1. Introduction

As a major carbon emitter, China is taking bold steps towards conserving energy, reducing emissions, and adjusting its economic structure, with the aim of reaching its “carbon peak” and “carbon neutrality” targets by 2030 and 2060, respectively [

1,

2]. As the micro-subject of the economy, enterprise low-carbon transformation is the key to achieving the overall economy’s low-carbon transformation. In the process of achieving the goal of “double carbon”, businesses in China are facing significant challenges in reducing their carbon emissions. According to the “Carbon emission ranking of listed companies” in China, in 2020, the carbon emissions of the 100 listed businesses in China participating in the survey exceeded 4.4 billion tons, accounting for about 44.7% of the total CO

2 emissions in the whole country. Empowering enterprises to achieve low-carbon transition is not only correlated with the survival of firms in the context of strict environmental policies, but is also connected to the attainment of carbon neutrality for the whole country.

Enterprises often require technical support for low-carbon transformation. Recently, with the advancement of digital technologies including big data, cloud computing, and blockchain [

3,

4], a growing number of enterprises have embraced the trend of digital economy and initiated digital transformation, utilizing emerging technologies. For one thing, digital transformation has prominent digital spillover effects in terms of fostering corporate innovation [

5,

6], optimizing organizational structures [

7], and enhancing financial performance [

8]. In addition, digital technology, due to its distinctive role in monitoring enterprise processes, operations, and energy consumption, has exerted a profound impact on corporate environmental performance [

9]. According to the “2019 Global Digital Transformation Income Report”, Schneider Electric and its global partners completed 230 projects, with enterprises that deployed digital technology platforms achieving the maximum energy savings of 85%, with an average reduction of 24% and a maximum CO

2 footprint optimization of 50%, with an average optimization of 20%. However, in the context of China’s “dual carbon” strategy, further research is needed on whether digital transformation can promote the reduction of carbon emissions by Chinese enterprises. Exploring this issue has important theoretical and practical significance for China to explore low-carbon economic transformation from a micro perspective.

Part of the research has begun on exploring the concept and evaluation of digital transformation. In terms of the concept, digital transformation essentially falls within the scope of the digital economy. Previous studies have proposed the term “digital economy” [

10] and provided definitions based on the description of digital economic phenomena [

11], a summarization of characteristics [

12], and the decomposition of structure [

13]. From an industry perspective, industrial digital transformation refers to the part of the broad digital economy where traditional industries increase output and enhance efficiency through the adoption of digital technologies [

14]. It involves leveraging advanced digital technologies, empowering and extracting value from data, and digitally transforming and upgrading all factors in the industrial chain (National Information Center, 2021). From an enterprise perspective, most studies consider enterprise digital transformation to be a process that involves the combination of information, computation, communication, and connectivity technologies to reconstruct products and services, business processes, organizational structures, business models, and collaboration models, thereby helping companies create and capture more value [

15,

16,

17] In terms of evaluation, existing research has measured the digitalization of industries from a macro-regional and industry-level perspective based on the broad-scale digital economy [

18]. This measurement is primarily carried out through input–output analysis [

19], and single or composite index evaluation methods [

20]. At the micro-level of enterprises, researchers have employed methods such as questionnaire surveys [

21], text analysis [

22], and index evaluation based on the “input-output” theory [

23] to measure enterprise digital transformation.

Another part of the research field examines the economic effects of digital transformation. From macro perspectives, Choi and Hoon Yi [

24] took the lead in discussing the promotion influence of the popularization of Internet technology on economic growth. On this basis, more and more scholars have further explored the positive impacts of digital technologies and digital transformation on economic development and green economic growth [

25,

26,

27]. Additionally, digital transformation plays an effective role in international trade. According to Freund and Weinhold [

28], web hosts growth can lead to an increase in export growth by reducing the search cost of export trade. Jiang and Jia [

29] found that digitalized service at a higher level can significantly improve digital service trade exports across countries. As for its impacts on industrial chains, Liu and Pan [

30] believed that the application of artificial intelligence may improve the engagement of a country’s industry in the global value chain by reducing trade costs, promoting technological innovation and optimizing resource allocation. From a micro perspective, the impacts of digital transformation on enterprises have attracted more and more attention from scholars. Shang and Wu [

31], Peng and Tao [

32], etc., all found that digital transformation is conducive to improving enterprises’ value. A study by Du and Jiang [

33] also analyzed the facilitation impacts between digital transformation and firm productivity, and showed which effect is, relatively, stronger in downstream firms. Furthermore, digital transformation is also an important factor in reducing firms’ costs, and in increasing operating revenue [

34]. In addition to enterprises’ performance, the corporate digital transformation also affects enterprises’ internal control [

35], management efficiency [

36], and capital market performance [

37], and further exerts influence on risk-taking [

38]. There have also been studies focusing on the effects of digitalization on technology innovation. Wen et al. [

39] discussed the positive effect of digital transformation in corporate innovative practices and indicated that digitalization is a vital driving force in corporate innovation investment. Digital transformation can prompt both the incremental and radical innovation of enterprises [

40].

There have also been studies starting to explore the environmental effects of digital transformation. From a macro perspective, some studies have used urban data from China and empirically found that big data [

41] and artificial intelligence [

42] significantly reduce carbon emissions, while digital finance increases resident carbon emissions through consumption and employment effects [

43]. Another study discovered an inverted U-shaped relationship between digitization and carbon emissions in China [

44], where the digital economy improves carbon emission performance through energy intensity, energy consumption scale, and urban greening, exhibiting non-linear characteristics under different conditions of energy consumption structure [

45]. Research has indicated that digital energy consumption and energy rebound are the main reasons for the non-linear impact of digital development and carbon emissions [

46]. Additionally, based on national panel data analysis, digital transformation reduces the carbon intensity of the transportation industry through technological progress, internal structural upgrades, and energy consumption improvements [

47]. Industrial robots increase productivity, optimize factor structures, promote technological innovation in production, and thus enhance energy efficiency and reduce carbon intensity [

48]. From a micro perspective, research has examined the emission reduction effects of enterprise digital transformation on Chinese industrial enterprises using imported digital products as a natural experiment. The empirical findings indicate that enterprise digital transformation can significantly reduce pollution emissions [

49]. The findings reveal a significant inverted U-shaped non-linear relationship between digital transformation and corporate environmental performance [

50]. Moreover, Shang et al. [

51] measured the level of enterprise digital transformation through the textual analysis of annual reports of A-share listed companies in the Shanghai and Shenzhen stock markets. The study empirically concluded that enterprise digital transformation can significantly reduce carbon emission intensity by enhancing technological innovation, internal control capability, and environmental information disclosure. The impact of digital transformation is stronger for companies in regions with stronger intellectual property protection and for capital-intensive enterprises, but there is no heterogeneity with respect to company type, environmental regulation intensity, and enterprise information infrastructure construction [

51].

In summary, while there is a significant body of literature closely related to this study, there are still areas for further exploration: (1) Most works in the literature primarily focus on the macro-level examination of the economic and environmental effects of digital transformation, as well as the micro-level investigation of the economic effects of digital transformation within enterprises. However, there is still a need to further supplement the literature by investigating the environmental effects of enterprise digital transformation from a micro-level perspective. (2) This study differs from the existing literature, specifically from the research conducted by Shang et al. [

51], in terms of the explored transmission mechanisms, heterogeneity analysis, and selection of instrumental variables. Therefore, there is scope for further research to elucidate the transmission mechanisms of digital transformation, analyze heterogeneity effects, and carefully select instrumental variables to enhance the robustness of the findings.

In view of this, the present study endeavors to utilize data from Chinese A-share listed companies spanning the years 2007 to 2020. The study aims to explore the impact and mechanisms of corporate digital transformation on carbon emissions from both theoretical and empirical perspectives. The potential incremental contributions of this research can be outlined in the following three aspects: (1) This study further reveals the transmission mechanisms of digital transformation on corporate carbon emissions by delving into energy utilization efficiency, financial performance, and green innovation, thereby enhancing the understanding of the interplay between the two phenomena. (2) This study systematically elucidates the heterogeneous impacts of digital transformation on corporate carbon emissions at the corporate level, considering attributes, carbon emission intensity, and financing capacity; at the industry level, assessing technological input intensity and energy consumption intensity; and at the regional level, considering urban environmental regulations, degree of marketization, and resource endowment. This systemic analysis aims to provide explanatory insights into the diverse effects of carbon reduction among different types of companies, industries, and cities. (3) Differing from the instrument variable employed by Shang et al. [

51], this study employs the total word count of annual corporate reports as the instrumental variable, aiming to address endogeneity issues in the model.

2. Theoretical Analysis and Hypothesis

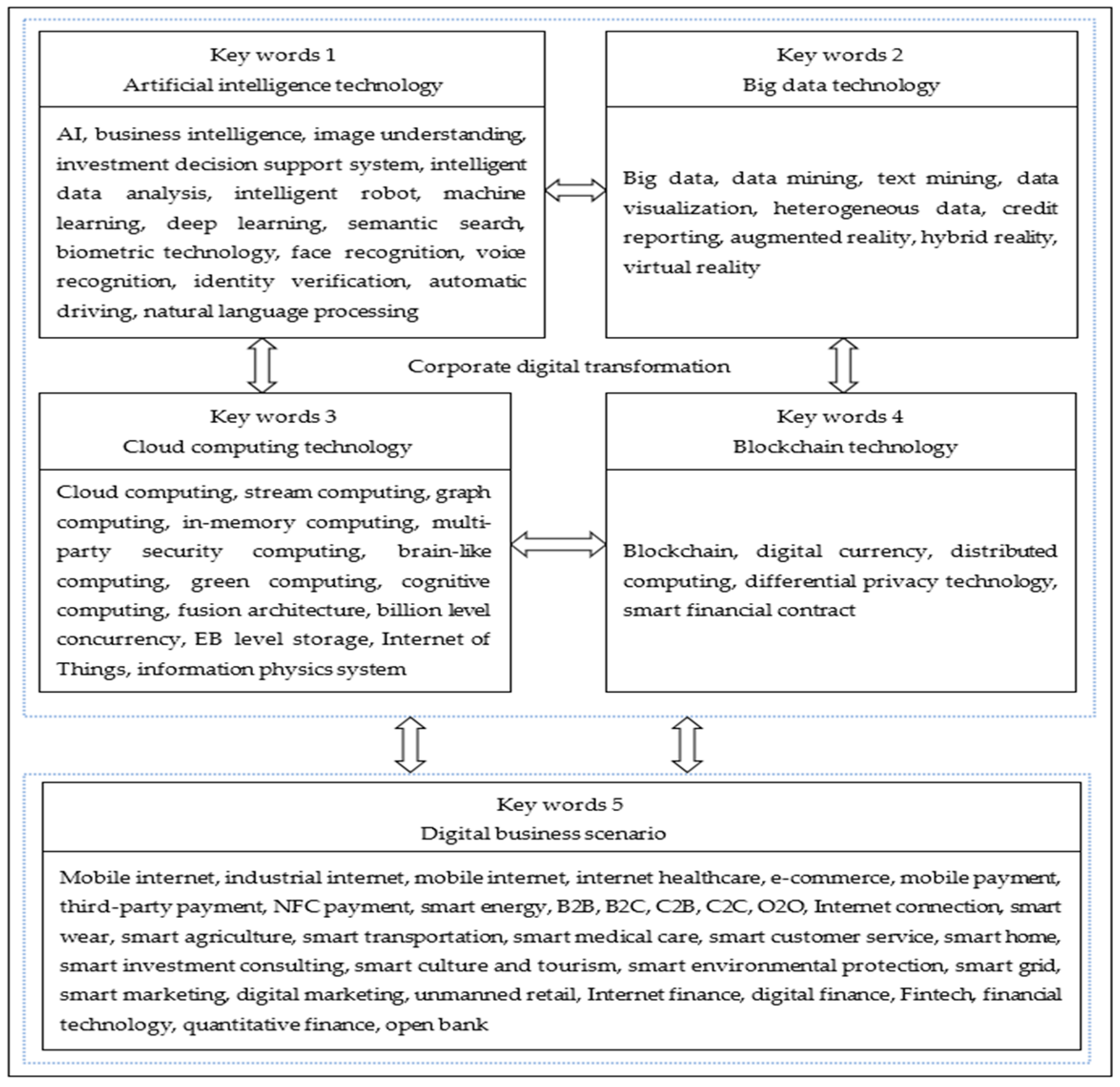

Dissimilar to enterprise informatization transformation, corporate digital transformation involves the utilization of digital technologies (ABCD—Artificial Intelligence, Blockchain, Cloud Computing, Big Data) [

52,

53] to reconstruct products and services, business processes, organizational structures, business models, and collaborative approaches. This process aims to assist enterprises in generating and acquiring greater value [

15,

16,

17]. Throughout this journey, enterprises rely heavily on various digital technologies to reduce costs, enhance operational efficiency, and boost competitiveness, thereby achieving energy conservation and emission reduction [

54].

According to traditional enterprise theory, the primary goal of firms is to maximize profits and the value of shareholders [

55]. However, modern corporate governance theory and stakeholder theory suggest that enterprises should not only be responsible for shareholders, but also take active steps to fulfill their responsibilities towards creditors, the government, and the environment, in order to maximize the overall interests of stakeholders [

56]. Despite the strong externalities associated with environmental protection practices and carbon emission reduction measures in enterprises, there is a significant lack of motivation for firms to pursue such initiatives. On the one hand, excessive investment in environmental protection would increase corporate expenditures, decrease corporate profitability, and harm the interests of shareholders. On the other hand, enterprises may encounter challenges such as resource limitations, technological constraints, informational constraints, and a shortage of talent, resulting in high costs for reducing carbon emissions and a limited capacity to carry out such measures. With the emergence of new digital technologies, enterprises now have the opportunity to reverse this trend. By combining digital technology with traditional production methods, enterprises can undergo digital transformation and transform their operations, which will not only increase enterprise value but also provide important support for cleaner production. Firstly, corporate digital transformation may offer energy-saving and emission-reduction technologies [

57], which can positively impact their ability to reduce carbon emissions. Secondly, digital technology applications can improve the allocation of production factors such as human and material capital, and enhance internal control within enterprises [

58], thereby reducing the cost of reducing carbon emissions. Finally, digital transformation offers a convenient way for enterprises to access production, technical, and market information, reducing the negative effects of information asymmetry [

59] and lowering transaction costs, thereby enhancing corporate governance and improving carbon performance. Based on the aforementioned analysis, we postulate the first research hypothesis.

Hypothesis 1 (H1). Digital transformation is beneficial for corporate carbon emissions reduction.

In addition to direct impacts, corporate digital transformation may influence carbon emissions through various transmission mechanisms.

One such mechanism is the improvement of energy use efficiency. Chen and Chen [

60] have found that there are significant differences in energy use efficiency among Chinese enterprises due to the scale effect. Small- and medium-sized companies often struggle with low energy efficiency due to outdated technology and equipment, but digital technologies can help improve their energy efficiency. From an energy consumption perspective, digital technology, for one thing, provides a certain technical basis for the promotion of R&D of clean energy, and is beneficial to the promotion and use of clean energy among enterprises [

61]. For another, digital technology enhances the substitution of cleaner energy for traditional fossil energy [

62], empowering the upgrading of the energy consumption structure. From the perspective of energy supply and demand, digital technologies such as cloud computing and big data can improve energy collection efficiency, digitize and optimize energy supply, and enable the more accurate prediction of energy consumption through data monitoring, thus improving energy use efficiency [

63]. Additionally, the usage of digital technology can also enhance the corporate monitoring of energy use processes, leading to a more effective identification and correction of issues. In conclusion, corporate digital transformation can enhance energy use efficiency, which has been shown to directly reduce carbon emissions [

64], enabling enterprises to achieve long-term clean production. As such, it can be argued that improving energy utilization efficiency is a crucial transmission mechanism for corporate digital transformation to reduce carbon emissions.

Second, the promotion effect on enterprises’ financial performance is an effective influence mechanism for digital transformation, helping to reduce corporate carbon emissions. According to the theory of redundant resources, the improvement of corporate financial performance can provide passive resources for corporations shouldering more social responsibility [

65]. Therefore, high-quality financial performance can provide more capital and resources for enterprises to improve carbon performance. Meanwhile, according to natural resources theory, the implementation of environmental strategy and management practice depends on organizational resources and organizational capacity, while organizational redundancy can provide disposable resources for the enhancement of corporate carbon performance [

66]. Therefore, the improvement of corporate financial performance plays a fundamental role in CO

2 abatement. Digital transformation can enhance a company’s financial performance through several channels. Firstly, digital technology can effectively integrate production factors, breaking down information silos between departments and improving production management. Additionally, intelligent data analysis and data-driven decision-making can refine production plans, resulting in improved production efficiency and financial performance [

67]. Thirdly, the application of digital networks also allows companies to receive customer feedback and optimize production, ultimately improving their financial performance [

68]. In conclusion, digital transformation can positively impact a company’s financial performance and, indirectly, reduce its carbon emissions.

The green innovation effect represents another transmission mechanism. Green technology innovation plays a crucial role in mitigating CO

2 emissions [

69]. Both innovations in green technology at the production end and those in the treatment of pollution at end-use contribute directly to reducing corporate carbon emissions [

70]. The digital transformation of enterprises provides a foundation for low-carbon and green technological innovation. First of all, the implementation of digital technology accelerates the digitization, algorithmic modeling, and streamlining of innovation processes, potentially significantly shortening the R&D cycle for low-carbon technology [

61]. Secondly, networking connectivity overcomes the barriers to innovation within enterprises and breaks down the “information barrier” to corporate green innovation, facilitating the exchange of innovation elements and enhancing the low-carbon spillover effects of green innovation. Finally, the use of embedded intelligent devices allows enterprises to continuously monitor energy consumption and pollutant emissions, improve information collection, and control carbon emissions [

71]. Enterprise digital transformation can thus effectively help control carbon emissions through facilitating green technology innovation.

Building upon the preceding analysis, we propose a second hypothesis:

Hypothesis 2 (H2). The digital transformation of corporations can help to decrease corporate carbon emissions by increasing energy usage efficiency, enhancing corporate financial performance, and inducing the green innovation effect.

{kind=link}