Challenges and How to Overcome Them in the Formulation and Implementation Process of a Sustainability Balanced Scorecard (SBSC)

Abstract

1. Introduction

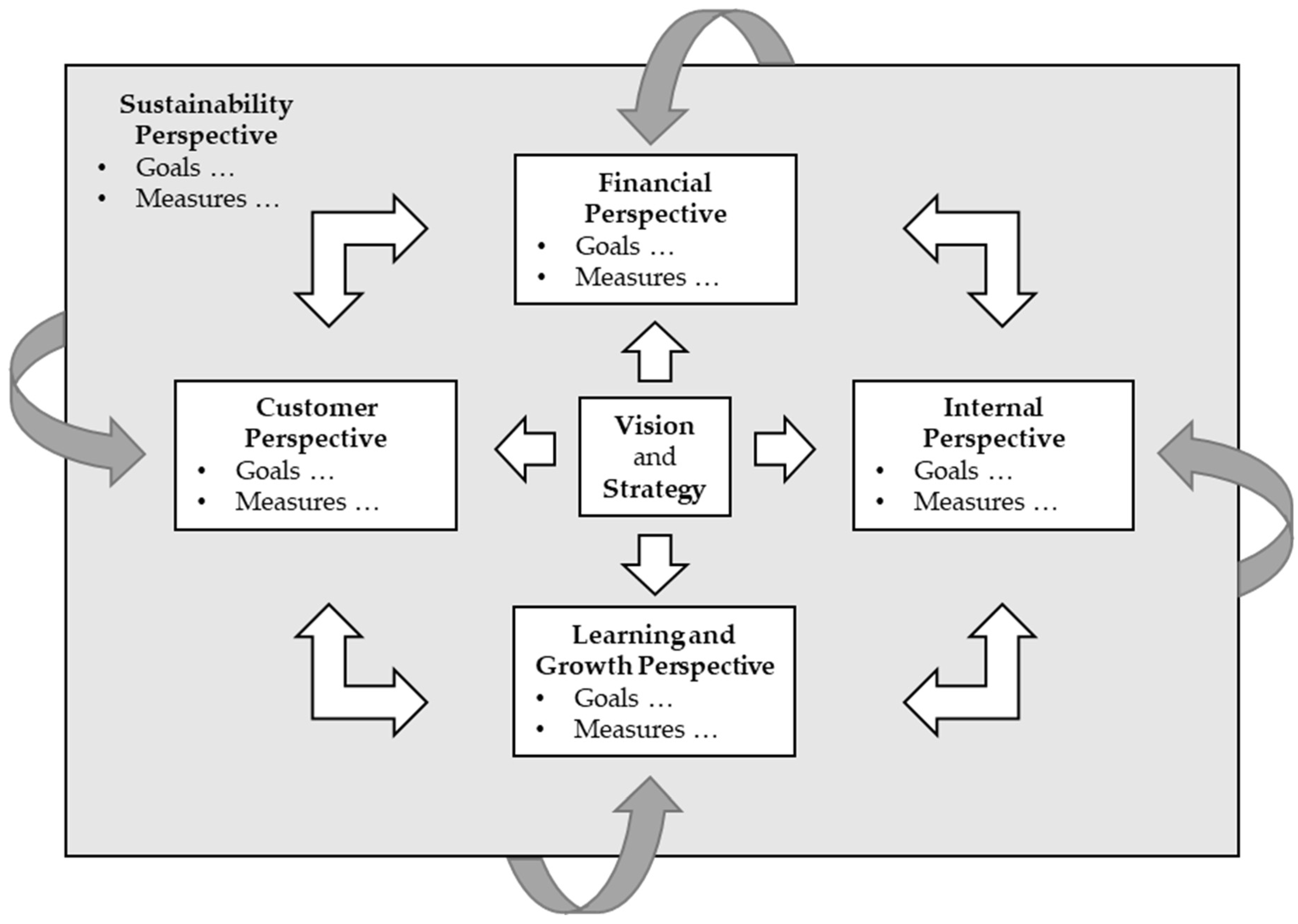

2. Theoretical Foundations of the SBSC

2.1. The BSC and the SBSC

2.2. The Integrative, the Extended and the Derived SBSC

3. Challenges with Formulating and Implementing a Sustainable Strategy for SBSC

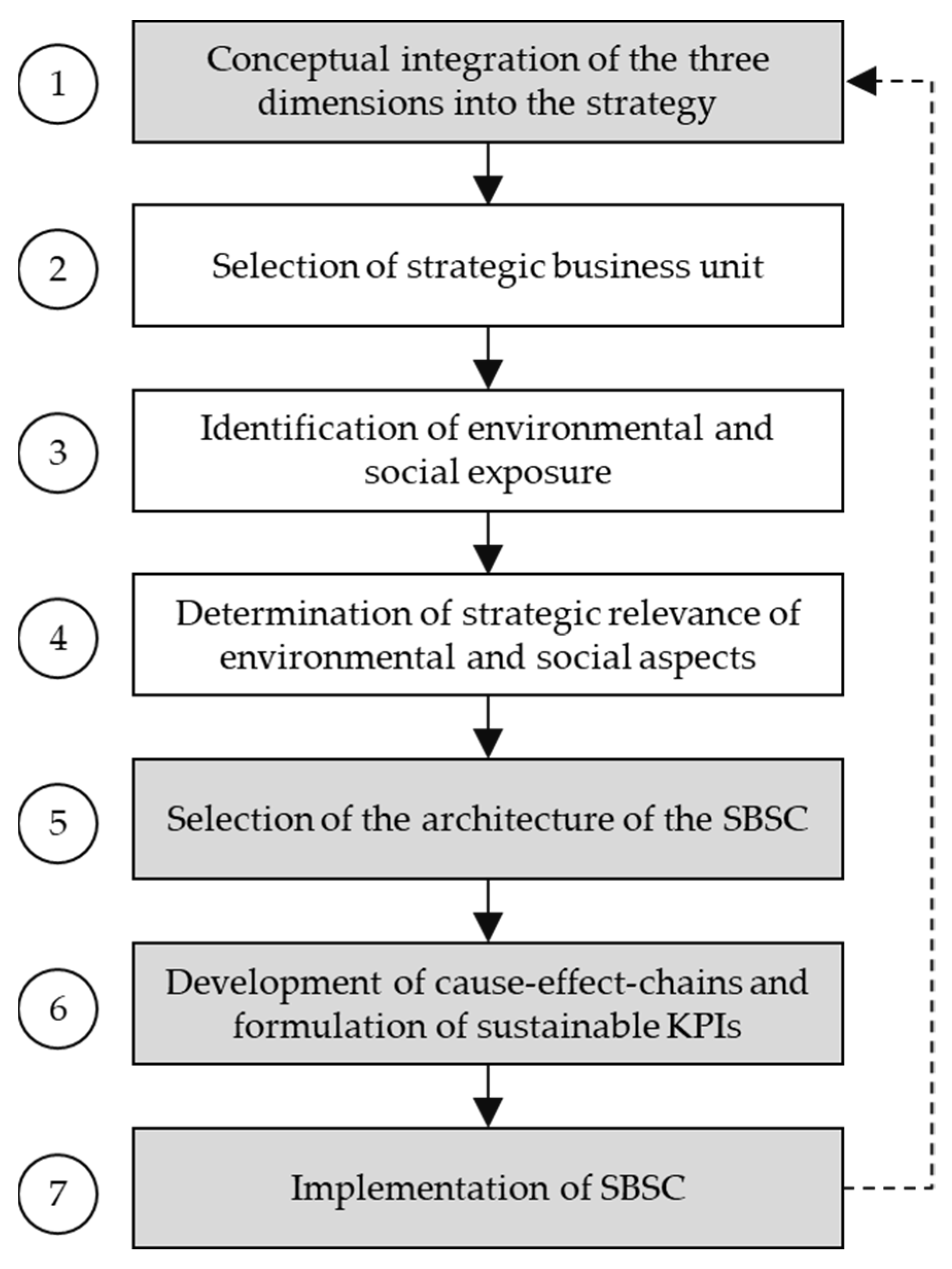

3.1. The Process of Formulating and Implementing an SBSC

3.2. Conceptual Integration of the Three Dimensions into the Strategy

3.3. Selection of the Architecture of the SBSC

3.4. Development of Cause-Effect Chains and Formulation of Sustainable KPIs

3.5. Implementation of SBSC

4. Improving the Process of Formulating and Implementing an SBSC

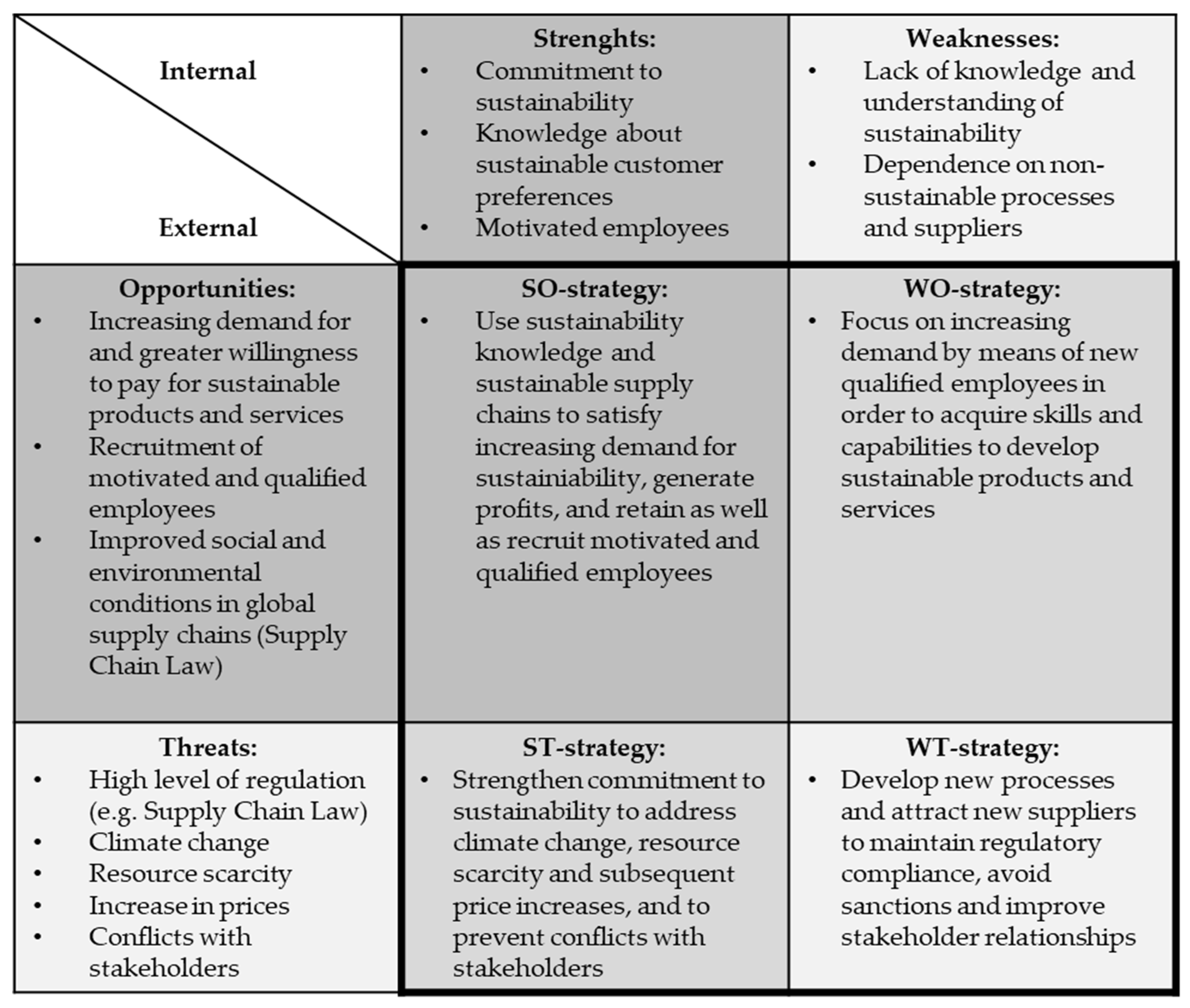

4.1. Techniques for Developing a Sustainable Strategy

4.2. Criteria for the Selection of a Suitable Architecture

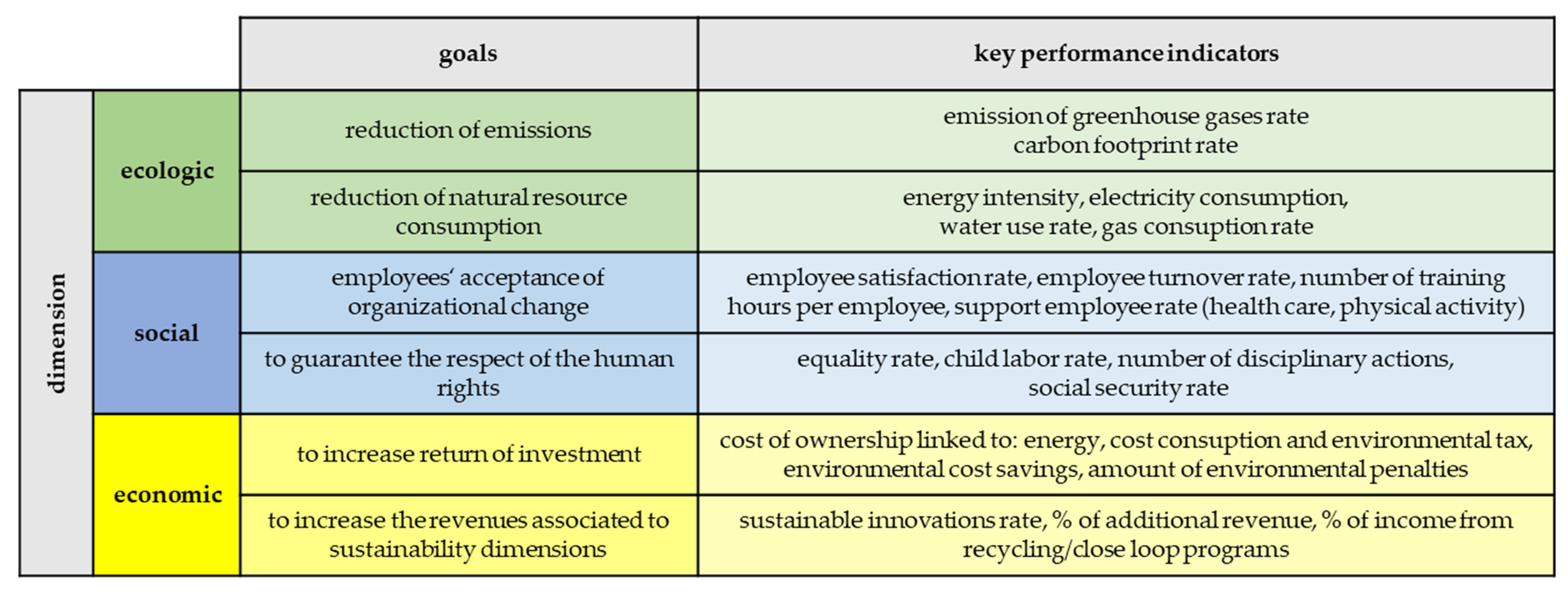

4.3. Guidelines for the Development of Cause-Effect Chains and the Formulation of Sustainable KPIs

4.4. Building Blocks of a Successful Implementation of an SBSC

5. Conclusions

6. Implications for Research and Practice

6.1. Implications for Researchers

6.2. Implications for Practitioners

6.3. Implications for Policy Makers

Author Contributions

Funding

Conflicts of Interest

References

- Meuer, J.; Koelbel, J.; Hoffmann, V.H. On the Nature of Corporate Sustainability. Organ. Environ. 2020, 33, 319–341. [Google Scholar] [CrossRef]

- Rudyanto, A.; Siregar, V.S. The effect of stakeholder pressure and corporate governance on the sustainability report quality. Int. J. Ethics Syst. 2018, 34, 233–249. [Google Scholar] [CrossRef]

- Ashrafi, M.; Adams, M.; Walker, T.R.; Magnan, G. How corporate social responsibility can be integrated into corporate sustainability: A theoretical review of their relationships. Int. J. Sustain. Dev. World Ecol. 2018, 25, 672–682. [Google Scholar] [CrossRef]

- Journeault, M. The Integrated Scorecard in support of corporate sustainability strategies. J. Environ. Manag. 2016, 182, 214–229. [Google Scholar] [CrossRef] [PubMed]

- Linnenluecke, M.K.; Griffiths, A. Corporate sustainability and organizational culture. J. World Bus. 2010, 45, 357–366. [Google Scholar] [CrossRef]

- Kropp, A. Grundlagen der Nachhaltigen Entwicklung: Handlungsmöglichkeiten und Strategien zur Umsetzung; Springer Gabler: Wiesbaden, Germany, 2019; ISBN 9783658230722. [Google Scholar]

- Purvis, B.; Mao, Y.; Robinson, D. Three pillars of sustainability: In search of conceptual origins. Sustain. Sci. 2019, 14, 681–695. [Google Scholar] [CrossRef]

- Dyllick, T.; Hockerts, K. Beyond the business case for corporate sustainability. Bus. Strategy Environ. 2002, 11, 130–141. [Google Scholar] [CrossRef]

- Sands, J.S.; Rae, K.N.; Gadenne, D. An empirical investigation on the links within a sustainability balanced scorecard (SBSC) framework and their impact on financial performance. ARJ 2016, 29, 154–178. [Google Scholar] [CrossRef]

- Hristov, I.; Chirico, A.; Appolloni, A. Sustainability Value Creation, Survival, and Growth of the Company: A Critical Perspective in the Sustainability Balanced Scorecard (SBSC). Sustainability 2019, 11, 2119. [Google Scholar] [CrossRef]

- Hansen, E.G.; Schaltegger, S. The Sustainability Balanced Scorecard: A Systematic Review of Architectures. J. Bus. Ethics 2016, 133, 193–221. [Google Scholar] [CrossRef]

- Nikolaou, I.E.; Tsalis, T.A. Development of a sustainable balanced scorecard framework. Ecol. Indic. 2013, 34, 76–86. [Google Scholar] [CrossRef]

- Gminder, C.U.; Bieker, T.; Hahn, T.; Wagner, M. Nachhaltig managen mit der Balanced Scorecard. ÖW 2002, 17, 27–29. [Google Scholar] [CrossRef][Green Version]

- Tsalis, T.A.; Nikolaou, I.E.; Grigoroudis, E.; Tsagarakis, K.P. A framework development to evaluate the needs of SMEs in order to adopt a sustainability-balanced scorecard. J. Integr. Environ. Sci. 2013, 10, 179–197. [Google Scholar] [CrossRef]

- Chaker, F.; Idrissi, M.A.J.; El Manouar, A. A critical evaluation of the sustainability balanced scorecard as a decision aid framework. Int. J. Appl. Eng. Res. 2017, 12, 4221–4237. [Google Scholar]

- Jaakkola, E. Designing conceptual articles: Four approaches. AMS Rev. 2020, 10, 18–26. [Google Scholar] [CrossRef]

- MacInnis, D.J. A Framework for Conceptual Contributions in Marketing. J. Mark. 2011, 75, 136–154. [Google Scholar] [CrossRef]

- Hörisch, J.; Schaltegger, S.; Freeman, R.E. Integrating stakeholder theory and sustainability accounting: A conceptual synthesis. J. Clean. Prod. 2020, 275, 124097. [Google Scholar] [CrossRef]

- Mihalic, T. Conceptualising overtourism: A sustainability approach. Ann. Tour. Res. 2020, 84, 103025. [Google Scholar] [CrossRef]

- Kaplan, R.S.; Norton, D.P. The balanced scorecard—Measures that drive performance. Harv. Bus. Rev. 1992, 70, 71–79. [Google Scholar]

- Hahn, T.; Wagner, M. Sustainability Balanced Scorecard: Von der Theorie zur Umsetzung. 2001. Available online: https://scholar.google.de/citations?user=jjcym74aaaaj&hl=de&oi=sra (accessed on 19 October 2022).

- Kaplan, R.S.; Norton, D.P. The Balanced Scorecard—Translating Strategy into Action; Harvard Business Review Press: Boston, MA, USA, 1996. [Google Scholar]

- Matlachowsky, P. Implementierungsstand der Balanced Scorecard: Fallstudienbasierte Analyse in Deutschen Unternehmen; Gabler: Wiesbaden, Germany, 2009; ISBN 9783834999306. [Google Scholar]

- Figge, F.; Hahn, T.; Schaltegger, S.; Wagner, M. The Sustainability Balanced Scorecard—Linking sustainability management to business strategy. Bus. Strat. Environ. 2002, 11, 269–284. [Google Scholar] [CrossRef]

- Epstein, M.J.; Wisner, P.S. Using a Balanced Scorecard to Implement Sustainability. Environ. Qual. Manag. 2001, 11, 1–10. [Google Scholar] [CrossRef]

- Asiaei, K.; Bontis, N. Using a balanced scorecard to manage corporate social responsibility. Knowl. Process Manag. 2019, 26, 371–379. [Google Scholar] [CrossRef]

- Figge, F.; Hahn, T.; Schaltegger, S.; Wagner, M. Sustainability Balanced Scorecard. Wertorientiertes Nachhaltigkeitsmanagement mit der Balanced Scorecard. Available online: http://pure.leuphana.de/ws/files/1127098/figge_hahn_schaltegger_wagner_sustainability_balanced_scorecard.pdf (accessed on 19 October 2022).

- Arnold, W.; Freimann, J.; Kurz, R. Sustainable Balanced Scorecard (SBS): Integration von Nachhaltigkeitsaspekten in das BSC-Konzept. Control. Manag. 2003, 47, 391–401. [Google Scholar] [CrossRef]

- Schaltegger, S. Sustainability Balanced Scorecard. Unternehmerische Steuerung von Nachhaltigkeitsaspekten. Controlling 2004, 16, 511–516. [Google Scholar] [CrossRef][Green Version]

- Schaltegger, S.; Lüdeke-Freund, F. The Sustainability Balanced Scorecard: Concept and the Case of Hamburg Airport (December 16, 2011). Centre for Sustainability Management (CSM), Leuphana Universität Lüneburg. 2011. Available online: https://ssrn.com/abstract=2062320 (accessed on 19 October 2022). [CrossRef]

- Görg, H.; Hanley, A.; Heidbrink, L.; Hoffmann, S.; Requate, T. Ein Lieferkettengesetz für Deutschland? KCG Policy Paper No. 7. 2021. Available online: https://www.econstor.eu/handle/10419/231361 (accessed on 19 October 2022).

- Kalender, Z.T.; Vayvay, Ö. The Fifth Pillar of the Balanced Scorecard: Sustainability. Procedia Soc. Behav. Sci. 2016, 235, 76–83. [Google Scholar] [CrossRef]

- Kaplan, R.S.; Norton, D.P. Strategic learning & the balanced scorecard. Strategy Leadersh. 1996, 24, 18–24. [Google Scholar]

- Jassem, S.; Zakaria, Z.; Che Azmi, A. Sustainability Balanced Scorecard Architecture and Environmental Investment Decision-Making. Found. Manag. 2020, 12, 193–210. [Google Scholar] [CrossRef]

- Kaplan, R.S.; Norton, D.P. The Strategy-Focused Organization: How Balanced Scorecard Companies Thrive in the New Business Environment, 9th ed.; Harvard Business School Press: Boston, MA, USA, 2001; ISBN 9781578512508. [Google Scholar]

- Krstić, B.; Sekulić, V.; Ivanović, V. How to Apply the Sustainability Balanced Scorecard Concept. Econ. Themes 2015, 52, 65–80. [Google Scholar] [CrossRef]

- Kaptein, M.; Wempe, J. Sustainability management: Balancing conflicting economic, environmental and social corporate responsibilities. J. Corp. Citizsh. 2001, 2, 91–106. [Google Scholar]

- Bieker, T. Sustainability Management with the Balanced Scorecard; Profil: Munich, Germany, 2005. [Google Scholar]

- Butler, J.B.; Henderson, S.C.; Raiborn, C. Sustainability and the balanced scorecard: Integrating green measures into business reporting. Manag. Account. Q. 2011, 12, 1–10. [Google Scholar]

- Hahn, T.; Figge, F. Why Architecture Does Not Matter: On the Fallacy of Sustainability Balanced Scorecards. J. Bus. Ethics 2018, 150, 919–935. [Google Scholar] [CrossRef]

- León-Soriano, R.; Muñoz-Torres, M.J.; Chalmeta-Rosaleñ, R. Methodology for sustainability strategic planning and management. Ind. Manag. Data Syst. 2010, 110, 249–268. [Google Scholar] [CrossRef]

- Jassem, S.; Azmi, A.; Zakaria, Z. Impact of Sustainability Balanced Scorecard Types on Environmental Investment Decision-Making. Sustainability 2018, 10, 541. [Google Scholar] [CrossRef]

- Kaufmann, L.; Becker, A. Overcoming the Barriers During Implementation and Use of the Balanced Scorecard by Multinational Companies in Brazil. Lat. Am. Bus. Rev. 2006, 6, 39–62. [Google Scholar] [CrossRef]

- Chaker, F.; El Manouar, A.; Idrissi, M.A.J. The dynamic adaptive sustainability balanced scorecard: A new framework for a sustainability-driven strategy. Int. J. Appl. Eng. Res. 2017, 12, 6182–6191. [Google Scholar]

- Hansen, E.G.; Schaltegger, S. Sustainability Balanced Scorecards and their Architectures: Irrelevant or Misunderstood? J. Bus. Ethics 2018, 150, 937–952. [Google Scholar] [CrossRef]

- Schneiderman, A.M. Why balanced scorecards fail. J. Strateg. Perform. Meas. 1999, 3, 6–11. [Google Scholar]

- Möller, A.; Schaltegger, S. The Sustainability Balanced Scorecard as a Framework for Eco-efficiency Analysis. J. Ind. Ecol. 2005, 9, 73–83. [Google Scholar] [CrossRef]

- Sattler, W.; Wange, A. Controlling der Nachhaltigkeit. Ethik im Mittelstand; Springer Gabler: Wiesbaden, Germany, 2016; pp. 271–283. [Google Scholar]

- Qorri, A.; Mujkić, Z.; Kraslawski, A. A conceptual framework for measuring sustainability performance of supply chains. J. Clean. Prod. 2018, 189, 570–584. [Google Scholar] [CrossRef]

- Rompho, N. Why the Balanced Scorecard Fails in SMEs: A Case Study. IJBM 2011, 6, 39–46. [Google Scholar] [CrossRef]

- Falle, S.; Rauter, R.; Engert, S.; Baumgartner, R. Sustainability Management with the Sustainability Balanced Scorecard in SMEs: Findings from an Austrian Case Study. Sustainability 2016, 8, 545. [Google Scholar] [CrossRef]

- Fuertes, G.; Alfaro, M.; Vargas, M.; Gutierrez, S.; Ternero, R.; Sabattin, J. Conceptual Framework for the Strategic Management: A Literature Review—Descriptive. J. Eng. 2020, 2020, 6253013. [Google Scholar] [CrossRef]

- Hristov, I.; Chirico, A. The Role of Sustainability Key Performance Indicators (KPIs) in Implementing Sustainable Strategies. Sustainability 2019, 11, 5742. [Google Scholar] [CrossRef]

- Julmi, C. When rational decision-making becomes irrational: A critical assessment and re-conceptualization of intuition effectiveness. Bus. Res. 2019, 12, 291–314. [Google Scholar] [CrossRef]

- Dias-Sardinha, I.; Reijnders, L.; Antunes, P. From environmental performance evaluation to eco-efficiency and sustainability balanced scorecards. Environ. Qual. Manag. 2002, 12, 51–64. [Google Scholar] [CrossRef]

- Colsmann, B. Nachhaltigkeitscontrolling: Strategien, Ziele, Umsetzung, 2nd ed.; Springer Gabler: Wiesbaden, Germany, 2016. [Google Scholar]

- Bieker, T. Managing corporate sustainability with the balanced scorecard: Developing a balanced scorecard for integrity management. Business 2002. [Google Scholar]

- Lee, S.F.; Sai On Ko, A. Building balanced scorecard with SWOT analysis, and implementing “Sun Tzu’s The Art of Business Management Strategies” on QFD methodology. Manag. Audit. J. 2000, 15, 68–76. [Google Scholar] [CrossRef]

- Ip, Y.K.; Koo, L.C. BSQ strategic formulation framework. Manag. Audit. J. 2004, 19, 533–543. [Google Scholar] [CrossRef]

- Fresner, J.; Engelhardt, G.; Nussbaumer, R.; Grabher, A.; Kumpf, A. Sustainability Balanced Scorecard im Nachhaltigkeitsbereich (ÖKOPROFIT): Bericht aus Energie- und Umweltforschung 28/2006; Bundesministerium für Verkehr, Innovation und Technologie: Wien, Austria, 2006. [Google Scholar]

- Koo, L.C.; Koo, H. Holistic approach for diagnosing, prioritising, implementing and monitoring effective strategies through synergetic fusion of SWOT, Balanced Scorecard and QFD. WREMSD 2007, 3, 62. [Google Scholar] [CrossRef]

- Koo, L.C.; Koo, H.; Luk, L. A pragmatic and holistic approach to strategic formulation through adopting balanced scorecard, SWOT analysis and blue ocean strategy—A case study of a consumer product manufacturer in China. Int. J. Manag. Financ. Account. 2008, 1, 127–146. [Google Scholar] [CrossRef]

- Manteghi, N.; Zohrabi, A. A proposed comprehensive framework for formulating strategy: A Hybrid of balanced scorecard, SWOT analysis, porter‘s generic strategies and Fuzzy quality function deployment. Procedia Soc. Behav. Sci. 2011, 15, 2068–2073. [Google Scholar] [CrossRef]

- Gurel, B.; Sari, I.U. Strategic Planning for Sustainability in a Start-Up Company: A Case Study on Human Resources Consulting Firm. EJSD 2015, 4, 313–322. [Google Scholar] [CrossRef]

- Shields, J.; Shelleman, J.M. Integrating Sustainability into SME Strategy. J. Small Bus. Strategy 2015, 25, 59–78. [Google Scholar]

- Pereira, L.; Pinto, M.; Da Costa, R.L.; Dias, Á.; Gonçalves, R. The New SWOT for a Sustainable World. JOItmC 2021, 7, 18. [Google Scholar] [CrossRef]

- Unrein, D. Die SWOT-Analyse. WIST 2013, 42, 516–519. [Google Scholar] [CrossRef]

- Sullivan, L.P. Quality Function Deployment. Qual. Prog. (ASQC) 1986, 19, 39–50. [Google Scholar]

- Chan, L.-K.; Wu, M.-L. Quality function deployment: A literature review. Eur. J. Oper. Res. 2002, 143, 463–497. [Google Scholar] [CrossRef]

- Baumgartner, R. Tools for Sustainable Business Management. WIT Trans. Ecol. Environ. 2003, 63, 187–196. [Google Scholar] [CrossRef]

- Dror, S. The Balanced Scorecard versus quality award models as strategic frameworks. Total Qual. Manag. Bus. Excell. 2008, 19, 583–593. [Google Scholar] [CrossRef]

- Aragón-Correa, J.A.; Hurtado-Torres, N.; Sharma, S.; García-Morales, V.J. Environmental strategy and performance in small firms: A resource-based perspective. J. Environ. Manag. 2008, 86, 88–103. [Google Scholar] [CrossRef]

- Jassem, S.; Zakaria, Z.; Che Azmi, A. Sustainability balanced scorecard architecture and environmental performance outcomes: A systematic review. IJPPM 2022, 71, 1728–1760. [Google Scholar] [CrossRef]

- Medel, F.; García, L.; Enriquez, S.; Anido, M. Reporting Models for Corporate Sustainability in SMEs. In Information Technologies in Environmental Engineering; Springer: Berlin/Heidelberg, Germany, 2011; pp. 407–418. [Google Scholar]

- Schaltegger, S.; Wagner, M. Managing Sustainability Performance Measurement and Reporting in an Integrated Manner. Sustainability Accounting as the Link between the Sustainability Balanced Scorecard and Sustainability Reporting. In Sustainability Accounting and Reporting; Schaltegger, S., Bennett, M., Burritt, R., Eds.; Springer: Dordrecht, The Netherlands, 2006; pp. 681–697. ISBN 978-1-4020-4079-5. [Google Scholar]

- EMAS. Umwelt Nachhaltig Nutzen, Effizienz Steigern: EMAS, das Gütesiegel der Europäischen Union. Available online: https://www.emas.de/was-ist-emas (accessed on 19 October 2022).

- Sidiropoulos, M.; Mouzakitis, Y.; Abamides, E.; Goutsos, S. Applying sustainable indicators to corporate strategy: The eco-balanced scorecard. Environ. Res. Eng. Manag. 2004, 27, 28–33. [Google Scholar]

- Dal-Bianco, E. Nachhaltigkeit messbar machen—Integration von ISO 26000 in die Sustainability Balanced Scorecard. In Corporate Social Responsibility; Schneider, A., Schmidpeter, R., Eds.; Springer: Berlin/Heidelberg, Germany, 2015; pp. 311–323. ISBN 978-3-662-43482-6. [Google Scholar]

- Yemeshvary Ashok Upadhyay, A.; Palo, S. Engaging employees through balanced scorecard implementation. Strateg. HR Rev. 2013, 12, 302–307. [Google Scholar] [CrossRef]

- Massingham, R.; Massingham, P.R.; Dumay, J. Improving integrated reporting. JIC 2019, 20, 60–82. [Google Scholar] [CrossRef]

- Hristov, I.; Appolloni, A.; Chirico, A. The adoption of the key performance indicators to integrate sustainability in the business strategy: A novel five-dimensional framework. Bus. Strat. Environ. 2022, 31, 3216–3230. [Google Scholar] [CrossRef]

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Sustainability Dimension | Financial Perspective | Customer Perspective | Internal Perspective | Learning and Growth Perspective |

|---|---|---|---|---|

| Economy | Return on Investment | Customer Satisfaction | Productivity | Innovation capability |

| Ecology | Investments in environmental protection | Recycling | Energy and resource efficiency | Eco-improvement suggestions |

| Social | Voluntary social benefits | Product safety | Improvement of working conditions | Qualifications |

| Process Step | Challenge | Description | Sources |

|---|---|---|---|

| Conceptual integration of the three dimensions into the strategy | Addressing conflicting goals | There are conflicting goals between both the three dimensions of sustainability and different stakeholder groups that have to be addressed. | Epstein and Wisner [25]; Kaptein and Wempe [37]; Bieker [38]; Butler et al. [39]; Hahn and Figge [40] |

| Understanding the contributions of the social and environmental dimensions to the company’s financial performance | Companies need to link social or ecological management systems to general management and therefore have to understand their contribution to the economic success. | Epstein and Wisner [25]; Figge et al. [24]; Bieker [38]; León-Soriano et al. [41]; Tsalis et al. [14]; Hristov et al. [10] | |

| Formulating an actionable strategy | If a strategy is not linked to the goals as well as the resources of a company, it becomes a barrier to successful SBSC implementation. | Kaplan and Norton [22]; León-Soriano et al. [41]; Hristov et al. [10] | |

| Selection of the architecture of the SBSC | Choosing between the integrative and extended SBSC | Since there is no consensus in the literature that either the integrative or the extended SBSC is generally superior, companies must choose the architecture that best fits their needs, characteristics and resources. | Epstein and Wisner [25]; Figge et al. [27]; Hahn and Wagner [21]; Figge et al. [24]; Hansen and Schaltegger [11]; Journeault [4]; Jassem et al. [42]; Jassem et al. [34] |

| Deciding whether to add a derived scorecard or not | After the company has decided on either the integrative or the extended SBSC, it must be further decided whether the SBSC should be extended by a derived SBSC. | Figge et al. [27]; Hahn and Wagner [21]; Figge et al. [24]; Journeault [4]; Kalender and Vayvay [32] | |

| Development of cause-effect chains and formulation of sustainable KPIs | Identifying cause-effect chains and connecting them with KPIs | The identification of the cause-effect chains and their connection with KPIs is a highly unstructured process fraught with the risks of reality distortions and lack of implementability. | Kaufmann and Becker [43]; Chaker et al. [15], Chaker et al. [44]; Hahn and Figge [40]; Hansen and Schaltegger [45] |

| Aligning KPIs with the company’s strategy | Even though KPIs may be easily controllable and measurable, they may not reflect the company’s strategy in a sufficient way. | Kaplan and Norton [22]; Schneiderman [46]; Möller and Schaltegger [47]; Kaufmann and Becker [43]; Schaltegger and Lüdeke-Freund [30]; Nikolaou and Tsalis [12]; Tsalis et al. [14]; Sattler and Wange [48]; Qorri et al. [49]; Hristov et al. [10] | |

| Implementation of SBSC | Involving employees to ensure commitment and to reduce mistrust | The implementation of the SBSC may cause distrust and resistance to change, which is why employees need to get involved and accept the instrument. | Bieker [38]; Kaufmann and Becker [43]; Rompho [50]; Nikolaou and Tsalis [12]; Tsalis et al. [14]; Falle et al. [51]; Hristov et al. [10] |

| Communicating the sustainability performance with key stakeholders | The SBSC needs to be connected to the sustainability reporting of a company and satisfy the stakeholder’s diverse need for information. | Bieker [12]; Schaltegger and Lüdeke-Freund [30]; Journault [4] | |

| Enhancing organizational learning and development | The BSC provides feedback about the strategy that needs to be integrated in the processes of organizational learning in order to continuously adapt the strategy. | Kaplan and Norton [33]; Epstein and Wisner [25]; Kaplan and Norton [35]; Hansen and Schaltegger [11] |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2022 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Eifert, A.; Julmi, C. Challenges and How to Overcome Them in the Formulation and Implementation Process of a Sustainability Balanced Scorecard (SBSC). Sustainability 2022, 14, 14816. https://doi.org/10.3390/su142214816

Eifert A, Julmi C. Challenges and How to Overcome Them in the Formulation and Implementation Process of a Sustainability Balanced Scorecard (SBSC). Sustainability. 2022; 14(22):14816. https://doi.org/10.3390/su142214816

Chicago/Turabian StyleEifert, Anna, and Christian Julmi. 2022. "Challenges and How to Overcome Them in the Formulation and Implementation Process of a Sustainability Balanced Scorecard (SBSC)" Sustainability 14, no. 22: 14816. https://doi.org/10.3390/su142214816

APA StyleEifert, A., & Julmi, C. (2022). Challenges and How to Overcome Them in the Formulation and Implementation Process of a Sustainability Balanced Scorecard (SBSC). Sustainability, 14(22), 14816. https://doi.org/10.3390/su142214816