Mitigating Contagion Risk by ESG Investing

Abstract

:1. Introduction

2. Research Hypothesis

3. The Model

4. Empirical Analysis

4.1. Dataset Description

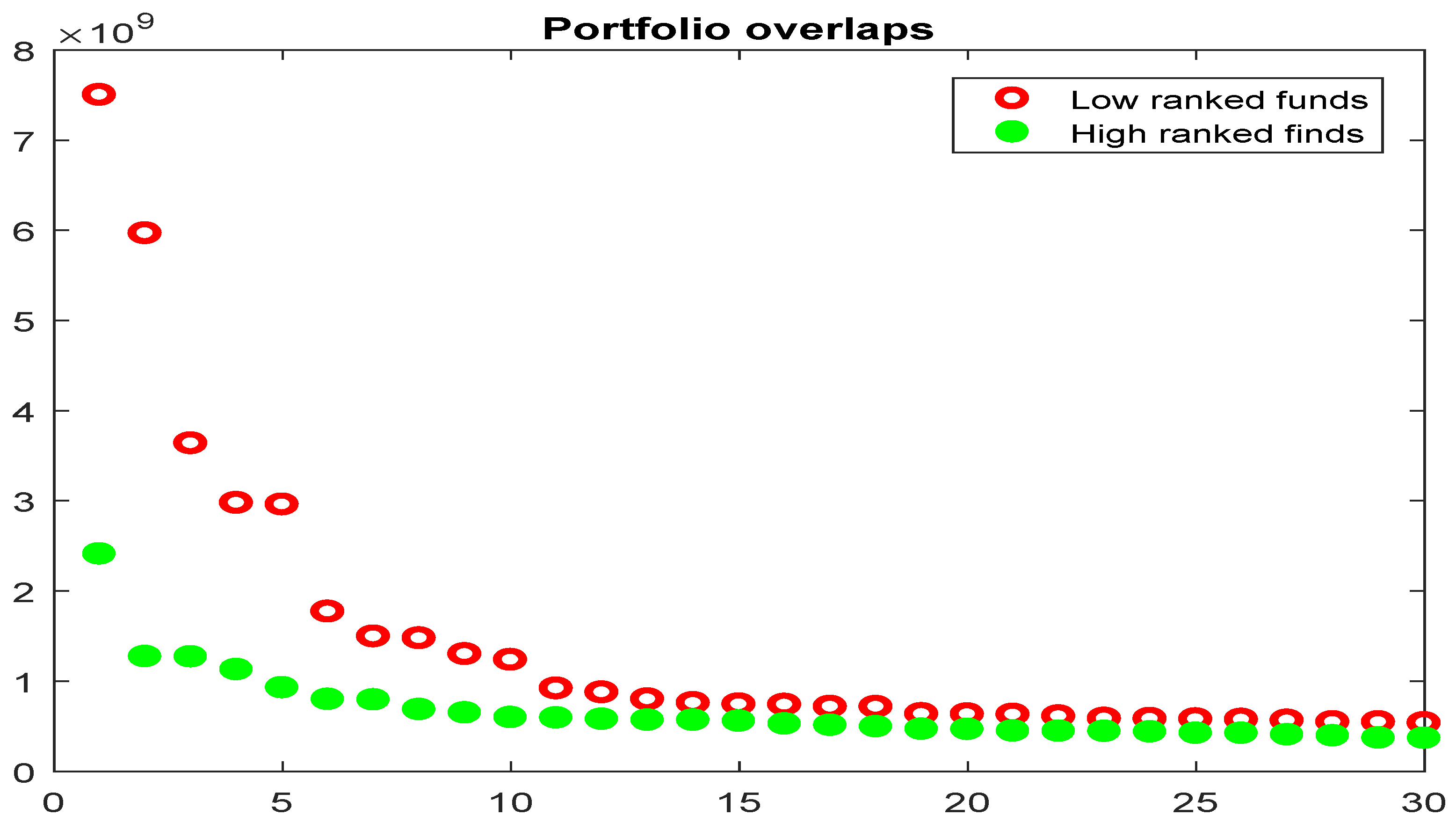

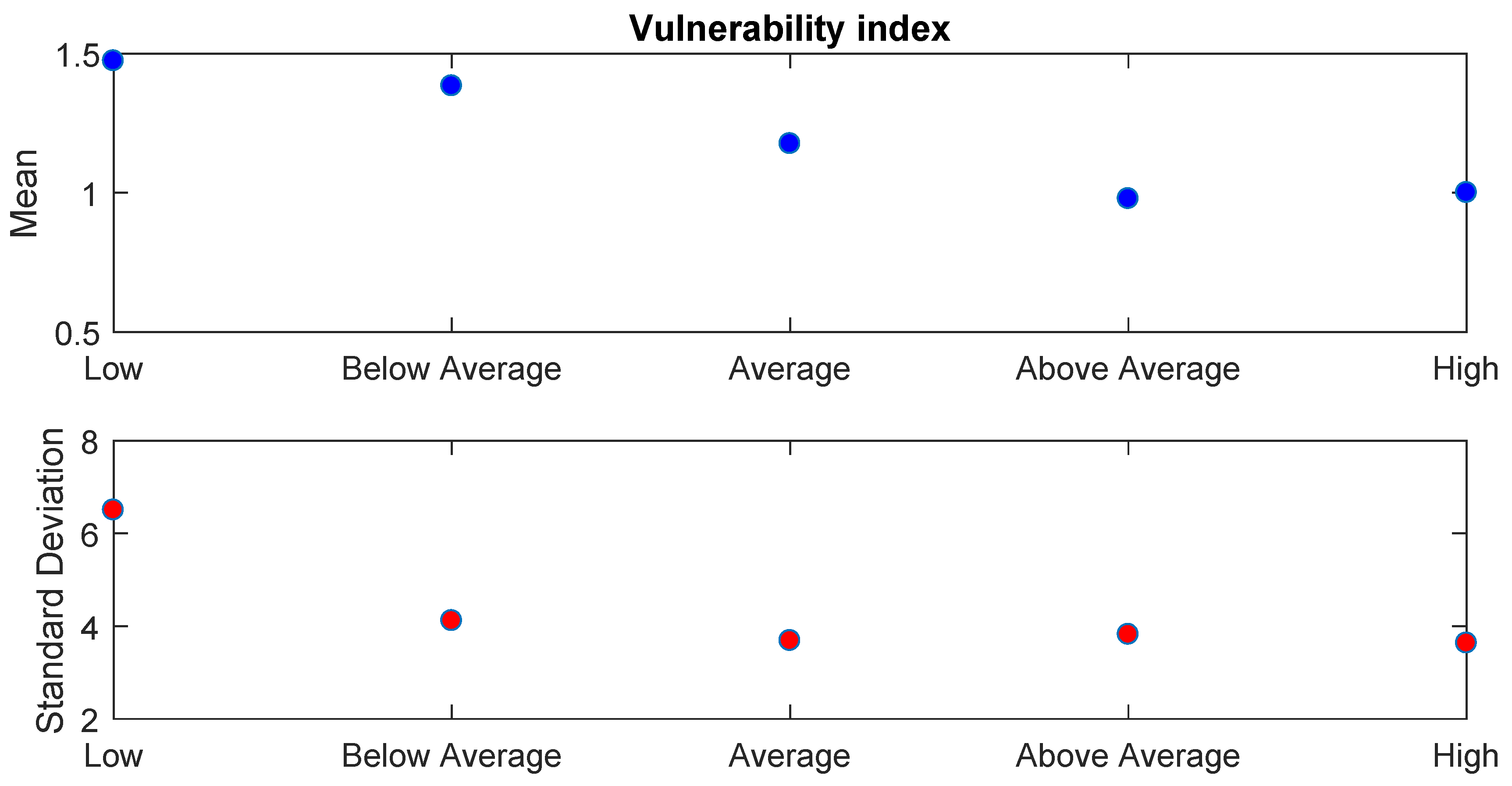

4.2. Results

5. Conclusions

6. Limitations and Outlook

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Conflicts of Interest

References

- Bauer, R.; Derwall, J.; Otten, R. The ethical mutual fund performance debate: New evidence from Canada. J. Bus. Ethics 2007, 70, 111–124. [Google Scholar] [CrossRef] [Green Version]

- El Ghoul, S.; Karoui, A. Does corporate social responsibility affect mutual fund performance and flows? J. Bank. Financ. 2017, 77, 53–63. [Google Scholar] [CrossRef]

- Nicolosi, M.; Grassi, S.; Stanghellini, E. Item response models to measure corporate social responsibility. Appl. Financ. Econ. 2014, 24, 1449–1464. [Google Scholar] [CrossRef] [Green Version]

- Herzel, S.; Nicolosi, M.; Stărică, C. The cost of sustainability in optimal portfolio decisions. Eur. J. Financ. 2012, 18, 333–349. [Google Scholar] [CrossRef]

- Kempf, A.; Osthoff, P. The effect of socially responsible investing on portfolio performance. Eur. Financ. Manag. 2007, 13, 908–922. [Google Scholar] [CrossRef] [Green Version]

- Glushkov, D.; Statman, M. The wages of social responsibility. Financ. Anal. J. 2009, 65, 33–46. [Google Scholar]

- Pástor, L.; Stambaugh, R.F.; Taylor, L.A. Sustainable investing in equilibrium. J. Financ. Econ. 2021, 142, 550–571. [Google Scholar] [CrossRef]

- Pedersen, L.H.; Fitzgibbons, S.; Pomorski, L. Responsible investing: The ESG-efficient frontier. J. Financ. Econ. 2021, 142, 572–597. [Google Scholar] [CrossRef]

- Heinkel, R.; Kraus, A.; Zechner, J. The effect of green investment on corporate behavior. J. Financ. Quant. Anal. 2001, 36, 431–449. [Google Scholar] [CrossRef]

- Merton, R.C. A simple model of capital market equilibrium with incomplete information. J. Financ. 1987, 42, 483–510. [Google Scholar] [CrossRef]

- Hong, H.; Kacperczyk, M. The price of sin: The effects of social norms on markets. J. Financ. Econ. 2009, 93, 15–36. [Google Scholar] [CrossRef]

- Luo, A.; Balvers, R. Social Screens and Systematic Investor Boycott Risk. J. Financ. Quant. Anal. 2017, 52, 365–399. [Google Scholar] [CrossRef] [Green Version]

- Kim, S.; Lee, G.; Kang, H.G. Risk management and corporate social responsibility. Strateg. Manag. J. 2021, 42, 202–230. [Google Scholar] [CrossRef]

- Bauer, R.; Koedijk, K.; Otten, R. International evidence on ethical mutual fund performance and investment style. J. Bank. Financ. 2005, 29, 1751–1767. [Google Scholar] [CrossRef] [Green Version]

- Bauer, R.; Otten, R.; Rad, A. Ethical investing in Australia: Is there a financial penalty? Pac.-Basin Financ. J. 2006, 14, 33–48. [Google Scholar] [CrossRef]

- Renneboog, L.; Horst, J.T.; Zhang, C. The price of ethics and stakeholder governance: The performance of socially responsible mutual funds. J. Corp. Finance 2008, 14, 302–322. [Google Scholar] [CrossRef]

- Ciciretti, R.; Daló, A.; Dam, L. The Contributions of Betas versus Characteristics to the ESG Premium; CEIS Working Paper No. 413.; 2019; Available online: https://papers.ssrn.com/sol3/Papers.cfm?abstract_id=3010234 (accessed on 31 January 2022).

- Chordia, T.; Goyal, A.; Shanken, J. Cross-Sectional Asset Pricing with Individual Stocks: Betas Versus Characteristics; SSRN Working Paper No. 2549578; SSRN: Rochester, NY, USA, 2017. [Google Scholar]

- Galema, R.; Plantinga, A.; Scholtens, B. The stocks at stake: Return and risk in socially responsible investment. J. Bank. Finance 2008, 32, 2646–2654. [Google Scholar] [CrossRef]

- Becchetti, L.; Ciciretti, R.; Dalò, A. Fishing the Corporate Social Responsibility Risk Factors. J. Financ. Stab. 2018, 37, 25–48. [Google Scholar] [CrossRef]

- Kim, Y.; Li, H.; Li, S. Corporate social responsibility and stock price crash risk. J. Bank. Finance 2014, 43, 1–13. [Google Scholar] [CrossRef] [Green Version]

- Boubaker, S.; Cellier, A.; Manita, R.; Saeed, A. Does corporate social responsibility reduce financial distress risk? Econ. Model. 2020, 91, 835–851. [Google Scholar] [CrossRef]

- Albuquerque, R.; Koskinen, Y.; Zhang, C. Corporate social responsibility and firm risk: Theory and empirical evidence. Manag. Sci. 2019, 65, 4451–4469. [Google Scholar] [CrossRef] [Green Version]

- Lins, K.V.; Servaes, H.; Tamayo, A. Social capital, trust, and firm performance: The value of corporate social responsibility during the financial crisis. J. Financ. 2017, 72, 1785–1824. [Google Scholar] [CrossRef] [Green Version]

- Nofsinger, J.; Varma, A. Socially responsible funds and market crises. J. Bank. Finance 2014, 48, 180–193. [Google Scholar] [CrossRef]

- Omura, A.; Roca, E.; Nakai, M. Does responsible investing pay during economic downturns: Evidence from the COVID-19 pandemic. Finance Res. Lett. 2021, 42, 101914. [Google Scholar] [CrossRef]

- Adamska, A.; Dąbrowski, T.J. Investor reactions to sustainability index reconstitutions: Analysis in different institutional contexts. J. Clean. Prod. 2021, 297, 126715. [Google Scholar] [CrossRef]

- Cerqueti, R.; Ciciretti, R.; Dalò, A.; Nicolosi, M. A new measure of the resilience for networks of funds with applications to socially responsible investments. Phys. A: Stat. Mech. Appl. 2022, 593, 126976. [Google Scholar] [CrossRef]

- Braverman, A.; Minca, A. Networks of common asset holdings: Aggregation and measures of vulnerability. J. Netw. Theory Finance 2018, 4, 53–78. [Google Scholar] [CrossRef]

- Coval, J.; Stafford, E. Asset fire sales (and purchases) in equity markets. J. Financ. Econ. 2007, 86, 479–512. [Google Scholar] [CrossRef] [Green Version]

- Flori, A.; Lillo, F.; Pammolli, F.; Spelta, A. Better to stay apart: Asset commonality, bipartite network centrality, and investment strategies. Ann. Oper. Res. 2021, 299, 177–213. [Google Scholar] [CrossRef] [Green Version]

- Guo, W.; Minca, A.; Wang, L. The topology of overlapping portfolio networks. Stat. Risk Model. 2016, 33, 139–155. [Google Scholar] [CrossRef]

- Cont, R.; Schaanning, E. Monitoring indirect contagion. J. Bank. Finance 2019, 104, 85–102. [Google Scholar] [CrossRef]

- Kyle, A.S. Continuous Auctions and Insider Trading. Econometrica 1985, 53, 1315–1335. [Google Scholar] [CrossRef] [Green Version]

- Charfeddine, L.; Najah, A.; Teulon, F. Socially responsible investing and Islamic funds: New perspectives for portfolio allocation. Res. Int. Bus. Finance 2016, 36, 351–361. [Google Scholar] [CrossRef]

- Joliet, R.; Titova, Y. Equity SRI funds vacillate between ethics and money: An analysis of the funds’ stock holding decisions. J. Bank. Finance 2018, 97, 70–86. [Google Scholar] [CrossRef]

- Bollen, N. Mutual fund attributes and investor behavior. J. Financ. Quant. Anal. 2007, 42, 683–708. [Google Scholar] [CrossRef] [Green Version]

- Amihud, Y. Illiquidity and stock returns: Cross-section and time-series effects. J. Financ. Mark. 2002, 5, 31–56. [Google Scholar] [CrossRef] [Green Version]

- Almgren, R.; Thum, C.; Hauptmann, E.; Li, H. Direct Estimation of Equity Market Impact. Risk 2005, 18, 57–62. [Google Scholar]

- Patel, S.; Sarkissian, S. To group or not to group? Evidence from mutual fund databases. J. Financ. Quant. Anal. 2017, 52, 1989–2021. [Google Scholar] [CrossRef] [Green Version]

- Cont, R.; Wagalath, L. Fire Sales Forensics: Measuring Endogenous Risk. Math. Finance 2016, 26, 835–866. [Google Scholar] [CrossRef] [Green Version]

- Ellul, A.; Jotikasthira, C.; Lundblad, C.T. Regulatory pressure and fire sales in the corporate bond market. J. Financ. Econ. 2011, 101, 596–620. [Google Scholar] [CrossRef]

{kind=link}

{kind=link}

{kind=link}

| L | A | H | |||

|---|---|---|---|---|---|

| L | 15,027 | 13,662 | 14,011 | 10,799 | 6885 |

| 16,014 | 14,475 | 10,878 | 7086 | ||

| A | 17,583 | 11,187 | 7072 | ||

| 11,711 | 7072 | ||||

| H | 7308 |

| Number of Assets—Panel A | |||||

|---|---|---|---|---|---|

| L | A | H | |||

| 14 | 16 | 16 | 15 | 15 | |

| 7807 | 7426 | 9699 | 4440 | 2661 | |

| 152 | 183 | 186 | 117 | 83 | |

| 607 | 512 | 409 | 220 | 189 | |

| 8.35 | 7.06 | 9.35 | 8.92 | 10.81 | |

| 81.53 | 67.11 | 165.94 | 135.36 | 136.28 | |

| Herfindahl–Hirschman Index—Panel B | |||||

| L | A | H | |||

| 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | |

| 0.22 | 0.17 | 0.27 | 0.19 | 0.21 | |

| 0.03 | 0.03 | 0.03 | 0.03 | 0.03 | |

| 0.02 | 0.02 | 0.02 | 0.02 | 0.02 | |

| 3.01 | 1.98 | 2.46 | 1.89 | 3.37 | |

| 23.49 | 11.66 | 17.20 | 10.14 | 22.50 | |

| Total Net Assets (Millions of USD)—Panel C | |||||

| L | A | H | |||

| 0.13 | 0.10 | 0.10 | 0.10 | 0.10 | |

| 3159.51 | 3129.50 | 3135.28 | 3055.27 | 3128.60 | |

| 177.84 | 166.92 | 184.46 | 196.11 | 204.68 | |

| 380.54 | 370.59 | 418.06 | 406.29 | 435.75 | |

| 3.95 | 4.13 | 4.04 | 3.71 | 3.47 | |

| 22.21 | 23.19 | 21.51 | 18.97 | 16.67 | |

| Annualized Average Daily Returns (%)—Panel D | |||||

| L | A | H | |||

| —32.21 | —114.34 | —73.12 | —35.15 | —28.52 | |

| 39.70 | 48.53 | 324.70 | 35.17 | 29.22 | |

| 6.38 | 4.99 | 4.84 | 4.54 | 3.72 | |

| 10.45 | 8.62 | 13.13 | 7.47 | 6.99 | |

| —0.02 | —2.03 | 12.99 | —0.27 | —0.28 | |

| 4.38 | 33.18 | 291.58 | 4.84 | 5.17 | |

| Standard Deviation (%) of Daily Returns—Panel A | |||||

|---|---|---|---|---|---|

| L | A | H | |||

| 2.22 | 2.15 | 2.17 | 2.01 | 1.93 | |

| 1.17 | 1.10 | 1.09 | 0.95 | 0.89 | |

| Average Daily Trading Volume (in Millions of Shares Traded)—Panel B | |||||

| L | A | H | |||

| 3.83 | 4.40 | 4.72 | 4.75 | 5.67 | |

| 160.40 | 155.61 | 148.53 | 181.79 | 228.80 | |

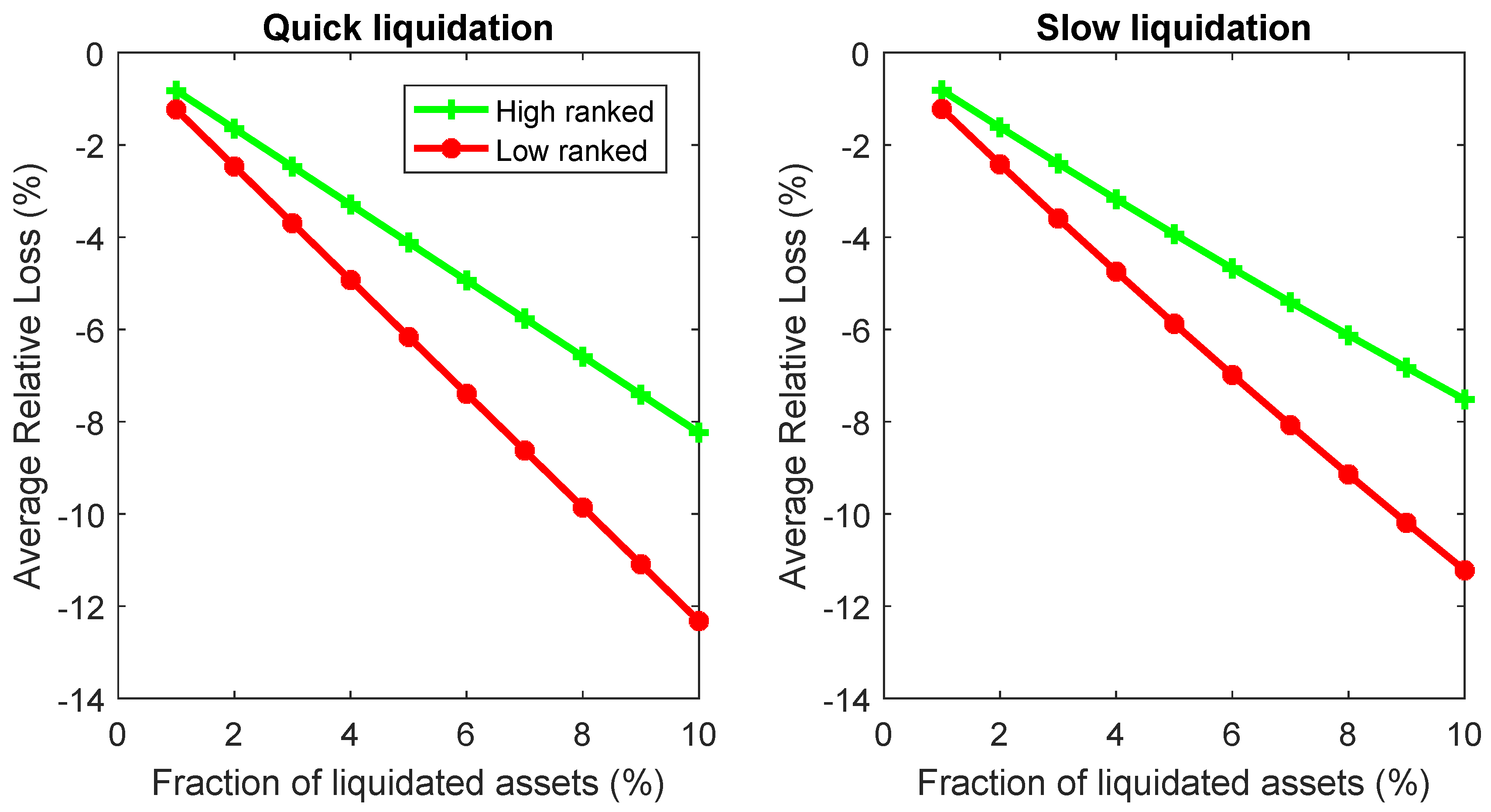

| Quick Liquidation | Slow Liquidation | |||

|---|---|---|---|---|

| LARGE | SMALL | |||

| 1 | 0.41 (*) | 0.02 | 0.73 (*) | 0.40 (*) |

| 2 | 0.82 (*) | 0.04 | 1.47 (*) | 0.80 (*) |

| 3 | 1.23 (*) | 0.05 | 2.20 (*) | 1.19 (*) |

| 4 | 1.64 (*) | 0.07 | 2.94 (*) | 1.57 (*) |

| 5 | 2.05 (*) | 0.09 | 3.67 (*) | 1.94 (*) |

| 6 | 2.45 (*) | 0.11 | 4.41 (*) | 2.31 (*) |

| 7 | 2.86 (*) | 0.13 | 5.14 (*) | 2.67 (*) |

| 8 | 3.27 (*) | 0.15 | 5.88 (*) | 3.02 (*) |

| 9 | 3.68 (*) | 0.16 | 6.61 (*) | 3.36 (*) |

| 10 | 4.09 (*) | 0.18 | 7.35 (*) | 3.70 (*) |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2022 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Cerqueti, R.; Ciciretti, R.; Dalò, A.; Nicolosi, M. Mitigating Contagion Risk by ESG Investing. Sustainability 2022, 14, 3805. https://doi.org/10.3390/su14073805

Cerqueti R, Ciciretti R, Dalò A, Nicolosi M. Mitigating Contagion Risk by ESG Investing. Sustainability. 2022; 14(7):3805. https://doi.org/10.3390/su14073805

Chicago/Turabian StyleCerqueti, Roy, Rocco Ciciretti, Ambrogio Dalò, and Marco Nicolosi. 2022. "Mitigating Contagion Risk by ESG Investing" Sustainability 14, no. 7: 3805. https://doi.org/10.3390/su14073805

APA StyleCerqueti, R., Ciciretti, R., Dalò, A., & Nicolosi, M. (2022). Mitigating Contagion Risk by ESG Investing. Sustainability, 14(7), 3805. https://doi.org/10.3390/su14073805