1. Introduction

Coal is China’s basic most energy source as well as an important raw material for industry. From the founding of China’s coal industry it has accumulated production of about 90 billion tons, providing reliable energy security for national economic and social development and effectively promoting the development of national industrialization [

1]. Although the proportion of coal in total energy consumption is declining, it is difficult for renewable energy to replace traditional fossil energy on a large scale in the short term at present. Therefore, the sustainable and stable development of the coal supply chain remains the main content of China’s energy security, and China’s basic national conditions dominated by coal will not change in a short time [

2,

3]. Although coal energy has effectively promoted economic and industrial development, its exploitation and use have seriously damaged the natural environment on which human beings rely for survival due to waste gas pollution, wastewater pollution, the destruction of land resources, etc. [

4,

5,

6,

7]. Therefore, all countries in the world have gradually begun to pay attention to the ecological problems caused by coal mining and use, and have taken corresponding measures in order to ensure global sustainable development. China has taken the lead in proposing the development goals of achieving peak carbon in 2030 and achieving carbon neutrality in 2060 [

8,

9]. The key factor in realizing these development goals is that China’s coal industry needs to build an environmentally aware supply chain and realize the green and low-carbon transformation of the coal industry based on the concept of green sustainable development [

10,

11]. However, financing problems (financing difficulties, expensive financing, etc.) have seriously hindered the daily operation and upgrading of small and medium-sized enterprises (SMEs) in the supply chain in the process of shaping the green supply chain in the coal industry, which is a major constraint factor for the transformation and upgrading of the coal industry under the concept of sustainable development [

12,

13].

According to previous studies, there are three main reasons why SMEs in the coal supply chain find it difficult to obtain development funds: First, financial institutions have higher financing conditions. The SMEs in the chain lack effective collateral, relying on their own credit, which makes it difficult to pass the credit audits of lending institutions (banks, etc.) [

14,

15,

16]. Second, SMEs cannot find suitable lending institutions in time due to information obstruction [

17]. Third, SMEs have a high probability of failure in the cruel market competition environment, which increases the risk of bad debts of accounts and increases the cautious lending of banks [

18]. Supply chain financing provides an effective solution to the financing problems of SMEs [

19,

20,

21]. Supply chain finance is a kind of financial service. The essence of supply chain finance is that each participating node (i.e., enterprise) realizes the effective circulation of its own assets by the circulation of four flows in the supply chain: logistics, capital flow, business flow, and information flow [

22,

23]. Supply chain financing can effectively link SMEs in the supply chain with core enterprises, helping SMEs in urgent need of funds to successfully apply to financial institutions for loans in order to complete their daily operations [

24,

25,

26]. The emergence of supply chain finance has effectively solved the financing problems of small and medium-sized enterprises in the supply chain to a certain extent. There are three modes of development thus far, namely, the accounts receivable financing mode, the advance payment financing mode, and the inventory pledge financing mode [

27]. The accounts receivable financing model is most widely used.

As a financial means that can effectively promote the development of supply chains in various industries, many scholars have begun to focus on research into supply chain financing with the aim of exploring the deep connotations and practical application effects of supply chain finance in order to further promote supply chain finance, help small and medium-sized enterprises to obtain development funds, and stabilize the economic market in the severe situation of the COVID-19 pandemic. Song Hua believes that building industrial trust chains is the primary task of developing supply chain finance in China [

28]. Sun Rui et al., have pointed out the phenomenon of joint loan fraud between SMEs and core enterprises in supply chain finance [

29]. Li Jian et al., believe that the key to business model innovation of supply chain finance lies in solving the problems of credit transmission and risk [

30]. Xu XH et al., found that factors such as imperfect credit systems and imperfect laws and regulations have hindered the development of supply chain finance to a certain extent [

31]. Zhang Min et al., studied the automobile supply chain through the KMV model and Copula model, and pointed out that there is a default contagion in the financing enterprise portfolio [

32]. Based on the above research, building trust foundations to control trust risk is the key task in promoting the development of supply chain finance. According to research, blockchain technology is well suited for this task.

Blockchain technology originated with Bitcoin, and can be seen as a decentralized distributed transaction account book. It has many characteristics, such as non-tampering, traceability, and decentralization [

33,

34,

35]. The role of blockchains in supply chain finance is mainly reflected in the following two aspects. On the one hand, enterprises in the industry can build industrial alliance chains through blockchain technology, complete the data-based chain of transaction information, realize reliable and transparent sharing of transaction information, and effectively solve the problem of data islands in the process of supply chain financing [

36,

37,

38]. On the other hand, the untamperable and traceable characteristics of blockchain technology provide financial institutions with greater convenience in verifying the authenticity of SMEs’ transaction information. This can help financial institutions to quickly find the entity responsible for transaction information and query the authenticity of transactions in order to effectively complete auditing tasks, improving financing efficiency [

39,

40,

41]. In addition, industrial alliance chains based on blockchain technology can permanently record the trading behavior of enterprises on the chain, which can be used as hard evidence for enterprises in determining credit ratings [

42,

43,

44].

In summary, the ‘Blockchain + Supply Chain Finance’ mode can effectively solve the financing problems encountered by SMEs in the daily operation and upgrade of the coal industry supply chain, accelerate the shaping of the coal industry environmental awareness supply chain, and further promote the sustainable development of the coal industry. In order to be general, this paper chooses the port-led coal supply chain as its research object and the more popular accounts receivable financing model as the research scene. This paper first proposes a coal accounts receivable financing model based on blockchain technology, then builds a coal accounts receivable financing system dominated by ports through blockchain technology. Next, the Stackelberg yield–benefit model is used to analyze the income function of each participant in the process of accounts receivable financing. Finally, this research comprehensively proposes the application architecture of blockchain technology in coal supply chain financing, which enriches the theoretical research on ‘blockchain + supply chain finance’ to a certain extent. This study provides a solution to the financing problems of SMEs in the coal supply chain, and has practical significance and reference value for helping the coal industry to achieve low carbon development.

2. The Coal Supply Chain Financing Business Model Led by Ports

2.1. Traditional Accounts Receivable Financing Business Model

There are two common financing modes in the coal supply chain led by ports: one is the inventory pledge financing mode for upstream suppliers, and the other is the accounts receivable financing mode for downstream dealers.

The latter financing mode is shown in

Figure 1.

The accounts receivable financing mode is one of the financing modes of downstream coal dealers in the coal supply chain, and can be divided into accounts receivable financing and factoring financing. At present, accounts receivable financing is more commonly used by coal dealers in the coal supply chain, which is the research object of this paper.

The main transaction process is as follows: downstream SMEs apply for financing from the accounts receivable issued by the power plant as a financing pledged object to apply for financing from financial institutions. Financial institutions entrust the port to verify the accounts receivable and the authenticity of the transaction. After the transaction information is verified and the power plant promises to expire the acceptance receivables, financial institutions provide financing services for downstream SMEs. The financing mode of accounts receivable pledges in the coal supply chain led by ports is shown in

Figure 2, which is explained in detail as follows:

A transaction arises between a power plant (core enterprise) and a downstream coal dealer, and the power plant issues an accounts receivable document to the downstream coal dealer.

The downstream coal dealer submits a financing application to the port and waits for approval.

The port verifies transactional information, the authenticity of accounts receivable, and the ability to repay from the power plant, which takes longer to review.

The power plant makes a payment commitment to the port.

The application is approved and the port grants loans to downstream coal dealers, who may continue to order coal from upstream coal suppliers.

At the end of the period, the power plant makes a repayment to the port.

Downstream coal dealers pay interest to the port at the end of the period.

The accounts receivable financing contract is canceled.

In traditional accounts receivable financing services, the port spends a significant amount of manpower, money, and time verifying the authenticity of the receivables and analyzing the financial status and creditworthiness of the financing enterprise and core enterprise in which the transaction takes place. The verification process is time-consuming and laborious, and the review of financing applications takes a long time, which reduces the efficiency of financing and increases its cost. The reasons why SMEs find it difficult to obtain funds include an imperfect supplier credit system in the secondary supply chain including core enterprises, weak risk resistance ability, opaque supply chain transaction information, high port verification cost, and high risks.

2.2. Accounts Receivable Financing Business Model Based on Blockchain Technology

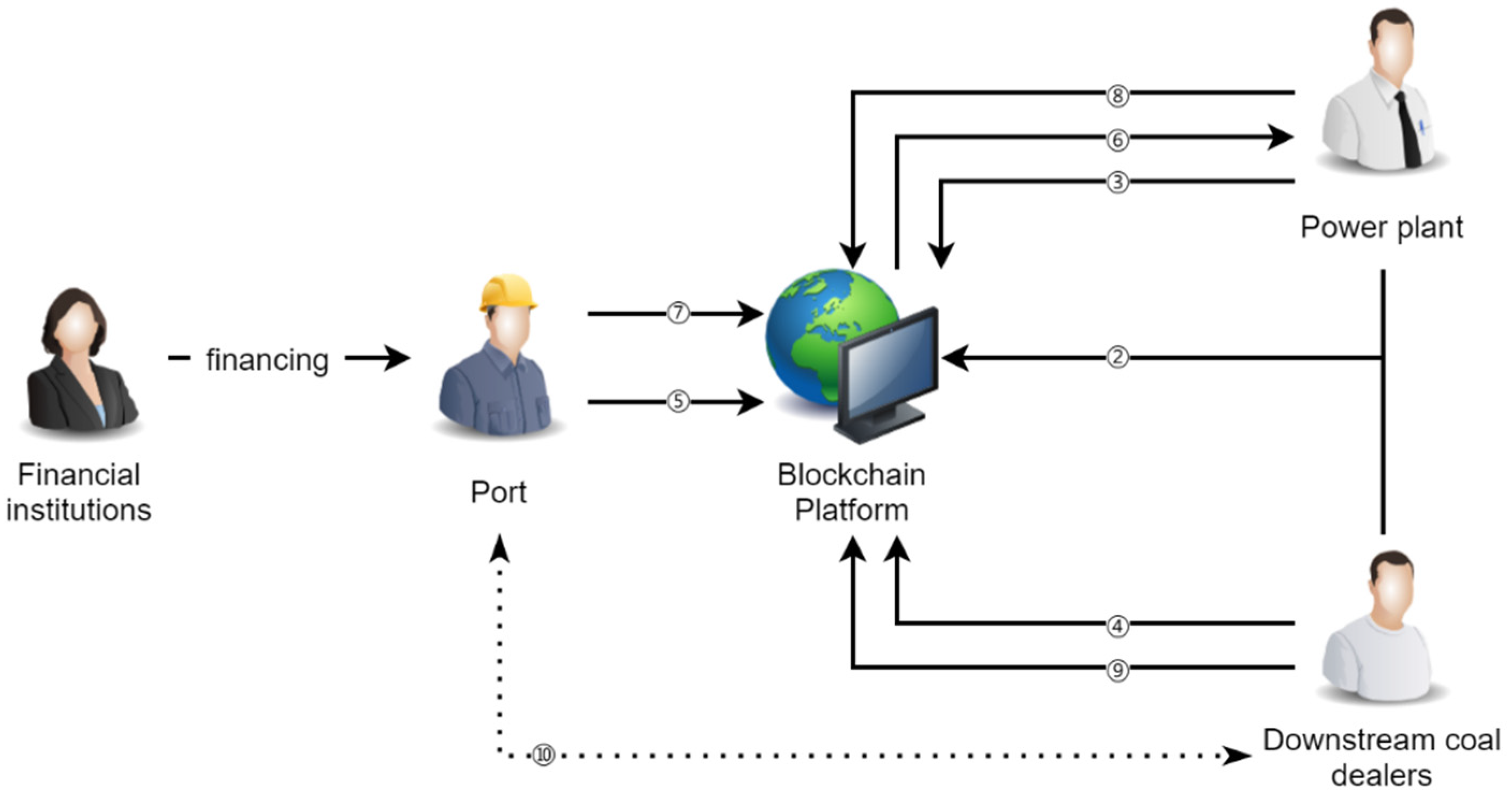

Because blockchain technology can realize data encryption, information sharing, and credit transmission of core enterprises, the use of blockchain technology can greatly improve the financing efficiency of accounts receivable financing in the coal supply chain led by ports. To build a coal accounts receivable financing system based on blockchain technology, this paper introduces blockchain technology into the accounts receivable financing platform. Participants at all levels downstream of the coal supply chain led by ports, such as ports, downstream coal dealers (DCDs), core enterprises, and financial institutions such as banks, can voluntarily choose to join according to their financing needs. The blockchain-based financing model for the coal receivables is shown in

Figure 3, and is explained in detail as follows:

If ports, downstream coal dealers (DCDs), power plants (core enterprises), banks, other financial institutions, and regulators want to pass system certification and participate in transactions in the alliance chain system based on blockchain technology as nodes, they must meet the pre-set access conditions. Banks and other financial institutions provide a certain amount of financing to the port, the port provides financing services for coal dealers and other DCDs downstream of the supply chain after the port verifies the authenticity of receivables transactions, and the system packages and stores the contracts and related information in the transaction process.

After a transaction between downstream coal dealers and power plants, relevant transaction information including contact information is encrypted and uploaded to the blockchain platform and signed by each party for confirmation. The system completes the electronic certification of the contract information on each node in the alliance chain by a consensus mechanism and writes the transaction-related certificates, including the contract, into a smart contract. Changes in the status parameters of smart contracts can be used as a basis for querying related information during the business process.

Downstream coal dealers provide goods as required within the time specified in the electronic contract and transmit the encrypted accounts receivable invoice information to the power plants. After receiving and accepting goods, the power plant issues digital receivables bills for the downstream coal dealers and promises to make the payment when it is due. The digital bills confirmed and issued by the core enterprises can be transferred and split among DCDs in the coal supply chain before the repayment date, which can be used as the financing basis for DCDs. Downstream coal dealers can pledge digital receivables notes to the port as collateral to obtain financing, and can split or transfer digital receivables bills in order to purchase raw materials from upstream suppliers or offset arrears.

The downstream coal dealer initiates a financing application to the port after obtaining the accounts receivable digital bills. Here, we assume that the downstream coal dealer chooses to pledge the accounts receivable digital bills to the port for financing.

The port verifies the authenticity of the accounts receivable through the blockchain platform. As the information on transactions and issuance of digital receivables bills by downstream coal dealers and power plants has been stored in each node of the system, the efficiency of the port’s review of transaction information is greatly improved and the review time is shortened.

The power plant makes a payment commitment to the port when due, then the system automatically generates a smart contract with automatic repayment when due. Finally, the port broadcasts the above transaction message to the whole network node.

After completing the audit, the port determines the loan interest rate and provides a financing line for downstream coal dealers to issue loans and automatically generates smart contracts for interest payments due from downstream coal dealers to the port.

By the end of the payment period, the smart contract triggered the power plant to automatically pay the port to the port of financing. By the end of the payment period, the smart contract trigger condition automatically executes the downstream coal dealer’s instruction to pay the interest to the port.

The accounts receivable financing contract is canceled. The accounts receivable digital document completes a life cycle and writes key information about this financing to the accounts receivable financing system to complete the round of accounts receivable financing. If a company is overdue, the relevant overdue records are written into the blockchain as a valid basis for the port to sue for recovery.

Core enterprises and DCDs conduct transactions, and then DCDs use the uncollected receivables accounts to borrow money from the port and promise to repay it when due. Because the core enterprise, small and medium-sized enterprises, and the port area are on the same blockchain platform, the characteristics of openness and transparency mean that it is not easy to tamper with information, while mutual trust and traceability between nodes can effectively reduce the cost of verifying the authenticity of transaction background in the process of receivables financing. This can reduce the time of financing application and help to improve the financing difficulties of DCDs.

3. Construction of Accounts Receivable Financing Platform Based on Blockchain Technology

3.1. Application Process Analysis of Financing Mode Based on Blockchain Technology

The improvement of the financing mode of accounts receivable in the port-led coal supply chain through blockchain technology is mainly reflected in the following four aspects: transaction data storage, transaction data encryption and sharing, data traceability, and settlement of transactions.

3.1.1. Transaction Data Storage

Stored transaction data can both facilitate each node to query transaction information and act as data for endorsement of nodes when determining credit ratings. In the coal accounts receivable financing system based on blockchain technology, the hash algorithm is the main technology used in the safe storage process of transaction data. Transaction data are composed of two types of information: one is the transaction information composed of purchase and sale contracts, orders, receipts, and other documents, and the other is the process information generated by the financing process. The storage process of transaction data in the blockchain financing system refers to the process of encrypting transaction data through the hash algorithm, generating a hash digest value (i.e., digital digest), and finally storing it on the blockchain.

The hash algorithm can generate a fixed-length string by calculating any input string or binary file data as the output value. The same input data produces the same output value, which is the digital digest of the input data (i.e., stored data). The digital digest is the unique identifier of source information, equivalent to the ‘digital fingerprint’ of information, which can verify the integrity and source of data such as files and network packets [

45]. The node uploads a binary transaction data file of accounts receivable and calculates the summary of the file in the financing process, then the transaction information and digital digest are stored on the blockchain together. The characteristic of the hash algorithm is that even if there is a small difference in data input, different hash values will be generated. At the same time, the output hash value cannot be used to push back the source file data. This can effectively ensure the security and credibility of the storage chain of the information on accounts receivable financing transactions. The specific process is shown in

Figure 4.

The transaction data storage in the accounts receivable financing process of port-led coal supply chains mainly occurs in processes ②, ⑧, and ⑩ of the transaction process (

Figure 3). The main transaction data include dynamic transaction information between power plants and downstream coal dealers, financing transaction contracts, dynamic records of financing processes, etc. These transaction data are broadcast to the whole network after the hashing algorithm is converted into the digital digest, then verified by each node in the system, and finally saved on the blockchain. The transaction data storage based on the blockchain can form a digital backup of accounts receivable financing transaction records in the system platform, which can effectively break the information barriers between trading ports and trading enterprises, greatly save the audit time of the port for transaction authenticity, improve business efficiency, and improve risk control ability. At the same time, the backup financing transaction records can be used as materials for each transaction node in determining credit ratings.

3.1.2. Encryption and Sharing of Transaction Data

The encryption and sharing of transaction data mainly uses an asymmetric encryption algorithm and the digital signature technology of blockchain technology, which can ensure the safety of information in the process of transmission.

The data senders need to ensure that data is protected from malicious interference during network transmission. Asymmetric encryption can guarantee data security and privacy based on authentication, data integrity, and confidentiality. The data sender encrypts the transmitted data by public key before transmission, and the transaction data cannot be changed during the transmission process. After receipt, the data receiver needs to use its private key to convert it into the original data form before reading the information content. The specific process is shown in

Figure 5.

In the process of port accounts receivable financing based on blockchain technology, the transmission of financing-related transaction data is different according to the sender and receiver, and the public key and private key are different, which makes it impossible to obtain the real information of the data even if it is stolen by others in the transmission process, effectively guaranteeing the security of data transmission. The digital signature technology provided by the blockchain can accurately locate the sender’s identity through the signature of the transaction information, allowing the relevant body responsible for the transaction information to be found and ensuring the authenticity of the transaction process. Digital signature technology and the asymmetric encryption algorithm cooperate to complete the encryption and sharing of transaction information data. The sender sends the digital signature and private key to the data receiver and the receiver verifies the public key and digital signature of the sender in order to confirm whether the transaction is effective. The process is shown in

Figure 6.

Transaction data encryption and sharing in the process of accounts receivable financing in the port-led coal supply chain mainly occurs in processes ④ and ⑤ in the transaction process (

Figure 3). When the port wants to query the transaction data stored in the blockchain of the power plant and the downstream coal dealers, the port needs to make a sharing information request to the downstream coal dealers and the power plant. With the consent of the power plant and the downstream coal dealers, the identity of the parties is confirmed. The financing parties share the transaction data with the port. In the process of accounts receivable financing business based on blockchain technology, the financing parties help ports to understand transaction data through encryption and sharing technology under the condition of data security, which is conducive to reducing the cost of verifying the authenticity of accounts receivable, both shortening the review time and improving financing efficiency.

3.1.3. Data Traceability

Prior to data sharing in the financing system, the authenticity of the original data in the blockchain should be ensured. When the port or other nodes in the chain question the authenticity of transaction data, the time stamp technology can be used to trace the transaction data. The time stamp technology can record the transaction records in accordance with the order in which the transaction records were generated, and can deposit the data or the time of the transaction to ensure the reliability of the system data. In addition, the time stamp is a key technology for connecting each block in the series into a chain. Its unique recording characteristics make each block in the chain have a unique and untamperable time label [

46]. Therefore, each participating node can accurately locate the time and location of transaction information generated on the chain based on blockchain technology and determine the responsible party in order to query the authenticity of data records. The specific process is shown in

Figure 7.

The transaction data are uploaded by each node in the blockchain-based accounts receivable financing system. After the transaction data are generated by the hash algorithm, the time stamp is automatically covered by the system. This process mainly occurs in processes ⑤ and ⑩ in the transaction process. There are two main roles in this stage: one is to ensure the traceability of audit material, and the other is to accurately record the time and place of each stage in the financing process.

3.1.4. Automated Settlement of Transactions

A smart contract is a computer code contract that can be programmed on a blockchain. It is a process for using computer code to represent the content of a paper contract. Its operation mechanism is shown in the

Figure 8. After the port signs a financing contract with the downstream coal distributors, the contract is uploaded to the blockchain platform. The smart contract has the characteristics of automatically executing the contract’s content through a virtual machine under certain conditions, reducing man-made malicious interference. When the contract expires, the debtor automatically repays the contract, which provides a credible application environment for the port to lend to the downstream coal dealers.

Transaction settlement in the financing process of accounts receivable in the coal supply chain dominated by ports mainly occurs in processes of ⑥, ⑧, and ⑨. The flow of funds is set through smart contracts, reducing human interference, and the credit level of core enterprises and downstream coal dealers is increased to a certain extent as well.

3.2. System Architecture

The architecture of the port receivables financing system based on blockchain technology is shown in

Figure 9; it includes an application layer, smart contract layer, consensus layer, network layer, and storage layer.

The storage layer stores transaction data through a Merkel tree structure as a block body, encrypting transaction information using asymmetric encryption, time stamping the block header to ensure that the data are protected from tampering, encrypting it using a hash algorithm, and the concatenated the blocks to form a chain storage structure.

The network layer determines the rules under which each enterprise joins the blockchain system as a participating node, and the block information is shared in the system using a P2P network, i.e., peer-to-peer.

The consensus layer obtains the information of each node through the consensus algorithm and then determines the rules for verifying the authenticity of the information, ensuring that each enterprise node stores the same information.

The smart contract layer executes pre-designed script code that can be executed automatically if certain conditions are met. In the accounts receivable financing blockchain system, the smart contract realizes user information records, transaction information records, transfer accounts receivable records, and other functions through the chain code.

The application layer mainly realizes user operation functions through smart contracts. It mainly includes user login registration and financing and information service functions.

3.3. Application Module Design

The financing process of the port receivables financing business can be divided into the transaction stage between coal dealers and power plants, the financing stage, in which coal dealers use receivables documents issued by power plants, and final stage, in which power plants repay the port. Each stage generates different transaction information.

The main players in the Coal Accounts Receivable Financing system (CRFS) are ports, coal traders, power plants, and regulators. Coal dealers and power plants, as nodes, use blockchain technology to finance and maintain the system; ports, as nodes, provide financing services and maintenance for the blockchain system; finally, regulators supervise and maintain the blockchain system.

After coal dealers trade coal with power plants, coal dealers and power plants upload the encrypted transaction information on trading volumes, receivables, trading time, and counterparties through their private key and the public keys of the other party and generate digital signatures. After both parties confirm, the system adds the transaction information record to the block. Coal dealers use the accounts receivable documents issued for them by the power plant to apply for financing from the port, thereby solving their financing problems. The port approves the application based on its verification of the authenticity of the transaction information, and the port, power plant, and coal dealer confirm the financing contract information, including the debtor, creditor, financing amount, transaction time, and repayment time. The contract information is broadcast across the network, and the contract transaction information record is added to the block. Smart contracts are used to determine the repayment date of the power plant, and the power plant automatically pays the loan to the port at the end of the period. The entire accounts receivable financing transaction information is added to the blockchain, ensuring the authenticity of the transaction information and traceability of the information, thereby improving the turnover rate of accounts receivable and reducing the difficulty of financing for coal dealers. Regulators can supervise the various processes and enterprises of accounts receivable financing through this system and quickly lock the main body of responsibility when something goes wrong. The technical flow chart of the business information uplink is shown in

Figure 10.

4. Revenue Analysis of Participants in Coal Supply Chain Finance

4.1. Hypothesis and Parameter Setting

Hypothesis (H1). Because this research is based on a three-tier supply chain scenario consisting of banks, ports, downstream coal dealers (DCDs), and power plants (core enterprises), the product prices remain unchanged during the sales cycle and product demand fluctuates with market conditions.

Hypothesis (H2). The four enterprises aim to maximize profits.

Hypothesis (H3). When the downstream coal dealers with their own insufficient funds decide to purchase coal from the upstream coal suppliers, they need to obtain accounts receivable documents issued by the power plant and finally carry out accounts receivable financing to the bank through the port.

Hypothesis (H4). There is information asymmetry between banks, ports, power plants (core companies), and port verification when they do not use blockchain technology. The cost of transaction information authenticity is () When using blockchain technology, the four companies can share transaction information.

Hypothesis (H5). Without loss of generality, this study considers the market demand of electric energy as inversely proportional to the product price; that is, the higher the price of electrical energy units produced on the market, the smaller the market demand for electric energy, in line with the functional relationship [

47],

where is the elastic coefficient. Here, represents the income level of consumers, while represents the conversion coefficient of products of similar price. In this research, we set the model parameters as follows based on the above hypothesis and the actual transaction process. As shown in

Table 1 below:

4.2. Revenue Function Analysis of Participants in Accounts Receivable Mode

Without using blockchain technology, the financially constrained downstream coal dealers need to use accounts receivable to finance loans to ports in order to solve their own shortage of funds and achieve optimal supply. The port’s verification of the authenticity of these accounts receivable takes a great deal of time and produces costs in the process of accounts receivable financing. Due to the large amount of accounts receivable involved in the coal industry and the small and medium-sized downstream coal dealers, the ports must reduce their pledge rate and increase the loan interest rate in order to select outstanding enterprises for lending to reduce the risk of bad debts.

The port revenue function can be expressed as follows:

The power plant (core enterprise) revenue function can be expressed as follows:

The downstream coal dealer revenue function can be expressed as follows:

Because the goal of each participant is to maximize profit according to the Stackelberg model backwards induction solution method, the optimal order quantity, optimal price per unit of product sales of downstream coal distributors, and optimal price per unit of product sales of the power plant (core enterprises) can be obtained, finalizing the maximum benefits for each participant.

First, we bring

W =

a −

bPc into Equation (2), meaning that we have

With the simultaneous partial derivatives of Pc on both sides of the Equation (4), we have

Bringing

W = a − bPc and (5) into Equation (3) yields

The partial derivative of Ps is obtained on both sides of Equation (6), as follows:

Bringing Formula (7) into Formula (5) yields

The optimal order quantity is then

By substituting Equations (7)–(9) into Equations (1)–(3), the maximum port revenues can be obtained as follows:

The maximum gain for power plants (core businesses) is

The downstream coal dealers’ maximum income is

By combining Equations (10)–(12), it can be seen that the pledge rate of accounts receivable and loan interest rate have a great impact on the trading revenue of ports, power plants, and downstream coal dealers.

Blockchain technology can break through information barriers, enabling real-time sharing of transaction information among participating nodes. Based on blockchain technology, the port can accurately and legally verify the authenticity of transactions and receivables between downstream coal dealers and power plants in a relatively short period of time and automatically complete the repayment operation at the end of the financing transaction using smart contracts, thereby reducing the risks of lending. Therefore, the ports increase their pledge rate of accounts receivable financing and reduce loan interest rates to attract more enterprises, increasing their interest income in the accounts receivable financing system of coal supply chain based on blockchain technology.

4.3. Numerical Analysis

This section is based on the numerical analysis of the parties’ income function in

Section 4.2, aiming to intuitively and clearly show the impact of the financing pledge rate and loan interest rate on the income of each participant in accounts receivable financing in the port-led coal supply chain.

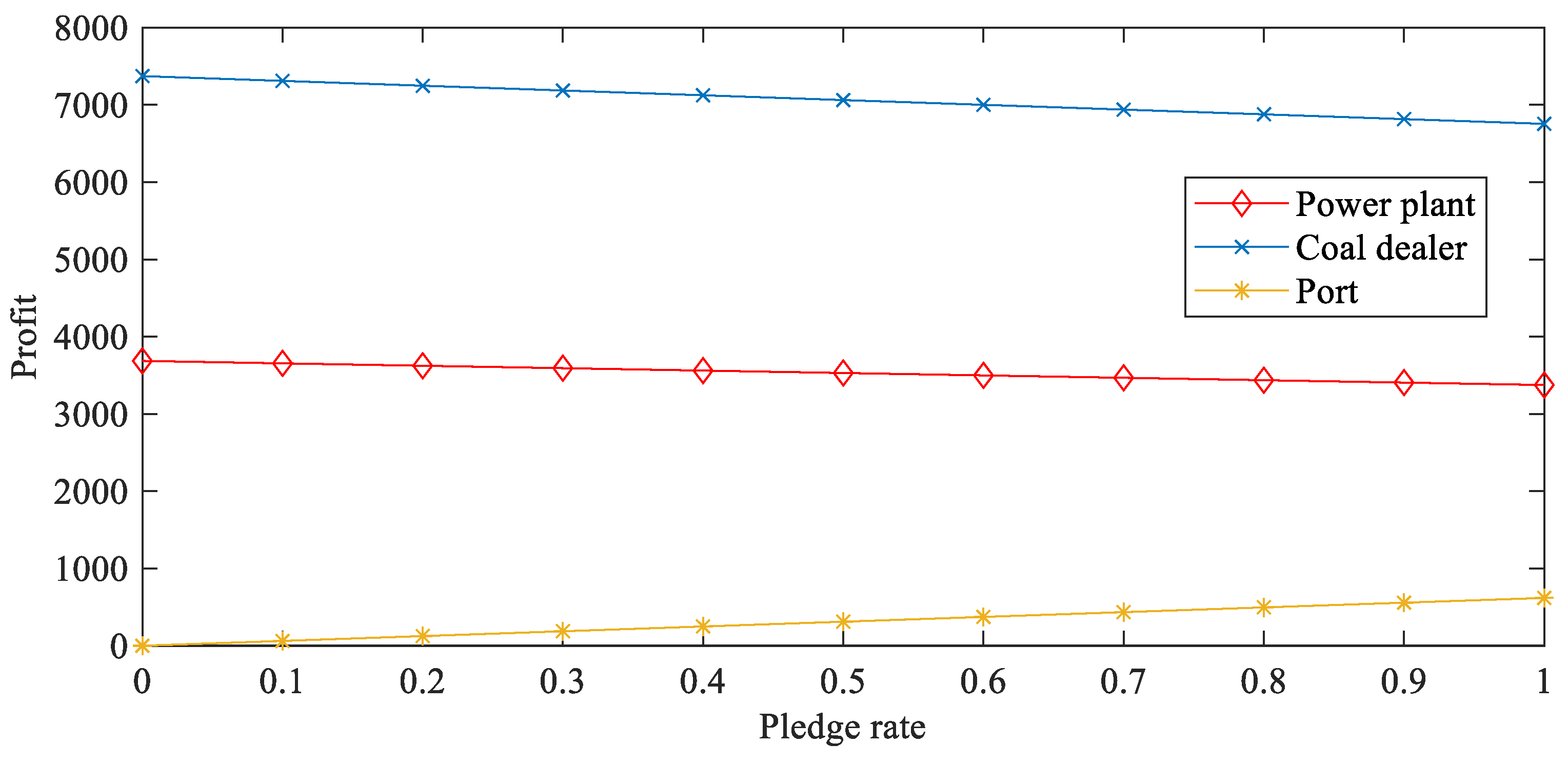

Here, we take a downstream coal dealer D, power plant, F and Tianjin Port as the research objects. The trading relationship among the three is as follows: downstream coal dealer D buys coal from upstream enterprises, and Tianjin Port is the transportation hub of coal transportation between the two. The downstream coal dealer D resells the coal to power plant F after classified processing, and power plant F usually settles accounts by issuing accounts receivable. When downstream coal dealer D has financial constraints, it applies for financing from Tianjin Port with the receivables issued by power plant F. Based on the actual situation, we set the parameters as follows: unit purchase cost C of downstream coal dealer Yuan/ton; port pledge rate ; port loan interest rate ; cost of verifying the authenticity of transaction information Yuan; and for power plant , the functional relationship between the ordered quantity of electric energy and unit product price satisfies the equation .

As can be seen in

Figure 11 and

Figure 12, as port pledge and loan rates increase, power plants and downstream coal dealers receive gains if the downward trend is downward and the revenue received by the port is upward. It is obvious from the two figures that the loan interest rate has a stronger influence on the income of the participants than the pledge rate of accounts receivable. The increase in the pledge interest rate and loan interest rate increases the pressure on coal traders to repay loans, making them less willing to offer high loans. This seriously affects the trading enthusiasm of coal dealers. Lack of funds leads to the failure of coal dealers to meet the optimal order quantity of power plants, thus affecting the profitability of power plants and ultimately reducing the overall profitability of the coal supply chain under the guidance of ports.

Blockchain technology is introduced into the coal supply chain finance under the leadership of the port. On the one hand, the port can audit the authenticity of the transaction information accurately and in real time through the transaction records on the alliance chain, saving audit costs and improving financing income. On the other hand, the port reduces the loan interest rate to increase the financing income of coal dealers, improve their financing enthusiasm, revitalize the supply chain, improving the overall profitability of the port-led supply chain and improving its competitiveness.

5. Conclusions

This paper takes the port-led coal supply chain as the research object and accounts receivable financing, which is widely used in supply chain finance, as the research scenario. This paper first puts forward a coal accounts receivable financing mode based on blockchain technology, then builds the application system framework based on blockchain technology combined with the coal accounts receivable financing mode. Finally, the Stackelberg model is used to analyze the income function of each participant in the coal accounts receivable mode, and the following conclusions are drawn:

- (1)

Blockchain technology can effectively build the trust chain among enterprises in the coal industry, greatly promoting the development of supply chain finance in the coal industry. The main reason that blockchain technology assists the sustainable development of supply chain finance is that its composition technology can solve the current constraints that hinder the development of supply chain finance. The consensus mechanism can break the information barriers between enterprises in the chain and realize transaction information sharing, the hash algorithm can deal with transaction data provided by participating enterprises and preserve uniqueness, asymmetric encryption ensures the security of transaction data in transmission, time stamps and digital signatures assist audit institutions to validate transaction information; and intelligent contracts reduce human interference and operational risks.

- (2)

The pledge rate of accounts receivable and the loan interest rate decided by financial institutions have a great influence on the financing enthusiasm of SMEs in the coal accounts receivable financing mode. However, compared with the pledge rate of accounts receivable, the loan interest rate has a greater impact on the enthusiasm of financing enterprises in applying for financing. Blockchain technology reduces the risk posed to financial institutions by bad debts by building the trust foundation between trading enterprises in the supply chain. Therefore, financial institutions reduce loan interest rates to attract more enterprises, increasing the interest income of their own funds. This can save on the audit costs of audit financing enterprises, further increasing financing income. Reduced lending rates from financial institutions can improve the maximum transaction income of downstream coal dealers and power plants, to improving the overall level of coal supply chains, enhancing their overall competitiveness, and promoting their development.

- (3)

The combination of blockchain and supply chain finance can effectively solve the financing problems between SMEs in the coal supply chain and provide urgent funds for daily operation and transformation and development of SMEs in the coal industry, thereby speeding up the coal industry’s green transformation and development and realizing the sustainable development goals of green mining, efficient use, and clean development.

In general, this paper provides great value to the reform, innovation, and development of supply chain finance at both the theoretical and practical levels. On the theoretical level, this paper demonstrates the applicability of blockchain technology in supply chain financing through the Stackelberg model. Using the empirical method of numerical analysis to supplement the results of the demonstration, we fully demonstrate that blockchain technology can provide multiple benefits to supply chain finance participants in their transaction activities. This paper proposes a port-based receivables financing model framework based on blockchain technology, which can provide a certain degree of theoretical guidance for the real-world practical application of blockchain technology in supply chain finance.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}