Implications of Mediated Market Access—Exploring the Nature of Vertical Relationships within the Croatian Wine Industry

Abstract

:1. Introduction

2. Theoretical Background

3. Model Development

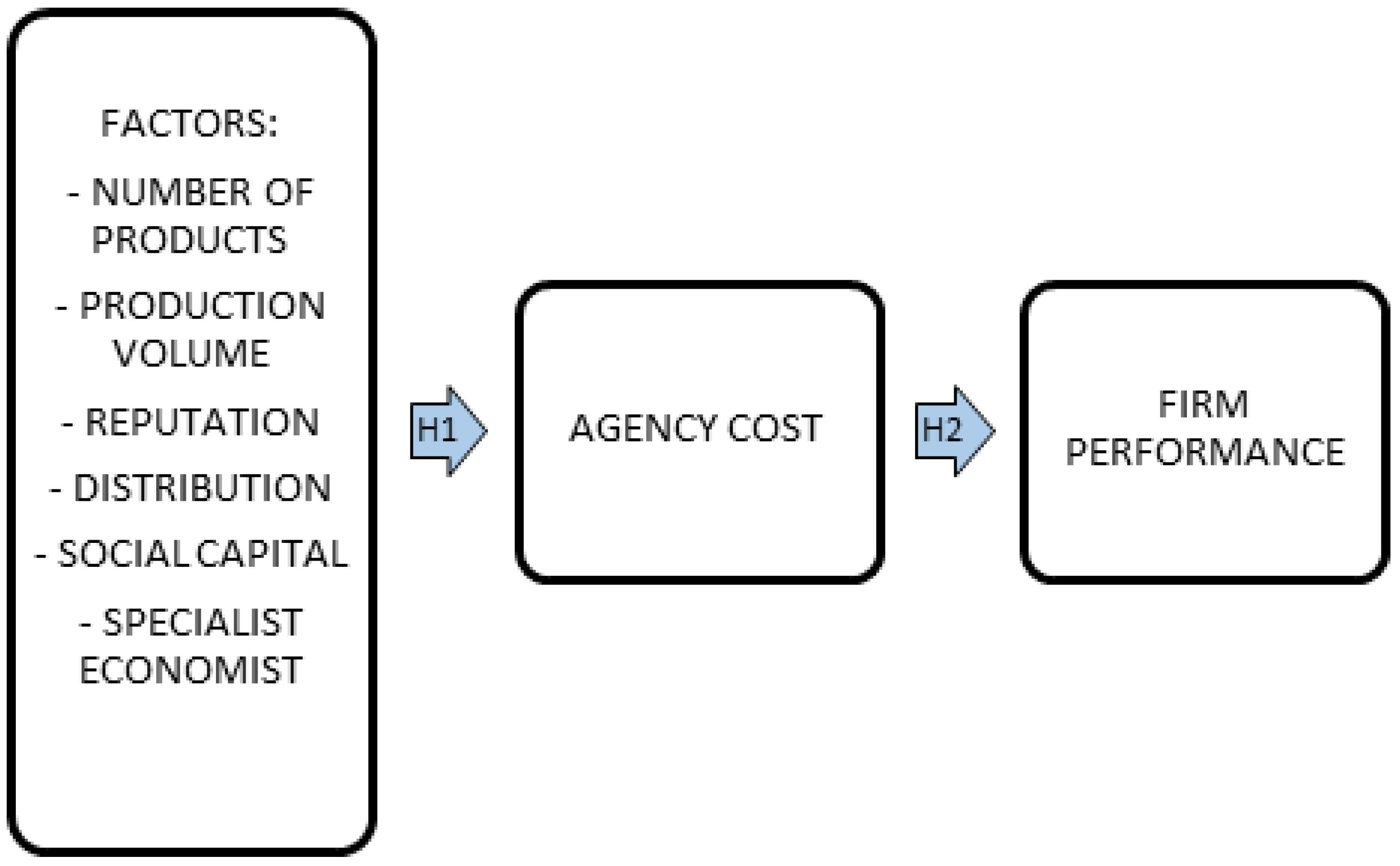

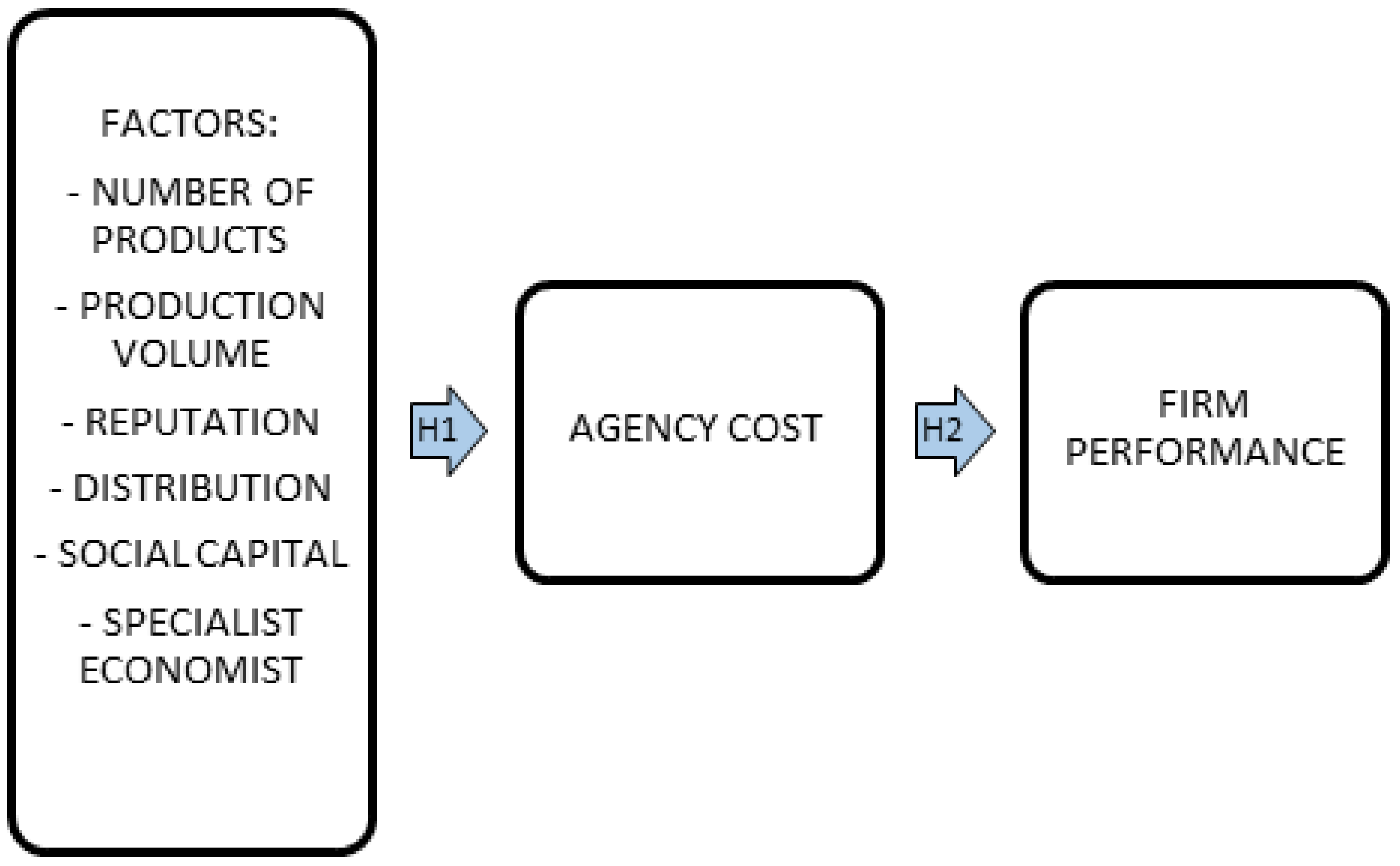

3.1. Variables and Hypotheses

3.2. Materials and Methods

3.2.1. Data and Sample Description

3.2.2. The Empirical Models

- Regression of X on Y.

- Regression of X on M.

- Regression of M on Y.

- Regression of both X and M on Y.

4. Results

5. Discussion

6. Conclusions

- We lacked observations that could explain the position of the distributors; apart from some interviews (not included in this report), we found no insight into factors affecting their economic performance (the value/costs of services they provide, profit margins, how market size and consumer preferences shifts affect their economic standing, etc.). It would be helpful to access contracts and see whether some wine-producers have been able to bargain for particular contract clauses that do not apply to others.

- We could make no estimations of the average margins and differences in margins earned in direct sales compared to margins earned in selling through market intermediaries. Moreover, we found no insight into data that would allow us to break down agency costs by components (such as monitoring, bonding, residual). Instead, we adapted our research model by reverting to the contributions of authors who have studied vertical agreements in the agricultural value chain [4,5,7,8,34].

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Conflicts of Interest

References

- Liverpolll-Tasie, L.S.; Wineman, A.; Young, S.; Tambo, J.; Vargas, C.; Reardon, T.; Adjognon, G.S.; Porciello, J.; Gathoni, N.; Bizikova, L.; et al. A scoping review of market links between value chain actors and small-scale producers in developing regions. Nat. Sustain. 2020, 3, 799–808. [Google Scholar] [CrossRef]

- Distribution of Added Value of the Organic Food Chain, Final Report. Available online: https://op.europa.eu/en/publication-detail/-/publication/a911740b-4cbe-11e7-a5ca-01aa75ed71a1 (accessed on 1 December 2021).

- Kuosmanen, T.; Niemi, J. What explains the widening gap between the retail and producer prices of food? Agric. Food Sci. 2009, 18, 317–331. [Google Scholar] [CrossRef]

- Monitoring the Implementation of Principles of Good Practice in Vertical Relationships in the Food Supply Chain- ARETE, Final Report, Revised Edition. Available online: https://op.europa.eu/en/publication-detail/-/publication/79ab6942-fc83-11e5-b713-01aa75ed71a1 (accessed on 3 December 2021).

- European Commission. Report from the Commission to the European Parliament, the Council, the European Economic and Social Committee and the Committee of the Regions on the State and the Transposition and Implementation of Directive (EU) 2019/633 of the European Parliament and of the Council of 17 April 2019 on Unfair Trading Practices in Business-to-Business Relationships in the Agricultural and Food Supply Chain. Available online: https://eur-lex.europa.eu/legal-content/EN/TXT/PDF/?uri=CELEX:32019L0633&from=en (accessed on 1 January 2022).

- Sorrentino, A.; Russo, C.; Cacchiarelli, L. Market power and bargaining power in the EU food supply chain: The role of Producer Organizations. Mediterr. J. Agric. Econ. Environ. 2018, 17, 21–31. [Google Scholar] [CrossRef]

- Velasquez, B.; Buffaria, B.; European Commission. About farmers’ bargaining power within the new CAP. Agric. Food Econ. 2017, 5, 16. [Google Scholar] [CrossRef] [Green Version]

- Baron, R.M.; Kenny, D.A. The moderator–mediator variable distinction in social psychological research: Conceptual, strategic, and statistical considerations. J. Personal. Soc. Psychol. 1986, 51, 1173–1182. [Google Scholar] [CrossRef]

- European Commission. Available online: ec.europa.eu (accessed on 15 March 2021).

- Croatian Bureau of Statistics. Available online: dzs.hr (accessed on 17 March 2021).

- International Organisation of Vine and Wine. Available online: oiv.int (accessed on 17 March 2021).

- Guth, M.; Smedzil-Ambrozy, K.; Czyzewski, B.; Stepiem, S. The Economic Sustainability of Farms under Common Agricultural Policy in the European Union Countries. Agriculture 2020, 10, 34. [Google Scholar] [CrossRef] [Green Version]

- Katunar, J. The Role of Regional Differences on Croatian Winemakers Business. Agroecon. Croat. 2019, 9, 14–24. [Google Scholar]

- Katunar, J.; Kaštelan Mrak, M.; Sokolić, D. The impact of distribution channels on the bargaining position of Croatian wine producers. Econ. Rev. Contemp. Bus. Entrep. Econ. 2020, 33, 545–558. [Google Scholar]

- Jensen, M.C.; Meckling, W.H. Theory of the Firm: Managerial Behavior, Agency Costs and Ownership Structure. J. Financ. Econ. 1976, 3, 305–360. [Google Scholar] [CrossRef]

- Maskin, E.; Tirole, J. Unforeseen Contingencies and Incomplete Contracts. Rev. Econ. Stud. 1999, 66, 83–114. [Google Scholar] [CrossRef]

- Alchian, A.A.; Demsetz, H. Production, Information Costs, and Economic Organization. Am. Econ. Rev. 1972, 62, 777–795. [Google Scholar]

- Jensen, M.C. Agency Costs of Free Cash Flow, Corporate Finance, and Takeovers. Am. Econ. Rev. 1986, 76, 323–329. [Google Scholar]

- Ramakrishnan, R.T.S.; Thakor, A.V. Cooperation versus Competition in Agency. J. Law Econ. Organ. 1991, 7, 248–283. [Google Scholar]

- Gogineni, S.; Yadav, P.K.; Linn, S.C. Vertical and Horizontal Agency Costs: Evidence from Public and Private Firms. Electron. J. 2021. [Google Scholar] [CrossRef]

- McGuire, J.B. Agency Theory and Organizational Analysis. Manag. Financ. 1988, 14, 6–9. [Google Scholar] [CrossRef]

- Perrow, C. Complex Organizations; Random House: New York, NY, USA, 1986. [Google Scholar]

- Joskow, P.L. Long Term Vertical Relationships and the Study of Industrial Organization and Government Regulation. J. Inst. Theor. Econ. 1985, 141, 586–593. [Google Scholar]

- Mishra, D.P.; Heide, J.B.; Cort, S.G. Information Asymmetry and Levels of Agency Relationships. J. Mark. Res. 1998, 35, 277–295. [Google Scholar] [CrossRef] [Green Version]

- Whipple, J.M.; Roh, J. Agency Theory and Quality Fade in Buyer-Supplier Relationships. Int. J. Logist. Manag. 2010, 21, 338–352. [Google Scholar] [CrossRef]

- Steinle, C.; Schiele, H.; Ernst, T. Information Asymmetries as Antecedents of Opportunism in Buyer-Supplier Relationships: Testing Principal-Agent Theory. J. Bus. Bus. Mark. 2014, 21, 123–140. [Google Scholar] [CrossRef]

- Yan, T.; Kull, T.J. Supplier Opportunism in Buyer-Supplier New Product Development: A China-U.S. Study of Antecedents, Consequences, and Cultural/Institutional Contexts. J. Decis. Sci. Inst. 2015, 46, 403–456. [Google Scholar] [CrossRef]

- Yang, Y. Reframing Buyer-Supplier Agency Problems Beyond the Dyad, Doctoral Dissertation; Arizona State University: Tempe, AZ, USA, 2016. [Google Scholar]

- Lassar, W.M.; Kerr, J.L. Strategy and Control in Supplier–Distributor Relationship: An Agency Perspective. Strateg. Manag. J. 1996, 17, 613–632. [Google Scholar] [CrossRef]

- Wang, G.Y. The Impacts of Free Cash Flows and Agency Costs on Firm Performance. J. Serv. Sci. Manag. 2010, 3, 408–418. [Google Scholar] [CrossRef] [Green Version]

- Jabbary, H.; Hajiha, Z.; Labesha, R.H. Investigation of the Effect of Agency Costs on Firm Performance of Listed Firms in Tehran Stock Exchange. Eur. Online J. Nat. Soc. Sci. 2013, 2, 771–776. [Google Scholar]

- Williamson, O.E. The Economic Institutions of Capitalism: Firms, Markets, Relational Contracting; The Free, Press; Macmillan, Inc.: New York, NY, USA; Collier Macmillan Publisher: London, UK, 1985. [Google Scholar]

- Salas, P.C. The Limits of Bargaining Power Contracts Are Incomplete: Evidence from Experiments. 2014. Available online: https://cla.auburn.edu/economics/assets/File/CorderoBargainingPower.pdf (accessed on 21 November 2021).

- Newton, S.K.; Gilinsky, A.; Jordan, D. Differentiation strategies and winery financial performance: An empirical investigation. Wine Econ. Policy. 2015, 4, 88–97. [Google Scholar] [CrossRef] [Green Version]

- Ashton, R.H. Wine as an Experience Good: Price versus Enjoyment in Blind Tastings of Expensive and Inexpensive Wines. J. Wine Econ. 2014, 9, 171–182. [Google Scholar] [CrossRef]

- Ang, J.S.; Cole, R.A.; Lin, J.W. Agency Costs and Ownership Structure. J. Financ. 2000, 55, 81–106. [Google Scholar] [CrossRef]

- Becker-Blease, J.R.; Kaen, F.R.; Etebari, A.; Baumann, H. Employees, Firm Size and Profitability in U. S. Manufacturing Industries. Invest. Manag. Financ. Innov. 2010, 7, 7–23. [Google Scholar]

- Pervan, M.; Višić, J. Influence of Firm Size on its Business Success. Croat. Oper. Res. Rev. 2012, 3, 213–223. [Google Scholar]

- Akinlo, A.E. Firm Size-Profitability Nexus: Evidence from Panel Data for Nigeria. Econ. Res. 2012, 25, 706–721. [Google Scholar] [CrossRef]

- Dogan, M. Does Firm Size Affect the Firm Profitability? Evidence from Turkey. Res. J. Financ. Account. 2013, 4, 53–59. [Google Scholar]

- Babalola, Y.A. The Effect of Firm Size on Firms’ Profitability in Nigeria. J. Econ. Sustain. Dev. 2013, 4, 90–94. [Google Scholar]

- Benfratello, L.; Piacenza, M.; Sacchetto, S. Taste or reputation: What drives market prices in the wine industry? Estimation of a hedonic model for Italian premium wines. Appl. Econ. 2009, 41, 2197–2209. [Google Scholar] [CrossRef] [Green Version]

- Caracciolo, F.; D’Amino, M.; Di Vita, G.; Pomarici, E.; Dal Bianco, A.; Cembalo, L. Private vs. Collective Wine Reputation. Int. Food Agribus. Manag. Rev. 2016, 19, 191–210. [Google Scholar]

- Eberl, M.; Schwaiger, M. Corporate Reputation: Disentangling the Effects on Financial Performance. Eur. J. Mark. 2005, 39, 838–854. [Google Scholar] [CrossRef]

- Carmeli, A.; Tishler, A. Perceived Organizational Reputation and Organizational Performance: An Empirical Investigation of Industrial Enterprises. Corp. Reput. Rev. 2005, 8, 13–30. [Google Scholar] [CrossRef]

- Sanchez, J.L.F.; Sotorrio, L.L. The Creation of Value through Corporate Reputation. J. Bus. Ethics 2007, 76, 335–346. [Google Scholar] [CrossRef]

- Stuebs, M.; Sun, L. Business Reputation and Labor Efficiency, Productivity, and Cost. J. Bus. Ethics 2010, 96, 265–283. [Google Scholar] [CrossRef]

- Vig, S.; Dumičić, K.; Klopotan, I. The Impact of Reputation on Corporate Financial Performance: Median Regression Approach. Bus. Syst. Res. 2017, 8, 40–58. [Google Scholar] [CrossRef] [Green Version]

- Meuleman, M.; Wright, M.; Manigart, S.; Lockett, A. Private Equity Syndication: Agency Costs, Reputation and Collaboration. J. Bus. Financ. Account. 2009, 36, 616–644. [Google Scholar] [CrossRef]

- Chiles, T.D.; McMackin, J.F. Integrating Variable Risk Preferences, Trust, and Transaction Cost Economics. Acad. Manag. Rev. 1996, 21, 73–99. [Google Scholar] [CrossRef]

- Coelho, F.; Easingwood, C.; Coelho, A. Exploratory evidence of channel performance in single vs. multiple channel strategies. Int. J. Retail Distrib. Manag. 2003, 31, 561–573. [Google Scholar] [CrossRef]

- Beccera, M.; Gupta, A.K. Trust Within the Organization: Integrating the Trust Literatre with Agency Theory and Transaction Costs Economics. Public Adm. Q. 1999, 23, 177–203. [Google Scholar]

- Pospech, P.; Spešna, D. What is the importance of social capital in Czech agriculture? An analysis of selected components. Agric. Econ. 2011, 57, 279–287. [Google Scholar] [CrossRef] [Green Version]

- Stam, W.; Arzlanian, S.; Elfring, T. Social Capital of Entrepreneurs and Small Firm Performance: A Meta-Analysis of Contextual and Methodological Moderators. J. Bus. Ventur. 2014, 29, 152–173. [Google Scholar] [CrossRef]

- Pratono, A.H.; Saputra, R.S.; Pudjibudojo, J.J. Social Capital and Firm Performance: Evidence from Indonesia Small Businesses. Int. J. Econ. Financ. Issues 2016, 6, 47–50. [Google Scholar]

- Agyapong, F.O.; Agyapong, A.; Poku, K. Nexus between Social Capital and Performance of Micro and Small Firms in an Emerging Economy: The Mediating Role of Innovation. Cogent Bus. Manag. 2017, 4, 1309784. [Google Scholar] [CrossRef]

- Storey, D.J. Education, Training and Development Policies and Practices in Medium-Sized Companies in the UK: Do They Raally Influence Firm Performance? Int. J. Manag. Sci. 2002, 30, 249–264. [Google Scholar] [CrossRef]

- Cadot, J. Agency costs of vertical integration–the case of family firms, investor-owned firms and cooperatives in the French wine industry. Agric. Econ. 2015, 46, 187–194. [Google Scholar] [CrossRef]

- Vineyard Register. Available online: www.apprrr.hr (accessed on 20 November 2020).

{kind=link}

| Variable | Acronym | Definition |

|---|---|---|

| Number of Products | nrp | Size of a wine producer is expressed through the number of wine labels (economies of scope) |

| Production Volume | vol | Size of a wine producer is expressed through the production volume in liters (economies of scale) |

| Reputation | rep | Reputation ranges from 1 to 5 on the Likert scale and implies the estimated recognizability of the wine producer on the Croatian wine market |

| Distribution | distr | % of sale through the intermediary |

| Social Capital | sc | Social capital ranges from 1 to 5 on the Likert scale and implies an estimated strength of the impact of the business owner or person in charge of negotiation on the inclusion of wine in the distributor’s offer |

| Specialist Economist | se | Existence of the economic expert, educated for negotiation, marketing, and brand building-(dummy variable) |

| Agency Cost | agc | The difference between the price to the distributor and the average retail price, increased by monitoring cost and expressed as a % of the retail price |

| Revenue per Employee | rpe | Revenues per employee, in kunas |

| Prizes | prizes | Number of prizes won in wine producers competitions |

| Region Dummy | jadran | Regional dummy with value 1 if the wine producers is situated in Jadranska (Adriatic) Hrvatska, 0 if it is in Kontinentalna (Continental) Hrvaska |

| Variable | Acronym | N | Mean | Std. Dev. | Skewness | Kurtosis |

|---|---|---|---|---|---|---|

| Number of Products | nrp | 124 | 9.725806 | 6.364713 | 2.651662 | 12.74236 |

| Production Volume | vol | 124 | 316,209.7 | 1,041,232 | 6.351775 | 46.99786 |

| Reputation | rep | 124 | 3.537634 | 0.955590 | −0.094476 | 2.207173 |

| Distribution | distr | 124 | 79.71774 | 19.39557 | −1.286389 | 4.657992 |

| Social Capital | sc | 124 | 3.975806 | 0.932378 | −0.677155 | 2.907829 |

| Specialist Economist | se | 124 | 0.387097 | 0.489062 | 0.463586 | 1.214912 |

| Agency Cost | agc | 124 | 51.49194 | 7.300458 | 0.513243 | 2.815672 |

| Revenue per Employee | rpe | 124 | 544,493 | 324,841.2 | 3.338189 | 22.23831 |

| Prizes | prizes | 124 | 3.320161 | 2.57224 | 1.171408 | 3.971669 |

| Region Dummy | jadran | 124 | 0.5564516 | 0.4988184 | −0.2272596 | 1.051647 |

| (1) | (2) | (3) | (4) | |

|---|---|---|---|---|

| Variables | rpe | agc | rpe | rpe |

| nrp | 1820 | −0.0223 | 1581 | |

| (9381) | (0.101) | (9925) | ||

| vol | 0.0261 | 6.76 × 10−7 | 0.0334 | |

| (0.0303) | (1.09 × 10−6) | (0.0328) | ||

| rep | 75,649 * | −2.074 *** | 53,359 | |

| (44,436) | (0.725) | (41,851) | ||

| distr | −37,665 | 10.90 *** | 79,507 | |

| (107,969) | (2.944) | (119,464) | ||

| sc | −28,244 | −1.110 | −40,177 | |

| (44,495) | (0.686) | (45,999) | ||

| se | 87,488 | −3.907 *** | 45,501 | |

| (62,283) | (1.113) | (59,158) | ||

| agc | −12,345 *** | −10,745 *** | ||

| (2957) | (3657) | |||

| Constant | 359,278 *** | 56.11 *** | 1.181 × 10−6 *** | 962,210 *** |

| (135,117) | (3.676) | (167,781) | (274,560) | |

| Observations | 124 | 124 | 124 | 124 |

| R-squared | 0.082 | 0.290 | 0.077 | 0.124 |

| (1) | (2) | (3) | (4) | |

|---|---|---|---|---|

| Variables | Prizes | agc | Prizes | Prizes |

| nrp | 0.146 *** | −0.0223 | 0.145 *** | |

| (0.0292) | (0.101) | (0.0285) | ||

| vol | 6.09 × 10−7 *** | 6.76 × 10− | 6.56 × 10−7 *** | |

| (1.41 × 10−7) | (1.09 × 10−6) | (1.32 × 10−7) | ||

| rep | 0.685 *** | −2.074 *** | 0.542 ** | |

| (0.261) | (0.725) | (0.247) | ||

| distr | 0.124 | 10.90 *** | 0.875 | |

| (1.079) | (2.944) | (1.098) | ||

| sc | −0.125 | −1.110 | −0.201 | |

| (0.223) | (0.686) | (0.219) | ||

| se | −0.126 | −3.907 *** | −0.396 | |

| (0.378) | (1.113) | (0.408) | ||

| agc | −0.0860 *** | −0.0689 ** | ||

| (0.0310) | (0.0281) | |||

| Constant | −0.269 | 56.11 *** | 7.752 *** | 3.598 * |

| (1.074) | (3.676) | (1.614) | (1.959) | |

| Observations | 124 | 124 | 124 | 124 |

| R-squared | 0.407 | 0.290 | 0.059 | 0.434 |

| (1) | (2) | (3) | (4) | |

|---|---|---|---|---|

| Variables | rpe | agc | rpe | rpe |

| nrp | 3477 | −0.0569 | 3029 | |

| (8502) | (0.116) | (9140) | ||

| vol | 0.0436 | 3.11 × 10−7 | 0.0460 | |

| (0.0300) | (1.09 × 10−7) | (0.0314) | ||

| rep | 42,165 | −1.374 ** | 31,353 | |

| (44,623) | (0.667) | (43,090) | ||

| distr | 51,754 | 9.033 *** | 122,853 | |

| (117,010) | (2.943) | (125,155) | ||

| sc | −25,435 | −1.169 * | −34,639 | |

| (43,700) | (0.626) | (45,589) | ||

| se | 50,895 | −3.142 *** | 26,167 | |

| (59,577) | (1.154) | (57,249) | ||

| agc | −8588 ** | −7871 ** | ||

| (3291) | (3900) | |||

| 1. Adriatic | 179,029 *** | −3.747 *** | 132,005 ** | 149,533 *** |

| (53,123) | (1.179) | (57,222) | (56,007) | |

| Constant | 288,231 ** | 57.60 *** | 913,574 *** | 741,601 *** |

| (130,575) | (3.720) | (190,293) | (279,154) | |

| Observations | 124 | 124 | 124 | 124 |

| R-squared | 0.141 | 0.341 | 0.111 | 0.162 |

| (1) | (2) | (3) | (4) | |

|---|---|---|---|---|

| Variables | rpe | agc | rpe | rpe |

| srm | 35,273 ** | −1.777 *** | 14,922 | |

| (14,315) | (0.517) | (16,401) | ||

| agc | −12,345 *** | −11,450 *** | ||

| (3880) | (3471) | |||

| Constant | 544,493 *** | 51.53 *** | 1.81 × 106 *** | 1.135 × 106 *** |

| (28,980) | (0.621) | (201,925) | (194,321) | |

| Observations | 124 | 124 | 124 | 124 |

| R-squared | 0.021 | 0.107 | 0.077 | 0.080 |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2022 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Katunar, J.; Mrak, M.K.; Zaninović, V. Implications of Mediated Market Access—Exploring the Nature of Vertical Relationships within the Croatian Wine Industry. Sustainability 2022, 14, 645. https://doi.org/10.3390/su14020645

Katunar J, Mrak MK, Zaninović V. Implications of Mediated Market Access—Exploring the Nature of Vertical Relationships within the Croatian Wine Industry. Sustainability. 2022; 14(2):645. https://doi.org/10.3390/su14020645

Chicago/Turabian StyleKatunar, Jana, Marija Kaštelan Mrak, and Vinko Zaninović. 2022. "Implications of Mediated Market Access—Exploring the Nature of Vertical Relationships within the Croatian Wine Industry" Sustainability 14, no. 2: 645. https://doi.org/10.3390/su14020645

APA StyleKatunar, J., Mrak, M. K., & Zaninović, V. (2022). Implications of Mediated Market Access—Exploring the Nature of Vertical Relationships within the Croatian Wine Industry. Sustainability, 14(2), 645. https://doi.org/10.3390/su14020645