3.1. Green Bond Issuance in V4 Countries

The start of green bond issuance in the V4 countries dates back to 2016 (in Poland). Since then, green bonds have been issued in all V4 countries, with both the number of issues and the value of issues varying. The largest number of issues was carried out in Poland (9 issues) and Hungary (8 issues), followed by the Czech Republic (7 issues), and finally, Slovakia, where only one issue was carried out [

49]. The currency of the green bond issues also differed in each country. In US dollar terms, Poland raised the most funds through green bond issues to the value of USD 5893.81 million, with the Czech Republic raising USD 5582.61 million. In contrast, Hungary’s issuance amounted to USD 3320.73 million and Slovakia’s to only USD 361.38 million [

49]. Green bond issuance across countries also varied by sector. Poland and Hungary were dominated by the government sector, while the Czech Republic and Slovakia were dominated by the corporate sector, mainly non-financial.

The issue of green bonds in Poland took place both in the state sector and in non-financial and financial enterprises. The value of the funds obtained, converted into US dollars, was as follows:

USD 3069.18 million for the state sector;

USD 862.67 million for the non-financial enterprise sector;

USD 720.20 million for the financial enterprise sector.

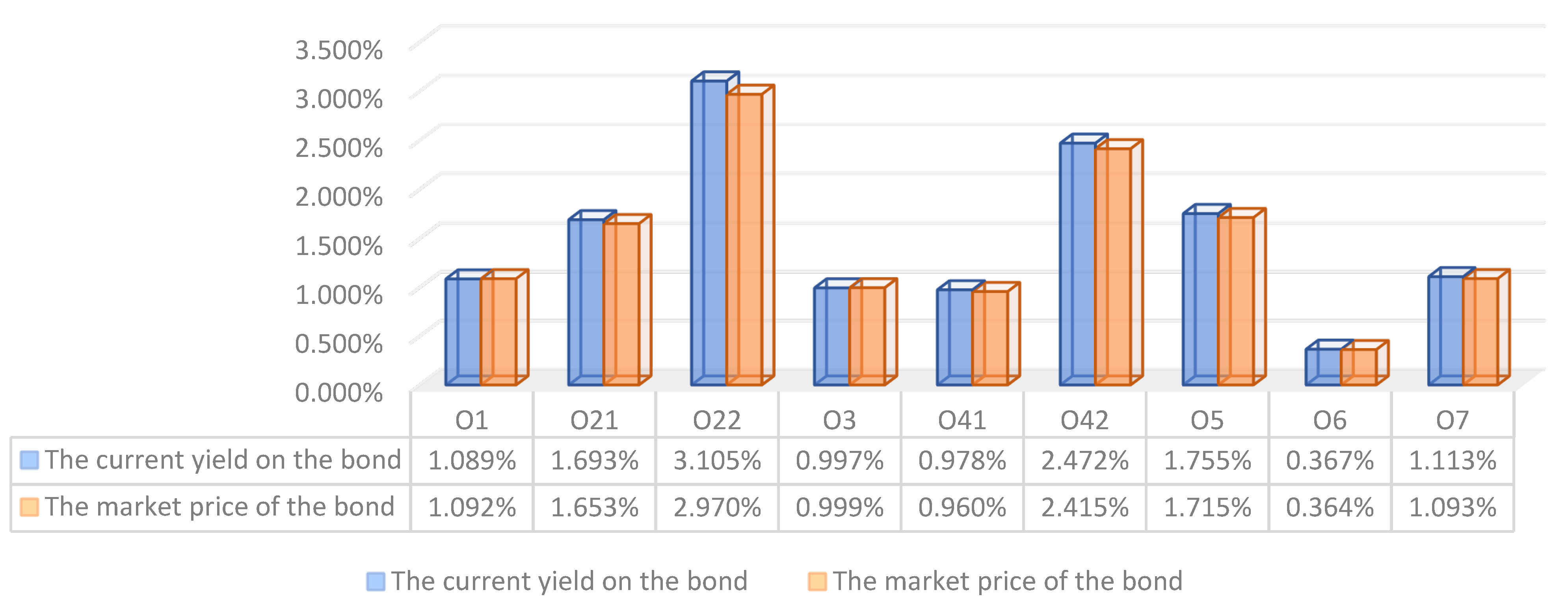

Since 2016, the Polish government has carried out four euro-denominated green bond issues. The first issue of government green bonds took place on 19 December 2016. These were 5-year bonds in which the yield was set at 0.5%. The Polish government raised €750 million ($791.89 million) through the bond issue. Another green bond issue by the Polish government (worth €1 billion, or $1243 million) took place on 7 February 2018. This issue matures on 7 August 2026 and has a coupon rate of 1.13%. The next largest green bond issue to date, conducted on 7 March 2019, enabled the Polish government to raise 50% more capital (USD 1707.06 million) at a cost 0.13% lower than the previous issue (1%). The maturity date of these bonds is 7 March 2029. In contrast, the longest tenor (i.e., the period from the bond issue to the scheduled redemption date) of the green bonds issued by the Polish government is 30 years and relates to the issue conducted on 7 March 2019. As a result of this issue, the Polish government raised €500 million, but with the highest cost of capital (2%) resulting from the coupon.

In addition to the government sector, the main issuers of green bonds in Poland have been non-financial companies, including PKN Orlen and Cyfrowy Polsat. PKN Orlen is a listed company active in energy and mobility based on advanced and clean technologies. The company’s main focus is on renewable energy and modern petrochemicals, as well as the search for innovative solutions in the areas of new mobility, hydrogen energy, and recycling. The company’s main objective is to achieve carbon neutrality in 2050. A natural consequence of the mission undertaken at PKN Orlen is to raise funds by issuing green bonds. PKN Orlen carried out its first and so far only green bond issue (denominated in euro) on 21 May 2021, from which it raised €500 million (USD 607.30 million). The bond yield was set at 1.13%, with a maturity date of 27 May 2028.

Another non-financial company that has issued green bonds in Poland is Cyfrowy Polsat. The company’s core business focuses on the provision of integrated media and telecommunications services in Poland, including satellite, terrestrial and internet television services, mobile and fixed telephony services, data transmission services, and broadband internet access, as well as wholesale services in the inter-operator telecommunications, television, and advertising markets. In December 2021, the company adopted a new programme called Strategy 2023+, which involves expanding its existing operations into a new area—clean energy production. One year prior to the adoption of the new strategy, Cyfrowy Polsat issued green bonds (denominated in the Polish zloty) with a nominal value of PLN 1 billion and with a maturity date of 12 February 2027. The yield on the bonds was determined based on 6m WIBOR plus 165 bps.

A similar yield calculation is represented by green bonds issued by financial companies in Poland. Among green bond issuers in the financial sector, two banks should be singled out: mBank and PKO Bank Polski. mBank was the first fully online bank in Poland. It is currently focusing on implementing innovative solutions, especially within online and mobile banking. In addition, mBank focuses on activities in five strategic segments, which include retail banking, the e-commerce segment, corporate banking, technology, security and data, and employees and organisational culture. mBank’s first and so far only green bond issue took place on 20 September 2021, with a maturity date of 21 September 2027. The bond’s yield is derived from the 3m EURIBOR interest rate, plus 1.25%. As a result of this issue, mBank raised €500 million ($590.65 million).

The last financial company to issue green bonds in Poland is PKO BP Bank. PKO BP is one of the largest and at the same time oldest banks operating in the Polish market. Its activities are based on the idea of sustainable development. PKO BP Bank has implemented a strategy aimed at protecting the environment, as well as a strategy assuming a positive impact on the social environment. In terms of environmental protection, the bank has taken measures to simplify and streamline processes by reducing paper documentation (optimising paper consumption) and by reducing energy consumption. In addition, the bank has implemented new procedures related to space optimisation and efficient waste management. Furthermore, as part of its cooperation with the social environment, PKO BP Bank has launched sponsorship and charity activities.

PKO BP Bank carried out two green bond issues. The first issue took place on 10 June 2019, maturing on 30 September 2024, with the bank raising PLN 250m (USD 65.70 million). The bond yield was set at 3m WIBOR, plus 0.6%. PKO BP’s second green bond issue took place on 27 November 2019 and matures on 2 December 2024. The cost per interest payment (coupon) was set at 3m WIBOR, plus 51 bps. The execution of the issue enabled the bank to raise PLN 250m (USD 63.85 million).

The second country in the V4 countries in terms of green bonds issued is the Czech Republic. In the Czech Republic, cash was raised exclusively for the corporate sector, with a significant portion for the non-financial sector (USD 4989.05 million), while only USD 593.56 million was raised for the financial sector.

The main issuer of green bonds in the Czech Republic is CTP Group N.V., which operates in the logistics and industrial real estate sector in Central and Eastern Europe. Its structure includes two economically related companies: CTP Property B.V. and CTP Invest spol., s r.o. CTP Property B.V. is involved in property management, while CTP Invest spol., s r.o. is a commercial property developer and asset manager. The portfolio of CTP Invest spol., s r.o. consists of 96 premium industrial business parks with a total leasable area of more than 5.5 million square metres. The company’s portfolio includes both industrial parks comprising warehouse space and other space necessary for business development, as well as business parks. The business parks focus on office space, office services, and shops located in the city centres of Central and Eastern Europe.

CTP Group N.V.’s activities are geared towards sustainability and take into account the impact on the environment and the surroundings in which it operates. The entire portfolio of the CTP N.V. Group is BREEAM-certified (Building Research Establishment Environmental Assessment Method), confirming the implementation of the sustainability concept for infrastructure and buildings. Consequently, the company’s financing is also based on the concept of sustainability, as the company has been raising cash through the issue of green bonds, denominated in euros, for the past three years. In 2020, CTP Group N.V. issued 2 series of green bonds with a total issue value of €1050 million (USD 1234.38 million), i.e., €650 million (USD 757.80 million) for the 5-year bond and €400 million (USD 476.58 million) for the 3-year bond. The yield on the €650 million issue value bond was set at 2.1250% and its maturity date is October 2025. In contrast, the yield on the bond with an issue value of €400 million was set at 0.0625%, and its maturity date falls in November 2025.

In 2021, CTP Group N.V. continued to issue green bonds and issued 3 series of bonds. The first issue took place on 18 February 2021. The issue value of the bonds issued with a maturity date of 18 February 2027 was EUR 500 million (USD 603 million) and their yield was set at 0.75%. The next green bond issue took place on 21 June 2021 and was divided into two equal tranches with a nominal value of €500 million (USD 593.10 million) each. The different tranches differed in maturity and interest rate level. The maturity of the first tranche (with a yield of 0.5%) was set as 21 June 2025, while the maturity of the second tranche (with a yield of 1.25%) was set as 21 June 2029. The tenor of the bonds for this issue was 4 and 8 years. A similar procedure also applied to the next green bond issue, which took place on 27 September 2021. The tenor of the issue was €1 billion (USD 1171.80 million) and was also divided into two tranches with issue values of €500 million. This time, the tenor of the bonds issued was the longest, at five and 10 years. The yield on the five-year green bond was set at 0.625% while the yield on the 10-year bond was set at 1.50%.

The procedure for financing CTP N.V.’s operations with green bonds was also maintained in 2022. The most recent green bond issue, with a maturity date of 20 January 2026, took place on 6 January 2022. During this issue, the CTP N.V. group raised EUR 700 million (USD 793.67 million) and the cost of this issue, resulting from the coupon, was set at 0.875%.

In addition to CTP N.V., another issuer of green bonds in the Czech Republic was Ceska Sporitelna AS, part of the Erste Group, which operates in Central Europe. Ceska Sporitelna AS is one of the oldest banks in the Czech market, offering banking and other financial market services to individuals, small and medium-sized enterprises, and large corporations, as well as cities and municipalities. The bank’s activities are guided by the principles of sustainable development. The bank adapts its business activities to the environment in which it operates. Above all, it supports the development of local communities, strives to improve education, supports the elderly and people with intellectual disabilities by adapting its services to people with different types of disabilities, and prevents the spread of drug addiction by taking preventive measures. The first and so far only green bond issue was carried out by Ceska Sporitelna AS Bank on 13 September 2021, through which it raised €500 million (USD 593.56 million). The maturity date of this issue was set for 13 September 2028 and the bond yield was set at 0.50%.

Hungary is the third country in the V4 countries in terms of green bond issuance. Green bond issuance in Hungary has taken place both in the state sector and in non-financial and financial companies. The value of funds raised, in US dollar terms, was as follows:

USD 2858.33 million for the state sector;

USD 300 million for the financial enterprise sector;

USD 162.40 million for the non-financial corporate sector.

Since 2020, the Hungarian government has carried out six green bond issues, denominated in both Hungarian forints and the euro, US dollars, Japanese yen, and Chinese yuan. Hungary’s first government green bond issue took place on 5 June 2020. The tenor of this issue is 15 years and the yield was set at 1.75%. Through the issue, the Hungarian government raised €1500 million (USD 1643.10 million). Another issue was denominated in Japanese yen and took place on 18 September 2020. The value of the issue was 40 million Japanese yen (USD 376.79 million). The issue was divided into three tranches, differentiated by value, tenor, and interest rate (

Table 4).

Two more green bond issues were carried out by the Hungarian government in 2021. The first issue, through which the government raised 30 million Hungarian forints (USD 162 million), took place on 22 April 2021. The maturity date of the bond was set for 28 April 2051 (the tenor is 30 years). The bond yield on this issue is 4%. In the same year, the Hungarian government also raised USD 157 million through another green bond issue. The issue took place on 14 December 2021 and was denominated in Chinese yuan. The tenor was set at three years and the yield was 3.28%.

A few weeks later (26 January 2022), the Hungarian government conducted another green bond issue with maturity set for 27 May 2032. The yield on the bonds issued was 4.50%. As a result of the issue, the government raised 20,799.98 million Hungarian forints (USD 66.87 million).

Hungary’s most recent government green bond issue took place on 25 February 2022 for a total of 59.30 million Japanese yen (USD 514.99 million). Like the previous issue denominated in Japanese yen, the current issue was also divided into three tranches, differentiated in terms of value, tenor, and interest rate (

Table 5).

In addition to the government sector, two companies from the corporate sector have also issued green bonds in Hungary. The first issue was carried out by Futureal, a group focusing on the real estate market in Hungary, Poland and the UK. Futureal is a group comprising three companies:

- -

Futureal—which develops retail properties;

- -

Cordia—which is a developer of residential properties;

- -

HelloParks—which develops industrial and logistics facilities.

In addition to its core business, the Futureal Group is also active in such areas as fund management, investment in public and private bonds, and factoring. The company’s mission is to implement the principles of sustainable development, which it does by:

- -

Minimising paper consumption through the use of technological improvements;

- -

Creating a green environment;

- -

Encouraging healthy eating;

- -

Selective waste collection;

- -

Providing filtered, clean water throughout offices;

- -

Providing electric car chargers, bicycle storage, and changing facilities to promote environmentally friendly transport.

Futureal Group’s first and so far only green bond issue raised 50 million Hungarian forints (USD 162.40 million). The bond matures on 23 March 2031 and has a yield of 4%.

The second company to issue green bonds on the Hungarian market is the Bank of China (Hungarian Branch). The bank was opened in December 2014 and has been an active participant in the Hungarian market since then. The Bank of China (Hungarian Branch) issued a green bond (denominated in US dollars) on 16 February 2022. The tenor of the bond was 2 years and the bond yield was set at 1.62%. With this issue, the Bank of China (Hungarian Branch) raised USD 300 million.

The smallest green bond issuance in the V4 countries was recorded in Slovakia, where only one issue took place. The issuer of the bond is Tatra Banka, a leader in financial innovation in the Slovak market. The bank’s strategy focuses on customer value-oriented innovation. From the green bond issue conducted on 23 April 2021 (maturing on 23 April 2028), the bank raised EUR 300 million (USD 361.38 million). The yield of the bond was 0.5%.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}