Australian Renewable-Energy Microgrids: A Humble Past, a Turbulent Present, a Propitious Future

Abstract

:1. Introduction

2. Materials and Methods: What Is a Microgrid?

3. Results

3.1. Recent Developments in the Australian Electricity Network and the Changing Role of Microgrids

3.2. Emerging Challenges and Opportunities

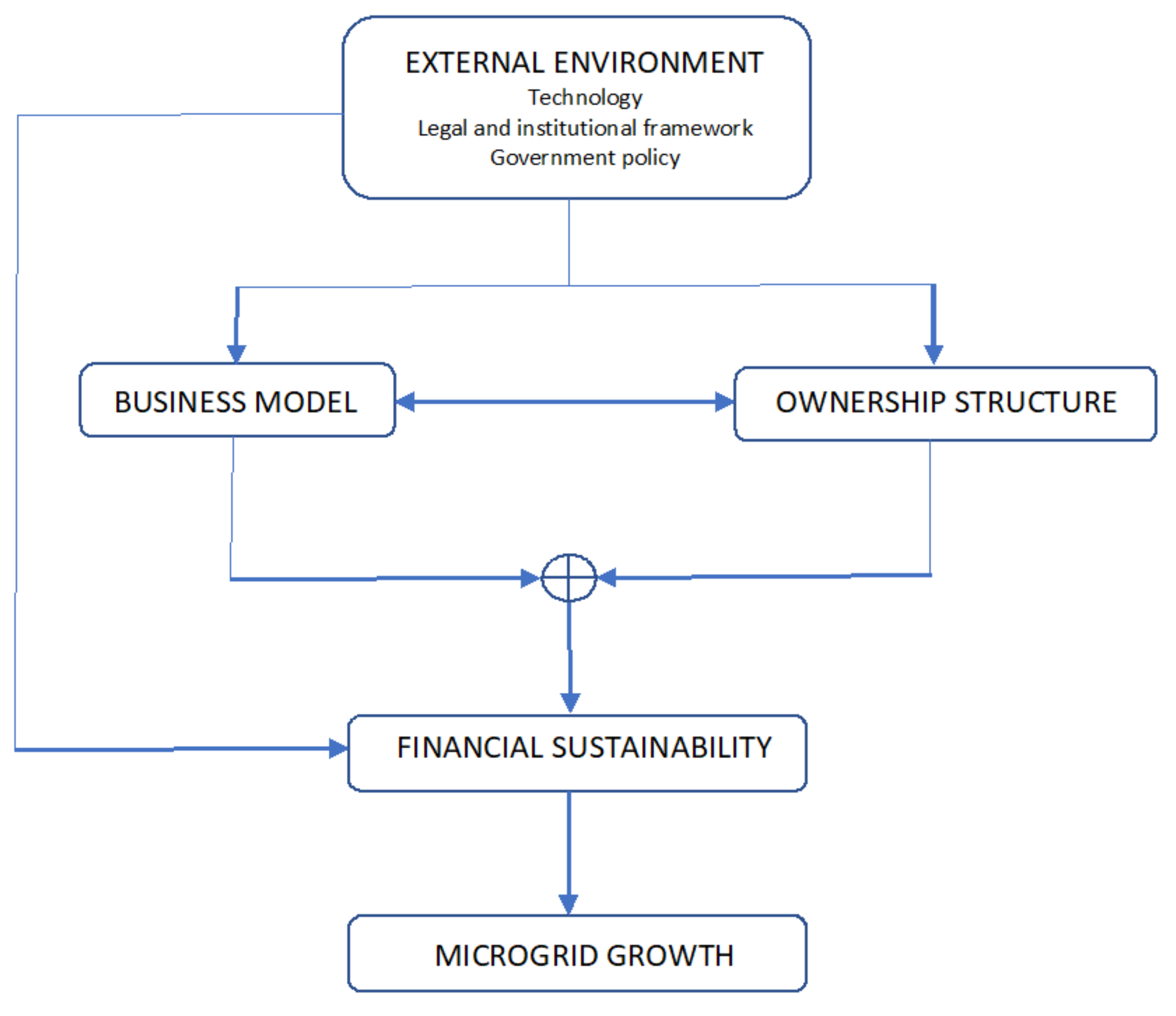

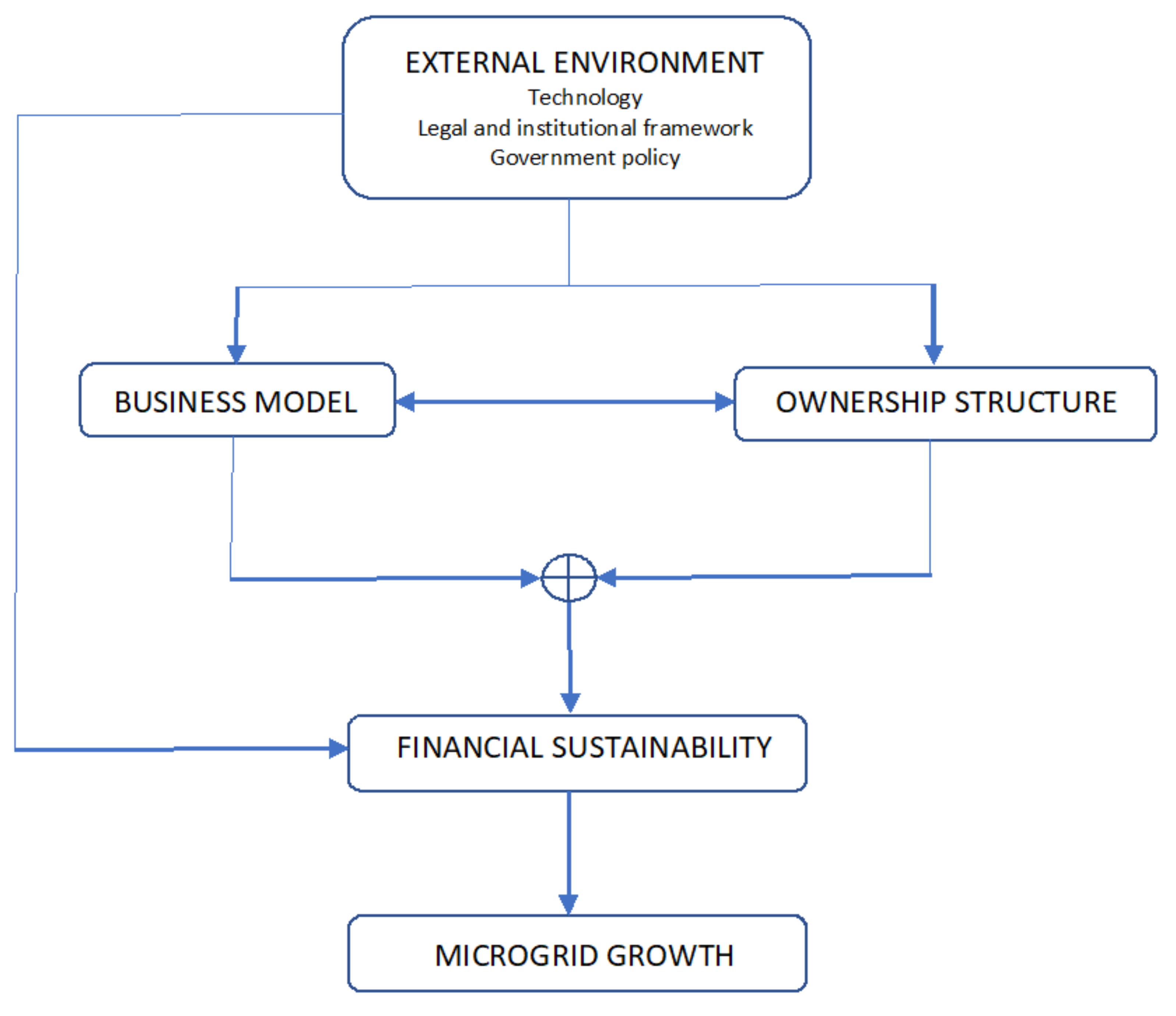

3.2.1. Ownership Structures and Business Models

3.2.2. Value Streams

3.2.3. Potential Sources of Finance

- Operating company with shareholders (investors, local investors and trustees on behalf of consumers), where the operating company sources the loan and operates the MG. The trusteeship provides consumer representation, while allowing larger owners some comfort, as well. Consumers can re-invest earnings into greater shareholding of the operating company. Tradability of consumer shares through trusteeship minimises disruption to other co-owners, and there is a cap on voting rights.

- A holding company is the owner and manager of the MG business. Financing and ownership are through the holding company. This structure also forms the basis of the third model.

- The third alternative is where the holding company controls more than one operating MG company, allowing for expansion geographically or horizontally.

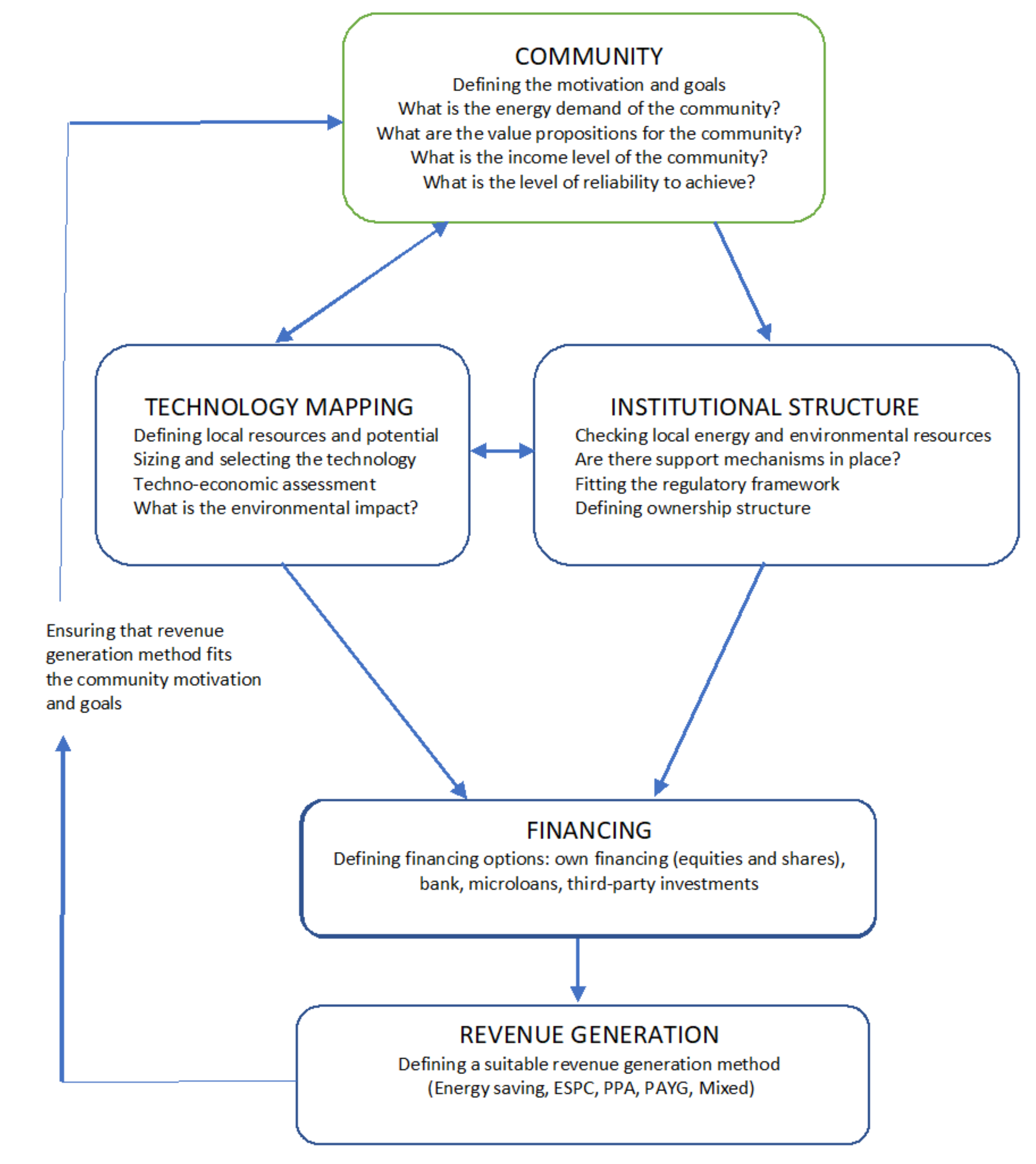

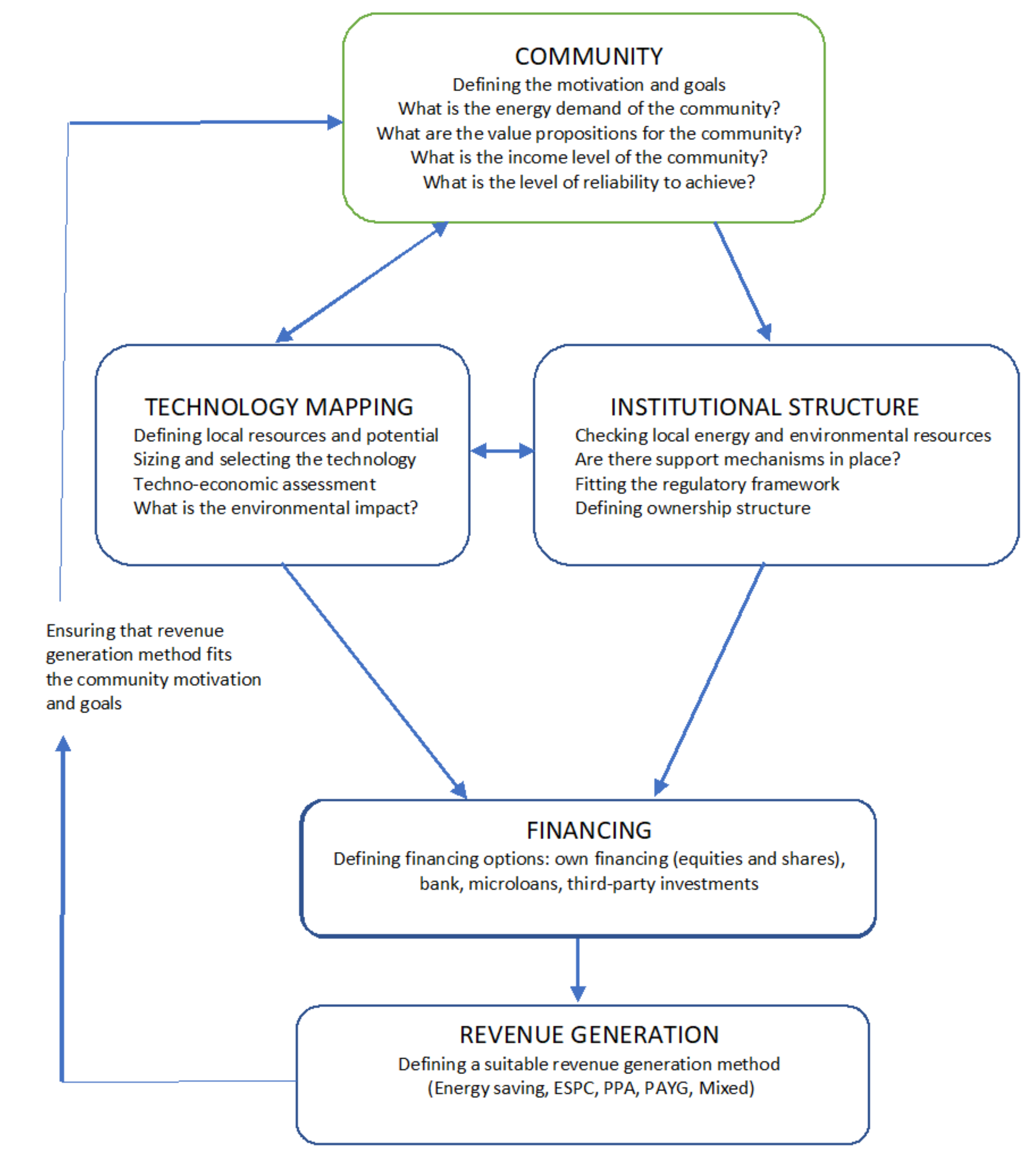

3.3. Community Microgrids

4. Discussion

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Acknowledgments

Conflicts of Interest

References

- Blakers, A.; Lu, B.; Stocks, M. 100% renewable energy in Australia. Energy 2017, 133, 471–482. [Google Scholar] [CrossRef]

- Green, J.; Newman, P. Citizen utilities: The emerging power paradigm. Energy Pol. 2017, 105, 283–293. [Google Scholar] [CrossRef]

- Howard, B.S.; Hamilton, N.E.; Diesendorf, M.; Wiedmann, T. Modeling the carbon budget of the Australian electricity sector’s transition to renewable energy. Renew. Energy 2018, 125, 712–728. [Google Scholar] [CrossRef]

- Shaukat, N.; Ali, S.M.; Mehmood, C.A.; Khan, B.; Jawad, M.; Farid, U.; Ullah, Z.; Anwar, S.M.; Majid, M. A survey on consumers’ empowerment, communication technologies, and renewable energy penetration within Smart Grid. Renew. Sustain. Energy Rev. 2018, 81, 1453–1475. [Google Scholar] [CrossRef]

- Wilkinson, S.; Hojckova, K.; Eon, C.; Morrison, G.M.; Sanden, B. Is peer-to-peer electricity trading empowering users? Evidence on motivations and roles in a prosumer business model trial in Australia. Energy Res. Soc. Sci. 2020, 66, 101500. [Google Scholar] [CrossRef]

- Warren, M. Blackout: How Is Energy-Rich Australia Running Out of Electricity? Affirm Press: South Melbourne, Australia, 2019. [Google Scholar]

- Li, H.X.; Edwards, D.J.; Hosseini, M.R.; Costin, G.P. A review on renewable energy transition in Australia: An updated depiction. J. Clean. Prod. 2020, 242, 118475. [Google Scholar] [CrossRef]

- Gui, E.M.; Diesendorf, M.; MacGill, I. Distributed energy infrastructure paradigm: Community microgrids in a new institutional economics context. Renew. Sustain. Energy Rev. 2017, 72, 1355–1365. [Google Scholar] [CrossRef]

- Lenhart, S.; Araujo, K. Microgrid decision-making by public power utilities in the United States: A critical assessment of adoption and technological profiles. Renew. Sustain. Energy Rev. 2021, 139, 110692. [Google Scholar] [CrossRef]

- Provance, M.; Donnelly, R.G.; Carayannis, E.G. Institutional influences on business model choice by new ventures in the microgenerated energy industry. Energy Policy 2011, 39, 5630–5637. [Google Scholar] [CrossRef]

- ARENA. Arena Opens $50 Million Fund for Regional Microgrid Projects; Australian Renewable Energy Agency, Australian Government: Canberra, Australia. Available online: https://arena.gov.au/blog/arena-opens-50-million-fund-for-regional-microgrid-projects (accessed on 10 December 2021).

- Warneryd, M.; Hakansson, M.; Karltop, K. Unpacking the complexity of community microgrids: A review of institutions’ roles for development of microgrids. Renew Sustain. Energy Rev. 2020, 121, 109690. [Google Scholar] [CrossRef]

- Austrade. Microgrids, Smart Grids and Energy Storage Solutions; Australian Trade and Investment Commission, Australian Government: Canberra, Australia, 2017. Available online: https://www.austrade.gov.au/ArticleDocuments/2814/Microgrids%20Smart%20Grids%20and%20Energy%20Storage%20Solutions.pdf.aspx (accessed on 10 December 2021).

- Antonelli, M.; Desideri, U.; Franco, A. Effects of large-scale penetration of renewables: The Italian case in the years 2008–2015. Renew. Sustain. Energy Rev. 2018, 81, 3090–3100. [Google Scholar] [CrossRef]

- Gielen, R.; Boshell, F.; Saygin, D.; Bazilian, M.D.; Wagner, N.; Gorini, R. The role of renewable energy in the global energy transformation. Energy Strat. Rev. 2019, 24, 38–50. [Google Scholar] [CrossRef]

- Millot, A.; Krook-Reikkola, A.; Maizi, N. Guiding the future energy transition to net zero emissions: Lessons from exploring the differences between France and Sweden. Energy Policy 2020, 139, 111358. [Google Scholar] [CrossRef]

- Alam, M.S.; Al-Ismail, F.S.; Salem, A.; Abido, M.A. High-level penetration of renewable energy sources into grid utility: Challenges and solutions. IEEE Access 2020, 8, 190278–190299. [Google Scholar] [CrossRef]

- Wilkinson, S.; Maticka, M.J.; Liu, Y.; John, M. The duck curve in a drying pond: The impact of rooftop PV on the Western Australian electricity market transition. Util. Policy 2021, 71, 101232. [Google Scholar] [CrossRef]

- Kasam-Griffith, A.; Turkmani, N.S.; Wolf, M.J.; Peluso, N.C.; Green, T.W. Transmission transition: Modernizing US transmission planning to support decarbonization. MIT Sci. Policy Rev. 2020, 1, 87–91. [Google Scholar] [CrossRef]

- Kyritsis, E.; Andersson, J.; Serletis, A. Electricity prices, large-scale renewable integration, and policy implications. Energy Policy 2017, 101, 550–560. [Google Scholar] [CrossRef] [Green Version]

- Dong, S.; Li, H.; Wallin, F.; Avelin, A.; Zhang, Q.; Yu, Z. Volatility of electricity price in Denmark and Sweden. Energy Procedia 2019, 158, 4331–4337. [Google Scholar] [CrossRef]

- Vittal, V. The impact of renewable resources on the performance and reliability of the electricity grid. Bridge 2010, 40, 5–12. [Google Scholar]

- Boyce, P.; Cantley-Smith, R.; Dkhissi, Y.; Ferraro, S.; Fullelove, T.; Fumei, S.; Gawler, R.; Leslie, G.; Young, D. Victorian Market Assessment for Microgrid Electricity Market Operators, White Paper; Monash University: Melbourne, VIC, Australia, 2019; Available online: https://www.monash.edu/__data/assets/pdf_file/0010/1857313/Monash-Net-Zero_Microgrid-Operator-Whitepaper_20190617-1.pdf (accessed on 10 December 2021).

- Hartmann, I. The Macro Impacts of Australian Microgrids. Energy Magazine. 2020. Available online: https://www.energymagazine.com.au/the-macro-impacts-of-australian-microgrids (accessed on 10 December 2021).

- Handberg, K. Microgrids: The Pathway to Australia’s Smarter, Cleaner Energy Future; International Specialised Skills Institute: Melbourne, VIC, Australia, 2016; Available online: https://www.issinstitute.org.au/wp-content/uploads/2016/10/handberg-Final-LowRes.pdf (accessed on 10 December 2021).

- Western Australia Parliament. Implications of a Distributed Energy Future: Interim report, Economics and Industry Standing Committee, Legislative Assembly; Parliament of Western Australia: Perth, WA, Australia, 2019. Available online: https://www.parliament.wa.gov.au/Parliament/commit.nsf/(Report+Lookup+by+Com+ID)/B78DC78FC2007FAE482583D7002E3073/$file/Microgrids%20Report-%20Part%201-%20FINAL%20for%20web.pdf (accessed on 10 December 2021).

- Ustun, T.S.; Ozansoy, C.; Zayegh, A. Recent developments in microgrids and example cases around the world—A review. Renew. Sustain. Energy Rev. 2011, 15, 4030–4041. [Google Scholar] [CrossRef]

- Genc, T.S.; Reynolds, S.S. Who should own a renewable technology? Ownership theory and an application. Int. J. Ind. Org. 2019, 63, 213–238. [Google Scholar] [CrossRef]

- Sachs, T.; Grundler, A.; Rusic, M.; Fridgen, G. Farming microgrid design from a business and information systems engineering perspective. Bus. Inform. Syst. Eng. 2019, 61, 729–744. [Google Scholar] [CrossRef] [Green Version]

- Vanadzina, E.; Mendes, G.; Honkapuro, S.; Pinomaa, A.; Melkas, H. Business models for community microgrids. In Proceedings of the 16th International Conference on the European Energy Market (EEM), Ljubljana, Slovenia, 18–20 September 2019; pp. 1–7. [Google Scholar]

- Martin-Martínez, F.; Sánchez-Miralles, A.; Rivier, M. A literature review of Microgrids: A functional layer-based classification. Renew. Sustain. Energy Rev. 2016, 62, 1133–1153. [Google Scholar] [CrossRef]

- Fioriti, D.; Frangioni, A.; Poli, P. Optimal sizing of energy communities with fair revenue sharing and exit clauses: Value, role and business models of aggregators and users. Appl. Energy 2021, 299, 117328. [Google Scholar] [CrossRef]

- Engelken, M.; Romer, B.; Drescher, M.; Welpe, I.M. Picot, Comparing drivers, barriers and opportunities of business models for renewable energies: A review. Renew. Sustain. Energy Rev. 2016, 60, 795–809. [Google Scholar] [CrossRef]

- Krog, L.; Sperling, K.; Lund, H. Barriers and recommendations to innovative ownership models for wind power. Energies 2018, 11, 2602. [Google Scholar] [CrossRef] [Green Version]

- Brummer, V. Community energy—Benefits and barriers: A comparative literature review of Community Energy in the UK, Germany and the USA, their benefits it provides for society and the barriers it faces. Renew. Sustain. Energy Rev. 2018, 94, 187–196. [Google Scholar] [CrossRef]

- Gorroño-Albizu, L.; Sperling, K.; Djørup, S. The past, present and uncertain future of community energy in Denmark: Critically reviewing and conceptualising citizen ownership. Energy Res. Soc. Sci. 2019, 57, 101231. [Google Scholar] [CrossRef]

- Sauter, R.; Watson, J. Strategies for the deployment of micro-generation: Implications for social acceptance. Energy Policy 2007, 35, 2770–2779. [Google Scholar] [CrossRef]

- Hanna, R.; Ghonima, M.; Kleissl, J.; Tynan, G.; Victor, D.G. Evaluating business models for microgrids: Interactions of technology and policy. Energy Policy 2017, 103, 47–61. [Google Scholar] [CrossRef]

- Ubilla, K.; Jiménez-Estévez, G.A.; Hernádez, R.; Reyes-Chamorro, L.; Irigoyen, C.H.; Severino, B.; Palmaehnke, R. Smart microgrids as a solution for rural electrification: Ensuring long-term sustainability through cadastre and business models. IEEE Trans. Sustain. Energy 2014, 5, 1310–1318. [Google Scholar] [CrossRef]

- Stadler, M.; Cardoso, G.; Mashayekh, S.; Forget, T.; DeForest, N.; Agarwal, A.; Schönbein, A. Value streams in microgrids: A literature review. Appl. Energy 2016, 162, 980–989. [Google Scholar] [CrossRef] [Green Version]

- Fridgen, G.; Kahlen, M.; Ketter, W.; Rieger, A.; Thimmel, M. One rate does not fit all: An empirical analysis of electricity tariffs for residential microgrids. Appl. Energy 2018, 210, 800–814. [Google Scholar] [CrossRef] [Green Version]

- Giraldez Miner, J.I.; Flores-Espino, F.; MacAlpine, S.; Asmus, P. Phase I Microgrid Cost Study: Data Collection and Analysis of Microgrid Costs in the United States; (No. NREL/TP-5D00-67821); National Renewable Energy Lab. (NREL): Golden, CO, USA, 2018. [Google Scholar]

- Weng, S. Distributed cooperative control for frequency and voltage stability in isolated microgrid under event-triggered mechanism. In Proceedings of the 2018 Australian & New Zealand Control Conference (ANZCC), Melbourne, VIC, Australia, 7–8 December 2018; pp. 366–370. [Google Scholar]

- Li, Y.; Nejabatkhah, F. Overview of control, integration and energy management of microgrids. J. Mod. Power Syst. Clean Energy 2014, 2, 212–222. [Google Scholar] [CrossRef] [Green Version]

- Marzband, M.; Sumper, A.; Domínguez-García, J.L.; Gumara-Ferret, R. Experimental validation of a real time energy management system for microgrids in islanded mode using a local day-ahead electricity market and MINLP. Energy Convers. Manag. 2013, 76, 314–322. [Google Scholar] [CrossRef]

- Maley, V.; Safarik, M.; Matousek, R. Consumer (Co-)Ownership in the Czech Republic. In Energy Transition: Financing Consumer Co-Ownership in Renewables; Lowitzsch, J., Ed.; Palgrave Macmillan: Frankfurt, Germany, 2018; pp. 201–222. [Google Scholar]

- Wokuri, P.; Yalcin-Riollet, M.; Gauthier, C. Consumer (Co-)Ownership in France. In Energy Transition: Financing Consumer Co-ownership in Renewables; Lowitzsch, J., Ed.; Palgrave Macmillan: Frankfurt, Germany, 2018; pp. 245–270. [Google Scholar]

- Borroni, A.; van Tulder, F. Consumer (Co-)Ownership in Italy. In Energy Transition: Financing Consumer Co-ownership in Renewables; Lowitzsch, J., Ed.; Palgrave Macmillan: Frankfurt, Germany, 2018; pp. 295–318. [Google Scholar]

- Akerboom, S.; van Tulder, F. Consumer (Co-)Ownership in the Netherlands. In Energy Transition: Financing Consumer Co-ownership in Renewables; Lowitzsch, J., Ed.; Palgrave Macmillan: Frankfurt, Germany, 2018; pp. 319–344. [Google Scholar]

- Willis, R.; Simcock, N. Consumer (Co-)Ownership in England and Wales (UK). In Energy Transition: Financing Consumer Co-ownership in Renewables; Lowitzsch, J., Ed.; Palgrave Macmillan: Frankfurt, Germany, 2018; pp. 369–394. [Google Scholar]

- Broughel, A.E.; Stauch, A.; Schmid, B.; Vuichard, P. Consumer (Co-)Ownership in Switzerland. In Energy Transition: Financing Consumer Co-ownership in Renewables; Lowitzsch, J., Ed.; Palgrave Macmillan: Frankfurt, Germany, 2018; pp. 451–476. [Google Scholar]

- Ronne, A.; Neilson, F.G. Consumer (Co-)Ownership in Denmark. In Energy Transition: Financing Consumer Co-ownership in Renewables; Lowitzsch, J., Ed.; Palgrave Macmillan: Frankfurt, Germany, 2018; pp. 223–244. [Google Scholar]

- Yildiz, O.; Gotchen, B.; Holsetnkamp, L.; Muller, J.R.; Welle, L. Consumer (Co-)Ownership in Germany. In Energy Transition: Financing Consumer Co-ownership in Renewables; Lowitzsch, J., Ed.; Palgrave Macmillan: Frankfurt, Germany, 2018; pp. 271–294. [Google Scholar]

- Lowitzsch, J. Consumer stock ownership plans (CSOPs)—The prototype business model for renewable energy communities. Energies 2020, 13, 118. [Google Scholar] [CrossRef] [Green Version]

- Schreuer, A. Energy Co-Operatives and Local Ownership in the Field Of Renewable Energy—Country Cases Austria and Germany; Research Institute for Co-Operation and Co-Operatives, WU Vienna University of Economics and Business: Vienna, Austria, 2012. [Google Scholar]

- Wirfs-Brock, J. Lost in transmission: How much electricity disappears between a power plant and your plug? Inside Energy 2015, 6. Available online: http://insideenergy.org/2015/11/06/lost-intransmission-how-much-electricity-disappears-between-a-power-plant-and-your-plug (accessed on 10 December 2021).

- Lovati, M.; Zhang, X.; Huang, P.; Olsmats, C.; Maturi, L. Optimal simulation of three peer to peer (P2P) business models for individual PV prosumers in a local electricity market using agent-based modelling. Buildings 2020, 10, 138. [Google Scholar] [CrossRef]

- Zhang, C.; Wu, J.; Cheng, M.; Zhou, Y.; Long, C. A bidding system for peer-to-peer energy trading in a grid-connected microgrid. Energy Procedia 2016, 103, 147–152. [Google Scholar] [CrossRef]

- Baez-Gonzalez, P.; Rodriguez-Diaz, E.; Carlini, M.A.R.; Bordons, C. A power P2P market framework to boost renewable energy exchanges in local microgrids. In Proceedings of the 2019 International Conference on Smart Energy Systems and Technologies (SEST), Porto, Portugal, 9–11 September 2019; pp. 1–6. [Google Scholar] [CrossRef]

- Paudel, A.; Beng, G.H. A hierarchical peer-to-peer energy trading in community microgrid distribution systems. In Proceedings of the 2018 IEEE Power & Energy Society General Meeting (PESGM), Portland, OR, USA, 5–10 August 2018; pp. 1–5. [Google Scholar] [CrossRef]

- Long, C.; Wu, J.; Zhou, Y.; Jenkins, N. Peer-to-peer energy sharing through a two-stage aggregated battery control in a community Microgrid. Appl. Energy 2018, 226, 261–276. [Google Scholar] [CrossRef]

- California Energy Commission. Microgrid Analysis and Case Studies Report California, North America, and Global Case Studies; Energy Research and Development: Sacramento, CA, USA, 2018. [Google Scholar]

- Robert, F.C.; Sisodia, G.S.; Gopalan, S. The critical role of anchor customers in rural microgrids: Impact of load factor on energy costs. In Proceedings of the 2017 International Conference on Computation of Power, Energy Information and Communication (ICCPEIC), Melmaruvathur, India, 22–23 March 2018; pp. 398–403. [Google Scholar] [CrossRef]

- Dibaba, H.; Vanadzina, E.; Mendes, G.; Pinomaa, A.; Honkapuro, S. Business model design for rural off-the-grid electrification and digitalization concept. In Proceedings of the 2020 17th International Conference on the European Energy Market (EEM), Stockholm, Sweden, 16–18 September 2020; pp. 1–5. [Google Scholar] [CrossRef]

- Arcos-Aviles, D.; Guinjoan, F.; Pascual, J.; Marroyo, L.; Sanchis, P.; Gordillo, R.; Ayala, P.; Marietta, M.P. A review of fuzzy-based residential grid-connected microgrid energy management strategies for grid power profile smoothing. In Energy Sustainability in Built and Urban Environments; Motoasca, E., Agarwal, A., Breesch, H., Eds.; Springer: Singapore, 2019; pp. 165–199. [Google Scholar] [CrossRef]

- Meena, N.K.; Yang, J.; Zacharis, E. Optimisation framework for the design and operation of open-market urban and remote community microgrids. Appl. Energy 2019, 252, 113399. [Google Scholar] [CrossRef]

- Li, J.; Liu, Y.; Wu, L. Optimal operation for community-based multi-party microgrid in grid-connected and Islanded modes. IEEE Trans. Smart Grid 2018, 9, 756–765. [Google Scholar] [CrossRef]

- Müller, S.C.; Welpe, I.M. Sharing electricity storage at the community level: An empirical analysis of potential business models and barriers. Energy Policy 2018, 118, 492–503. [Google Scholar] [CrossRef]

- Walker, G. What are the barriers and incentives for community-owned means of energy production and use? Energy Policy 2008, 26, 4401–4405. [Google Scholar] [CrossRef]

- Geels, F.W. Processes and patterns in transitions and system innovations: Refining the co-evolutionary multi-level perspective. Technol. Forecast. Soc. Chang. 2005, 72, 681–696. [Google Scholar] [CrossRef]

- Geels, F.W.; Marko, P.H.; Jacobsson, S. The dynamics of sustainable innovation journeys. Tech. Anal. Strat. Manag. 2008, 20, 521–536. [Google Scholar] [CrossRef] [Green Version]

- Raven, R.P.J.M. Niche accumulation and hybridisation strategies in transition processes towards a sustainable energy system: An assessment of differences and pitfalls. Energy Policy 2007, 35, 2390–2400. [Google Scholar] [CrossRef]

- Verbong, G.; Geels, F.W.; Raven, R. Multi-niche analysis of dynamics and policies in Dutch renewable energy innovation journeys (1970–2006): Hype-cycles, closed networks and technology-focused learning. Technol. Anal. Strateg. 2008, 20, 555–573. [Google Scholar] [CrossRef]

- Geels, F.W.; Schot, J. Typology of sociotechnical transition pathways. Res. Policy 2007, 36, 399–417. [Google Scholar] [CrossRef]

- Smith, A.; Hargreaves, T.; Hielscher, S.; Martiskainen, M.; Seyfang, G. Making the most of community energies: Three perspectives on grassroots innovation. Environ. Plan. A 2016, 48, 407–432. [Google Scholar] [CrossRef] [Green Version]

{kind=link}

{kind=link}

| Microgrids by Ownership Types/Users | |||||

|---|---|---|---|---|---|

| Capital/Revenue Source | Customer-Owned/Mixed | Public Utility | Third Party | Community | Industrial |

| Grants from government. | * | * | |||

| Commercial loans | * | * | * | * | * |

| Debt/equity (private investors) | * | * | * | * | |

| Debt/equity (public investors) | * | * | * | * | |

| Venture capital/private equity | * | ||||

| Community cooperatives | * | * | |||

| Energy agreement (ESA/PPA) | * | * | * | * | * |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2022 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Wright, S.; Frost, M.; Wong, A.; Parton, K.A. Australian Renewable-Energy Microgrids: A Humble Past, a Turbulent Present, a Propitious Future. Sustainability 2022, 14, 2585. https://doi.org/10.3390/su14052585

Wright S, Frost M, Wong A, Parton KA. Australian Renewable-Energy Microgrids: A Humble Past, a Turbulent Present, a Propitious Future. Sustainability. 2022; 14(5):2585. https://doi.org/10.3390/su14052585

Chicago/Turabian StyleWright, Simon, Mark Frost, Alfred Wong, and Kevin A. Parton. 2022. "Australian Renewable-Energy Microgrids: A Humble Past, a Turbulent Present, a Propitious Future" Sustainability 14, no. 5: 2585. https://doi.org/10.3390/su14052585

APA StyleWright, S., Frost, M., Wong, A., & Parton, K. A. (2022). Australian Renewable-Energy Microgrids: A Humble Past, a Turbulent Present, a Propitious Future. Sustainability, 14(5), 2585. https://doi.org/10.3390/su14052585