Benefit–Risk Perceptions of FinTech Adoption for Sustainability from Bank Consumers’ Perspective: The Moderating Role of Fear of COVID-19

Abstract

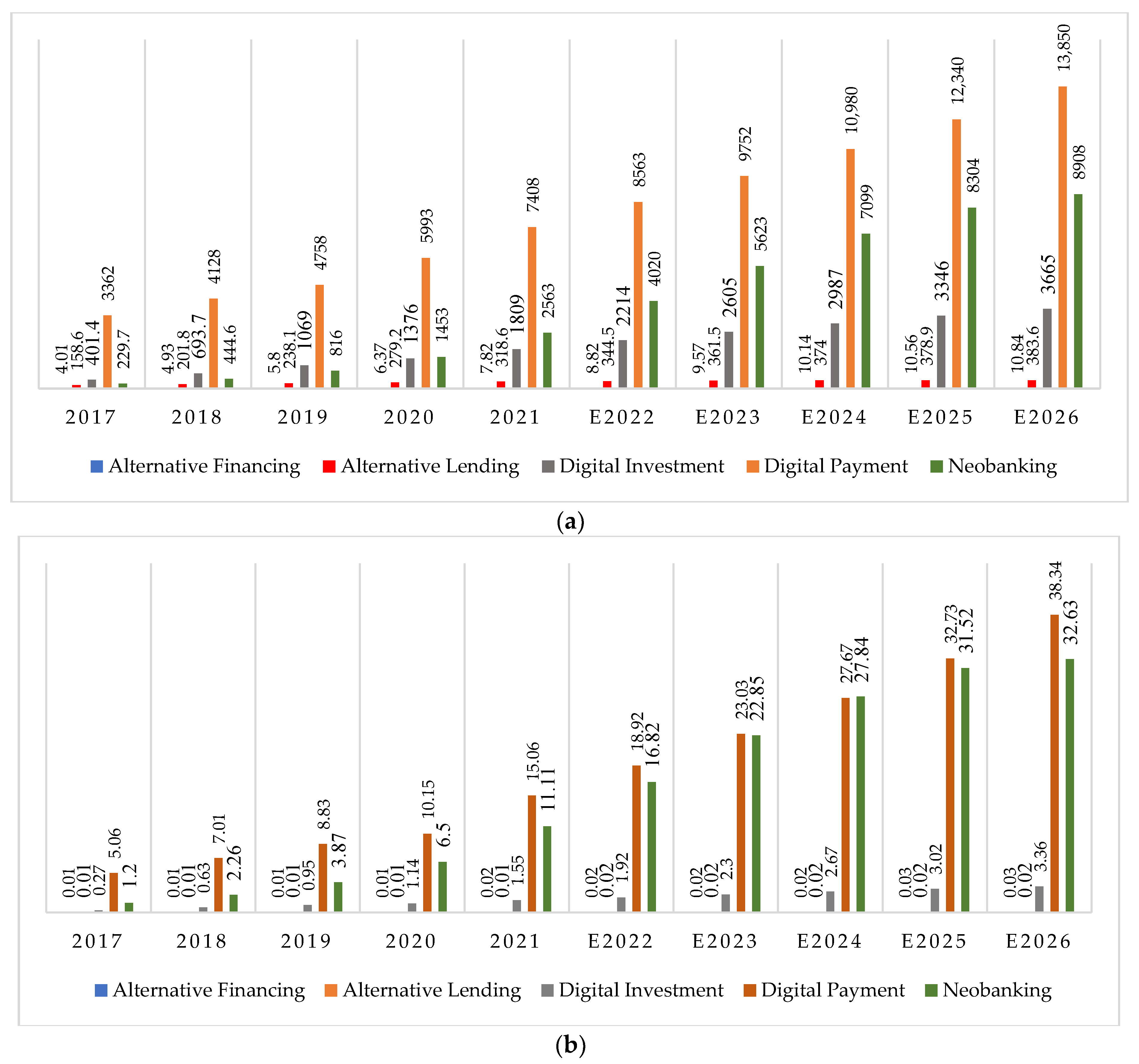

:1. Introduction

- (1)

- To examine whether perceived benefit and risk significantly influence FinTech behavioral adoption;

- (2)

- To examine whether bank consumers’ fear of COVID-19 moderates the relationship between perceived benefit and risk with FinTech behavioral adoption;

- (3)

- To examine whether FinTech behavioral adoption contributes to sustainability.

2. Literature Review and Hypothesis Development

2.1. FinTech Behavioral Adoption in the Net Valence Framework

2.2. FinTech Adoption and Sustainability from an SIS Perspective

2.3. FinTech Adoption and Fear of COVID-19 from a PMT Perspective

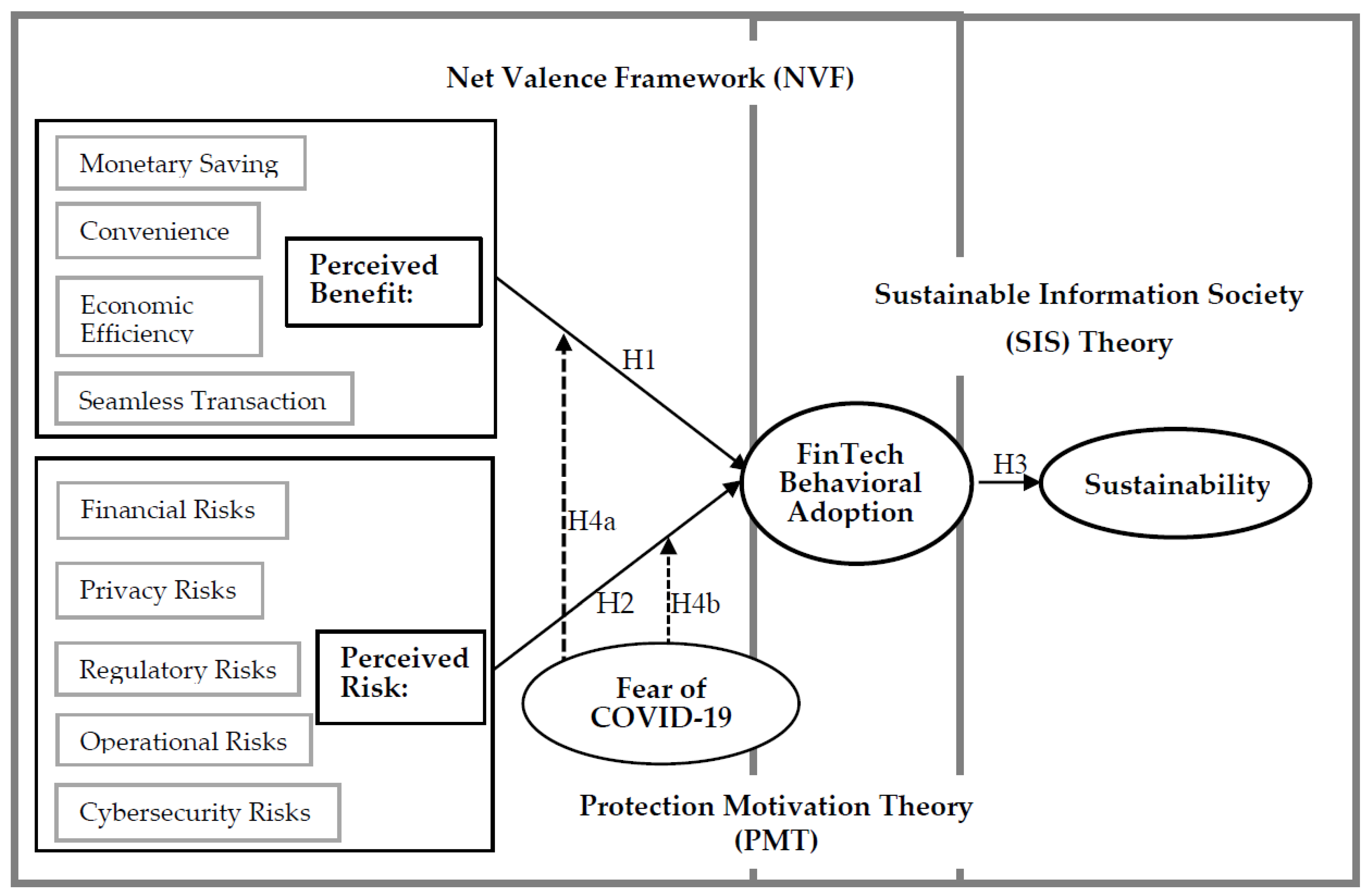

2.4. The Conceptual Framework

3. Methodology

3.1. Designing the Survey Instrument

3.2. Data Analytical Methods

3.3. Sampling for the Field Study

4. Results

4.1. Profile of Respondents

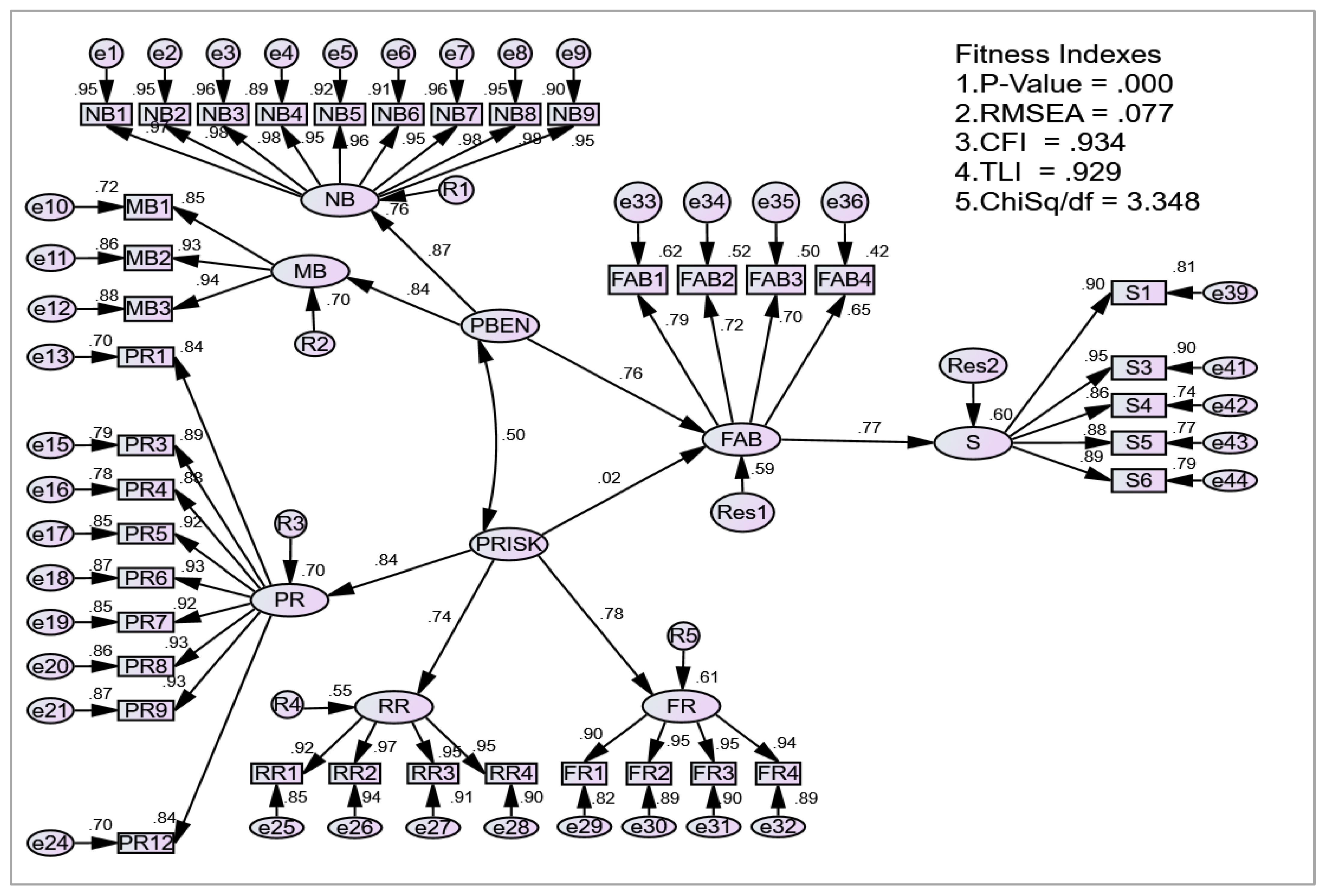

4.2. Results of the CFA Procedures

4.3. Results of SEM Path Analysis

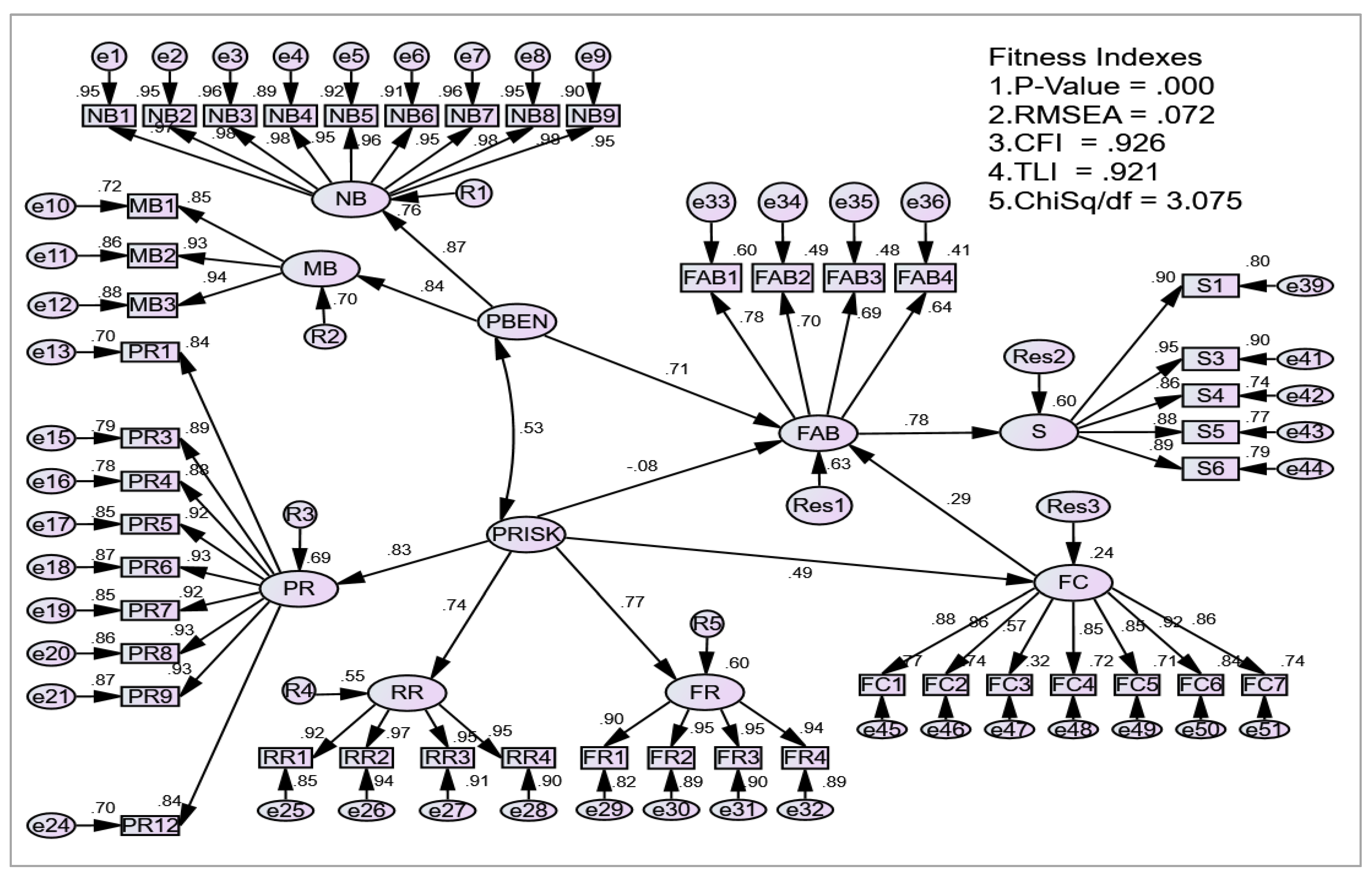

4.4. Results of MCFA on Moderator Effect of the Fear of COVID-19

4.5. Results of SEM Path Analysis on Mediation Effect of Fear of COVID-19

5. Discussion

6. Conclusions

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Acknowledgments

Conflicts of Interest

Appendix A

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Constructs | Code | Sub-Constructs and Item Statements | Sources |

|---|---|---|---|

| Perceived Benefits Construct | Non-monetary Benefits Dimension | ||

| NB1 | Using FinTech allows me to use financial services anytime | [11] | |

| NB2 | Using FinTech allows me to use financial services anywhere | [11] | |

| NB3 | Using FinTech makes it easier to access financial services | [19] | |

| NB4 | Using FinTech is easy for me (in setting up, configuring, and using the service) | [19] | |

| NB5 | Using FinTech is more convenient than traditional financial services | [30] | |

| NB6 | Using FinTech avoids much unnecessary hassle for me (e.g., going to the branches, avoiding traffic) | [16] | |

| NB7 | Using FinTech enables me to use financial services more quickly (contactless) | [19] | |

| NB8 | Using FinTech allows me to use financial services more effectively (save time and effort) | [19] | |

| NB9 | Using FinTech eliminates the time-consuming payment processes (the speed at checkout) | [16] | |

| Monetary Benefits Dimension | |||

| MB1 | Using FinTech allows me to save money (e.g., discounts, promotions, coupons) | [11] | |

| MB2 | Using FinTech allows me to use various financial services at a low cost | ||

| MB3 | Using FinTech allows me to expect financial gains (e.g., cashback, higher interest, vouchers, rewards) | ||

| Perceived Risk Construct | Personal Data Protection Risk Dimension | ||

| PR1 | Using FinTech makes me worried about the abuse of my financial information (e.g., transaction information) | [11] | |

| PR3 | Using FinTech makes me worried that other people might steal my account information | [11] | |

| PR4 | I think the cybersecurity risk is much higher using FinTech than traditional financial services | [11] | |

| PR5 | The chances of using FinTech and losing control over my personal information privacy are high | [16] | |

| PR6 | Signing up and using FinTech would lead me to lose privacy because my personal information would be used without my knowledge | [16] | |

| PR7 | I am concerned that FinTech is collecting too much personal information from me | [16] | |

| PR8 | I am concerned that FinTech allows unauthorized persons to hack into my personal information | [45] | |

| PR9 | Using FinTech, I am concerned about the privacy of my personal information during a transaction | [45] | |

| PR12 | I worry about the way FinTech providers respond to financial losses or financial information leakages | [45] | |

| Regulatory Risk Dimension | |||

| RR1 | I am reluctant to use FinTech due to insufficient regulations | [11] | |

| RR2 | I doubt FinTech due to its unclear legal status | ||

| RR3 | I doubt FinTech due to a lack of regulations | ||

| RR4 | It is difficult to use various FinTech applications due to the lack of regulations | ||

| Financial Risk Dimension | |||

| FR1 | Using FinTech, I am more likely to experience financial fraud or payment fraud | [11] | |

| FR2 | Using FinTech, I may suffer financial losses due to a lack of interoperability with other services | [11] | |

| FR3 | Using FinTech, I may suffer a monetary loss due to fluctuations in exchange rates | [45] | |

| FR4 | Using FinTech, I may suffer a monetary loss due to fluctuations in cryptocurrencies | [45] | |

| FinTech Behavioral Adoption * | To make payment … | ||

| FAB1 | I always use internet/online banking (using a browser, e.g., Maybank2u.com, CIMBclicks.com) | [58,59] | |

| FAB2 | I always use a mobile banking app (using a smartphone, e.g., Maybank app, CIMB app) | ||

| FAB3 | I always use contactless debit/credit/prepaid cards (e.g., PayWave, PayPass, ExpressPay) | ||

| FAB4 | I always use e-wallets (e.g., Touch’nGo, GrabPay, Boost, BigPay, WeChat Pay, AliPay, MAE) | ||

| Fear of COVID-19 | FC1 | I am afraid of COVID-19 | [27] |

| FC2 | It makes me uncomfortable to think about COVID-19 | ||

| FC3 | My hands become sweaty when I think about COVID-19 | ||

| FC4 | I am afraid of losing my life because of COVID-19 | ||

| FC5 | I feel uneasy when watching news and stories about COVID-19 on social media | ||

| FC6 | I worry about getting COVID-19 | ||

| FC7 | I am nervous when I think about getting COVID-19 | ||

| Sustainability | S1 | FinTech adoption could reduce costs (e.g., through lower purchase prices of goods/services on the internet, eliminating travel expenses, and lower costs of communication over the internet than telephone or personal communication) | [6] |

| S3 | FinTech adoption could expand existing knowledge and skills along with gaining new ones (e.g., including digital knowledge and skills, financial knowledge and awareness) | ||

| S4 | FinTech adoption could increase the security of people and social groups through access to information and dissemination of information on various dangers and risks (e.g., alerts on phishing, scam calls, pandemic-related issues) | ||

| S5 | FinTech adoption could reduce social exclusion due to age, education, place of residence, or disability, which causes difficult participation in banking and finance and limited or difficult access to financial services | ||

| S6 | FinTech adoption could reduce energy consumption (e.g., fuel) and increase protection of the environment through FinTech | ||

References

- Deng, X.; Huang, Z.; Cheng, X. FinTech and Sustainable Development: Evidence from China Based on P2P Data. Sustainability 2019, 11, 6434. [Google Scholar] [CrossRef] [Green Version]

- Oláh, J.; Aburumman, N.; Popp, J.; Khan, M.A.; Haddad, H.; Kitukutha, N. Impact of Industry 4.0 on Environmental Sustainability. Sustainability 2020, 12, 4674. [Google Scholar] [CrossRef]

- Khan, H.U.R.; Usman, B.; Zaman, K.; Nassani, A.A.; Haffar, M.; Muneer, G. The impact of carbon pricing, climate financing, and financial literacy on COVID-19 cases: Go-for-green healthcare policies. Environ. Sci. Pollut. Res. 2022, 29, 35884–35896. [Google Scholar] [CrossRef] [PubMed]

- UNSGSA. Annual Report to The Secretary-General September 2018. Financial Inclusion: Technology, Innovation, Progress; United Nations: New York, NY, USA, 2018; pp. 18–41. [Google Scholar]

- Moro-Visconti, R.; Rambaud, S.C.; Pascual, J.L. Sustainability in FinTechs: An Explanation through Business Model Scalability and Market Valuation. Sustainability 2020, 12, 10316. [Google Scholar] [CrossRef]

- Ziemba, E. The contribution of ICT adoption to sustainability: Households’ perspective. Inf. Technol. People 2019, 32, 731–753. [Google Scholar] [CrossRef]

- Dubey, R.; Gunasekaran, A.; Childe, S.J.; Papadopoulos, T.; Luo, Z.; Wamba, S.F.; Roubaud, D. Can big data and predictive analytics improve social and environmental sustainability? Technol. Forecast. Soc. Chang. 2019, 144, 534–545. [Google Scholar] [CrossRef]

- Senyo, P.; Osabutey, E.L. Unearthing antecedents to financial inclusion through FinTech innovations. Technovation 2020, 98, 102155. [Google Scholar] [CrossRef]

- Meiling, L.; Yahya, F.; Waqas, M.; Shaohua, Z.; Ali, S.A.; Hania, A. Boosting Sustainability in Healthcare Sector through Fintech: Analyzing the Moderating Role of Financial and ICT Development. Inq. J. Health Care Organ. Provis. Financ. 2021, 58, 469580211028174. [Google Scholar] [CrossRef]

- Shin, Y.J.; Choi, Y. Feasibility of the Fintech Industry as an Innovation Platform for Sustainable Economic Growth in Korea. Sustainability 2019, 11, 5351. [Google Scholar] [CrossRef] [Green Version]

- Ryu, H.-S. What makes users willing or hesitant to use Fintech? The moderating effect of user type. Ind. Manag. Data Syst. 2018, 118, 541–569. [Google Scholar] [CrossRef]

- Ryu, H.-S.; Ko, K.S. Sustainable Development of Fintech: Focused on Uncertainty and Perceived Quality Issues. Sustainability 2020, 12, 7669. [Google Scholar] [CrossRef]

- Stewart, H.; Jürjens, J. Data security and consumer trust in FinTech innovation in Germany. Inf. Comput. Secur. 2018, 26, 109–128. [Google Scholar] [CrossRef]

- Gbongli, K.; Peng, Y.; Ackah, O. Selection and ranking of Perceived Risk Associated with Mobile Banking in West Africa: An AHP Approach from Customers’ Perspective. Int. J. Sci. Eng. Res. 2016, 7, 80–86. [Google Scholar]

- Razzaque, A.; Cummings, R.T.; Karolak, M.; Hamdan, A. The Propensity to Use FinTech: Input from Bankers in the Kingdom of Bahrain. J. Inf. Knowl. Manag. 2020, 19, 2040025. [Google Scholar] [CrossRef]

- Breward, M.; Hassanein, K.; Head, M. Understanding Consumers’ Attitudes Toward Controversial Information Technologies: A Contextualization Approach. Inf. Syst. Res. 2017, 28, 760–774. [Google Scholar] [CrossRef]

- Ozturk, A.B.; Bilgihan, A.; Salehi-Esfahani, S.; Hua, N. Understanding the mobile payment technology acceptance based on valence theory. Int. J. Contemp. Hosp. Manag. 2017, 29, 2027–2049. [Google Scholar] [CrossRef]

- Al Nawayseh, M. FinTech in COVID-19 and Beyond: What Factors Are Affecting Customers’ Choice of FinTech Applications? J. Open Innov. Technol. Mark. Complex. 2020, 6, 153. [Google Scholar] [CrossRef]

- Ali, M.; Raza, S.A.; Khamis, B.; Puah, C.H.; Amin, H. How perceived risk, benefit and trust determine user Fintech adoption: A new dimension for Islamic finance. Foresight 2021, 23, 403–420. [Google Scholar] [CrossRef]

- Lee, J.-M.; Kim, H.-J. Determinants of adoption and continuance intentions toward Internet-only banks. Int. J. Bank Mark. 2020, 38, 843–865. [Google Scholar] [CrossRef]

- Onyiriuba, L. Bank Risk Management in Developing Economies, 2nd ed.; Elsevier: Amsterdam, The Netherlands, 2016. [Google Scholar]

- The Star. Malaysia Leads Mobile Wallet Usage in South-East Asia. Available online: https://www.thestar.com.my/business/business-news/2020/06/24/malaysia-leads-mobile-wallet-usage-in-south-east-asia (accessed on 24 June 2020).

- Laato, S.; Islam, A.N.; Farooq, A.; Dhir, A. Unusual purchasing behavior during the early stages of the COVID-19 pandemic: The stimulus-organism-response approach. J. Retail. Consum. Serv. 2020, 57, 102224. [Google Scholar] [CrossRef]

- Prentice, C.; Chen, J.; Stantic, B. Timed intervention in COVID-19 and panic buying. J. Retail. Consum. Serv. 2020, 57, 102203. [Google Scholar] [CrossRef]

- Pantano, E.; Pizzi, G.; Scarpi, D.; Dennis, C. Competing during a pandemic? Retailers’ ups and downs during the COVID-19 outbreak. J. Bus. Res. 2020, 116, 209–213. [Google Scholar] [CrossRef] [PubMed]

- Auer, R.; Cornelli, G.; Frost, J. COVID-19, Cash, and the Future of Payments. BIS Bull. 2020, 3, 7. [Google Scholar]

- Fu, J.; Mishra, M. The Global Impact of COVID-19 on Fintech Adoption; Swiss Finance Institute Research Paper 20-38; University of Zurich: Zürich, Switzerland, 2020. [Google Scholar] [CrossRef]

- Ahorsu, D.K.; Lin, C.; Imani, V.; Saffari, M.; Griffiths, M.D.; Pakpour, A.H. The Fear of COVID-19 Scale: Development and Initial Validation. Int. J. Ment. Health Addict. 2020, 20, 1537–1545. [Google Scholar] [CrossRef] [Green Version]

- Tamele, B.; Zamora-Pérez, A.; Litardi, C.; Howes, J.; Steinmann, E.; Todt, D. Catch Me (If You Can): Assessing the Risk of SARS-Cov-2 Transmission via Euro Cash; European Central Bank (ECB) Occasional Paper Series, 259; ECB: Frankfurt, Germany, 2021; p. 15. [Google Scholar]

- BNM. Financial Sector Blueprint 2011–2020; Bank Negara Malaysia: Kuala Lumpur, Malaysia, 2011; pp. 152–192. [Google Scholar]

- BNM. Financial Sector Blueprint 2022–2026; Bank Negara Malaysia: Kuala Lumpur, Malaysia, 2022; pp. 10–100. [Google Scholar]

- BNM. Malaysia Experience in Financial Inclusion: Unlocking Shared Benefits for All through Inclusive Finance; Bank Negara Malaysia: Kuala Lumpur, Malaysia, 2016; pp. 8–11. [Google Scholar]

- Peter, J.P.; Tarpey, S.L.X. A Comparative Analysis of Three Consumer Decision Strategies. J. Consum. Res. 1975, 2, 29–37. [Google Scholar] [CrossRef]

- Rogers, R.W. A Protection Motivation Theory of Fear Appeals and Attitude Change. J. Psychol. 1975, 91, 93–114. [Google Scholar] [CrossRef]

- Servaes, J.; Carpentier, N. Towards a sustainable information society. In Deconstructing WSIS; Intellect Ltd.: Portland, OR, USA, 2006; p. 7. [Google Scholar]

- Xie, J.; Ye, L.; Huang, W.; Ye, M. Understanding FinTech Platform Adoption: Impacts of Perceived Value and Perceived Risk. J. Theor. Appl. Electron. Commer. Res. 2021, 16, 1893–1911. [Google Scholar] [CrossRef]

- Hu, Z.; Ding, S.; Li, S.; Chen, L.; Yang, S. Adoption Intention of Fintech Services for Bank Users: An Empirical Examination with an Extended Technology Acceptance Model. Symmetry 2019, 11, 340. [Google Scholar] [CrossRef] [Green Version]

- Albayati, H.; Kim, S.K.; Rho, J.J. Accepting financial transactions using blockchain technology and cryptocurrency: A customer perspective approach. Technol. Soc. 2020, 62, 101320. [Google Scholar] [CrossRef]

- Mangini, E.R.; Silva, N.G.; De Carvalho, J.R.C. Os bancos virtuais e avaliação do risco percebido e das expectativas de desempenho e de esforço na intenção comportamental. Rev. Bras. De Mark. 2020, 19, 838–861. [Google Scholar] [CrossRef]

- Barbu, C.; Florea, D.; Dabija, D.-C.; Barbu, M. Customer Experience in Fintech. J. Theor. Appl. Electron. Commer. Res. 2021, 16, 1415–1433. [Google Scholar] [CrossRef]

- Museba, T.J.; Ranganai, E.; Gianfrate, G. Customer perception of adoption and use of digital financial services and mobile money services in Uganda. J. Enterp. Communities People Places Glob. Econ. 2021, 15, 177–203. [Google Scholar] [CrossRef]

- Kassim, N.M.; Ramayah, T. A Measurement Model of Risk Perception in Internet Banking Based on Malaysian Context. ARPN J. Eng. Appl. Sci. 2015, 10, 17635. [Google Scholar]

- Schindler, J. FinTech and Financial Innovation: Drivers and Depth. In Finance and Economics Discussion Series 2017-081; Board of Governors of the Federal Reserve System: Washington, DC, USA, 2017. [Google Scholar] [CrossRef]

- Stone, R.N.; Grønhaug, K. Perceived Risk: Further Considerations for the Marketing Discipline. Eur. J. Mark. 1993, 27, 39–50. [Google Scholar] [CrossRef]

- Bauer, R. Consumer Behavior as Risk Taking. In Risk Taking and Information Handling in Consumer Behavior; Cox, D., Ed.; Harvard University Press: Cambridge, MA, USA, 1967. [Google Scholar]

- Mou, J.; Cohen, J.; Dou, Y.; Zhang, B. International buyers’ repurchase intentions in a Chinese cross-border e-commerce platform. Internet Res. 2019, 30, 403–437. [Google Scholar] [CrossRef]

- Sullivan, Y.W.; Kim, D.J. Assessing the effects of consumers’ product evaluations and trust on repurchase intention in e-commerce environments. Int. J. Inf. Manag. 2018, 39, 199–219. [Google Scholar] [CrossRef]

- Gomber, P.; Kauffman, R.J.; Parker, C.; Weber, B.W. On the Fintech Revolution: Interpreting the Forces of Innovation, Disruption, and Transformation in Financial Services. J. Manag. Inf. Syst. 2018, 35, 220–265. [Google Scholar] [CrossRef]

- Weiser, P.; Scheider, S.; Bucher, D.; Kiefer, P.; Raubal, M. Towards sustainable mobility behavior: Research challenges for location-aware information and communication technology. GeoInformatica 2016, 20, 213–239. [Google Scholar] [CrossRef]

- UNWCED. Report of the World Commission on Environment and Development. In Our Common Future; Oxford University Press: Oxford, UK, 1987; p. 41. [Google Scholar]

- Aker, J.C.; Boumnijel, R.; McClelland, A.; Tierney, N. Payment Mechanisms and Antipoverty Programs: Evidence from a Mobile Money Cash Transfer Experiment in Niger. Econ. Dev. Cult. Chang. 2016, 65, 1–37. [Google Scholar] [CrossRef] [Green Version]

- Chikalipah, S. The pyrrhic victory of FinTech and its implications for achieving the Sustainable Development Goals: Evidence from fieldwork in rural Zambia. World J. Sci. Technol. Sustain. Dev. 2020, 17, 329–340. [Google Scholar] [CrossRef]

- Suri, T.; Bharadwaj, P.; Jack, W. Fintech and household resilience to shocks: Evidence from digital loans in Kenya. J. Dev. Econ. 2021, 153, 102697. [Google Scholar] [CrossRef]

- Buckley, R.P.; Webster, S. Fintech in Developing Countries: Charting New Customer Journeys. Capco Inst. J. Financ. Transform. 2016, 44, 151–159. Available online: https://www.capco.com/Capco-Institute/Journal-44-Financial-Technology (accessed on 5 July 2022).

- Vasenska, I.; Dimitrov, P.; Koyundzhiyska-Davidkova, B.; Krastev, V.; Durana, P.; Poulaki, I. Financial Transactions Using FINTECH during the Covid-19 Crisis in Bulgaria. Risks 2021, 9, 48. [Google Scholar] [CrossRef]

- MacKenzie, A. The Fintech Revolution. Lond. Bus. Sch. Rev. 2015, 26, 50–53. [Google Scholar] [CrossRef]

- Kashif, M.; Rehman, M.A.; Pilelienė, L. Customer perceived service quality and loyalty in Islamic banks. TQM J. 2016, 28, 62–78. [Google Scholar] [CrossRef]

- Venkatesh, V.; Morris, M.G.; Davis, G.B.; Davis, F.D. User Acceptance of Information Technology: Toward a Unified View. MIS Q. 2003, 27, 425–478. [Google Scholar] [CrossRef] [Green Version]

- Ziemba, E. The Contribution of ICT Adoption to the Sustainable Information Society. J. Comput. Inf. Syst. 2017, 59, 116–126. [Google Scholar] [CrossRef]

- Awang, Z.; Afthanorhan, A.; Mamat, M. The Likert Scale Analysis Using Parametric based Structural Equation Modelling (SEM). Comput. Methods Soc. Sci. 2016, 4, 13–21. [Google Scholar]

- Hair, J.F., Jr.; Hult, G.T.M.; Ringle, C.; Sarstedt, M. A Primer on Partial Least Squares Structural Equation Modeling (PLS-SEM); Sage Publications: Los Angeles, CA, USA, 2016. [Google Scholar]

- Afthanorhan, A.; Awang, Z.; Majid, N.A.; Foziah, H.; Ismail, I.; Al Halbusi, H.; Tehseen, S. Gain More Insight from Common Latent Factor in Structural Equation Modeling. J. Phys. Conf. Ser. 2021, 1793, 012030. [Google Scholar] [CrossRef]

- Wolf, E.J.; Harrington, K.; Clark, S.L.; Miller, M. Sample Size Requirements for Structural Equation Models. Educ. Psychol. Meas. 2013, 73, 913–934. [Google Scholar] [CrossRef]

- Hair, J.F.; Black, W.C.; Babin, B.J.; Anderson, R.E. Multivariate Data Analysis, 8th ed.; Pearson Prentice Hall: Hoboken, NJ, USA, 2019. [Google Scholar]

| Demographic/Characteristics | Frequency | % | Demographic/Characteristics | Frequency | % |

|---|---|---|---|---|---|

| Gender: | Age: | ||||

| Male | 129 | 32.3 | 18–21 years | 95 | 23.8 |

| Female | 271 | 67.8 | 22–25 years | 194 | 48.5 |

| Total | 400 | 100 | 26–29 years | 27 | 6.8 |

| 30–34 years | 28 | 7.0 | |||

| Highest Education Level: | 35–39 years | 16 | 4.0 | ||

| SPM/STPM/STAM a | 33 | 8.4 | 40–49 years | 23 | 5.8 |

| A-level/Foundation/Matriculation | 4 | 1.2 | 50 years and older | 17 | 4.3 |

| Diploma | 34 | 4.6 | Total | 400 | 100 |

| Bachelor | 259 | 64.8 | |||

| Master and Professional Certificate | 70 | 17.6 | Main Profession Category: | ||

| Total | 400 | 100 | Professionals in the Tech field b | 34 | 8.5 |

| Other Professionals c | 58 | 14.5 | |||

| Total monthly income: | Management | 31 | 7.8 | ||

| MYR 1000 or less | 237 | 59.3 | Technical staff and technician | 6 | 1.5 |

| MYR 1001 to MYR 3000 | 68 | 17.0 | Front line employees | 3 | 0.8 |

| MYR 3001 to MYR 5000 | 45 | 11.3 | Business owner (online) | 4 | 1.0 |

| MYR 5001 to MYR 8000 | 31 | 7.8 | Business owner (offline) | 5 | 1.3 |

| MYR 8001 to MYR 10,000 | 7 | 1.8 | Student | 247 | 61.8 |

| More than MYR 10,000 | 12 | 3.0 | Do not work | 12 | 3.0 |

| Total | 400 | 100 | Total | 400 | 100 |

| Construct (Abbreviation) | Sub-Construct/Item-Label | Factor Loading | AVE (above 0.5) | CR (above 0.6) |

|---|---|---|---|---|

| (1) Perceived Benefits (PBEN) | Non-monetary benefits Monetary benefits | 0.869 0.836 | 0.727 | 0.842 |

| Non-monetary benefits (NBs) | NB1 NB2 NB3 NB4 NB5 NB6 NB7 NB8 NB9 | 0.975 0.976 0.982 0.945 0.962 0.952 0.982 0.977 0.951 | 0.935 | 0.992 |

| Monetary benefits (MBs) | MB1 MB2 MB3 | 0.847 0.927 0.937 | 0.818 | 0.931 |

| (2) Perceived Risk (PRISK) | Personal Data Protection Risk Regulatory Risk Financial Risk | 0.832 0.747 0.778 | 0.619 | 0.829 |

| Personal Data Protection Risk (PR) | PR1 PR2 PR3 PR4 PR5 PR6 PR7 PR8 PR9 PR10 PR11 PR12 | 0.839 removed 0.888 0.881 0.921 0.932 0.920 0.925 0.931 removed removed 0.839 | 0.806 | 0.974 |

| Regulatory Risk (RR) | RR1 RR2 RR3 RR4 | 0.920 0.967 0.954 0.947 | 0.897 | 0.972 |

| Financial Risk (FR) | FR1 FR2 FR3 FR4 | 0.904 0.945 0.946 0.944 | 0.874 | 0.965 |

| (3) FinTech Behavioral Adoption of Basic FinTech Services (FAB) | FAB1 FAB2 FAB3 FAB4 | 0.780 0.745 0.755 0.673 | 0.547 | 0.828 |

| Adoption of Advanced FinTech Services (FAA) | FAA1 FAA2 | removed removed | ||

| (4) Fear of COVID-19 (FC) | FC1 FC2 FC3 FC4 FC5 FC6 FC7 | 0.881 0.859 0.565 0.848 0.844 0.920 0.857 | 0.692 | 0.939 |

| (5) Sustainability (S) | S1 S2 S3 S4 S5 S6 S7 S8 S9 | 0.901 removed 0.948 0.860 0.879 0.892 removed removed removed | 0.804 | 0.953 |

| Construct | Perceived Benefits | Perceived Risk | FinTech Behavioral Adoption | Fear of COVID-19 | Sustainability |

|---|---|---|---|---|---|

| Perceived Benefits | 0.853 | ||||

| Perceived Risk | 0.502 | 0.787 | |||

| FinTech Behavioral Adoption | 0.678 | 0.329 | 0.740 | ||

| Fear of COVID-19 | 0.429 | 0.467 | 0.468 | 0.832 | |

| Sustainability | 0.762 | 0.466 | 0.698 | 0.484 | 0.897 |

| Construct | Path | Construct | Estimate | SE. | CR. | Prob. | Result |

|---|---|---|---|---|---|---|---|

| Perceived Benefits | → | FinTech Behavioral Adoption | 0.693 | 0.061 | 11.357 | *** | Significant |

| Perceived Risk | → | FinTech Behavioral Adoption | 0.023 | 0.055 | 0.419 | 0.676 | Not Significant |

| FinTech Behavioral Adoption | → | Sustainability | 0.856 | 0.059 | 14.462 | *** | Significant |

| Level of COVID-19 Fear | Tests | Constrained Model | Unconstrained Model | Chi-Square Difference | Result on Moderation |

|---|---|---|---|---|---|

| Low-fear group | Chi-square | 1814.570 | 1810.295 | 4.28 | Significant |

| df | 660 | 659 | 1 | ||

| High-fear group | Chi-square | 1603.672 | 1563.507 | 40.17 | Significant |

| df | 660 | 659 | 1 |

| Construct | Path | Construct | Estimate (β) | Std. Estimate (β) | Prob. | Result |

|---|---|---|---|---|---|---|

| Perceived Risk | → | Fear of COVID-19 | 0.640 | 0.491 | *** | Significant |

| Fear of COVID-19 | → | FinTech Behavioral Adoption | 0.212 | 0.292 | *** | Significant |

| Perceived Risk | → | FinTech Behavioral Adoption | −0.077 | −0.082 | 0.208 | Not significant |

| Statistics | Indirect Effect | Direct Effect |

|---|---|---|

| Bootstrapping Estimate | 0.143 | −0.082 |

| Bootstrapping p-value | 0.001 | 0.241 |

| Results | Significant | Not significant |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2022 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Abdul-Rahim, R.; Bohari, S.A.; Aman, A.; Awang, Z. Benefit–Risk Perceptions of FinTech Adoption for Sustainability from Bank Consumers’ Perspective: The Moderating Role of Fear of COVID-19. Sustainability 2022, 14, 8357. https://doi.org/10.3390/su14148357

Abdul-Rahim R, Bohari SA, Aman A, Awang Z. Benefit–Risk Perceptions of FinTech Adoption for Sustainability from Bank Consumers’ Perspective: The Moderating Role of Fear of COVID-19. Sustainability. 2022; 14(14):8357. https://doi.org/10.3390/su14148357

Chicago/Turabian StyleAbdul-Rahim, Ruzita, Siti Aisah Bohari, Aini Aman, and Zainudin Awang. 2022. "Benefit–Risk Perceptions of FinTech Adoption for Sustainability from Bank Consumers’ Perspective: The Moderating Role of Fear of COVID-19" Sustainability 14, no. 14: 8357. https://doi.org/10.3390/su14148357

APA StyleAbdul-Rahim, R., Bohari, S. A., Aman, A., & Awang, Z. (2022). Benefit–Risk Perceptions of FinTech Adoption for Sustainability from Bank Consumers’ Perspective: The Moderating Role of Fear of COVID-19. Sustainability, 14(14), 8357. https://doi.org/10.3390/su14148357