Green GDP Indicator with Application to Life Cycle of Sugar Industry in Thailand

Abstract

:1. Introduction

1.1. Green GDP Evaluation Background

1.1.1. A Perform in the Global Green Economy

1.1.2. Thailand’s Green GDP Research

1.1.3. Towards Integration of Green GDP and Circular Economy

2. Materials and Methods

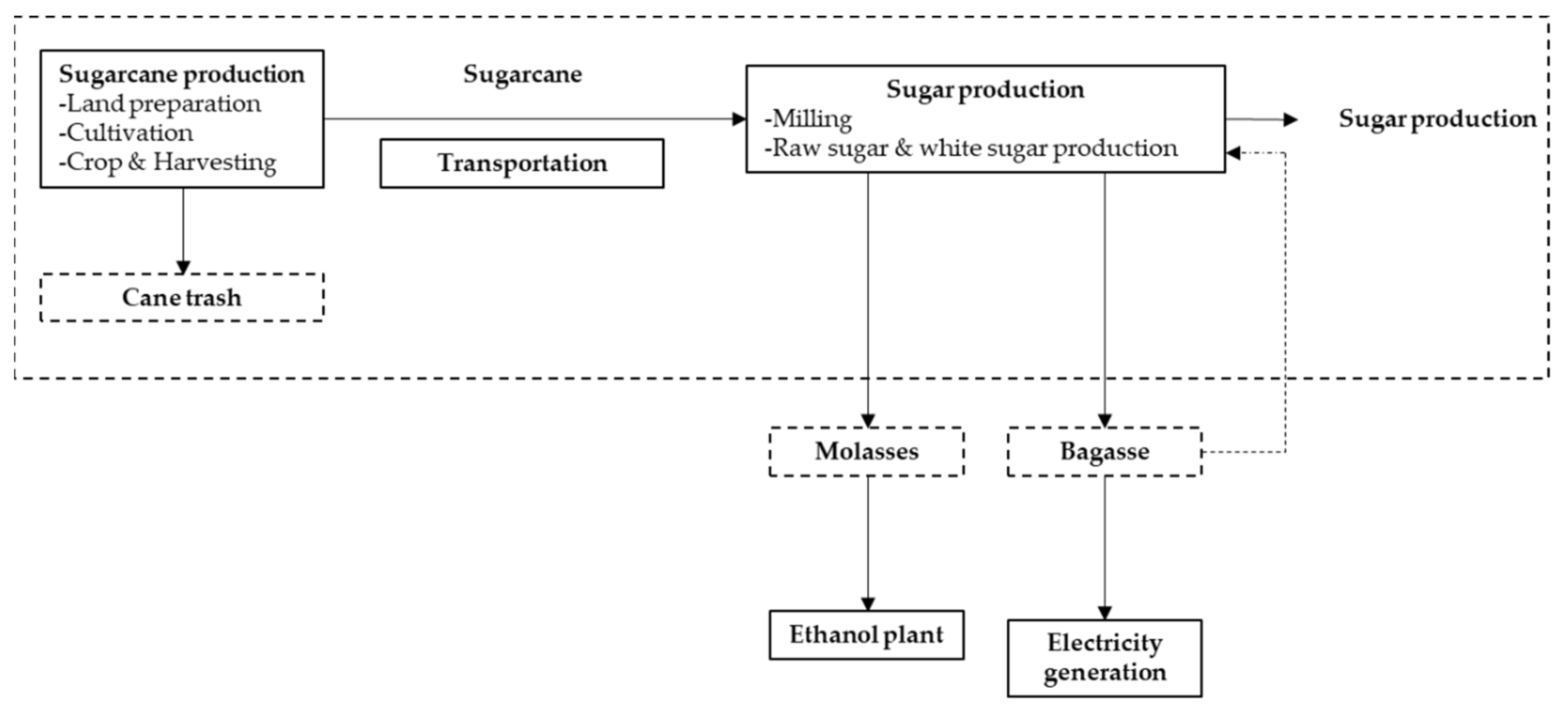

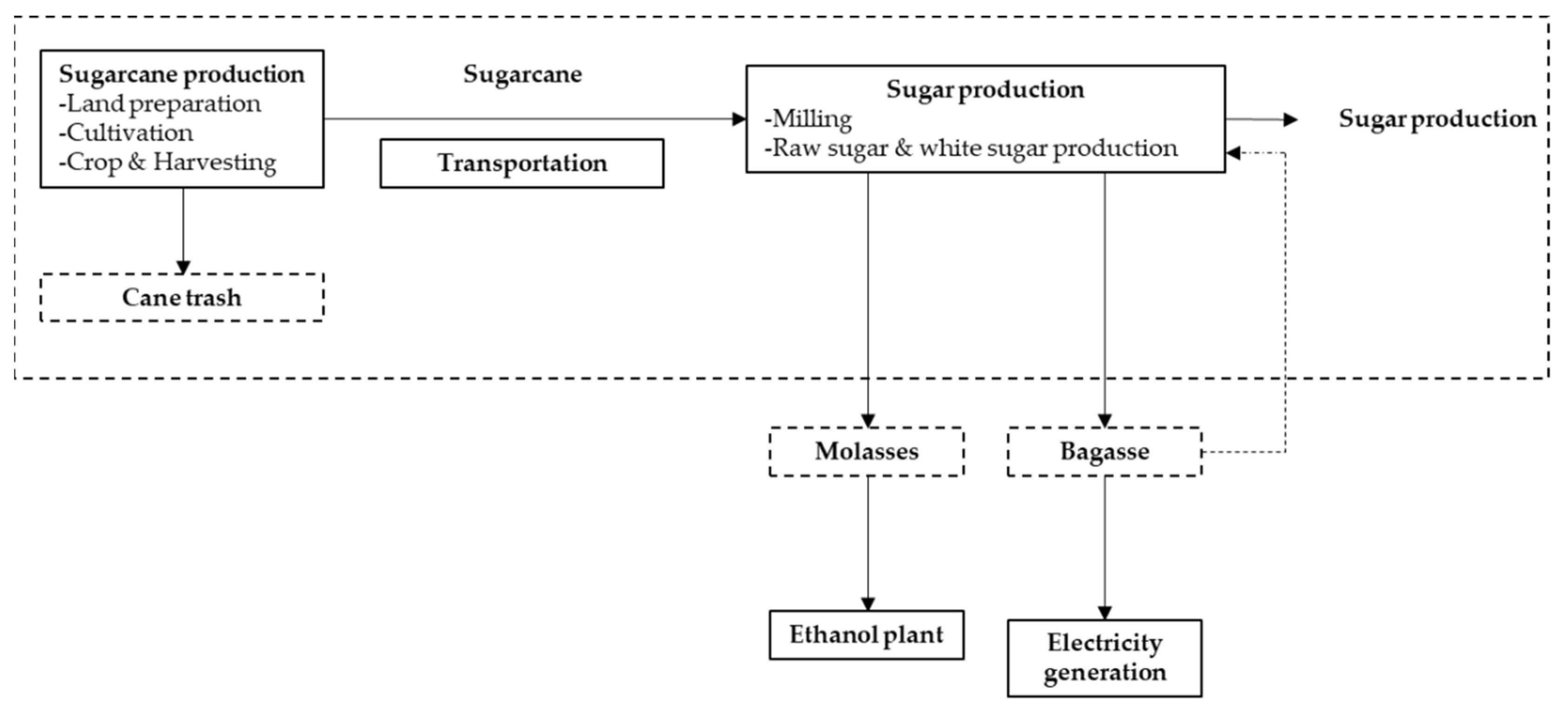

2.1. Functional Unit and System Boundary

2.2. Data Sources and Analysis

2.3. Sugar Production in Thailand

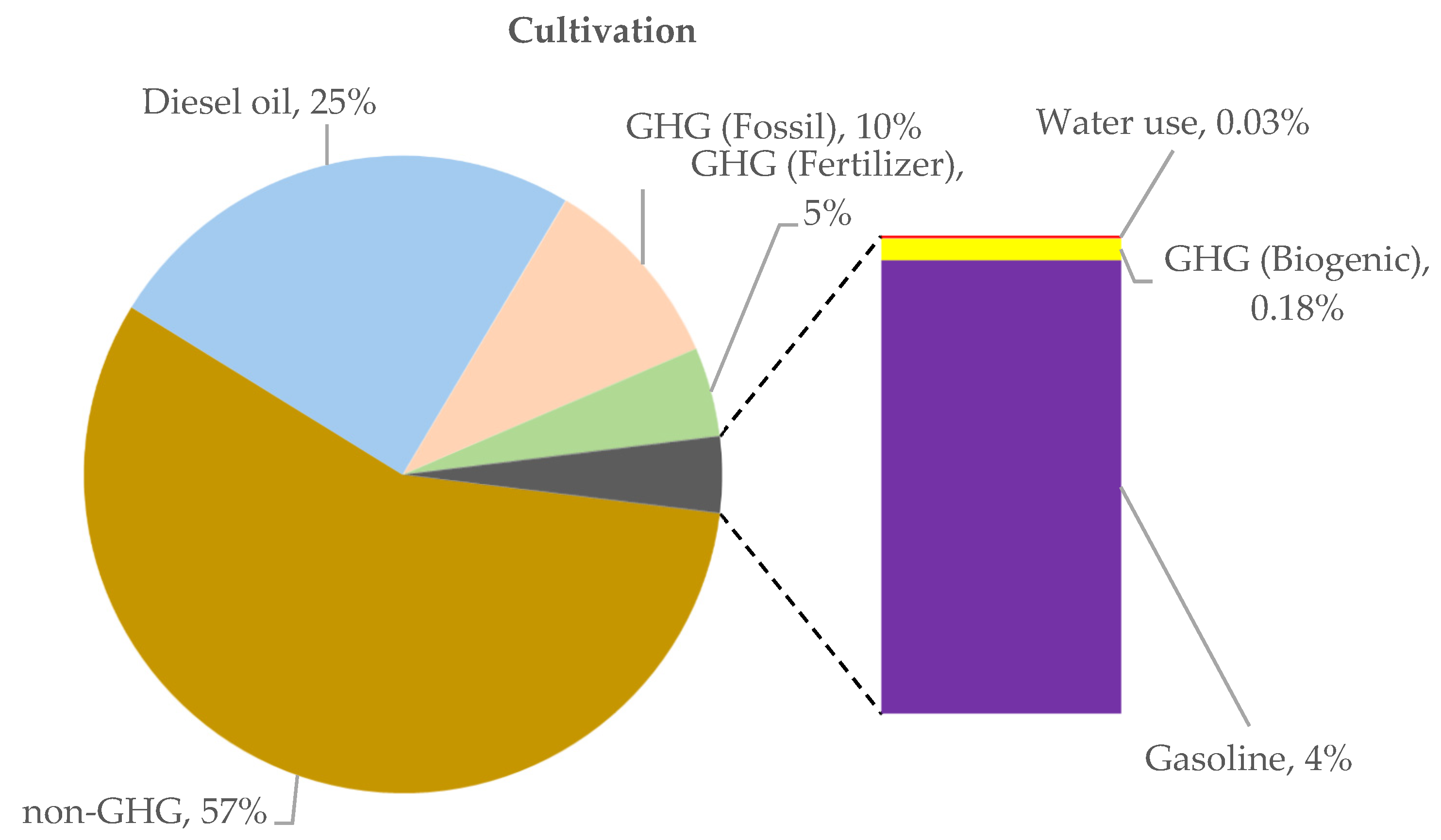

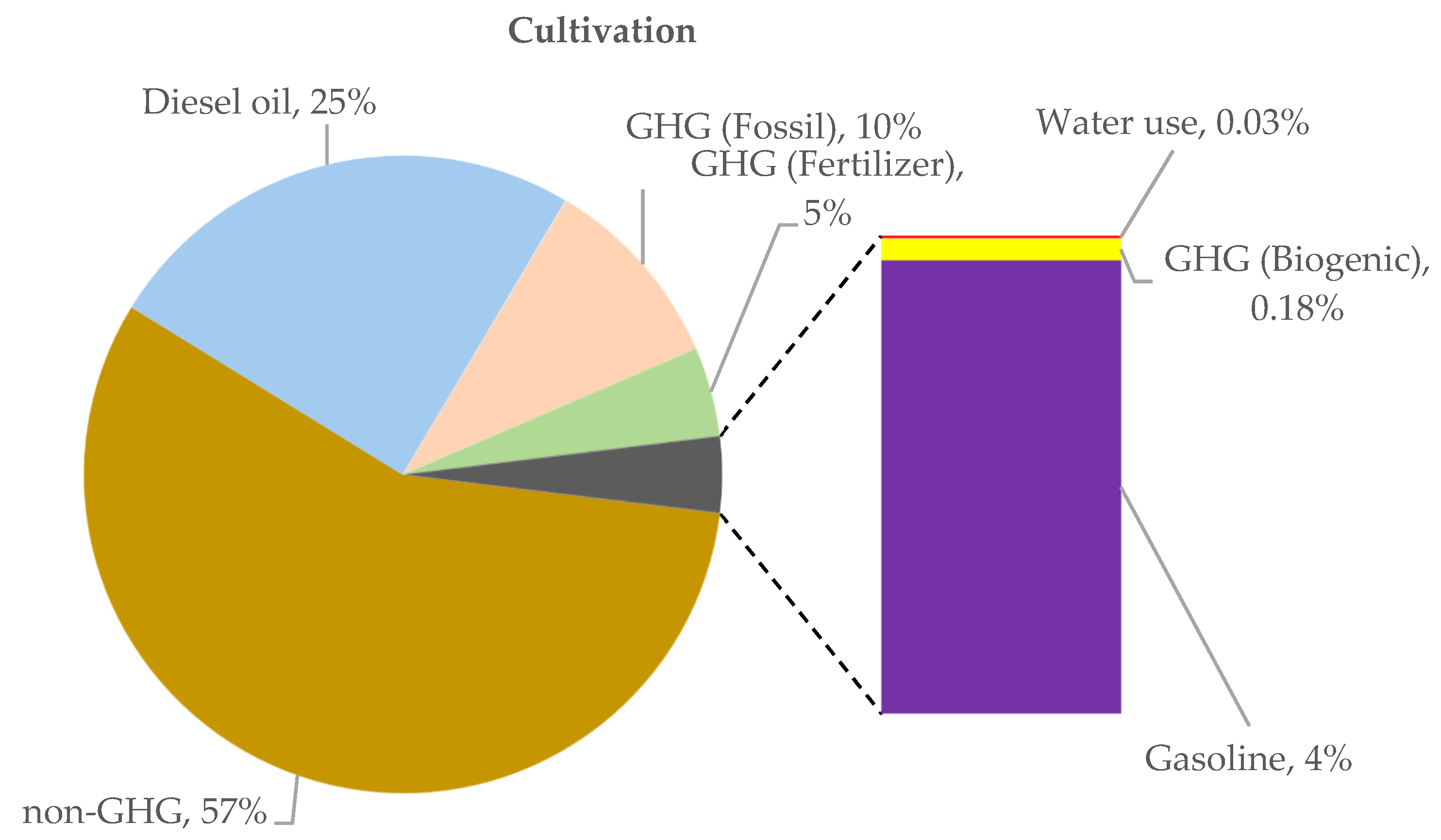

2.3.1. Cultivation

- The chemical fertilizer (15-15-15) 312 kg per hectare was used [28].

- Diesel use in tractor machine for land preparation and harvesting.

- Emission to air of ammonia, nitrous oxide and nitrogen oxides due to fertilizer consumption were estimated by [29], whereas calculated from cradle to gate and assume that the fertilizers use in Thailand as N-P-K in terms of Urea, Diammonium phosphate, and Potassium oxide, whereas nitrogen losses to air in terms of nitrous oxide were estimated with a factor of 1%.

- GHG emissions from fertilizer was calculated from Equation (1).

- GHG emissions from diesel combustion was calculated from Equation (2).

- Sugarcane productivity was transported to sugar milling plant, the proportion as 70% fresh sugarcane and 30% burned sugarcane, of all the sugarcane planted per hectare. In addition, the average sugarcane yield is 58 t per hectare.

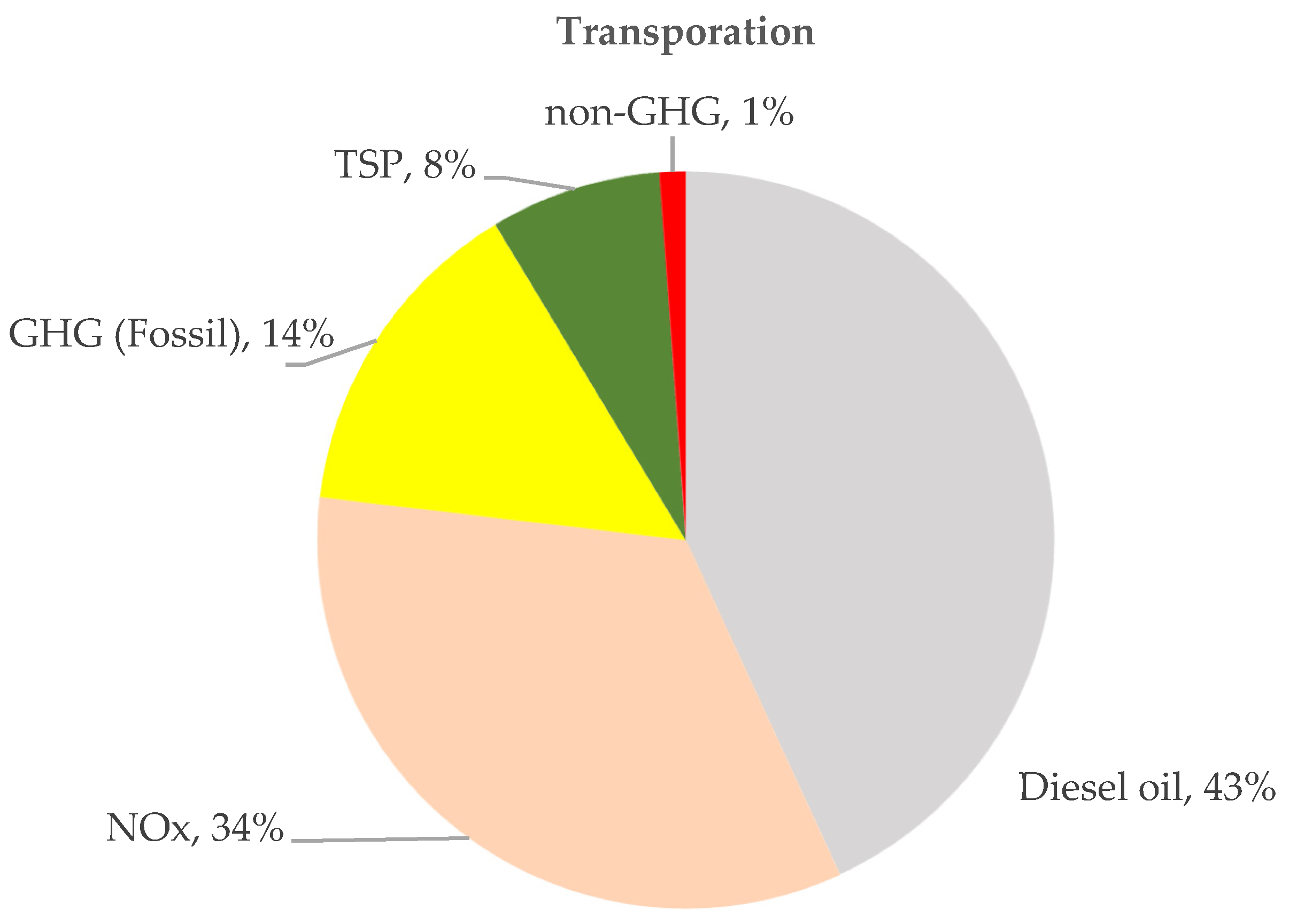

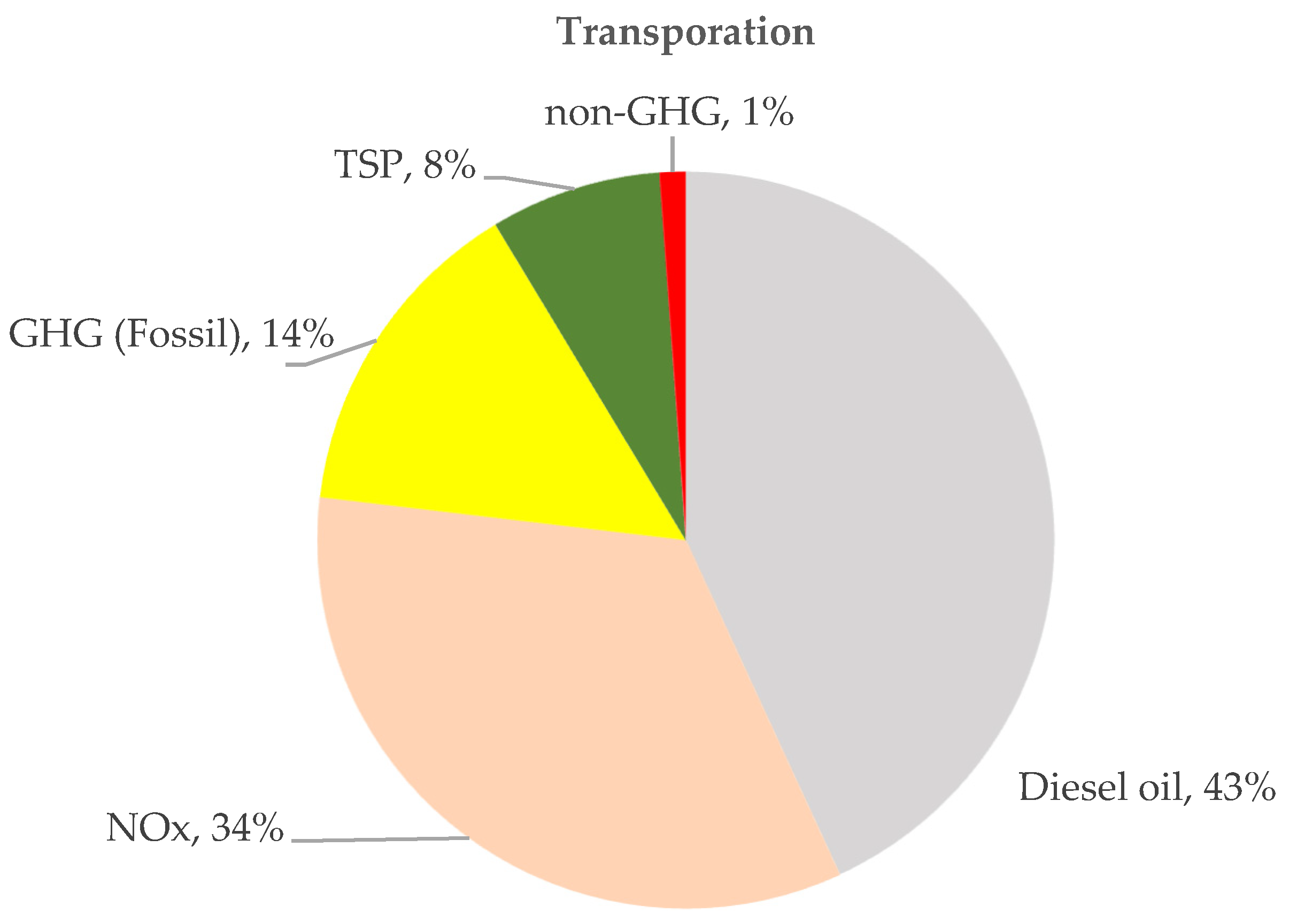

2.3.2. Transportation

- Diesel use in transportation, which use diesel amounted 2.30 L per ton of sugarcane.

- GHG emissions from diesel combustion was calculated from Equation (2).

2.3.3. Sugar Production

- Diesel, LPG and fuel oil use in stationary machine and GHG emissions from their combustion was calculated from Equation (2).

- Emission to air and water from sugar production were calculated by Equations (3) and (4), respectively.

2.3.4. GHG Emissions from Fertilizers Use, Transportation and Sugar Production

2.3.5. Airborne Emission from Sugar Production

2.3.6. Waterborne Emission from Sugar Production

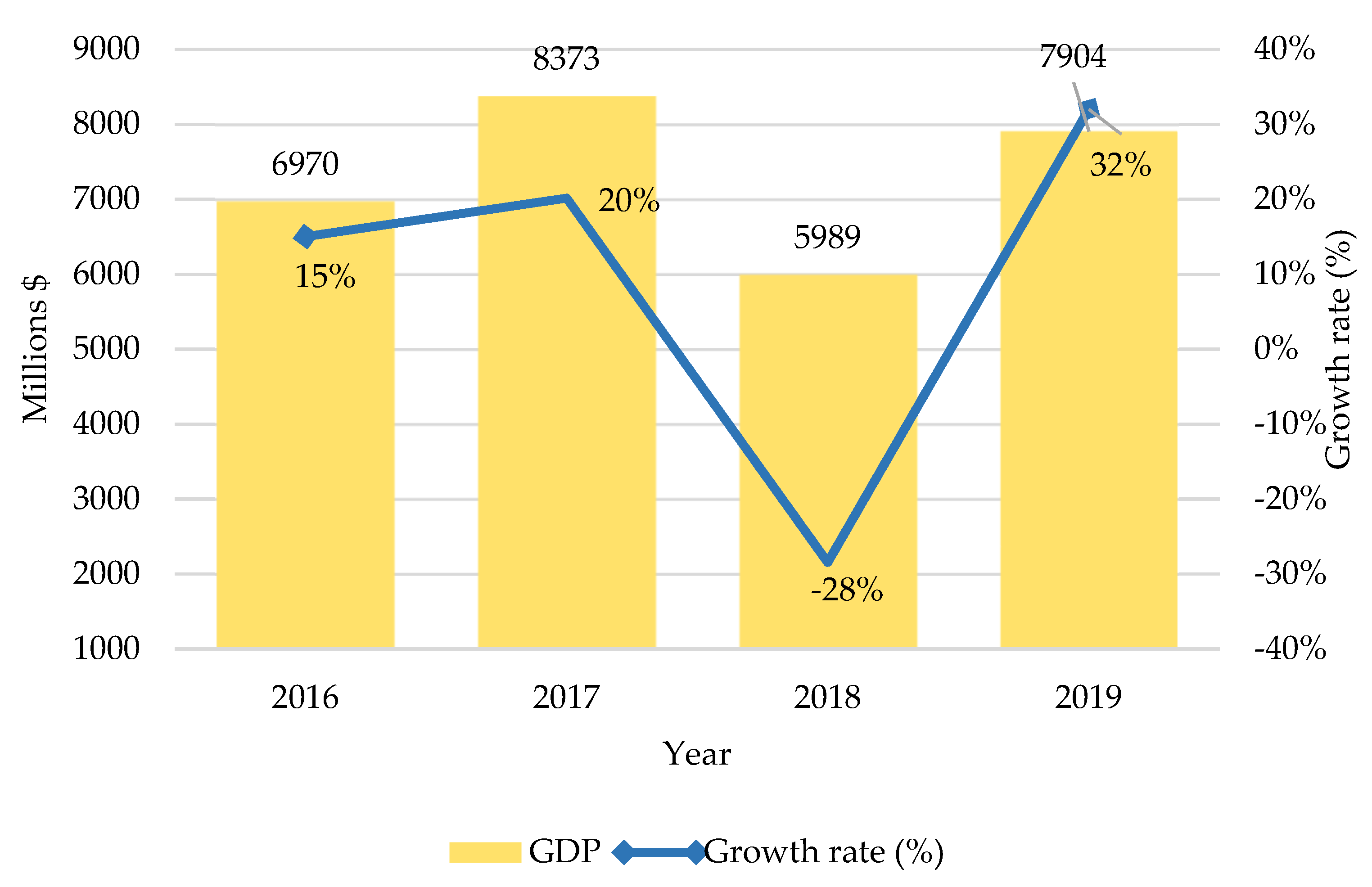

2.4. GDP of Sugar Industry

2.5. Green GDP Model

2.5.1. Purchasing Power Parity (PPP)

2.5.2. Green GDP Calculation

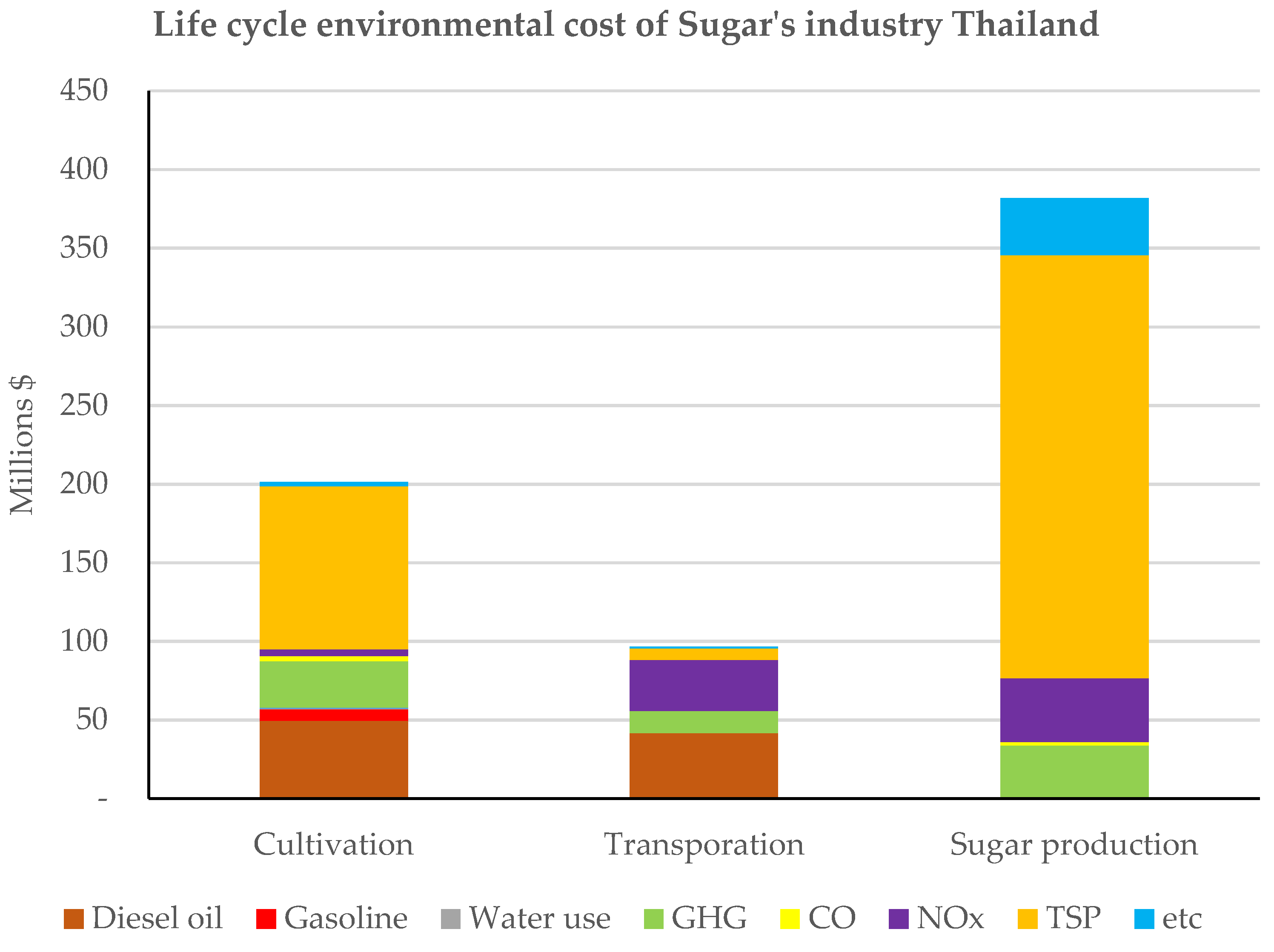

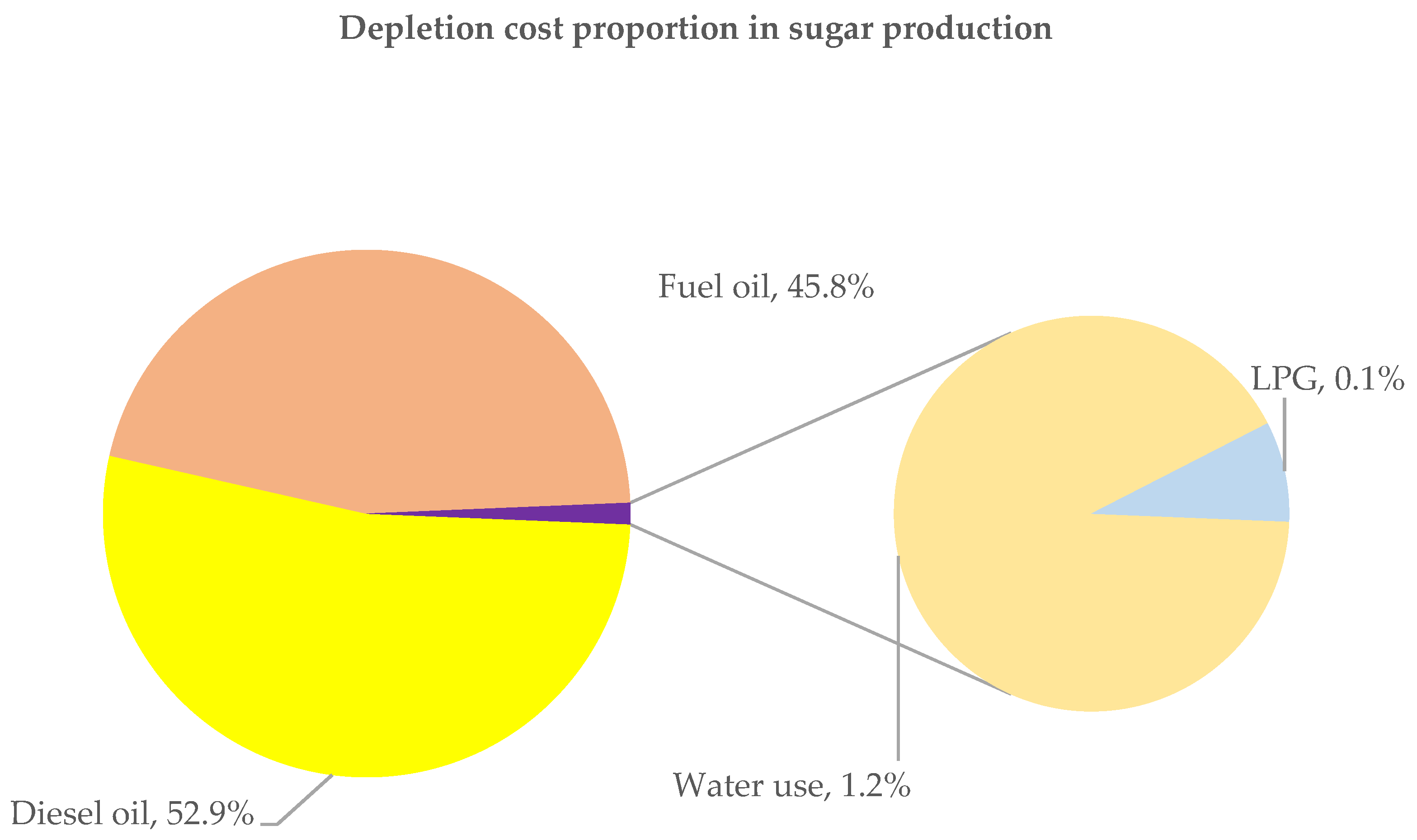

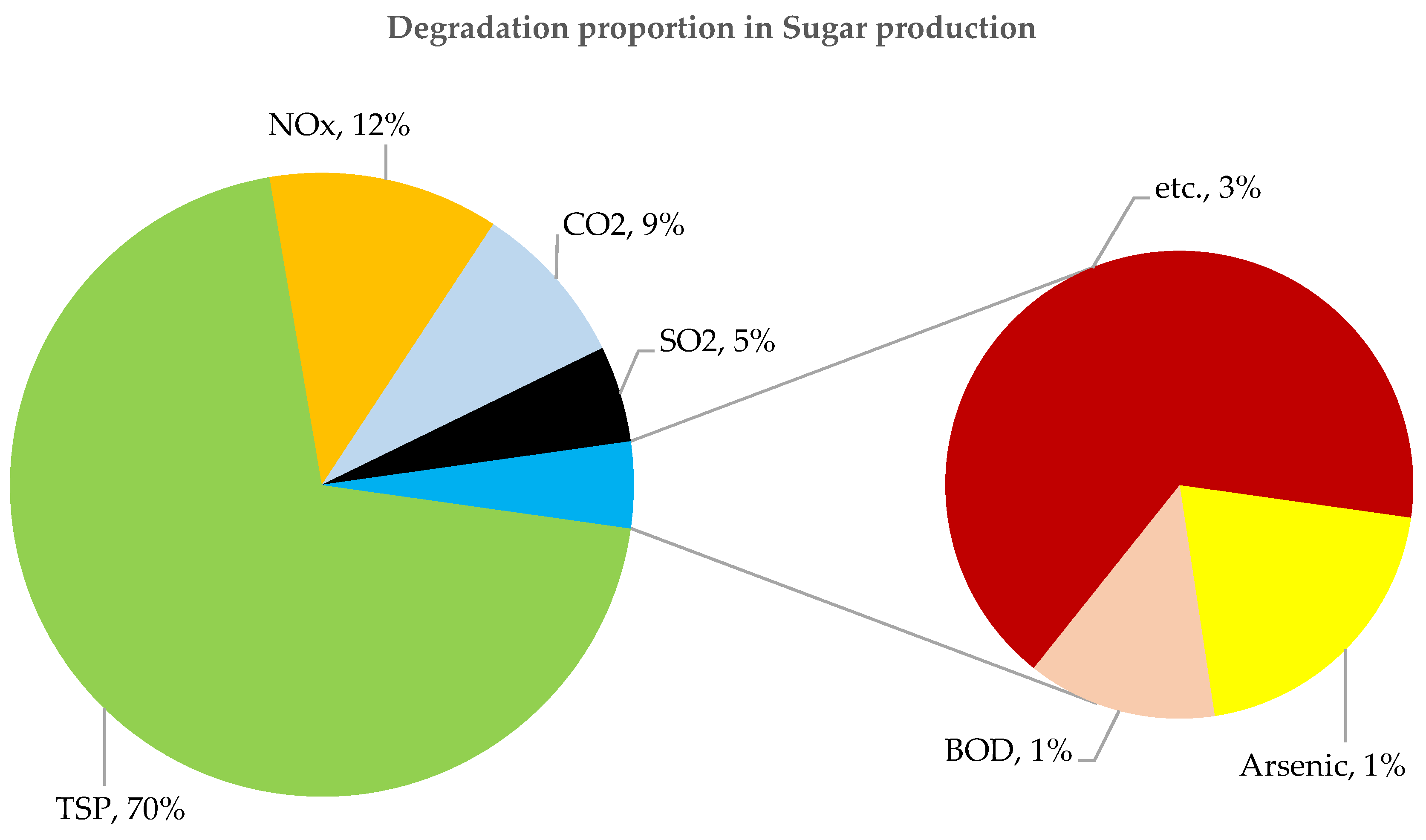

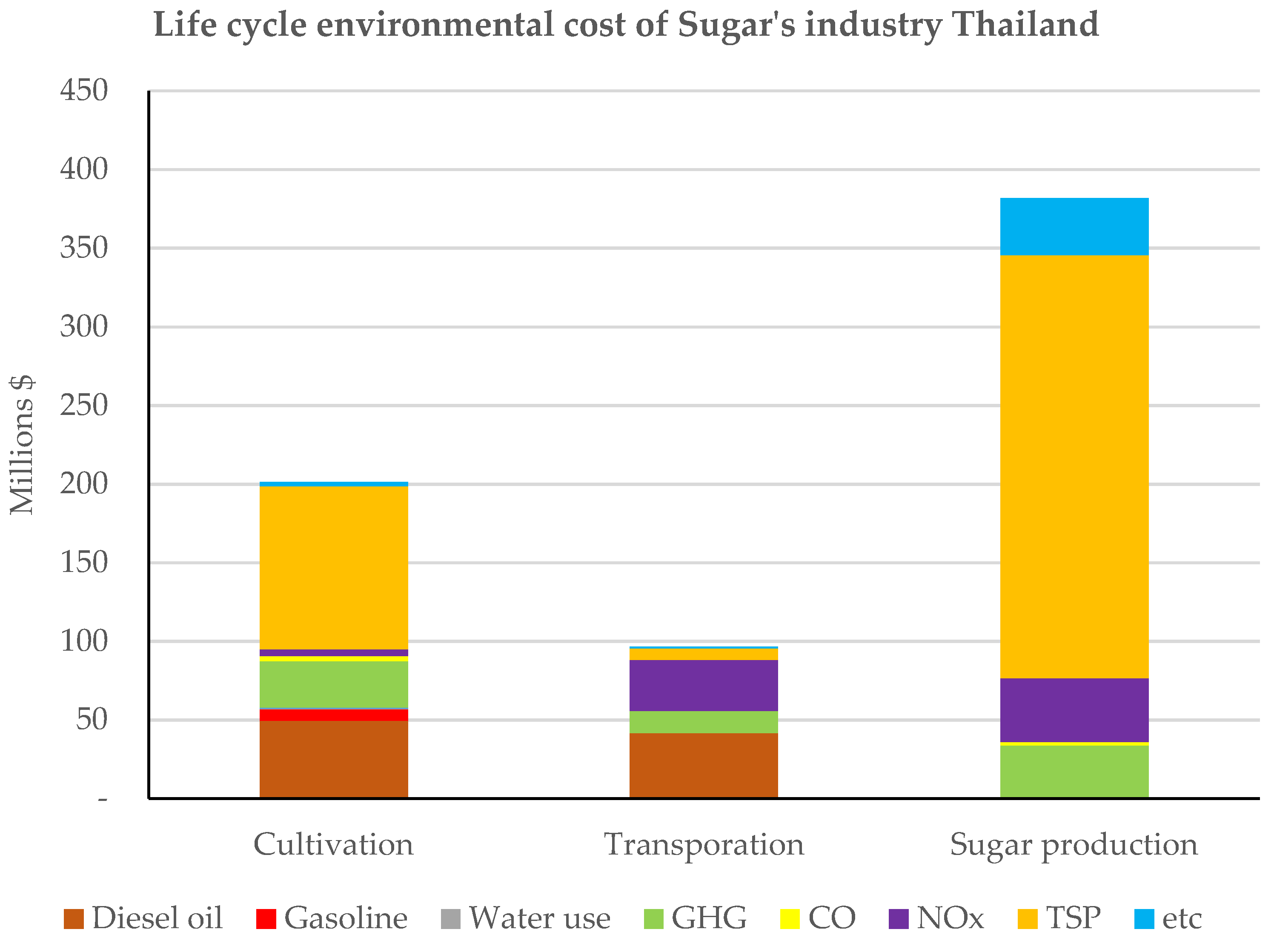

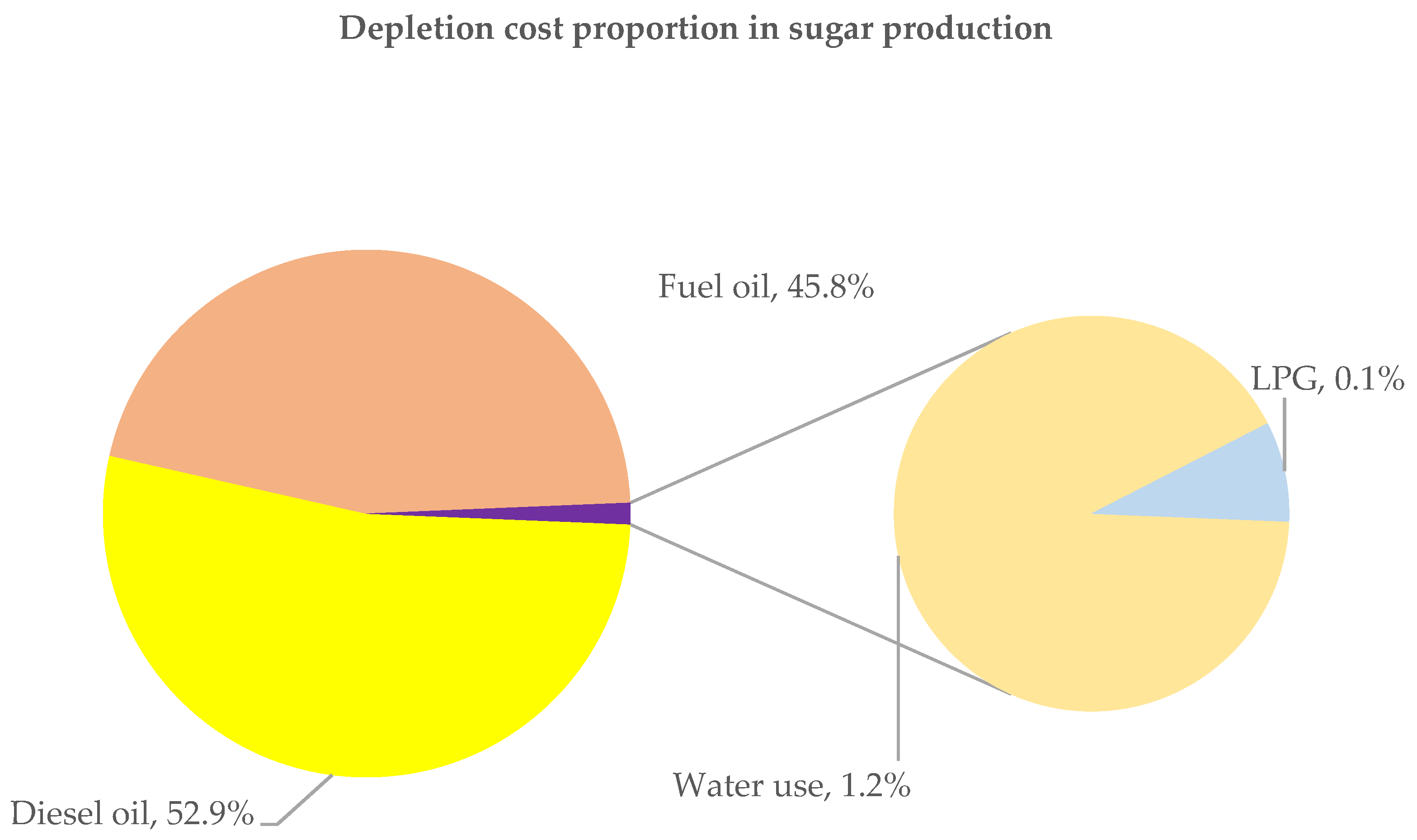

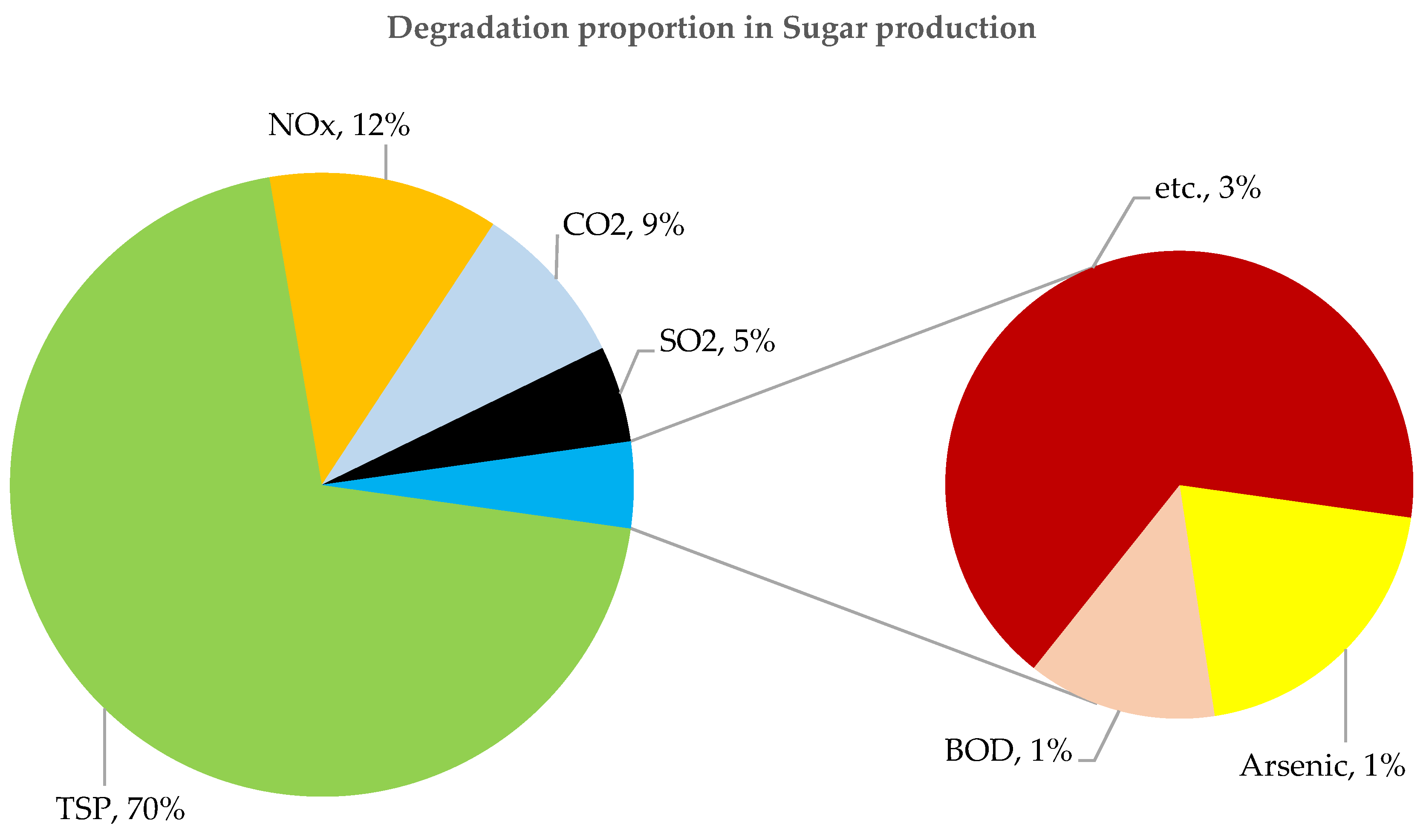

3. Results and Discussion

3.1. Life Cycle Inventory of Sugar Industry

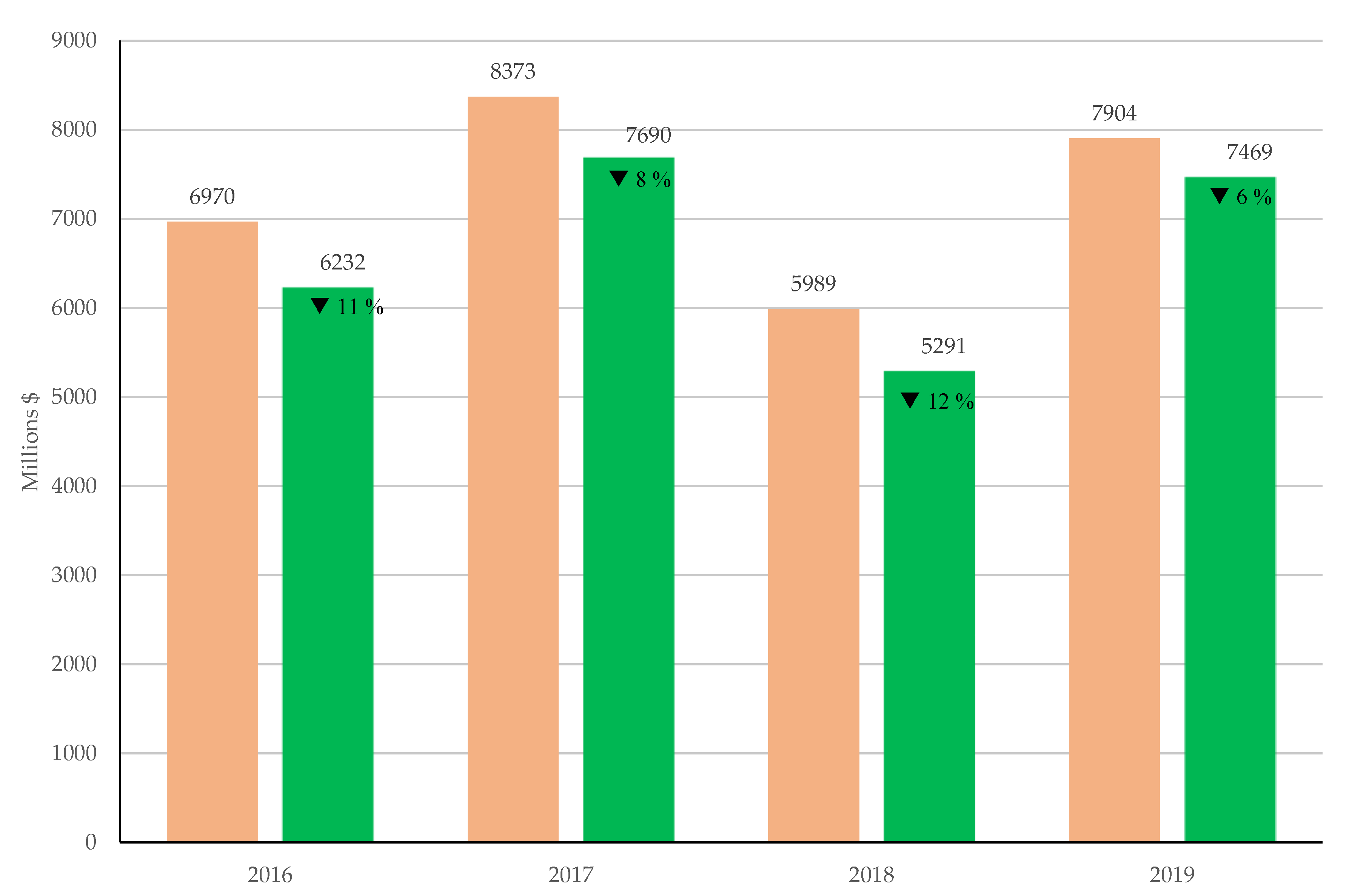

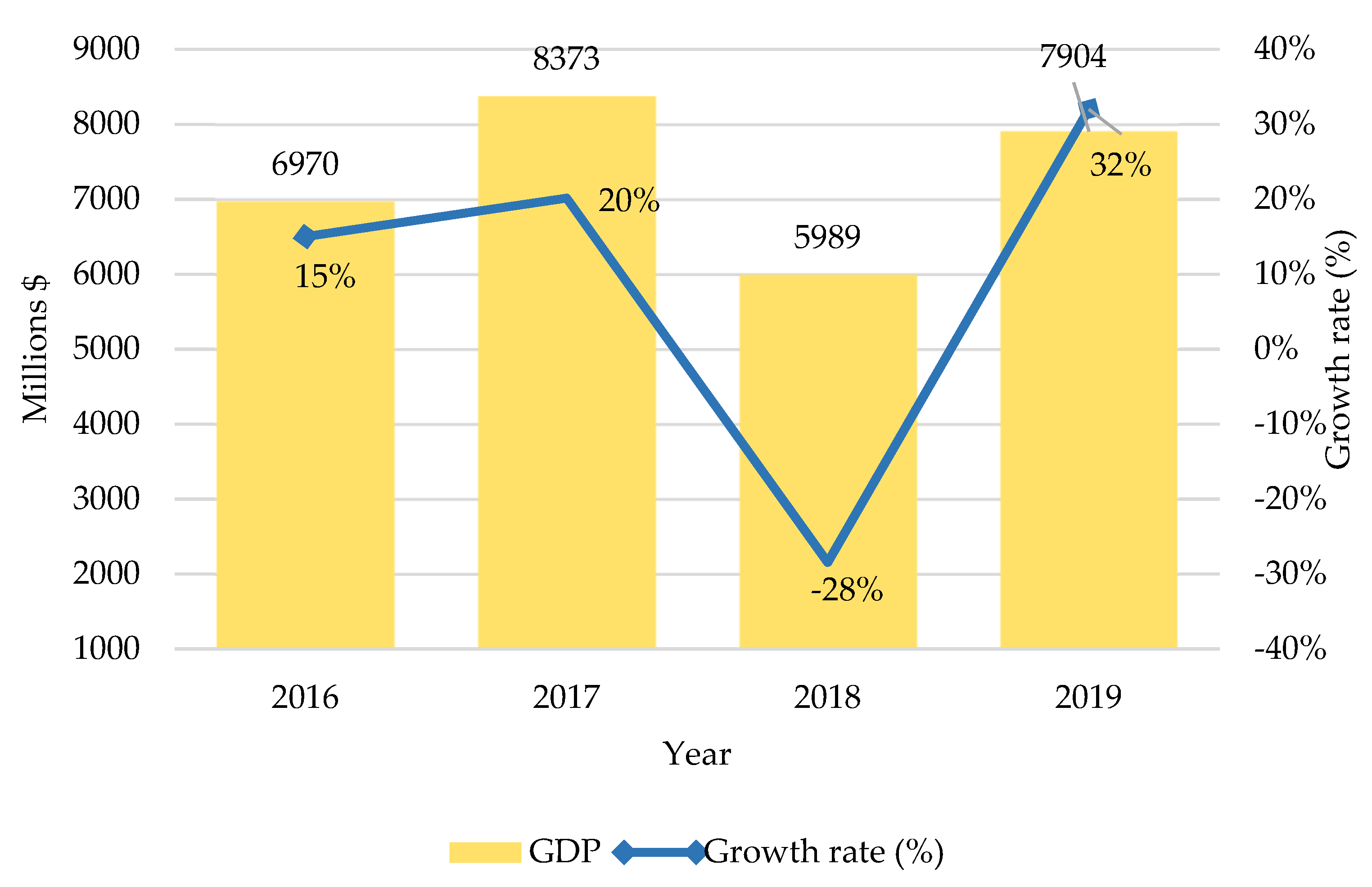

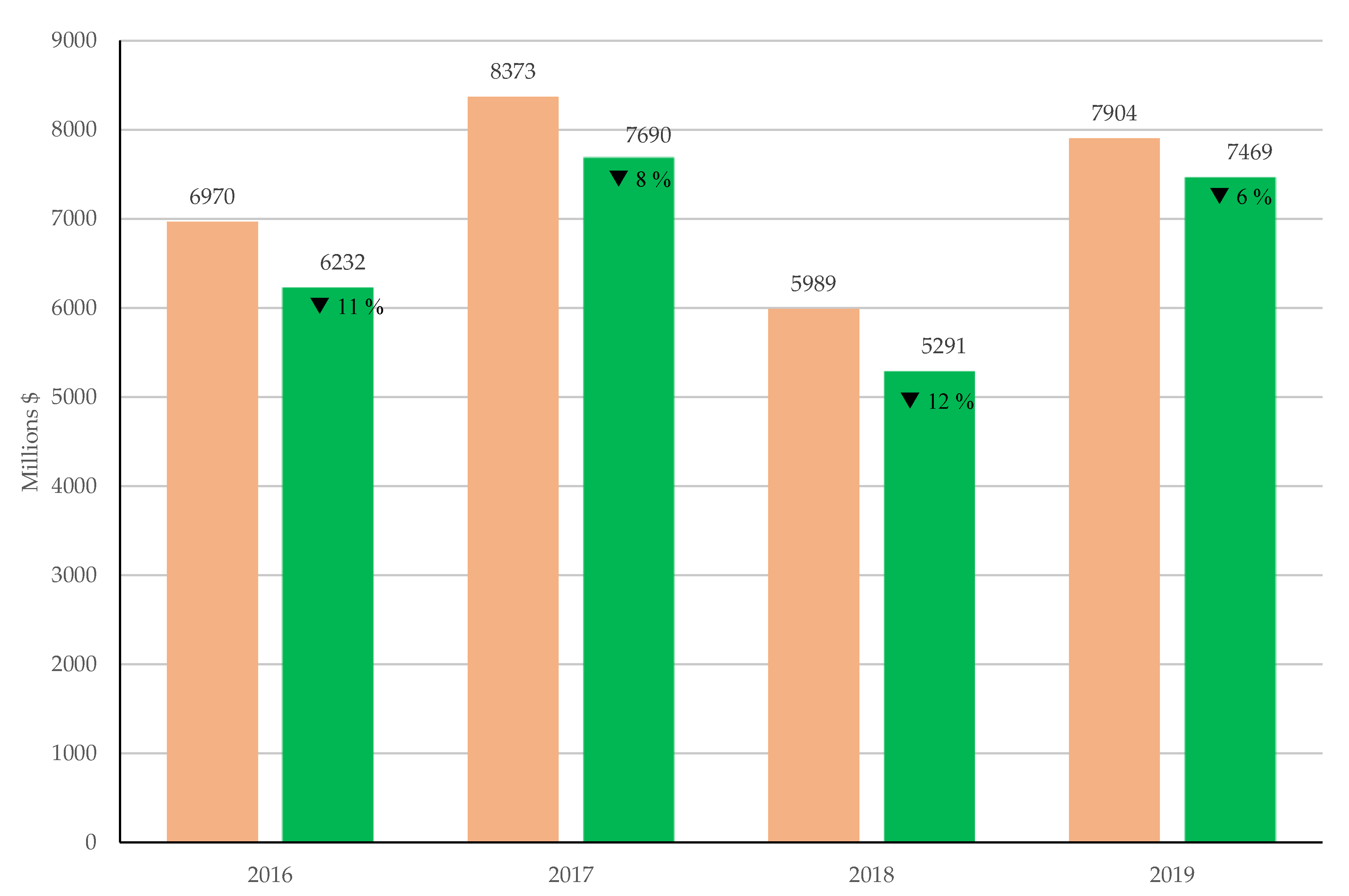

3.2. Green GDP of Sugar Industrial Sector Evaluation

3.3. Sensitivity Analysis for Factor Contribution in Green GDP Model

4. Conclusions

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Acknowledgments

Conflicts of Interest

References

- Office of the National Economic and Social Development Council. I/O table of Thailand 2015. Available online: https://www.nesdc.go.th/ewt_news.php?nid=9712&filename=io_page (accessed on 4 November 2021). (In Thai)

- USDA, United States Department of Agriculture (Foreign Agricultural Service). Sugar: World Markets and Trade. Available online: https://apps.fas.usda.gov/psdonline/circulars/Sugar.pdf (accessed on 4 November 2021).

- UN, United Nations. The Paris Agreement: Frequently Asked Questions. 2016. Available online: https://www.un.org/sustainabledevelopment/blog/2016/09/the-paris-agreement-faqs/ (accessed on 4 November 2021).

- United Nations; European Commission; International Monetary Fund; Organisation for Economic Co-operation and Development; World Bank. Handbook of National Accounting-Integrated Environmental and Economic Accounting 2003. 2003. Available online: https://unstats.un.org/unsd/environment/seea2003.pdf (accessed on 4 November 2021).

- Asafu-Adjaye, J. Green National Accounting and the Measurement of Genuine (Extended) Saving. In Integrating Economic and Environmental Policies: The Case of Pacific Island Countries; Development Papers No.25; Raj Kumar; United Nations: Bangkok, Thailand, 2004; pp. 59–77. Available online: https://library.sprep.org/sites/default/files/603.pdf (accessed on 5 November 2021).

- Xu, L.; Yu, B.; Yue, W. A method of green GDP accounting based on eco-service and a case study of Wuyishan, China. Procedia Environ. Sci. 2010, 2, 1865–1872. [Google Scholar] [CrossRef] [Green Version]

- Yanhong, L.; Jia, L.; Yihua, Z. A Study on the Sustainable Relationship among the Green Finance, Environment Regulation and Green-Total-Factor Productivity in China. Sustainability 2021, 13, 11926. [Google Scholar]

- Mahnaz, K.; Hamed Najafi, A. Spatial Effects of Energy Consumption and Green GDP in Regional Agreements. Sustainability 2021, 13, 10078. [Google Scholar] [CrossRef]

- Office of The National Economic and Social Development Board. Personal Communication about A System of Environmental and Economic Accounting—SEEA: Water and Mineral Resources; Office of The National Economic and Social Development Board: Bangkok, Thailand, 2010.

- National Center for Genetic Engineering and Biotechnology. Thailand Green GDP: A Study of a Framework for Environmental and Economic Accounting of Agricultural Sector; NSTDA: Bangkok, Thailand, 2014.

- Attavanich, W.; Mungkung, R.; Mahathanaseth, I.; Sanglestsawai, S.; Jirajariyav, A. Developing green GDP accounting for Thai Agricultural Sector using the economic input output-life cycle assessment to assess green growth. In Proceedings of the SEE 2016 in Cojunction with ICGSI 2016 and CTI 2016, Bangkok, Thailand, 28–30 November 2016. [Google Scholar]

- Kunanuntakij, K.; Varabuntoonvit, V.; Vorayos, N.; Panjapornpon, C.; Mungcharoen, T. Thailand Green GDP assessment based on environmentally extended input-output model. J. Clean. Prod. 2017, 167, 970–977. [Google Scholar] [CrossRef]

- Kunanuntakij, K.; Varabuntoonvit, V.; Vorayos, N.; Mungcharoen, T. Green GDP Study Based on Life Cycle Impact Assessment of Refinery Sector in Thailand. In Proceedings of the 11th International Conference on EcoBalance 2014, Tsukuba, Japan, 27–30 October 2014. [Google Scholar]

- Pantavisid, S. Natural Resource and Environmental Costs of Good and Service Production via Sustainable Consumption and Production Approach towards Prioritizing the Environmental Management in Thailand. Ph.D. Dissertation, National Institute of Development Administration, Bangkok, Thailand, 25 September 2012. [Google Scholar]

- Silalertruksa, T.; Gheewala, S.H.; Hunecke, K.; Fritsche, U.R. Biofuels and employment effects: Implications for socio-economic development in Thailand. Biomass Bioenergy 2012, 46, 409–418. [Google Scholar] [CrossRef]

- Silalertruksa, T.; Gheewala, S.H.; Pongpat, P. Sustainability assessment of sugarcane biorefinery and molasses ethanol production in Thailand using eco-efficiency indicator. Appl. Energy 2015, 160, 603–609. [Google Scholar] [CrossRef]

- Giannetti, B.F.; Agostinho, F.; Almeida, C.M.V.B.; Huisingha, D. A review of limitations of GDP and alternative indices to monitor human wellbeing and to manage eco-system functionality. J. Clean. Prod. 2015, 87, 11–25. [Google Scholar] [CrossRef]

- Zvonimira, S.G.; Marinela, K.N.; Elena, R. Circular Economy Concept in the Context of Economic Development in EU Countries. Sustainability 2020, 12, 3060. [Google Scholar]

- Chi-Hung, T.; Yun-Hwei, S.; Wen-Tien, T. Sustainable Material Management of Industrial Hazardous Waste in Taiwan: Case Studies in Circular Economy. Sustainability 2021, 13, 9410. [Google Scholar]

- Marzena, S.; Joanna, D.; Agnieszka, K.; Dominika, S. Transformation towards Circular Economy (CE) in Municipal Waste Management System: Model Solutions for Poland. Sustainability 2020, 12, 4561. [Google Scholar]

- Marit, B.; Sigurd, V. Life Cycle Assessment to Ensure Sustainability of Circular Business Models in Manufacturing. Sustainability 2021, 13, 11014. [Google Scholar] [CrossRef]

- Gillian, E.; Isabel, L. Sustainability Issues and Opportunities in the Sugar and Sugar-Bioproduct Industries. Sustainability 2015, 7, 12209–12235. [Google Scholar]

- Munagala, M.; Yogendra, S. Sustainable valorization of sugar industry waste: Status, opportunities, and challenges. Bioresour. Technol. 2020, 303, 122929. [Google Scholar]

- International Organization for Standardization. Environment Management-Life Cycle Assessment-Principle and Framework, 2nd ed.; International Organization for Standardization: Geneva, Switzerland, 2006. [Google Scholar]

- International Organization for Standardization. Environment Management-Requirements and Guideline (ISO 14044:2006), 2nd ed.; International Organization for Standardization: Geneva, Switzerland, 2006. [Google Scholar]

- Eggleston, H.S.; Buendia, L.; Miwa, K.; Ngara, T.; Tanabe, K. 2006 IPCC Guidelines for National Greenhouse Gas Inventories; Volume 2 Energy; Institute for Global Environmental Strategies (IGES): Hayama, Japan, 2006. [Google Scholar]

- Eggleston, H.S.; Buendia, L.; Miwa, K.; Ngara, T.; Tanabe, K. 2006 IPCC Guidelines for National Greenhouse Gas Inventories; Volume 5 Waste; Institute for Global Environmental Strategies (IGES): Hayama, Japan, 2006. [Google Scholar]

- Department of Agriculture, Thailand. Study on Effective Method of Chemical Fertilizer Application to Increase Cane Yield. 2008. Available online: https://www.doa.go.th/research/attachment.php?aid=1618 (accessed on 4 November 2021). (In Thai)

- Thailand Greenhouse Gas Management Organization (Public Organization). Emission Factor, Carbon Footprint of Product, GHG emissions from Fertilizer. 2013. Available online: http://thaicarbonlabel.tgo.or.th/index.php?lang=TH&mod=Y0hKdlpIVmpkSE5mWkc5M2JteHZZV1E9 (accessed on 4 November 2021). (In Thai).

- Nguyen, T.L.T.; Gheewala, S.H. Life Cycle Assessment of fuel ethanol from cane molasses in Thailand. Int. J. Life Cycle Assess. 2008, 13, 301–311. [Google Scholar] [CrossRef]

- Office of the Cane and Sugar Board, Ministry of Industry, Thailand. Personal Communication about the Productivity of Sugarcane and Sugar Production from 2016 to 2019; Office of the Cane and Sugar Board, Ministry of Industry: Bangkok, Thailand, 2021.

- Department of Industrial Works, Ministry of Industry, Thailand. Personal Communication about the System for Reporting the Type and Amount of Pollutants Discharged from the Factory (RV2, RV3); Department of Industrial Works, Ministry of Industry: Bangkok, Thailand, 2021.

- The Working Group I Contribution to the IPCC 4th Assessment Report. Available online: https://www.ipcc.ch/site/assets/uploads/2018/05/ar4-wg1-errata.pdf (accessed on 4 November 2021).

- Pollution Control Department, Ministry of Natural Resources and Environment, Thailand. Calculating Emissions from Measurement Data. Available online: https://www.pcd.go.th/wp-content/uploads/2020/05/pcdnew-2020-05-25_04-41-26_574047.pdf (accessed on 4 November 2021). (In Thai)

- Office of the National Economic and Social Development Council. Personal Communication about Sugar INDUSTRY’s GDP from 2016 to 2019; Office of the National Economic and Social Development Council: Bangkok, Thailand, 2021.

- Goedkoop, M.; Heijungs, R.; Huijbregts, M.; Schryyer, A.; Struijs, J.; Zelm, R.V. ReCiPe 2008 A Life Cycle Impact Assessment Method which Comprises Harmonized Category Indicators at the Midpoint and Endpoint Level, 1st ed.; (Version 1.08); Report I: Characterization; Ministry of Housing, Spatial Planning and the Environment (VROM): Zoelermeer, The Netherlands, 2013. [Google Scholar]

- Itsubo, N.; Tokyo City University, Yokohama Campus, Yokohama, Japan. Personal Communication, About LIME 2: Life—Cycle Impact Assessment Method Based on Endpoint Modeling. 2015.

- PPP Conversion Factor, GDP (LCU Per International $)—Japan, United States. Available online: https://data.worldbank.org/indicator/PA.NUS.PPP?page=1&locations=JP-US (accessed on 4 November 2021).

- George, K.V.; Manjunath, S.; Chalapati Rao, C.V.; Bopche, A.M. Cyclone as a precleaner to ESP—A need for Indian coal based thermal power plants. Environ. Technol. 2008, 24, 1425–1430. [Google Scholar] [CrossRef] [PubMed]

- Mianquiang, X.; Bin-Le, L.; Kiyotaka, T.; Kimitaka, M.; Tetsuya, N.; Tohru, K. Life Cycle Assessment of Nitrogen Circular Economy-Based NOx Treatment Technology. Sustainability 2021, 13, 7826. [Google Scholar] [CrossRef]

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Process Information | Data Information | Unit | Data Source |

|---|---|---|---|

| Cultivation Land preparation Planting and treatment | Inputs | ||

| Sugarcane stocks | ton | 1 Questionnaires | |

| Diesel oil | liter | 1 Questionnaires | |

| Harvesting | Gasoline | liter | 1 Questionnaires |

| Fertilizer | kg | [28] | |

| Paraquat | liter | 1 Questionnaires | |

| Water from ground | liter | 1 Questionnaires | |

| Outputs | |||

| GHG emissions and etc. | kg | [26,27,29] | |

| Tops and leaves | kg | [30] | |

| Sugarcane | ton | 1 Questionnaires | |

| Sugar production and transportation | Inputs | ||

| Sugarcane | ton | [31] | |

| Diesel oil | liter | 1 Questionnaires | |

| Liquefied Petroleum Gas (LPG) | kg | 1 Questionnaires | |

| Fuel oil | liter | 1 Questionnaires | |

| Water from ground | liter | 1 Questionnaires | |

| Chemicals | kg, ton | 1 Questionnaires | |

| Outputs | |||

| Sugar | ton | [31] | |

| Molasses | ton | 1 Questionnaires | |

| Bagasse | ton | 1 Questionnaires | |

| Emission to air | kg, ton | [26,27,32] | |

| Emission to water | kg, ton | [32] |

| Input | Output | ||

|---|---|---|---|

| Unit Process 1: Sugarcane Production (Per Hectare) | |||

| Non-renewable resource | Amount | Emission to air | Amount |

| Diesel | 56 L | 1 CO2 | 22.56 kg |

| Pesticides | 2.06 kg | 2 N2O | 0.12 kg |

| Fertilizers | 312 kg | Solid waste | |

| Top and leaves | 0.20 kg | ||

| Renewable resource | Product | ||

| Water use | 43,750 L | Sugarcane | 58 t |

| Unit process 2: Transportation (per ton of sugarcane) | |||

| Non-renewable resource | Amount | Emission to air | Amount |

| Diesel | 6.90 L | CO2 | 18.60 kg |

| N2O | 0.001 kg | ||

| CH4 | 0.001 kg | ||

| Unit process 3: Sugar production (per 1 kg of sugar production) | |||

| Non-renewable resource | Amount | Emission to air | Amount |

| Diesel | 0.203 kg | TSP | 0.76 kg |

| LPG | 3.0 × 10−4 kg | HCl | 1.10 × 10−2 kg |

| Fuel oil | 5.30 × 10−2 kg | CO | 2.00 kg |

| Chemicals | 4.60 × 10−4 kg | SO2 | 4.00 × 10−2 kg |

| Renewable resource | NOx | 8.50 × 10−1 kg | |

| Water use | 0.88 m3 | NMVOC | 3.50 × 10−2 kg |

| Energy consumption | CO2 | 0.14 t | |

| Electricity | 135 kWh | N2O | 4.90 × 10−3 kg |

| CH4 | 3.70 × 10−5 kg | ||

| Emission to water | |||

| TDS | 0.08 t | ||

| SS | 0.64 kg | ||

| COD | 0.01 t | ||

| BOD | 0.13 kg | ||

| Description | Affected Factors | |

|---|---|---|

| Base case | Conventional sugarcane production, transportation and sugar production | |

| Scenario 1 | Base case, Productivity increases 5% or decrease 5% | GDP |

| Scenario 2 | Base case, Energy consumption increases 15% or decrease 15% | Depletion cost |

| Scenario 3 | Base case, Efficiency of air pollution control system and wastewater treatment system increases 15% or decrease 15% | Degradation cost |

| Scenario 4 | Base case, PPP conversion factor increases 10% or decrease 10% | PPP conversion factor |

| GDP (Millions $) | Depletion Cost (Millions $) | Degradation Cost (Millions $) | Green GDP Result (Millions $) | Comparison with Green GDP of Base Case | |

|---|---|---|---|---|---|

| Base case | 6400 | 10.83 | 350.32 | 6038.84 | |

| Scenario 1 | |||||

| +5% | 6720 | 10.83 | 350.32 | 6358.84 | +5% |

| −5% | 6080 | 10.83 | 350.32 | 5718.84 | −5% |

| Scenario 2 | |||||

| +15% | 6400 | 12.46 | 350.32 | 6037.22 | −0.03% |

| −15% | 6400 | 9.21 | 350.32 | 6040.47 | +0.03% |

| Scenario 3 | |||||

| +15% | 6400 | 10.83 | 402.87 | 5986.30 | −0.9% |

| −15% | 6400 | 10.83 | 297.77 | 6091.39 | +0.9% |

| Scenario 4 | |||||

| +10% | 6400 | 11.92 | 385.35 | 6002.73 | −0.6% |

| −10% | 6400 | 9.75 | 315.30 | 6074.96 | +0.6% |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2022 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Nawapanan, E.; Kongboon, R.; Sampattagul, S. Green GDP Indicator with Application to Life Cycle of Sugar Industry in Thailand. Sustainability 2022, 14, 918. https://doi.org/10.3390/su14020918

Nawapanan E, Kongboon R, Sampattagul S. Green GDP Indicator with Application to Life Cycle of Sugar Industry in Thailand. Sustainability. 2022; 14(2):918. https://doi.org/10.3390/su14020918

Chicago/Turabian StyleNawapanan, Ekkaporn, Ratchayuda Kongboon, and Sate Sampattagul. 2022. "Green GDP Indicator with Application to Life Cycle of Sugar Industry in Thailand" Sustainability 14, no. 2: 918. https://doi.org/10.3390/su14020918

APA StyleNawapanan, E., Kongboon, R., & Sampattagul, S. (2022). Green GDP Indicator with Application to Life Cycle of Sugar Industry in Thailand. Sustainability, 14(2), 918. https://doi.org/10.3390/su14020918