To Use or Not to Use: It Is a Question—An Empirical Study on the Adoption of Mobile Finance

Abstract

:1. Introduction

2. Theoretical Background

2.1. Fintech and Mobile Finance

2.2. UTAUT

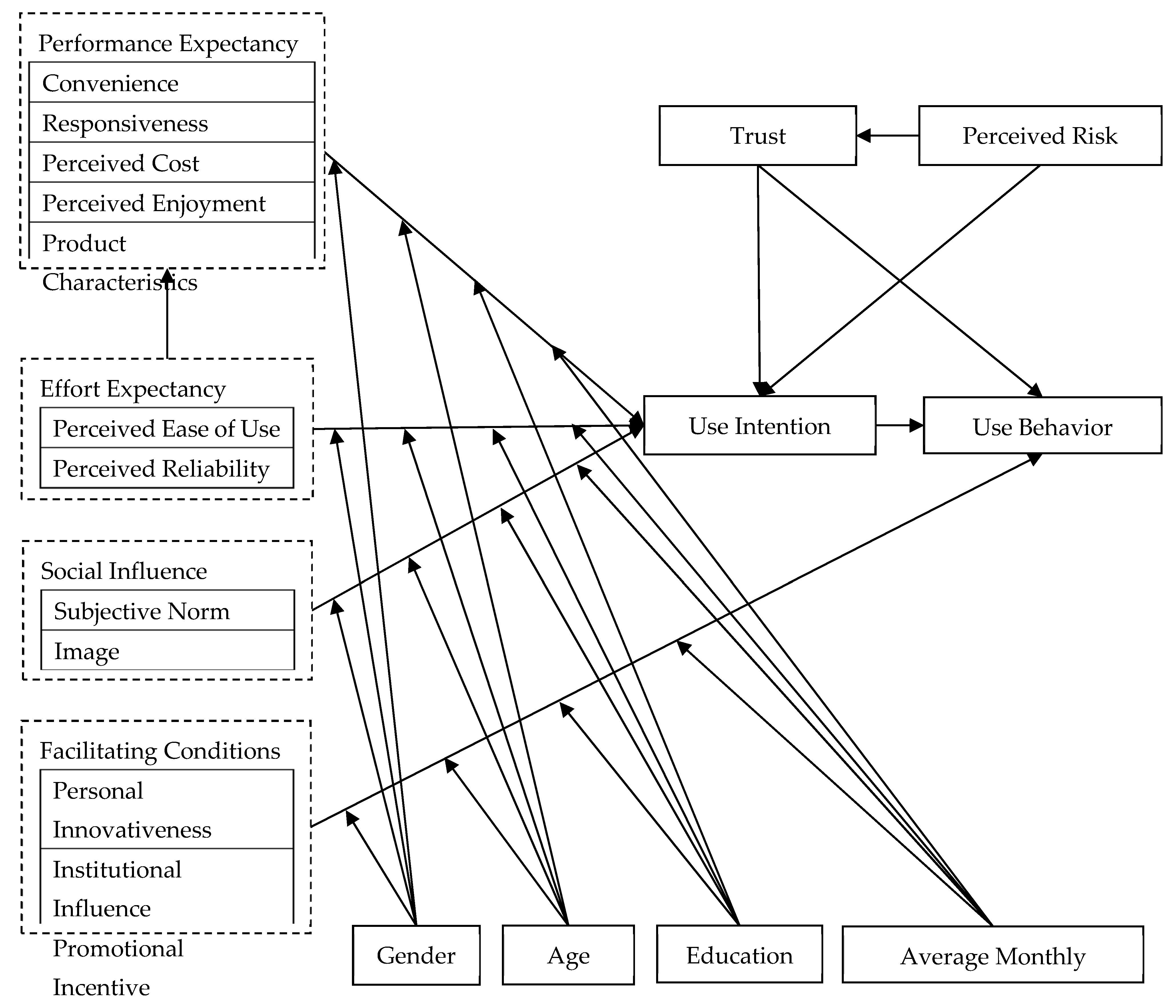

3. Research Model and Hypotheses

3.1. Performance Expectancy

3.1.1. Convenience

3.1.2. Responsiveness

3.1.3. Perceived Cost

3.1.4. Perceived Enjoyment

3.1.5. Product Characteristics

3.2. Effort Expectancy

3.2.1. Perceived Ease of Use

3.2.2. Perceived Reliability

3.3. Social Influence

3.3.1. Subjective Norm

3.3.2. Image

3.4. Facilitating Conditions

3.4.1. Personal Innovativeness

3.4.2. Institutional Influence

3.4.3. Promotional Incentive

3.5. Trust

3.6. Perceived Risk

3.7. Use Intention and Use Behavior

3.8. Moderate Variable

4. Research Methodology

4.1. Measurement

4.2. Data

4.3. Profile of Participants

4.4. Nonresponse Bias

4.5. Common Method Bias

5. Result

5.1. Measurement Model

5.2. Structural Model

5.2.1. Model Fitness

5.2.2. Assessment of Construct Relations

5.2.3. Users Versus Non-Users

6. Conclusion and Contribution

6.1. Key Findings

6.2. Contribution and Implication

6.2.1. Theoretical Contributions

6.2.2. Practical Implications

6.3. Limitation and Future Research Direction

Author Contributions

Funding

Informed Consent Statement

Data Availability Statement

Conflicts of Interest

Appendix A. Measurement items

{kind=link}

| Constructs | Item | Source | |

|---|---|---|---|

| Performance Expectancy | Convenience | 3 items | Hoehle et al. [37]; Mansour [36] |

| Responsiveness | 2 items | Parasuraman et al. [38]; Jun & Cai [39] | |

| Perceived Cost | 3 items | Zhou [40] | |

| Perceived Enjoyment | 2 items | Zhou [42]; Alalwan et al. [30] | |

| Product Characteristics | 3 items | These items are developed by ourselves. | |

| Effort Expectancy | Perceived Ease of Use | 3 items | Yoon & Steege [45] |

| Perceived Reliability | 3 items | Hanafizadeh et al. [48] | |

| Social Influence | Subjective Norm | 3 items | Liebana-Cabanillas [50] |

| Image | 3 items | Liebana-Cabanillas [50] | |

| Facilitating Conditions | Personal Innovativeness | 3 items | Tun-Pin et al. [55] |

| Institutional Influence | 2 items | Ammar & Ahmed [80] | |

| Promotional Incentive | 2 items | Zhao, Anong, & Zhang [81] | |

| Trust | 4 items | Wang et al. [60] | |

| Perceived Risk | 3 items | Gefen [66] | |

| Use Intention | 3 items | Venkatesh [29] | |

| Use Behavior | 2 items | Venkatesh [29] | |

Appendix B. The First Goodness of Fit Indices of the Structural Model

| Fit Indices | The Proposed Model Fit | Benchmark |

|---|---|---|

| df | 344 | |

| Chi-square () | 979.594 | |

| 2.848 | <3 | |

| GFI | 0.826 | >0.9 |

| AGFI | 0.790 | >0.8 |

| NFI | 0.857 | >0.90 |

| NNFI | 0.895 | >0.90 |

| CFI | 0.890 | >0.90 |

| IFI | 0.910 | >0.90 |

| RMR | 0.119 | <0.05 |

| RMSEA | 0.075 | <0.08 |

References

- Lorenz, E.; Pommet, S. Mobile money, inclusive finance and enterprise innovativeness: An analysis of East African nations. Ind. Innov. 2020, 28, 136–159. [Google Scholar] [CrossRef]

- Hasan, M.; Le, T.; Hoque, A. How does financial literacy impact on inclusive finance? Financ. Innov. 2021, 7, 401–423. [Google Scholar] [CrossRef]

- Arslanian, H.; Fischer, F. The Future of Finance: The Impact of FinTech, AI, and Crypto on Financial Services; Springer: Berlin, Germany, 2019. [Google Scholar]

- Arslanian, H.; Fischer, F. Fintech and the Future of the Financial Ecosystem. In The Future of Finance: The Impact of FinTech, AI, and Crypto on Financial Services; Arslanian, H., Fischer, F., Eds.; Springer International Publishing: Cham, Switzerland, 2019; pp. 201–216. [Google Scholar] [CrossRef]

- Corrado, G.; Corrado, L. Inclusive finance for inclusive growth and development. Curr. Opin. Environ. Sustain. 2017, 24, 19–23. [Google Scholar] [CrossRef]

- Liu, T.; He, G.; Turvey, C.G. Inclusive Finance, Farm Households Entrepreneurship, and Inclusive Rural Transformation in Rural Poverty-stricken Areas in China. Emerg. Mark. Finance Trade 2021, 57, 1929–1958. [Google Scholar] [CrossRef]

- Dorfleitner, G.; Hornuf, L. FinTech Business Models. In FinTech and Data Privacy in Germany: An Empirical Analysis with Policy Recommendations; Dorfleitner, G., Hornuf, L., Eds.; Springer International Publishing: Cham, Switzerland, 2019; pp. 85–106. [Google Scholar]

- Dai, S.; Taube, M. The long tail thesis. Chin. Manag. Stud. 2019, 14, 433–454. [Google Scholar] [CrossRef]

- Senyo, P.K.; Karanasios, S.; Gozman, D.; Baba, M. FinTech ecosystem practices shaping financial inclusion: The case of mobile money in Ghana. Eur. J. Inf. Syst. 2021, 31, 112–127. [Google Scholar] [CrossRef]

- Yiteng, Y. A Review on the Effect of Digital Inclusive Finance on Income Disparity. In Proceedings of the 7th International Conference on Social Sciences and Economic Development (ICSSED 2022), Wuhan, China, 29 April 2022; pp. 591–594. [Google Scholar]

- Hasan, M.; Yajuan, L.; Khan, S. Promoting China’s Inclusive Finance Through Digital Financial Services. Glob. Bus. Rev. 2020, 23, 984–1006. [Google Scholar] [CrossRef]

- Riyanto, A.; Primiana, I.; Yunizar; Azis, Y. Disruptive Technology: The Phenomenon of FinTech towards Conventional Banking in Indonesia. IOP Conf. Series: Mater. Sci. Eng. 2018, 407, 012104. [Google Scholar] [CrossRef]

- Senyo, P.; Osabutey, E.L. Unearthing antecedents to financial inclusion through FinTech innovations. Technovation 2020, 98, 102155. [Google Scholar] [CrossRef]

- Allen, F.; Gu, X.; Jagtiani, J. A Survey of Fintech Research and Policy Discussion. Rev. Corp. Finance 2021, 1, 259–339. [Google Scholar] [CrossRef]

- Schierz, P.G.; Schilke, O.; Wirtz, B.W. Understanding consumer acceptance of mobile payment services: An empirical analysis. Electron. Commer. Res. Appl. 2010, 9, 209–216. [Google Scholar] [CrossRef]

- Makanyeza, C. Determinants of consumers’ intention to adopt mobile banking services in Zimbabwe. Int. J. Bank Mark. 2017, 35, 997–1017. [Google Scholar] [CrossRef]

- Milian, E.Z.; Spinola, M.D.M.; de Carvalho, M.M. Fintechs: A literature review and research agenda. Electron. Commer. Res. Appl. 2019, 34, 100833. [Google Scholar] [CrossRef]

- Gomber, P.; Koch, J.-A.; Siering, M. Digital Finance and FinTech: Current research and future research directions. J. Bus. Econ. 2017, 87, 537–580. [Google Scholar] [CrossRef]

- Liu, J.; Li, X.; Wang, S. What have we learnt from 10 years of fintech research? A scientometric analysis. Technol. Forecast. Soc. Chang. 2020, 155, 120022. [Google Scholar] [CrossRef]

- Zhichao, X.; Han-Teng, L.; Chung-Lien, P.; Wenjun, M. Exploring the Research Fronts of Fintech: A Scientometric Analysis. In Proceedings of the 5th International Conference on Financial Innovation and Economic Development (ICFIED 2020), Sanya, China, 11 March 2020; pp. 5–11. [Google Scholar]

- Daragmeh, A.; Sági, J.; Zéman, Z. Continuous Intention to Use E-Wallet in the Context of the COVID-19 Pandemic: Inte-grating the Health Belief Model (HBM) and Technology Continuous Theory (TCT). J. Open Innov. Technol. Mark. Complex. 2021, 7, 132. [Google Scholar] [CrossRef]

- Baganzi, R.; Lau, A.K.W. Examining Trust and Risk in Mobile Money Acceptance in Uganda. Sustainability 2017, 9, 2233. [Google Scholar] [CrossRef]

- Chen, W.-C.; Chen, C.-W.; Chen, W.-K. Drivers of Mobile Payment Acceptance in China: An Empirical Investigation. Information 2019, 10, 384. [Google Scholar] [CrossRef]

- Murendo, C.; Wollni, M.; De Brauw, A.; Mugabi, N. Social Network Effects on Mobile Money Adoption in Uganda. J. Dev. Stud. 2017, 54, 327–342. [Google Scholar] [CrossRef]

- Mswahili, A. Factors for Acceptance and Use of Mobile Money Interoperability Services. J. Inform. 2022, 2, 1993–2714. [Google Scholar]

- Ngubelanga, A.; Duffett, R. Modeling Mobile Commerce Applications’ Antecedents of Customer Satisfaction among Millen-nials: An Extended TAM Perspective. Sustainability 2021, 13, 5973. [Google Scholar] [CrossRef]

- Venkatesh, V.; Morris, M.G.; Davis, G.B.; Davis, F.D. User Acceptance of Information Technology: Toward a Unified View. MIS Q. 2003, 27, 425–478. [Google Scholar] [CrossRef]

- Venkatesh, V.; Zhang, X. Unified Theory of Acceptance and Use of Technology: U.S. Vs. China. J. Glob. Inf. Technol. Manag. 2010, 13, 5–27. [Google Scholar] [CrossRef]

- Venkatesh, V.; Thong, J.Y.L.; Xu, X. Consumer Acceptance and Use of Information Technology: Extending the Unified Theory of Acceptance and Use of Technology. MIS Q. 2012, 36, 157–178. [Google Scholar] [CrossRef]

- Alalwan, A.; Dwivedi, Y.K.; Rana, N. Factors influencing adoption of mobile banking by Jordanian bank customers: Extending UTAUT2 with trust. Int. J. Inf. Manag. 2017, 37, 99–110. [Google Scholar] [CrossRef]

- Queiroz, M.M.; Wamba, S.F. Blockchain adoption challenges in supply chain: An empirical investigation of the main drivers in India and the USA. Int. J. Inf. Manag. 2018, 46, 70–82. [Google Scholar] [CrossRef]

- Yang, Y.; Liu, Y.; Li, H.; Yu, B. Understanding perceived risks in mobile payment acceptance. Ind. Manag. Data Syst. 2015, 115, 253–269. [Google Scholar] [CrossRef]

- Oliveira, T.; Faria, M.; Thomas, M.A.; Popovič, A. Extending the understanding of mobile banking adoption: When UTAUT meets TTF and ITM. Int. J. Inf. Manag. 2014, 34, 689–703. [Google Scholar] [CrossRef]

- Tarhini, A.; El-Masri, M.; Ali, M.; Serrano, A. Extending the UTAUT model to understand the customers’ acceptance and use of internet banking in Lebanon. Inf. Technol. People 2016, 29, 830–849. [Google Scholar] [CrossRef]

- Laforet, S.; Li, X. Consumers’ attitudes towards online and mobile banking in China. Int. J. Bank Mark. 2005, 23, 362–380. [Google Scholar] [CrossRef]

- Mansour, I.H.F.; Eljelly, A.M.; Abdullah, A.M. Consumers’ attitude towards e-banking services in Islamic banks: The case of Sudan. Rev. Int. Bus. Strat. 2016, 26, 244–260. [Google Scholar] [CrossRef]

- Hoehle, H.; Scornavacca, E.; Huff, S. Three decades of research on consumer adoption and utilization of electronic banking channels: A literature analysis. Decis. Support Syst. 2012, 54, 122–132. [Google Scholar] [CrossRef]

- Parasuraman, A.; Zeithaml, V.A.; Berry, L.L. A Conceptual Model of Service Quality and Its Implications for Future Research. J. Mark. 1985, 49, 41–50. [Google Scholar] [CrossRef]

- Jun, M.; Cai, S. The key determinants of Internet banking service quality: A content analysis. Int. J. Bank Mark. 2001, 19, 276–291. [Google Scholar] [CrossRef]

- Zhou, T. An Empirical Examination of Initial Trust in Mobile Payment. Wirel. Pers. Commun. 2014, 77, 1519–1531. [Google Scholar] [CrossRef]

- Wessels, L.; Drennan, J. An investigation of consumer acceptance of M-banking. Int. J. Bank Mark. 2010, 28, 547–568. [Google Scholar] [CrossRef]

- Zhou, T. An empirical examination of continuance intention of mobile payment services. Decis. Support Syst. 2013, 54, 1085–1091. [Google Scholar] [CrossRef]

- Verkijika, S.F. Factors influencing the adoption of mobile commerce applications in Cameroon. Telemat. Inform. 2018, 35, 1665–1674. [Google Scholar] [CrossRef]

- Davis, F.D.; Bagozzi, R.P.; Warshaw, P.R. User Acceptance of Computer Technology: A Comparison of Two Theoretical Models. Manag. Sci. 1989, 35, 982–1003. [Google Scholar] [CrossRef]

- Yoon, H.S.; Steege, L.M.B. Development of a quantitative model of the impact of customers’ personality and perceptions on Internet banking use. Comput. Hum. Behav. 2013, 29, 1133–1141. [Google Scholar] [CrossRef]

- Upadhyay, P.; Jahanyan, S. Analyzing user perspective on the factors affecting use intention of mobile based transfer payment. Internet Res. 2016, 26, 38–56. [Google Scholar] [CrossRef]

- Shaikh, A.A.; Karjaluoto, H. Mobile banking adoption: A literature review. Telemat. Inform. 2015, 32, 129–142. [Google Scholar] [CrossRef]

- Hanafizadeh, P.; Behboudi, M.; Koshksaray, A.A.; Tabar, M.J.S. Mobile-banking adoption by Iranian bank clients. Telemat. Inform. 2014, 31, 62–78. [Google Scholar] [CrossRef]

- Chemingui, H.; Ben Lallouna, H. Resistance, motivations, trust and intention to use mobile financial services. Int. J. Bank Mark. 2013, 31, 574–592. [Google Scholar] [CrossRef]

- Liébana-Cabanillas, F.; Sánchez-Fernández, J.; Muñoz-Leiva, F. Antecedents of the adoption of the new mobile payment systems: The moderating effect of age. Comput. Hum. Behav. 2014, 35, 464–478. [Google Scholar] [CrossRef]

- Oliveira, T.; Thomas, M.; Baptista, G.; Campos, F. Mobile payment: Understanding the determinants of customer adoption and intention to recommend the technology. Comput. Hum. Behav. 2016, 61, 404–414. [Google Scholar] [CrossRef]

- Zhou, T.; Lu, Y.; Wang, B. Integrating TTF and UTAUT to explain mobile banking user adoption. Comput. Hum. Behav. 2010, 26, 760–767. [Google Scholar] [CrossRef]

- Rogers, E.M.; Singhal, A.; Quinlan, M.M. Diffusion of innovations. In An Integrated Approach to Communication Theory and Research; Routledge: London, UK, 2014; pp. 432–448. [Google Scholar]

- Patil, P.; Tamilmani, K.; Rana, N.P.; Raghavan, V. Understanding consumer adoption of mobile payment in India: Extending Meta-UTAUT model with personal innovativeness, anxiety, trust, and grievance redressal. Int. J. Inf. Manag. 2020, 54, 102144. [Google Scholar] [CrossRef]

- Tun-Pin, C.; Keng-Soon, W.C.; Yen-San, Y.; Pui-Yee, C.; Hong-Leong, J.T.; Shwu-Shing, N. An adoption of fintech service in Malaysia. South East Asia J. Contemp. Bus. 2019, 18, 134–147. [Google Scholar]

- Chiu, I.H.-Y. A new era in fintech payment innovations? A perspective from the institutions and regulation of payment systems. Law Innov. Technol. 2017, 9, 190–234. [Google Scholar] [CrossRef]

- Nwogugu, M.I. Earnings Management, Fintech-Driven Incentives and Sustainable Growth: On Complex Systems, Legal and Mechanism Design Factors; Routledge: London, UK, 2019. [Google Scholar]

- Mallat, N. Exploring consumer adoption of mobile payments—A qualitative study. J. Strat. Inf. Syst. 2007, 16, 413–432. [Google Scholar] [CrossRef]

- Meyliana, M.; Fernando, E.; Surjandy, S. The Influence of Perceived Risk and Trust in Adoption of FinTech Services in Indonesia. CommIT (Commun. Inf. Technol.) J. 2019, 13, 31–37. [Google Scholar] [CrossRef]

- Wang, Z.; Guan, Z.; Hou, F.; Li, B.; Zhou, W. What determines customers’ continuance intention of FinTech? Evidence from YuEbao. Ind. Manag. Data Syst. 2019, 119, 1625–1637. [Google Scholar] [CrossRef]

- Jünger, M.; Mietzner, M. Banking goes digital: The adoption of FinTech services by German households. Financ. Res. Lett. 2020, 34, 101260. [Google Scholar] [CrossRef]

- Bauer, R.A. Consumer Behavior as Risk. Marketing: Critical Perspectives on Business Management; Routledge: London, UK, 2001; Volume 3, p. 13. [Google Scholar]

- Ryu, H.-S. Understanding Benefit and Risk Framework of Fintech Adoption: Comparison of Early Adopters and Late Adopters. In Proceedings of the 51st Hawaii International Conference on System Sciences, Hilton Waikoloa Village, HI, USA, 3–6 January 2018; pp. 3864–3873. [Google Scholar]

- Tang, K.L.; Ooi, C.K.; Chong, J.B. Perceived Risk Factors Affect Intention to Use FinTech. J. Account. Finance Emerg. Econ. 2020, 6, 453–463. [Google Scholar] [CrossRef]

- Narteh, B.; Mahmoud, M.A.; Amoh, S. Customer behavioural intentions towards mobile money services adoption in Ghana. Serv. Ind. J. 2017, 37, 426–447. [Google Scholar] [CrossRef]

- Gefen, D.; Karahanna, E.; Straub, D.W. Trust and TAM in Online Shopping: An Integrated Model. MIS Q. 2003, 27, 51–90. [Google Scholar] [CrossRef]

- Chen, Y.-C.; Shang, R.-A.; Shu, C.-Y.; Lin, C.-K. The Effects of Risk and Hedonic Value on the Intention to Purchase on Group Buying Website: The Role of Trust, Price and Conformity Intention. Univers. J. Manag. 2015, 3, 246–256. [Google Scholar] [CrossRef]

- Taylor, S.; Todd, P.A. Understanding Information Technology Usage: A Test of Competing Models. Inf. Syst. Res. 1995, 6, 144–176. [Google Scholar] [CrossRef]

- Shaikh, A.A.; Karjaluoto, H. Mobile banking services continuous usage--case study of Finland. In Proceedings of the 2016 49th Hawaii International Conference on System Sciences (HICSS), Koloa, HI, USA, 5–8 January 2016; pp. 1497–1506. [Google Scholar]

- Leong, L.-Y.; Hew, T.-S.; Tan, G.W.-H.; Ooi, K.-B. Predicting the determinants of the NFC-enabled mobile credit card acceptance: A neural networks approach. Expert Syst. Appl. 2013, 40, 5604–5620. [Google Scholar] [CrossRef]

- Ryu, H.-S. What makes users willing or hesitant to use Fintech? The moderating effect of user type. Ind. Manag. Data Syst. 2018, 118, 541–569. [Google Scholar] [CrossRef]

- Brislin, R.W. The wording and translation of research instruments. In Field Methods in Cross-Cultural Research; Cross-cultural research and methodology series; Sage Publications, Inc.: Thousand Oaks, CA, USA, 1986; Volume 8, pp. 137–164. [Google Scholar]

- Hair, J.F. Multivariate Data Analysis: An Overview. In International Encyclopedia of Statistical Science; Lovric, M., Ed.; Springer: Berlin/Heidelberg, Germany, 2011; pp. 904–907. [Google Scholar]

- Armstrong, J.S.; Overton, T.S. Estimating Nonresponse Bias in Mail Surveys. J. Mark. Res. 1977, 14, 396–402. [Google Scholar] [CrossRef]

- Podsakoff, P.M.; Organ, D.W. Self-Reports in Organizational Research: Problems and Prospects. J. Manag. 1986, 12, 531–544. [Google Scholar] [CrossRef]

- Mattila, A.S.; Enz, C.A. The Role of Emotions in Service Encounters. J. Serv. Res. 2002, 4, 268–277. [Google Scholar] [CrossRef]

- Pavlou, P.A.; El Sawy, O.A. From IT Leveraging Competence to Competitive Advantage in Turbulent Environments: The Case of New Product Development. Inf. Syst. Res. 2006, 17, 198–227. [Google Scholar] [CrossRef]

- Fornell, C.; Larcker, D.F. Structural equation models with unobservable variables and measurement error: Algebra and statistics. J. Mark. Res. 1981, 18, 382–388. [Google Scholar] [CrossRef]

- Stone, R.N.; Grønhaug, K. Perceived Risk: Further Considerations for the Marketing Discipline. Eur. J. Mark. 1993, 27, 39–50. [Google Scholar] [CrossRef]

- Ammar, A.; Ahmed, E.M. Factors influencing Sudanese microfinance intention to adopt mobile banking. Cogent Bus. Manag. 2016, 3, 1154257. [Google Scholar] [CrossRef]

- Zhao, H.; Anong, S.T.; Zhang, L. Understanding the impact of financial incentives on NFC mobile payment adoption. Int. J. Bank Mark. 2019, 37, 1296–1312. [Google Scholar] [CrossRef]

| Variable | Size | Percentage | |

|---|---|---|---|

| Gender | Male | 182 | 52.3% |

| Female | 166 | 47.7% | |

| Age | 18–25 | 13 | 3.7% |

| 26–30 | 68 | 19.5% | |

| 31–40 | 230 | 66.1% | |

| 41–50 | 27 | 7.8% | |

| More than 50 | 10 | 2.9% | |

| Education | College | 22 | 6.3% |

| Bachelor | 152 | 43.7% | |

| Master’s degree and above | 174 | 50% | |

| Average Monthly Income | Less than USD 724.91 | 37 | 10.6% |

| USD 724.91–1449.82 | 139 | 39.9% | |

| USD 1449.83–2899.64 | 106 | 30.5% | |

| USD 2899.65–7249.11 | 59 | 17% | |

| More than USD 7249.11 | 7 | 2% | |

| Use Hours | Less than 5 years | 177 | 50.9% |

| More than 5 years | 68 | 19.5% | |

| Never used | 103 | 29.6% | |

| Use Frequency | Less than once a month | 114 | 32.8% |

| At least once a month | 120 | 34.5% | |

| At least once a week | 58 | 16.7% | |

| At least once a day | 56 | 16.1% |

| Levene’s Test | t-Test for Equality of Means | |||||

|---|---|---|---|---|---|---|

| Test Variable | F | Sig. | t | Sig. (2-Tailed) | 95% Confidence Interval of the Difference | |

| Lower | Upper | |||||

| Performance Expectancy | 0.049 | 0.824 | 0.593 | 0.553 | −0.151 | 0.282 |

| 0.594 | 0.553 | −0.151 | 0.282 | |||

| Effort Expectancy | 0.999 | 0.318 | −10.448 | 0.149 | −0.496 | 0.075 |

| −10.351 | 0.179 | −0.518 | 0.097 | |||

| Social Influence | 0.345 | 0.558 | −0.790 | 0.430 | −0.441 | 0.188 |

| −0.768 | 0.444 | −0.452 | 0.199 | |||

| Facilitating Conditions | 0.454 | 0.501 | −0.406 | 0.685 | −0.303 | 0.199 |

| −0.408 | 0.684 | −0.302 | 0.198 | |||

| Trust | 20.640 | 0.105 | −0.299 | 0.765 | −0.330 | 0.243 |

| −0.279 | 0.781 | −0.352 | 0.265 | |||

| Perceived Risk | 0.124 | 0.725 | 10.118 | 0.264 | −0.130 | 0.473 |

| 10.087 | 0.279 | −0.140 | 0.483 | |||

| Use intention | 20.371 | 0.125 | −0.354 | 0.723 | −0.413 | 0.286 |

| −0.341 | 0.734 | −0.428 | 0.302 | |||

| Use Behavior | 0.487 | 0.486 | 0.328 | 0.743 | −0.209 | 0.293 |

| 0.334 | 0.739 | −0.206 | 0.290 | |||

| Construct | AVE | CR | Cronbach’s Alpha | |

|---|---|---|---|---|

| Performance Expectancy | Convenience | 0.563 | 0.712 | 0.681 |

| Responsiveness | 0.560 | 0.718 | 0.718 | |

| Perceived Cost | 0.647 | 0.785 | 0.781 | |

| Perceived Enjoyment | 0.603 | 0.710 | 0.733 | |

| Product Characteristics | 0.724 | 0.840 | 0.774 | |

| Effort Expectancy | Perceived Ease of Use | 0.830 | 0.907 | 0.907 |

| Perceived Reliability | 0.645 | 0.784 | 0.784 | |

| Social Influence | Subjective Norm | 0.594 | 0.812 | 0.815 |

| Image | 0.524 | 0.680 | 0.680 | |

| Facilitating Conditions | Personal Innovativeness | 0.576 | 0.689 | 0.688 |

| Institutional Influence | 0.543 | 0.737 | 0.725 | |

| Promotional Incentive | 0.695 | 0.820 | 0.820 | |

| Trust | 0.575 | 0.843 | 0.838 | |

| Perceived Risk | 0.552 | 0.720 | 0.754 | |

| Use intention | 0.759 | 0.904 | 0.903 | |

| Use Behavior | 0.572 | 0.728 | 0.726 | |

| Convenience | Responsive-ness | Perceived Cost | Perceived Enjoyment | Product Characteristics | Perceived Ease of Use | Perceived Reliability | Subjective Norm | Image | Personal Innovative-ness | Institutional Influence | Promotional Incentive | Trust | Perceived Risk | Use intention | Use Behavior | |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Convenience | 0.750 | |||||||||||||||

| Responsiveness | 0.602 | 0.748 | ||||||||||||||

| Perceived Cost | 0.503 | 0.525 | 0.804 | |||||||||||||

| Perceived Enjoyment | 0.564 | 0.571 | 0.617 | 0.777 | ||||||||||||

| Product Characteristics | 0.540 | 0.420 | 0.503 | 0.557 | 0.851 | |||||||||||

| Perceived Ease of Use | 0.453 | 0.440 | 0.317 | 0.530 | 0.571 | 0.911 | ||||||||||

| Perceived Reliability | 0.559 | 0.456 | 0.522 | 0.490 | 0.647 | 0.692 | 0.803 | |||||||||

| Subjective Norm | 0.259 | 0.292 | 0.313 | 0.411 | 0.593 | 0.455 | 0.610 | 0.771 | ||||||||

| Image | 0.398 | 0.572 | 0.479 | 0.417 | 0.403 | 0.337 | 0.504 | 0.411 | 0.724 | |||||||

| Personal Innovativeness | 0.546 | 0.548 | 0.411 | 0.356 | 0.528 | 0.285 | 0.488 | 0.419 | 0.479 | 0.759 | ||||||

| Institutional Influence | 0.369 | 0.217 | 0.565 | 0.401 | 0.449 | 0.399 | 0.692 | 0.335 | 0.376 | 0.534 | 0.737 | |||||

| Promotional Incentive | 0.304 | 0.391 | 0.260 | 0.434 | 0.446 | 0.209 | 0.369 | 0.345 | 0.465 | 0.271 | 0.326 | 0.834 | ||||

| Trust | 0.644 | 0.484 | 0.564 | 0.553 | 0.491 | 0.370 | 0.504 | 0.652 | 0.440 | 0.310 | 0.627 | 0.430 | 0.758 | |||

| Perceived Risk | 0.176 | 0.045 | 0.149 | 0.289 | 0.309 | 0.126 | 0.161 | 0.088 | 0.110 | 0.125 | 0.381 | 0.296 | 0.344 | 0.743 | ||

| Use intention | 0.541 | 0.567 | 0.423 | 0.572 | 0.486 | 0.549 | 0.625 | 0.516 | 0.560 | 0.304 | 0.233 | 0.542 | 0.532 | 0.584 | 0.871 | |

| Use Behavior | 0.378 | 0.300 | 0.237 | 0.243 | 0.299 | 0.322 | 0.401 | 0.506 | 0.327 | 0.384 | 0.102 | 0.143 | 0.261 | 0.104 | 0.491 | 0.756 |

| Fit Indices | The Proposed Model Fit | Benchmark |

|---|---|---|

| df | 278 | |

| Chi-square () | 703.763 | |

| 2.532 | <3 | |

| GFI | 0.864 | >0.90 |

| AGFI | 0.828 | >0.80 |

| NFI | 0.880 | >0.90 |

| NNFI | 0.910 | >0.90 |

| CFI | 0.923 | >0.90 |

| IFI | 0.924 | >0.90 |

| RMR | 0.105 | <0.05 |

| RMSEA | 0.066 | <0.08 |

| Hypothesis | Full Sample | Users | Non-Users | |||

|---|---|---|---|---|---|---|

| β | T-Value | β | T-Value | β | T-Value | |

| H1 (+) | 0.289 | 2.335 * | 0.543 | 2.822 ** | 0.155 | 2.281 * |

| H2 (+) | 0.235 | 2.148 * | 0.384 | 1.993 * | 0.194 | 1.986 * |

| H3 (+) | 0.883 | 14.570 *** | 0.900 | 11.064 *** | 0.847 | 8.479 *** |

| H4 (+) | 0.750 | 7.976 *** | 0.717 | 5.872 *** | 0.693 | 4.543 *** |

| H5 (+) | 0.242 | 2.820 ** | 0.305 | 2.688 ** | 0.204 | 1.210 |

| H6 (+) | 0.187 | 2.834 ** | 0.138 | 2.695 ** | 0.326 | 2.600 ** |

| H7 (+) | 0.175 | 2.655 ** | 0.127 | 2.199* | 0.157 | 2.669 ** |

| H8 (−) | −0.092 | −1.727 | −0.078 | −1.247 | −0.118 | −1.122 |

| H9 (−) | −0.448 | −4.217 ** | −0.150 | −1.609 | −0.648 | −5.600 *** |

| H10 (+) | 0.671 | 9.918 *** | 0.747 | 5.548 *** | 0.314 | 3.328 *** |

| H1a (+) | 0.632 | 3.345 *** | 0.403 | 2.810 ** | 0.340 | 2.755 ** |

| H1b (+) | 0.067 | 1.565 | 0.073 | 0.697 | 0.014 | 1.858 |

| H1c (−) | −0.240 | −2.304 * | −0.139 | −1.312 | −0.258 | −1.981 * |

| H1d (+) | 0.011 | 0.076 | 0.112 | 1.378 | 0.034 | 0.858 |

| H1e (+) | 0.352 | 2.657 ** | 0.216 | 2.614 ** | 0.313 | 2.747 ** |

| H2a (+) | 0.135 | 1.997 * | 0.138 | 1.973 * | 0.198 | 2.356 * |

| H2b (+) | 0.162 | 2.136* | 0.191 | 2.386 * | 0.143 | 1.975 * |

| H4a (+) | 0.481 | 3.925 *** | 0.425 | 3.357 *** | 0.372 | 4.093 *** |

| H4b (+) | 0.320 | 3.355 *** | 0.301 | 3.184 *** | 0.262 | 3.813 *** |

| H5a (+) | 0.218 | 2.044 * | 0.231 | 2.055 * | 0.097 | 1.458 |

| H5b (+) | 0.270 | 3.160 ** | 0.355 | 2.820 ** | 0.125 | 1.106 |

| H5c (+) | 0.129 | 2.248 * | 0.122 | 1.974 * | 0.154 | 2.397 * |

| Main Effect | Moderator | ||||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Gender | Age | Education | Income | ||||||||||||

| Male | Female | ||||||||||||||

| H [1] | H | β | T-value | β | T-value | P [2] | H | β | T-value | H | β | T-value | H | β | T-value |

| H1 | H11a | 0.547 | 8.787 *** | 0.583 | 9.210 *** | 0.388 | H12a | 0.083 | 0.404 | H13a | 0.233 | 0.768 | H14a | 0.305 | 1.025 |

| H2 | H11b | 0.507 | 7.923 *** | 0.610 | 9.883 *** | 0.240 | H12b | −0.135 | −0.748 | H13b | 0.072 | 0.261 | H14b | −0.044 | 0.180 |

| H4 | H11c | 0.667 | 12.054 *** | 0.705 | 12.988 *** | 0.326 | H12c | −0.144 | −1.188 | H13c | −0.582 | 0.004 *** | H14c | −0.009 | −0.057 |

| H5 | H11d | 0.548 | 8.801 *** | 0.553 | 8.528 *** | 0.516 | H12d | 0.225 | 0.820 | H14d | 0.350 | 1.195 | H14d | 0.484 | 2.099 ** |

| Hypotheses | Result | Hypotheses | Result |

|---|---|---|---|

| H1 | Supported | H11a | Not supported |

| H1a | Supported | H11b | Not supported |

| H1b | Not supported | H11c | Not supported |

| H1c | Supported | H11d | Not supported |

| H1d | Not supported | H12a | Not supported |

| H1e | Supported | H12b | Not supported |

| H2 | Supported | H12c | Not supported |

| H3 | Supported | H12d | Not supported |

| H2a | Supported | H13a | Not supported |

| H2b | Supported | H13b | Not supported |

| H4 | Supported | H13c | Supported |

| H4a | Supported | H13d | Not supported |

| H4b | Supported | H14a | Not supported |

| H5 | Supported | H14b | Not supported |

| H5a | Supported | H14c | Not supported |

| H5b | Supported | H14d | Supported |

| H5c | Supported | ||

| H6 | Supported | ||

| H7 | Supported | ||

| H8 | Not supported | ||

| H9 | Supported | ||

| H10 | Supported |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2022 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Li, G.; Zhang, X.; Zhang, G. To Use or Not to Use: It Is a Question—An Empirical Study on the Adoption of Mobile Finance. Sustainability 2022, 14, 10516. https://doi.org/10.3390/su141710516

Li G, Zhang X, Zhang G. To Use or Not to Use: It Is a Question—An Empirical Study on the Adoption of Mobile Finance. Sustainability. 2022; 14(17):10516. https://doi.org/10.3390/su141710516

Chicago/Turabian StyleLi, Gaoyong, Xin Zhang, and Ge Zhang. 2022. "To Use or Not to Use: It Is a Question—An Empirical Study on the Adoption of Mobile Finance" Sustainability 14, no. 17: 10516. https://doi.org/10.3390/su141710516

APA StyleLi, G., Zhang, X., & Zhang, G. (2022). To Use or Not to Use: It Is a Question—An Empirical Study on the Adoption of Mobile Finance. Sustainability, 14(17), 10516. https://doi.org/10.3390/su141710516