1. Introduction

Lean management can positively affect the performance of an organization in terms of quality, delivery, and other economic improvements. However, it is necessary to create the organizational culture required for the effective implementation and continuation of lean management. The Cultural Web, developed by Gerry Johnson and Kevan Scholes in 1992, helps to provide a look at an organization’s culture and its changes [

1]. The biggest challenge related to implementing and maintaining lean management is identifying an organizational culture infrastructure that will allow this system to function well in other corporate areas. Continuous improvement is the primary goal of kaizen, the Japanese concept of management, which is an integral part of lean management. It is expected that all staff members will stop working when any non-compliance is encountered and, together with their supervisor, suggest an improvement to correct the non-compliance. Kaizen can be used in everyday life, not only during working hours, and the improvement should be gradual and constant, as we all strive for excellence [

1]. This life-style philosophy applied at an organization level helps the business to strive for optimal performance, using the full potential of our resources, i.e., employees. The primary goal of kaizen is to create a permanent habit of improving the organization [

2]. By building foundations, kaizen aims to develop a learning enterprise that engages both management and employees, thereby achieving common goals and establishing value. If such an environment is created, improvement is a way of life, employees demonstrate pride in their work, exhibit continuous growth of their skill sets and are empowered to solve problems at every level [

3].

Evolution is a natural method for improvement. Every single concept can be improved and expanded to the current needs.

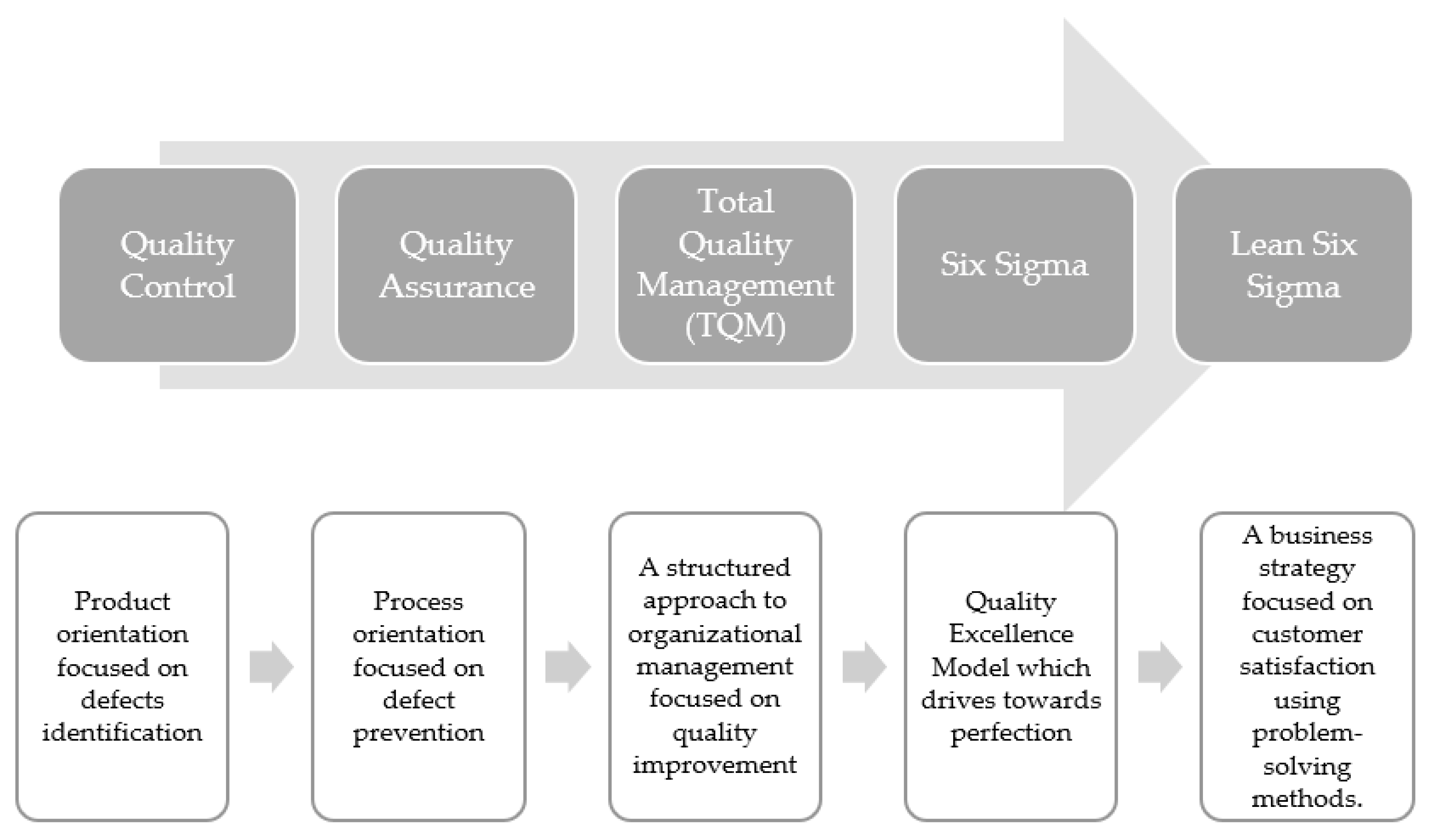

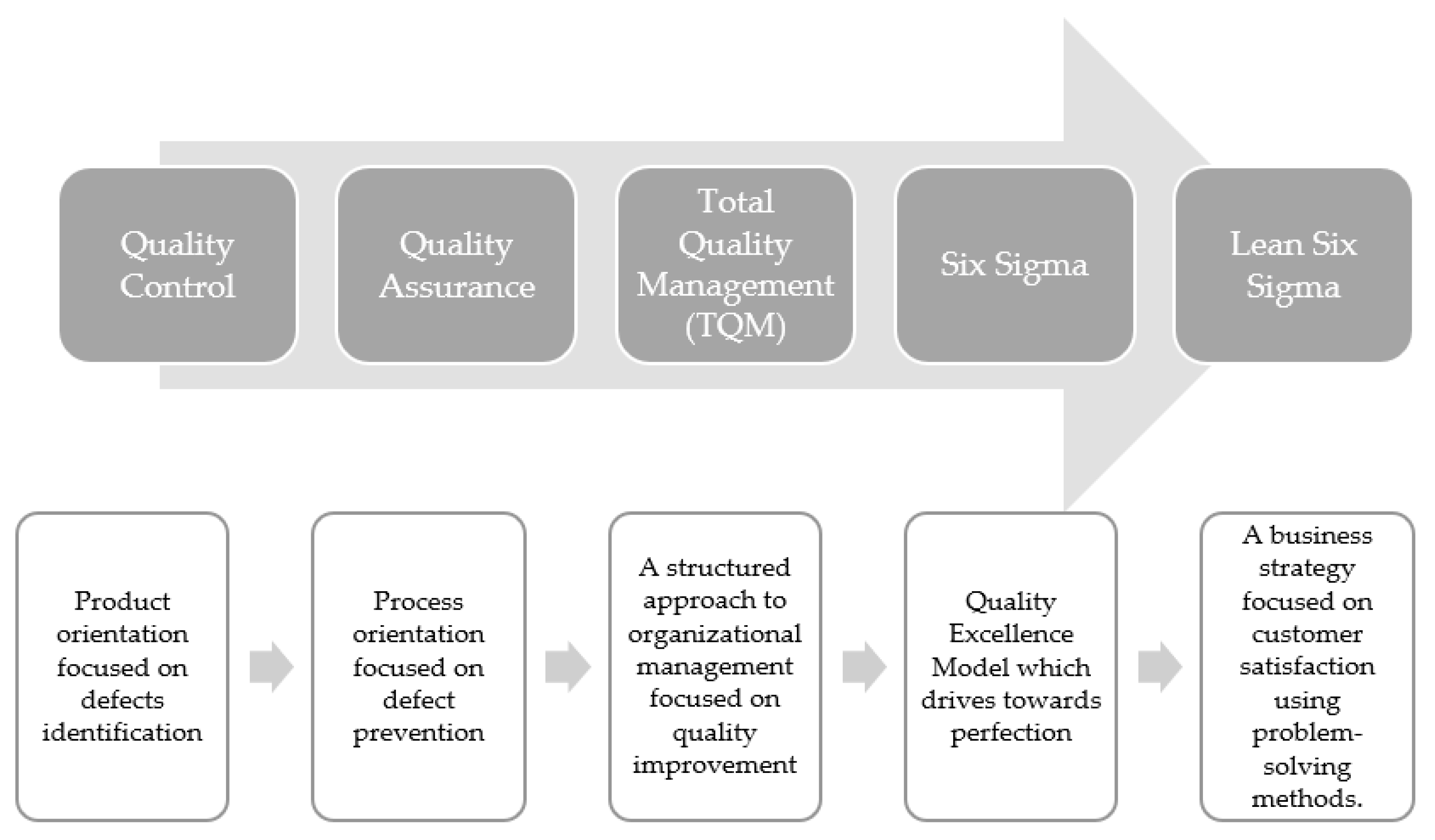

Figure 1 shows how different concepts evolved to create Lean Six Sigma, the most mature concept of lean thinking nowadays.

The quality control concept can be treated as the basis for further definitions, evolving into quality assurance. Perfection was the main driver to define the TQM concept, which is strongly focused on continuous improvement. The question is how TQM evolved into the Six Sigma methodology. Setting a new performance standard using tools that were part of the total quality management concepts is the leading indicator of the Six Sigma methodology [

4]. The current commonly used term is Lean Six Sigma (LSS). This combined approach of lean management and Six Sigma is the most mature methodology driving process excellence for many experts. Lean management is focused on waste reduction while Six Sigma continuously improves quality. Less emphasis on the statistical analysis requirements included in the Six Sigma methodology and more focus on lean approaches is the easiest way to define what is, in reality, the LSS methodology. Consequently, the LSS methodology focuses on waste reduction, with less emphasis on reducing variation [

4].

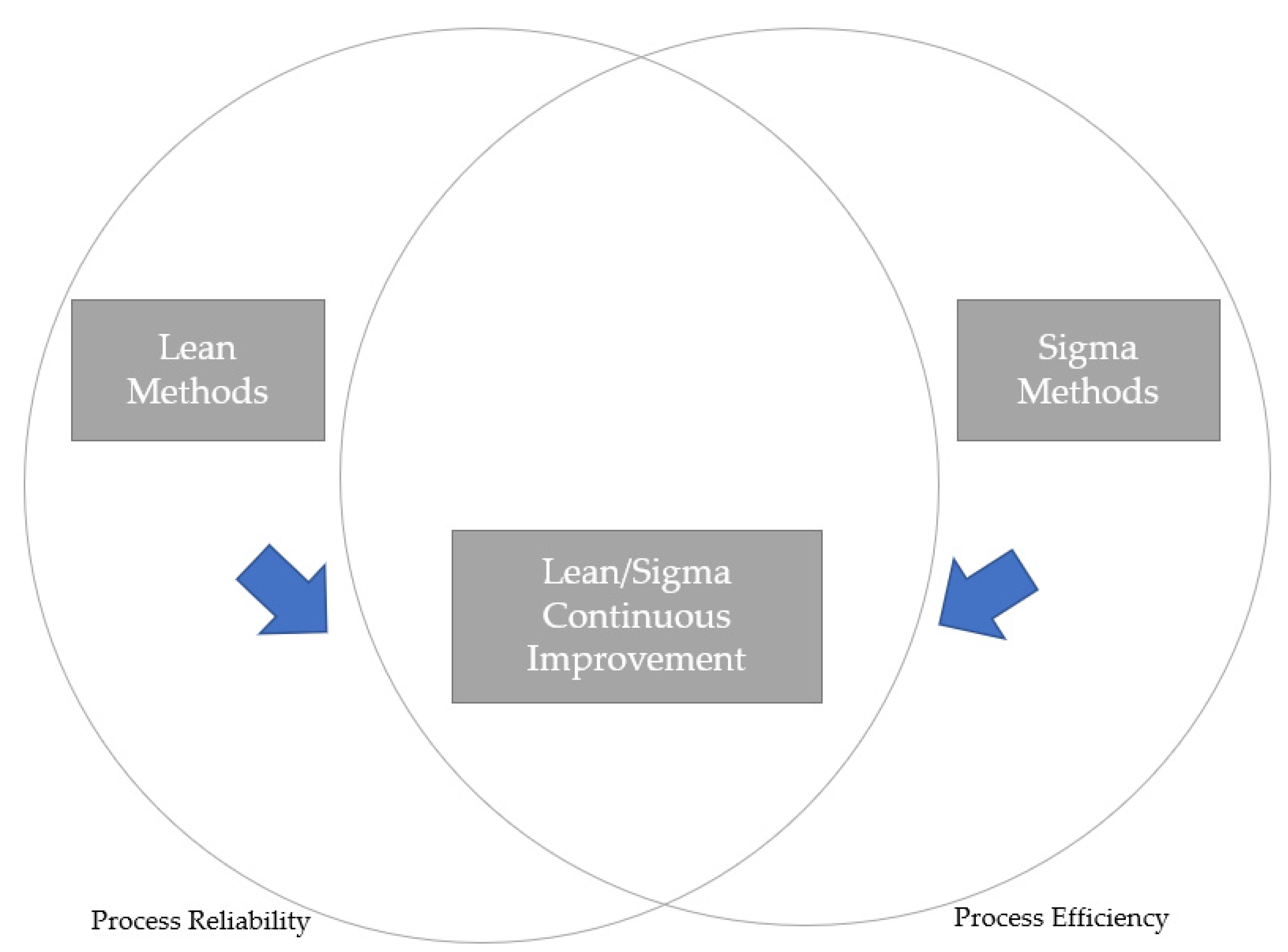

Continuous improvement drives both concepts, as shown in

Figure 2. In the past, companies started their journey with lean management or Six Sigma, depending on their goals and strategy. Because the ultimate ending point for both concepts is continuous improvement, LSS was an expected step for the evolution and ultimate concept to build an efficient organization [

5].

Lean Six Sigma can be described as “doing quality quickly,” which may initially seem counter-intuitive [

6] because intuition suggests that the faster a process goes, the more likely it is for mistakes to occur. Lean Six Sigma works not by speeding up the workers or machines but by reducing the unnecessary waiting time between value-added steps [

7].

In principle, all lean management concepts commonly used in an industry also apply to service organizations. The challenge is to be creative enough, to use them most effectively and to adapt industry value streams to customer expectations [

8]. It should be noted that Lean Six Sigma concept can be extremely powerful in improving the quality and speed of all types of “transactional” processes, including sales (quotations/pricing/order processing), marketing, and financial, administrative and human resources [

5], i.e., in the real scope of standard SSC.

Utilizing a third-party to perform various tasks and/or services, is a business practice that has been in existence for centuries, even dating back to Rome for tax collection [

9]. Officially, the concept of outsourcing was first proposed by Adam Smith in 1776 in

The Wealth of Nations [

10]. Labor division and specialization critically influence productivity optimization due to increased cooperation between groups of employees and the promotion of individual efficiency [

11].

Over the last 20 years, outsourcing for businesses has grown from the traditional outsourcing of facilities management to outsourcing more administrative support functions, such as information technology, finance, accounting, and human resources. In these cases, a business will choose to transfer functions to an outside entity rather than performing internally, most often for efficiency and financial benefits. [

12]. As Henry Ford suggested, “if there is a thing that we cannot do more efficiently, cheaper or better than a competition, there is no point in doing it further—we should hire the one who does it better than we do” [

13].

SSCs are in some ways similar to outsourcing in that they are separate entities, but the existing units are not liquidated. Only certain activities and processes separate from these units are transferred and consolidated in the centers. The SSC differs from outsourcing primarily in that the tasks are not outsourced, but are carried out by a specially established unit that remains within the structures and under the parent company’s control. An SSC operates as a business with full responsibility for managing their costs, quality, and timeliness of services and has organizational independence, utilizing contractual arrangements (known as service-level agreement—SLA) with their internal customers to define the type, scope, and price of the provided services. Moreover, an SSC provides well-defined process- or knowledge-based services for more than one unit of a company (e.g., division, business unit), with their own dedicated resources [

14].

SSCs are a viable alternative to outsourcing, reengineering, organizational restructuring, and other related “solutions” for costing and building service performance. Innovative structures, strategies, and solutions to complex business problems result from rapid technological progress and the pursuit of global performance standards [

14]. Increasingly complex and costly support services within the organization are prime candidates for reducing costs and building efficiency. The modern market and the development of the outsourcing industry have made lean management popular, not only in production but also in the area of SSCs created to outsource functions such as IT, accounting, and HR, as presented in

Table 1.

As continuous improvement is an essential element of any successful business strategy, lean management is an excellent guide to building an effective and solid organization that is constantly evolving, identifying real problems, and solving them. Regardless of the improvement scale, the goal remains the same: better use of the organization’s resources to create optimal value for customers and other key stakeholders.

Lean management is focused on bringing value to customers by reducing inefficiencies. Lean Six Sigma is a method that relies on a collaborative team effort to improve performance by systematically removing waste and reducing variation [

6]. Managing risk contributes to the improvement of management systems leading to improved performance, encouragement of innovation, and achievement of objectives [

17]. Every rework and control may be treated as potential waste. Considering that, lean management should strongly impact the risk management process, where controls are implemented as risk responses. If this dependency can be verified, additional question is about reporting perspective.

In previous studies, the scholars unanimously state the critical necessity (mandatory character) for integrating risk analysis during lean management process redesign [

18,

19,

20,

21,

22,

23,

24,

25,

26,

27,

28,

29,

30,

31,

32], but so far, the relationship between lean management and risk management has not been analyzed in greater detail. At this research stage, this paper aims to study how processes are selected for improvements in SSCs, and if the risk management aspect is considered during process improvements. With the identification of this research need, the following hypotheses are offered and tested:

Hypothesis 1 (H1): The risk management aspect is not considered during process selection for improvements.

Hypothesis 2 (H2): There is no sufficient cooperation between risk management and lean management teams enabling the full use of risk reduction opportunities.

While the literature provides models that can be used, a lack of specific guidelines, especially considering the risk management aspect, has been recognized. It is believed that this current study contributes valuable empirical insights. When discussing lean management in SSCs, insufficient attention is paid to the right choice of processes. In the last decade, the focus was on the expected benefits, ignoring the adaptation difficulties of lean management to shared services centers processes. Additionally, the lack of sufficient empirical research reveals the marginalization of potential possibilities for building synergies between lean management and risk management.

On top of that, from the reporting perspective, the role of Environmental, Social, and Governance (ESG) plays a significant role. The demand for transparency on sustainable and socially responsible practices is rising. The terms “ESG” and “sustainability” are used interchangeably, especially when it comes to benchmarking and disclosing data. Sustainability is an umbrella term for corporate responsibility and many green concepts. ESG has become the preferred term for investors and the capital markets.

In Poland, as of 2018, approximately 300 Polish companies are required to submit non-financial statements together with a report on their activities. The provisions on non-financial reporting apply only to large companies, which are public interest entities (PIE), employing more than 500 employees and meeting one of the two financial conditions: PLN 85 million in total assets on the balance sheet at the end of the financial year or PLN 170 million in net revenues from the sale of goods and products for the financial year [

33]. On 24 February 2022, the EU Competitiveness Council adopted the so-called general approach to the draft directive on corporate sustainability reporting (CSR). The new directive replaces the existing EU regulations on disclosing non-financial information and expands the catalog of entities required to report. The member states propose a significant deadline extension for transposing the directive. In the first term, the new provisions would apply only to those entities that already report non-financial information (i.e., large public-interest entities with more than 500 employees). In the second term—all other large entities, i.e., meeting any two of the three criteria (balance sheet total over EUR 20 million, net income over EUR 40 million, number of employees over 250), regardless of whether they are public interest entities or not. In the third term—all small and medium-sized listed companies. The directive’s scope will also cover large capital groups [

34].

It is in every company’s interest to address environmental, social, and governance risks and opportunities adequately because the costs to repair damages can be higher than preventative measures and proactive ESG risk management. Evidence shows that companies that fully integrate ESG and are accountable to stakeholders and transparent are better positioned for long-term success. The financial sector is mainstreaming ESG, and its integration in finance is expected to accelerate further [

35].

Integrating ESG in risk management is an essential step on a sustainability journey. Being aware of ESG risks and handling these adequately is fundamental to running a business and pursuing operational excellence. Mapping and prioritizing ESG risks, for example, by filling out a materiality matrix and managing this over time is important.

While the demand and practice of ESG reporting have increased, there still lies a considerable knowledge gap between ESG information and supply, which results from several factors like varying ESG reporting standards and frameworks, nonmandatory reporting regimes, and steep costs to collect and report data.

To meet the research objectives, this article is organized as follows.

Section 2 presents the research methodology on procedures and methods utilized.

Section 3 presents results:

Based on a review of Polish and international literature, the principles of selecting lean management processes were analyzed.

Expert interviews conducted in the first half of April 2021 constituted the basis for preliminary considerations of the drivers and barriers to selecting lean management processes.

Surveys were sent to the SSC audience working in lean management area in October 2021 to examine lean management implementation.

Case study on measurements of testing the effectiveness of applying lean management methodology helped formulate conclusions and future directions for the research.

Section 4 discusses empirical findings contributed by the analysis, and

Section 5 contains conclusions and future direction for this research.

2. Research Methods

This study is exploratory research, conducted on an issue that has not been previously investigated in Poland within shared services centers. It is descriptive and analytic from the viewpoint of the exploratory objective, including two steps. The first step entails targeted reviewing the existing literature, followed by empirical research covering expert interviews, surveys and case study. Both steps are explained further below.

To evaluate current trends, the targeted literature review [

36] was conducted using Web of Science database to identify the most popular approaches for the selection of processes subject to lean management. The search strategy applied included specific keywords: “process selection for improvements” and keywords associated with organization (e.g., shared services, BPO—Business Process Outsourcing, SSC). The search was limited to studies published within the last 12 years (2010–2022). No language restriction was applied to the search but only studies with an abstract written in English and full text in English and Polish were eligible for inclusion. All retrieved articles were reviewed by a researcher, and those considered irrelevant were removed. The remaining articles were further assessed to identify those studies that met the eligibility criteria. A quality check was conducted on a sample of the selected articles/abstracts by a second researcher, and a full-text review was conducted to determine relevance to the eligibility criteria. The literature search identified 387 records through the selected database. All records were screened and 370 were excluded based on the eligibility criteria. A full-text analysis was conducted on the remaining 17 articles and resulted in the exclusion of 8 articles that did not meet the eligibility criteria. For completeness check purposes additional verification of available literature was conducted using Google where additional 6 articles reviewed. A total of 15 references were included in the qualitative analysis.

To learn the context of the drivers and barriers in the selection of processes subject to lean management, individual interviews were conducted with experts [

37] certified at the minimum level of Green Belt in the area of lean management. There are four types of certification: White, Yellow, Green, and Black Belt. An expert with a Green Belt has extensive business experience and comprehensive knowledge of processes. In contrast, an expert with a Black Belt is fluent in the methodology of the DMAIC improvement cycle (define, measure, analysis, improve, control), mastering a wide range of tools and a unique way of working. Experts were selected based on their professional experience in SSC distributed across international capital groups, providing services to at least 20 internal entities and employing at least 100 employees. It was also crucial to have professional qualifications at the minimum Green Belt level. The interviews were conducted in a video conversation, mainly due to the COVID-19 pandemic situation. Each interview lasted approximately 60 min and was partially structured. The three interviewees did not know the questions beforehand. Through guiding or refining the questions, essential information was obtained to understand the context. As the interviewees cited examples from their practice and some of the information was insightful, it made it possible to understand the principles not previously described for selecting processes subject to lean management.

Three research questions were formulated:

What criteria must the process meet to apply the lean management concept?

Which of the processes are most often not considered regarding applying the lean management concept due to the high probability of failure?

Are the process risk analysis and the risk response analyzed before applying lean management tools?

Qualitative analysis of the interviews was performed using the QDA Miner Lite software. As a result of the coding process, four main categories were distinguished and specific codes were assigned. The software was then used to analyze the frequency of the codes in the statement, and after summarizing the data for the codes, the results for the categories were obtained. Analysis of the frequency of codes allowed us to determine which categories were most frequently discussed by experts. Further analyses were mainly devoted to “process selection” since they were most closely related to the research questions. The remaining categories were considered less important in the context of the research questions. The “risk analysis” category was also distinguished because, in the authors’ opinion, it brings important research questions that will be the subject of further analysis.

The next step was designing the survey, a quantitative method of research [

38], which was created based on interviews with experts. It was developed taking into account two sets: companies that implemented the Lean methodology and companies that did not. In relation to companies that have implemented the lean methodology, the intention was to understand:

The measurements of the effects of applying lean management.

The priorities are taken into account during process selection.

The relationship between lean management and process automation.

The approach took in risk management during the work on process modeling after applying the lean management methodology.

The effects of applying lean management in the SSC as an element of a business strategy.

In the second set of companies, a survey was closed after confirming that the company does not implement lean management. The online questionnaire performed in the MS Forms application ran online between 17 October 2021 and 31 October 2021. This format was chosen because online questionnaires present numerous advantages in terms of cost, time, easiness of administration, data organization, and analysis [

38]. The data file with the answers obtained was downloaded in MS Excel format. The first section of the questionnaire addressed respondents whose companies had already implemented Lean tools. The second section of the questionnaire consisted of generic questions aiming at characterizing the respondents and the companies.

The questions asked in the questionnaire were translated into qualitative variables (nominal and ordinal) and quantitative variables containing Likert-type scale questions from 1 to 5, and the lean management implementation was measured. The study of companies was grouped in terms of the role performed by the respondent, size of the company (number of internal entities and number of employees), years of lean implementation, phase of lean progress, and the scope of services. Based on these groups, statistical tests were carried out to verify any standardization or differentiation.

Quantitative data analysis was performed using descriptive statistics to summarize the information collected, followed by inferential statistical techniques based on the graphical presentation of data [

38]. The statistical analysis was completed using Microsoft Excel and Statistica application.

The population of the present study consisted of companies operating in Poland, with SSCs that were created as part of an international capital groups, providing services to at least 20 internal entities and employing at least 100 employees. Firstly, based significantly on annual research executed by ABSL on Business Services Sector in Poland [

39], 128 companies were defined as a population meeting research criteria. Additional search on the Internet (LinkedIn social medium) allowed to collect a list of firms’ representatives for the study. They were selected based on position related to one of the keywords “lean management,” “process excellence,” or “continuous improvement.” The survey was fully anonymous, and made available to selected people in a private message on LinkedIn. Considering population size: 128 companies in scope for the research, confidence level: 90% and maximum error: 5%, sample size was defined as 87. In total, 90 questionnaires were sent out successfully, and 23 with answers were collected (a percentage of 25%). Even though the return of the questionnaires was low, the research results obtained with different methods are complementary, and the results of the questionnaire were additionally confirmed by the case study method. However, the conclusions from this research cannot become the basis for generalization. The main limitation of the research itself was the size and selection of the research sample based on willingness to participate in the research. This is also the reason why this survey will be repeated in the future. In addition, the authors plan to create a new survey focused on the risk management perspective to have comparable results from two sides: lean management and risk management.

The last stage in the research cycle was preparing a case study [

38,

40] for a selected SSC. Case study is an in-depth research of processes in their real environment. The selection of cases is subordinated to the presentation of the research subject. It is intended to contribute to a better understanding of the reality that is the subject of the study. A crucial matter in question was how to examine the measurement of testing effectiveness of lean management in practice. To answer this research question, a deliberate case selection was made. The selected SSC was established in 2011. Currently, their team consists of over 200 people. They provide business services in finance, accounting, purchasing, tax, internal control, law, and human resources and support companies based in Europe, India, Africa, and the Middle East. Lean Management in the capital group has been used for decades and in the SSC area for over five years. A field study was conducted to collect data, and while staying in the company’s seat, access to two project cards carried out in 2020 was obtained. On their basis, a pattern was selected, which was then subjected to further analysis.

3. Results

3.1. Targetet Literature Review

To further the research purpose, this study performed a targeted review using the methodological approach explained in

Section 2. Based on the review of the 15 articles sorted by publication year, it was found that the approach in area of selection process for lean improvements has evolved progressively over the years.

Assuming that lean management aims to eliminate errors, and thus waste, a problem-based approach can be suggested. This problem must be significant, visible, and understandable to employees; otherwise, the employees will not see the need to change. The problem cannot be too broad because a large problem that must be overcome in the first stages carries a high risk of failure, which may discourage employees from further actions in a scenario where the problem cannot be solved. In such a case, it is worth dividing such a problem into more minor elements and initiating improvement [

41]. From this perspective, selecting an area subject to lean management requires selecting an appropriate method, which may not be easy due to the multitude of options. According to other authors, the implementation should start with value stream mapping (VSM) [

8,

42], which may indicate the redundancy of some processes. Value stream management includes the process of measuring, understanding, and improving, as well as managing the flow and interaction of all related tasks to keep the costs, service, quality of products, and services of the company as competitive as possible. More importantly, value stream management sets the stage for implementing lean management transformation across the enterprise. The basic value stream management tool is of course VSM [

8]. The basis of this approach is to go to the

gemba (workplace) and define the current state as an “as is” process map. Then, the future state or process should be determined. The gap between the two maps indicates the actions that need to be taken to move from the present state to the future. After improvements are introduced and the process stabilizes, new maps of the present and future state are generated, and the cycle begins. However, the initially defined future state is never reached. Through successive cycles, one strives for the ideal vision of a lean process [

8]. Another comprehensive approach to process transformation using the lean management and VSM concepts may be the hierarchical transformation framework, which, at the first stage, involves taking a step back and viewing from a broad perspective (gain the big picture) to apply lean management [

43,

44,

45].

Methods of selection and adoption of improvement initiatives in today’s competitive environment and with a confusingly large number of improvement programs to chose from, are rarely structured, and the selection criteria are inconsistent. Much literature discusses the perspective for decision making and defines management ideas as fads or fashions. As a result, the adoption of management fashion is complex and strongly influenced by the power of fashion setters. Existence of the management fashion phenomenon was confirmed and its better understanding using the case of improvement initiatives was provided [

46].

There is no doubt that the choice of lean management tools and methods is extensive. In addition, not only should tools and methods be defined but also the processes for which they will be applied should be listed. There is no clarity about the order in which the lean tools are implemented. Many experts believe an organization should start with a methodology known as 5S (Sort, Straighten, Shine, Standardize, Sustain), which helps to create a more organized environment and serves as a solid foundation for further lean tools to be implemented [

47,

48]. 5S is certainly useful and encouraged for all lean endeavors and can progress naturally to the next step of an organization identifying value and where to prioritize their efforts.

In the area of SSC operations, a process-based view of the organization’s activities may be of crucial importance. The processes transferred to an SSC, although in the center itself they can be called an end-to-end (E2E) process, are often part of a much larger, engaging process that is also undergoing the transformation of owners from companies supported by the centers. Actions should be taken to improve processes if their assessment is unsatisfactory. The first method is to select the processes for improvement based on the extent to which they generate value for the customer. Only those processes that create high value should be continuously improved [

49].

Where E2E focuses on an entire process, organizations may also choose to analyze particular projects, resources and portfolio using project portfolio selection (PPS) [

50]. It is to be noted that this tactic becomes increasingly complicated as organizational size and the number of potential projects increases which has often led to complicated ways of managing portfolios.

The lean solution to PPS is an information technology (IT) derived value-based management approach. Failure rate is inherently higher for more complex implementations which contradicts the lean approach. With this solution, a business can assess the potential for process improvement within projects by utilizing IT to reduce complexities. First a catalog of non-value added (NVA) activities that can be used in management control and governance procedures for the systematic identification of process inefficiencies is provided. Next, by breaking down processes to the level of atomic activities, it can be shown that minimizing NVA activities provides a systematic means to mitigate process inefficiencies. A significant observation is that different NVA activities may impact process performance to varying degrees. Consequently, line items in the request for proposals should be weighted accordingly, contrary to the common practice of treating all line items equally [

51,

52].

A slightly different approach may be to identify and isolate those essential processes, not only in the opinion of customers and shareholders but also in the critical factors of the company’s success. Pareto analysis accomplishes just that. The basic principle of this technique is that all processes are contending for resources (input) each with an outcome of varying benefits (output). Processes can be selected for lean management based on the analysis performed to derive value closest to the maximum benefit [

49]. There is a belief that 20% of processes involve 80% of resources and, at the same time, that about 20% of operations performed in the process generate about 80% of the results of the process [

49]. Think of what an organization could do if they had the tools to analyze and reprioritize their resources for maximum results.

With the continuing proliferation of decision methods and their variants, it is crucial to have an understanding of their comparative value. Decision-making is the act of choosing between two or more options. However, there may not always be a “correct’” decision among the available choices. Multi-criteria decision-making (or MCDM) is the most well-known model of decision-making. Its basic working principle is the same [

53]: selection of criteria, selection of alternatives, selection of aggregation methods, and selection of alternatives based on weights or outranking. MCDM methods are widely used in many fields and disciplines and were inspiration to create many various models [

54,

55,

56,

57,

58,

59,

60,

61,

62], which are built systematically by incorporating all related decision criteria with suitable tools required to select improvement alternatives. Generally the developed models used to prioritize the problem scope and select the solutions from various options, because it can be challenging for organizations to select the most appropriate improvement projects from a pool of many potential project ideas.

The lack of a strategic approach to the selection of processes subject to lean management may result in a lack of effects and a departure from this concept. It is worth highlighting that in the area of services for which lean management method was applied, results may not be as spectacular as in a production environment. Colloquially called myopia, it is a persistent focus on the here and now at the cost of a more or less uncertain future. Since people create the organization, we find the short-sightedness of people in the organization [

63]. In addition, the improper implementation of the lean concept can lead to adverse effects, such as simple rationalization, a loss of quality, employee stress, decreased motivation, superficial staff reduction, and an increase in the demand for professional forces, while neglecting the problems of employees with lower qualifications [

64]. There is no doubt, however, that continuous improvement should serve the implementation of the company’s strategy and not only short-term benefits.

Based on above analysis it is possible to conclude that there is significant amount of offered tools and methods which could be utilized for process improvement selection. However, it should be emphasized that the application of these models in the case of processes transferred to shared service centers has not been studied in greater detail, and none of these models has been tested in such conditions. The conclusions from this research cannot become the basis for generalization. The main limitation of the research itself was the size and selection of the research sample based on willingness to participate in the research.

3.2. Expert Interviews

Based on the conducted expert interviews, it was agreed that to choose a process for applying lean management principles, it is necessary to have knowledge of the principle and appropriate people resources who perform a given process. Observation, active collection of information, and visualization of this process are inseparable elements that must occur before the actual work begins. From a practical point of view, it is also essential that the process remains unchanged over a specific period of time and awareness of the boundaries of the process exist in the company. Processes can be viewed broadly or narrowly, but the optimal approach, suggested by the experts, is the end-to-end analysis of processes, although this is not always possible, especially in SSCs.

During interviews, it was confirmed that the strategic goal to which the organization aims in selecting processes should be guided and that process optimization should move within this strategic goal. Unfortunately, organizations are usually driven by the need of the moment and the occurrence of dissatisfaction on the part of the beneficiary. Additionally, the results of internal control are often a factor in the fact that a given process is analyzed at all.

Thinking only about the potential savings may miss the chance of effective implementation of lean management. It seems that to be able to apply lean management tools to all processes and see these benefits, it is necessary to develop an organizational culture and commit to continuous improvement of processes with the correct presentation of results. It is essential to share ideas so that everyone can use them to see if the same or a similar improvement can be introduced in their work, which will result in savings.

Based on the conducted interviews, significant problems with the inventory of processes were also indicated. The organization’s unawareness of the number of processes, their owners, and measures of a given process (key performance indicator—KPI) destroys the strategic approach to selecting processes subject to the lean management concept.

Processes cannot be changed, if it’s in no one’s interest. People involved in the process often take bottom-up initiatives, but if no one in the organization cares about the process itself, it is likely not to be optimized. Support from middle management to the highest level is critical, especially when implementing optimization solutions. If there is no such support, then continuously operational work, ongoing performance of tasks, and an attempt to keep up with deadlines will be more important than improvements. In addition, employees often become content with completing work in the manner it has historically been done (especially seasoned employees). It is often not until leaders empower their employees that process improvement and change is sought.

Processes that do not happen in a particular system are also a challenge.

There is also a lean trap in the lack of a strategic approach, especially in organizations that introduce automation solutions. It manifests itself in the fact that such automation must concern stable and repeatable processes, and in practice, waste or ineffectiveness of the process is automated.

Experts were also asked about the use of risk analysis in process optimization projects. In terms of supporting tools, FMEA (failure modes and effects analysis) was mainly used, which allows one to track and build weights of how a change may prevent one from detecting a potential error in a structured way. As a result of the research, it was confirmed that although the lean concept included such risk analysis in the work on process optimization, praxis excluded this approach. Some focus on the process and involving people from a given process narrowed the possibility of including risk analysis in process optimization. Even if risks were identified within the project, there was no support from the risk manager to make a proper assessment, and often, such departments did not exist at all within the SSC.

Based on the results of the performed expert interview, it is possible to conclude on the drivers and barriers in the selection of processes for improvements summarized in the

Table 2.

An important finding coming from the expert interview phase is connected with risk management. It can be defined as a lack of cooperation between lean management, and risk management teams manifested in no further actions in identified and remodeled risks.

3.3. Surveys

Bearing in mind the multidimensionality of the concept of lean management, in the shared survey, for systematization purposes, authors presented general understanding of this concept for the purposes of the survey. The reason for the need of systematization is coming from the discussion with experts working in SSCs which pointed out, based on their experiences, that research should not be limited only for lean management and cover much more advanced and broader concept of Lean Six Sigma. As a result, following clarification was added to the survey, directly in the introduction: “A company operating according to the principles of lean management is a company focused on creating maximum value for the client using minimal resources, which is possible thanks to perfectly organized processes, which are in turn the result of using the talents of people at every level of the organization and minimizing waste. Lean Six Sigma (LSS) derives directly from the combination of Lean and Six Sigma methodologies, giving greater benefits than when used separately. Lean Six Sigma is an evidence-based and data-driven improvement philosophy that prevents product defects from arising by detecting them and continuously improving processes. Ensures customer satisfaction and focuses on the end result (end product) reducing process variability, waste and cycle time, while promoting the use of standardization and workflow, thus creating a competitive advantage.” In addition, authors decided to add to the survey’s introduction, clarification around Shared Services Center (SSC) versus Global Business Services (GBS): “In the Shared Services Center (SSC) model an independent entity is separated from the organization and responsible for providing services to other units. The Global Business Services (GBS) model is based on creating a global, integrated and centrally managed organization that provides comprehensive end-to-end services. For the purposes of the survey, GBS is defined as the last, most advanced step on the SSC organization maturity scale.”

Specifically for the survey, a key issue in this study was to identify drivers to process selection for improvements in the companies where lean management or Lean Six Sigma is implemented.

To do that, first few questions were focused on general information about the lean management approach. The most important information needed for further analysis was the confirmation around lean implementation. This specific section of the questionnaire was addressed only to companies that practice the lean philosophy (96%, where lean management is 52% and Lean Six Sigma is 44%). Almost all respondents confirmed that they use this methodology for between 1 and 3 years (68%) or more than 5 years (23%). The levels of lean management implementation were varied. A significant proportion of the responses confirmed that almost all organizations analyzed at least identified processes in the scope of the SSC (19%), created value stream maps for them (18%), created a standard process (16%), and implemented a culture of continuous improvement (16%). This specific set of questions helped to understand how mature and advanced lean management is in the shared services center structures.

The next set of questions was focused on the main purpose of the research and looked at hypothesis confirmation or rejection. Based on the survey responses, main drivers to process selection for improvements were, among others, the biggest expected benefits from improving the efficiency of the process (as a relation of the obtained effects to the expenditure incurred)—27%, and the effectiveness of the process (as a relation between the adequacy of the obtained result of the completed activity with the goal specified for this activity)—21%. Respondents reported also that potential reduction of the number of processes without value added (14%) is driving lean improvements. Respondents did not mention high-risk-related processes, which is driving the initial conclusion that this factor is not taken into account during selection. In addition, through the structure of the survey, authors were investigating who is decision-maker on the process selection for further improvements to better understand the process itself and the ownership behind. Based on the survey, it was concluded that the processes were designated for improvement with the lean management method based on the decisions of the management (31%), the assessment performed by dedicated experts (25%), and the profitability assessment of the processes (17%). Respondents were asked if tools and models that the organization uses were diversified and provided the following responses: scoring model, customer satisfaction surveys, KPIs, benchmarking, end-to-end process analysis, and value stream mapping (VSM).

Measuring effectiveness of implementation was also in the area of research because the Authors wanted explicitly to analyze how crucial specific risk measurements factors are at this stage. The most important measures for assessing the effectiveness of lean management reported by the respondents involved in lean management activities were:

Time reduction (22%).

Creation of a standard process (19%).

Cost reduction (15%).

Quality improvement (14%).

Number of potential automation opportunities (12%)

Only 5% of respondents reported a reduction of operational risk and a decrease in control activities: 4%. It is a significant finding coming from this research, especially for risk management and ESG (Environmental, social, and governance) reporting. Despite the enormous pressure on international organizations, none of the respondents indicated the possibility of reporting lean management effects in ESG reporting.

The last layer of the survey was focused on the organizational structure of the lean team to gain an understanding of potential dependencies and relations with other structures in the organization. Based on respondents’ responses, the team responsible for lean management is organized mainly as a separate team (50%), or there is an independent expert in the organization (27%). Specifically asking about process risks and mitigating controls discussion when streamlining processes using the Lean Management method, 68% of respondents confirmed that it is taking place, and it is discussed with a representative of the Internal Controls Team (47%) or Risk Management Team (13%). In almost 40% of responses, no Risk Management/Internal Controls representative is taking part in the discussion, the knowledge of people in the team and their general understanding of risk is used. This initial result is giving new light on the organization of the process itself and how proper cooperation should look like to build proper synergy between lean management and risk management team. In terms of risk assessment during the improvement process using the lean management method, 70% of respondents confirmed that risks and mitigating controls were discussed and 53% of respondents indicated that a representative of the internal control or risk management team participated in the process improvement. After the process transformation, risk analysis was not executed in 55% of responses and the risk matrix was updated less often than once a month for more than 50% of responses. All these conclusions raised additional questions and require more in-depth analysis via additional surveys and case studies from a risk-management perspective.

The second part of the questionnaire characterizes the sample distributed by the following components presented in the

Table 3.

Based on the results of the conducted surveys, it is possible to conclude that no risk management factors were considered as drivers to process selection for improvements. In addition, significant differentiation was identified in the area of models used for the selection of processes. Potentially the barrier to building synergy can be the placement of the lean management and risk management teams in the organizational structure because, based on this empirical research, in almost 40% of responses, no risk management/internal controls representative is taking part in the discussion. The knowledge of people in the team and their general understanding of risk is used. It is important to highlight that this research shows only one perspective because respondents represent a lean management team. Further discussion should take place with representatives of the risk management stream.

3.4. Case Study

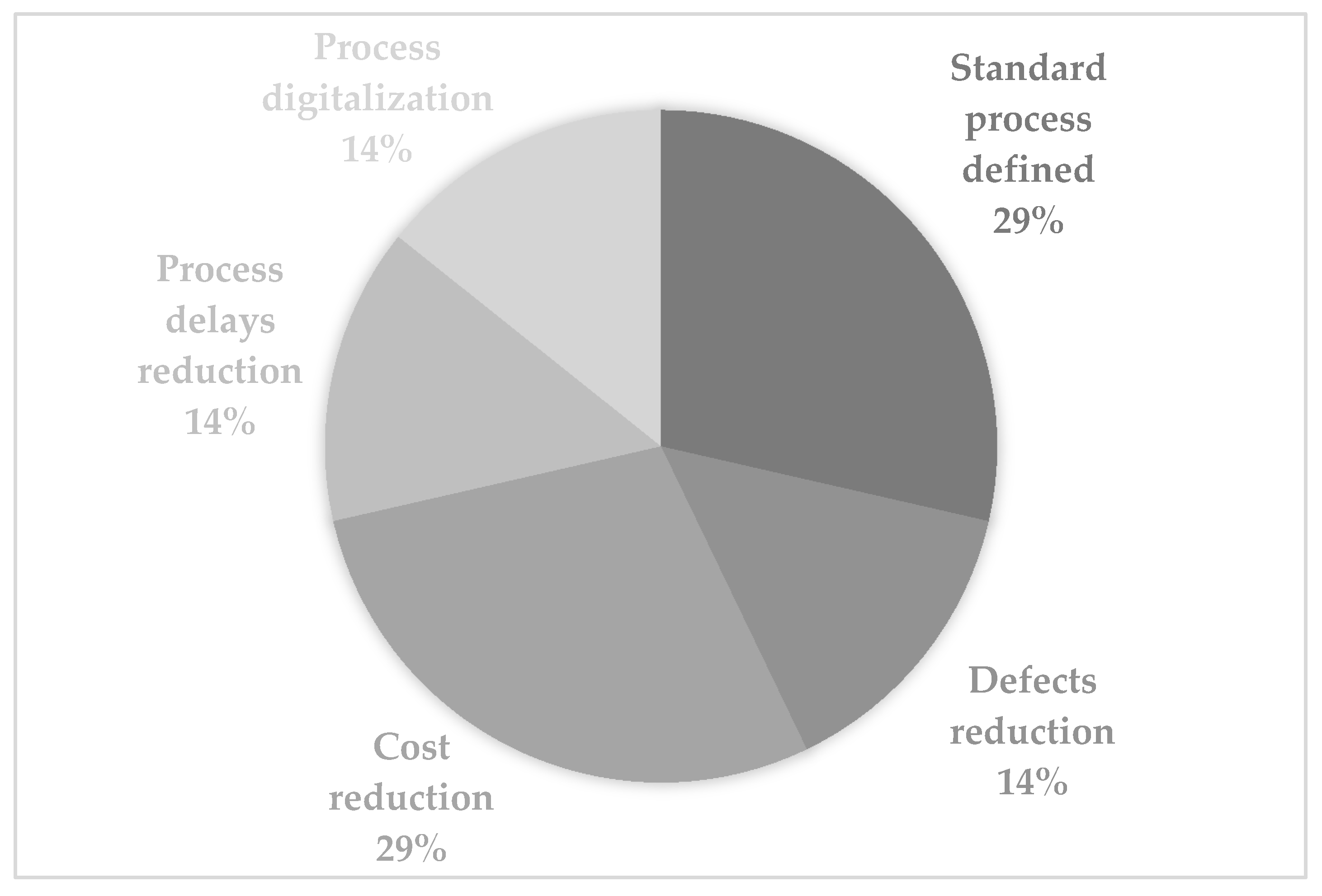

The analyzed entity supported over 50 internal units in the field of processing receivables, liabilities, payments, operations on the general ledger, and other corporate functions. The scale of the overall processes that were significantly transferred to this entity was still small, as processes such as customer service or purchasing remained outside the SSC. Taking this into account, the scope of the lean management application was limited, mainly due to the lack of responsibility for the entire process. From an efficiency perspective, it is clear that the definition of the standard process (29%) and cost reduction (29%) were the two main measurements used to assess process transformation (

Figure 3), which confirmed the conclusions found based on the surveys. Defects reduction (14%), process delays reduction (14%), and process digitalization (14%) were also mentioned as measurements showing whether lean management was implemented successfully.

It can be concluded that the results of the case study identifies and confirms the same benefits measured by SSC in the area of process improvements as results of the survey.

4. Discussion

The received results from targeted literature review and empirical research confirmed hypotheses H1 and H2 and proved that the risk management aspect is not considered during process selection for improvements, and there is no sufficient cooperation between risk management and lean management teams enabling the full use of risk reduction opportunities. In this initial stage of research, in this paper, to achieve the synergy between lean management and risk management teams, the authors offer a systemic implementation of both concepts highlighting the need for proper placement of both teams or their representatives in the organizational structure. The future is unknown, but alternative future outcomes can be identified, assuming that the chances of possible alternatives are known [

65,

66]. The risk should be assessed and proper actions should be taken to respond to the risk. One possible response can be the implementation of control activities, which connect risk management to lean management, as control activities are often treated as waste due to the assumption that a perfect process should eliminate errors and, simultaneously, control activities.

It should be noted that outsourcing for cost savings is something that is still heavily exercised today. The COVID-19 pandemic brought new importance to outsourcing because organizations of all sizes and industries have started using this process of engaging a third party, either locally or internationally, to handle certain business activities for them at a lower cost. The use of remote teams, virtual assistants, and the ability to work from anywhere in the world has made business more accessible, faster, and cheaper. Outsourcing allows a business to streamline practices by focusing on an improved outcome with less resources; a main goal of lean management.

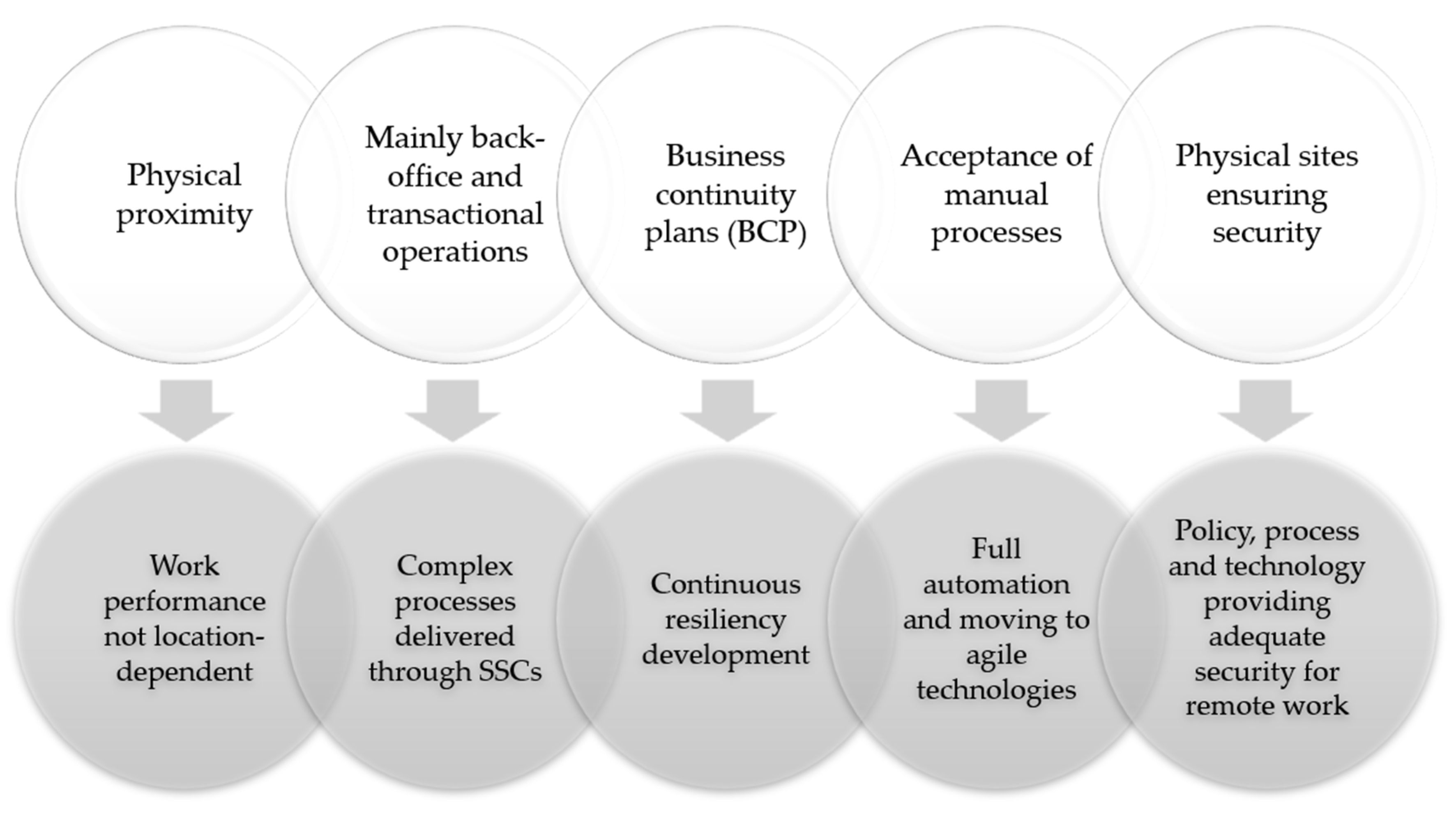

For shared services organizations, best practices have been challenged during the pandemic and changes focusing on better performance were expected by clients. The new standard for shared services includes operational practices that were previously thought impossible since they required physical attendance in the office. To understand the challenges and responses of organizations to the COVID-19 pandemic, in 2020, Deloitte conducted more than 40 in-depth interviews with GBS, SSC, and business process outsourcing (BPO) organizations [

67].

Figure 4 presents an examination of traditional service delivery practices versus the new standard, which could be defined only because of the COVID-19 pandemic’s challenges to conventional logic.

Working from home (WFH), offering complex process delivery, and ensuring proper security are the biggest challenges affecting organizations worldwide.

In recent decades, large office spaces were created in the best locations of city centers to ensure good communication routes and increase the flexibility of working hours. Physical proximity was treated as a standard that should not be challenged. Teams can cooperate and build relationships, and supervisors can directly observe people’s performances. No one was interested in challenging this current state because organizations traditionally believed physical proximity was critical to achieving goals and effectively executing more complex tasks. Many companies with highly face-to-face-intensive processes, such as month-end close and financial planning and analysis, shifted and performed them virtually, demonstrating that face-to-face interactions may not always be required for effective process performance. Work that previously required proximity transitioned effectively to a virtual environment during the pandemic, breaking down conventional wisdom in this area. This has expanded opportunities in terms of the potential scope delivered through shared services and outsourcing delivery models. The same approach could be applied to lean management, with the main focus on repeatable and transactional processes, which are migrated to the SSCs. By default, more complex and less repeatable processes would not be considered during process redesigning using lean management tools. Considering the results of Deloitte’s research in 2020, a massive transformation of complex processes can be expected. Now, new obstacles need to be considered in how lean management is approached. COVID-19 has drastically altered the typical the working environment which may require us to alter our way of thinking how to approach lean management. Older approaches may not be as effective, etc. We need to be agile not only with internal business processes but also with our thinking and acceptance of external factors.

Data security and lack of direct oversight strongly increase doubt in the new standard. How is it possible to ensure that all important data is well secured? Is a VPN enough for a secure connection? How is it possible to ensure that employees are not sharing sensitive information? Shared services organizations had to quickly adapt to support the data and security needs coming from the new remote work requirements. For companies in financial services, insurance, and healthcare with significant PII (personal identifiable information) or PHI (protected health information), the risk and data security represent the greatest challenges. As reported by Deloitte, to succeed in these difficult conditions, these organizations implemented short-term technology solutions to address potential security concerns and secure sensitive data, which include the following [

67]:

- -

The ability to remotely lock down an employee’s computer;

- -

Camera recognition on devices to prevent picture taking by onlookers;

- -

Voice recognition for customers;

- -

Privacy screens.

Currently, the global development of economic relations is characterized by two key features: digitalization and multipolarity. Due to the emergence of a new growth pole in developing countries under the conditions of the digital economy, for the first time in the modern history of the world economy, it could be stated that its multipolarity stimulates the reduction of countries’ inequalities rather than an increase [

68], and thus contributes to the implementation of the Sustainable Development Goals (particularly SDG 10 [

69]). Sustainable management is now more critical than ever because it should be driven in a beneficial manner to present and future generations. Environmental, social, and governance (ESG) metrics are widely used to measure the firms’ social performance. The scope of non-financial information reported by enterprises includes issues related to sustainable development, business responsibility, natural environment, social affairs and remediation, ethics, human capital, and health. This additional qualitative information provides insight into the company’s internal and external policies, vision and values, risk management, and future prospects [

70]. The introduction of non-financial reporting obligations is nothing new. According to Directive 2013/34/EU, enterprises classified as public interest entities have been obliged to disclose information on environmental, social, and employment-related issues, including protecting human rights, combating fraud and corruption, and respecting the principle of diversity management. This directive was amended by Directive 2014/95/EU of the European Parliament and the Council regarding disclosure of non-financial and diversity information by certain large companies and groups [

71]. Authors’ intention is to highlight that lean management activities could be recognized as a part of ESG reporting, especially in area of risk management under Governance pillar as it is the internal system of practices, controls, and procedures a company adopts in order to govern itself, make effective decisions, comply with the law, and meet the needs of external stakeholders [

35]. In addition, operational risks arise from external events or imperfect and unfruitful internal systems, people, and processes. Digitalization strongly affects all management practices, shedding light on exceptional thinking and non-standard approaches. Cyber risks are a type of operational risks and are constantly evolving due to new technologies and the rapid development of computer information systems [

72]. It is mentioned here because the COVID-19 pandemic strongly changed the perception of cyber risk definitions and treatment, what can impact the future research.

5. Conclusions, Implications and Future Directions

The risk management aspect is not considered during process selection for improvements, and there is no sufficient cooperation between risk management and lean management teams enabling the full use of risk reduction opportunities. The qualitative and quantitative treatment of the obtained results shows that the analysis of only one perspective: lean management is not sufficient to conclude entirely on the final results of this research. Further studies are necessary to fully understand the organizational impact of the lean and risk management relationship.

In the lean management approach, control itself can indicate the existence of inefficiencies or errors in the process. The process should be built in such a way as to avoid making a mistake, and the organization should be committed to improving and streamlining the process, but not at the expense of making errors. Optimization itself would be teams working together, combining efforts in the framework of risk management and lean management. They have similar goals (minimization of errors) but perceive the process from a different angle. It is worth noting that not all risks should be controlled, particularly those related to minor processes. However, to be able to assess it, an entire process inventory is required. The scope of risk management also plays an important role, focusing on material risks and those potentially significant in terms of the company’s overarching goals.

The presented article highlights the context of the selection of lean management processes implemented in SSCs, defining the future research direction. Based on targeted literature review models and tools proposed by researchers were presented and discussed. Expert interviews helped to define preliminary considerations of the drivers and barriers to selecting lean management processes. A deeper analysis was necessary to examine how SSCs implemented lean management, not only from an organizational perspective but also in terms of the extent and scope of implementation. The results of the survey shed new light on this subject because the answers received were provided by people working in the lean management sector. This discussion should take place with the risk management teams working in the SSC in question. Lean management impacts not only risk management process, but also ESG reporting, in the area of governance. This is the reason why future direction of the research will be focused on following aspects:

It should also be pointed out that the conclusions from this research cannot become the basis for generalization; they only serve as concepts that should be taken into account when designing research that deepens understanding of the phenomenon. The main limitation of the research itself was the size and selection of the research sample based on willingness to participate in the research. The practical aspect of this part of the research is related to the usefulness of this knowledge for decision makers in the organization. People involved in lean management organizations and management staff can design activities in such a way as to implement lean management more effectively or at least avoid the practical pitfalls associated with it. Upon analyzing the statements, one could ask exploratory questions. One of them could refer to the short-sightedness of management in creating lean management structures, as described by one of the interviewees.

Conclusions based on empirical research allow for the conclusion that an SSC is often created to reduce costs; only in the long term can the potential benefits of standardization, automation, and building effective and efficient processes be noticed. Often, however, in the pursuit of cost reduction and the desire to achieve short-term benefits, these types of organizations do not focus sufficiently on a long-term strategy.

{kind=link}

{kind=link}

{kind=link}

{kind=link}