4.2. Generalized Method of Moments (GMM) Estimators

When conventional OLS, FE, and RE techniques cannot account for the potential endogeneity problem, economists estimate model parameters using the Generalized Methods of Moments (GMM). GMM estimators use moment conditions derived from the population to evaluate the model’s parameters. These moment conditions are data functions where the population mean is zero.

Because they can deal with various problems, including unobserved heterogeneity, endogeneity, and measurement error, GMM estimators are frequently used in panel data analysis. They are considered more effective than conventional techniques because they estimate the model’s parameters using all of the information in the data, including momentary conditions.

GMM estimators are frequently used in the financial industry to estimate asset pricing models and investigate the correlation between macroeconomic factors and stock returns. When working with financial data that may display non-stationarity, time-varying volatility, and heteroskedasticity, GMM estimators are especially helpful. They enable researchers to consider these variables and estimate the model’s parameters more accurately.

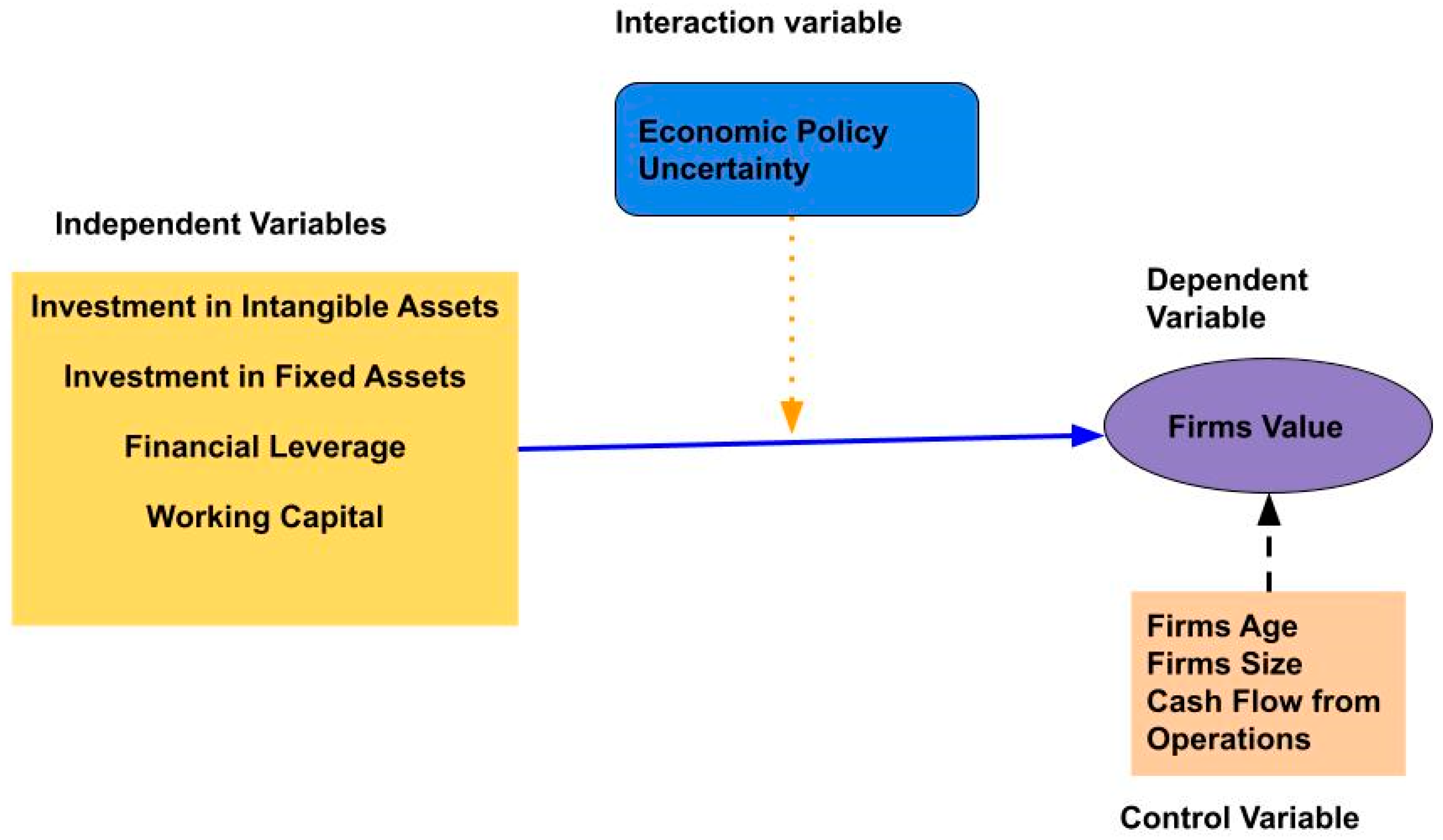

Statistics descriptive: Table 1 offers descriptive statistics for the key variables and an overview of the data utilized in the research. The variables in the data include: IFA (investing in non-moving assets), INTA (investing in intangible assets), FLR (financial leverage ratio), WCR (working capital ratio), EPU (economic policy uncertainty index), FS (firm size), AGE (firm age), CFO (cashflow from operations), Tobin’s Q, and MPPS (market price per share) are some other financial metrics. While WCR is derived by dividing current assets by current liabilities, FLR is computed by dividing total assets by equity. Scott Baker, Nicholas Bloom, and Steven Davis created a gauge of economic policy uncertainty known as the EPU index. AGE, CFO, and FS are all measurements of the age and performance of a corporation, and FS is calculated by taking the logarithm of the total assets. Essential determinants of a company’s financial performance are Tobin’s Q and MPPS. As opposed to MPPS, which is the market price per share of a company’s stock, Tobin’s Q is calculated by dividing the market value of a firm by the cost of replacing its assets. The research seeks to thoroughly understand the link between economic policy uncertainty and company investment behavior by considering these factors.

Additionally, MPPS is calculated by dividing the share price as of the current day by the total number of outstanding shares. We used the natural logarithm approach to standardize the initial annual data. The cash flow is calculated annually by subtracting the net operating cash flow.

The average Tobin’s Q and market price per share values in Pakistani manufacturing companies are 1.411 and 93.513, respectively, representing the income based on shareholder investment. The average financial leverage is 6.766, the average EPU is 95.326 percent, and the average CFO is 0.226 for businesses that want to balance current assets and liabilities. The average INTA value is approximately 6.632. It suggests that very few intangible assets are owned by Pakistani companies, and they have less of a predisposition to hold assets that would swiftly and gradually amortize. While investing in fixed assets indicates a 15.763 mean value. Age is shown to have a mean value of 30.600 across all manufacturing industries. Examining the mean size value, which in this case is 15.783, which indicates a very high correlation between total assets, is the next factor that is particularly appropriate. We can see that some variables have a more comprehensive range of values than others based on the descriptive statistics given in the table. For instance, the maximum value of the variable FL is 195.511, significantly higher than its mean value of 6.766. It implies that the distribution of this variable may contain some extreme values. The variable MPPS is similarly widely dispersed from the mean, as shown by its high standard deviation of 253.211. The range of values for the variable INTA is smaller, with a minimum and maximum value of 6.632 and 18.371, respectively, and a relatively low standard deviation (5.740).

Table 2: INTA and IFA strongly connect with MPPS and Tobin’s Q. The firm performance accounting model will enable meaningful, apparent linkages between macroeconomic indicators such as EPU, Tobin’s Q, and MPPS. Tobin’s Q and MPPS are output-dependent and closely associated with the macroeconomic vector and EPU.

Table 3 and

Table 4 (2.76 and 2.08) show how variance inflation analysis (VIF) handled the variable multicollinearity issue. All values are less than 10, and in all models, the greatest VIF value is linked to the variance influence factor values of 2.76 and 2.08, respectively. The variables’ impacts will not have multicollinearity.

Table 2 shows how much INTA, IFA, FL, and WC affect company success. Further research has shown strong evidence for the association and hypothesis effects in

Table 3.

The yearly financial statement includes fixed assets, intangible assets, and other long-term assets. Capital expenditure measures companies’ fixed asset investments as a percentage of total assets at the start of the fiscal year. The Pakistan Monthly Index of Policy Uncertainty measures economic policy uncertainty. Scott Baker, Nicholas Bloom, and Steven Davis calculated “Measuring Economic Policy Uncertainty”, the EPU index. Net operational cash flow is divided by total assets at the start of the fiscal year. Total debt is divided by total assets one period later to calculate the market value of traded and non-traded shares. A one-period lag leverage ratio is the ratio of total debt to total assets. Size is the current total asset’s natural logarithm.

The correlation matrix was examined to see whether economic policy uncertainty negatively affected company investment. Economic policy uncertainty affects firm investment. Corporate investment tends to drop when economic policy is unclear.

Table 2 shows relevant variable correlation coefficients. As shown, Tobin’s Q and investments in physical and intangible assets (0.410; 0.433) and firms’ size and intangible assets (0.517; 0.866) are the only significant correlations. Corporate investment correlates positively with other factors but negatively with the CFO’s measure of economic policy uncertainty.

EPU negatively correlates with Tobin’s Q, intangible assets, and fixed assets. The variance inflation factor (VIF) tests regression analysis for multicollinearity. Both leaner models (below 10) had VIFs of 2.76 and 2.08, indicating no multicollinearity.

Real options theory is used practically by examining how different factors affect a firm’s Tobin’s Q, which calculates the market value of a company’s assets based on their replacement cost. The following factors were considered in this analysis: MPPS, IntA, IFA, FL, WC, EPU, age, size, and CFO. According to this study, MPPS significantly improves Tobin’s Q. This implies that businesses that make new investments or increase their operational capacity frequently enjoy greater market value. Tobin’s Q is positively influenced by IntA, age, size, and CFO, suggesting that investors often value bigger, older companies with better financial performance.

On the other hand, IFA, FL, and EPU negatively impact Tobin’s Q. According to this, elements including significant financial debt, an unclear economic outlook, and a lack of investment in fixed assets may affect a company’s market value. Overall, the analysis’s findings emphasize the significance of considering natural choices when making investment decisions and the possible effects that outside influences may have on a company’s value. Firms may more accurately determine the future value of their assets and make better investment choices by adding real options theory into their decision-making processes.

Table 5 also reports several diagnostic tests commonly used to evaluate the model’s validity. We used several tests to assess errors in the model’s specification, including the B&P LM test, the Hausman test, the heteroskedasticity test, the autocorrelation test, and the VIF test. In contrast, the Sargan and Hansen tests test the validity of the instruments used in the GMM estimation. The AR1 and AR2 tests test for autocorrelation in the model’s residuals. The threshold is that the problem is not present in the model if its value is significant. In this model, the dependent variable is Tobin’s Q, a financial metric used to measure a firm’s market value relative to its assets. The model includes nine independent variables: IntA, IFA, FL, WC, EPU, age, size, CFO, and a constant term. Model GMM is a regression model estimated using the Generalized Method of Moments (GMM) estimation technique. GMM is a popular econometric method used to estimate a model’s parameters when the assumptions of ordinary least squares (OLS) or fixed effects (FE) regression models are violated.

We applied both static and dynamic statistical models in this research. Ultimately Our baseline regression equation is based on research investments in intangible assets, investments in fixed assets, and working capital [

43,

44]. We observed how much focus financial managers have on financial leverage and decisions regarding the use of internal funds or external sources and found that it has a negative relationship with Tobin’s Q, which means the usage of internal funds is supportive as compared with debts. We lag Tobin’s Q and MPPS variable by one period, following [

45,

46]. The following is the central equation in Model 4, the primary model for our upcoming empirical discussion. In

Table 3,

Table 4,

Table 5 and

Table 6, our major focus will be Model Four.

where MPPS

it is the market price per share and Tobin’s Q

it, a firm’s market performance indicator, are used. INTA

it represents intangible value at the end of each year, FL

it represents leverage ratio in the previous period, WC

it represents current assets to current liabilities during the last period, EPU

it represents uncertainty in economic policies in each period, CFO

it represents cash flow, Firm size

it represents firm size, which is sales revenue scaled by assets, and Firm age

it represents firm age. We hypothesize that businesses spend less on tangible and intangible assets when economic policy uncertainty is high. This anticipation is predicated on the idea that uncertainty breeds risk aversion and postpones investment choices. We estimated a regression model using our dataset to test our hypothesis, and the results are shown in

Table 6.

Based on the empirical findings, we determine that Model 4, in

Table 7 and

Table 8 which contains a lag-dependent variable, is the best specification for our research. We interpret the results in light of the significant coefficients produced by the GMM system model. Economic policy uncertainty, our main factor of interest, is proven to have a significant detrimental impact on company investment in both tangible and intangible assets. This result implies that enterprises are less inclined to invest in assets with long-term advantages when uncertainty is high, maybe due to the option value of delaying investments in uncertain situations. This outcome is consistent with the idea that investments are irreversible [

47].

Additionally, we expand Model 4 to include age, size, and CFO as three control variables. These variables are designed to measure how business characteristics affect investment choices. Our results indicate that economic policy uncertainty significantly influences corporate investment choices in tangible and intangible assets, even after adjusting for other firm-specific factors.

The finding is consistent with the principle of irreversibility in investments and the expected benefit of postponing investments, e.g., [

48]. We extend Model (4) to include the three control variables age, size, and CFO. The results demonstrate that, despite the sizeable and favorable impacts of economic policy uncertainty, cash flow from operations, age, and business size all have a large negative effect on Tobin’s Q. Therefore, our first hypothesis is not supported. It suggests that enterprises involved in Pakistani manufacturing are not focusing on external macroeconomic uncertainty when developing their plans to invest in fixed or intangible assets because of the uncertain economic policy climate. We employed interaction terms in Model 4 of

Table 5 when Tobin’s Q is our dependent variable. In the open discussion, we will focus on

Table 4’s finding Model 4 in the last column.

Real options theory is a financial theory that enables businesses to choose their strategic investments based on their possible future worth. It tries to estimate the investment’s worth considering its ambiguity and flexibility. In this situation, the GMM model examines how real option theory is used to make business investment choices. Tobin’s Q, a measurement of the market value of a firm’s assets relative to their replacement cost, is a component of the model. Additional factors that affect a company’s financial and operational success include IntA, IFA, FL, WC, EPU, age, size, and CFO.

Each variable’s influence on the firm’s investment choice is represented by a set of coefficients in the model, some of which are statistically significant while others are not. The EPUIFA, EPUINTA, EPUFL, and EPUWC coefficients show how the company’s economic policy uncertainty (EPU) interacts with each of the other variables. Diagnostic tests, including the Sargan test, Hansen test, and AR1 and AR2 tests, are utilized to guarantee the validity and correctness of the model. These tests look for problems, including heteroscedasticity, autocorrelation, and endogeneity. This model, among others, applies real options theory in this situation to examine investment choices and estimate their prospective worth in light of hazy future developments.

Tobin’s Q, which gauges a company’s market value, and the number of independent variables are estimated using GMM in this model. Here is a basic explanation of how Tobin’s Q relates to each independent variable. When discussing investment in intangible assets, the coefficient is positive and statistically significant. It reveals that companies with larger intangible asset investments have higher Tobin’s Qs. It could be because intangible assets, such as patents and trademarks, can give businesses a competitive edge and raise their market value. The statistically significant positive coefficient indicates that enterprises with more fixed asset investments have higher Tobin’s Qs. It can be the case since investing in fixed assets can increase a company’s capacity for output and competitiveness, raising its market value. Financial leverage has a positive, statistically significant coefficient, meaning that businesses with more financial leverage and more debt compared with equity have a positive association with Tobin’s Q and are more valuable.

If the firm can provide a return on investment greater than the cost of its debt, then increased leverage may result in better returns for equity investors. The positive and statistically significant working capital ratio coefficient shows that businesses with a greater working capital ratio of more current assets than current liabilities tend to have higher Tobin’s Qs. It could be the case because investors may perceive a firm favorably if it has a greater working capital ratio as a sign that it has more liquidity and is better equipped to satisfy its short-term commitments. A greater Tobin’s Q is often seen with businesses functioning in an environment with more uncertain economic policy, according to the positive and statistically significant uncertainty coefficient. It can seem illogical to do this. However, investors may reward firms that can navigate and adapt to ambiguous economic situations. Because the age coefficient is statistically significant and negative, it shows that older businesses often have a lower Tobin’s Q. Younger businesses may have more development potential and are seen as more inventive and energetic, which might account for this. The positive and statistically significant size coefficient shows that bigger businesses often have a greater Tobin’s Q. The size, operating cash flow, and unpredictability of economic policy are a few variables that affect a company’s share price in the market. Market valuations are often higher for bigger, more powerful firms. Furthermore, companies with greater cash flow from operations often have higher market values because they may reinvest their gains into the business or pay them to shareholders.

Economic policy uncertainty affects the link between each independent variable and Tobin’s Q, a metric of a company’s market value in proportion to its assets. The interaction terms EPUIFA, EPUINTA, EPUFL, and EPUWC describe this connection. The negative coefficients of these components show the weakening of the positive association between each independent variable and Tobin’s Q when economic policy uncertainty is high. It shows that the unpredictability of economic policy may moderate the link between these variables and Tobin’s Q.

Depending on their financial status and limits, various enterprises may be impacted differently by economic policy uncertainty. According to our data, companies with higher Tobin’s Q scores, greater internal financing capacity, and non-state ownership are less likely to be adversely affected by uncertain economic conditions when making investment choices. These businesses could be better equipped to manage unpredictable times and keep making investments in their assets. Following [

48,

49], we make the following adjustments to our original regression equation to account for interaction terms:

When estimating the parameters in Equation (1), the Generalized Method of Moments (GMM) method considers any possible unmeasured error factors or endogeneity of the model’s explanatory variables. In the middle of the 1990s, refs. [

49,

50] created the GMM estimate technique. The GMM technique combines equations at the level for which lagging variances of endogenous constructs are utilized as instruments with equations at the first difference that employ lagging levels of endogenous constructs as instruments. The endogenous variables in this research are INTA

it, IFA

it, FL

it, and WC

it, as well as the terms that govern their interactions with EPU

it. Cash flows from operations and economic policy uncertainties are further factors. A series of instruments are used with delays starting from the second on the back for the first-difference equations and with lag 2 in the levels equation to handle the potential of delayed impacts of economic policy shocks on the real economy. The Sargan–Hansen test of over-identifying constraints is used to assess the validity of instruments. The squared correlation between the dependent variable’s actual and anticipated values is the goodness-of-fit metric.

The error term is examined for potential autocorrelation problems using the Lagrange multiplier test. We use the [

51] STATA system GMM estimation tool, xtabond2, for econometric estimation. Model 4 generates the GMM estimate when the general interaction effect of economic policy uncertainty is considered, as shown in

Table 5. The delayed Tobin’s Q shows that Sargan–Hansen tests do not challenge the validity of over-identifying limitations; all anticipated variables have extremely significant signals that make intuitive sense. However, Lagrange multiplier tests for second-order correlation in the error component cannot disprove the null hypothesis that there is no autocorrelation in empirical models. The model seems to have great potential for explanatory power based on the goodness-of-fit statistics produced from the inverse correlation between the actual and anticipated values of Tobin’s Q. The linearity terms included in the model make sure that missing variables are not to blame for the substantial model and relative significance of an interaction effect. The result shows that the relationship between Tobin’s Q and investment in tangible and intangible assets increases when firm-level uncertainty rises [

52].

A rise in investment in intangible assets is linked to an increase in MPPS, according to the positive and statistically significant coefficient for IntA. It implies that investors may believe businesses with stronger intangible asset investments (such as patents or intellectual property) have more growth potential and long-term profitability. A rise in investment in fixed assets is linked to a drop in MPPS, according to the negative and statistically significant IFA coefficient. Investors could assume that businesses with larger fixed asset investments are less effective or quick to adjust to shifting market circumstances. As shown by the negative and statistically significant coefficient for FL, higher levels of financial leverage are linked to lower MPPS. Investors can interpret this to mean that more leverage raises the possibility of economic difficulty or insolvency. The working capital coefficient is negative and weakly significant, showing that a lower MPPS correlates with a greater working capital ratio (current assets minus current liabilities). Investors could assume that businesses with greater working capital are less adept at managing their cash flow or inventories. Greater degrees of economic policy uncertainty are linked to greater MPPS, according to the positive and statistically significant coefficient for EPU. Investors may believe that uncertainty increases the likelihood of future gains or expansion prospects. The statistically significant negative age coefficient shows that older enterprises have lower MPPS than younger ones. It may imply that investors think more innovatively or with more growth potential about younger companies. Larger enterprises have greater MPPS than smaller firms, according to the positive and statistically significant size coefficient, which is positive. It can imply that investors believe bigger companies are more diversified or have more dependable cash flows.

CFO: The statistically significant negative coefficient for CFO shows that lower MPPS are connected with greater cash flow from operations. It can imply that investors think the company is not investing enough in successful ideas if its cash reserves are large. The coefficients for these four interaction terms, EPUIFA, EPUINTA, EPUFL, and EPUWC, are negative and statistically significant, demonstrating that levels of economic policy uncertainty mitigate the impacts of IFA, IntA, FL, and WPS on MPPS. The negative coefficient for each interaction term indicates that the negative effects of IFA, IntA, FL, and WPS on MPPS are less pronounced at times of significant economic policy uncertainty. It could imply that during difficult times, investors consider businesses with substantial investments in fixed or intangible assets or high levels of financial leverage less hazardous, potentially due to these businesses’ higher physical assets or more diversification. Similarly, the positive coefficient for EPU indicates that high levels of uncertainty may boost the possibility of growth, which may partially counteract the negative consequences of excessive financial leverage or investment in fixed or intangible assets.

The shown models illustrate the effects of different independent factors on the dependent variables of Tobin’s Q and market price per share. The research discovered substantial positive connections between Tobin’s Q and IFA, FL, WC, EPU, and size. Tobin’s Q, on the other hand, was negatively impacted by age, showing that older businesses had lower market values. IntA, EPU, and size were shown to have a positive link with market price per share, whereas IFA, WC, and CFO had a negative relationship. FL had hardly any impact on MPPS. It is important to highlight that the findings may not generalize to other situations since they depend on the particular dataset and model parameters utilized in the research.

Overall, the findings suggest that various factors, including a firm’s investment in fixed and intangible assets, financial leverage, working capital, economic policy uncertainty, and firm size, can influence a firm’s market valuation.

According to the results of the Generalized Method of Moments (GMM) analysis, the variables MPPS (market price per share), IntA (investment in fixed assets), IFA (investment in fixed assets), FL (firm leverage), WC (working capital), EPU (economic policy uncertainty), age, size, and CFO (cash flow from operations) are significant determinants of firm value. These variables influence businesses’ real option value in the real option theory setting. For instance, companies with high MPPS may have more latitude to postpone investment choices since they have a larger value of actual options. Similarly, businesses with high levels of cash flow from operations (CFO) could better adapt their investment plans to changes in the macroeconomic environment. The findings imply that a considerable impact on company value is caused by the interplay between EPU and certain firm-specific characteristics, including IFA, IntA, FL, and WC. It is suggested that the effect of EPU on company value depends on the unique traits of the business and the worth of its actual choices. These results may aid businesses in making investment choices in hazy economic climates. Firms may choose the best time to invest, the amount to invest, and the investment strategy by knowing the variables that impact the value of their real choices. Moreover, companies may more accurately analyze the influence of EPU on their investment choices and modify their strategies as necessary by considering the interplay between EPU and firm-specific variables.

The stock market price of a company is the dependent variable in this research. The shift in economic policy uncertainty from positive to negative is estimated using the market price per share shock (MPPS) lag. Economic policy irrationality impacts this connection, which has a positive and statistically significant coefficient for the lag-dependent variable. The importance of other coefficient estimates is mostly unaffected by the interaction term and the lack of a change in economic policy uncertainty.

The effect of uncertain economic policy on a firm’s investment in physical and intangible assets, financial leverage, and working capital is examined in Column 4 of

Table 6. This column contains “company stock market price volatility” and “economic policy uncertainty.” The EPUINTA and EPUWC interaction variables are negative in Column 4 of the system GMM regression equation, suggesting a negative impact on businesses’ short- and long-term investment choices. Column 4’s significance threshold is set at 1%.

The lag-dependent variable MPPS’s positive and significant coefficient estimates align with what we anticipated. Given that all coefficients are effective at the 1% level, we utilized the system GMM model in Column 4 to conclude that economic policy uncertainty moderates the variables. Our research suggests that, in addition to the influence of policy shocks, individual business uncertainty, such as stock price volatility, influences company-level investment choices. It is consistent with the real alternatives hypothesis, which holds that when faced with uncertainty, firms are more likely to postpone investment and production [

53]. When intrinsic uncertainty increases, businesses are more susceptible to negative extrinsic economic policy shocks.

The share market price of a company is a key metric for assessing its success in the world of finance. A GMM regression analysis result is shown in

Table 6, which reveals the correlation between MPPS, the dependent variable, and several independent variables. The table contains a wealth of data that may aid analysts and investors in making wise choices.

The degree of confidence in the findings is indicated by the numbers in parenthesis next to the coefficient estimations. As we go down the rows, we can see that certain factors influence MPPS positively while others have a negative impact. When an independent factor changes, the coefficients indicate how much the share market price is expected to vary.

By closely reviewing the findings, we may find patterns and insights that are not immediately obvious. For instance, we may see that a firm’s investment in physical and intangible assets, financial leverage, and working capital are negatively impacted by economic policy’s unpredictability. It shows that firms are more cautious in their investment decisions when the policy climate is unclear.

Table 6 comprehensively examines the intricate world of money and economics. Anyone trying to make wise selections in investing and corporate finance may benefit from the insights included in it.

The findings demonstrate a high positive correlation between Tobin’s Q Lag value and MPPS, with a coefficient estimate of 0.998 and a standard error of 0.0896. It implies that businesses with a high Tobin’s Q also often have high MPPS [

54]. With a coefficient estimate of 29.23 and a standard error of 12.02, IntA likewise exhibits a favorable connection with MPPS. It implies that businesses with significant intangible assets also have significant MPPS. With a coefficient estimate of −54.52 and a standard error of 67.31, IFA has a bad connection with MPPS. It implies that businesses with substantial financial asset investments often have low MPPS. With a coefficient estimate of −1.348 and a standard error of 4.959, FL has a bad connection with MPPS. It implies that businesses with significant financial leverage often have poor MPPS. With a coefficient estimate of 0.731 and a standard error of 2.924, WC shows a favorable connection with MPPS. It implies that businesses with large working capital have higher MPPS levels. With a coefficient estimate of −4.745 and a standard error of 4.261, EPU has a bad connection with MPPS. It implies that businesses that operate in highly unpredictable environments often have low MPPS. With a coefficient estimate of 15.58 and a standard error of 11.91, age positively correlates with MPPS. It implies that older businesses often have higher MPPS. With a coefficient estimate of 4.975 and a standard error of 8.840, size positively correlates with MPPS. It means that bigger firms often have higher MPPS. With a coefficient estimate of −7.098 and a standard error of 14.95, the CFO has a poor connection with MPPS. According to this, companies with insufficient cash flows often have low MPPS.

The outcomes also demonstrate a positive relationship between MPPS and the interaction between EPU and IFA, with an estimated coefficient of 0.275 and a standard error of 0.286. It suggests that firms operating in a high-uncertainty environment with high investments in financial assets tend to have high MPPS. Similarly, the interaction between EPU and INTA has a negative relationship with MPPS, with a coefficient estimate of −0.0572 and a standard error of 0.122. It suggests that firms operating in highly uncertain environments with high intangible assets tend to have low MPPS. The interaction between EPU and FL has a positive relationship with MPPS, with a coefficient estimate of 0.00907 and a standard error of 0.0422. It suggests that firms operating in a high-uncertainty environment with high financial leverage tend to have high MPPS.

Finally, the interaction between EPU and WC has a negative relationship with MPPS, with a coefficient estimate of −0.0111 and a standard error of 0.0306. It suggests that firms operating in a high-uncertainty environment with high working capital tend to have low MPPS.

Overall, the results of the GMM analysis provide insights into the relationship between various independent variables and MPPS. The findings suggest that Tobin’s Q, intangible assets, working capital, age, and size have positive relationships with MPPS, while financial assets, financial leverage,

The findings of a GMM regression study that looked at the correlation between the dependent variable MPPS and several independent factors are shown in

Table 6. In parenthesis, the table gives the coefficient estimates and the accompanying standard errors. These coefficients show the magnitude and axis of the link between the independent and dependent variables. The analysis’s findings indicate that several different factors and MPPS are significantly correlated. While FL and EPU have negative relationships with MPPS, IntA, size, and WC have favorable relationships with them. Additionally, only the IFA coefficient is significant, whereas the age, CFO, and IFA coefficients are all negative.

Additionally, the significant interactions between EPU, IFA, INTA, FL, and WC indicate that the values of IFA, INTA, FL, and WC affect the link between EPU and MPPS. These findings suggest that IntA, size, and WC favorably impact MPPS, whereas FL and EPU are adversely impacted. However, given that these results are based on a particular dataset and model, it is crucial to use care when extrapolating them to other scenarios.

These findings emphasize the need to consider various variables when examining how uncertainty in economic policy affects MPPS. According to the results, businesses may be more likely to keep more working capital and invest in physical and intangible assets when there is less economic policy uncertainty. On the other hand, high levels of economic policy uncertainty may cause businesses to lower their financial leverage and put off making investment choices. The impact of interactions between EPU and other independent variables shows how complicated this connection is and how important it is to grasp the variables at work thoroughly. By closely reviewing the findings, we may find patterns and insights that are not immediately obvious. For instance, we may see that a firm’s investment in physical and intangible assets, financial leverage, and working capital are negatively impacted by economic policy’s unpredictability. It shows that firms are more cautious in their investment decisions when the policy climate is unclear.

Table 6 comprehensively examines the intricate world of money and economics. Anyone trying to make wise selections in investing and corporate finance may benefit from the insights included in it.

,

,

{kind=link}

{kind=link}

{kind=link}