Abstract

Mobile banking has the benefits of internet banking, in which the customer can access bank services over an internet connection anytime and anywhere. Millennials in Malaysia’s business environment are an enormous segment of the Malaysian population, and they are moving to take their places in the middle and high levels of their companies’ managerial governance pyramid these days and in the near future. This study examines the question, “What are the main factors that may influence mobile banking use (MBU) and the intention to use mobile banking (IU) among millenial consumers in Malaysia?”. The determining factors of UTAUT, performance expectancy (PE), effort expectancy (EE), social influence (SI), facilitating conditions (FC), hedonic motivation (HM), price value (PV), habit (Ha), perceived risk (PDR), and interface design quality (IDQ) were tested in this study. Method: SPSS and PLS-SEM are employed on a collected sample of 504 respondents of Millennials in Malaysia using a well-defined questionnaire to carry out all statistical analyses of this study. Result: The study model can explain 55.3% of the variance of mobile banking use (MBU) and 60.3% of the intention to use mobile banking (IU). In this study, all the relations of the model are significant, except the relation between price value (PV) and the intention to use mobile banking. For both IU and MBU in the model, the factor “Interface design quality” (IDQ) has the highest impact. In contrast, the factor “Perceived Risk” (PDR) has the lowest impact. The findings of this study extend the knowledge on mobile banking as an approach of financial technology implementation, from which mobile banking providers and interface designers can provide new potential solutions to expand the usage of mobile banking services in Malaysia. This study proposed a modified model with eleven variables. While the designed model was evaluated successfully and explained 55% of actual use and 60% of intentional use, the remaining portion (45% for actual use and 40% for intended usage) exposes yet other factors that are still unrevealed. Therefore, further studies are required to assess the design in various other financial sectors, and further studies are invited to conduct qualitative research to reveal other variables for a better understanding of the intention and actual use of mobile banking.

1. Introduction

Mobile banking, known as “m-banking”, is defined as “ a service offered by either a bank or a financial institution that can be carried out via a mobile device, such as a mobile phone, tablet, or personal digital assistant” [1]. Cell phones offer most of the services in the banking industry, such as requests for account balance, business from accounts, transferring money, trading, or even selling and cost information [2]. Nevertheless, mobile banking uptake has been slower than the latest development of mobile devices in smartphone hardware, programs, security, and information transmission. However, the new generation of mobile phones and the reduced costs accelerated its use; mobile banking has emerged as a brand-new alternative mode of banking, more user-friendly and convenient than the regular type of banking. It addresses the idea of “anytime”, “anywhere”, banking into truth [3]. During the Global Islamic Finance Forum 5.0 on 11 May 2016, the chairman of Bank Negara Malaysia, Dato Muhammad Bin Ibrahim, pointed out that the birth of “Fintech” is one of the most significant transformational developments in the banking sector as a result of maturing social and mobile technologies. Fintech innovations are influencing the revolution of new financial products and services; within less than one year, Fintech start-ups doubled from 1000 in 2015 to more than 2000 in 2016.

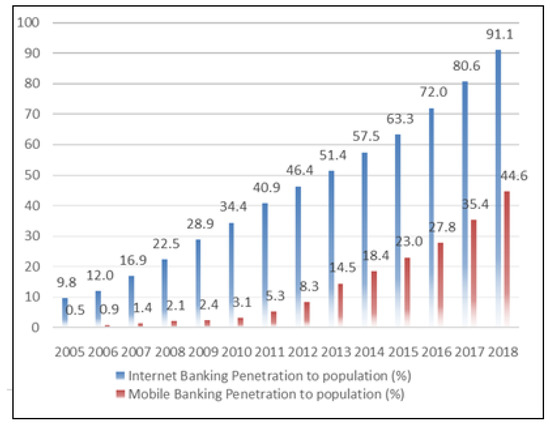

Technological development has quickly transformed every element of our lives and the way of banking business throughout the last ten years. Integration of web technology and mobile networks produces brand-new possibilities; therefore, the banking business has never observed such a fundamental change as mobile banking [4]. Therefore, banks must be innovative and produce intelligent products to supply banking services. Many individuals today use a broad array of mobile products to carry out banking services, and millions more have anticipated potentially going mobile [5]. Mobile payments and mobile banking are becoming increasingly common, with improved dissemination of technology and a broad array of choices; customer adoption of mobile financial solutions has risen. By 2018, 44.6% of the Malaysian populace had signed up for mobile banking, and 91.1% had subscribed to electronic banking, according to Bank Negara Malaysia (see Figure 1).

Figure 1.

Usage of mobile banking. Source: BNM 2019 Report.

Mobile banking and payments are growing in popularity with customers. It was reported that more than one billion worldwide cell phone users would have used their mobile devices for banking reasons by the end of 2017 compared to only more than 590 million in 2012. The development and product development that are taking place provide customers with increased flexibility to carry out their daily banking using a convenient and new channel (Juniper research January 2013). Therefore, the main research question for this study is, “what are the main factors that influence the use and intention to use mobile banking among Malaysian Millennials?” Additionally, the sub-questions are:

- a

- What are the technological determinants of the intention to use mobile banking systems among Malaysian Millennials?

- b

- What are the significant dimensions of the perceived risk of mobile banking use among Malaysian Millennials?

- c

- What interface design qualities impact the intention to use mobile banking systems among Malaysian Millennials?

- d

- What is the relation between the intention to use and the actual use of mobile banking among Malaysian Millennials?

- e

- What is an improved model to assess mobile banking use among Malaysian Millennials?

This study is a quantitative-based study that follows the systematic steps of the scientific approach. Therefore, the study has eight sections: Introduction, Statement of Problem, Literature Review, Theoretical Framework, Method, Results, Conclusions and Recommendations for Future Research.

2. Statement of Problem

“Fintech” in Malaysia is contributing to 20% the GDP of Malaysia, whereas mobile banking has reached 61.8% (equivalent to 936 million volume) of total bank account holders [6]. The revolution of mobile banking as the Fintech approach contributes to the economy and the business environment is inevitable in the coming years. Thus, finding ways to allow this industry to enhance and support the economy is essential, especially for Malaysia as a developing country. Based on the analysis of the statistical reports issued by Bank Negara Malaysia, there is a contradiction between the volume and value of mobile banking transactions. From 2005 to 2018, mobile banking transactions showed a dramatic increase; according to the statistics of Bank Negara in 2018, the volume of mobile banking transactions was almost three times more than internet banking transactions. However, these transactions were passive and not converted to actual payment transactions. In contrast, the value of mobile banking transactions was almost ten times less than internet banking transactions in 2018. There is a clear gap between the high volume and low weight of mobile banking transactions in Malaysia; therefore, this study investigates the possible causes of the intention to use and the actual use of mobile banking in Malaysia.

Malaysian values over payment channels, i.e., “ATM payment transaction, credit card, charge card, debit card, mobile banking and internet banking”, are the total amounts of money transferred using these channels. Although the internet banking channel had the highest-value total transactions of MYR 607.5 billion in 2018, mobile banking was the third-highest-value payment channel with MYR 78.36 billion in the same year. Notably, payments via internet banking experienced a downward trend in 2018, while mobile banking payments increased dramatically fourfold from 2015 to 2018. The volume of transactions (the number of transactions) using mobile banking has speedily increased since 2012 and hit 1688.8 million transactions in 2018, passing the volumes of both internet banking (557 million transactions) and credit cards (366 million transactions).

Although the mobile banking approach has been welcomed internationally, including in Malaysia, issues related to privacy, security, bank customers’ needs, advancement of banking infrastructure, and governmental regulations are significant challenges faced by individual users. In terms of the adoption of bank services offered online for smartphone users, a few studies were completed in Malaysia [7,8,9,10,11,12]. Thus, different countries face distinct challenges, but this study has focused on the Malaysian context because of advancement in mobile banking adoption and explores factors that may create hurdles in its use.

Many scholars relate the ineffective use of payments over the Internet, such as mobile banking and electronic banking, to the perceived risk and lack of trust in using mobile banking in Malaysians’ financial management [13]. Ref. [14] mentioned that assessing the protection system of mobile banking and the quality of mobile communications significantly contribute to mobile banking usage. Ref. [15] linked the loyalty and transaction process of mobile banking with the concepts of diffusion of innovation and the trust principle. The results indicate that individual advantage and perceived capacity significantly impact mobile users’ attitudes towards mobile banking. Therefore, this study accounts for the different dimensions of perceived risk as potential predictors of mobile banking use.

Moreover, Ref. [16] argued that the quality of the screen interface layout for banking services could be more apparent. Hence, this study accounts for the interface design quality as a potential factor of mobile banking use. There needs to be more investigation evaluating the role of the mobile banking interface quality.

As Millennials make up the most significant portion of the Malaysian population, understanding their behaviour towards mobile phone banking will help financial institutions to have the proper advertising and marketing approaches to attract this enormous slice of users. Therefore, this study accounts for Malaysian Millennials’ perceptions, as this age group is the majority. With the above discussion, this study points out a significant problem: although mobile banking appears to be the most popular usage channel, the total value of transactions made through this channel is the lowest compared to other alternative financial channels in Malaysia. Thus, it is essential to identify factors that prevent Malaysians from making banking transactions through their mobile devices. Therefore, this study aims to investigate the phenomenon of the lack of use of mobile banking services among Millennials in Malaysia. In addition, this study will examine the role of perceived risk besides other technical and human factors. The findings will help Malaysia further boost the adoption of mobile banking to enhance its Fintech industry in the coming years.

3. Literature Review

The emergence of the Internet, smartphones, social media, and cloud computing has been a fundamental source of large-scale transformations across multiple sectors and industries. However, according to a report by the World Economic Forum, the role of these technologies is shifting because digital technologies will no longer just be drivers of marginal efficiency but enablers of fundamental innovation and disruption across different sectors [17]. Technological improvements in financial services have changed how economic solutions are transacted. Fintech is an excellent example of a technology niche changing the present monetary routine, and mobile banking is acquiring the latest development within this particular industry. Mobile banking permits banking clients to use cell phones or portable processing devices to execute banking transactions such as checking profile balances, paying bills, transmitting cash, or searching for ATM locations.

Fintech is a combination of both finance and technology, which is extensively used in banks. During the 21st century, Fintech has dramatically risen around the globe, particularly in Malaysia [18]. According [19], the term has grown to consist of any technology in the financial industry and the cutting-edge usage of technology in the layout and shipment of financial solutions, including digital purses, money cards, mobile phones, etc.

3.1. Mobile Banking in Malaysia

By the end of 2014, the total number of mobile banking subscribers in Malaysia was estimated at around 5.5 million, accounting for about 18.6% of the Malaysian population [20]. In addition, two-thirds of these subscribers had been using mobile banking services. In early 2012, the leading financial institutions teamed up, and two primary mobile area drivers delivered a new mobile purchase and banking company, MyMobile. One of the various advantages of MyMobile is its power to aid in transferring funds with the telephone number of recipients rather than savings account number, and it comes with all types of phones [20]. With MyMobile, signed-up owners can make several financial purchases, including fund transmission, cost payments, pre-paid credit scores, and monthly memory card payments at any moment and from any site.

3.2. Millennials

A generation is called an identifiable team which shares birth years, age region, and notable life occasions at critical developing phases [21]. A generational group, often called a cohort, comprises people who share social or historical life experiences [22,23]. Furthermore, young adulthood is crucial because incidents encountered throughout that period have reasonably secure effects on one’s living [24]. Based on the research of the Center for Generational Kinetics (CGK), the leader in generational study that operates throughout the U.S., Europe, Middle East, and South America: A development is a team of individuals created close to the same period and raised close to the same spot. Individuals in the same team show very similar qualities, tastes, and values throughout their lifetimes. Millennials are probably the most consistent model globally.

Based on [25], every development is affected by broad forces (i.e., parents, colleagues, media, critical financial and community functions, along with popular culture), which produce typical benefit systems distinguishing them from individuals who were raised in dissimilar conditions. The values, perspectives, and perceptions of development are often affected by necessary historical and social life experiences they discussed when they were created and raised [21,22]. Many raised simultaneously have a robust identification because of their historical period and can think, feel, and act similarly. Those similarities among people of a shared group are usually apparent in the style of their lives [23].

In August 1993, the editorial media company Ad Age was the first fabricator of the term Generation Y, also known as Millennials. They used the term to designate a specific group with age characteristics, in which the group included all people aged 11 years at that time with the expectation to include all those born in the upcoming ten years. According to the concept, the year 1982 was the commencing year of this generation [26]. However, a previous director of I.T. at Ad Age argues that the Generation Y label will continue to be valid and the most applicable until we discover a much more usable term [27]. According to [28] Millennials in Malaysia constitute the most significant customer population. They frequently take over much more senior jobs and develop the most critical customer segment. Therefore, financial institutions in Malaysia have a fantastic chance to promote the bulk of Millennial customers through clearly understanding Millennials’ requirements and behaviours. There is a chance to deliver the Millennials and tap this untapped segment of Malaysia through investigating the attainable factors impacting Millennials, which can be understood via examining models and theories in Malaysia [29]. According to [30], Millennials dominate the population’s pyramid nearly worldwide, including Malaysia; presently, Millennials are a typing workforce and beginning to make cash. In addition, the investing design of this particular development is, amazingly, almost MYR 1.8 billion yearly in e-commerce solely.

Various scholars, such as [29,31,32], mentioned that exhaustive exploration of Millennial consumers’ intention to use mobile banking is required to make any development of the future offered services and marketing plans much reliable. A heuristic decision in the provided services will contribute to improving the adoption of mobile banking. Ref. [33] recently investigated the critical factors affecting Millennials consumer intention towards mobile banking in Malaysia. They found that consumer intention has a significant positive relation with ease of use and perceived usefulness, whereas a significant negative relationship is perceived risk. Using qualitative analysis, Ref. [34] compared consumers’ expectations and experiences among Generations X, Y, and Z. The study revealed that each generation has distinct characteristics, where Generation X finds it complicated, and Generation Y (Millennials) prefers mobile banking services. In contrast, Generation Z prefers to use more customized service.

Although mobile banking is the most popular usage channel, the total value of transactions made through this channel is the lowest compared to other alternative financial channels in Malaysia. Thus, it is essential to identify factors that prevent Malaysians from making banking transactions through their mobile devices. Therefore, this study aims to investigate the phenomenon of the lack of use of mobile banking services among Millennials in Malaysia. In addition, this study will examine the role of perceived risk besides other technical and human factors. The findings will help Malaysia boost the further adoption of mobile banking to enhance its Fintech industry in the coming years.

4. Theoretical Framework

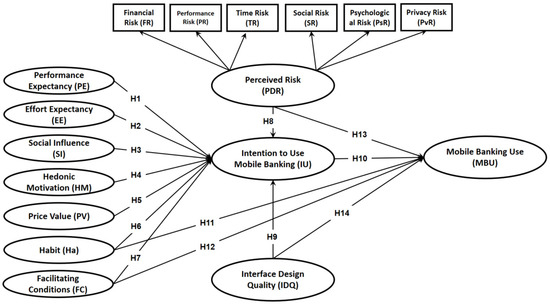

Given the present moment, this study will assess the variables in a more established and extensive method using recommendations of existing analyses in the appropriate literature that directly or indirectly increase the opportunity of actual use and intention to use mobile banking systems. This study model is modified based on the UTAUT2 model, using the seven determinants in the original UTAUT2 model in addition to two additional determinants, perceived risk and information system quality. The perceived risk dimension is added from the perceived risk model proposed by [35], and interface design quality is added with support from the literature. Figure 2 demonstrates the structure of the variables and their relation to this particular study.

Figure 2.

Proposed research model with hypothesis.

4.1. Hypotheses Development

4.1.1. Intention to Use (I.U.)

I.U. is, in simple fact, a swift antecedent of consumption practices and deals with evidence relating to an individual’s preparedness to perform specific habits. Genuine behaviour reveals a visible effect in a specific condition when it comes to a specific target [36]. There is a considerable amount of evidence of the significant influence of B.I. on I.U., including detailed technology recognition studies [37,38,39]. Lately, this has been stretched to electronic and mobile banking [40,41]. In a 2016 study in Lebanon, authors used the UTAUT style as the foundation for looking at the web economically. They uncovered that the connection between the intention to make use of and genuine usage is sound, with a course coefficient truly worth 0.452 [42]. In another study which was executed in Saudi Arabia, Jordan, and Egypt in 2015 to analyse the relevancy of UTAUT variation in the domain title of internet economics in producing countries, for the authors uncovered an extreme significance (course coefficient = 0.84) of the relationship between motive and additionally genuine usage [43]. Thus, the following is hypothesised:

H1.

Regarding mobile banking acceptance in Malaysia, the behavioural intention concept positively influences the system.

4.1.2. Facilitating Conditions (F.C.)

According to [37], facilitating conditions (F.C.) are determined as “the degree to which a private strongly believes that a technical and company structure exists to use the system”. Ref. [38] discussed that facilitating conditions directly impact each consumer’s behavioural intention to use and their technology actions. Ref. [44] examined the factors that affect mobile banking fostering in Libya as a developing country. The authors analysed 319 individuals and found that facilitating conditions positively impact the mobile banking adoption behaviour of the customers. Likewise [45,46,47] found that facilitating conditions (F.C.) positively predict the behavioural intention to adopt mobile banking. Besides, Ref. [48] study reported that facilitating conditions substantially influence the user’s mobile banking personality. Ref. [49] examined the variables determining the preservice approval of understanding the administration software program at Universiti Utara Malaysia. They found that facilitating conditions are considered a predictor of behavioural intention. According to [50], based on the survey’s responses from 300 young users of cell phone tools, various regression tests were used to analyse the adopted (UTAUT2) version to find out the crucial determinants that determine the behavioural intention to adopt mobile phone uses (applications) in Malaysia. The authors revealed that facilitating conditions certainly do not determine behavioural intention in mobile phone functions.

Facilitating conditions are one of the most significant elements influencing behavioural intention and mobile banking adoption. To examine factors influencing M-payment and M-banking adoption in the UK, Ref. [51] found that 186 partnerships between dependent and independent variables have been examined through 32 observational M-payment and M-banking fostering research studies. Similarly, Ref. [52] found that the impact of facilitating conditions favourably predicts behavioural intention (B.I.) based on the responses received from the sample of 344 Jordanian financial clients, which favourably influences the fostering of mobile banking.

Thus, the following is hypothesised:

H2.

Regarding mobile banking acceptance in Malaysia, the concept of facilitating conditions has a significant positive impact on behavioural intention.

H3.

Regarding mobile banking acceptance in Malaysia, the concept of facilitating conditions has a significant positive impact on system use.

4.1.3. Hedonic Motivation (H.M.)

Hedonic motivation (H.M.) is determined as “the enjoyment or satisfaction derived from using an innovation”. The variable is an added variable in UTAUT2. Numerous current observational evaluations verified that H.M. has the primary role in clarifying the variance of technology, making use of objectives, and accurate use [37,38].

Ref. [52] examined factors based on the UTAUT version that affect the recognition and use of mobile banking from a sample of 343 situations from Jordanian mobile banking consumers. Their results revealed that hedonic motivation and price worth presented beneficial sturdy predictors of the behavioural intention to use mobile banking. In another study, Ref. [45] concluded that hedonic motivation (HM) is a notable positive predictor of the behavioural intention to take on mobile banking. Generally, hedonic motivation showed a substantial influence on the user behaviour of mobile banking in several research studies [48,53]. Ref. [54] suggested that hedonic motivation positively affects pupils’ mobile phone understanding and fostering. This is similar to [50], who found that hedonic motivation affects behavioural intention in adopting mobile phone apps in Malaysia.

Thus, the following is hypothesised:

H4.

Regarding mobile banking acceptance in Malaysia, hedonic measures have a significant positive impact on behavioural intention.

4.1.4. Price Value (P.V.)

Ref. [38] pointed out that price value (P.V.) is described as “individuals’ intellectual tradeoff between the recognized perks of the applications and the monetary price for using them”. Unlike how organisations utilize modern technology for purchasing, consumers usually need to pay all the costs of using modern technology in customer usage situations. So, they proposed that the price value will positively impact behavioural intention when buyers view the advantages of utilizing technology as higher than the cost of such usage.

In the latest research study by [48], UTAUT2 was combined with the Delone and McLean information system to determine factors that influence the recognition and use of mobile banking by 700 individuals in Saudi Arabia. The authors found that price value (P.V.) considerably affects mobile banking usage behaviour. Moreover, Ref. [45] reported that price value (P.V.) is a considerable predictor of behavioural intention to take on mobile banking.

Ref. [47] investigated the price value factor as one of the UTAUT factors through collecting data through a survey from 362 participants. They applied confirmatory factor analysis (CFA), showing that price value and other UTAUT factors were responsible for positive intention towards mobile banking adoption.

In mobile banking adoption, private intention to embrace mobile banking was considerably affected by perceived economic expense [41]. Price value (P.V.) was among the most notable elements influencing behavioural intention to foster mobile banking [51]. Ref. [55] suggested that perceived cost substantially determined customer adoption of payment over mobile banking in Thailand.

Thus, the following is hypothesised:

H5.

Regarding mobile banking acceptance in Malaysia, price value measures have a significant positive relationship with behavioural intention.

4.1.5. Performance Expectancy (P.E.)

According to [37], performance expectancy (P.E.) is determined as “the degree to which a person feels that using the unit is going to acquire gains in job efficiency”. Performance expectancy is considered to affect behavioural intention to adopt and use modern technology directly. Performance expectancy has been discussed in the technology acceptance model (TAM), predicting the person’s opinion using the new technology [37,56].

Abbas, Hassan, Asif, Hassan, and Ahmed (2018) [57] employed the UTAUT model, initial trust model (ITM), and task technology fit (TTF) to study the perspectives of mobile banking adoption in Pakistan. The study found that performance expectancy was notable, and the parts of UTAUT reveal and highlight the favourable importance of partnership and mobile banking adoption. Ref. [58] argued that performance expectancy efficiently influences mobile banking adoption. They discussed that consumers use the mobile banking company if it offers the expected favourability and efficiency. Ref. [52] showed that the intent of mobile banking adoption is positively and dramatically affected by performance expectancy. Ref. [59] presented that performance expectancy substantially impacts the intention to take on electronic banking. Ref. [60] stated that performance expectancy has a significant influence on the efficiency of behavioural intention towards making use of M-banking.

To study the adoption of mobile banking, Ref. [31] used a sample of 347 participants to examine the consumer behaviour intention among Malaysian Generation Y buyers. The authors depicted that performance expectancy is considered a predictor of intention to embrace mobile banking. Moreover, their results are consistent with [52], showing that the effect of performance expectancy favourably forecasts behavioural intention, which, consequently, favourably affects the embrace of mobile banking. Ref. [61] also revealed that perceived effectiveness was favourably associated with taking on bank solutions delivered online for mobile phone users. According to [54], performance expectancy influences students’ mobile phone adoption favourably. Likewise, Ref. [49] pointed out that performance expectancy considerably influences behavioural intention. In addition, Ref. [62] uncovered the impact of performance expectancy on the behavioural intention of mobile app users in Malaysia.

According to [37], performance expectancy (P.E.) is specified as “the degree to which a specific thinks that making use of the system will help achieve increases in task efficiency”. Performance expectancy shares identical characteristics with viewed effectiveness in the technology acceptance model (TAM). The pair of definitions emphasize the person’s belief that functionality will be boosted through utilizing brand-new modern technology or even a unit [63]. Refs. [46,47,58] argued that performance expectancy significantly impacts mobile banking adoption. The authors demonstrated that customers accept and embrace mobile banking if it is as helpful and efficient as expected.

Thus, the following is hypothesised:

H6.

Regarding mobile banking acceptance in Malaysia, performance expectancy measures have a significant positive relationship with behavioural intention.

4.1.6. Effort Expectancy (E.E.)

Ref. [37], effort expectancy (E.E.) is specified as “the degree of ease associated with making use of the system”, and the convenience of utilisation has a direct influence on customers’ behavioural intention to embrace and make use of modern technology. Effort expectancy shares similar qualities with perceived simplicity according to the technology acceptance model (TAM) [38,56]. The perceived simplicity of making use of a technology resembles effort expectancy. Ref. [56] defined perceived simplicity of use as “the degree to which a person strongly believes that utilizing a specific device would certainly be devoid of effort”.

Ref. [58] analysed the elements that influence the affirmation and use of mobile banking with 309 pupils from a college in the U.S. The results disclosed that effort expectancy is considered a sturdy forecaster of the intention to take on mobile banking. People will be more likely to take on and use a mobile banking service if they believe that they will not face any challenges and it is quick and easy to use. Ref. [59] explored the variables influencing the approval and use of internet finance in Malaysia. Based on a sample of 200 Malaysian online banking customers, the outcome revealed that perceived simplicity of use, identified effectiveness as effort expectancy, and performance expectancy had a significant influence on the intention to embrace internet financial services.

An examination of the UTAUT2 approach was applied to 288 students who took part in an online study, using predisposed minimum squares (PLS) to check out the partnerships between the constructs of UTAUT2 that might influence the Preservice Acceptance of Knowing Monitoring Software Program in Universiti Utara Malaysia [49] discussed that the results confirmed that effort and performance expectancy has a considerable effect on behavioural intention. Refs. [47,48] suggested that behavioural intention (B.I.) and, after that, use goals are influenced by enablers such as effort expectancy and performance expectancy.

Ref. [61] examined the factors that affect Malaysians’ intention to embrace mobile banking through expanding the technology acceptance model (TAM) platform. They found that the perceived simplicity of use was favourably associated with using online banking company services offered for cell phone users. This is sustained by [31], who pointed out that effort expectancy (E.E.) was looked at as a sturdy forecaster of intention to adopt mobile banking. These observational studies reveal that effort expectancy (E.E.) significantly affects the behavioural intention (B.I.) to take on mobile banking technology.

Ref. [37] stated that effort expectancy (E.E.) is determined as “the degree of ease connected along with the use of the unit”, and the ease of use has a direct result on an individual’s behavioural intention to accept and use a modern technology. The interpretation of regarded ease of use is comparable to effort expectancy. Davis described perceived convenience as “the level to which an individual feels that utilizing a specific system would be free of charge from the initiative” [56].

Thus, the following is hypothesised:

H7.

Regarding mobile banking acceptance in Malaysia, effort expectancy measures have a significant positive relationship.

4.1.7. Social Influence (S.I.)

According to [37], social influence (S.I.) is described as “the degree to which personal views that it is vital for others (e.g., household and friends) to believe that he or she utilizes the brand innovation or even complies with others’ assumptions”. Moreover, they mentioned that social influence could positively affect an individual’s behavioural intention to adopt and utilize a technology.

In their study [64] performed a quantitative investigation of 404 individuals utilizing SEM to evaluate the sample of members depending on the factors that affect mobile banking fostering and dependence in Jordan. Their findings show that social influence has a harsh effect on the private behaviour of adopting and leaving M-banking. In addition, Ref. [53] examined the elements that impact mobile banking adoption in the north dab of Jordan amongst 579 participants. They found that social influence favours the customer’s actions for fostering, and mobile banking makes use of it.

Ref. [55] executed an empirical assessment of the intention to use the mobile settlement system in Thailand. Based upon SEM evaluation of 256 sample members’ answers and a design based upon an extended variation of the technology acceptance model (TAM), they found that subjective standards have a considerable effect on consumer embracement of M-payment services. In conclusion, this result resided in conformity, and [54], suggested that social influence positively influences pupils’ mobile phone adoption. Social influence notably impacts the behavioural intention of Understanding Administration Software at Universiti Utara Malaysia [49]. Social influence was significant in anticipating a consumer’s intention to use electronic banking in Jordan [63].

Regarding mobile banking adoption, based on a sample of 347 cases and several regression studies, Ref. [31] studied the intention to adopt financial institution services on the web for cell phone users with Malaysian Generation Y buyers in university or college, utilizing the unified theory of affirmation and usage of innovation (UTAUT). Their result revealed that social influence (S.I.) is considered a solid forecaster of the intention to adopt mobile banking. This result was sustained by [46,65], who discovered that social influence (S.I.) has a considerable influence on mobile banking adoption and behavioural intention.

Ref. [50] collected responses from a survey of 300 younger consumers of cell phone gadgets; regression tests were made use of to review the adopted (UTAUT2) model to find out the essential components that affect the behavioural intention to adopt mobile treatments (apps) in Malaysia. They disclosed that social influence (S.I.) does not determine behavioural intention in adopting mobile phone treatments. The same outcome [61] mentioned that the effect of social norms on the behavioural intention of mobile banking adoption was irrelevant.

In enhancement, Gharaibeh and Arshad (2018) [53] researched the factors that impact mobile banking adoption in the north dab of Jordan amongst 579 individuals. They found that social influence positively affects consumer actions for fostering mobile banking usage. The findings show that social influence (S.I.) does not determine behavioural intention in using mobile phone treatments.

Thus, the following is hypothesised:

H8.

Regarding mobile banking acceptance in Malaysia, social influence measures have a significant positive relationship with behavioural intention.

4.1.8. Habit (H.A.)

Habit is defined as “a perceptual construct that mirrors the results of a person’s previous experiences”. Ref. [38] stated that habit has both straight and mediated results on modern technology behavioural intention and use behaviour. Ref. [57] studied 490 mobile banking customers in Pakistan—using UTAUT2’s design, trust, and perceived threat—and ended up finding that habit (H.T.), with all other planned constructs, was a considerable forecaster in the behavioural intention to adopt mobile banking. Accordingly, Ref. [48] said that habit revealed a significant influence on the usage personality of mobile banking.

However, another meaning in which habit is constructed on previous expertise and through learning, Ref. [66] determined habit as “The magnitude to which folks tend to perform actions automatically due to learning”. Ref. [66] have included a poll and perception-based strategy for the dimension of habit. They empirically examined the design in the circumstance of wilful continuous information superhighway use. They discussed that habit had been presented to have a direct effect on everyday technology use and the effect of intention to use the technology. In the circumstance of longevity behaviour, habit has been shown to moderate the effect of purpose on the continuance of innovation and usage such that intention to proceed with use is less essential along with boosting habit.

A research study by [67] discovered that habit affects behavioural intention in taking on mobile functions. On the other side, Ref. [49] discovered that habit does not determine behavioural intention to recognize the Learning Software Program at Universiti Utara Malaysia.

Thus, the following are hypothesised:

H9.

Regarding mobile banking acceptance in Malaysia, the habit concept significantly positively influences the behavioural intention concept.

H10.

Regarding mobile banking acceptance in Malaysia, the habit concept significantly positively influences the system use concept.

4.1.9. Perceived Risk (PDR)

In their definition of perceived risk as “the capacity for loss in the interest of an intended result of making use of an e-service” [35] also recognized seven dangers related to seven possible prospective losses, such as performance, privacy, opportunity, economic, mental, social, and general threat.

In the latest research study by [64] to analyse the factors that affect mobile banking adoption and dependability, they found that safety and personal privacy threats showed a moderately damaging effect on personal habits for adoption and relying on M-banking. For [45], perceived risk (public relations) presented substantial favourable forecasters in the behavioural intention to take on mobile banking. Moreover, in an additional study in Malaysia to comprehend the barricades that impact mobile phone commerce adoption, Ref. [68] polled 227 Generation X consumers, showing that risk barricades significantly affect mobile commerce selection. One more research used the technology acceptance model (TAM) in combination with perceived risk to examine the best crucial aspects that influence the affirmation and use of mobile banking in the United Arab Emirates. Ref. [69] described their proposal design based on a sample of 90 cases coming from mobile banking clients. Within this study, the sample members pinpoint performance, time threat, and economic danger as the most necessary threats impacting the acceptance of mobile banking services. The result showed that the significant challenges of online bank services for savvy device users in the UAE are the absence of personal privacy and the minimal number of financial institutions using the services.

Ref. [70] conducted a study with 120 buyers to examine factors influencing the fostering and use of web banking services delivered to mobile phone consumers in Tanzania. Using SPSS and several regressions, results showed that perceived risk has a substantial adverse effect on adopting and using the internet bank companies supplied for smartphone consumers. Ref. [71] found that perceived risk has a negative effect on the intention to adopt mobile banking service. In another research study, which expanded the technology acceptance model (TAM) along with understanding and perceived risk, Ref. [72] evaluated 482 questions to recognize the intention to use mobile banking in Yemen. They discovered that the customer’s understanding of mobile banking companies lessens the understanding of danger. Furthermore, perceived risks (personal privacy danger, time threat, financial danger, surveillance risk, and mental risk) are attenuating the recognized convenience of utilisation and the effectiveness of mobile banking. All affect the purpose behaviour of mobile banking adoption. Ref. [73] performed a quantitative investigation of 384 participants. Their results show that perceived risk considerably impacts the client’s fostering and mobile banking actions. Two of the most impactful identified threats are functionality and personal privacy.

Thus, the following are hypothesised:

H11.

Regarding mobile banking acceptance in Malaysia, the perceived risk concept negatively influences the behavioural intention concept.

H12.

Regarding mobile banking acceptance in Malaysia, the perceived risk concept has a negative influence on the system use concept.

4.1.10. Interface Design Quality (IDQ)

The principal and first action in mobile banking is looking at the mobile screen. The mobile interface design quality is recommended for the contextual functions regarding typeface measurements, mobile phone helpful buttons, colours, and many more design qualities to promote relevant information on the display screen and discussion [74]. Consequently, bringing in a perfect first perception is essential to strike individuals [75].

Ref. [15] empirically evaluated the design appearance as an antecedent of mobile banking usage and identified that design appearance has little effect on personal computer customer perspectives. However, the author found a partial influence of customized design features. Further, Ref. [76] distinguished the customer fulfilment of mobile phone financial use in Saudi Arabia and the United Kingdom based on interface design quality. The authors’ study signifies that user interface design quality has considerable outcomes on consumer conduct and customers’ complete satisfaction in both the U.K. and Saudi Arabia.

Interface design quality was uncovered to be crucial for personal computer recommendation of technologies [77]; and alsosuggested that a cell phone user interface’s visual appeal impacts consumers’ instincts. Meanwhile, Ref. [78] found that aesthetic concepts dramatically determined looks at fulfilment. Particularly in the circumstance of mobile phone monetary applications, incorrectly created screens and customer interfaces can lead to consumers’ excessive problems, affecting their utilisation of ambience.

In another study, Ref. [79] examine the impact of interface design quality on the intention to use and use behaviour of mobile banking services in Mongolia using 209 collected questionnaires; SmartPLS was applied to analyse the data, and the findings show that interface design quality has a significant positive impact on the intention to use mobile banking services.

Thus, the following are hypothesised:

H13.

Regarding mobile banking acceptance in Malaysia, the interface design quality concept significantly influences the behavioural intention concept.

H14.

Regarding mobile banking acceptance in Malaysia, interface design quality significantly influences the system use concept.

5. Method

A research framework was designed based on the objectives, where hypotheses were established. The research objectives were examined using a quantitative approach; quantitative methods were used to prove the desired hypotheses numerically. Most deductive academic studies use the approach to achieve solid results for their examined hypotheses. Next, a questionnaire was designed, and sampling and data collection were selected.

Based on the collected data, suitable statistical analyses were carried out, followed by interpreting the results and conclusions.

The proposed model in this study is a modified model based on the UTAUT2 model. The seven determinants in the original UTAUT2 model are used in addition to two determinants, perceived risk and information system quality. The perceived risk dimension was added with the support of the perceived risk model proposed by [35], and interface design quality was added with support from the literature.

The deductive reasoning approach is the one used for the standard scientific method. The study follows purposive sampling to collect data from Malaysian Millennial mobile banking consumers using commercial or public banks in Klang Valley. The study population is Malaysian people who belong to the age group “Millennials” and use bank services offered online for smartphone users by commercial and public banks in Klang Valley, Malaysia. Millennials are a significant slice of the Malaysian population and have more technology-friendly users. The banks include the following banks: AmBank, CIMB Bank, Malayan Banking, OCBC Bank (Malaysia), Public Bank, RHB Bank, and Alliance Bank Malaysia.

The targeted sample size is 384, which exceeds the G*Power adequate sample size (166) and the minimum sample size for PLS analysis (90). After cleaning the data, the researcher plans to collect double the target sample size to secure the correct size.

A purposive sample is a non-probability sampling technique that is selected based on population features and the research goal. Purposive sampling is likewise known as judgmental, discerning, or subjective sampling. In this research, only some of the available samples are proper; only individuals with experience with mobile banking services and also from the Millennial generation were recruited [80]. Therefore, judging the sample for its suitability is essential.

SmartPLS version 3 is a software application with an aesthetically specific user interface for variance-based sequence equation modelling (SEM) utilizing the partial least squares (PLS) modelling technique. This specific investigation uses PLS to approximate the course coefficient, significance amount, electrical power evaluation, reliability, and trustworthiness assessments.

Table 1 shows the operational definition of the variables:

Table 1.

Operationalized definitions of variables.

6. Results

This section shows the results from various statistical tests, including frequencies, descriptive statistics, reliability, and regression analysis.

6.1. Reliability Test

Table 2 reveals reliability test outcomes using Cronbach Alfa values for each study variable. The stated variables in the table have a higher Cronbach Alfa than the threshold value of 0.70.

Table 2.

Pilot study reliability results.

6.2. Respondent Profile

Table 3 summarizes the counts and percentages for all the characteristics of the demographic data in this study and information of eight characteristics, i.e., gender, age, race, education level, employment status, monthly income, personal use, and experience of online banking services for smartphone users.

Table 3.

Summary of demographic characteristics of the study sample.

6.3. Descriptive Statistics

This section describes the extent to which Malaysian mobile banking customers evaluate every variable through calculating the mean value. This study explored information regarding all sixteen variables of this study. Table 4 sums up the variables’ descriptive statistics in terms of minimum, maximum, mean, and standard deviation as acquired from the descriptive analysis using the SPSS statistical package.

Table 4.

Descriptive statistics of research variables.

Malaysian customers find the performance of mobile banking services at a high level, which is consistent with the current development in online bank services offered for smartphone users in Malaysia, and they save their effort when using online bank services offered, which is a logical result of the enormous development of online bank services offered in Malaysia. Malaysian customers find their decision to use mobile banking moderately affected by society and find that online bank services are easy to achieve and adopt. Price value does not play a significant role in adopting mobile bank services, and it is moderately pleasant. Malaysian customers evaluate the financial risk of mobile banking services as only fair, and the screen and interface design quality of mobile banking services are at a medium level.

6.4. Average Variance

The study results show that all AVE values are above 0.5, ranging between 0.646 (for facilitating conditions) and 0.858 (for mobile banking use). The illustrated scores in Table 5 show that the items of every construct are interrelated, and convergent validity has been achieved.

Table 5.

Summary of average variance extracted measures.

6.5. Model Fit Examination

The study results show that all AVE values are above 0.5, ranging between 0.646 (for facilitating conditions) and 0.858 (for mobile banking use). The illustrated scores in Table 5 show that the items of every construct are interrelated, and convergent validity has been achieved.

In SEM analysis, it is common to use some measures to reveal the model’s overall reliability and validity fit [82]. SmartPLS suggests different measures as the following:

SRMR (Standardized Root Mean Square Residual)

Exact fit criteria d_ULS and d_G

NFI (Normed Fit Index)

Chi2

RMS_theta

For comparative match indices, including SRMR and NFI, scholars might assess the results of a PLS-SEM design evaluation (i.e., the outcomes state), and the rule of thumb for the proper scale values of these two scores is SRMR < 0.08 and NFI > 0.90 [82]. As illustrated in Table 6, the values of SRMR and NFI are at the proper levels; therefore, the proposed design of the model is fit and has the proper level of reliability and validity to proceed with relational examinations.

Table 6.

Summary of model fit measures.

Table 7 illustrates the calculated values of the adequate size measure for the different determinants of the proposed model. The adequate size of the variables PE, EE, Ha, FC, and IDQ on intention to use (IU) is satisfactory, ranging between 0.016 and 0.032. The variables SI, HM, PV, and PDR have an inadequate size with values less than 0.007. The variables Ha, FC, IDQ, PDR, and IU have a satisfactory level of adequate size on mobile banking use (MBU), ranging between 0.018 and 0.060.

Table 7.

Summary of Effective Size Measures.

6.6. Path Coefficient

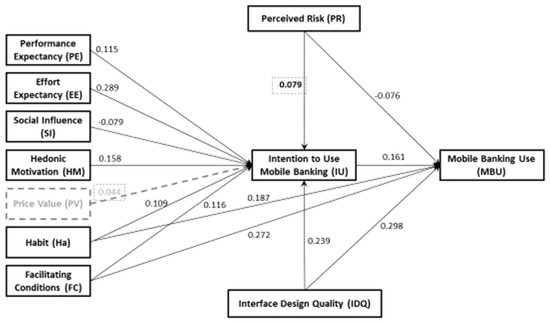

Regarding mobile banking use (MBU), the measures of relations’ significance are illustrated in Table 8. The five antecedent variables (Ha, FC, IDQ, PDR, and IU) have significant relations with MBU, with p-value scores less than 0.05 and T statistics scores higher than 1.65. The priority for the associations based upon the coefficient worth (Beta) are IDQ (0.298), Ha (0.187), FC (0.272), IU (0.161), and also PDR (−0.076). The results are visually summarized in Figure 3.

Table 8.

Summary of path coefficient measures.

Figure 3.

Path coefficient values of the proposed relational model.

For intention to use (IU), the measures of relations’ significance are illustrated in Table 8. Eight antecedent variables (EE, FC, Ha, IDQ, HM, PDR, SI and PE) have significant relations with MBU, which have p value scores less than 0.05 and have T statistics scores higher than 1.65, but one relation associated with the variables PV was rejected. The priority for the associations based upon the coefficient worth (Beta) are EE (0.289), FC (0.116), Ha (0.109), IDQ (0.239), HM (0. 0.158), PDR (−0.079), SI (−0.079), and PE (0.115). The results are visually summarized in Figure 3.

From the fourteen hypotheses, one hypothesis is rejected (H5: the relation between price value and intention to use) while all the others are accepted. Table 9 lists the hypotheses and their confirmation (or not).

Table 9.

List of the hypotheses along with their confirmation.

7. Discussion and Conclusions

RO1: To examine the determinants of intention to use mobile banking systems among Malaysian Millennials.

A literary works assessment strategy has been performed to achieve this objective. The literary works assessment strategy assists the scientist in creating a theoretical platform that comprehensively understands the relevant ideas. The leading theory of this particular study is the UTAUT 2 model, which was designed by [38]. This contemporary model was the principal resource for components of modern technology usage and the goal to utilize modern-day mobile phone financial devices.

For this research objective, seven hypotheses were designed to achieve this objective related to the original antecedents of the UTAUT2 model. Results show that performance expectancy, effort expectancy, social influence, hedonic motivation, habit, and facilitating conditions are significant antecedents for the intention to use mobile banking. However, price value was found to have no significant impact. The results are the following:

- -

- Performance expectancy’s relationship with intention to use is significant at the degree of 5% and 1-tailed degree (T-statistics = 3.122). This relationship is marked with a substantial coefficient value of Beta = 0.115.

- -

- Efforts expectancy’s relationship with intention to use is significant at the 5% significant level and 1-tailed degree (T-statistics = 6.647). This relationship is associated with a substantial coefficient value of Beta = 0.289 and a significant satisfactory measure of adequate construct size (f2 = 0.039).

- -

- Social influence’s connection to intention to use is positive and substantial at the 5% significant level and 1-tailed degree (T-statistics = 2.029). This relationship is marked with a substantial coefficient value of Beta = −0.079 and a significant satisfactory measure of adequate construct size (f2 = 0.003).

- -

- Hedonic motivation’s relationship with intention to use is positive and substantial at the 5% significant level and 1-tailed degree (T-statistics = 4.145). This relationship is discussed along with a significant coefficient value of Beta = 0.158 and a significant satisfactory measure of adequate construct size (f2 = 0.015).

- -

- Price value’s relationship with intention to use variable is not significant at the level of 5% or even a level of 10% and 1-tailed (T-statistics = 0.33). This relation is associated with an unsatisfactory measure of the adequate construct size (f2 = 0.001).

- -

- Habit’s relationship with intention to use is positive and substantial at the 5% significant level and 1-tailed degree (T-statistics = 2.553). This relationship is discussed along with a substantial coefficient value of Beta = 0.109 and a significant satisfactory measure of adequate construct size (f2 = 0.006).

- -

- The relationship between facilitating condition and intention to use is positive and substantial at the 5% significant level and 1-tailed degree (T-statistics = 3.143). This relationship is discussed along with a substantial coefficient value of Beta = 0.116 and a significant satisfactory measure of adequate construct size (f2 = 0.008).

RO2: To identify the significant dimensions of perceived risk in mobile banking use among Malaysian Millennials.

The literature suggests threat style, as suggested by [35], is the primary component of the perceived threat of present-day mobile phone financial services. The pinpointed constructs that comprise perceived risk were classified into six classes: efficiency, economical, time, emotional, social, and personal privacy.

The overall perceived risk is assumed to negatively impact the intention to use mobile banking. Perceived risk connection and intention to use are beneficial and substantial at 5% and 1-tailed degree (T-statistics = 2.706). This relationship is discussed along with a significant coefficient value of Beta = −0.079 and a significant satisfactory measure of adequate construct size (f2 = 0.005).

RO3: To assess the impact of interface design quality on intention to use mobile banking systems among Malaysian Millennials.

This study proposed a modified model with eleven variables. The interface design quality variable was added for its importance in mobile applications based on the study of [75].

Interface design quality’s relationship with intention to use is positive and substantial at the 5% significant level and 1-tailed degree (T-statistics = 6.243). This relationship is discussed along with a substantial coefficient value of Beta = 0.239 and a significant satisfactory measure of adequate construct size (f2 = 0.032).

RO4: To examine the relation between intention to use and the actual use of mobile banking among Malaysian Millennials.

The intention to use mobile banking is assumed one stage before the actual use, which is hypothesised based on the theory of planned behaviour. The intention to use connection with MBU is positive and substantial at 5% and 1-tailed degree (T-statistics = 3.819). This relationship is discussed along with a substantial coefficient value of Beta = 0.161 and a significant satisfactory measure of adequate construct size (f2 = 0.012).

RO5: To propose an improved model to assess mobile banking use among Malaysian Millennials.

This purpose was completed through utilizing a measurable technique. Analytical evaluation aids scientists in translating the pathway coefficient variations with the designed factors. The results were mainly acquired from regression-based analysis using PLS-SEM techniques. The scores of path coefficient, t values, significant values, and adequate size were used to identify the success factors. Regarding the highest outcome variable, mobile banking use, the five antecedent variables of habit, facilitating conditions, interface design quality, perceived risk, and intention to use have significant relations with mobile banking use, with p-value scores less than 0.05 and T statistics scores higher than 1.65. The priorities of the relations’ association are scored as coefficient value (Beta) and are as follows: interface design quality (0.298), habit (0.187), facilitating condition (0.272), intention to use (0.161), and also perceived risk (−0.076). Regarding the second outcome variable, intention to use, eight antecedent variables have significant relations with it, which have p-value scores less than 0.05 and have T statistics scores higher than 1.65. However, one relation associated with the variables price value was rejected. The priority of the relations’ association are scored as coefficient value (Beta) and are as follows: facilitating condition (0.116), efforts expectancy (0.289), perceived risk (−0.079), habit (0.109), hedonic motivation (0. 0.158), social influence (−0.079), performance expectancy (0.115), and interface design quality (0.239).

It is easily confirmed that research objective five was achieved using the measurable technique. Substantial distinction credit ratings were utilized to obtain the outcomes.

Ref. [28] introduced UTAUT2, which is composed of eight factors as predictors of technology use and intention (behavioural intention to use, performance expectancy, effort expectancy, social influence, facilitating conditions, hedonic motivation, price value and habit); UTAUT2 reveals 52% of the actual use of a variance. This study model developed UTAUT2 via adding another two factors; the perceived risk factor was added for its importance in mobile applications as safety, personal privacy, and financial threats showed an essential effect on personal habits for adoption and reliance on mobile banking, and the interface design quality factor was added for its importance in mobile application use and to complete the mobile information system quality scene. The developed model of this study is composed of ten factors (behavioural intention to use, performance expectancy, effort expectancy, social influence, facilitating conditions, hedonic motivation, price value, habit, perceived risk, and interface design quality) as predictors of mobile banking intention to use (IU) and mobile banking actual use (MBU). This developed model can predict 60.3% of variance in intention to use and 55.3% of variance in actual mobile banking adoption.

Results show that interface design quality is the highest predictor of actual mobile banking use and the second predictor of the intentional use of mobile banking in Malaysia. At the same time, effort expectancy is the highest predictor of intentional use, which is rationally related to interface design. When the interface design is simple and easy to use, the users will not spend much effort using it. Malaysian Millennials will be more likely to use the mobile banking service if they believe that they can handle the challenges and it is easy to use. These findings suggest that mobile application designers should develop an attractive interface design that allows users to assess mobile banking services efficiently with little effort. The following recommendations could help in designing the interface for smartphones:

- (i)

- Minimise the cognitive load for the user.

- (ii)

- Keep the content to a minimum.

- (iii)

- Keep interface elements as simple as they can be.

- (iv)

- Look for alternatives for anything that requires user effort.

- (v)

- Divide long tasks into subtasks.

- (vi)

- Use easy and familiar screens.

In addition, perceived risk was found to impact the intention to use and actual use of mobile banking in Malaysia. While this is the weakest impact, it is supposed that people become familiar with advanced technologies and feel safe using mobile apps. Therefore, the following recommendations are suggested for banking management and decision-makers:

- (i)

- Conduct campaigns and provide transparent information on the security policies used to increase users’ awareness of mobile banking use.

- (ii)

- Use recent security approaches and provide users with the information to use them.

- (iii)

- The risk dimensions include performance and time risk; therefore, an excellent interface design would help deal with those dimensions.

This study is restricted to Malaysian Millennials, so the results are limited and only represent a specific Malaysian culture and population category. Other groups in various countries could have different contextual conditions, resulting in different results. This study used closed inquiries, and there were no open-end inquiries. The opinions are limited to pre-defined variables. This research study outcome is restricted to mobile banking users only, while there are numerous other Fintech innovations such as internet repayment channels, cashless cards, digital cash, and E-wallets.

8. Recommendations for Future Research

This research proposed a developed version with new constructs and relations. While the designed model was evaluated successfully, further studies are required to assess the design in various settings. One of the restraints is the restricted method of implementation, which reduces generalisation; for that reason, reproducing the same analysis in various other financial sectors in various other nations is advised to obtain a much better understanding and generalisation.

An additional restraint is the targeted participants, as this study targeted Millennials, which reduced the potential for generalisation. So, imitating the same examination in various other teams such as Generation X or Generation Z is advised to increase generalisability and to obtain a much better understanding.

We recommend testing the design and instrument in different Fintech services or to evaluate whether this design is suitable for various other modern innovation-located approaches. Therefore, it is recommended to check the design in various scenarios and settings to enhance the generality of the designed model.

Results reveal that the recommended model can easily predict 55% of the actual use and 60% of the intentional use of mobile banking. The remaining portion (45% for actual use and 40% for intended usage) exposes yet another factor that must be dealt with in this research study. Therefore, future studies need to focus on exploring and looking at added unrevealed variables of the actual use of mobile banking.

From the quantitative analysis, price value is not considered a factor that affects the adoption and use of mobile banking, and that can be explained logically because using mobile banking applications is free of charge by most banks. However, the question is why social influence negatively predicts intention to use mobile banking in Malaysia. Therefore, further studies are invited to be conducted using interviews to explain why social influence is a weak predictor of the intention to use mobile banking.

The measurable analysis recognized that risk is the variable that affects the intention to use or use mobile phone banking the least. As a result, more academic exploration may conduct qualitative research studies using meetings to investigate why the risk variable has a negligible impact on mobile banking usage.

While it is reasonable that the best-noted variable (mobile banking use) has to possess greater power than the middle variable (intention to use), this research study reveals that the IU forecast is 5% more than the MBU forecast. These results show that the determinants of mobile banking use are different from the determinants of intention to use. This result needs even more potential investigation, and scholars are invited to explore these distinctions.

9. Patent

A newly developed model for mobile banking use with new merging of variables.

Author Contributions

All authors contributed to this paper in various ways. M.A.A.T., T.P.L.N. and D.G.F.Y. contributed to conceptualisation and methodology; M.A.A.T. carried out validation, formal analysis, and initial draft preparation; T.P.L.N. and D.G.F.Y. provided supervision; M.A/P.D. performed visualisation and editing. All authors have read and agreed to the published version of the manuscript.

Funding

This research received no external funding.

Institutional Review Board Statement

Not applicable.

Informed Consent Statement

Informed consent was obtained from all subjects involved in the study.

Data Availability Statement

Not applicable.

Acknowledgments

We appreciate all respondents’ voluntary participation in this project. Without them, this research would not be possible.

Conflicts of Interest

The authors declare no conflict of interest.

References

- Kwateng, K.O.; Atiemo, K.A.; Appiah, C. Acceptance and use of mobile banking: An application of UTAUT2. J. Enterp. Inf. Manag. 2019, 32, 118–151. [Google Scholar] [CrossRef]

- Sharma, A. Mobile Banking as Technology Adoption and Challenges: A Case of M-Banking in India. Int. J. Sci. Res. Publ. 2012, 2, 1–3. [Google Scholar]

- Kaur, B.; Madan, S. Factors Influencing Trust in Online Shopping: An Indian Consumer’s Perspective. Eur. J. Bus. Manag. 2013, 5, 132–138. [Google Scholar]

- David, H. Digital transformation in banks: The trials, opportunities and a guide to what is important. J. Digit. Bank. 2016, 1, 136–145. [Google Scholar]

- Markoska, K.; Ivanochko, I.; Gregus Ml., M. Mobile Banking Services—Business Information Management with Mobile Payments. In Agile Information Business; Flexible Systems Management; Kryvinska, N., Gregus, M., Eds.; Springer: Singapore, 2018. [Google Scholar] [CrossRef]

- Available online: https://fintechnews.my/wp-content/uploads/2021/05/Fintech-Report-Malaysia-2021-Fintech-News-Malaysia-x-BigPay.pdf (accessed on 9 February 2023).

- Krishanan, D.; Khin, A.A.; Low, K.; Teng, L. Attitude towards Using Mobile Banking in Malaysia: A Conceptual Framework. Br. J. Econ. Manag. Trade 2015, 7, 306–315. [Google Scholar] [CrossRef] [PubMed]

- Amran, A.M.; Mohamed, I.S.; Yusuf, S.N.S. Effects of recipient behaviour towards mobile banking performance in microfinance institutions. Asia-Pac. Manag. Account. J. 2018, 13, 186–206. [Google Scholar]

- Ewe, S.Y.; Yap, S.F. Understanding the fundamental building blocks of mobile banking adoption: A qualitative approach. In Proceedings of the World Business and Economics Research Conference, Auckland, New Zealand, 10–11 December 2012. [Google Scholar]

- Low, Y.M.; Goh, C.F.; Tan, O.K.; Rasli, A. Usersâ   Loyalty towards Mobile Banking in Malaysia. J. Internet Bank. Commer. 2017, 22, 1–12. [Google Scholar]

- Shaikh, A.A.; Karjaluoto, H. Mobile banking adoption: A literature review. Telemat. Inform. 2014, 32, 129–142. [Google Scholar] [CrossRef]

- Suhaimi, A.I.H.; Hassan, M.S.B.A. Determinants of Branchless Digital Banking Acceptance Among Generation Y in Malaysia. In Proceedings of the 2018 IEEE Conference on e-Learning e-Management and e-Services (IC3e), Langkawi, Malaysia, 21–22 November 2018; pp. 103–108. [Google Scholar]

- Sun, B.; Sun, C.; Liu, C.; Gui, C. Research on Initial Trust Model of Mobile Banking Users. J. Risk Anal. Crisis Response 2017, 7, 13–20. [Google Scholar] [CrossRef]

- Afshan, S.; Sharif, A. Acceptance of mobile banking framework in Pakistan. Telemat. Inform. 2016, 33, 370–387. [Google Scholar] [CrossRef]

- Lin, H.-F. An empirical investigation of mobile banking adoption: The effect of innovation attributes and knowledge-based trust. Int. J. Inf. Manag. 2011, 31, 252–260. [Google Scholar] [CrossRef]

- Zamzami, I.; Mahmud, M. Technology, CMobile Interface for m-Government Services: A Framework for Information Quality Evaluation. Int. J. Sci. Eng. Res. 2012, 3, 1–5. [Google Scholar]

- Spelman, M.; Weinelt, B.; Shah, A. Digital Transformation of Industries: Digital Enterprise. World Economic Forum White Paper. 2016. Available online: https://www.weforum.org/reports/digital-transformation-of-industries/ (accessed on 25 September 2020).

- Sarkawi, M.N.; Shamsuddin, J.; Jaafar, A.R.; Abd Rahim, N.F. Impact of GNS on the Link between Family Satisfaction and JS. Syst. 2020, 11, 36–39. [Google Scholar]

- Lee, I.; Shin, Y.J. Fintech: Ecosystem, business models, investment decisions, and challenges. Bus. Horiz. 2018, 61, 35–46. [Google Scholar] [CrossRef]

- Bank Negara Malaysia. Electronic Payments: Volume and Value of Transactions. 2015. Available online: http://www.bnm.gov.my/payment/statistics/pdf/02_epayment.pdf (accessed on 9 February 2023).

- Kupperschmidt, B.R. Multigeneration employees: Strategies for effective management. Health Care Manag. 2000, 19, 65–76. [Google Scholar] [CrossRef] [PubMed]

- Smola, K.W.E.Y.; Sutton, C.D. Generational differences: Revisiting generational work values for the new millennium. J. Organ. Behav. 2002, 382, 363–382. [Google Scholar] [CrossRef]

- Chi, C.G.; Maier, T.A.; Gursoy, D. Employees’ perceptions of younger and older managers by generation and job category. Int. J. Hosp. Manag. 2013, 34, 42–50. [Google Scholar] [CrossRef]

- Park, J.; Gursoy, D. Generation Effect on the Relationship between Work Engagement, Satisfaction, and Turnover Intention among US Hotel Employees. Int. J. Hosp. Manag. 2012, 31, 1195–1202. [Google Scholar] [CrossRef]

- Twenge, J.M.; Campbell, S.M.; Hoffman, B.J.; Lance, C.E. Generational Differences in Work Values: Leisure and Extrinsic Values Increasing, Social and Intrinsic Values Decreasing. J. Manag. 2010, 36, 1117–1142. [Google Scholar] [CrossRef]

- Yu, H.-C.; Miller, P. The generation gap and cultural influence–a Taiwan empirical investigation. Cross Cult. Manag. Int. J. 2003, 10, 23–41. [Google Scholar]

- Raphelson, S. Amid the Stereotypes, Some Facts about Millennials. NPR. 2014. Available online: https://www.npr.org/2014/11/18/354196302/amid-the-stereotypes-some-facts-about-millennials (accessed on 9 February 2023).

- Asian Institute of Finance. Bridging the Knowledge Gap of Malaysia’s Millennials. 2015. Available online: http://www.aif.org.my/clients/aif_d01/assets/multimediaMS/publication/Finance_Matters_Understanding_Gen_Y_Bridging_the_Knowledge_Gap_of_Malaysias_Millennials.pdf (accessed on 9 February 2023).

- San, L.Y.; Omar, A.; Thurasamy, R. Online Purchase: A Study of Generation Y in Malaysia. Int. J. Bus. Manag. 2015, 10, 298. [Google Scholar] [CrossRef]

- Kumar, A.; Lim, H. Age differences in mobile service perceptions: Comparison of Generation Y and baby boomers. J. Serv. Mark. 2008, 22, 568–577. [Google Scholar] [CrossRef]

- Tan, E.; Leby Lau, J. Behavioural intention to adopt mobile banking among the millennial generation. Young Consum. 2016, 17, 18–31. [Google Scholar] [CrossRef]

- Jambulingam, M.; Sorooshian, S.; Selvarajah, C.S. Tendency of generation Y in Malaysia to purchase online technological products. Int. Bus. Manag. 2016, 10, 134–146. [Google Scholar]

- Rahman, M.; Ismail, I.; Bahri, S. Analysing consumer adoption of cashless payment in Malaysia. Digit. Bus. 2020, 1, 100041. [Google Scholar] [CrossRef]

- Shams, G.; Rehman, M.A.; Samad, S.; Oikarinen, E.-L. Exploring customer’s mobile banking experiences and expectations among generations X.; Y and Z. J. Financ. Serv. Mark 2020, 25, 1–13. [Google Scholar] [CrossRef]

- Featherman, M.; Fuller, M. Applying TAM to e-services adoption: The moderating role of perceived risk. In Proceedings of the 36th Annual Hawaii International Conference on System Sciences, Big Island, HI, USA, 6–9 January 2003. [Google Scholar] [CrossRef]

- Ajzen, I. The theory of planned behaviour. Organ. Behav. Hum. Process 1991, 50, 179–211. [Google Scholar] [CrossRef]

- Venkatesh, V.; Morris, M.G.; Davis, G.B.; Davis, F.D. User acceptance of information technology: Toward a unified view. MIS Q. 2003, 27, 425–478. [Google Scholar] [CrossRef]

- Venkatesh, V.; Thong, J.Y.L.; Xu, X. Consumer acceptance and use of information technology: Extending the unified theory of acceptance and use of technology. Theory Plan. Behav. 2012, 36, 157–178. [Google Scholar] [CrossRef]

- Tarhini, A.; El-masri, M.; Ali, M.; Serrano, A. Extending the UTAUT model to understand the customers ’ acceptance and use of internet banking in Lebanon A structural equation modeling approach. People 2016, 29, 830–849. [Google Scholar] [CrossRef]

- Im, I.; Hong, S.; Kang, M.S. An international comparison of technology adoption. Inf. Manag. 2011, 48, 1–8. [Google Scholar] [CrossRef]

- Yu, C.-S. Factors Affecting Individuals to Adopt Mobile Banking: Empirical Evidence from the UTAUT Model. J. Electron. Commer. Res. 2012, 13, 104–121. [Google Scholar]

- Ali, M.; Kan, K.A.S.; Sarstedt, M. Direct and configurational paths of absorptive capacity and organizational innovation to successful organizational performance. J. Bus. Res. 2016, 69, 5317–5323. [Google Scholar] [CrossRef]

- Al-qeisi, K.; Dennis, C.; Hegazy, A.; Abbad, M. How Viable Is the UTAUT Model in a Non-Western Context? Int. Bus. Res. 2015, 8, 204–219. [Google Scholar] [CrossRef]

- Mostafa, A.A.N.; Eneizan, B. Factors Affecting Acceptance of Mobile Banking in Developing Countries. Int. J. Acad. Res. Bus. Soc. Sci. 2018, 8, 340–351. [Google Scholar] [CrossRef]

- Farah, M.F.; Hasni, M.J.S.; Abbas, A.K. Mobile-banking adoption: Empirical evidence from the banking sector in Pakistan. Int. J. Bank Mark. 2018, 36, 1386–1413. [Google Scholar] [CrossRef]

- Hassan, J. Investigating the Determinants Impacting Adoption of Mobile Banking: Evidence from Jammu and Kashmir. J. Internet Bank. Commer. 2022, 27, 1–14. [Google Scholar]

- Mehra, A.; Rajput, S.; Paul, J. Determinants of adoption of latest version smartphones: Theory and evidence. Technol. Forecast. Soc. Change 2022, 175, 121410. [Google Scholar] [CrossRef]

- Baabdullah, A.M.; Alalwan, A.A.; Rana, N.P.; Kizgin, H.; Patil, P. Consumer use of mobile banking (M-Banking) in Saudi Arabia: Towards an integrated model. Int. J. Inf. Manag. 2019, 44, 38–52. [Google Scholar] [CrossRef]

- Raman, A.; Don, Y. Preservice teachers’ acceptance of learning management software: An application of the UTAUT2 model. Int. Educ. Stud. 2013, 6, 157–164. [Google Scholar] [CrossRef]

- Kit, A.H.L.; Ni, A.H.; Badri, M.; Nur Freida, E.; Tang, K.Y. UTAUT2 influencing the behavioural intention to adopt mobile applications. Bachelor’s Thesis, Universiti Tunku Abdul Rahman, Kampar, Malaysia, 2014. [Google Scholar]

- Slade, E.L.; Dwivedi, Y.K.; Piercy, N.C.; Williams, M.D. Modeling Consumers’ Adoption Intentions of Remote Mobile Payments in the United Kingdom: Extending UTAUT with Innovativeness, Ris, and University of Bristol—Explore Bristol Research. Psychol. Mark. 2015, 32, 860–873. [Google Scholar] [CrossRef]

- Alalwan, A.A.; Dwivedi, Y.K.; Rana, N.P. Factors influencing adoption of mobile banking by Jordanian bank customers: Extending UTAUT2 with trust. Int. J. Inf. Manag. 2017, 37, 99–110. [Google Scholar] [CrossRef]

- Gharaibeh, M.K.; Arshad, M.R.M. Determinants of intention to use mobile banking in the North of Jordan: Extending UTAUT2 with mass media and trust. J. Eng. Appl. Sci. 2018, 13, 2023–2033. [Google Scholar]

- Yang, S. Understanding Undergraduate Students’ Adoption of Mobile Learning Model: A Perspective of the Extended UTAUT2. J. Converg. Inf. Technol. 2013, 8, 969–979. [Google Scholar] [CrossRef]

- Phonthanukitithaworn, C.; Sellitto, C.; Fong, M.W.L. User intentions to adopt mobile payment services: A study of early adopters in Thailand. J. Internet Bank. Commer. 2015, 20, 1–29. [Google Scholar]

- Davis, F.F.D. Perceived Usefulness, Perceived Ease of Use, and User Acceptance of Information Technology. MIS Q. 1989, 13, 319–340. Available online: http://www.jstor.org/stable/10.2307/249008 (accessed on 9 February 2023). [CrossRef]