A Sustainable Development Evaluation Framework for Chinese Electricity Enterprises Based on SDG and ESG Coupling

Abstract

1. Introduction

2. Literature Review

2.1. Corporate Sustainability Performance Evaluation

2.2. Application of ESG in Corporate Sustainability

2.3. ESG Integration with Sustainable Development Goals (SDG)

3. Methods

3.1. Framework Design Principles and Structure

3.2. Indicator Bank and Indicator Selection

- The GRI guidelines;

- ESG issues and indicators that link ESG concerns to SDGs.

- The number of penalties received by enterprises from regulatory authorities for environmental issues: According to the regulations of the China Securities Regulatory Commission, for enterprises penalized for environmental issues, the number of penalties received and related information must be disclosed in their annual reports. For enterprises that did not disclose such information, we assumed that the number of occurrences of the event was 0.

- The number of occurrences of major equipment accidents (times): According to the regulations of the China Securities Regulatory Commission, for enterprises suffering from major equipment accidents, the number of occurrences and related information must be reported. For enterprises that did not disclose information on this indicator, we assumed that the number of major equipment accidents was 0.

- The number of patents granted per capita (items/person): For enterprises that did not disclose the annual number of patents granted, we assumed that the number of patents granted per capita for the year was 0.

3.3. Corporate Sustainability Index Calculation

3.3.1. Determination of Indicator Thresholds

- The optimal value that can be achieved in the enterprise’s achievement of sustainable development, for example, 100% comprehensive utilization rate of fly ash in thermal power generation, 100% recycling and reuse rate of water and water extraction, 100% coverage rate of work-related injury insurance, and a number of occupational health and safety accidents equal to 0.

- If the indicators are in line with the international context and the best-performing enterprises in China are also far behind the international level, the indicator values of the best-performing international enterprises were used.

- For all other indicators in the base indicator pool, the average of the data of the three best-performing enterprises in the observed sample were used.

3.3.2. Normalization Process

3.3.3. Weight Setting

3.3.4. Aggregate Evaluation

3.4. Power Company Sustainability Dashboard

3.5. Data and Samples

4. Results

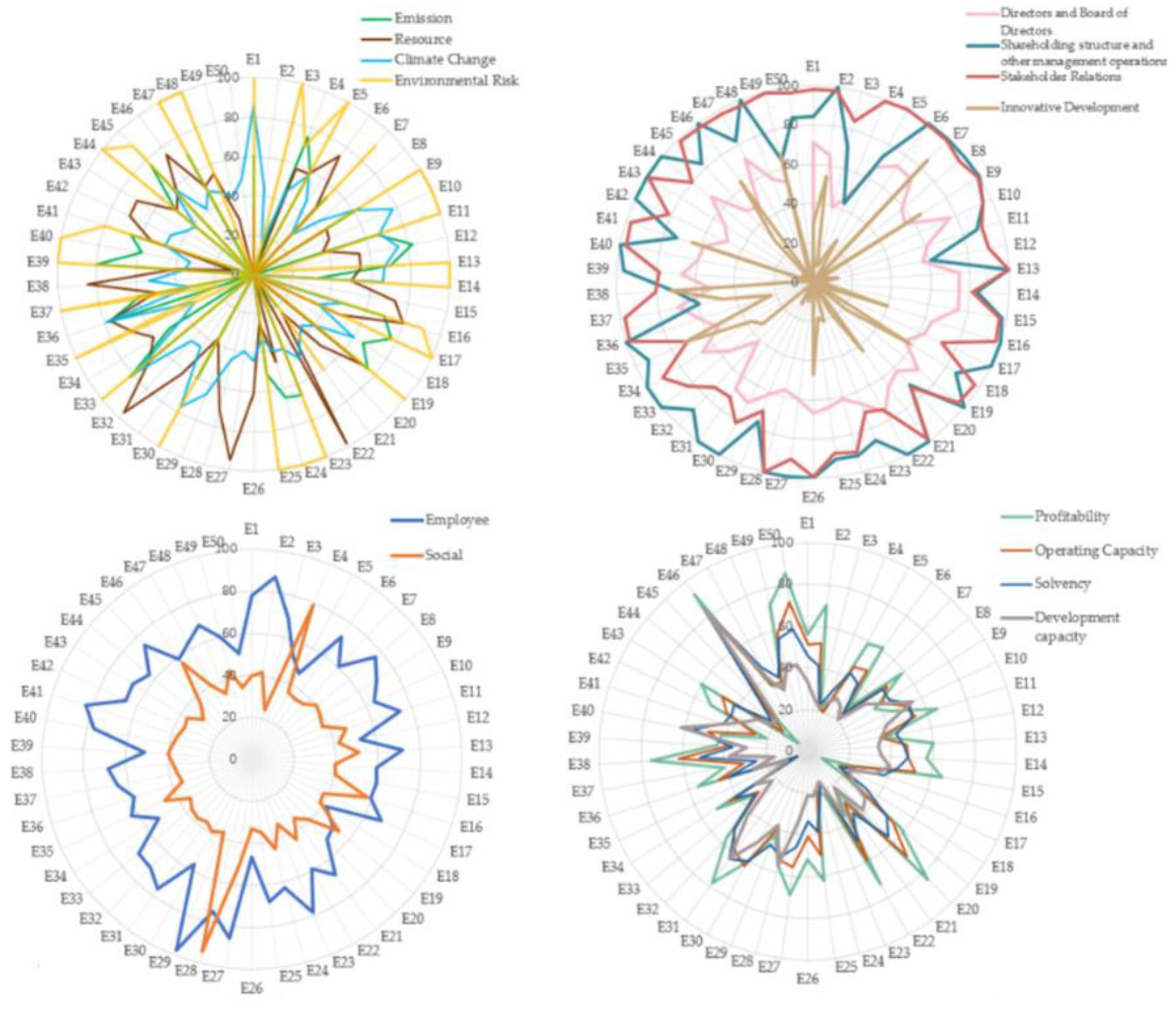

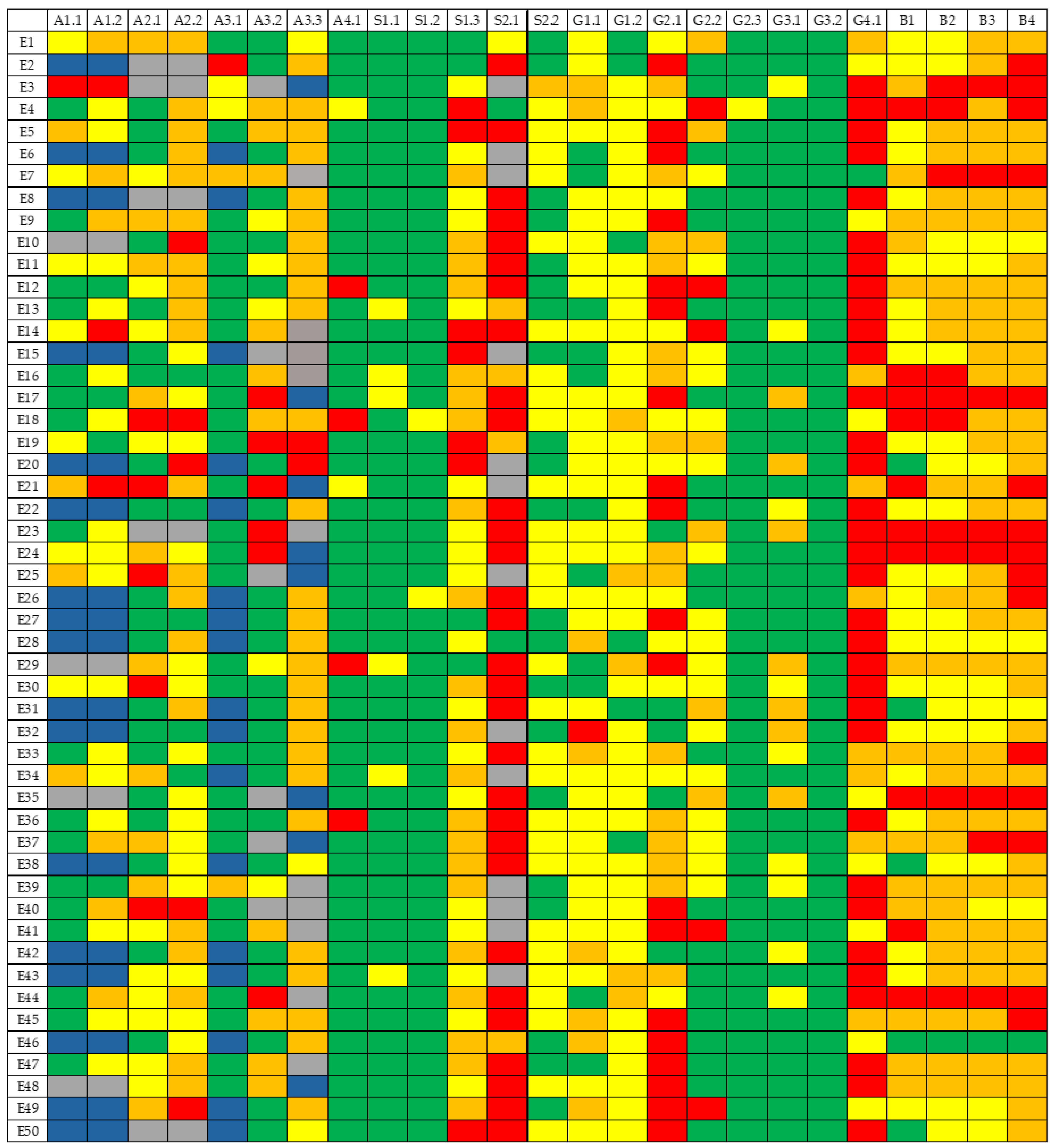

4.1. Sustainable Information Disclosure

4.2. Corporate Sustainability Performance

4.3. Corporate Sustainability Index and Dashboard

5. Discussion

5.1. Collinearity/Redundancy Analysis

5.2. Sensitivity Analysis

5.3. Analysis of Performance Causes

6. Conclusions

- A sustainable development evaluation index system for the power generation industry, consisting of a dimensional layer, an issue layer, a standard layer, and an indicator layer, was constructed. In order to comprehensively and systematically evaluate the sustainable development level of the power generation industry, an evaluation index system of 75 indicators was constructed with respect to four dimensions: economic, environmental, governance, and social. Compliance indicators were also used to eliminate companies that had no will to achieve sustainable development.

- The status of sustainability disclosure in China’s electric power industry was analyzed. Overall, Chinese power companies need to improve their environmental, social, and governance disclosures. At the dimensional level, the environmental dimension showed the severest lack of information, with a missing rate of 17.38%. The disclosure of the social dimension was better, but companies should still focus on quantitative information disclosure related to employee issues (missing rate: 30.93%) and rural revitalization (missing rate: 24.00%). In terms of corporate governance, enterprises should strengthen the information disclosure of innovation investment and achievements; the completeness of indicators under the economic dimension reached over 99%. Regulators can set stricter disclosure regulations to enhance corporate information disclosure. Enterprises should increase investor participation and enhance the degree to which the profound notion of corporate sustainability through high corporate governance levels is understood in order to promote the improvement of corporate disclosure.

- Considering the target of the sustainable development of electric power enterprises, a sustainable development evaluation index and indicator board for China’s electric power industry were established by drawing on the practical exploration and typical experience of SDG progress assessment. Economic sustainability is the dimension that Chinese power enterprises need to pay special attention to. Innovation investment, resource saving, and social welfare level constrain the overall sustainability level of China’s electric power industry. In conjunction with the results of this research, companies have actively disclosed the schemes of their environmental protection business, increased investment in environmental protection, vigorously promoted the transformation of low-carbon clean energy, and increased their low-carbon clean energy share. At the same time, companies should accelerate the modernization of the governance system and governance capacity and promote the soundness of the modern enterprise system, the rule of law, and risk control systems.

- A robustness analysis was conducted on the framework system established in this paper. Firstly, an independence analysis was conducted for the selection of sustainable development topics, and the results showed that there was no significant correlation between the dimensions of the framework established in this paper and the topics. Second, the sensitivity of the framework was verified. Through running Monte Carlo (MC) simulations to assign different weighting schemes to the indicators, the results showed that the evaluation framework established in this study had good stability.

- Although this framework used 75 indicators in four dimensions, namely, environmental, social, governance, and economic, some of the more important indicators for sustainable development were not selected due to the availability of indicators, such as water use and conservation, wastewater discharge, land use and conservation, other energy (e.g., oil) consumption indicators, carbon emission identification and measurement, green office indicators, species diversity conservation, etc. A more comprehensive evaluation of corporate sustainability would be based on a deeper understanding of sustainability and the more comprehensive disclosure of sustainability information. This paper only analyzed the sustainability performance in 2021; sustainability performance in previous years was not studied, and a future trend analysis could be conducted on sustainability performance in recent years.

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Acknowledgments

Conflicts of Interest

Appendix A

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Company Name | Power Generation Type | Company Code |

|---|---|---|

| GUANGDONG BAOLIHUA NEW ENERGY STOCK CO., LTD. | Integrated power generation | E1 |

| SICHUAN CHUANTOU ENERGY CO., LTD. | Clean energy generation | E2 |

| DALIAN THERMAL POWER CO., LTD. | Thermal power generation | E3 |

| DATANGINTERNATIONALPOWERGENERATIONCO., LTD. | Integrated power generation | E4 |

| FUJIAN FUNENG CO., LTD. | Integrated power generation | E5 |

| GEPIC ENERGY DEVELOPMENT CO., LTD. | Clean energy generation | E6 |

| JIANGXI GANNENG CO., LTD. | Integrated power generation | E7 |

| SICHUAN GUANGAN AAAPUBLIC CO., LTD. | Clean energy generation | E8 |

| GUANGZHOU DEVELOPMENT GROUP INCORPORATED. | Integrated power generation | E9 |

| GUANGXI GUIDONG ELECTRIC POWER CO., LTD. | Integrated power generation | E10 |

| GUANGXI GUIGUAN ELECTRIC POWER CO., LTD. | Integrated power generation | E11 |

| GD POWER DEVELOPMENT CO., LTD. | Integrated power generation | E12 |

| SDIC POWER HOLDINGS CO., LTD. | Integrated power generation | E13 |

| HUBEI ENERGY GROUP CO., LTD. | Integrated power generation | E14 |

| HUNAN DEVELOPMENT GROUP CO., LTD. | Clean energy generation | E15 |

| HUADIAN POWER INTERNATIONAL CORPORATION LIMITED. | Integrated power generation | E16 |

| HUADIAN ENERGY COMPANY LIMITED. | Thermal power generation | E17 |

| HUANENG POWER INTERNATIONAL, INC. | Integrated power generation | E18 |

| JILIN ELECTRIC POWER CO., LTD. | Integrated power generation | E19 |

| NINGXIAJIAZE RENEWABLES CORPORATION LIMITED. | Clean energy generation | E20 |

| JOINTO ENERGY INVESTMENT CO., LTD. HEBEI. | Thermal power generation | E21 |

| CECEP WIND-POWER CORPORATION. | Clean energy generation | E22 |

| SHENYANG JINSHAN ENERGY CO., LTD | Integrated power generation | E23 |

| BEIJING JINGNENG POWER CO., LTD. | Thermal power generation | E24 |

| LUENMEIQUANTUMCO., LTD. | Thermal power generation | E25 |

| GUANGDONG MEIYANJIXIANG HYDROPOWER CO., LTD. | Clean energy generation | E26 |

| FUJIAN MINDONG ELECTRIC POWER LIMITED COM. | Clean energy generation | E27 |

| SICHUAN MINGXING ELECTRIC POWER CO., LTD. | Clean energy generation | E28 |

| INNER MONGOLIA MENGDIAN HUANENG THERMAL POWER. | Integrated power generation | E29 |

| NINGBO ENERGY GROUP CO., LTD. | Integrated power generation | E30 |

| GUIZHOU QIANYUAN POWER CO., LTD. | Clean energy generation | E31 |

| CHONGQING THREE GORGES WATER CONSERVANCY AND ELECTRIC POWER CO., LTD. | Clean energy generation | E32 |

| SHANGHAI ELECTRIC POWER CO., LTD. | Integrated power generation | E33 |

| GUANGDONG SHAONENG GROUP CO., LTD. | Integrated power generation | E34 |

| SHENZHEN NANSHAN POWER CO., LTD. | Thermal power generation | E35 |

| SHENZHEN ENERGY GROUP CO., LTD. | Integrated power generation | E36 |

| GUANGZHOU HENGYUN ENTERPRISES HOLDING LTD. | Thermal power generation | E37 |

| CECEP SOLAR ENERGY CO., LTD. | Clean energy generation | E38 |

| XINJIANG TIANFU ENERGY CO., LTD. | Integrated power generation | E39 |

| TOP ENERGY COMPANY LTD. SHANXI. | Thermal power generation | E40 |

| AN HUI WENERGY COMPANY LIMITED. | Thermal power generation | E41 |

| SICHUAN XICHANG ELECTRIC POWER CO., LTD. | Clean energy generation | E42 |

| NING XIA YIN XING ENERGY CO.LTD. | Clean energy generation | E43 |

| HENAN YUNENG HOLDINGS CO., LTD. | Integrated power generation | E44 |

| GUANGDONG ELECTRIC POWER DEVELOPMENT CO., LTD. | Integrated power generation | E45 |

| CHINA YANGTZE POWER CO., LTD. | Clean energy generation | E46 |

| CHN ENERGY CHANGYUAN ELECTRIC POWER CO., LTD. | Integrated power generation | E47 |

| ZHEJIANG ZHENENG ELECTRIC POWER CO., LTD. | Thermal power generation | E48 |

| CHINA NATIONAL NUCLEAR POWER CO., LTD. | Clean energy generation | E49 |

| ZHONGMIN ENERGY CO., LTD. | Clean energy generation | E50 |

References

- Sun, L.; Cui, H.; Ge, Q. Will China Achieve Its 2060 Carbon Neutral Commitment from the Provincial Perspective? Adv. Clim. Chang. Res. 2022, 13, 169–178. [Google Scholar] [CrossRef]

- Qi, L.; Lin, X.; Shi, X.; Zhang, Y.; Pan, H.; Sharp, B. Feed-in Tariffs and the Carbon Emission Trading Scheme under China’s Peak Emission Target: A Dynamic CGE Analysis for the Development of Renewable Electricity. J. Environ. Manag. 2023, 335, 117535. [Google Scholar] [CrossRef]

- Qazi, U.; Jahanzaib, M. An Integrated Sectoral Framework for the Development of Sustainable Power Sector in Pakistan. Energy Rep. 2018, 4, 376–392. [Google Scholar] [CrossRef]

- Li, T.-T.; Wang, K.; Sueyoshi, T.; Wang, D.D. ESG: Research Progress and Future Prospects. Sustainability 2021, 13, 11663. [Google Scholar] [CrossRef]

- Tamimi, N.; Sebastianelli, R. Transparency among S&P 500 Companies: An Analysis of ESG Disclosure Scores. Manag. Decis. 2017, 55, 1660–1680. [Google Scholar]

- Plastun, A.; Bouri, E.; Gupta, R.; Ji, Q. Price Effects after One-Day Abnormal Returns in Developed and Emerging Markets: ESG versus Traditional Indices. North Am. J. Econ. Financ. 2022, 59, 101572. [Google Scholar]

- Gibson Brandon, R.; Krueger, P.; Schmidt, P.S. ESG Rating Disagreement and Stock Returns. Financ. Anal. J. 2021, 77, 104–127. [Google Scholar] [CrossRef]

- Escrig-Olmedo, E.; Fernández-Izquierdo, M.Á.; Ferrero-Ferrero, I.; Rivera-Lirio, J.M.; Muñoz-Torres, M.J. Rating the Raters: Evaluating How ESG Rating Agencies Integrate Sustainability Principles. Sustainability 2019, 11, 915. [Google Scholar] [CrossRef]

- Barnett, M.L.; Salomon, R.M. Beyond Dichotomy: The Curvilinear Relationship between Social Responsibility and Financial Performance. Strateg. Manag. J. 2006, 27, 1101–1122. [Google Scholar]

- Manchiraju, H.; Rajgopal, S. Does Corporate Social Responsibility (CSR) Create Shareholder Value? Evidence from the Indian Companies Act 2013. J. Account. Res. 2017, 55, 1257–1300. [Google Scholar]

- Roblek, V.; Pejić Bach, M.; Meško, M.; Kresal, F. Corporate Social Responsibility and Challenges for Corporate Sustainability in First Part of the 21st Century; Firenze University Press: Florence, Italy, 2019; pp. 31–46. [Google Scholar]

- Antolín-López, R.; Delgado-Ceballos, J.; Montiel, I. Deconstructing Corporate Sustainability: A Comparison of Different Stakeholder Metrics. J. Clean. Prod. 2016, 136, 5–17. [Google Scholar]

- Searcy, C. Updating Corporate Sustainability Performance Measurement Systems. Meas. Bus. Excell. 2011, 15, 44–56. [Google Scholar]

- Pranugrahaning, A.; Donovan, J.D.; Topple, C.; Masli, E.K. Corporate Sustainability Assessments: A Systematic Literature Review and Conceptual Framework. J. Clean. Prod. 2021, 295, 126385. [Google Scholar] [CrossRef]

- San Ong, T.; Teh, B.H.; Ang, Y.W. The Impact of Environmental Improvements on the Financial Performance of Leading Companies Listed in Bursa Malaysia. Int. J. Trade Econ. Financ. 2014, 5, 386. [Google Scholar]

- Olsthoorn, X.; Tyteca, D.; Wehrmeyer, W.; Wagner, M. Environmental Indicators for Business: A Review of the Literature and Standardisation Methods. J. Clean. Prod. 2001, 9, 453–463. [Google Scholar]

- Wartick, S.L.; Cochran, P.L. The Evolution of the Corporate Social Performance Model. Acad. Manag. Rev. 1985, 10, 758–769. [Google Scholar]

- Delmas, M.; Blass, V.D. Measuring Corporate Environmental Performance: The Trade-offs of Sustainability Ratings. Bus. Strategy Environ. 2010, 19, 245–260. [Google Scholar]

- Wood, D.J. Measuring Corporate Social Performance: A Review. Int. J. Manag. Rev. 2010, 12, 50–84. [Google Scholar]

- Schaltegger, S.; Lüdeke-Freund, F.; Hansen, E.G. Business Cases for Sustainability: The Role of Business Model Innovation for Corporate Sustainability. Int. J. Innov. Sustain. Dev. 2012, 6, 95–119. [Google Scholar]

- Delai, I.; Takahashi, S. Sustainability Measurement System: A Reference Model Proposal. Soc. Responsib. J. 2011, 7, 438–471. [Google Scholar]

- Rahdari, A.H.; Rostamy, A.A.A. Designing a General Set of Sustainability Indicators at the Corporate Level. J. Clean. Prod. 2015, 108, 757–771. [Google Scholar]

- Nikolaou, I.E.; Tsalis, T.A.; Evangelinos, K.I. A Framework to Measure Corporate Sustainability Performance: A Strong Sustainability-Based View of Firm. Sustain. Prod. Consum. 2019, 18, 1–18. [Google Scholar] [CrossRef]

- Mayorova, E. Corporate Social Responsibility Disclosure: Evidence from the European Retail Sector. Entrep. Sustain. Issues 2019, 7, 891–905. [Google Scholar] [CrossRef]

- Wang, Y.; Yang, J.; Zhou, M.; Zhang, D.; Song, F.; Dong, F.; Zhu, J.; Liu, L. Evaluating the Sustainability of China’s Power Generation Industry Based on a Matter-Element Extension Model. Util. Policy 2021, 69, 101166. [Google Scholar] [CrossRef]

- Deng, Y.; Zou, S.; You, D. Financial Performance Evaluation of Nuclear Power-Related Enterprises from the Perspective of Sustainability. Environ. Sci. Pollut. Res. 2020, 27, 11349–11363. [Google Scholar] [CrossRef]

- Sarangi, G.K.; Mishra, A.; Chang, Y.; Taghizadeh-Hesary, F. Indian electricity sector, energy security and sustainability: An empirical assessment. Energy Policy 2019, 135, 110964. [Google Scholar] [CrossRef]

- Sartori, S.; Witjes, S.; Campos, L.M.S. Sustainability Performance for Brazilian Electricity Power Industry: An Assessment Integrating Social, Economic and Environmental Issues. Energy Policy 2017, 111, 41–51. [Google Scholar] [CrossRef]

- Bachev, H. Governance of Agrarian Sustainability. Adv. Plants Agric. Res. 2018, 8, 1. [Google Scholar]

- Bosselmann, K.; Engel, R.; Taylor, P. Governance for Sustainability: Issues, Challenges, Successes; IUCN: Gland, Switzerland, 2008; ISBN 2-8317-1105-3. [Google Scholar]

- Simberova, I.; Kocmanova, A.; Nemecek, P. Corporate Governance Performance Measurement–Key Performance Indicators. Econ. Manag. 2012, 17, 1585–1593. [Google Scholar]

- Shanaev, S.; Ghimire, B. When ESG Meets AAA: The Effect of ESG Rating Changes on Stock Returns. Financ. Res. Lett. 2022, 46, 102302. [Google Scholar]

- Eliwa, Y.; Aboud, A.; Saleh, A. ESG Practices and the Cost of Debt: Evidence from EU Countries. Crit. Perspect. Account. 2021, 79, 102097. [Google Scholar]

- Zhang, Q.; Loh, L.; Wu, W. How Do Environmental, Social and Governance Initiatives Affect Innovative Performance for Corporate Sustainability? Sustainability 2020, 12, 3380. [Google Scholar]

- Miralles-Quirós, M.M.; Miralles-Quirós, J.L.; Valente Gonçalves, L.M. The Value Relevance of Environmental, Social, and Governance Performance: The Brazilian Case. Sustainability 2018, 10, 574. [Google Scholar]

- Yoon, B.; Lee, J.H.; Byun, R. Does ESG Performance Enhance Firm Value? Evidence from Korea. Sustainability 2018, 10, 3635. [Google Scholar]

- Gyönyörová, L.; Stachoň, M.; Stašek, D. ESG Ratings: Relevant Information or Misleading Clue? Evidence from the S&P Global 1200. J. Sustain. Financ. Investig. 2021, 1–35. [Google Scholar] [CrossRef]

- Abhayawansa, S.; Tyagi, S. Sustainable Investing: The Black Box of Environmental, Social, and Governance (ESG) Ratings. J. Wealth Manag. 2021, 24, 49–54. [Google Scholar]

- Berg, F.; Koelbel, J.F.; Rigobon, R. Aggregate Confusion: The Divergence of ESG Ratings. Rev. Financ. 2022, 26, 1315–1344. [Google Scholar]

- Escrig-Olmedo, E.; Munoz-Torres, M.J.; Fernandez-Izquierdo, M.A. Socially Responsible Investing: Sustainability Indices, ESG Rating and Information Provider Agencies. Int. J. Sustain. Econ. 2010, 2, 442–461. [Google Scholar]

- Windolph, S.E. Assessing Corporate Sustainability through Ratings: Challenges and Their Causes. J. Environ. Sustain. 2011, 1, 5. [Google Scholar]

- Escrig-Olmedo, E.; Muñoz-Torres, M.J.; Fernández-Izquierdo, M.Á.; Rivera-Lirio, J.M. Measuring Corporate Environmental Performance: A Methodology for Sustainable Development. Bus. Strategy Environ. 2017, 26, 142–162. [Google Scholar]

- Liu, M. Quantitative ESG Disclosure and Divergence of ESG Ratings. Front. Psychol. 2022, 13, 936798. [Google Scholar] [CrossRef]

- O’Riordan, T. The Challenge for Environmentalism. In New Models in Geography; Routledge: Abingdon, UK, 2002; Volume 1, pp. 100–127. ISBN 0-203-40053-4. [Google Scholar]

- Landrum, N.E. Stages of Corporate Sustainability: Integrating the Strong Sustainability Worldview. Organ. Environ. 2018, 31, 287–313. [Google Scholar] [CrossRef]

- Escrig-Olmedo, E.; Rivera-Lirio, J.M.; Muñoz-Torres, M.J.; Fernández-Izquierdo, M.Á. Integrating Multiple ESG Investors’ Preferences into Sustainable Investment: A Fuzzy Multicriteria Methodological Approach. J. Clean. Prod. 2017, 162, 1334–1345. [Google Scholar]

- Rajesh, R. Exploring the Sustainability Performances of Firms Using Environmental, Social, and Governance Scores. J. Clean. Prod. 2020, 247, 119600. [Google Scholar] [CrossRef]

- Jayachandran, S.; Kalaignanam, K.; Eilert, M. Product and Environmental Social Performance: Varying Effect on Firm Performance. Strateg. Manag. J. 2013, 34, 1255–1264. [Google Scholar]

- Chen, Y.-C.; Hung, M.; Wang, Y. The Effect of Mandatory CSR Disclosure on Firm Profitability and Social Externalities: Evidence from China. J. Account. Econ. 2018, 65, 169–190. [Google Scholar]

- Hull, C.E.; Rothenberg, S. Firm Performance: The Interactions of Corporate Social Performance with Innovation and Industry Differentiation. Strateg. Manag. J. 2008, 29, 781–789. [Google Scholar]

- Saraswat, S.K.; Digalwar, A.K. Empirical Investigation and Validation of Sustainability Indicators for the Assessment of Energy Sources in India. Renew. Sustain. Energy Rev. 2021, 145, 111156. [Google Scholar] [CrossRef]

- Desa, U.N. Transforming Our World: The 2030 Agenda for Sustainable Development. J. Public Health Policy 2016, 37, 13–31. [Google Scholar]

- Maia, R.G.T.; Olimpio Pereira Junior, A.; Moreira Pessanha, J.F.; Garcia, K.C. Methodology for Setting Corporate Sustainability Targets. J. Clean. Prod. 2022, 369, 133359. [Google Scholar] [CrossRef]

- Betti, G.; Consolandi, C.; Eccles, R.G. The Relationship between Investor Materiality and the Sustainable Development Goals: A Methodological Framework. Sustainability 2018, 10, 2248. [Google Scholar]

- Consolandi, C.; Phadke, H.; Hawley, J.; Eccles, R.G. Material ESG Outcomes and SDG Externalities: Evaluating the Health Care Sector’s Contribution to the SDGs. Organ. Environ. 2020, 33, 511–533. [Google Scholar]

- Khaled, R.; Ali, H.; Mohamed, E.K.A. The Sustainable Development Goals and Corporate Sustainability Performance: Mapping, Extent and Determinants. J. Clean. Prod. 2021, 311, 127599. [Google Scholar] [CrossRef]

- Phadke, H.; DeMates, L. Investing with the Sustainable Development Goals; White Paper TruValue Labs: San Francisco, CA, USA, 2017. [Google Scholar]

- Nikolaou, I.E.; Kazantzidis, L. Sustainable Consumption Index/Label to Reduce Information Asymmetry among Consumers and Producers. Sustain. Prod. Consum. 2016, 6, 51–61. [Google Scholar]

- Global Reporting Initiative. Linking the SDGs and the GRI Standards; Global Reporting Initiative: Amsterdam, The Netherlands, 2020. [Google Scholar]

- Medel-González, F.; García-Ávila, L.; Acosta-Beltrán, A.; Hernández, C. Measuring and Evaluating Business Sustainability: Development and Application of Corporate Index of Sustainability Performance. In Sustainability Appraisal: Quantitative Methods and Mathematical Techniques for Environmental Performance Evaluation; Springer: Berlin/Heidelberg, Germany, 2013; pp. 33–61. [Google Scholar]

- Ioannou, I.; Serafeim, G. The Consequences of Mandatory Corporate Sustainability Reporting; Harvard Business School Research Working Paper No. 11-100; Oxford University Press: Oxford, UK, 2017; pp. 11–100. [Google Scholar]

- Hediger, W. Reconciling “Weak” and “Strong” Sustainability. Int. J. Soc. Econ. 1999, 26, 1120–1144. [Google Scholar]

- Manrique, S.; Martí-Ballester, C.-P. Analyzing the Effect of Corporate Environmental Performance on Corporate Financial Performance in Developed and Developing Countries. Sustainability 2017, 9, 1957. [Google Scholar]

- Cheng, B.; Ioannou, I.; Serafeim, G. Corporate Social Responsibility and Access to Finance. Strateg. Manag. J. 2014, 35, 1–23. [Google Scholar]

- Alsayegh, M.F.; Abdul Rahman, R.; Homayoun, S. Corporate Economic, Environmental, and Social Sustainability Performance Transformation through ESG Disclosure. Sustainability 2020, 12, 3910. [Google Scholar] [CrossRef]

- Balakrishnan, R.; Sprinkle, G.B.; Williamson, M.G. Contracting Benefits of Corporate Giving: An Experimental Investigation. Account. Rev. 2011, 86, 1887–1907. [Google Scholar]

- Carnahan, S.; Kryscynski, D.; Olson, D. When Does Corporate Social Responsibility Reduce Employee Turnover? Evidence from Attorneys before and after 9/11. Acad. Manag. J. 2017, 60, 1932–1962. [Google Scholar]

- Farooq, O.; Rupp, D.E.; Farooq, M. The Multiple Pathways through Which Internal and External Corporate Social Responsibility Influence Organizational Identification and Multifoci Outcomes: The Moderating Role of Cultural and Social Orientations. Acad. Manag. J. 2017, 60, 954–985. [Google Scholar]

- Brammer, S.; Millington, A. Does It Pay to Be Different? An Analysis of the Relationship between Corporate Social and Financial Performance. Strateg. Manag. J. 2008, 29, 1325–1343. [Google Scholar]

- Hussainey, K.; Salama, A. The Importance of Corporate Environmental Reputation to Investors. J. Appl. Account. Res. 2010, 11, 229–241. [Google Scholar]

- Xie, J.; Nozawa, W.; Yagi, M.; Fujii, H.; Managi, S. Do Environmental, Social, and Governance Activities Improve Corporate Financial Performance? Bus. Strategy Environ. 2019, 28, 286–300. [Google Scholar]

- Ludwig, P.; Sassen, R. Which Internal Corporate Governance Mechanisms Drive Corporate Sustainability? J. Environ. Manag. 2022, 301, 113780. [Google Scholar] [CrossRef]

- Zhao, Z.; Yan, H.; Zuo, J.; Tian, Y.; Zillante, G. A Critical Review of Factors Affecting the Wind Power Generation Industry in China. Renew. Sustain. Energy Rev. 2013, 19, 499–508. [Google Scholar] [CrossRef]

- Eng, L.L.; Fikru, M.G. Are US Electric Utilities Improving Their Sustainability Disclosures and Performance? Electr. J. 2022, 35, 107221. [Google Scholar] [CrossRef]

- Lee, M.; Lee, S. Evaluating Internal Technological Capabilities in Energy Companies. Energies 2016, 9, 145. [Google Scholar] [CrossRef]

- Fan, J.-L.; Zhang, H.; Zhang, X. Unified Efficiency Measurement of Coal-Fired Power Plants in China Considering Group Heterogeneity and Technological Gaps. Energy Econ. 2020, 88, 104751. [Google Scholar] [CrossRef]

- Sheveleva, G.I. Corporate Governance in Generating Companies of the Russian Electric Power Industry in the Context of ESG Agenda. Glob. Energy Interconnect. 2022, 5, 512–523. [Google Scholar] [CrossRef]

- Cornet, Y.; Gudmundsson, H. Building a Metaframework for Sustainable Transport Indicators: Review of Selected Contributions. Transp. Res. Rec. 2015, 2531, 103–112. [Google Scholar]

- Sueyoshi, T.; Goto, M. Environmental assessment by DEA radial measurement: US coal-fired power plants in ISO (Independent System Operator) and RTO (Regional Transmission Organization). Energy Econ. 2012, 34, 663–676. [Google Scholar]

| Dimensions | Topics | Criteria | Indicators |

|---|---|---|---|

| Environment | Emission (A1) | Emission intensity (A1.1) | NOx emission intensity (A1.1.1). Soot emission intensity (A1.1.2). Sulfur dioxide emission intensity (A1.1.3). |

| Emissions Reduction Effectiveness (A1.2) | NOx emission intensity reduction rate (A1.2.1). Reduction rate of soot emission intensity (A1.2.2). Sulfur dioxide emission intensity reduction rate (A1.2.3). | ||

| Resource (A2) | Resource consumption (A1.3) | Electricity consumption rate of power plants (A2.1.1). Standard coal consumption for electricity supply (A2.1.2). | |

| Resource conservation (A2.1) | Power plant electricity consumption rate reduction rate (A2.2.1). Reduction rate of standard coal consumption for electricity supply (A2.2.2). Comprehensive utilization rate of fly ash (A2.2.3). Comprehensive utilization rate of slag (A2.2.4). | ||

| Climate Change (A3) | Green technology (A2.2) | Operating rate of desulfurization facilities (A3.1.1). Operation rate of denitrification facilities (A3.1.2). | |

| Greenhouse gas emissions and effectiveness (A3.1) | CO2 reduction through non-fossil energy generation (A3.2.1). Greenhouse gas emissions reduction growth rate (A3.2.2). Carbon dioxide emission intensity (A3.2.3). | ||

| Green electricity (A3.2) | Standard coal saved through non-fossil energy generation (A3.3.1). Sulfur dioxide reduction through non-fossil energy generation (A3.3.2). NOx reduction from over non-fossil energy generation (A3.3.3). | ||

| Environmental Risks (A4) | Negative information (A4.1) | Number of times punished by relevant regulatory authorities due to environmental problems (A4.1.1). | |

| Social | Employee (S1) | Employment stability (S1.1) | Labor-contract-signing rate (S1.1.1). Employee turnover rate (S1.1.2). |

| Occupational health and employee development (S1.2) | Employee medical examination rate (S1.2.1). Social Insurance Coverage (S1.2.2). Number of employee workplace accidents (S1.2.3). Average number of training sessions for employees (S1.2.4). | ||

| Equality and diversity (S1.3) | Percentage of ethnic minority employees (S1.3.1). Percentage of female managers (S1.3.2). Ratio of male to female employees (S1.3.3). | ||

| Social (S2) | Social contribution (S2.1) | Consumption of poverty alleviation funds as a proportion of operating income (S2.1.1). | |

| Safe and efficient production (S2.2) | Number of general equipment accidents (S2.2.1). On-grid power/generation capacity (S2.2.2). Unit cost of electricity generation (S2.2.3). Unit power generation cost reduction rate (S2.2.4). On-grid tariff (S2.2.5). Rate of increase in electricity on the grid (S2.26). Safety hazard correction rate (S2.2.7). Hours of utilization of power generation equipment (S2.2.8). | ||

| Governance | Directors and Board of Directors (G1) | Board operation status (G1.1) | Attendance of directors’ representatives in the Board of Directors (G1.1.1). Number of board meetings (G1.1.2). Director turnover rate (G1.1.3). |

| Board composition (G1.2) | Percentage of independent directors (G1.2.1). Number of board of directors members (G1.2.2). Percentage of female directors (G1.2.3). Independent directors’ remuneration as a percentage of directors’ and supervisors’ salaries (G1.2.4). | ||

| Shareholding structure and other management operations (G2) | Shareholding structure (G2.1) | Shareholding ratio of the second to tenth largest shareholders to the first largest shareholder (G2.1.1). Shareholding percentage of the largest shareholder (G2.1.2). | |

| Managerial operation status (G2.2) | Frequency of managerial staff changes (G2.2.1). | ||

| Supervisory board structure and operation status (G2.3) | Percentage of employee supervisors (G2.3.1). Number of supervisory board members (2.3.2). Supervisor turnover rate (G2.3.3). | ||

| Stakeholder Relations (G3) | Information disclosure (G3.1) | Company indicator completeness (G3.1.1). Frequency of updating information on company website (G3.1.2). | |

| Stakeholder engagement (G3.2) | Response rate to stakeholder inquiries (G3.2.1). | ||

| Innovative Development (G4) | Innovation input and effectiveness (G4.1) | R&D expenses/revenue (G4.1.1). Number of R&D staff as a percentage of total company headcount (G41.2). Number of patents granted per capita (G4.1.3). | |

| Economy | Profitability (B1) | Basic earnings per share (B1.1.1). Return on Net Assets (B1.1.2). Return on total assets (B1.1.3). Return on main business (B1.1.4). Return on power generation business (B1.1.5) | |

| Operating capacity (B2) | Total assets turnover ratio (B2.1.1). Current assets turnover ratio (B2.1.2). Accounts receivable turnover ratio (B2.1.3). | ||

| Solvency (B3) | Balance sheet ratio (B3.1.1). Current ratio (B3.1.2). Cash flow ratio (B3.1.3). Equity ratio (B3.1.4). | ||

| Development capacity (B4) | Operating income growth rate (B4.1.1). Capital accumulation ratio (B4.1.2). Total assets growth rate (B4.1.3). Fixed assets growth rate (B4.1.4). Net profit growth rate (B4.1.5). | ||

| Dimensionality | Indicators |

|---|---|

| Environmental | New construction projects for environmental impact assessment and preparation of environmental impact assessment reports |

| Establishment of specialized environmental management positions | |

| Corporate environmental management policy/system | |

| Social | Use criteria for screening suppliers |

| Contingency planning | |

| Measures to avoid child labor and forced labor | |

| Governance | Compensation of directors, supervisors, and senior management; decision-making process and basis for determination |

| The listed company and its directors, supervisors, senior management, controlling shareholders for suspected illegal and non-compliant behavior |

| Mean | Max. | Min. | Std. Dev. | |

|---|---|---|---|---|

| Environmental Dimension Score | 65.10 | 85.54 | 38.30 | 10.74 |

| Social Dimension Score | 64.69 | 86.04 | 51.82 | 8.23 |

| Governance Dimension Score | 76.79 | 94.08 | 53.95 | 9.08 |

| Economic Dimension Score | 41.37 | 84.35 | 6.97 | 15.02 |

| Code | Mean | Max. | Min. | Std. Dev. |

|---|---|---|---|---|

| A1.1 | 69.32 | 98.34 | 0.00 | 20.66 |

| A1.2 | 54.16 | 83.73 | 0.00 | 21.43 |

| A2.1 | 64.36 | 100.00 | 0.00 | 29.06 |

| A2.2 | 47.34 | 100.00 | 0.00 | 24.69 |

| A3.1 | 92.51 | 100.00 | 47.34 | 16.62 |

| A3.2 | 65.06 | 100.00 | 10.21 | 29.56 |

| A3.3 | 64.67 | 96.67 | 32.62 | 20.66 |

| A4.1 | 85.15 | 100.00 | 0.00 | 30.83 |

| S1.1 | 89.31 | 100.00 | 50.00 | 13.84 |

| S1.2 | 82.34 | 100.00 | 51.03 | 11.29 |

| S1.3 | 46.41 | 99.81 | 13.66 | 19.76 |

| S2.1 | 11.72 | 100.00 | 0.00 | 22.37 |

| S2.2 | 72.30 | 88.41 | 48.47 | 7.49 |

| G1.1 | 59.35 | 87.25 | 11.46 | 16.74 |

| G1.2 | 61.69 | 87.88 | 44.21 | 9.64 |

| G2.1 | 36.32 | 100.00 | 0.00 | 25.98 |

| G2.2 | 64.46 | 100.00 | 0.00 | 33.09 |

| G2.3 | 96.38 | 100.00 | 63.16 | 6.44 |

| G3.1 | 80.32 | 100.00 | 41.67 | 20.23 |

| G3.2 | 96.37 | 100.00 | 96.00 | 1.34 |

| G4.1 | 23.05 | 85.32 | 0.00 | 24.85 |

| B1 | 45.97 | 92.58 | 6.30 | 21.72 |

| B2 | 40.82 | 76.86 | 5.43 | 16.12 |

| B3 | 40.58 | 84.20 | 5.43 | 13.64 |

| B4 | 32.94 | 83.76 | 10.66 | 13.62 |

| Code | Index | Code | Index | Code | Index |

|---|---|---|---|---|---|

| E1 | 62.68 | E18 | 44.60 | E35 | 40.49 |

| E2 | 65.93 | E19 | 65.45 | E36 | 60.85 |

| E3 | 44.44 | E20 | 60.96 | E37 | 53.63 |

| E4 | 47.85 | E21 | 51.99 | E38 | 66.94 |

| E5 | 57.10 | E22 | 69.07 | E39 | 57.59 |

| E6 | 66.18 | E23 | 47.65 | E40 | 67.15 |

| E7 | 54.83 | E24 | 48.91 | E41 | 60.86 |

| E8 | 64.92 | E25 | 61.63 | E42 | 60.48 |

| E9 | 61.73 | E26 | 58.03 | E43 | 63.72 |

| E10 | 64.33 | E27 | 67.94 | E44 | 45.92 |

| E11 | 63.68 | E28 | 71.07 | E45 | 54.48 |

| E12 | 54.11 | E29 | 54.36 | E46 | 75.28 |

| E13 | 63.75 | E30 | 65.25 | E47 | 59.20 |

| E14 | 57.82 | E31 | 67.87 | E48 | 58.04 |

| E15 | 67.82 | E32 | 67.94 | E49 | 57.50 |

| E16 | 57.68 | E33 | 58.15 | E50 | 65.35 |

| E17 | 44.72 | E34 | 59.28 |

| Economy | Environmental | Social | Governance | |

|---|---|---|---|---|

| Economy | 1 | |||

| Environmental | 0.14 | 1 | ||

| Social | 0.16 | −0.06 | 1 | |

| Governance | 0.08 | 0.06 | −0.03 | 1 |

| A1 | A2 | A3 | A4 | S1 | S2 | G1 | G2 | G3 | G4 | B1 | B2 | B3 | B4 | |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| A1 | 1 | |||||||||||||

| A2 | 0.11 | 1 | ||||||||||||

| A3 | −0.22 | −0.43 | 1 | |||||||||||

| A4 | −0.37 | 0.55 | −0.28 | 1 | ||||||||||

| S1 | −0.12 | 0.14 | 0.34 | 0.58 | 1 | |||||||||

| S2 | 0.43 | 0.43 | −0.6 | 0.12 | 0.19 | 1 | ||||||||

| G1 | −0.49 | 0.31 | 0.13 | 0.52 | 0.52 | −0.36 | 1 | |||||||

| G2 | −0.12 | 0.05 | −0.07 | 0.44 | 0.48 | −0.36 | 0.48 | 1 | ||||||

| G3 | −0.60 | 0.07 | −0.43 | 0.01 | −0.16 | 0.26 | −0.33 | 0.18 | 1 | |||||

| G4 | −0.14 | −0.36 | −0.22 | −0.26 | −0.2 | −0.28 | −0.41 | 0.42 | 0.52 | 1 | ||||

| B1 | −0.33 | 0.18 | 0.31 | 0.60 | 0.42 | −0.36 | 0.72 | 0.27 | −0.33 | −0.57 | 1 | |||

| B2 | 0.17 | 0.06 | 0.18 | 0.41 | 0.37 | −0.30 | 0.35 | 0.38 | 0.11 | −0.21 | 0.8 | 1 | ||

| B3 | 0.03 | −0.16 | 0.39 | 0.236 | 0.35 | −0.38 | 0.24 | 0.23 | −0.13 | −0.27 | 0.77 | 0.81 | 1 | |

| B4 | −0.10 | −0.09 | 0.49 | 0.28 | 0.57 | −0.44 | 0.20 | 0.38 | −0.31 | −0.14 | 0.65 | 0.73 | 0.88 | 1 |

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2023 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Dong, R.; Shao, C.; Xin, S.; Lu, Z. A Sustainable Development Evaluation Framework for Chinese Electricity Enterprises Based on SDG and ESG Coupling. Sustainability 2023, 15, 8960. https://doi.org/10.3390/su15118960

Dong R, Shao C, Xin S, Lu Z. A Sustainable Development Evaluation Framework for Chinese Electricity Enterprises Based on SDG and ESG Coupling. Sustainability. 2023; 15(11):8960. https://doi.org/10.3390/su15118960

Chicago/Turabian StyleDong, Ruiyu, Chaofeng Shao, Shuqi Xin, and Zhirui Lu. 2023. "A Sustainable Development Evaluation Framework for Chinese Electricity Enterprises Based on SDG and ESG Coupling" Sustainability 15, no. 11: 8960. https://doi.org/10.3390/su15118960

APA StyleDong, R., Shao, C., Xin, S., & Lu, Z. (2023). A Sustainable Development Evaluation Framework for Chinese Electricity Enterprises Based on SDG and ESG Coupling. Sustainability, 15(11), 8960. https://doi.org/10.3390/su15118960