Off-Farm Employment and Agricultural Credit Fungibility Nexus in Rural Ghana

,

,  ,

,  ,

,

Abstract

1. Introduction

1.1. Background of the Study

1.2. A Brief Overview of Agricultural Credit in Developing Countries

1.3. Conceptual Analysis

2. Materials and Methods

2.1. Data

2.2. Analytical Techniques

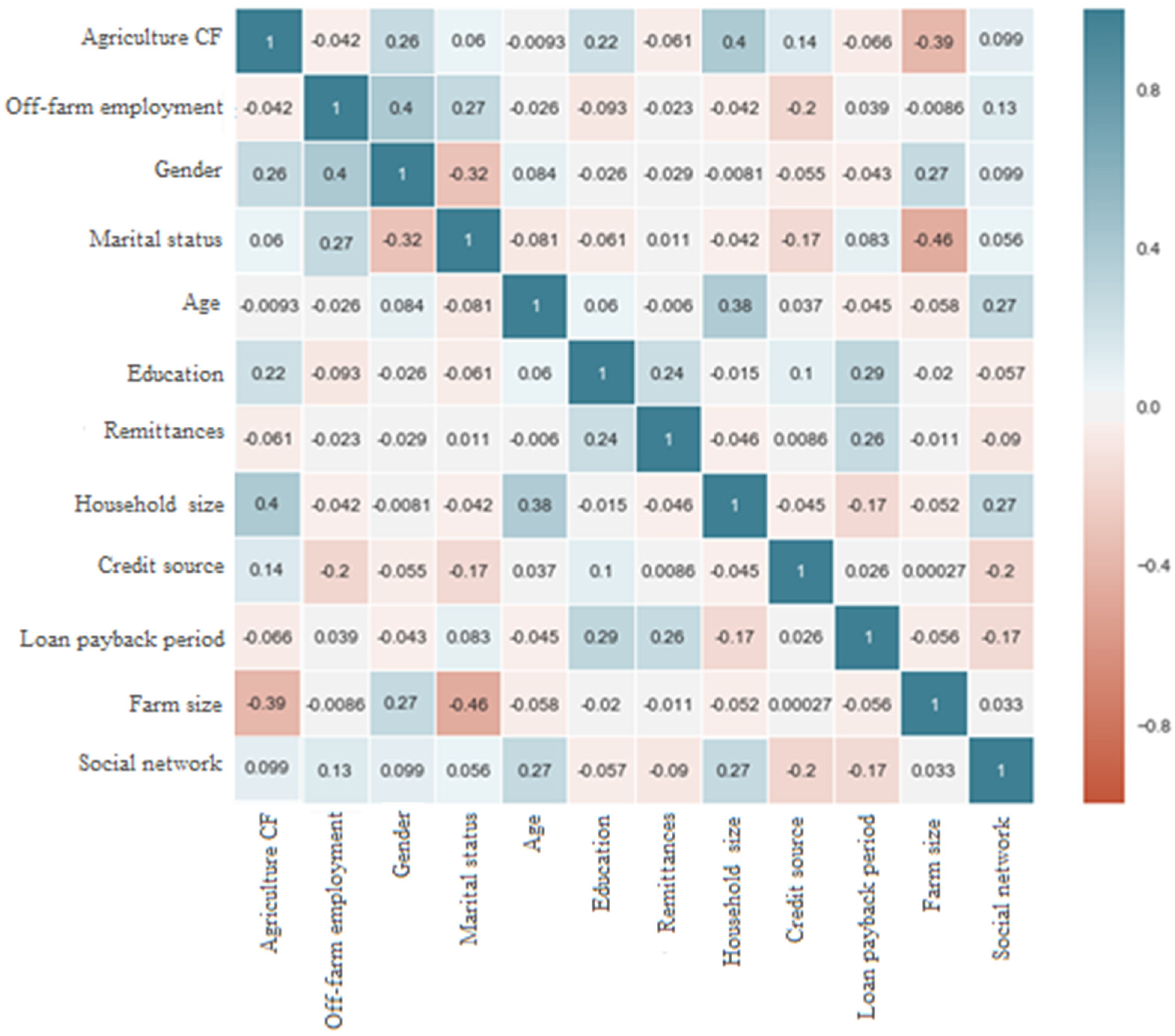

2.3. Variable Selection

2.4. Empirical Model

3. Results and Discussions

3.1. Descriptive Analysis

3.2. Difference between Means of Farmers with and without Off-Farm Employment Annual Credit Received, Agriculture CF and Credit Margin of Farm Investment Status

3.3. Empirical Results

3.3.1. The Determinants of Off-Farm Employment

3.3.2. The Impact of Off-Farm Employment on Agriculture Credit Fungibility (CF)

3.3.3. Additional Analysis

4. Conclusions

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Acknowledgments

Conflicts of Interest

Appendix A

{kind=link}

| Variables | First Stage Selection Equation | Second Stage Agriculture Credit Fungibility Equation | |

|---|---|---|---|

| Off-Farm Employment | Off-Farm Employment | Non-Off-Farm Employment | |

| Gender | 0.0343 (0.0129) ** | −0.0213 (0.0130) | 0.0436 (0.0173) *** |

| Marital status | −0.0153 (0.0125) | 0.0086 (0.0064) | 0.0832 (0.0643) |

| Age | 0.0249 (0.0168) | 0.0056 (0.0018) ** | 0.0106 (0.0051) * |

| Age2 | −0.1204 (0.0437) ** | −0.0173 (0.0086) * | −0.0024 (0.0009) ** |

| Education | 0.0476 (0.0173) ** | 0.0278 (0.0191) | 0.1644 (0.1207) |

| Remittances | 0.0339 (0.0120) *** | −0.0149 (0.0056) ** | −0.0020 (0.0007) ** |

| Household Size | 0.0724 (0.0980) | 0.0078 (0.0051) | 0.0201 (0.0093) *** |

| Credit source | −0.1047 (0.0788) | −0.0068 (0.0022) *** | 1.1028 (0.9139) |

| Loan payback period | 0.0155 (0.0089) | −0.0261 (0.0108) * | −0.9261 (0.7308) |

| Farm size | −0.0270 (0.0537) | −0.0211 (0.0098) * | −0.0011 (0.0009) |

| Social Network | 0.0165 (0.0029) *** | ||

| Constant | 0.1372 (0.1005) | 0.2783 (0.0745) *** | 1.1654 (1.8317) |

| 0.1483 (0.1007) | |||

| 0.3126 (0.2521) | |||

| 0.0125 (0.0039) *** | |||

| −0.0132 (0.0193) | |||

| LR test of indep. eqns.: chi2(1) = 6.43 Prob > chi2 = 0.0007 | |||

| Variables | Correlation Coefficient | p-Value |

|---|---|---|

| Off-farm employment | 0.1201 * | 0.0525 |

| Share of agriculture CF | 0.3886 | 0.2132 |

References

- Petrick, M. Farm investment, credit rationing, and governmentally promoted credit access in Poland: A cross-sectional analysis. Food Policy 2004, 29, 275–294. [Google Scholar] [CrossRef]

- Li, R.; Li, Q.; Huang, S.; Zhu, X. The credit rationing of Chinese rural households and its welfare loss: An investigation based on panel data. China Econ. Rev. 2013, 26, 17–27. [Google Scholar] [CrossRef]

- Feder, G.; Lau, L.J.; Lin, J.Y.; Luo, X. The Relationship between Credit and Productivity in Chinese Agriculture: A Microeconomic Model of Disequilibrium. Am. J. Agric. Econ. 1990, 72, 1151–1157. [Google Scholar] [CrossRef]

- Kumar, C.; Turvey, C.G.; Kropp, J.D. Credit Constraint Impacts on Farm Households: Survey Results from India and China. SSRN Electron. J. 2012, 2034487. [Google Scholar] [CrossRef]

- Twumasi, M.A.; Jiang, Y.; Acheampong, M.O. Capital and credit constraints in the engagement of youth in Ghanaian agriculture. Agric. Financ. Rev. 2019, 80, 22–37. [Google Scholar] [CrossRef]

- Baffoe, G.; Matsuda, H. Understanding the Determinants of Rural Credit Accessibility: The Case of Ehiaminchini, Fanteakwa District, Ghana. J. Sustain. Dev. 2015, 8, 183. [Google Scholar] [CrossRef]

- Du, J.; Zeng, M.; Xie, Z.; Wang, S. Power of Agricultural Credit in Farmland Abandonment: Evidence from Rural China. Land 2019, 8, 184. [Google Scholar] [CrossRef]

- Diagne, A.; Zeller, M. Research Report 116; International Food Policy Research Institute: Washington, DC, USA, 2001. [Google Scholar]

- Kuwornu, J.K.M.; Apiors, E.K.; Kwadzo, G.T.M. Access and Intensity of Mechanization: Empirical Evidence of Rice Farmers in Southern Ghana. Braz. Arch. Biol. Technol. 2017, 60. [Google Scholar] [CrossRef]

- Dong, F.; Lu, J.; Featherstone, A.M. Effects of credit constraints on household productivity in rural China. Agric. Financ. Rev. 2012, 72, 402–415. [Google Scholar] [CrossRef]

- Adams, D.W.; Von Pischke, J.D. Microenterprise credit programs: Déja vu. World Dev. 1992, 20, 1463–1470. [Google Scholar] [CrossRef]

- Coleman, B.E. The impact of group lending in Northeast Thailand. J. Dev. Econ. 1999, 60, 105–141. [Google Scholar] [CrossRef]

- Annim, S.K.; Dasmani, I.; Armah, M. Does Access and Use of Financial Service Smoothen Household Food Consumption? In MPRA; University Library of Munich: Munich, Germany, 2011; pp. 1–25. [Google Scholar]

- Atakora, A. Measuring the Effectiveness of Financial Literacy Programs in Ghana. Int. J. Manag. Bus. Res. 2016, 3, 135–148. [Google Scholar]

- Hussain, A.; Thapa, G.B. Fungibility of Smallholder Agricultural Credit: Empirical Evidence from Pakistan. Eur. J. Dev. Res. 2016, 28, 826–846. [Google Scholar] [CrossRef]

- Saqib, S.E.; Khan, H.; Panezai, S.; Ali, U.; Ali, M. Credit Fungibility and Credit Margin of Investment: The Case of Subsistence Farmers in Khyber Pakhtunkhwa. Sarhad J. Agric. 2017, 33, 661–667. [Google Scholar] [CrossRef]

- Chandio, A.A.; Jiang, Y.; Rehman, A. Credit margin of investment in the agricultural sector and credit fungibility: The case of smallholders of district Shikarpur, Sindh, Pakistan. Financ. Innov. 2018, 4, 27. [Google Scholar] [CrossRef]

- Enimu, S.; Eyo, E.O.; Ajah, E.A. Determinants of loan repayment among agricultural microcredit finance group members in Delta state, Nigeria. Financ. Innov. 2017, 3, 21. [Google Scholar] [CrossRef]

- Odoemenem, I.U.; Alimba, J.O.; Ezike, K.N.N. Assessing capital resource mobilization and allocation efficiency of small scale cereal crop farmers in Benue State, Nigeria. Indian J. Sci. Technol. 2008, 1, 1–8. [Google Scholar] [CrossRef]

- Sharma, M.; Zeller, M. Repayment performance in group-based credit programs in Bangladesh: An empirical analysis. World Dev. 1997, 25, 1731–1742. [Google Scholar] [CrossRef]

- De Janvry, A.; Sadoulet, E.; Zhu, N. The Role of Non-Farm Incomes in Reducing Rural Poverty and Inequality in China; University of California: Berkeley, CA, USA, 2005. [Google Scholar]

- Chang, H.H.; Mishra, A. Impact of off-farm labor supply on food expenditures of the farm household. Food Policy 2008, 33, 657–664. [Google Scholar] [CrossRef]

- Démurger, S.; Wang, X. Remittances and expenditure patterns of the left behinds in rural China. China Econ. Rev. 2016, 37, 177–190. [Google Scholar] [CrossRef]

- Ma, W.; Zhou, X.; Renwick, A. Impact of off-farm income on household energy expenditures in China: Implications for rural energy transition. Energy Policy 2019, 127, 248–258. [Google Scholar] [CrossRef]

- Deng, X.; Xu, D.; Qi, Y.; Zeng, M. Labor Off-Farm Employment and Cropland Abandonment in Rural China: Spatial Distribution and Empirical Analysis. Int. J. Environ. Res. Public Health 2018, 15, 1808. [Google Scholar] [CrossRef] [PubMed]

- World Bank. World Development Indicators 2015; World Bank: Washington, DC, USA, 2015. [Google Scholar]

- Asante-Addo, C.; Mockshell, J.; Zeller, M.; Siddig, K.; Egyir, I.S. Agricultural credit provision: What really determines farmers’ participation and credit rationing? Agric. Financ. Rev. 2017, 77, 239–256. [Google Scholar] [CrossRef]

- Amenyogbe, E.; Chen, G.; Wang, Z.; Lin, M.; Lu, X.; Atujona, D.; Abarike, E.D. A Review of Ghanas Aquaculture Industry. J. Aquac. Res. Dev. 2018, 9, 1–6. [Google Scholar] [CrossRef]

- Stiglitz, J.; Weiss, A. Credit rationing in markets with imperfect information. Am. Econ. Rev. 1981, 71, 393–410. [Google Scholar]

- Yaron, J.; Anderson, J.-R.; de-Haan, C. (Eds.) Rural Finance in Developing Countries; World Bank Policy Research Dissemination Press: Washington, DC, USA, 1992; pp. 31–44. [Google Scholar]

- Linh, T.N.; Long, H.T.; Van Chi, L.; Tam, L.T.; Lebailly, P. Access to Rural Credit Markets in Developing Countries, the Case of Vietnam: A Literature Review. Sustainability 2019, 11, 1468. [Google Scholar] [CrossRef]

- Chandio, A.A.; Jiang, Y. Determinants of Credit Constraints: Evidence from Sindh, Pakistan. Emerg. Mark. Financ. Trade 2018, 54, 3401–3410. [Google Scholar] [CrossRef]

- Mukherjee, S. Access to Formal Banks and New Technology Adoption: Evidence from India. Am. J. Agric. Econ. 2020, 102, 1532–1556. [Google Scholar] [CrossRef]

- Jia, X.; Xiang, C.; Huang, J. Microfinance, self-employment, and entrepreneurs in less developed areas of rural China. China Econ. Rev. 2013, 27, 94–103. [Google Scholar] [CrossRef]

- Shoji, M.; Aoyagi, K.; Kasahara, R.; Sawada, Y.; Ueyama, M. Social Capital Formation and Credit Access: Evidence from Sri Lanka. World Dev. 2012, 40, 2522–2536. [Google Scholar] [CrossRef]

- Ali, D.A.; Deininger, K. Causes and Implications of Credit Rationing in Rural Ethiopia: The Importance of Zonal Variation. J. Afr. Econ. 2014, 23, 493–527. [Google Scholar] [CrossRef]

- Nakano, Y.; Magezi, E.F. The impact of microcredit on agricultural technology adoption and productivity: Evidence from randomized control trial in Tanzania. World Dev. 2020, 133, 104997. [Google Scholar] [CrossRef]

- Shiferaw, B.; Kebede, T.; Kassie, M.; Fisher, M. Market imperfections, access to information and technology adoption in Uganda: Challenges of overcoming multiple constraints. Agric. Econ. 2015, 46, 475–488. [Google Scholar] [CrossRef]

- Alia, D.Y.; Diagne, A.; Adegbola, P.; Kinkingninhoun, F. Distributional Impact of Agricultural Technology Adoption on Rice Farmers’ Expenditure: The Case of Nigeria in Benin. J. African Dev. 2018, 20, 91–103. [Google Scholar] [CrossRef]

- Li, X.; Gan, C.; Hu, B. Accessibility to microcredit by Chinese rural households. J. Asian Econ. 2011, 22, 235–246. [Google Scholar] [CrossRef]

- Bogan, V.L.; Turvey, C.G.; Salazar, G. The Elasticity of Demand for Microcredit: Evidence from Latin America. Dev. Policy Rev. 2015, 33, 725–757. [Google Scholar] [CrossRef]

- Danquah, M.; Quartey, P.; Iddrisu, A.M. Access to Financial Services Via Rural and Community Banks and Poverty Reduction in Rural Households in Ghana. J. Afr. Dev. 2017, 19, 67–76. [Google Scholar] [CrossRef]

- Lin, L.; Wang, W.; Gan, C.; Nguyen, Q.T.T. Credit Constraints on Farm Household Welfare in Rural China: Evidence from Fujian Province. Sustainability 2019, 11, 3221. [Google Scholar] [CrossRef]

- Kim, J.Y. Investing in Opportunity Ending Poverty; World Bank: Washington, DC, USA, 2018; p. 97. [Google Scholar]

- Sana, M.; Massey, D.S. Household Composition, Family Migration, and Community Context: Migrant Remittances in Four Countries*. Soc. Sci. Q. 2005, 86, 509–528. [Google Scholar] [CrossRef]

- Mariyono, J. Micro-credit as catalyst for improving rural livelihoods through agribusiness sector in Indonesia. J. Entrep. Emerg. Econ. 2019, 11, 98–121. [Google Scholar] [CrossRef]

- Etea, B.G.; Zhou, D.; Abebe, K.A.; Sedebo, D.A. Is income diversification a means of survival or accumulation? Evidence from rural and semi-urban households in Ethiopia. Environ. Dev. Sustain. 2020, 22, 5751–5769. [Google Scholar] [CrossRef]

- Ma, W.; Abdulai, A.; Ma, C. The effects of off-farm work on fertilizer and pesticide expenditures in China. Rev. Dev. Econ. 2018, 22, 573–591. [Google Scholar] [CrossRef]

- Hussain, A.; Thapa, G.B. Smallholders’ access to agricultural credit in Pakistan. Food Secur. 2012, 4, 73–85. [Google Scholar] [CrossRef]

- MoFA. Ghana-Ghana Agricultural Production Survey (Minor Season) 2013, Second Round. 2014. Available online: http://www.statsghana.gov.gh/nada/index.php (accessed on 20 October 2021).

- Ghana Statistical Service. Ghana Living Standards Survey Round 7 (GLSS 7): Main Report; Ghana Statistical Service: Accra, Ghana, 2019.

- Kotrlik, J.; Higgins, C.; Bartlett, J.E. Organizational research: Determining appropriate sample size in survey research appropriate sample size in survey research. Inf. Technol. Learn. Perform. J. 2001, 19, 1. [Google Scholar]

- Cohen, J. Integrating the Real and Financial via the Linkage of Financial Flow. J. Financ. 1968, 23, 1–27. [Google Scholar] [CrossRef]

- Foster, G.; Kalenkoski, C.M. Tobit or OLS? An empirical evaluation under different diary window lengths. Appl. Econ. 2013, 45, 2994–3010. [Google Scholar] [CrossRef]

- Wilsont, C.; Tisdell, C.A. OLS and Tobit Estimates: When is Substitution Defensible Operationally? In Economic Theory, Applications and Issues: Working Paper; The University of Queensland: Brisbane, Australia, 2002; p. 15. [Google Scholar]

- Ma, W.; Nie, P.; Zhang, P.; Renwick, A. Impact of Internet use on economic well-being of rural households: Evidence from China. Rev. Dev. Econ. 2020, 24, 503–523. [Google Scholar] [CrossRef]

- Tesfaye, W.; Tirivayi, N. The impacts of postharvest storage innovations on food security and welfare in Ethiopia. Food Policy 2018, 75, 52–67. [Google Scholar] [CrossRef]

- Twumasi, M.A.; Jiang, Y.; Zhou, X.; Addai, B.; Darfor, K.N.; Akaba, S.; Fosu, P. Increasing Ghanaian fish farms’ productivity: Does the use of the internet matter? Mar. Policy 2021, 125, 104385. [Google Scholar] [CrossRef]

- Ma, W.; Zhu, Z. Internet use and willingness to participate in garbage classification: An investigation of Chinese residents. Appl. Econ. Lett. 2020, 28, 788–793. [Google Scholar] [CrossRef]

- Pfeiffer, L.; López-Feldman, A.; Taylor, J.E. Is off-farm income reforming the farm? Evidence from Mexico. Agric. Econ. 2009, 40, 125–138. [Google Scholar] [CrossRef]

- Fink, G.; Masiye, F. Health and agricultural productivity: Evidence from Zambia. J. Health Econ. 2015, 42, 151–164. [Google Scholar] [CrossRef] [PubMed]

- Lokshin, M.; Sajaia, Z. Maximum Likelihood Estimation of Endogenous Switching Regression Models. Stata J. 2004, 4, 282–289. [Google Scholar] [CrossRef]

- Rees, H.; Maddala, G.S. Limited-Dependent and Qualitative Variables in Econometrics. Econ. J. 1985, 95, 493. [Google Scholar] [CrossRef]

- Greene, W.W.H. Econometric Analysis, 7th ed.; Prentice-Hall: Hoboken, NJ, USA, 2012; ISBN 978-0-273-75356-8. [Google Scholar]

- Wooldridge, J.M. Control Function Methods in Applied Econometrics. J. Hum. Resour. 2015, 50, 420–445. [Google Scholar] [CrossRef]

- Tang, S.; Guo, S. Formal and informal credit markets and rural credit demand in China. In Proceedings of the 4th International Conference on Industrial Economics System and Industrial Security Engineering (IEIS 2017), Kyoto, Japan, 24–27 July 2017. [Google Scholar]

- Twumasi, M.A.; Jiang, Y.; Asante, D.; Addai, B.; Akuamoah-Boateng, S.; Fosu, P. Internet use and farm households food and nutrition security nexus: The case of rural Ghana. Technol. Soc. 2021, 65, 101592. [Google Scholar] [CrossRef]

- Liu, Y.; Renwick, A.; Fu, X. Off-farm income and food expenditure of rural households in China. Br. Food J. 2019, 121, 1088–1100. [Google Scholar] [CrossRef]

- Leng, C.; Ma, W.; Tang, J.; Zhu, Z. ICT adoption and income diversification among rural households in China. Appl. Econ. 2020, 52, 3614–3628. [Google Scholar] [CrossRef]

- Babatunde, R.O.; Qaim, M. Impact of off-farm income on food security and nutrition in Nigeria. Food Policy 2010, 35, 303–311. [Google Scholar] [CrossRef]

- Dedehouanou, S.F.A.; Araar, A.; Ousseini, A.; Harouna, A.L.; Jabir, M. Spillovers from off-farm self-employment opportunities in rural Niger. World Dev. 2018, 105, 428–442. [Google Scholar] [CrossRef]

- Twumasi, M.A.; Jiang, Y. The impact of climate change coping and adaptation strategies on livestock farmers’ technical efficiency: The case of rural Ghana. Environ. Sci. Pollut. Res. 2021, 28, 14386–14400. [Google Scholar] [CrossRef] [PubMed]

- Bocher, T.F.; Alemu, B.A.; Kelbore, Z.G. Does access to credit improve household welfare? Evidence from Ethiopia using endogenous regime switching regression. Afr. J. Econ. Manag. Stud. 2017, 8, 51–65. [Google Scholar] [CrossRef]

| Variables | Definitions and Assignment | Mean | S.D |

|---|---|---|---|

| Agriculture CF proportion | The share of household’s agriculture CF | 0.42 | 0.25 |

| Agriculture CF amount (GH¢) | Amount of fungible agriculture credit | 600.35 | 637.17 |

| Margin of farm Investment amount (GH¢) | Amount of agriculture credit on farm investment | 826.05 | 603.11 |

| Margin of farm Investment amount proportion | The share of household’s margin of farm investment | 0.58 | 0.25 |

| Credit received (GH¢) | Amount of agriculture credit received | 1426.40 | 1029.73 |

| Off-farm employment | Whether the respondent had any off-farm employment (1 = yes, 0 = otherwise) | 0.52 | 0.50 |

| Gender | Whether the respondent is a male (1 = yes, 0 = otherwise) | 0.70 | 0.46 |

| Marrital Status | Whether the respondent is married (1 = yes; 0 otherwise) | 0.63 | 0.54 |

| Age | Respondent age (numbers) | 41.72 | 12.20 |

| Education | Whether the respondent had high school education (1 = yes; 0 otherwise) | 0.43 | 0.49 |

| Remittances | Whether the respondent has received remittances in past years (1 = yes; 0 otherwise) | 0.46 | 0.49 |

| Household Size | Number of members in the household(number) | 4.68 | 1.97 |

| Credit source | Whether the respondent obtained credit from formal source (1 = yes; 0 otherwise) | 0.44 | 0.47 |

| Loan payback period | Whether the respondents feel that the loan payback period is long (1 = yes; 0 otherwise) | 0.33 | 0.47 |

| Farm size | Respondent farm size (in acres) | 3.34 | 1.87 |

| Social network | Whether the respondent has a link with relatives in the city; 0 otherwise | 0.57 | 0.49 |

| Variables | Pool Sample | Farmers with Off-Farm Job Model 1 | Male Farmers with Off-Farm Job Model 2 | Female Farmers with Off-Farm Job Model 3 | ||||||

|---|---|---|---|---|---|---|---|---|---|---|

| Total | Yes | No | Diff | Yes | No | Diff | Yes | No | Diff | |

| 1426.4 (1029.7) | 1305.2 (968.6) | 1552.0 (1076.8) | 246.8 *** | 1381.8 (983.4) | 1452.1 (1055.9) | 70.3 | 1186.1 (955.3) | 1469 (1037.5) | 282.9 ** | |

| 600.3 (637.1) | 422.3 (515.0) | 784.7 (697.2) | 362.4 *** | 473.7 (558.9) | 673.3 (668.1) | 199.6 *** | 357 (446.9) | 643.4 (656.2) | 286.4 *** | |

| 826.1 (603.1) | 882.9 (618.4) | 767.3 (582.1) | −115.6 *** | 908.13 (604.53) | 778.79 (598.03) | −129.35 ** | 829.1 (643.3) | 825.5 (596.4) | −3.6 | |

| 42.10 | 32.4 | 50.4 | 34.3 | 46.4 | 30.1 | 43.8 | ||||

| 57.90 | 67.6 | 49.4 | 65.7 | 53.6 | 69.9 | 56.2 | ||||

| Mean Share of Agriculture CF (ESR) | Treatment Effect | t-Value | ||

|---|---|---|---|---|

| Off-Farm Employment | Non-Off-Farm Employment | |||

| Off-farm employment | 0.3013 | 0.4825 | ATT = −0.1812 | −7.94 *** |

| Non-off-farm employment | 0.4118 | 0.5322 | ATU = −0.1204 | −3.91 *** |

| Heterogeneity effects | −0.1105 | −0.0497 | −0.0608 | |

| Mean Share of Agriculture CF (PSM a) | ||||

| Off-farm employment | 0.3148 | 0.4209 | ATT = −0.1061 | −11.67 *** |

| The Share of Agriculture CF Mean | |||||

|---|---|---|---|---|---|

| Variables | Off-Farm Employment | Non-Off-Farm Employment | ATTESR | t-Value | |

| Source of credit | Formal | 0.3788 (0.0124) | 0.5007 (0.0319) | −0.1219 | −12.15 *** |

| Informal | 0.3021 (0.1120) | 0.4819 (0.0455) | −0.1798 | −8.81 *** | |

| Gender | Male | 0.4570 (0.0662) | 0.5144 (0.2491) | −0.0574 | −16.13 *** |

| Female | 0.3429 (1.3821) | 0.4703 (0.0574) | −0.1274 | −7.41 *** | |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2022 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Ankrah Twumasi, M.; Chandio, A.A.; Sargani, G.R.; Asare, I.; Zhang, H. Off-Farm Employment and Agricultural Credit Fungibility Nexus in Rural Ghana. Sustainability 2022, 14, 9109. https://doi.org/10.3390/su14159109

Ankrah Twumasi M, Chandio AA, Sargani GR, Asare I, Zhang H. Off-Farm Employment and Agricultural Credit Fungibility Nexus in Rural Ghana. Sustainability. 2022; 14(15):9109. https://doi.org/10.3390/su14159109

Chicago/Turabian StyleAnkrah Twumasi, Martinson, Abbas Ali Chandio, Ghulam Raza Sargani, Isaac Asare, and Huaquan Zhang. 2022. "Off-Farm Employment and Agricultural Credit Fungibility Nexus in Rural Ghana" Sustainability 14, no. 15: 9109. https://doi.org/10.3390/su14159109

APA StyleAnkrah Twumasi, M., Chandio, A. A., Sargani, G. R., Asare, I., & Zhang, H. (2022). Off-Farm Employment and Agricultural Credit Fungibility Nexus in Rural Ghana. Sustainability, 14(15), 9109. https://doi.org/10.3390/su14159109