Supply Chain Emission Reduction Decisions, Considering Overconfidence under Conditions of Carbon Trading Price Volatility

Abstract

1. Introduction

2. Literature Review

2.1. Studies Related to Carbon Trading Prices

2.2. Overconfidence

2.3. Research Related to Supply Chain Emissions Reduction Decisions under a Carbon Policy

3. Methodology and Model Assumptions

3.1. Methodology

3.2. Problem Description

3.3. Model Assumptions

4. Decision-Making Models

4.1. Decision-Making Model for Emission Reduction by Manufacturers without Carbon Trading (Scenario 1)

4.2. Decision-Making Model for Manufacturers to Reduce Emissions under the Carbon Trading Market (Scenario 2)

4.3. Emission Reduction Decision-Making Model Considering Manufacturer Overconfidence under a Carbon Trading Market (Scenario 3)

5. Model Analysis and Discussion

5.1. Analysis of the Impact of Carbon Trading Markets on Manufacturers’ Emissions Reductions and Profits

5.2. Analysis of the Impact of Overconfidence on Supply Chain Members’ Emissions Reductions and Profits

6. Numerical Study

6.1. Overconfidence and the Impact of Carbon Trading Prices on Supply Chain Members

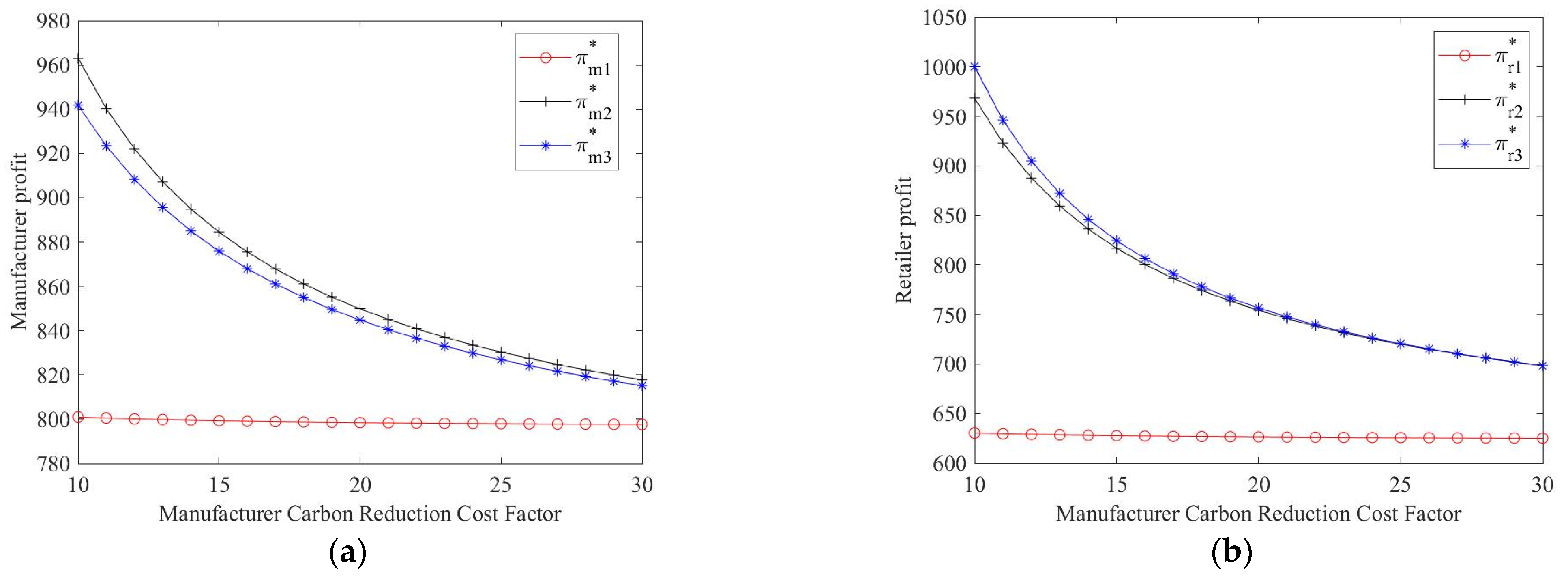

6.2. Impact of the Manufacturer’s Emission Reduction Cost Factor

7. Conclusions

7.1. Main Conclusions

7.2. Management Insights and Future Research

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Conflicts of Interest

Appendix A

References

- Shakoor, A.; Ashraf, F.; Shakoor, S.; Mustafa, A.; Rehman, A.; Altaf, M.M. Biogeochemical transformation of greenhouse gas emissions from terrestrial to atmospheric environment and potential feedback to climate forcing. Environ. Sci. Pollut. Res. 2020, 27, 38513–38536. [Google Scholar] [CrossRef] [PubMed]

- Hu, Y.G.; Xu, B.X.; Wang, Y.N.; He, Z.Z.; Zhang, P.; Wang, G.J. Reference for different sensitivities of greenhouse gases effluxes to warming climate among types of desert biological soil crust. Sci. Total Environ. 2022, 830, 11. [Google Scholar] [CrossRef]

- Li, H.M.; Wang, X.C.; Zhao, X.F.; Qi, Y. Understanding systemic risk induced by climate change. Adv. Clim. Chang. Res. 2021, 12, 384–394. [Google Scholar] [CrossRef]

- Kannan, D.; Solanki, R.; Kaul, A.; Jha, P.C. Barrier analysis for carbon regulatory environmental policies implementation in manufacturing supply chains to achieve zero carbon. J. Clean. Prod. 2022, 358, 18. [Google Scholar] [CrossRef]

- Hintermann, B.; Zarkovic, M. A carbon horse race: Abatement subsidies vs. permit trading in Switzerland. Clim. Policy 2021, 21, 290–306. [Google Scholar] [CrossRef]

- Ma, C.; Yang, H.G.; Zhang, W.P.; Huang, S. Low-carbon consumption with government subsidy under asymmetric carbon emission information. J. Clean. Prod. 2021, 318, 17. [Google Scholar] [CrossRef]

- Chen, X.; Lin, B.Q. Towards carbon neutrality by implementing carbon emissions trading scheme: Policy evaluation in China. Energy Policy 2021, 157, 12. [Google Scholar] [CrossRef]

- Yang, X.; Pang, J.; Teng, F.; Gong, R.X.; Springer, C. The environmental co-benefit and economic impact of China’s low-carbon pathways: Evidence from linking bottom-up and top-down models. Renew. Sustain. Energy Rev. 2021, 136, 22. [Google Scholar] [CrossRef]

- Teixido, J.; Verde, S.F.; Nicolli, F. The impact of the EU Emissions Trading System on low-carbon technological change: The empirical evidence. Ecol. Econ. 2019, 164, 13. [Google Scholar] [CrossRef]

- Stern, N. Towards a carbon neutral economy: How government should respond to market failures and market absence. J. Gov. Econ. 2022, 6, 100036. [Google Scholar] [CrossRef]

- Cheng, Y.; Fan, T.; Zhou, L. Optimal strategies of automakers with demand and credit price disruptions under the dual-credit policy. J. Manag. Sci. Eng. 2022, 7, 453–472. [Google Scholar] [CrossRef]

- Cheng, F.; Chen, T.; Chen, Q. Cost-reducing strategy or emission-reducing strategy? The choice of low-carbon decisions under price threshold subsidy. Transp. Res. Pt. E-Logist. Transp. Rev. 2022, 157, 20. [Google Scholar] [CrossRef]

- Kahneman, D.; Tversky, A. Prospect Theory: An Analysis of Decision under Risk. Econometrica 1979, 47, 263–292. [Google Scholar] [CrossRef]

- Fischhoff, B.; Slovic, P.; Lichtenstein, S. Knowing with certainty the appropriateness of extreme confidence. J. Exp. Psychol. 1977, 3, 552–564. [Google Scholar] [CrossRef]

- Zhou, J.G.; Wang, Q.Q. Forecasting Carbon Price with Secondary Decomposition Algorithm and Optimized Extreme Learning Machine. Sustainability 2021, 13, 17. [Google Scholar] [CrossRef]

- Zhou, J.G.; Chen, D.F. Carbon Price Forecasting Based on Improved CEEMDAN and Extreme Learning Machine Optimized by Sparrow Search Algorithm. Sustainability 2021, 13, 20. [Google Scholar] [CrossRef]

- Wang, J.J.; Cui, Q.; Sun, X. A novel framework for carbon price prediction using comprehensive feature screening, bidirectional gate recurrent unit and Gaussian process regression. J. Clean. Prod. 2021, 314, 19. [Google Scholar] [CrossRef]

- Yun, P.; Zhang, C.; Wu, Y.; Yang, X.; Wagan, Z.A. A Novel Extended Higher-Order Moment Multi-Factor Framework for Forecasting the Carbon Price: Testing on the Multilayer Long Short-Term Memory Network. Sustainability 2020, 12, 1869. [Google Scholar] [CrossRef]

- Song, X.H.; Zhang, W.; Ge, Z.Q.; Huang, S.Q.; Huang, Y.M.; Xiong, S.J. A Study of the Influencing Factors on the Carbon Emission Trading Price in China Based on the Improved Gray Relational Analysis Model. Sustainability 2022, 14, 27. [Google Scholar] [CrossRef]

- Zhang, S.B.; Ji, H.; Tian, M.X.; Wang, B.Y. High-dimensional nonlinear dependence and risk spillovers analysis between China’s carbon market and its major influence factors. Ann. Oper. Res. 2022. [Google Scholar] [CrossRef]

- Xu, Y.; Zhai, D. Impact of Changes in Membership on Prices of a Unified Carbon Market: Case Study of the European Union Emissions Trading System. Sustainability 2022, 14, 13806. [Google Scholar] [CrossRef]

- Hao, Y.; Tian, C.S.; Wu, C.Y. Modelling of carbon price in two real carbon trading markets. J. Clean. Prod. 2020, 244, 15. [Google Scholar] [CrossRef]

- Fan, Y.; Jia, J.J.; Wang, X.; Xu, J.H. What policy adjustments in the EU ETS truly affected the carbon prices? Energy Policy 2017, 103, 145–164. [Google Scholar] [CrossRef]

- Hao, Y.; Tian, C.S. A hybrid framework for carbon trading price forecasting: The role of multiple influence factor. J. Clean. Prod. 2020, 262, 20. [Google Scholar] [CrossRef]

- Hasan, M.R.; Roy, T.C.; Daryanto, Y.; Wee, H.-M. Optimizing inventory level and technology investment under a carbon tax, cap-and-trade and strict carbon limit regulations. Sustain. Prod. Consum. 2021, 25, 604–621. [Google Scholar] [CrossRef]

- Fleschutz, M.; Bohlayer, M.; Braun, M.; Henze, G.; Murphy, M.D. The effect of price-based demand response on carbon emissions in European electricity markets: The importance of adequate carbon prices. Appl. Energy 2021, 295, 15. [Google Scholar] [CrossRef]

- Li, J.; Liang, L.; Xie, J.Q.; Xie, J.P. Manufacture’s entry and green strategies with carbon trading policy. Comput. Ind. Eng. 2022, 171, 15. [Google Scholar] [CrossRef]

- Wu, D.; Yang, Y. Study on the Differential Game Model for Supply Chain with Consumers’ Low Carbon Preference. Chin. J. Manag. Sci. 2021, 29, 126–137. [Google Scholar]

- Xia, L.; Kong, Q.; Li, Y.; Xu, C. Emission Reduction and Pricing Strategies of a Low-carbon Supply Chain Considering Cross-shareholding. Chin. J. Manag. Sci. 2021, 29, 70–81. [Google Scholar]

- Ohlendorf, N.; Flachsland, C.; Nemet, G.F.; Steckel, J.C. Carbon price floors and low-carbon investment: A survey of German firms. Energy Policy 2022, 169, 113187. [Google Scholar] [CrossRef]

- Stern, N. The economics of climate change. Am. Econ. Rev. 2008, 98, 1–37. [Google Scholar] [CrossRef]

- Entezaminia, A.; Gharbi, A.; Ouhimmou, M. A joint production and carbon trading policy for unreliable manufacturing systems under cap-and-trade regulation. J. Clean. Prod. 2021, 293, 19. [Google Scholar] [CrossRef]

- De Bondt, W.F.M.; Thaler, R.H.; Thaler, R.H. Do Security Analysts Overreact? Am. Econ. Rev. 1990, 80, 52–57. [Google Scholar]

- Moore, D.A.; Healy, P.J. The trouble with overconfidence. Psychol. Rev. 2008, 115, 502–517. [Google Scholar] [CrossRef] [PubMed]

- Wan, X.; Wang, H.; Du, Y.; Meng, Q. Study on a Cross-shareholding Supply Chain Decision Considering Over-confidence. Chin. J. Manag. Sci. 2022, 30, 191–203. [Google Scholar]

- Li, M.; Petruzzi, N.C.; Zhang, J. Overconfident Competing Newsvendors. Manag. Sci. 2017, 63, 2637–2646. [Google Scholar] [CrossRef]

- Ancarani, A.; Di Mauro, C.; D’Urso, D. Measuring overconfidence in inventory management decisions. J. Purch. Supply Manag. 2016, 22, 171–180. [Google Scholar] [CrossRef]

- Du, X.J.; Zhan, H.M.; Zhu, X.X.; He, X.L. The upstream innovation with an overconfident manufacturer in a supply chain. Omega-Int. J. Manag. Sci. 2021, 105, 14. [Google Scholar] [CrossRef]

- Xu, L.; Shi, X.R.; Du, P.; Govindan, K.; Zhang, Z.C. Optimization on pricing and overconfidence problem in a duopolistic supply chain. Comput. Oper. Res. 2019, 101, 162–172. [Google Scholar] [CrossRef]

- Pu, X.; Zhuge, R. Impact of Overconfidence and Fairness Concerns on the Performance of R&D Cooperation in the Equipment Manufacturing Industry Supply Chain. J. Ind. Eng. Eng. Manag. 2017, 31, 10–15. (In Chinese) [Google Scholar]

- Xiao, Q.Z.; Chen, L.; Xie, M.; Wang, C. Optimal contract design in sustainable supply chain: Interactive impacts of fairness concern and overconfidence. J. Oper. Res. Soc. 2021, 72, 1505–1524. [Google Scholar] [CrossRef]

- Zhang, Z.; Wang, P.; Wan, M.; Guo, J.; Liu, J. Supply Chain Decisions and Coordination under the Combined Effect of Overconfidence and Fairness Concern. Complexity 2020, 2020, 3056305. [Google Scholar]

- Song, J.; Chutani, A.; Dolgui, A.; Liang, L. Dynamic innovation and pricing decisions in a supply-Chain. Omega-Int. J. Manag. Sci. 2021, 103, 24. [Google Scholar] [CrossRef]

- Zhao, D.Z.; Lv, X. Vender Managed Inventory Model Based on Overconfident Suppliers under Stochastic Demand. Syst. Eng. 2011, 29, 1–7. (In Chinese) [Google Scholar]

- Liu, Z.B.; Zhao, R.Q.; Liu, X.Y.; Chen, L. Contract designing for a supply chain with uncertain information based on confidence level. Appl. Soft. Comput. 2017, 56, 617–631. [Google Scholar] [CrossRef]

- Wang, L.L.; Wu, Y.; Hu, S.Q. Make-to-order supply chain coordination through option contract with random yields and overconfidence. Int. J. Prod. Econ. 2021, 242, 19. [Google Scholar] [CrossRef]

- Liu, J.; Zhou, H.; Wan, M.Y.; Liu, L. How Does Overconfidence Affect Decision Making of the Green Product Manufacturer? Math. Probl. Eng. 2019, 2019, 14. [Google Scholar] [CrossRef]

- Lu, X.; Shang, J.; Wu, S.Y.; Hegde, G.G.; Vargas, L.; Zhao, D.Z. Impacts of supplier hubris on inventory decisions and green manufacturing endeavors. Eur. J. Oper. Res. 2015, 245, 121–132. [Google Scholar] [CrossRef]

- Zhou, H.; Liu, L.; Jiang, W.F.; Li, S.S. Green Supply Chain Decisions and Revenue-Sharing Contracts under Manufacturers’ Overconfidence. J. Math. 2022, 2022, 11. [Google Scholar] [CrossRef]

- Handayani, D.I.; Masudin, I.; Rusdiansyah, A.; Suharsono, J. Production-Distribution Model Considering Traceability and Carbon Emission: A Case Study of the Indonesian Canned Fish Food Industry. Logistics 2021, 5, 59. [Google Scholar] [CrossRef]

- Luo, Y.J.; Li, X.Y.; Qi, X.L.; Zhao, D.Q. The impact of emission trading schemes on firm competitiveness: Evidence of the mediating effects of firm behaviors from the guangdong ETS. J. Environ. Manag. 2021, 290, 9. [Google Scholar] [CrossRef] [PubMed]

- Yang, L.; Ji, J.N.; Wang, M.Z.; Wang, Z.Z. The manufacturer’s joint decisions of channel selections and carbon emission reductions under the cap-and-trade regulation. J. Clean. Prod. 2018, 193, 506–523. [Google Scholar] [CrossRef]

- Li, Z.M.; Pan, Y.C.; Yang, W.; Ma, J.H.; Zhou, M. Effects of government subsidies on green technology investment and green marketing coordination of supply chain under the cap-and-trade mechanism. Energy Econ. 2021, 101, 14. [Google Scholar] [CrossRef]

- Xia, X.Q.; Li, C.Y.; Zhu, Q.H. Game analysis for the impact of carbon trading on low-carbon supply chain. J. Clean. Prod. 2020, 276, 12. [Google Scholar] [CrossRef]

- Xu, X.Y.; Xu, X.P.; He, P. Joint production and pricing decisions for multiple products with cap-and-trade and carbon tax regulations. J. Clean. Prod. 2016, 112, 4093–4106. [Google Scholar] [CrossRef]

- Diao, X.; Zeng, Z.; Sun, C. Research on Coordination of Supply Chain with Two Products Based on Mix Carbon Policy. Chin. J. Manag. Sci. 2021, 29, 149–159. [Google Scholar]

- Wang, X.F.; Zhu, Y.T.; Sun, H.; Jia, F. Production decisions of new and remanufactured products: Implications for low carbon emission economy. J. Clean. Prod. 2018, 171, 1225–1243. [Google Scholar] [CrossRef]

- Salcedo-Diaz, R.; Ruiz-Femenia, J.R.; Amat-Bernabeu, A.; Caballero, J.A. A cooperative game strategy for designing sustainable supply chains under the emissions trading system. J. Clean. Prod. 2021, 285, 19. [Google Scholar] [CrossRef]

- Liu, H.; Kou, X.; Xu, G.; Qiu, X.; Liu, H. Which emission reduction mode is the best under the carbon cap-and-trade mechanism? J. Clean. Prod. 2021, 314, 128053. [Google Scholar] [CrossRef]

- Wang, Y.L.; Xu, X.; Zhu, Q.H. Carbon emission reduction decisions of supply chain members under cap-and-trade regulations: A differential game analysis. Comput. Ind. Eng. 2021, 162, 18. [Google Scholar] [CrossRef]

- Gao, Y.; Xu, J.T.; Xu, H.X. A Flexible Cap-and-Trade Policy and Limited Demand Information Effects on a Sustainable Supply Chain. Sustainability 2021, 13, 23. [Google Scholar] [CrossRef]

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Author(s) | Focus Point | Overconfidence | Carbon Trading | Methods |

|---|---|---|---|---|

| Xu, X et al. [38] | Production, price | × | √ | Stackelberg game model |

| Wan, X et al. [35] | Profit | √ | × | Stackelberg game model |

| Zhou, H et al. [42] | Revenue-sharing, R&D | √ | × | Stackelberg game model |

| Yang, L et al. [51] | Channel selections | × | √ | Stackelberg game model |

| Wu, D et al. [28] | Emission reduction | × | √ | Differential game model |

| Xu, L et al. [39] | Price | √ | × | Game model |

| Lu, X et al. [41] | Emission reduction, Inventory optimization | √ | × | VMI model |

| Liu, J et al. [40] | Production, R&D | √ | × | Newsboy model |

| Hasan et al. [25] | Inventory optimization | × | √ | EOQ model |

| Our model | Emission reduction | √ | √ | Stackelberg game model |

| Symbol | Meaning |

|---|---|

| Selling price of products | |

| Wholesale price of products | |

| Actual market demand for the product | |

| Overconfidence in the market demand as perceived by the manufacturer | |

| Manufacturer’s initial carbon emissions per unit of product | |

| Carbon quota per unit of product allocated by the government to manufacturers | |

| Unit product carbon trading price | |

| Manufacturer product reduction rate | |

| Manufacturer carbon reduction cost factor | |

| Consumer sensitivity to product reduction rate | |

| Manufacturer overconfidence factor | |

| Retailer profit | |

| Manufacturer profit | |

| Overconfidence in manufacturer’s expected profits |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2022 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Yu, J.; Sun, L. Supply Chain Emission Reduction Decisions, Considering Overconfidence under Conditions of Carbon Trading Price Volatility. Sustainability 2022, 14, 15432. https://doi.org/10.3390/su142215432

Yu J, Sun L. Supply Chain Emission Reduction Decisions, Considering Overconfidence under Conditions of Carbon Trading Price Volatility. Sustainability. 2022; 14(22):15432. https://doi.org/10.3390/su142215432

Chicago/Turabian StyleYu, Jinhan, and Licheng Sun. 2022. "Supply Chain Emission Reduction Decisions, Considering Overconfidence under Conditions of Carbon Trading Price Volatility" Sustainability 14, no. 22: 15432. https://doi.org/10.3390/su142215432

APA StyleYu, J., & Sun, L. (2022). Supply Chain Emission Reduction Decisions, Considering Overconfidence under Conditions of Carbon Trading Price Volatility. Sustainability, 14(22), 15432. https://doi.org/10.3390/su142215432