The Impact of Environmental Uncertainty on Corporate Innovation: Evidence from Chinese Listed Companies

Abstract

:1. Introduction

2. Literature Review and Hypothesis Development

3. Research Design

3.1. Sample Selection and Data Sources

3.2. Variable Definition and Description

3.2.1. Corporate Innovation (rd)

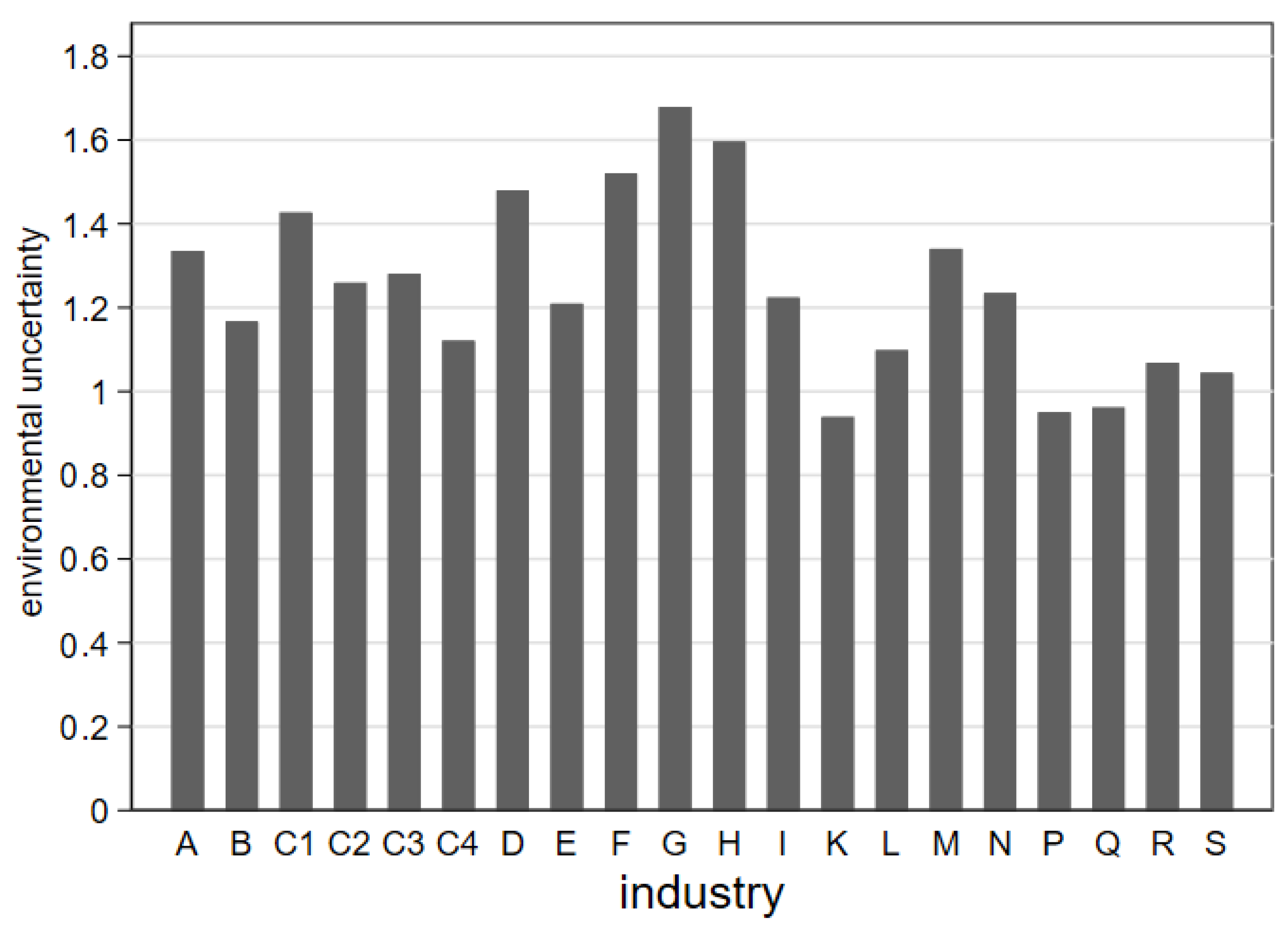

3.2.2. Environmental Uncertainty (eu)

3.2.3. Risk-Taking Ability

3.2.4. Control Variables

3.3. Model Specification

4. Analysis of Empirical Results

4.1. Descriptive Analysis

4.2. Correlation Analysis

4.3. Analysis of Basic Regression Results

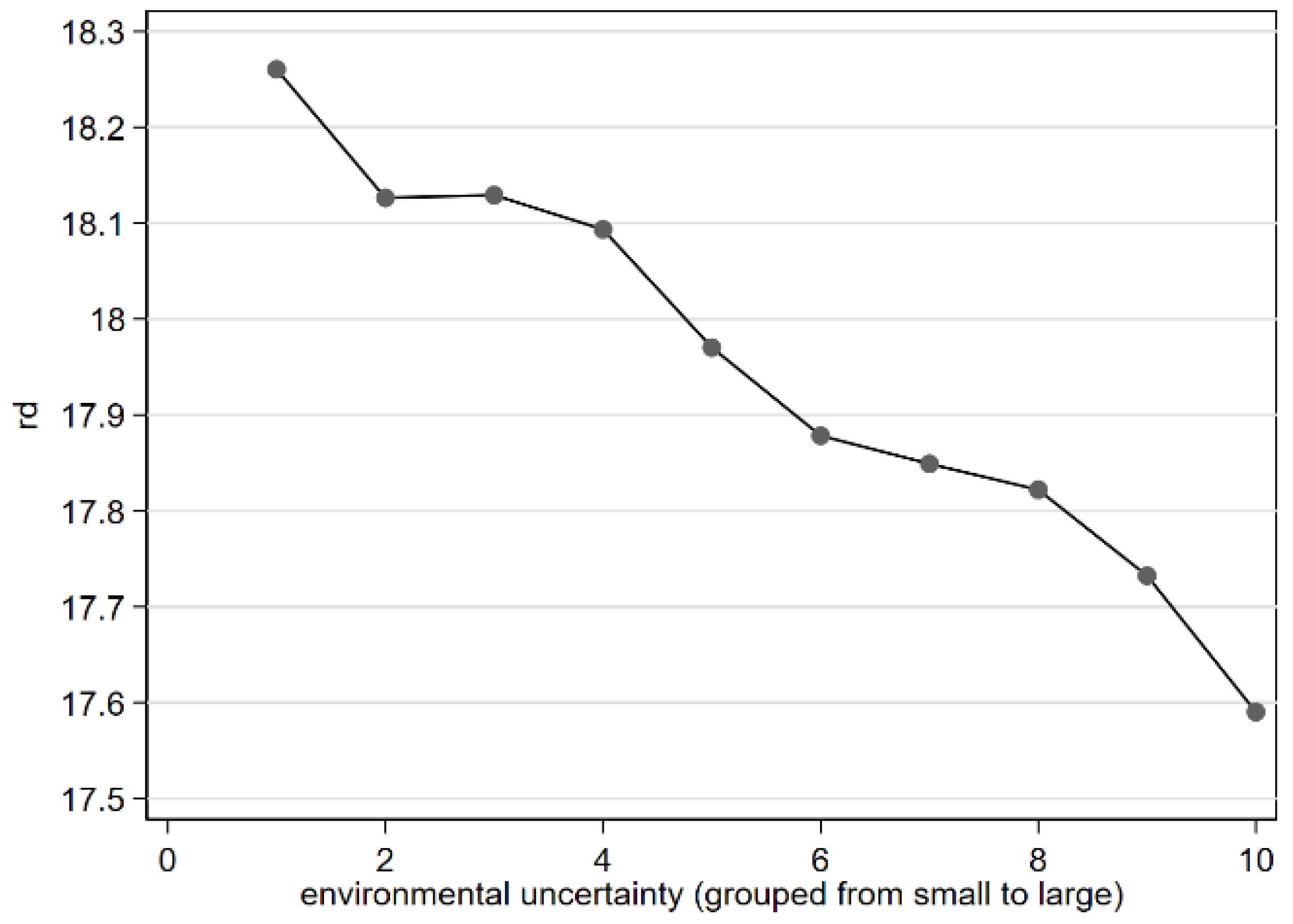

4.3.1. The Impact of Environmental Uncertainty on Corporate Innovation

4.3.2. Heterogeneity Analysis

4.4. Further Discussion: The Mediating Effect of Financing Constraints

4.5. Robustness Test

4.5.1. Endogeneity Test

4.5.2. Change the Sample Interval

4.5.3. Test Nonlinearity

4.5.4. Replace Corporate Innovation Indicators

5. Conclusions and Implications

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Acknowledgments

Conflicts of Interest

References

- Romer, P. The origins of endogenous growth. J. Econ. Perspect. 1994, 8, 3–22. [Google Scholar] [CrossRef] [Green Version]

- He, F.; Ma, Y.; Zhang, X. How does economic policy uncertainty affect corporate Innovation?—Evidence from China listed companies. Int. Rev. Econ. Financ. 2020, 67, 225–239. [Google Scholar] [CrossRef]

- Li, K.; Xia, B.; Chen, Y.; Ding, N.; Wang, J. Environmental uncertainty, financing constraints and corporate investment: Evidence from China. Pac.-Basin Financ. J. 2021, 70, 3–22. [Google Scholar] [CrossRef]

- Baker, S.R.; Bloom, N.; Davis, S.J. Measuring economic policy uncertainty. Q. J. Econ. 2016, 131, 1593–1636. [Google Scholar] [CrossRef]

- Julio, B.; Yook, Y. Political uncertainty and corporate investment cycles. J. Financ. 2012, 67, 45–83. [Google Scholar] [CrossRef]

- Boyle, G.W.; Guthrie, G.A. Investment, uncertainty and liquidity. J. Financ. 2003, 58, 2143–2166. [Google Scholar] [CrossRef] [Green Version]

- Minton, B.A.; Schrand, C. The impact of cash flow volatility on discretionary investment and the costs of debt and equity financing. J. Financ. Econ. 1999, 54, 423–460. [Google Scholar] [CrossRef] [Green Version]

- Liu, B.; Li, Z.; Wang, H.; Yang, J. Cash flow uncertainty and corporate innovation. Econ. Res. J. 2017, 3, 166–180. (In Chinese) [Google Scholar]

- Gilchrist, S.; Sim, J.W.; Zakrajek, E. Uncertainty, financial frictions, and investment dynamics. J. Financ. Econ. Discuss. Ser. 2014, 69, 1–58. [Google Scholar] [CrossRef]

- Huang, Y.; Luk, P. Measuring economic policy uncertainty in China. China Econ. Rev. 2020, 59, 101367. [Google Scholar] [CrossRef]

- Guan, J.; Xu, H.; Huo, D.; Hua, Y.; Wang, Y. Economic policy uncertainty and corporate innovation: Evidence from China. Pac.-Basin Financ. J. 2021, 67, 101542. [Google Scholar] [CrossRef]

- Steven, J.; Davis, D.Q.; Sheng, X.G. Economic Policy Uncertainty in China since 1949. Mainland Newspapers, 2019. Available online: https://stevenjdavis.com/s/EPU-in-China-View-from-Mainland-Newspapers-August-2019.pdf(accessed on 15 December 2021).

- Cao, Y.; Chen, Y.; Zhang, Y. Political uncertainty, innovation-driven strategy, and corporate R&D. Res. Int. Bus. Financ. 2022, 60, 101612. [Google Scholar] [CrossRef]

- Pertuze, J.A.; Reyes, T.; Vassolo, R.S.; Olivares, N. Political uncertainty and innovation: The relative effects of national leaders’ education levels and regime systems on firm-level patent applications. Res. Policy 2019, 48, 103808. [Google Scholar] [CrossRef]

- Govindarajan, V.J. Appropriateness of accounting data in performance evaluation: An empirical examination of environmental uncertainty as an intervening variable. Account. Organ. Soc. 1984, 9, 125–135. [Google Scholar] [CrossRef]

- Shen, H.; Yu, P.; Wu, L. State ownership, environmental uncertainty and investment efficiency. Econ. Res. J. 2012, 7, 113–126. (In Chinese) [Google Scholar]

- Bloom, N.; Stephen, B.; John, V.R. Uncertainty and investment dynamics. J. Rev. Econ. Stud. 2007, 74, 391–415. [Google Scholar] [CrossRef] [Green Version]

- Wang, Y.; Chen, C.R.; Huang, Y.S. Economic policy uncertainty and corporate investment: Evidence from China. Pac.-Basin Financ. J. 2014, 26, 227–243. [Google Scholar] [CrossRef]

- Kim, H.; Kung, H. The asset redeployability channel: How uncertainty affects corporate investment. J. Rev. Financ. Stud. 2017, 30, 245–280. [Google Scholar] [CrossRef]

- Chen, X.; Le, C.H.A.; Shan, Y.; Taylor, S. Australian policy uncertainty and corporate investment. Pac.-Basin Financ. J. 2020, 61, 101341. [Google Scholar] [CrossRef]

- Hall, B. The financing of research and development. Oxf. Rev. Econ. Policy 2002, 18, 35–51. [Google Scholar] [CrossRef]

- P’astor, Ľ.; Veronesi, P. Political uncertainty and risk premia. J. Financ. Econ. 2013, 110, 520–545. [Google Scholar] [CrossRef] [Green Version]

- Allen, F.; Qian, J.; Qian, M.J. Law, finance, and economic growth in China. J. Financ. Econ. 2005, 77, 57–116. [Google Scholar] [CrossRef] [Green Version]

- Gordon, R.; Li, W. Government as a discriminating monopolist in the financial market: The case of China. J. Public Econ. 2003, 87, 283–312. [Google Scholar] [CrossRef] [Green Version]

- Lee, C.; Wang, C.; Ho, S. Financial innovation and bank growth: The role of institutional environments. N. Am. J. Econ. Financ. 2020, 53, 101195. [Google Scholar] [CrossRef]

- Ghosh, D.; Olsen, L. Environmental uncertainty and managers’ use of discretionary accruals. Account. Organ. Soc. 2009, 34, 188–205. [Google Scholar] [CrossRef]

- Phan, H.V.; Nguyen, N.H.; Nguyen, H.T.; Hegde, S. Policy uncertainty and firm cash holdings. J. Bus. Res. 2019, 95, 71–82. [Google Scholar] [CrossRef]

- Gulen, H.; Ion, M. Policy uncertainty and corporate investment. Rev. Financ. Stud. 2016, 29, 523–564. [Google Scholar] [CrossRef]

- Hua, F.; Xu, F. How does environmental uncertainty affect corporate idiosyncratic risk—An intermediary effect test based on cash flow fluctuation and accounting information quality. Nankai Bus. Rev. 2018, 21, 122–133. (In Chinese) [Google Scholar]

- Liao, Y. Environmental uncertainty, diversification and cost of equity capital. J. Financ. Theory Pract. 2015, 1, 78–83. (In Chinese) [Google Scholar]

- Wang, H.; Chen, X. Corporate governance, environmental uncertainty and debt capital cost. J. Nanjing Audit Univ. 2016, 5, 66–74. (In Chinese) [Google Scholar]

- Manso, G. Motivating innovation. J. Financ. 2011, 66, 1823–1860. [Google Scholar] [CrossRef] [Green Version]

- Lou, Z.; Chen, S.; Yin, W.; Zhang, C.; Yu, X. Economic policy uncertainty and corporate innovation: Evidence from a risk-taking perspective. Int. Rev. Econ. Financ. 2022, 77, 78–96. [Google Scholar] [CrossRef]

- Duncan, R.B. Characteristics of organizational environments and perceived environmental uncertainty. Admin. Sci. Q. 1972, 17, 313–327. [Google Scholar] [CrossRef] [Green Version]

- Tan, J. Innovation and risk-taking in a Transitional Economy: A comparative study of Chinese managers and entrepreneurs. J. Bus. Ventur. 2001, 16, 359–376. [Google Scholar] [CrossRef]

- Tosi, H.; Aldag, R.; Storey, R. On the measurement of the environment: An assessment of the lawrence and lorsch environmental uncertainty subscale. Adm. Sci. 1973, 18, 27–36. [Google Scholar] [CrossRef]

- Bergh, D.D.; Lawless, M.W. Portfolio restructuring and limits to hierarchical governance: The effects of environmen-tal uncertainty and diversification strategy. Organ. Sci. 1998, 9, 87–102. [Google Scholar] [CrossRef]

- Mishra, R.; Mishra, O.N. Prioritising dimensions of entrepreneurial orientation for supply chain flexibility development in an uncertain environment. J. Manuf. Technol. Manag. 2019, 30, 483–505. [Google Scholar] [CrossRef]

- Rao, P.; Xu, Z. Does economic policy uncertainty affect corporate executive change? Man World 2017, 1, 45–157. (In Chinese) [Google Scholar]

- Chang, C.; Chen, X.; Liao, G. What are the reliably important determinants of capital structure in China? Pac.-Basin Financ. J. 2014, 30, 87–113. [Google Scholar] [CrossRef]

- Lu, Z.; He, J.; Dou, H. Whose leverage is more excessed, State-owned or non-state-owned enterprises? Econ. Res. J. 2015, 12, 54–67. (In Chinese) [Google Scholar]

- Walls, M.R.; Dyer, J.S. Risk propensity and firm performance: A study of the petroleum exploration industry. Manag. Sci. 1996, 42, 1004–1021. [Google Scholar] [CrossRef]

- Talavera, O.; Tsapin, A.; Zholud, O. Macroeconomic uncertainty and Bank lending: The case of Ukraine. J. Econ. Syst. 2012, 46, 279–293. [Google Scholar] [CrossRef] [Green Version]

- Baron, R.M.; Kenny, D.A. The moderator-mediator variable distinction in social psychological research: Conceptual, strategic, and statistical considerations. J. Personal. Soc. Psychol. 1986, 51, 1173–1182. [Google Scholar] [CrossRef]

- Kaplan, S.N.; Zingales, L. Do investment-cash flow sensitivities provide useful measures of financing constraints? Q. J. Econ. 1997, 112, 169–215. [Google Scholar] [CrossRef] [Green Version]

- Lewbel, A. Constructing instruments for regressions with measurement error when no additional data are available. Econometrica 1997, 65, 1201–1213. [Google Scholar] [CrossRef]

- Tajaddini, R.; Gholipour, H.F. Economic policy uncertainty, R&D expenditures and innovation outputs. J. Econ. Stud. 2021, 48, 413–427. [Google Scholar] [CrossRef]

- Shen, H.; Hou, F. Trade policy uncertainty and corporate innovation evidence from Chinese listed firms in new energy vehicle industry. Energy Econ. 2021, 97, 105217. [Google Scholar] [CrossRef]

- Zhang, C.; Sun, Y.; Lu, X. Cash flow uncertainty, managers’ risk preference and corporate innovation. J. Zhongnan Univ. Econ. Law 2019, 6, 71–81. (In Chinese) [Google Scholar]

{kind=link}

{kind=link}

{kind=link}

| Variables | Symbol | Description |

|---|---|---|

| Corporate innovation | rd | The natural logarithm of firm R&D spending |

| Environmental uncertainty | eu | For the fluctuation of corporation sales revenue, see the model for the specific calculation method (1) |

| Profitability | roa | Net profit/Total assets |

| Corporate growth | grow | Growth rate of operating income, current year operating income/same period last year operating income |

| Corporate leverage ratio | lev | Total liabilities/Total assets |

| Capital intensity | fixed | Fixed assets ratio, fixed assets to total assets |

| Investment opportunities | tobinq | Market value/Total assets |

| Company scale | size | The natural logarithm of a firm’s total assets at the end |

| Ownership concentration | shrcr1 | Shareholding ratio of the largest shareholder |

| Board size | board | The natural log of the number of board members |

| Proportion of independent directors | indep | Number of independent directors/number of directors |

| Variable | Obs. | Mean | Std. Dev. | Min | Median | Max |

|---|---|---|---|---|---|---|

| rd | 15,096 | 17.95 | 1.623 | 13.192 | 18.011 | 22.04 |

| eu | 15,096 | 1.284 | 1.281 | 0.010 | 0.953 | 23.62 |

| roa | 15,096 | 0.032 | 0.065 | −0.285 | 0.032 | 0.197 |

| grow | 15,096 | 0.150 | 0.377 | −0.493 | 0.092 | 2.370 |

| lev | 15,096 | 0.442 | 0.194 | 0.068 | 0.439 | 0.869 |

| fixed | 15,096 | 0.222 | 0.153 | 0.005 | 0.192 | 0.677 |

| tobinq | 15,096 | 2.071 | 1.294 | 0.845 | 1.657 | 8.137 |

| size | 15,096 | 22.457 | 1.253 | 20.122 | 22.219 | 26.337 |

| shrcr1 | 15,096 | 0.335 | 0.143 | 0.090 | 0.312 | 0.729 |

| indep | 15,096 | 0.375 | 0.054 | 0.333 | 0.333 | 0.571 |

| board | 15,096 | 2.140 | 0.197 | 1.609 | 2.197 | 2.708 |

| rd | eu | roa | grow | lev | fixed | tobinq | size | shrcr1 | indep | board | |

| rd | 1 | ||||||||||

| eu | −0.091 *** | 1 | |||||||||

| roa | 0.131 *** | −0.088 *** | 1 | ||||||||

| grow | 0.047 *** | 0.435 *** | 0.236 *** | 1 | |||||||

| lev | 0.117 *** | 0.041 *** | −0.306 *** | 0.014 * | 1 | ||||||

| fixed | −0.080 *** | −0.038 *** | −0.056 *** | −0.064 *** | 0.088 *** | 1 | |||||

| tobinq | −0.140 *** | −0.0120 | 0.208 *** | 0.044 *** | −0.352 *** | −0.125 *** | 1 | ||||

| size | 0.497 *** | −0.014 * | 0.063 *** | 0.043 *** | 0.481 *** | 0.086 *** | −0.438 *** | 1 | |||

| shrcr1 | 0.062 *** | 0.009 | 0.118 *** | −0.003 | 0.116 *** | 0.122 *** | −0.067 *** | 0.269 *** | 1 | ||

| indep | 0.043 *** | −0.017 ** | −0.020 ** | −0.018 ** | −0.006 | −0.038 *** | 0.035 *** | 0.035 *** | 0.047 *** | 1 | |

| board | 0.056 *** | −0.036 *** | 0.035 *** | −0.005 | 0.160 *** | 0.147 *** | −0.132 *** | 0.244 *** | 0.058 *** | −0.515 *** | 1 |

| (1) Full Sample | (2) Full Sample | (3) High eu | (4) Low eu | |

|---|---|---|---|---|

| rd | rd | rd | rd | |

| eu | −0.1288 *** | −0.1088 *** | −0.0568 *** | −0.1528 |

| (−11.4358) | (−10.5367) | (−3.7152) | (−1.1460) | |

| roa | 0.7005 *** | 1.5276 *** | 0.8322 *** | 2.3660 *** |

| (3.6494) | (8.3534) | (2.8180) | (5.7890) | |

| grow | 0.2180 *** | 0.2038 *** | 0.1529 *** | 1.0516 *** |

| (5.8768) | (6.3107) | (4.0353) | (5.2910) | |

| lev | −1.0221 *** | −0.5370 *** | −0.4996 *** | −0.4763 *** |

| (−13.8103) | (−8.0060) | (−3.9083) | (−3.2425) | |

| fixed | −1.0359 *** | −0.5045 *** | −0.4976 *** | −0.5122 *** |

| (−11.6247) | (−6.4248) | (−3.0507) | (−3.1803) | |

| tobinq | 0.0663 *** | 0.0496 *** | 0.0272 | 0.0458 *** |

| (7.3352) | (5.6923) | (1.3981) | (2.8548) | |

| size | 0.7974 *** | 0.8387 *** | 0.8289 *** | 0.8039 *** |

| (61.2848) | (75.6083) | (36.3822) | (36.3281) | |

| shrcrl | −0.8200 *** | −0.1623 ** | 0.2159 | −0.1108 |

| (−9.5596) | (−2.3898) | (1.4873) | (−0.9306) | |

| indep | −0.3461 | 0.0194 | −1.0896 ** | 0.3228 |

| (−1.3776) | (0.0948) | (−2.3247) | (0.9232) | |

| board | −0.4838 *** | −0.0842 | −0.4143 *** | 0.2430 ** |

| (−6.4769) | (−1.3414) | (−3.0962) | (2.0981) | |

| _cons | 2.1326 *** | −2.2677 *** | −1.1682 * | −3.0147 *** |

| (6.5042) | (−7.5747) | (−1.9352) | (−5.1441) | |

| Industry | No | Yes | Yes | Yes |

| Year | No | Yes | Yes | Yes |

| r2_a | 0.2986 | 0.5314 | 0.4644 | 0.6074 |

| N | 15096 | 15096 | 3774 | 3774 |

| (1) State-Owned | (2) Non State-Owned | (3) Large Scale | (4) Small Scale | (5) High Profitability | (6) Low Profitability | |

|---|---|---|---|---|---|---|

| rd | rd | rd | rd | rd | rd | |

| eu | −0.1046 *** | −0.1235 *** | −0.0997 *** | −0.1191 *** | −0.0887 *** | −0.1087 *** |

| (−6.2379) | (−10.0907) | (−6.2455) | (−8.8815) | (−8.1544) | (−9.1431) | |

| roa | 1.8904 *** | 1.1391 *** | 1.7198 *** | 1.1454 *** | 1.1101 *** | 0.5381 ** |

| (4.7607) | (5.7320) | (5.0273) | (5.6101) | (4.8425) | (2.0764) | |

| grow | 0.1950 *** | 0.2122 *** | 0.1952 *** | 0.2048 *** | 0.1916 *** | 0.2376 *** |

| (3.6803) | (5.3090) | (3.9395) | (5.0086) | (4.7837) | (5.7701) | |

| lev | −0.7658 *** | −0.3983 *** | −0.7673 *** | −0.3352 *** | 0.2267 *** | −0.5995 *** |

| (−6.9041) | (−4.8163) | (−6.9631) | (−4.0296) | (2.5884) | (−6.5141) | |

| fixed | −0.7372 *** | −0.0245 | −0.3990 *** | −0.5084 *** | −0.3487 *** | −0.2922 *** |

| (−6.1041) | (−0.2537) | (−3.6365) | (−4.6136) | (−3.6603) | (−2.8585) | |

| tobin | 0.0012 | 0.0828 *** | 0.1165 *** | 0.0318 *** | 0.0673 *** | 0.0007 |

| (0.0757) | (8.2762) | (6.9039) | (3.0992) | (6.6513) | (0.0445) | |

| size | 0.8268 *** | 0.8710 *** | 0.8119 *** | 0.9181 *** | 0.8028 *** | 0.8108 *** |

| (47.9600) | (60.0903) | (42.3463) | (37.3910) | (59.8440) | (50.4107) | |

| shrcr1 | 0.0267 | −0.1375 * | 0.1689 * | −0.4815 *** | −0.2388 *** | −0.1257 |

| (0.2323) | (−1.6543) | (1.7303) | (−5.5436) | (−2.8480) | (−1.1891) | |

| indep | 0.1360 | 0.3907 | 0.1774 | 0.2280 | −0.0246 | 0.4613 |

| (0.4290) | (1.5053) | (0.6033) | (0.8650) | (−0.0949) | (1.5563) | |

| board | −0.1296 | 0.1805 ** | −0.1631 * | 0.0121 | −0.0305 | −0.0793 |

| (−1.3290) | (2.2818) | (−1.8109) | (0.1543) | (−0.4182) | (−0.9039) | |

| _cons | −1.7673 *** | −3.9557 *** | −2.3374 *** | −3.9096 *** | −1.7033 *** | −1.9717 *** |

| (−4.0876) | (−9.3529) | (−4.8723) | (−6.7960) | (−4.8658) | (−4.9036) | |

| Industry | Yes | Yes | Yes | Yes | Yes | Yes |

| Year | Yes | Yes | Yes | Yes | Yes | Yes |

| r2_a | 0.5792 | 0.5080 | 0.5117 | 0.4091 | 0.5570 | 0.5203 |

| N | 6297 | 8799 | 7545 | 7551 | 7546 | 7550 |

| (1) | (2) | (3) | |

|---|---|---|---|

| rd | kz | rd | |

| eu | −0.1088 *** | 0.0798 *** | −0.1048 *** |

| (−10.5367) | (6.5151) | (−10.2109) | |

| kz | −0.0503 *** | ||

| (−7.7809) | |||

| roa | 1.5276 *** | −11.7026 *** | 0.9394 *** |

| (8.3534) | (−38.5334) | (4.7492) | |

| grow | 0.2038 *** | −0.2288 *** | 0.1923 *** |

| (6.3107) | (−4.7984) | (5.9608) | |

| lev | −0.5370 *** | 5.9079 *** | −0.2400 *** |

| (−8.0060) | (67.5686) | (−3.1635) | |

| fixed | −0.5045 *** | 0.5639 *** | −0.4762 *** |

| (−6.4248) | (6.6753) | (−6.0516) | |

| tobinq | 0.0496 *** | 0.2017 *** | 0.0598 *** |

| (5.6923) | (13.6632) | (6.8856) | |

| size | 0.8387 *** | −0.2364 *** | 0.8269 *** |

| (75.6083) | (−16.6555) | (73.6675) | |

| shrcr1 | −0.1623 ** | −0.7924 *** | −0.2021 *** |

| (−2.3898) | (−8.9956) | (−2.9657) | |

| indep | 0.0194 | 0.5466 ** | 0.0468 |

| (0.0948) | (2.1145) | (0.2297) | |

| board | −0.0842 | −0.1133 | −0.0899 |

| (−1.3414) | (−1.4987) | (−1.4334) | |

| _cons | −2.2677 *** | 2.1873 *** | −2.1577 *** |

| (−7.5747) | (6.0237) | (−7.2040) | |

| Industry | Yes | Yes | Yes |

| Year | Yes | Yes | Yes |

| r2_a | 0.5314 | 0.5310 | 0.5334 |

| N | 15096 | 15096 | 15096 |

| (1) IV: l.eu l2.eu | (2) IV: (eu-eu_mean)^3 | |

|---|---|---|

| rd | rd | |

| eu | −0.1539 *** | −0.0422 ** |

| (−9.7036) | (−2.4876) | |

| roa | 0.8542 *** | 1.8184 *** |

| (4.2711) | (10.0114) | |

| grow | 0.3099 *** | 0.0898 ** |

| (7.5332) | (2.3313) | |

| lev | −0.4882 *** | −0.5314 *** |

| (−6.6052) | (−8.4878) | |

| fixed | −0.2722 *** | −0.4672 *** |

| (−3.2877) | (−6.6113) | |

| tobinq | 0.0611 *** | 0.0505 *** |

| (5.8060) | (5.7669) | |

| size | 0.8619 *** | 0.8401 *** |

| (71.3388) | (80.9256) | |

| shrcr1 | −0.1476 * | −0.1885 *** |

| (−1.8220) | (−2.7566) | |

| indep | −0.2594 | 0.0712 |

| (−1.1130) | (0.3548) | |

| board | −0.1561 ** | −0.0686 |

| (−2.3229) | (−1.1831) | |

| _cons | −1.3026 *** | −2.4381 *** |

| (−4.2689) | (−9.0974) | |

| Industry | Yes | Yes |

| Year | Yes | Yes |

| r2_a | 0.5554 | 0.5293 |

| N | 9406 | 15096 |

| (1) | (2) | (3) | (4) | |

|---|---|---|---|---|

| rd | rd | rd | rd_1 | |

| eu | −0.1395 *** | −0.1103 *** | −0.1725 *** | −0.1396 *** |

| (−12.2073) | (−9.5640) | (−10.8257) | (−12.0824) | |

| eu2 | 0.0077 *** | |||

| (4.1526) | ||||

| roa | 1.6960 *** | 1.7295 *** | 1.4484 *** | 2.3075 *** |

| (8.1958) | (8.2794) | (7.9235) | (8.1399) | |

| grow | 0.2700 *** | 0.1964 *** | 0.1960 *** | 0.2043 *** |

| (7.2198) | (5.5036) | (6.1127) | (5.2142) | |

| lev | −0.4581 *** | −0.5380 *** | −0.5374 *** | −0.1790 ** |

| (−6.2062) | (−7.2115) | (−8.0213) | (−2.0546) | |

| fixed | −0.4688 *** | −0.4819 *** | −0.5154 *** | −0.7957 *** |

| (−5.5987) | (−5.5012) | (−6.5639) | (−8.9158) | |

| tobin | 0.0296 *** | 0.0334 *** | 0.0498 *** | 0.2084 *** |

| (3.1211) | (3.2672) | (5.7359) | (12.6477) | |

| size | 0.8899 *** | 0.8238 *** | 0.8378 *** | −0.0754 *** |

| (73.6202) | (63.4994) | (75.6264) | (−5.0941) | |

| shrcr1 | −0.0107 | −0.1034 | −0.1684 ** | −0.2008 ** |

| (−0.1489) | (−1.3614) | (−2.4817) | (−2.2924) | |

| indep | 0.0428 | 0.0065 | −0.0009 | 0.3596 |

| (0.1975) | (0.0285) | (−0.0046) | (1.3398) | |

| board | −0.1822 *** | −0.1137 | −0.0920 | −0.0940 |

| (−2.7251) | (−1.6220) | (−1.4690) | (−1.1240) | |

| _cons | −2.6925 *** | −1.5434 *** | −2.1527 *** | 1.6915 *** |

| (−8.5889) | (−4.7288) | (−7.1817) | (4.6244) | |

| Industry | Yes | Yes | Yes | Yes |

| Year | Yes | Yes | Yes | Yes |

| r2_a | 0.5568 | 0.5145 | 0.5325 | 0.3202 |

| N | 10781 | 12222 | 15096 | 15096 |

| (1) | (2) | (3) | (4) | |

|---|---|---|---|---|

| patent 1 | patent 2 | patent 3 | patent 4 | |

| L.eu | −0.1193 *** | −0.1348 *** | −0.1017 *** | −0.1004 *** |

| (−9.4345) | (−9.2191) | (−8.6389) | (−8.4620) | |

| L.roa | 1.8817 *** | 1.9549 *** | 1.2334 *** | 1.8517 *** |

| (7.5207) | (6.7852) | (5.3665) | (7.5466) | |

| L.grow | 0.2373 *** | 0.2773 *** | 0.2178 *** | 0.1962 *** |

| (5.8867) | (5.9609) | (5.7555) | (5.1064) | |

| L.lev | −0.0173 | −0.0603 | −0.1767 ** | 0.1843 ** |

| (−0.2042) | (−0.6256) | (−2.2218) | (2.2091) | |

| L.fixed | −1.1145 *** | −1.2121 *** | −1.0956 *** | −0.8516 *** |

| (−11.6627) | (−11.1505) | (−12.2763) | (−9.0612) | |

| L.tobin | 0.0077 | 0.0035 | 0.0508 *** | −0.0249 ** |

| (0.6301) | (0.2506) | (4.4170) | (−2.0612) | |

| L.size | 0.5537 *** | 0.5970 *** | 0.5772 *** | 0.4649 *** |

| (38.6018) | (37.1524) | (41.3068) | (32.7929) | |

| L.shrcr1 | −0.4416 *** | −0.5654 *** | −0.4712 *** | −0.2320 ** |

| (−4.7689) | (−5.3667) | (−5.3115) | (−2.5538) | |

| L.indep | 0.3820 | 0.5244 * | 0.6527 ** | 0.0922 |

| (1.4333) | (1.7545) | (2.5216) | (0.3420) | |

| L.board | 0.2178 *** | 0.2941 *** | 0.2449 *** | 0.1327 * |

| (2.8166) | (3.3636) | (3.2595) | (1.7382) | |

| _cons | −11.0873 *** | −11.7513 *** | −12.3437 *** | −9.4680 *** |

| (−31.2076) | (−29.4521) | (−35.6377) | (−26.9073) | |

| Industry | Yes | Yes | Yes | Yes |

| Year | Yes | Yes | Yes | Yes |

| r2_a | 0.3732 | 0.3559 | 0.3336 | 0.3813 |

| N | 11896 | 11896 | 11896 | 11896 |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2022 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Deng, M.; Fang, X.; Tian, Z.; Luo, W. The Impact of Environmental Uncertainty on Corporate Innovation: Evidence from Chinese Listed Companies. Sustainability 2022, 14, 4902. https://doi.org/10.3390/su14094902

Deng M, Fang X, Tian Z, Luo W. The Impact of Environmental Uncertainty on Corporate Innovation: Evidence from Chinese Listed Companies. Sustainability. 2022; 14(9):4902. https://doi.org/10.3390/su14094902

Chicago/Turabian StyleDeng, Mingjun, Xusheng Fang, Ziyan Tian, and Wenbing Luo. 2022. "The Impact of Environmental Uncertainty on Corporate Innovation: Evidence from Chinese Listed Companies" Sustainability 14, no. 9: 4902. https://doi.org/10.3390/su14094902

APA StyleDeng, M., Fang, X., Tian, Z., & Luo, W. (2022). The Impact of Environmental Uncertainty on Corporate Innovation: Evidence from Chinese Listed Companies. Sustainability, 14(9), 4902. https://doi.org/10.3390/su14094902