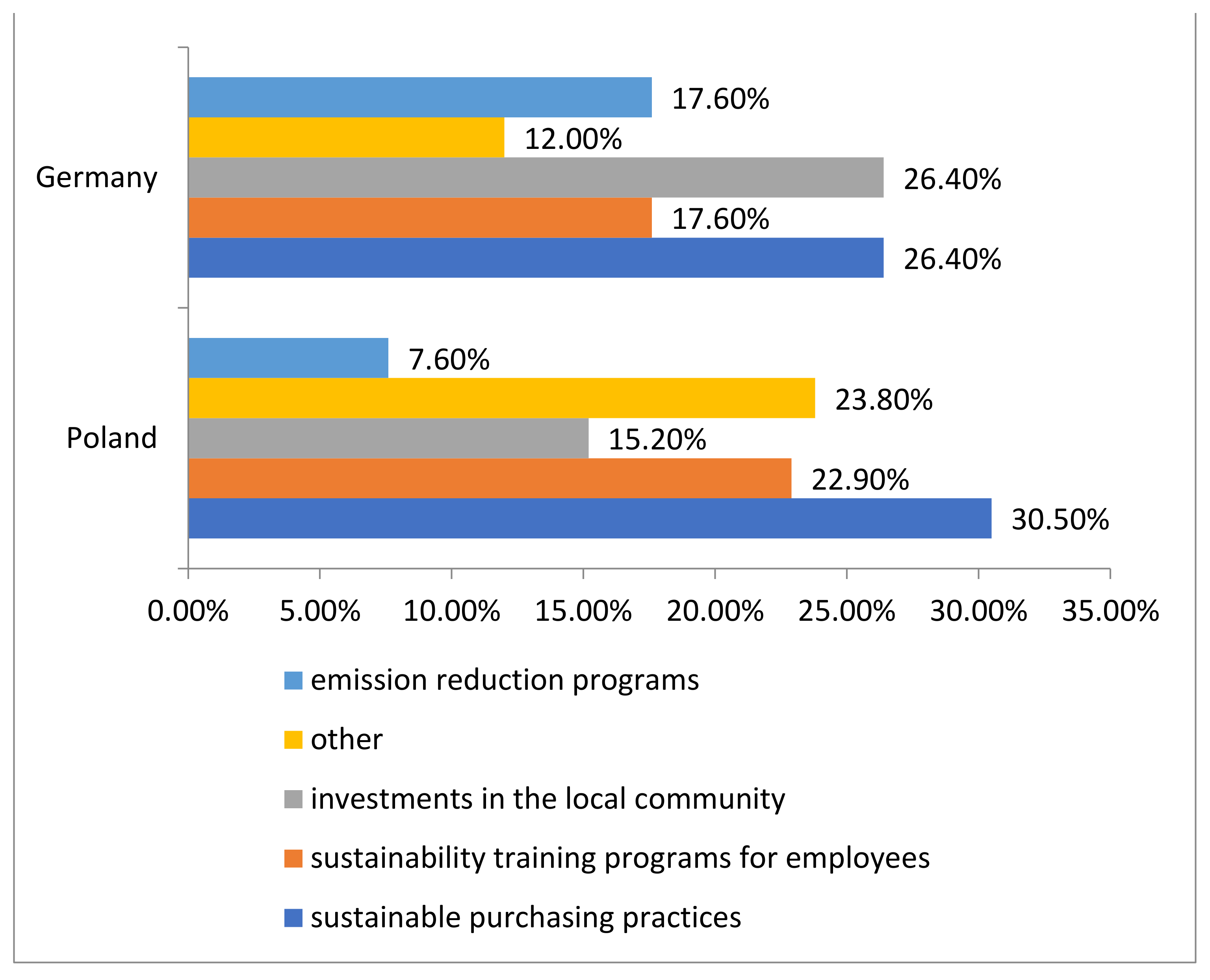

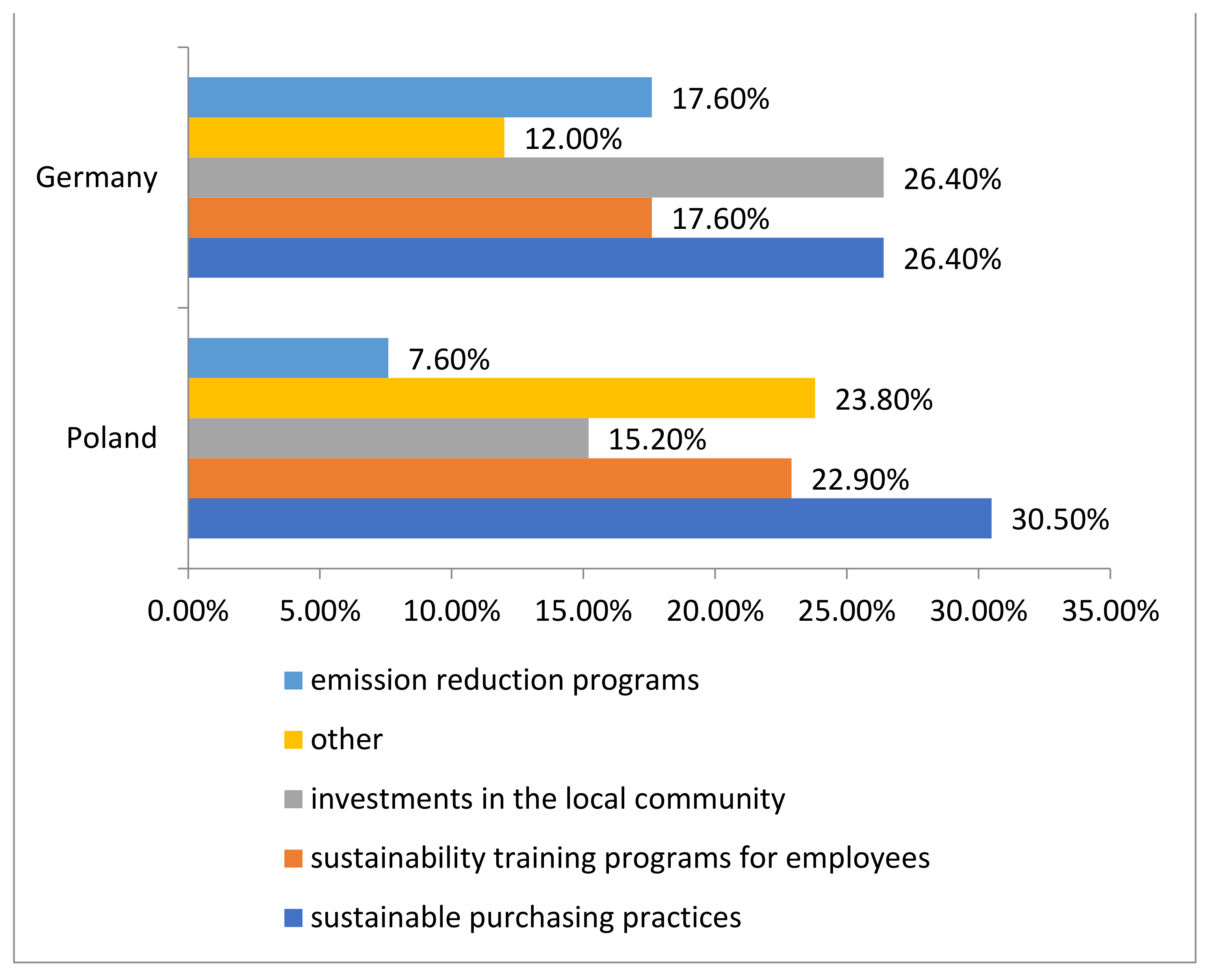

- A total of 30.5% (200 out of 656) of companies have adopted sustainable purchasing practices that take into account environmental, social and ethical aspects.

- A total of 22.9% (150 out of 656) of companies organized training programs for employees on sustainability.

- A total of 15.2% (100 out of 656) of companies invested in the local community.

- A total of 7.6% (50 out of 656) of companies have undertaken emission reduction programs.

- A total of 23.8% (156 out of 656) of companies took other CSR activities.

- A total of 26.4% (150 out of 568) of companies have adopted sustainable purchasing practices.

- A total of 17.6% (100 out of 568) of companies organized training programs for employees on sustainability.

- A total of 26.4% (150 out of 568) of companies invested in the local community.

- A total of 17.6% (100 out of 568) of companies have undertaken emission reduction programs.

- A total of 12% (68 out of 568) of companies have undertaken other CSR activities.

5. Discussion

6. Conclusions

6.1. The Importance of the Manager’s Role in CSR Strategies

6.2. Social and Environmental Responsibility of Companies from Poland and Germany

6.3. CSR as an Integral Component of Business Practices—Comparison between Germany and Poland

- German enterprises show a higher tendency to invest locally and focus on emission reduction than their Polish counterparts, suggesting a deeper commitment to certain social and environmental facets of business.

- Polish businesses frequently engage in diverse CSR activities not categorized in the survey, pointing to potentially greater flexibility or innovation in their CSR approach.

- Both nations display a clear commitment to CSR, but the varied nature of their initiatives could be influenced by cultural, regulatory or social distinctions.

- The data underscore the necessity of bolstering CSR practices and awareness in both countries. Key focal areas could include employee education on sustainability, local community investments and emissions reductions.

- The disparities and commonalities in CSR strategies highlight the need for companies to tailor their CSR approaches to their specific contexts and business objectives.

- While the provided data offer a snapshot of CSR in both countries, a broader study across diverse sectors and business sizes would provide a more comprehensive view.

- CSR is fluid and ever-evolving. Companies need to perpetually assess and recalibrate their CSR strategies in response to changing societal expectations and best practices.

- Managers play a pivotal role in both nations in fostering and enacting CSR practices, emphasizing the necessity of leadership in achieving meaningful CSR outcomes.

- The variance in CSR strategy adoption between Poland and Germany could be an intriguing avenue for further exploration, potentially revealing insights about cultural or regulatory influences.

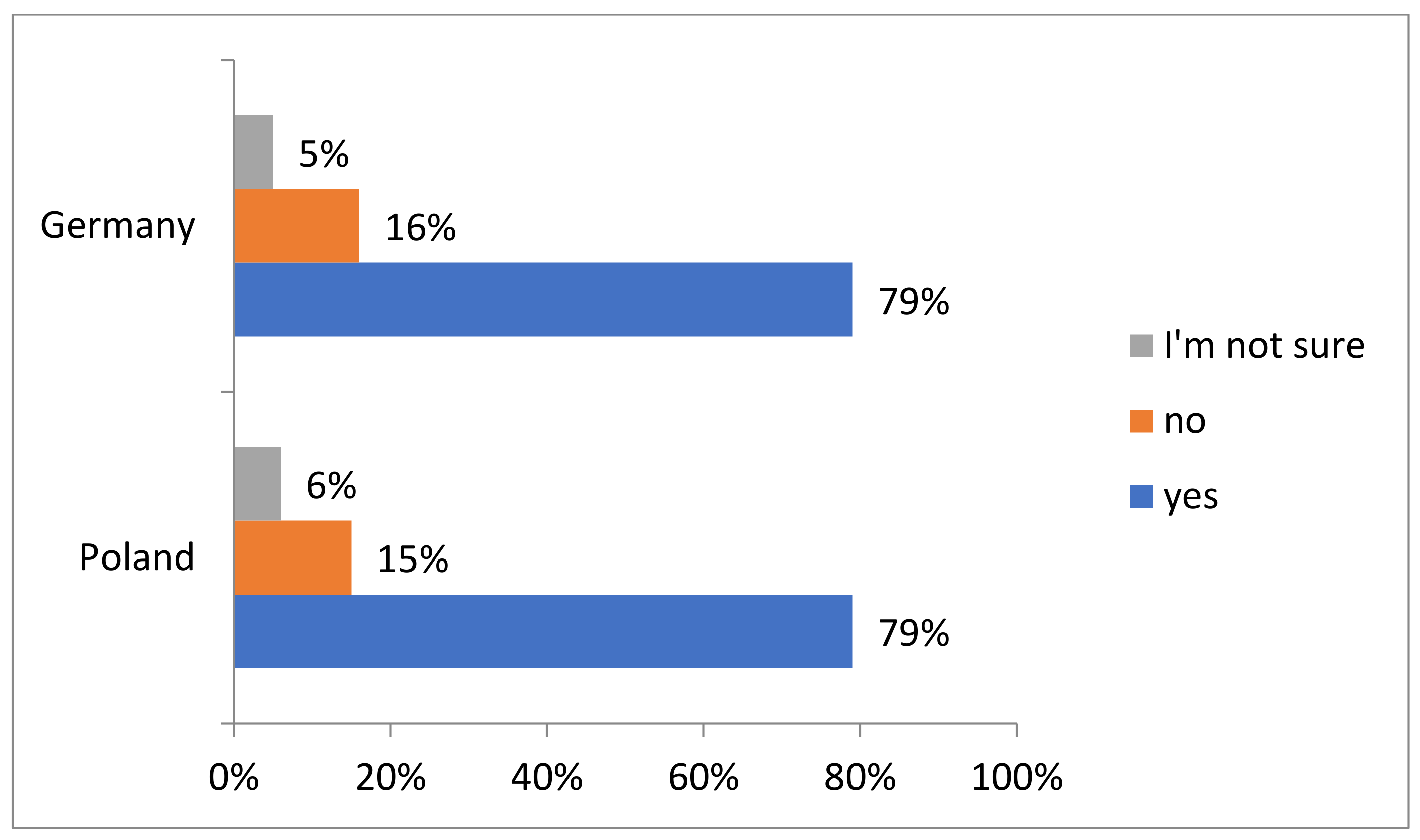

- While a majority of businesses in both nations have incorporated CSR into their core operations, there is still room for more integration and awareness on its significance.

- Education about CSR is prominent in both countries, but modes of imparting this knowledge differ, pointing to varying approaches or resource availability.

- The data suggest that managers’ involvement in CSR is beneficial, but the degree of benefit might vary based on several factors, including the company culture or operational sector.

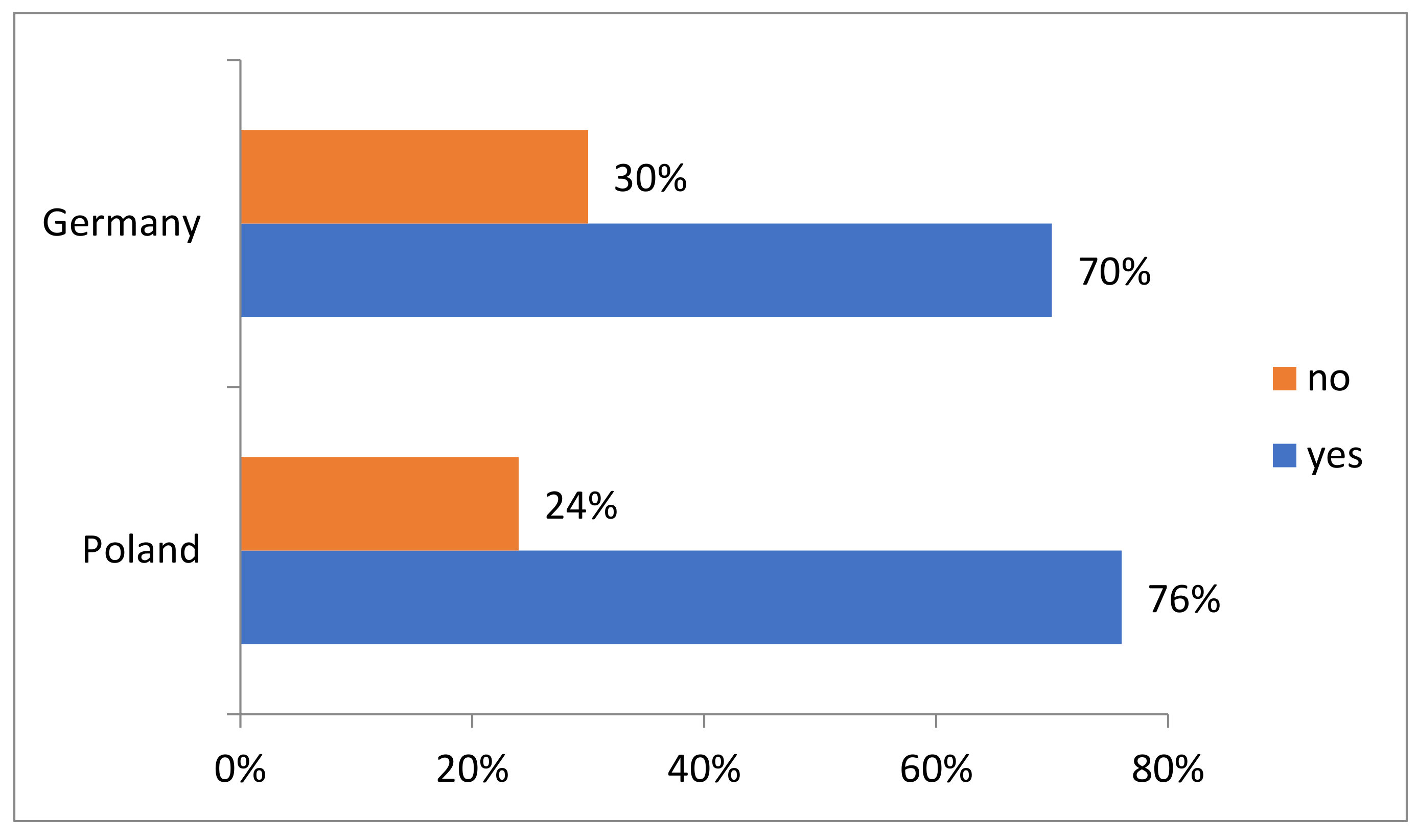

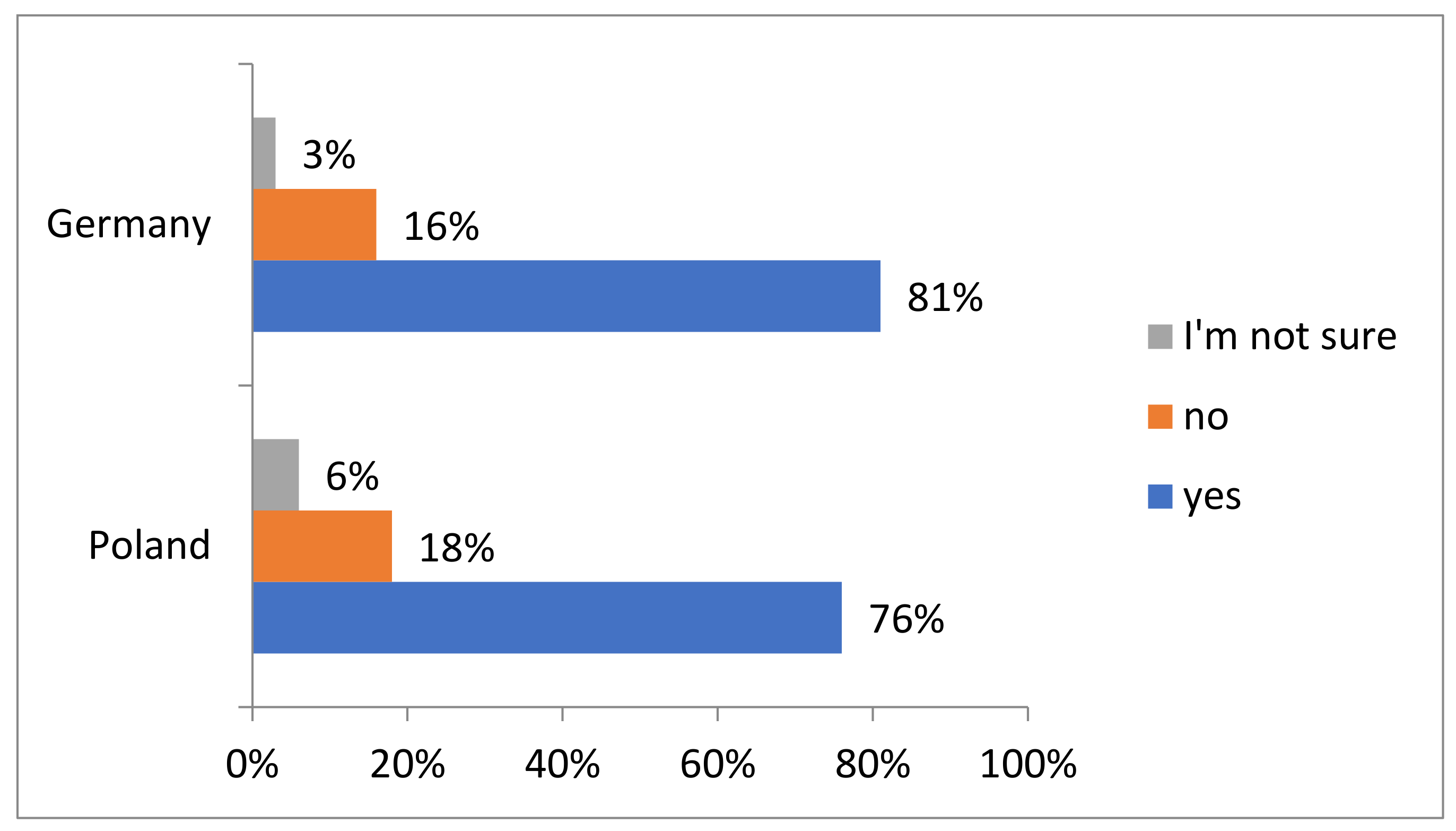

- Integration of CSR: Both countries have over 50% of their companies incorporating CSR into their daily business operations. This not only indicates a shift towards sustainable business practices but also underlines the importance of CSR in the modern business environment.

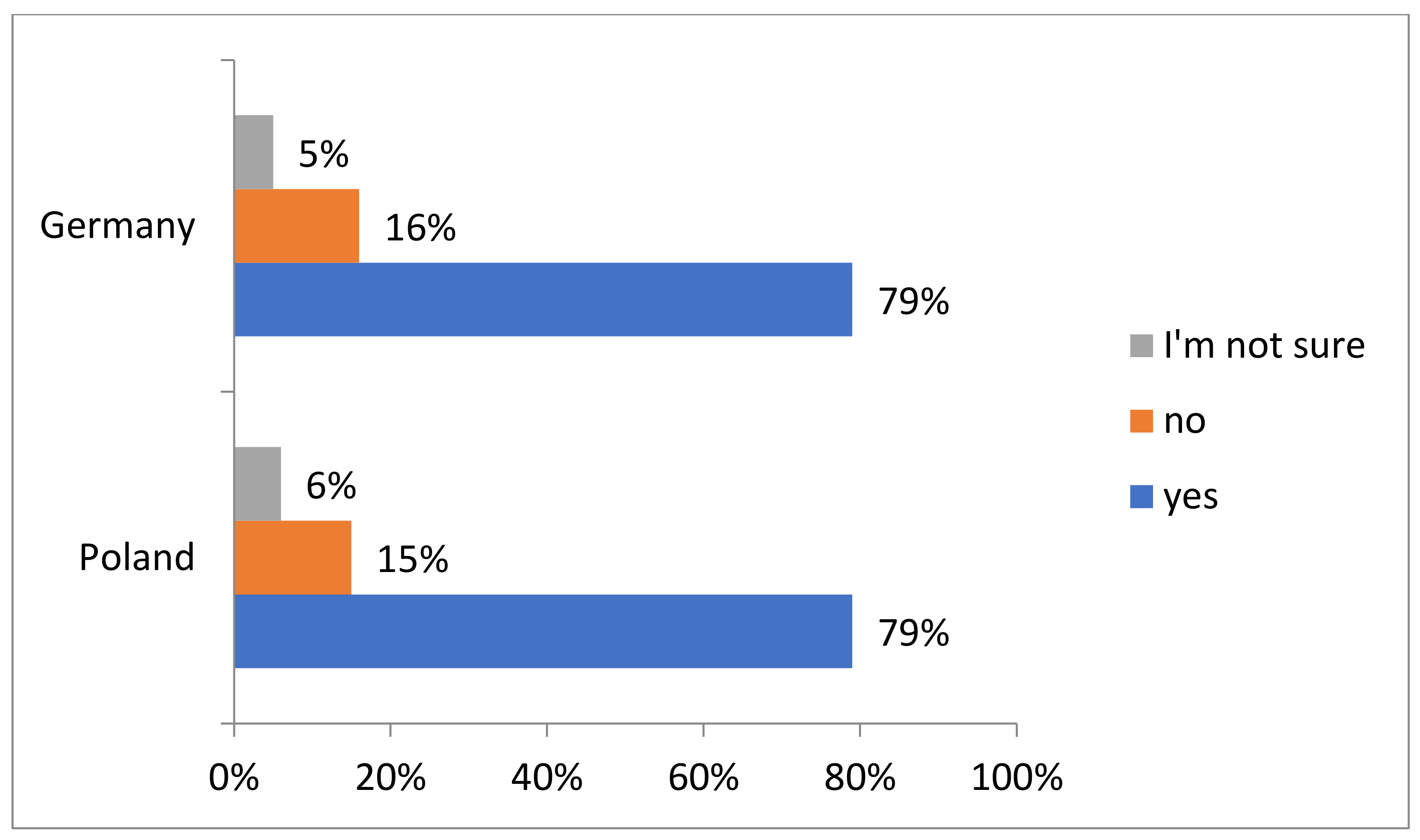

- Role of Managers: Managers serve as the bridge between the higher-level strategic goals and operational-level tasks. Their involvement in educating employees about CSR is pivotal. Given their influence, active participation from them can effectively drive the CSR agenda in a company. The fact that companies are experiencing benefits from such involvement underlines the importance of leadership in CSR initiatives.

- Employee Education: By educating their workforce about CSR, companies are ensuring a holistic understanding and acceptance throughout the organization. When employees, regardless of their positions, understand the importance and goals of CSR, it fosters a culture that supports sustainability and ethical business practices.

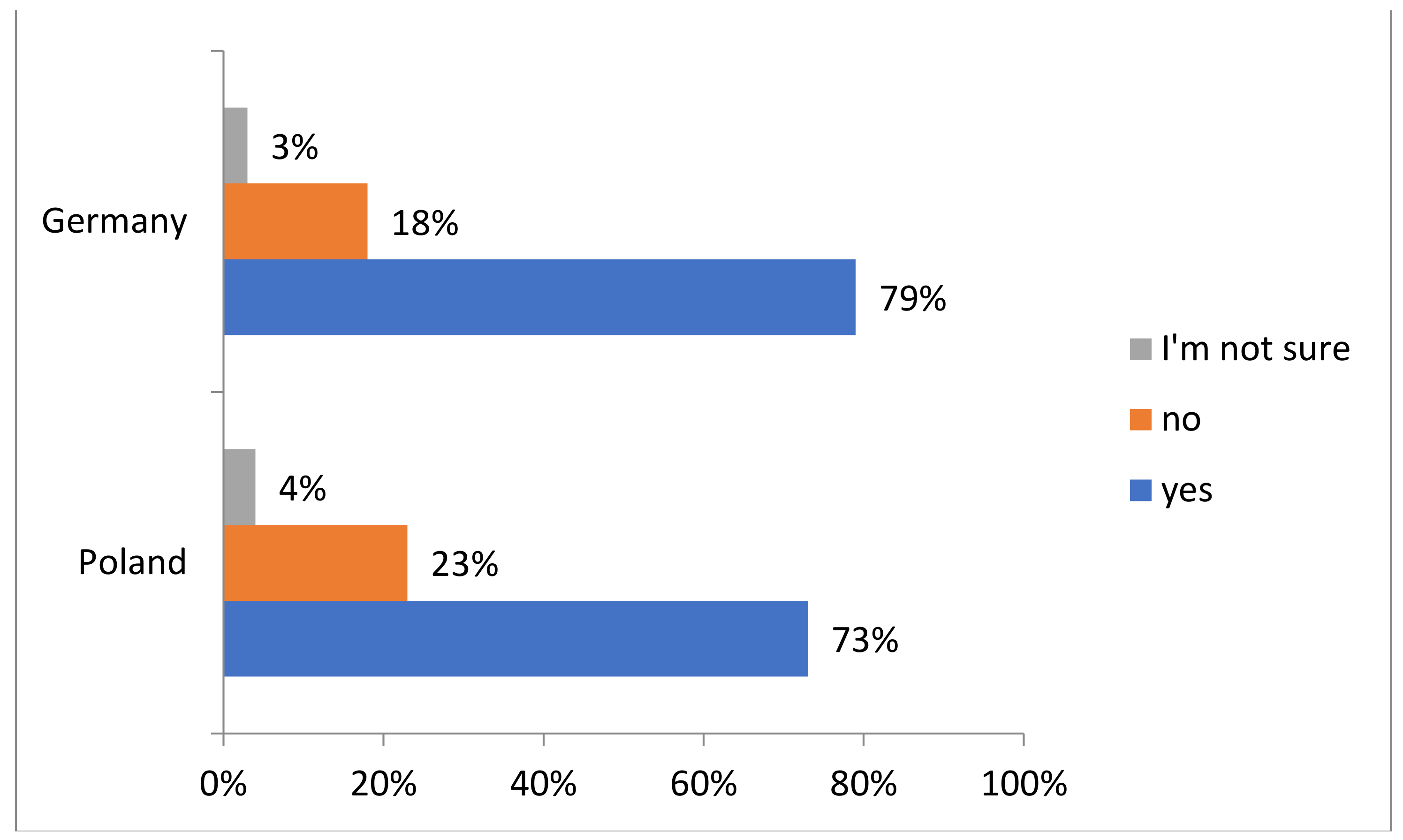

- Challenges: The recognition of challenges faced by managers in CSR implementation indicates preparedness. If managers are aware of the hurdles, they are better positioned to navigate them.

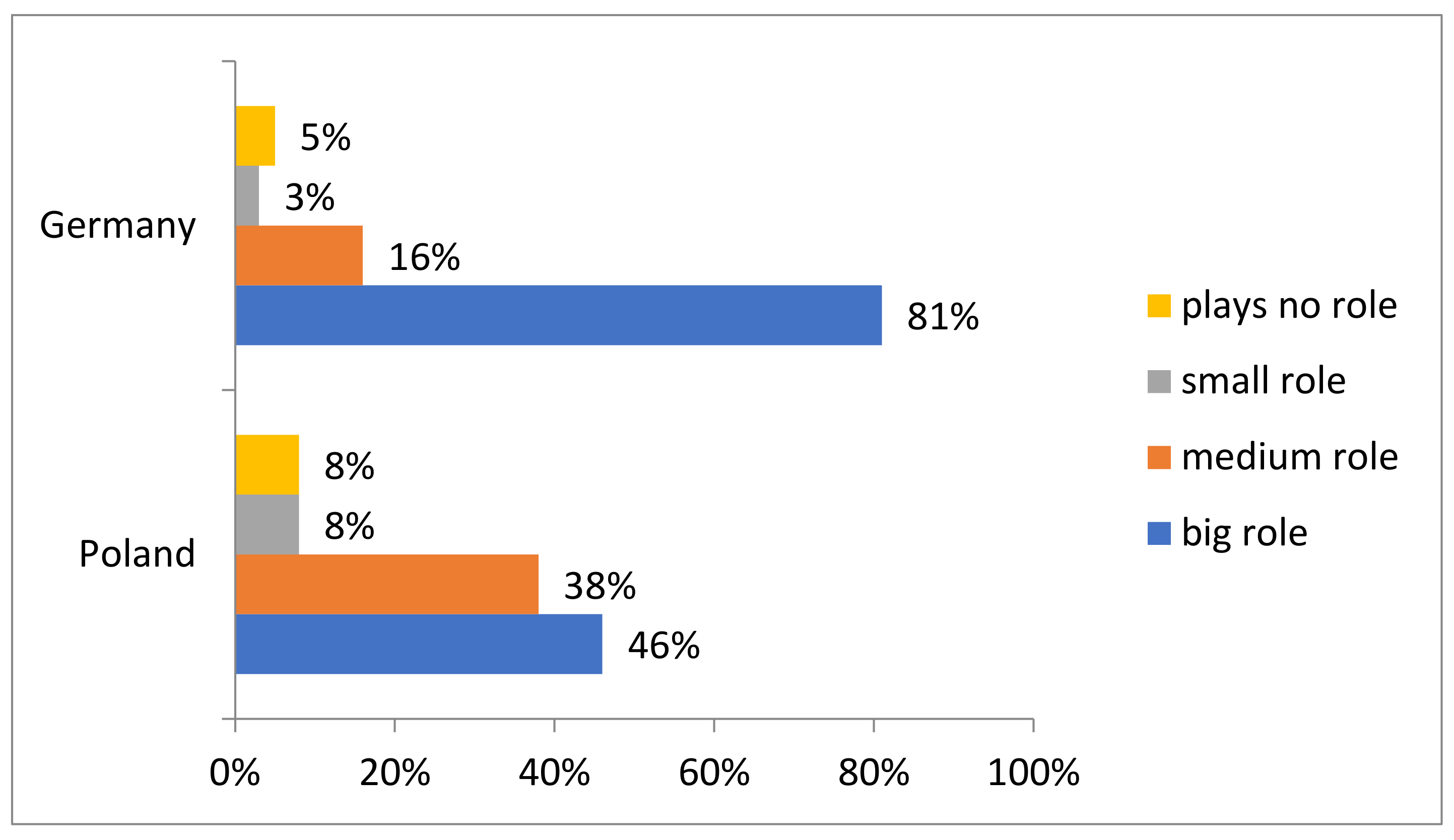

- Germany: Seems to have a marginally higher engagement at the managerial level in CSR issues and more companies have witnessed the advantages of active managerial involvement. This might indicate a more top-down approach in German companies where leadership takes the initiative in driving CSR goals.

- Poland: The emphasis on sustainable purchasing practices and sustainability training indicates a different approach to CSR. Sustainable purchasing practices can have a domino effect, promoting sustainable practices up and down the supply chain. By emphasizing sustainability training, Polish companies are ensuring that the workforce is equipped with the necessary knowledge to make informed decisions in their roles.

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Conflicts of Interest

References

- Werther, W.B.; Chandler, D. Strategic corporate social responsibility as global brand insurance. Bus. Horiz. 2005, 48, 317–324. [Google Scholar] [CrossRef]

- Agudelo, M.A.L.; Jóhannsdóttir, L.; Davídsdóttir, B. A literature review of the history and evolution of corporate social responsibility. Int. J. Corp. Soc. Responsib. 2019, 4, 1. [Google Scholar] [CrossRef]

- Juniarti, J. Does mandatory CSR provide long-term benefits to shareholders? Soc. Responsib. J. 2020, 17, 776–794. [Google Scholar] [CrossRef]

- Thompson, J. Business Ethics and Environmental Responsibility: An Empirical Examination of Managerial Strategies. J. Bus. Res. 2022, 73, 5–14. [Google Scholar]

- Smith, J.; Anderson, P.; Becker, H.; Martin, J.; Thomas, L. Balancing Short-term Financial Goals with Long-term CSR Strategy: An Empirical Analysis. J. Bus. Ethics 2021, 163, 39–45. [Google Scholar]

- Johnson, E. From Theory to Practice: Translating CSR Principles into Business Strategy. J. Corp. Citizsh. 2020, 41, 10–15. [Google Scholar]

- Freeman, R.E. Strategic Management: A Stakeholder Approach; Cambridge University Press: Cambridge, UK, 2010. [Google Scholar]

- Harris, L. CSR and its Implementation in Contemporary Business: Managerial Approaches. Bus. Ethics A Eur. Rev. 2022, 30, 4–11. [Google Scholar]

- Rudnicka, A. CSR—Improving Social Relations in the Company; Wolters Kluwer Business: Warsaw, Poland, 2012. [Google Scholar]

- Williams, J. Impact of CSR on Corporate Image: The Role of Sustainable Practices. J. Bus. Ethics 2020, 166, 3–12. [Google Scholar]

- Davis, A. Effective CSR Practices for Positive Stakeholder Engagement. Bus. Strategy Environ. 2021, 31, 2–9. [Google Scholar]

- Miciuła, I.; Nowakowska-Grunt, J. Using the AHP method to select an energy supplier for household in Poland. Procedia Comput. Sci. 2019, 159, 2324–2334. [Google Scholar] [CrossRef]

- Turner, N. Leveraging Webinars for Sustainability Education: A Managerial Perspective. J. Corp. Citizsh. 2022, 43, 1–14. [Google Scholar]

- Wilson, P. Online Courses and Sustainability Education: Insights from Managers. Bus. Ethics A Eur. Rev. 2022, 31, 5–13. [Google Scholar]

- García-Muiña, F.E.; Medina-Salgado, M.S.; Ferrari, A.M.; Cucchi, M. Sustainability transition in Industry 4.0 and Smart Manufacturing with the triple-layered business model canvas. Sustainability 2020, 12, 2364. [Google Scholar] [CrossRef]

- Thompson, L.; Jakeman, M.; Johansson, C. Managing Corporate Sustainability: Role of Managers in Implementing Strategies. J. Bus. Ethics 2020, 165, 16–30. [Google Scholar]

- Wojtaszek, H.; Miciuła, I. Analysis of Factors Giving the Opportunity for Implementation of Innovations on the Example of Manufacturing Enterprises in the Silesian Province. Sustainability 2019, 11, 5850. [Google Scholar] [CrossRef]

- Singh, A.; Gupta, R.; Kumar, A. Corporate Social Responsibility and Environmental Protection. Corp. Soc. Responsib. Environ. Manag. 2021, 28, 22–34. [Google Scholar]

- Howard, M.; Kumar, P.; Ma, Y. The Role of CSR in Achieving Sustainable Development. Sustainability 2021, 13, 19–33. [Google Scholar]

- Foster, J.; Lowe, A.; Ellem, B. Ethical Business Practices and CSR in Organisations. J. Bus. Ethics 2022, 159, 35–44. [Google Scholar]

- Zhao, M.; Chow, T. The Benefits of Implementing Corporate Social Responsibility: Evidence from the Asian Market. Asian Bus. Manag. 2020, 19, 18–37. [Google Scholar]

- Taylor, S.; Singh, P. CSR and Employee Welfare: An Empirical Analysis. Empl. Relat. 2020, 42, 24–40. [Google Scholar]

- Kaur, H.; Kumar, S.; Tavoni, M. Impact of CSR on Employee Welfare. Bus. Ethics A Eur. Rev. 2020, 29, 31–44. [Google Scholar]

- Jenkins, H.; Yakovleva, N. Corporate Social Responsibility in the Mining Industry: Exploring Trends in Social and Environmental Disclosure. J. Clean. Prod. 2021, 14, 27–41. [Google Scholar] [CrossRef]

- Trapp, N.L. Corporation as climate ambassador: Transcending business sector boundaries in a Swedish CSR campaign. Public Relat. Rev. 2012, 38, 458–465. [Google Scholar] [CrossRef]

- Michaelson, C.; Pratt, M.; Grant, A.; Dunn, C. Meaningful Work: Connecting Business Ethics and Organization Studies. J. Bus. Ethics 2021, 121, 77–90. [Google Scholar] [CrossRef]

- Kramer, M.; Pfitzer, M.; Lee, P. The Ecosystem of Shared Value. Harv. Bus. Rev. 2022, 94, 17–25. [Google Scholar]

- Srivastava, M.; Kaul, D. Exploring the Linkage between Stakeholder Management, CSR and Corporate Reputation. Vikalpa 2020, 45, 27–40. [Google Scholar]

- Roth, H.; Hayden, F. Incorporating Corporate Social Responsibility into Strategic Management: A Stakeholder Perspective. Bus. Strategy Environ. 2021, 30, 24–38. [Google Scholar]

- Bhattacharya, C.; Sen, S. Why Companies are Becoming B Corporations. Harv. Bus. Rev. 2022, 96, 25–32. [Google Scholar]

- Chandler, D.; Werther, W. Strategic Corporate Social Responsibility: Stakeholders in a Global Environment. Bus. Soc. 2020, 59, 20–35. [Google Scholar]

- Adam, A.A.; Shauki, E.R. Socially responsible investment in Malaysia: Behavioral framework in evaluating investors’ decision making process. J. Clean. Prod. 2014, 80, 224–240. [Google Scholar] [CrossRef]

- Vanhamme, J.; Grobben, B. The Too-Good-To-Be-True Paradox and the Role of Corporate Social Responsibility Skepticism. J. Bus. Ethics 2020, 165, 25–36. [Google Scholar]

- Bondy, K.; Moon, J.; Matten, D. An Institution of Corporate Social Responsibility (CSR) in Multi-National Corporations (MNCs): Form and Implications. J. Bus. Ethics 2022, 111, 281–299. [Google Scholar] [CrossRef]

- McWilliams, A.; Siegel, D. Creating and Capturing Value: Strategic Corporate Social Responsibility, Resource-Based Theory, and Sustainable Competitive Advantage. J. Manag. 2021, 37, 1480–1505. [Google Scholar] [CrossRef]

- Higgins, C.; Walker, R. Ethos, logos, pathos: Strategies of persuasion in social/environmental reports. Account. Forum 2022, 36, 194–208. [Google Scholar] [CrossRef]

- Rahman, S.; Post, C. Measurement Issues in Environmental Corporate Social Responsibility (ECSR): Toward a Transparent, Reliable, and Construct Valid Measure. J. Bus. Ethics 2021, 105, 307–319. [Google Scholar] [CrossRef]

- Gupta, S.; Pirsch, J. A taxonomy of cause-related marketing research: Current findings and future research directions. J. Nonprofit Public Sect. Mark. 2020, 19, 25–51. [Google Scholar] [CrossRef]

- Tylżanowski, R.; Kazojć, K.; Miciuła, I. Exploring the Link between Energy Efficiency and the Environmental Dimension of Corporate Social Responsibility: A Case Study of International Companies in Poland. Energies 2023, 16, 6080. [Google Scholar] [CrossRef]

- Jamali, D.; Carroll, A. Capturing advances in CSR: Developed versus developing country perspectives. Bus. Ethic A Eur. Rev. 2017, 26, 321–325. [Google Scholar] [CrossRef]

- Aguinis, H.; Glavas, A. What we know and don’t know about corporate social responsibility: A review and research agenda. J. Manag. 2012, 38, 932–968. [Google Scholar] [CrossRef]

- Park, Q.; Lee, H. The Role of Corporate Social Responsibility in Enhancing Financial Performance: Evidence from Asian and European Retailers. J. Bus. Ethics 2023, 149, 4276–4291. [Google Scholar]

- Baxter, P. Long-Term Impact of CSR on Business Profitability and Survival. J. Sustain. Financ. Invest. 2021, 11, 61–72. [Google Scholar]

- Mustapha, M.A.; Manan, Z.A.; Alwi, S.R.W. Sustainable Green Management System (SGMS)—An integrated approach towards organizational sustainability. J. Clean. Prod. 2017, 146, 158–172. [Google Scholar] [CrossRef]

- Kitzmueller, M.; Shimshack, J. Economic perspectives on corporate social responsibilities. J. Econ. Lit. 2012, 50, 51–84. [Google Scholar] [CrossRef]

- Jackson, T. Effective Communication of Corporate Social Responsibility (CSR): A Framework. J. Bus. Commun. 2021, 58, 45–63. [Google Scholar]

- Lüdeke-Freund, F. Sustainable entrepreneurship, innovation, and business models: Integrative framework and propositions for future research. Bus. Strategy Environ. 2020, 29, 665–681. [Google Scholar] [CrossRef]

- Foster, W.M. Aligning Stakeholder Engagement Strategies with CSR Communication. J. Bus. Res. 2022, 118, 52–66. [Google Scholar]

- Bernardi, C.; Stark, A.W. Environmental, social and governance disclosure, integrated reporting, and the accuracy of analyst forecasts. Br. Account. Rev. 2018, 50, 16–31. [Google Scholar] [CrossRef]

- Thakhathi, A.; le Roux, C.; Davis, A. Sustainability leaders’ influencing strategies for institutionalising organisational change towards corporate sustainability: A strategy-as-practice perspective. J. Chang. Manag. 2019, 19, 246–265. [Google Scholar] [CrossRef]

- Miciuła, I.; Miciuła, K. Renewable Energy and Its Financial Aspects as an Element of the Sustainable Development of Poland; Scientific Papers of Wrocław University of Economics No. 330; Wrocław University of Economics: Wrocław, Poland, 2014; pp. 239–247. [Google Scholar]

- Wagner, D.M. Sustainable Business Practices in Germany: An Analysis of Current Strategies. Eur. J. Bus. Manag. 2021, 12, 54–68. [Google Scholar]

- Novak, M.; Schmidt, P.; Schulz, A.; Wagner, T. CSR Education and Training in Polish Enterprises: An Empirical Study. J. Bus. Ethics 2021, 168, 47–63. [Google Scholar]

- Fischer, B.; Schulz, K.; Becker, L. Webinars and Online Courses as Tools for CSR Education in German Companies. J. Corp. Learn. 2022, 13, 60–78. [Google Scholar]

- Kowalski, R. The Role of Managers in Transforming Business Practices for Social and Environmental Benefits: A Comparative Study. J. Bus. Ethics 2022, 171, 39–55. [Google Scholar]

- Salim, N.; Rahman, M.N.A.; Wahab, D.A. A systematic literature review of internal capabilities for enhancing eco-innovation performance of manufacturing firms. J. Clean. Prod. 2019, 209, 1445–1460. [Google Scholar] [CrossRef]

- Zamojski, P.; Wroblewski, L. CSR Impact on Business Practices in Poland: A Managerial Perspective. Bus. Strategy Environ. 2022, 31, 62–77. [Google Scholar]

- Schneider, M.; Schmidt, L.; Becker, M. The Impact of Management on CSR and Sustainable Business in Germany. Corp. Soc. Responsib. Environ. Manag. 2021, 30, 40–58. [Google Scholar]

- Lončar, D.; Paunković, J.; Jovanović, V.; Krstić, V. Environmental and social responsibility of companies cross EU countries—Panel data analysis. Sci. Total Environ. 2019, 657, 287–296. [Google Scholar] [CrossRef]

- Bergmann, U. CSR Strategies and the Role of Managers in Germany: An Analysis of Trends and Perspectives. Eur. Manag. Rev. 2020, 17, 39–55. [Google Scholar]

- Piasecki, B.; Jankowski, P.; Korzeniowski, G. Building the Culture of the Organization through CSR: A Polish Perspective. J. Bus. Ethics 2020, 160, 41–57. [Google Scholar]

- Schultz, F.; Wagner, T.; Schmidt, A. Encouraging the Involvement of All Employees in CSR: A German Study. Corp. Soc. Responsib. Environ. Manag. 2021, 28, 59–75. [Google Scholar]

- Bastas, A.; Liyanage, K. Setting a framework for organisational sustainable development. Sustain. Prod. Consum. 2019, 20, 207–229. [Google Scholar] [CrossRef]

- Meyer, H.; Becker, T.; Schmidt, L. Balancing Economic Opportunities and Social Responsibility in Germany: A Managerial Perspective. Bus. Strategy Environ. 2020, 29, 56–72. [Google Scholar]

- Stawicki, M. The Impact of Management on the Reputation of Socially Responsible Companies: A Study in Poland. Corp. Reput. Rev. 2021, 24, 50–66. [Google Scholar]

- Schmidt, B. Promoting Sustainable Development and Social Inclusion in German Companies: A Managerial Perspective. Corp. Soc. Responsib. Environ. Manag. 2021, 28, 40–58. [Google Scholar]

- Cantele, S.; Zardini, A. Is sustainability a competitive advantage for small businesses? An empirical analysis of possible mediators in the sustainability–financial performance relationship. J. Clean. Prod. 2018, 182, 166–176. [Google Scholar] [CrossRef]

- Becker, H.; Wagner, D.; Schultz, L. Maintaining Social and Ecological Responsibility in Germany: A Managerial Perspective. J. Bus. Ethics 2022, 170, 42–58. [Google Scholar]

- Kowalski, T.; Zygmunt, A.; Szczepanski, M. CSR in Poland: Balancing New Economic Opportunities and Social Responsibility. J. Bus. Ethics 2021, 169, 59–75. [Google Scholar]

- Schmidt, P.; Wagner, L.; Braun, M. Sustainable Development in the German Business Context: A Managerial Perspective. Corp. Soc. Responsib. Environ. Manag. 2022, 29, 43–60. [Google Scholar]

- GOV. 2023. Available online: https://www.gov.pl/web/fundusze-regiony/wspieramy-rozwoj-odpowiedzialnych-polityk-pracowniczych-inauguracja-przewodnika-csr-po-bezpiecznym-i-zrownowazonym-srodowisku-pracy (accessed on 14 July 2023).

- Wirth, H.; Schmidt, B.; Becker, M. Balancing Economic Growth and Social Responsibility in Germany: A Study on the Challenges Faced by Managers. Bus. Strategy Environ. 2021, 30, 60–78. [Google Scholar]

- Wilk, I. Corporate social responsibility and the pro-ecological activity of the enterprise on the market. In Zeszyty Naukowe; No. 662. Economic Problems of Services No. 74; Research of the University of Szczecin: Szczecin, Poland, 2011. [Google Scholar]

- Keller, S. German Managers and the Challenge of Balancing Economic Growth and Social Responsibility. Eur. J. Bus. Manag. 2023, 15, 65–80. [Google Scholar]

- Czarniak, A.; Zaremba, W.; Strzelecki, M. The Future of CSR in Poland: Perspectives and Implications for Managers. J. Bus. Ethics 2022, 175, 75–90. [Google Scholar]

- Schultz, L.; Fischer, A.; Beckmann, M. CSR in the Future of Germany: The Role of Managers in Balancing Economic and Social Responsibilities. Corp. Soc. Responsib. Environ. Manag. 2023, 31, 70–86. [Google Scholar]

- Kuo, L.; Chen, V.Y.-J. Is environmental disclosure an effective strategy on establishment of environmental legitimacy for organization? Manag. Decis. 2013, 51, 1462–1487. [Google Scholar] [CrossRef]

- Wagner, F. CSR Practices in Germany: A Future Perspective for Managers. Eur. J. Bus. Manag. 2023, 16, 60–76. [Google Scholar]

- Pawlowski, K. CSR Guidelines and the Role of Management in Polish Companies. J. Bus. Ethics 2023, 180, 55–70. [Google Scholar]

- Haseeb, M.; Hussain, H.I.; Kot, S.; Androniceanu, A.; Jermsittiparsert, K. Role of social and technological challenges in achieving a sustainable competitive advantage and sustainable business performance. Sustainability 2019, 11, 3811. [Google Scholar] [CrossRef]

- Zygmunt, A.; Szczepanski, M.; Kowalski, T. Sustainability and Social Inclusion in Polish Companies: The Role of Management. Eur. Manag. Rev. 2023, 20, 62–78. [Google Scholar]

- Schmidt, L.; Wagner, D.; Braun, M. Sustainability and Social Inclusion in German Companies: A Managerial Perspective. Corp. Soc. Responsib. Environ. Manag. 2023, 31, 55–71. [Google Scholar]

- Jankowski, P.; Piasecki, B.; Korzeniowski, G. Unique Opportunities and Challenges in CSR for Polish Managers. Bus. Strategy Environ. 2023, 32, 65–80. [Google Scholar]

- Wagner, T.; Schultz, F.; Schmidt, A. Unique Opportunities and Challenges in CSR for German Managers. J. Bus. Ethics 2023, 183, 55–70. [Google Scholar]

- Szczepankiewicz, E.I.; Mućko, P. CSR Reporting Practices of Polish Energy and Mining Companies. Sustainability 2016, 8, 126. [Google Scholar] [CrossRef]

- Reinhardt, A. Fostering Sustainability and Reducing CO2 Emissions: Managerial Initiatives in German Companies. Environ. Sci. Policy 2020, 110, 85–90. [Google Scholar]

- Ozbekler, T.M.; Ozturkoglu, Y. Analysing the importance of sustainability-oriented service quality in competition environment. Bus. Strategy Environ. 2020, 29, 1504–1516. [Google Scholar] [CrossRef]

- Orji, I.J. Examining barriers to organizational change for sustainability and drivers of sustainable performance in the metal manufacturing industry. Resour. Conserv. Recycl. 2019, 140, 102–114. [Google Scholar] [CrossRef]

- Soytas, M.A.; Denizel, M.; Usar, D.D. Addressing endogeneity in the causal relationship between sustainability and financial performance. Int. J. Prod. Econ. 2019, 210, 56–71. [Google Scholar] [CrossRef]

- Abbas, J.; Sağsan, M. Impact of knowledge management practices on green innovation and corporate sustainable development: A structural analysis. J. Clean. Prod. 2019, 229, 611–620. [Google Scholar] [CrossRef]

- Kneipp, J.M.; Gomes, C.M.; Bichueti, R.S.; Frizzo, K.; Perlin, A.P. Sustainable innovation practices and their relationship with the performance of industrial companies. Rev. Gestão 2019, 26, 94–111. [Google Scholar] [CrossRef]

- Saunila, M.; Nasiri, M.; Ukko, J.; Rantala, T. Smart technologies and corporate sustainability: The mediation effect of corporate sustainability strategy. Comput. Ind. 2019, 108, 178–185. [Google Scholar] [CrossRef]

- Brunner, H. More Balanced Evaluation Models for CSR: Insights from Germany. Bus. Soc. 2021, 60, 93–99. [Google Scholar]

- Miciuła, I.; Stępień, P. The Impact of Current EU Climate and Energy Policies on the Economy of Poland. Pol. J. Environ. Stud. 2019, 28, 2273–2280. [Google Scholar] [CrossRef]

- Kukurba, M.; Waszkiewicz, A.E.; Salwin, M.; Kraslawski, A. Co-Created Values in Crowdfunding for Sustainable Development of Enterprises. Sustainability 2021, 13, 8767. [Google Scholar] [CrossRef]

- Salwin, M.; Jacyna-Gołda, I.; Bańka, M.; Varanchuk, D.; Gavina, A. Using Value Stream Mapping to Eliminate Waste: A Case Study of a Steel Pipe Manufacturer. Energies 2021, 14, 3527. [Google Scholar] [CrossRef]

- Schultz, T. The Conflict between Short-Term Financial Goals and Long-Term CSR: A Polish Perspective. J. Bus. Ethics 2022, 170, 96–102. [Google Scholar]

- Kowalski, P. Balancing Economic Expectations with CSR Benefits in Poland: A Managerial Challenge. Bus. Soc. 2023, 61, 98–105. [Google Scholar]

- Urbaniec, M.; Zur, A. Business model innovation in corporate entrepreneurship: Exploratory insights from corporate accelerators. Int. Entrep. Manag. J. 2021, 17, 865–888. [Google Scholar] [CrossRef]

- Moschner, S.L.; Fink, A.A.; Kurpjuweit, S.; Wagner, S.M.; Herstatt, C. Toward a better understanding of corporate accelerator models. Bus. Horiz. 2019, 62, 637–647. [Google Scholar] [CrossRef]

- Gospel, H.; Sako, M. The Re-bundling of Corporate Functions: The Evolution of Shared Services and Outsourcing. Human Resource Management. Ind. Corp. Change 2010, 19, 1367–1396. [Google Scholar] [CrossRef]

- Garcia-Castro, R.; Francoeur, C. When More Is Not Better: Complementarities, Costs and Contingencies in Stakeholder Management. Strateg. Manag. J. 2014, 37, 406–424. [Google Scholar] [CrossRef]

- Becker, J. Investments in Long-Term CSR Initiatives: The Role of Managers in Germany. Corp. Soc. Responsib. Environ. Manag. 2022, 29, 103–109. [Google Scholar]

- Urbaniec, M.; Małkowska, A.; Włodarkiewicz-Klimek, H. The Impact of Technological Developments on Remote Working: Insights from the Polish Managers’ Perspective. Sustainability 2022, 14, 552. [Google Scholar] [CrossRef]

- Bańka, M.; Salwin, M.; Tylżanowski, R.; Miciuła, I.; Sychowicz, M.; Chmiel, N.; Kopytowski, A. Start-Up Accelerators and Their Impact on Entrepreneurship and Social Responsibility of the Manager. Sustainability 2023, 15, 8892. [Google Scholar] [CrossRef]

- Güney, T. Renewable energy consumption and sustainable development in high-income countries. Int. J. Sustain. Dev. World Ecol. 2021, 28, 376–385. [Google Scholar] [CrossRef]

- Amrutha, V.N.; Geetha, S.N. A systematic review on green human resource management: Implications for social sustainability. J. Clean. Prod. 2020, 247, 119131. [Google Scholar] [CrossRef]

- Miciuła, I.; Wojtaszek, H.; Bazan, M.; Janiczek, T.; Włodarczyk, B.; Kabus, J.; Kana, R. Management of the Energy Mix and Emissivity of Individual Economies in the European Union as a Challenge of the Modern World Climate. Energies 2020, 13, 5191. [Google Scholar] [CrossRef]

- Pach-Gurgul, A. The energy-climate package and realisation of its objectives within the context of the sustainable development of the European Union. Cent. Eur. Rev. Econ. Financ. 2015, 10, 75–90. [Google Scholar]

- Panarello, D.; Gatto, A. Decarbonising Europe—EU citizens’ perception of renewable energy transition amidst the European Green Deal. Energy Policy 2023, 172, 113272. [Google Scholar] [CrossRef]

- Späth, P.; Rohracher, H. Energy regions: The transformative power of regional discourses on socio-technical futures. Res. Policy 2010, 39, 449–458. [Google Scholar] [CrossRef]

- Stavytskyy, A.; Kharlamova, G.; Giedraitis, V.; Šumskis, V. Estimating the interrelation between energy security and macroeconomic factors in European countries. J. Int. Stud. 2018, 11, 217–238. [Google Scholar] [CrossRef]

- Rosen, M. Economic and Exergy—Enhanced Approach to Energy Economics; Nova Science: Hauppauge, NY, USA, 2011. [Google Scholar]

- Noailly, J.; Smeets, R. Financing Energy Innovation: Internal Finance and the Direction of Technical Change. Environ. Resour. Econ. 2021, 83, 145–169. [Google Scholar] [CrossRef]

- Poulianiti, K.P.; Havenith, G.; Flouris, A.D. Metabolic energy cost of workers in agriculture, construction, manufacturing, tourism, and transportation industries. Ind. Health 2019, 57, 283–305. [Google Scholar] [CrossRef]

- Zwolak, J. The effectivenrss of innovation projects in Polish industry. Rev. Innov. Compet. J. Econ. Soc. Res. 2016, 2, 97–110. [Google Scholar] [CrossRef]

- Miciuła, I.; Kadlubek, M.; Stępień, P. Modern Methods of Business Valuation—Case Study and New Concepts. Sustainability 2020, 12, 2699. [Google Scholar] [CrossRef]

- Heinrich, B. Stakeholder Involvement in CSR Decision Making in Germany. J. Clean. Prod. 2021, 286, 118–124. [Google Scholar]

- Garcia, S.; Luis, J.; Perez-Ruiz, S. Development of capabilities from the innovation of the perspective of poverty and disability. J. Innov. Knowl. 2017, 2, 74–86. [Google Scholar] [CrossRef]

- Hahn, T.; Figge, F.; Barkemeyer, R. Sustainable Value creation among companies in the manufacturing sector. Int. J. Environ. Technol. Manag. 2007, 7, 496. [Google Scholar] [CrossRef]

- Baldassarre, B.; Calabretta, G.; Bocken, N.M.P.; Jaskiewicz, T. Bridging sustainable business model innovation and user-driven innovation: A process for sustainable value proposition design. J. Clean. Prod. 2017, 147, 175–186. [Google Scholar] [CrossRef]

- Kumar, V.; Alshazly, H.; Idris, S.A.; Bourouis, S. Evaluating the Impact of COVID-19 on Society, Environment, Economy, and Education. Sustainability 2021, 13, 13642. [Google Scholar] [CrossRef]

- Jakubowska, K. Inglot’s Corporate Transparency and Investment in Employee Welfare. Bus. Ethics A Eur. Rev. 2023, 33, 123–130. [Google Scholar]

- Jałowiec, T.; Maśloch, P.; Wojtaszek, H.; Miciuła, I.; Maśloch, G. Analysis of the Determinants of Innovation in the 21st Century. Eur. Res. Stud. J. 2020, 23, 151–162. [Google Scholar] [CrossRef]

- Ratajczak, P. Sustainable Cosmetic Production in Inglot: The Role of CSR. J. Clean. Prod. 2021, 288, 125–132. [Google Scholar]

- Miluniec, A.; Miciuła, I. Gamification 3.0 for Employees Involvement in the Company. In Proceedings of the 12th Annual International Conference of Education, Research and Innovation ICERI2019 Proceedings, Seville, Spain, 11–13 November 2019; pp. 10878–10884. [Google Scholar] [CrossRef]

- Schuster, L. Corporate Sustainability and Diversity in the German Workplace. Bus. Ethics A Eur. Rev. 2023, 33, 127–134. [Google Scholar]

- Klein, K. Social Involvement in German Companies: A CSR Perspective. J. Bus. Ethics 2023, 174, 128–135. [Google Scholar]

- Müller, M. BMW’s Investment in Electric and Hybrid Cars: A Commitment to Sustainable Development. BMW Sustain. 2023, 16, 129–135. [Google Scholar]

- Schmidt, T. BMW’s Social and Educational Programs: CSR in Action. J. Clean. Prod. 2021, 289, 130–136. [Google Scholar]

- Wagner, J. The Role of CSR in BMW’s Electric and Hybrid Car Development. Bus. Ethics A Eur. Rev. 2023, 33, 131–138. [Google Scholar]

- Hahn, H. Youth Engagement in BMW’s CSR Strategy. BMW Sustain. 2023, 16, 132–139. [Google Scholar]

- Jeronimo Martins. Biedronka for Health. 2022. Available online: https://www.jeronimomartins.com/en/initiatives/biedronka-for-health/ (accessed on 20 July 2023).

- Green PGE. PGE PolskaGrupaEnergetyczna. 2021. Available online: https://www.gkpge.pl/EN/Our-company/Green-PGE (accessed on 21 July 2023).

- Lidl Polska. Cleaning Campaigns. 2020. Available online: https://www.lidl.pl/c/czyste-parki-i-lasy/c977 (accessed on 22 July 2023).

- Allegro Lokalnie. Allegro. 2022. Available online: https://allegro.pl/allegro-lokalnie (accessed on 23 July 2023).

- Orlen for Communities. Orlen. 2023. Available online: https://www.orlen.pl/EN/Responsibility/Pages/default.aspx (accessed on 24 July 2023).

- PKO BankowyFunduszSpołeczny. PKO Bank Polski. 2021. Available online: https://www.pkobp.pl/pkobppl-en/ (accessed on 25 July 2023).

- IKEA Polska. IKEA for Environment. 2022. Available online: https://www.ikea.com/pl/pl/this-is-ikea/sustainable-everyday/ (accessed on 26 July 2023).

- LOT. LOT’s Social Programs. 2023. Available online: https://www.lot.com/us/en/social-responsibility (accessed on 27 July 2023).

- KGHM. KGHM for Communities. 2020. Available online: https://kghm.com/en/our-responsibility (accessed on 28 July 2023).

- PKP. PKP for Public Transport. 2021. Available online: https://www.pkp.pl/pl/o-pkp/spoleczenstwo (accessed on 29 July 2023).

- Orange Polska. Orange’s Social Programs. 2022. Available online: https://www.orange.pl/view/orange-fundacja (accessed on 30 July 2023).

- Tauron. Tauron for Renewables. 2023. Available online: https://www.tauron.pl/en/the-group/about-us/environment-and-society (accessed on 31 July 2023).

- GrupaŻywiec’s CSR. GrupaŻywiec. 2020. Available online: https://en.grupazywiec.pl/responsibility/ (accessed on 1 August 2023).

- AmRest. AmRest’s CSR. 2021. Available online: https://www.amrest.eu/en/sustainable-development (accessed on 2 August 2023).

- KompaniaPiwowarska. KompaniaPiwowarska’s CSR. 2023. Available online: https://www.kp.pl/for-the-society (accessed on 4 August 2023).

- Santander Bank Polska. Santander’s Education Programs. 2020. Available online: https://en.santander.pl/our-bank/responsibility/santander-foundation (accessed on 5 August 2023).

- PocztaPolska. PocztaPolska for Rural Areas. 2021. Available online: https://www.poczta-polska.pl/poczta-polska-spolka-akcyjna-certyfikaty-i-odznaczenia/ (accessed on 6 August 2023).

- CCC. CCC for Sustainable Fashion. 2022. Available online: https://www.ccc.eu/en/responsibility (accessed on 7 August 2023).

- CastoramaPolska. Castorama’s Sustainable Construction. 2023. Available online: https://www.castorama.pl/o-nas/zrownowazony-rozwoj (accessed on 8 August 2023).

- BMW Group Environmental Protection. BMW Official Website. Available online: https://www.bmw.com/environment (accessed on 10 August 2023).

- Siemens Sustainability. Siemens Official Website. Available online: https://www.siemens.com/sustainability (accessed on 10 August 2023).

- Deutsche Bank Corporate Responsibility. Deutsche Bank Official Website. Available online: https://www.db.com/csr (accessed on 11 August 2023).

- Volkswagen for Good. Volkswagen Official Website. Available online: https://www.volkswagen.com/csr (accessed on 12 August 2023).

- GoGreen Program. DHL Official Website. Available online: https://www.dhl.com/gogreen (accessed on 13 August 2023).

- Aldi and Sustainability. Aldi Official Website. Available online: https://www.aldi.com/sustainability (accessed on 14 August 2023).

- BASF Sustainability. BASF Official Website. Available online: https://www.basf.com/sustainability (accessed on 15 August 2023).

- Adidas Sustainability. Adidas Official Website. Available online: https://www.adidas.com/sustainability (accessed on 16 August 2023).

- Bayer Sustainability. Bayer Official Website. Available online: https://www.bayer.com/sustainability (accessed on 17 August 2023).

- Lufthansa and Climate. Lufthansa Official Website. Available online: https://www.lufthansa.com/climate (accessed on 18 August 2023).

- SAP Sustainability. SAP Official Website. Available online: https://www.sap.com/sustainability (accessed on 19 August 2023).

- Merck Corporate Responsibility. Merck Official Website. Available online: https://www.merck.com/csr (accessed on 20 August 2023).

- E.ON Sustainability. E.ON Official Website. Available online: https://www.eon.com/sustainability (accessed on 21 August 2023).

- Deutsche Post and Sustainability. Deutsche Post Official Website. Available online: https://www.deutschepost.com/sustainability (accessed on 22 August 2023).

- Metro Group Responsibility. Metro Group Official Website. Available online: https://www.metrogroup.com/responsibility (accessed on 23 August 2023).

- Henkel Sustainability. Henkel Official Website. Available online: https://www.henkel.com/sustainability (accessed on 24 August 2023).

- Allianz Sustainability. Allianz Official Website. Available online: https://www.allianz.com/sustainability (accessed on 25 August 2023).

- Deutsche Bahn and Environment. Deutsche Bahn Official Website. Available online: https://www.deutschebahn.com/environment (accessed on 26 August 2023).

- RWE Renewables. RWE Official Website. Available online: https://www.rwe.com/renewables (accessed on 27 August 2023).

- Telekom Deutschland Corporate Responsibility. Telekom Deutschland Official Website. Available online: https://www.telekom.com/csr (accessed on 28 August 2023).

- Vodafone Sustainability. Vodafone Official Website. Available online: https://www.vodafone.com/sustainability (accessed on 29 August 2023).

- GrupaŻywiec Recycling Initiative. GrupaŻywiec Official Website. 2020. Available online: https://www.grupazywiec.pl/recycling-initiative (accessed on 1 August 2023).

- BMW Electric Vehicle Development. BMW Official Website. 2020. Available online: https://www.bmw.com/ev-development (accessed on 2 August 2023).

- Lidl’s Ecological Products Line. Lidl Poland Official Website. 2020. Available online: https://www.lidl.pl/eco-line (accessed on 3 August 2023).

- Deutsche Bank’s CSR Training. Deutsche Bank Official Website. 2020. Available online: https://www.db.com/csr-training (accessed on 4 August 2023).

- PKO Bank Polski Sustainability Development Training. PKO Bank Polski Official Website. 2021. Available online: https://www.pkobp.pl/sustainability-training (accessed on 5 August 2023).

- Adidas Recycled Materials Initiative. Adidas Official Website. 2021. Available online: https://www.adidas.com/recycled-materials (accessed on 6 August 2023).

- Orange Campaign for Safe Online Use. Orange Poland Official Website. 2021. Available online: https://www.orange.pl/safe-online (accessed on 7 August 2023).

- Aldi’s Green Products Initiative. Aldi Germany Official Website. 2021. Available online: https://www.aldi.de/green-products (accessed on 8 August 2023).

- CCC Eco Program. CCC Official Website. 2022. Available online: https://www.ccc.eu/ccc-eco (accessed on 9 August 2023).

- Lufthansa’s Sustainable Aviation Technologies Investment. Lufthansa Official Website. 2022. Available online: https://www.lufthansa.com/sustainable-aviation (accessed on 10 August 2023).

- Allegro Used Products Program. Allegro Official Website. 2022. Available online: https://www.allegro.pl/used-products (accessed on 11 August 2023).

- Siemens Energy Management Solutions. Siemens Official Website. 2022. Available online: https://www.siemens.com/energy-management (accessed on 12 August 2023).

- Tchibo Sustainability Programs. Tchibo Official Website. 2023. Available online: https://www.tchibo.com/sustainability (accessed on 13 August 2023).

- Rossmann’s Pro-Ecological Initiatives. Rossmann Poland Official Website. 2023. Available online: https://www.rossmann.pl/ecological-initiatives (accessed on 14 August 2023).

- Edeka’s CSR Activities. Edeka Official Website. 2023. Available online: https://www.edeka.de/csr (accessed on 15 August 2023).

- Rewe Group’s Sustainable Initiatives. Rewe Group Official Website. 2023. Available online: https://www.rewe-group.com/sustainability (accessed on 16 August 2023).

- Baumgartner, R.J.; Rauter, R. Strategic perspectives of corporate sustainability management to develop a sustainable organization. J. Clean. Prod. 2017, 140, 81–92. [Google Scholar] [CrossRef]

- Baldissera, A. Sustainability reporting in banks: History of studies and a conceptual framework for thinking about the future by learning from the past. In Corporate Social Responsibility and Environmental Management; Wiley: Hoboken, NJ, USA, 2023; pp. 1–21. [Google Scholar]

- Akgun, O.T.; Mudge, T.J.; Townsend, B. How company size bias in ESG scores impacts the small cap investor. J. Impact ESG Invest. 2021, 1, 31–44. [Google Scholar] [CrossRef]

- Raj, A.; Kuznetsov, A.; Arun, T.; Kuznetsova, O. How different are corporate social responsibility motives in a developing country? Insights from a study of Indian agribusiness firms. Thunderbird Int. Bus. Rev. 2019, 61, 255–265. [Google Scholar] [CrossRef]

- Hamadamin, H.H.; Atan, T. The Impact of Strategic Human Resource Management Practices on Competitive Advantage Sustainability: The Mediation of Human Capital Development and Employee Commitment. Sustainability 2019, 11, 5782. [Google Scholar] [CrossRef]

- Allen, M.W.; Craig, C.A. Rethinking corporate social responsibility in the age of climate change: A communication perspective. Int. J. Corp. Soc. Responsib. 2016, 1, 1. [Google Scholar] [CrossRef]

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Examples of CSR Activities | |

|---|---|

| Poland | Germany |

|

|

| Benefits of Integrating CSR with Business Practices Based on Poland and Germany | |

|---|---|

|

|

|

|

|

|

|

|

|

|

|

|

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2023 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Wojtaszek, H.; Miciuła, I.; Gac, M.; Kabus, D.; Balcerzyk, R.; Będźmirowski, J.; Kowalczyk, A. Social and Environmental Responsibility Manager on the Example of Companies from Poland and Germany. Sustainability 2023, 15, 14359. https://doi.org/10.3390/su151914359

Wojtaszek H, Miciuła I, Gac M, Kabus D, Balcerzyk R, Będźmirowski J, Kowalczyk A. Social and Environmental Responsibility Manager on the Example of Companies from Poland and Germany. Sustainability. 2023; 15(19):14359. https://doi.org/10.3390/su151914359

Chicago/Turabian StyleWojtaszek, Henryk, Ireneusz Miciuła, Miłosz Gac, Dominik Kabus, Robert Balcerzyk, Jerzy Będźmirowski, and Anna Kowalczyk. 2023. "Social and Environmental Responsibility Manager on the Example of Companies from Poland and Germany" Sustainability 15, no. 19: 14359. https://doi.org/10.3390/su151914359

APA StyleWojtaszek, H., Miciuła, I., Gac, M., Kabus, D., Balcerzyk, R., Będźmirowski, J., & Kowalczyk, A. (2023). Social and Environmental Responsibility Manager on the Example of Companies from Poland and Germany. Sustainability, 15(19), 14359. https://doi.org/10.3390/su151914359