ESG and Firm Performance: Focusing on the Environmental Strategy

Abstract

:1. Introduction

2. Theoretical Background and Hypotheses

2.1. Institutional Theory and Eco-Friendly Strategy

2.2. Eco-Friendly Strategy and Firm Performance

2.3. Excess Growth and Firm Performance

2.4. Eco-Friendly Strategy and Disparate Firm Performance by Industry

3. Methodology

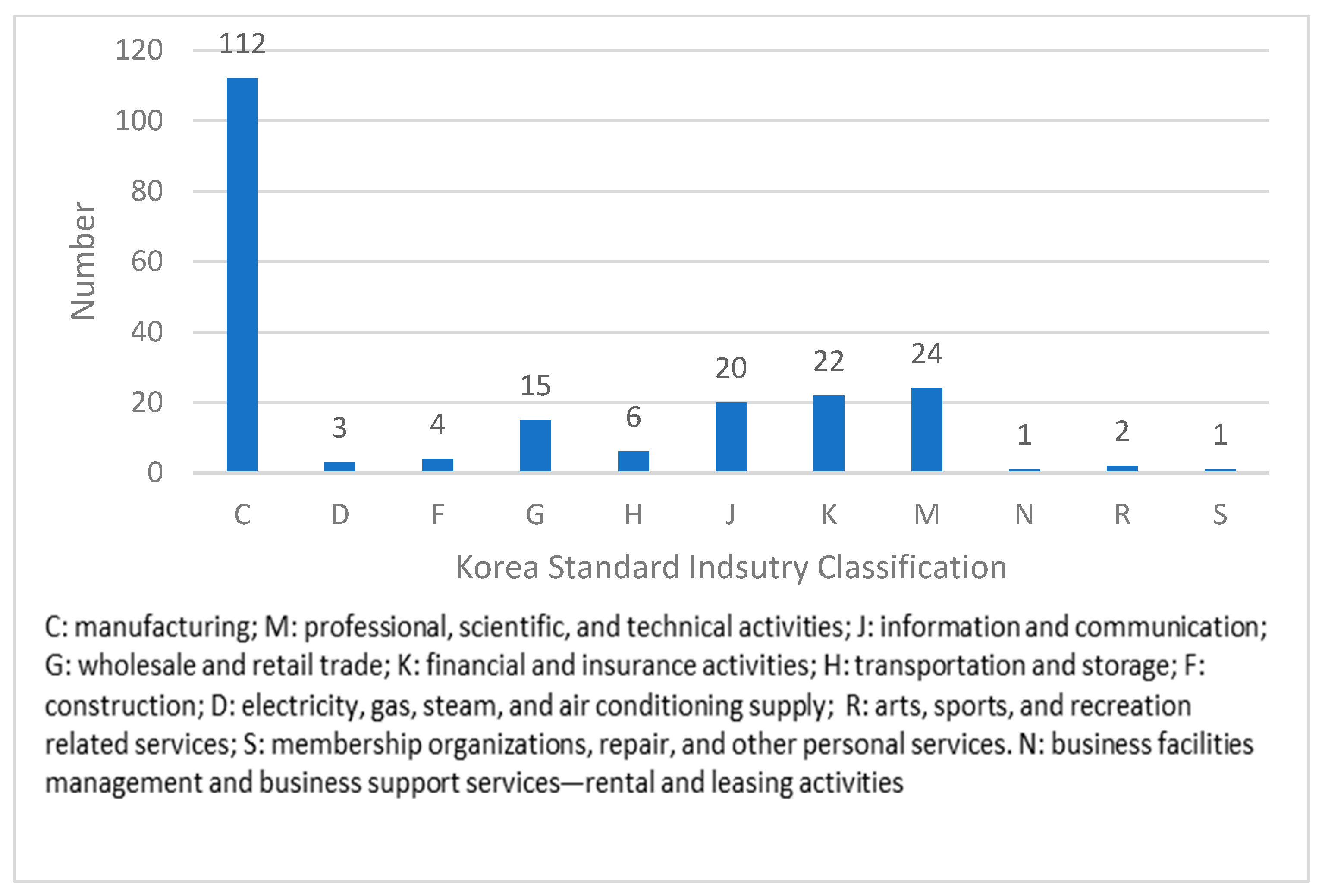

3.1. Sample

3.2. Variables and Measures

3.2.1. Dependent Variable

3.2.2. Independent Variables

3.2.3. Moderating Variables

3.2.4. Control Variables

3.3. Estimation

4. Results and Discussion

4.1. Descriptive Statistics

4.2. Main Results

4.3. Results by Industry

4.4. Robustness Checks

5. Conclusions

Funding

Data Availability Statement

Conflicts of Interest

References

- Ministry of Environment of Korea. The Republic of Korea’s Enhanced Update of Its First Nationally Determined Contribution; Ministry of Environment of Korea: Seoul, Korea, 2021.

- Available online: www.there100.org (accessed on 1 April 2022).

- Hwang, J.; Kim, H.; Jung, D. The Effect of ESG Activities on Financial Performance during the COVID-19 Pandemic—Evidence from Korea. Sustainability 2021, 13, 11362. [Google Scholar] [CrossRef]

- Ok, Y.; Kim, J. Which corporate social responsibility performance affects the cost of equity? Evidence from Korea. Sustainability 2019, 11, 2947. [Google Scholar] [CrossRef] [Green Version]

- Friedman, M. The methodology of positive economics. In Essays in Positive Economics; University of Chicago Press: Chicago, IL, USA, 1966; pp. 3–43. [Google Scholar]

- DiMaggio, P.J.; Powell, W.W. The iron cage revisited: Institutional isomorphism and collective rationality in organizational fields. Am. Sociol. Rev. 1983, 48, 147–160. [Google Scholar] [CrossRef] [Green Version]

- Lin, N.H.; Tsay, S.C.; Maring, H.B.; Yen, M.C.; Sheu, G.R.; Wang, S.H.; Liu, G.R. An overview of regional experiments on biomass burning aerosols and related pollutants in Southeast Asia: From BASE-ASIA and the Dongsha Experiment to 7-SEAS. Atmos. Environ. 2013, 78, 1–19. [Google Scholar] [CrossRef] [Green Version]

- Fernández-Alles, M.; Valle-Cabrera, R. Reconciling institutional theory with organizational theories, How neoinstitutionalism resolves five paradoxes. J. Organ. Chang. Manag. 2006, 19, 503–517. [Google Scholar] [CrossRef]

- Hofer, C.; Cantor, D.; Dai, J. The competitive determinants of a firm’s environmental management activities: Evidence from US manufacturing industries. J. Oper. Manag. 2012, 30, 69–84. [Google Scholar] [CrossRef]

- Available online: www.sec.gov (accessed on 1 April 2022).

- Available online: https://ec.europa.eu/info/business-economy-euro/banking-and-finance/sustainable-finance/eu-taxonomy-sustainable-activities_en (accessed on 1 April 2022).

- Kotler, P.; Armstrong, G. Principles of Marketing; Prentice-Hall: Englewood Cliffs, NJ, USA, 1996. [Google Scholar]

- Rugman, A.M.; Verbeke, A. Corporate strategy and international environmental policy. J. Int. Bus. Stud. 1998, 29, 819–833. [Google Scholar] [CrossRef]

- Scanlon, N.L. An analysis and assessment of environmental operating practices in hotel and resort properties. Int. J. Hosp. Manag. 2007, 26, 711–723. [Google Scholar] [CrossRef]

- Brammer, S.J.; Pavelin, S. Corporate reputation and social performance: The importance of fit. J. Manag. Stud. 2006, 43, 435–455. [Google Scholar] [CrossRef]

- Vance, S.C. Are socially responsible corporations good investment risks? Acad. Manag. Rev. 1975, 64, 18–24. [Google Scholar]

- Wright, P.; Ferris, S.P. Agency conflict and corporate strategy: The effect of divestment on corporate value. Strateg. Manag. J. 1997, 18, 77–83. [Google Scholar] [CrossRef]

- Schroder, M. Is there a difference? The performance characteristics of SRI equity indices. J. Bus. Financ. Account. 2007, 34, 331–348. [Google Scholar] [CrossRef]

- Friede, G.; Busch, T.; Bassen, A. ESG and financial performance: Aggregated evidence from more than 2000 empirical studies. J. Sustain. Financ. Invest. 2015, 5, 210–233. [Google Scholar] [CrossRef] [Green Version]

- Barney, J. Firm resources and sustained competitive advantage. J. Manag. 1991, 17, 99–120. [Google Scholar] [CrossRef]

- Fraj-Andrés, E.; Martinez-Salinas, E.; Matute-Vallejo, J. A multidimensional approach to the influence of evironmental marketing and orientation on the firm’s organizational performance. J. Bus. Ethics 2008, 99, 263–286. [Google Scholar] [CrossRef]

- Eiadat, Y.; Kelly, A.; Roche, F.; Eyadat, H. Green and competitive? An empirical test of the mediating role of environmental innovation strategy. J. World Bus. 2008, 43, 131–145. [Google Scholar] [CrossRef]

- Porter, M.E.; Van der Linde, C. Toward a new conception of the environment-competitiveness relationship. J. Econ. Perspect. 1995, 9, 97–118. [Google Scholar] [CrossRef] [Green Version]

- Chen, Y.S.; Lai, S.B.; Wen, C.T. The influence of green innovation performance on corporate advantage in Taiwan. J. Bus. Ethics 2006, 67, 331–339. [Google Scholar] [CrossRef]

- Rao, P. Greening the supply chain: A new initiative in South East Asia. Int. J. Oper. Prod. Manag. 2002, 22, 632–655. [Google Scholar] [CrossRef]

- Zhu, Q.; Sarkis, J. Relationships between operational practices and performance among early adopters of green supply chain management practices in Chinese manufacturing enterprises. J. Oper. Manag. 2004, 22, 265–289. [Google Scholar] [CrossRef]

- Brush, T.H.; Bromiley, P.; Hendrickx, M. The free cash flow hypothesis for sales growth and firm performance. Strateg. Manag. J. 2000, 21, 455–472. [Google Scholar] [CrossRef]

- Eliasson, G. Business Economic Planning; John Wiley: Chichester, UK, 1976. [Google Scholar]

- Hubbard, G.; Bromiley, P. How do top managers measure and assess firm performance. In Proceedings of the Academy of Management Meetings, Dallas, TX, USA, 14–17 August 1994. [Google Scholar]

- Afinindy, I.; Salim, U.; Ratnawati, K. The Effect of profitability, firm size, liquidity, sales growth on firm value mediated capital structure. IJBEL 2021, 24, 15–22. [Google Scholar]

- Fakhroni, Z.; Ghozali, I.; Harto, P.; Yuyetta, E.N.A. Free cash flow, investment inefficiency, and earnings management: Evidence from manufacturing firms listed on the Indonesia Stock Exchange. Invest. Manag. Financ. Innov. 2018, 15, 299–310. [Google Scholar] [CrossRef] [Green Version]

- Febriyanto, F.C. The effect of leverage, sales growth and liquidity to the firm value of real estate and property sector in Indonesia stock exchange. EAJ 2018, 1, 198–205. [Google Scholar] [CrossRef]

- Bromiley, P. Testing a causal model of corporate risk taking and performance. Acad. Manag. J. 1991, 34, 37–59. [Google Scholar] [CrossRef] [Green Version]

- Cheng, J.L.; Kesner, I.F. Organizational slack and response to environmental shifts: The impact of resource allocation patterns. J. Manag. 1997, 23, 1–18. [Google Scholar] [CrossRef]

- Nohria, N.; Gulati, R. Is slack good or bad for innovation? Acad. Manag. J. 1996, 39, 1245–1264. [Google Scholar] [CrossRef]

- Bourgeois, L.J., III. On the measurement of organizational slack. Acad. Manag. Rev. 1981, 6, 29–39. [Google Scholar] [CrossRef]

- Bradley, S.W.; Wiklund, J.; Shepherd, D.A. Swinging a double-edged sword: The effect of slack on entrepreneurial management and growth. J. Bus. Ventur. 2011, 26, 537–554. [Google Scholar] [CrossRef]

- Cyert, R.M.; March, J.G. A Behavioral Theory of the Firm; Prentice-Hall: Englewood Cliffs, NJ, USA, 1963; Volume 2, pp. 169–187. [Google Scholar]

- Levinthal, D.A. Adaptation on rugged landscapes. Manag. Sci. 1997, 43, 934–950. [Google Scholar] [CrossRef]

- Voss, G.B.; Sirdeshmukh, D.; Voss, Z.G. The effects of slack resources and environmental threat on product exploration and exploitation. Acad. Manag. J. 2008, 51, 147–164. [Google Scholar] [CrossRef] [Green Version]

- Bowen, F.E. Does size matter? Organizational slack and visibility as alternative explanations for environmental responsiveness. Bus. Soc. 2002, 41, 118–124. [Google Scholar] [CrossRef]

- Aldy, J.E.; Pizer, W.A. Issues in the Design of U.S. Climate Change Policy. Energy J. 2008, 30. [Google Scholar] [CrossRef]

- Available online: http://www.kesis.net/main/main.jsp (accessed on 1 April 2022).

- Yoon, B.; Lee, J.H.; Byun, R. Does ESG performance enhance firm value? Evidence from Korea. Sustainability 2018, 10, 3635. [Google Scholar] [CrossRef] [Green Version]

- Lin, C.J. An examination of board and firm performance: Evidence from Taiwan. Int. J. Bus. Res. 2011, 5, 17–34. [Google Scholar]

- Zabri, S.M.; Ahmad, K.; Wah, K.K. Corporate governance practices and firm performance: Evidence from top 100 public listed companies in Malaysia. Procedia Econ. Financ. 2016, 35, 287–296. [Google Scholar] [CrossRef] [Green Version]

- Lin, W.L.; Ho, J.A.; Lee, C.; Ng, S.I. Impact of positive and negative corporate social responsibility on automotive firms’ financial performance: A market-based asset perspective. Corp. Soc. Responsib. Environ. Manag. 2020, 27, 1761–1773. [Google Scholar] [CrossRef]

- Fatemi, A.; Glaum, M.; Kaiser, S. ESG performance and firm value: The moderating role of disclosure. Glob. Financ. J. 2018, 38, 45–64. [Google Scholar] [CrossRef]

- Available online: https://www.cdp.net/en/companies/companies-scores (accessed on 1 April 2022).

- Velte, P. Does ESG performance have an impact on financial performance? Evidence from Germany. J. Glob. Responsib. 2017, 8, 169–178. [Google Scholar] [CrossRef]

- Pindado, J.; De Queiroz, V.; De La Torre, C. How do firm characteristics influence the relationship between R&D and firm value? Financ. Manag. 2010, 39, 757–782. [Google Scholar] [CrossRef]

- Artz, K.W.; Norman, P.M.; Hatfield, D.E.; Cardinal, L.B. A longitudinal study of the impact of R&D, patents, and product innovation on firm performance. J. Prod. Innov. Manag. 2010, 27, 725–740. [Google Scholar] [CrossRef]

- Cho, Y. The effects of knowledge assets and path dependence in innovations on firm value in the Korean semiconductor industry. Sustainability 2020, 12, 2319. [Google Scholar] [CrossRef] [Green Version]

- Morbey, G.K.; Reithner, R.M. How R&D affects sales growth, productivity and profitability. Res. Technol. Manag. 1990, 33, 11–14. [Google Scholar] [CrossRef]

- Zalaghi, H.; Godini, M.; Mansouri, K. The moderating role of firms characteristics on the relationship between working capital management and financial performance. Adv. Math. Financ. Appl. 2019, 4, 71–88. [Google Scholar] [CrossRef]

- Mackey, A.; Mackey, T.B.; Barney, J.B. Corporate social responsibility and firm performance: Investor preferences and corporate strategies. Acad. Manag. Rev. 2007, 32, 817–835. [Google Scholar] [CrossRef]

- Jackling, B.; Johl, S. Board structure and firm performance: Evidence from India’s top companies. Corp. Gov. Int. Rev. 2009, 17, 492–509. [Google Scholar] [CrossRef]

- Elsayed, K.; Paton, D. The impact of financial performance on environmental policy: Does firm life cycle matter? Bus Strategy Environ. 2009, 18, 397–413. [Google Scholar] [CrossRef]

- Hasan, M.M.; Habib, A. Corporate life cycle, organizational financial resources and corporate social responsibility. J. Contemp. Account. Econ. 2017, 13, 20–36. [Google Scholar] [CrossRef]

- Nelling, E.; Webb, E. Corporate social responsibility and financial performance: The “virtuous circle” revisited. Rev. Quant. Financ. Account. 2009, 32, 197–209. [Google Scholar] [CrossRef]

- Azmi, W.; Hassan, M.K.; Houston, R.; Karim, M.S. ESG activities and banking performance: International evidence from emerging economies. J. Int. Financ. Mark. Inst. Money 2021, 70, 101277. [Google Scholar] [CrossRef]

- Shakil, M.H. Environmental, social and governance performance and financial risk: Moderating role of ESG controversies and board gender diversity. Resour. Policy 2021, 72, 102144. [Google Scholar] [CrossRef]

{kind=link}

{kind=link}

| Government | Contents |

|---|---|

| Republic of Korea | Korea enacted and promulgated the “Basic Act on Carbon Neutrality and Green Growth” on 24 September 2020, to convert to a carbon-neutral society. It is a law that contains legal procedures and policy measures to achieve the goal of “2050 carbon neutrality.” On 25 March 2022, the Enforcement Decree of the Framework Act on Carbon Neutral and Green Growth (hereinafter referred to as the Enforcement Decree) was implemented. This made Korea the 14th country to legislate the 2050 carbon neutrality vision. This enforcement ordinance includes the 2050 carbon-neutral vision and implementation system, greenhouse gas reductions, climate crisis adaptation and just transition, green growth, carbon-neutral finance, and the foundation for practice. |

| United States | In March 2022, the Securities and Exchange Commission (SEC) prepared a regulatory plan that mandates listed companies disclose information on greenhouse gas emissions and climate change risks. According to the SEC’s regulations, listed companies must disclose carbon emissions generated by the direct activities of companies, such as production (scope 1) and indirect carbon emissions generated through electricity, steam, and cooling purchased and consumed by companies (scope 2). In particular, the disclosure obligation of scope 3 (all carbon emissions from the value chain of companies, such as consumers, partners, and logistics), which was controversial, was imposed with a limit. It applies when listed companies judge scope 3 information as “significant information” to investors, or when the content is included in the company’s own greenhouse gas reduction goals [10]. |

| European Union | The European Union (EU) announced the world’s first green taxonomy in June 2020. Green Taxonomy is a combination of green (meaning green industry) and taxonomy, and it defines the scope of environmentally sustainable economic activities. In other words, it is a green industry classification system that classifies which industries are eco-friendly industries and is used as a criterion for determining whether or not industries can receive green investment [11]. |

| Variables | Observation | Mean | Standard Deviation | Minimum | Maximum |

|---|---|---|---|---|---|

| 1. ROA | 1029 | 1.26 | 0.94 | 0 | 3.99 |

| 2. Eco-friendly strategy | 1029 | 0 | 0.97 | −0.72 | 2.27 |

| 3. Excess growth | 1029 | 0.02 | 1 | −1.38 | 0.72 |

| 4. Market share | 1029 | 0.36 | 1.36 | −0.4 | 9.67 |

| 5. R&D investment | 1029 | 0.01 | 0.36 | −0.05 | 3.66 |

| 6. Cash flow | 1029 | −0.09 | 0.59 | −2.81 | 2.79 |

| 7. Debt ratio | 1029 | 0.21 | 1.14 | −1.89 | 2.58 |

| 8. Firm size | 1029 | −0.13 | 0.52 | −0.44 | 2.04 |

| 9. Firm age | 1029 | 0.09 | 1.03 | −1.46 | 2.98 |

| Variables | 1 | 2 | 3 | 4 | 5 | 6 | 7 | 8 | 9 |

|---|---|---|---|---|---|---|---|---|---|

| 1. ROA | 1 | ||||||||

| 2. Eco-friendly strategy | −0.16 | 1 | |||||||

| 3. Excess growth | 0.08 | 0.05 | 1 | ||||||

| 4. Market share | −0.13 | 0.22 | −0.06 | 1 | |||||

| 5. R&D investment | 0.22 | −0.11 | −0.17 | −0.10 | 1 | ||||

| 6. Cash flow | 0.12 | 0.1 | −0.03 | 0.53 | −0.04 | 1 | |||

| 7. Debt ratio | −0.59 | 0.27 | 0.07 | 0.22 | −0.16 | −0.07 | 1 | ||

| 8. Firm size | −0.18 | 0.19 | −0.04 | 0.49 | −0.10 | 0.26 | 0.18 | 1 | |

| 9. Firm age | −0.18 | 0.09 | 0.06 | 0.18 | −0.15 | 0.11 | 0.22 | 0.16 | 1 |

| 5 Years | 3 Years | |||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| ROA | ROE | Tobin’s Q | ROA | ROE | Tobin’s Q | |||||||

| VARIABLES | Model1 | Model2 | Model3 | Model4 | Model5 | Model6 | Model7 | Model8 | Model9 | Model10 | Model11 | Model12 |

| Market share | 0.681 *** | 0.677 *** | 0.718 *** | 0.710 *** | 0.0512 | 0.0521 | 0.503 * | 0.504 * | 0.530 ** | 0.524 ** | 0.0454 | 0.0506 |

| (0.195) | (0.195) | (0.205) | (0.205) | (0.0334) | (0.0334) | (0.271) | (0.272) | (0.264) | (0.265) | (0.0428) | (0.0429) | |

| R&D investment | −27.62 *** | −27.64 *** | −27.57 *** | −27.62 *** | 0.0746 *** | 0.0752 *** | −53.45 *** | −53.42 *** | −52.70 *** | −52.86 *** | 0.0415 | 0.0446 |

| (3.668) | (3.670) | (3.941) | (3.938) | (0.0222) | (0.0223) | (9.672) | (9.710) | (9.585) | (9.620) | (0.0289) | (0.0289) | |

| Cash flow | 0.0801 * | 0.0780 | 0.0822 | 0.0766 | 0.0100 | 0.0105 | 0.0581 | 0.0586 | 0.0797 | 0.0773 | 0.00807 | 0.0103 |

| (0.0476) | (0.0477) | (0.0504) | (0.0505) | (0.00955) | (0.00958) | (0.0572) | (0.0582) | (0.0557) | (0.0566) | (0.0107) | (0.0108) | |

| Debt ratio | −0.511 *** | −0.511 *** | −0.205 *** | −0.203 *** | 0.670 *** | 0.670 *** | −0.382 *** | −0.382 *** | −0.0919 | −0.0910 | 0.688 *** | 0.687 *** |

| (0.0691) | (0.0691) | (0.0728) | (0.0728) | (0.0113) | (0.0113) | (0.103) | (0.103) | (0.102) | (0.102) | (0.0161) | (0.0161) | |

| Firm size | −0.0989 | −0.0991 | −0.395 * | −0.394 * | 0.0132 | 0.0135 | −0.127 | −0.127 | −0.370 | −0.371 | 0.0505 | 0.0509 |

| (0.225) | (0.225) | (0.229) | (0.229) | (0.0339) | (0.0339) | (0.348) | (0.348) | (0.343) | (0.343) | (0.0671) | (0.0670) | |

| Firm age | −0.0948 | −0.0988 | −0.114 | −0.124 | −0.00246 | −0.00169 | −0.0445 | −0.0436 | −0.0202 | −0.0246 | −0.0454 | −0.0418 |

| (0.117) | (0.117) | (0.125) | (0.125) | (0.0242) | (0.0243) | (0.279) | (0.280) | (0.276) | (0.277) | (0.0535) | (0.0536) | |

| Eco-friendly strategy | 0.110 *** | 0.109 *** | 0.120 *** | 0.117 *** | 0.00171 | 0.00180 | 0.106 * | 0.106 * | 0.134 ** | 0.134 ** | 0.0134 | 0.0128 |

| (0.0377) | (0.0377) | (0.0401) | (0.0401) | (0.00751) | (0.00751) | (0.0572) | (0.0573) | (0.0564) | (0.0565) | (0.0107) | (0.0107) | |

| Excess growth | 0.119 *** | 0.112 *** | 0.123 *** | 0.104 *** | 0.00839 ** | 0.00968 ** | 0.132 *** | 0.133 *** | 0.132 *** | 0.128 *** | 0.00844 * | 0.0120 ** |

| (0.0193) | (0.0226) | (0.0204) | (0.0241) | (0.00360) | (0.00420) | (0.0246) | (0.0298) | (0.0242) | (0.0293) | (0.00433) | (0.00516) | |

| Eco-friendly strategy × Excess growth | 0.0161 | 0.0411 | −0.00310 | −0.00163 | 0.00854 | −0.00812 | ||||||

| (0.0262) | (0.0277) | (0.00519) | (0.0341) | (0.0337) | (0.00634) | |||||||

| Constant | 0.271 | 0.270 | 1.077 *** | 1.075 *** | −0.868 *** | −0.868 *** | −0.987 ** | −0.986 ** | −0.139 | −0.146 | −0.864 *** | −0.864 *** |

| (0.174) | (0.174) | (0.187) | (0.187) | (0.00673) | (0.00673) | (0.444) | (0.446) | (0.441) | (0.442) | (0.00574) | (0.00576) | |

| Observations | 909 | 909 | 921 | 921 | 1,025 | 1,025 | 555 | 555 | 559 | 559 | 628 | 628 |

| R-squared | 0.237 | 0.238 | 0.193 | 0.195 | 0.819 | 0.819 | 0.250 | 0.250 | 0.249 | 0.249 | 0.822 | 0.823 |

| Number of id | 202 | 202 | 202 | 202 | 210 | 210 | 201 | 201 | 201 | 201 | 210 | 210 |

| Id FE | YES | YES | YES | YES | YES | YES | YES | YES | YES | YES | YES | YES |

| Year FE | YES | YES | YES | YES | YES | YES | YES | YES | YES | YES | YES | YES |

| 5 Years | 3 Years | |||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| ROA | ROE | Tobin’s Q | ROA | ROE | Tobin’s Q | |||||||

| VARIABLES | Model1 | Model2 | Model3 | Model4 | Model5 | Model6 | Model7 | Model8 | Model9 | Model10 | Model11 | Model12 |

| Market share | 2.053 ** | 2.102 ** | 2.307 ** | 2.287 ** | −0.109 | −0.0966 | 2.415 ** | 2.549 ** | 2.423 ** | 2.498 ** | 2.423 ** | 2.498 ** |

| (0.916) | (0.921) | (0.933) | (0.939) | (0.151) | (0.152) | (1.186) | (1.190) | (1.143) | (1.150) | (1.143) | (1.150) | |

| R&D investment | −26.47 *** | −26.44 *** | −26.49 *** | −26.50 *** | 0.0320 | 0.0345 | −48.35 *** | −47.51 *** | −47.86 *** | −47.40 *** | −47.86 *** | −47.40 *** |

| (4.108) | (4.112) | (4.188) | (4.193) | (0.0534) | (0.0535) | (11.08) | (11.09) | (10.68) | (10.72) | (10.68) | (10.72) | |

| Cash flow | 0.167 * | 0.174 * | 0.169 * | 0.166 * | 0.0110 | 0.0131 | −0.00355 | 0.0174 | 0.0122 | 0.0241 | 0.0122 | 0.0241 |

| (0.0896) | (0.0907) | (0.0912) | (0.0924) | (0.0155) | (0.0157) | (0.115) | (0.116) | (0.111) | (0.112) | (0.111) | (0.112) | |

| Debt ratio | −0.455 *** | −0.457 *** | −0.0464 | −0.0458 | 0.597 *** | 0.597 *** | −0.358 ** | −0.376 ** | −0.0219 | −0.0319 | −0.0219 | −0.0319 |

| (0.101) | (0.101) | (0.103) | (0.103) | (0.0148) | (0.0148) | (0.166) | (0.166) | (0.160) | (0.161) | (0.160) | (0.161) | |

| Firm size | −0.281 | −0.293 | −0.324 | −0.319 | 0.0338 | 0.0328 | −0.197 | −0.220 | −0.368 | −0.381 | −0.368 | −0.381 |

| (0.311) | (0.312) | (0.317) | (0.318) | (0.0371) | (0.0371) | (0.497) | (0.497) | (0.479) | (0.480) | (0.479) | (0.480) | |

| Firm age | 0.0492 | 0.0532 | 0.0230 | 0.0215 | −0.0160 | −0.0148 | 0.0301 | 0.0673 | 0.0451 | 0.0656 | 0.0451 | 0.0656 |

| (0.156) | (0.156) | (0.159) | (0.159) | (0.0277) | (0.0278) | (0.361) | (0.362) | (0.348) | (0.350) | (0.348) | (0.350) | |

| Eco-friendly strategy | 0.136 ** | 0.138 ** | 0.157 *** | 0.156 *** | 0.00255 | 0.00312 | 0.0587 | 0.0600 | 0.0730 | 0.0737 | 0.0730 | 0.0737 |

| (0.0533) | (0.0535) | (0.0541) | (0.0543) | (0.00919) | (0.00922) | (0.0821) | (0.0820) | (0.0792) | (0.0793) | (0.0792) | (0.0793) | |

| Excess growth | 0.151 *** | 0.161 *** | 0.148 *** | 0.144 *** | 0.0137 *** | 0.0161 *** | 0.205 *** | 0.231 *** | 0.196 *** | 0.210 *** | 0.196 *** | 0.210 *** |

| (0.0283) | (0.0330) | (0.0286) | (0.0335) | (0.00465) | (0.00540) | (0.0359) | (0.0420) | (0.0344) | (0.0403) | (0.0344) | (0.0403) | |

| Eco-friendly strategy × Excess growth | −0.0221 | 0.00866 | −0.00575 | −0.0553 | −0.0308 | −0.0308 | ||||||

| (0.0392) | (0.0396) | (0.00665) | (0.0476) | (0.0459) | (0.0459) | |||||||

| Constant | 1.089 *** | 1.102 *** | 1.915 *** | 1.910 *** | −0.856 *** | −0.853 *** | 0.211 | 0.275 | 0.979 * | 1.015 * | 0.979 * | 1.015 * |

| (0.332) | (0.333) | (0.338) | (0.339) | (0.0457) | (0.0459) | (0.600) | (0.602) | (0.578) | (0.581) | (0.578) | (0.581) | |

| Observations | 515 | 515 | 518 | 518 | 566 | 566 | 315 | 315 | 316 | 316 | 316 | 316 |

| R-squared | 0.275 | 0.276 | 0.258 | 0.258 | 0.792 | 0.793 | 0.338 | 0.343 | 0.349 | 0.351 | 0.349 | 0.351 |

| Number of id | 114 | 114 | 114 | 114 | 116 | 116 | 114 | 114 | 114 | 114 | 114 | 114 |

| Id FE | YES | YES | YES | YES | YES | YES | YES | YES | YES | YES | YES | YES |

| Year FE | YES | YES | YES | YES | YES | YES | YES | YES | YES | YES | YES | YES |

| 5 Years | 3 Years | |||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| ROA | ROE | Tobin’s Q | ROA | ROE | Tobin’s Q | |||||||

| VARIABLES | Model1 | Model2 | Model3 | Model4 | Model5 | Model6 | Model7 | Model8 | Model9 | Model10 | Model11 | Model12 |

| Market share | 0.777 *** | 0.778 *** | 0.763 *** | 0.765 *** | 0.0800 ** | 0.0802 ** | 0.791 *** | 0.752 *** | 0.768 *** | 0.729 *** | 0.0667 | 0.0736 |

| (0.169) | (0.169) | (0.199) | (0.198) | (0.0358) | (0.0359) | (0.239) | (0.237) | (0.254) | (0.253) | (0.0508) | (0.0511) | |

| R&D investment | −42.49 ** | −43.36 ** | −40.92 | −42.24 * | 0.0836 *** | 0.0837 *** | −57.16 ** | −63.32 ** | −55.93 * | −61.43 ** | 0.0476 | 0.0524 |

| (20.81) | (20.78) | (24.99) | (24.92) | (0.0246) | (0.0247) | (27.57) | (27.38) | (29.80) | (29.75) | (0.0358) | (0.0360) | |

| Cash flow | 0.00146 | 0.00390 | 0.00517 | 0.00808 | 0.0130 | 0.0130 | 0.0551 | 0.0360 | 0.0813 | 0.0658 | 0.0157 | 0.0182 |

| (0.0494) | (0.0493) | (0.0582) | (0.0581) | (0.0123) | (0.0123) | (0.0572) | (0.0572) | (0.0606) | (0.0608) | (0.0145) | (0.0147) | |

| Debt ratio | −0.599 *** | −0.599 *** | −0.412 *** | −0.407 *** | 0.753 *** | 0.753 *** | −0.393 *** | −0.395 *** | −0.134 | −0.136 | 0.706 *** | 0.707 *** |

| (0.0868) | (0.0867) | (0.100) | (0.0998) | (0.0166) | (0.0166) | (0.114) | (0.112) | (0.123) | (0.122) | (0.0236) | (0.0236) | |

| Firm size | −0.185 | −0.208 | −0.846 ** | −0.866 ** | −0.0825 | −0.0823 | −0.340 | −0.317 | −0.644 | −0.633 | 0.0595 | 0.0566 |

| (0.344) | (0.344) | (0.353) | (0.352) | (0.0726) | (0.0727) | (0.511) | (0.505) | (0.546) | (0.542) | (0.134) | (0.134) | |

| Firm age | −0.460 *** | −0.478 *** | −0.380 * | −0.406 ** | −0.000829 | −0.000526 | −0.691 | −0.715 * | −0.559 | −0.577 | −0.0925 | −0.0934 |

| (0.170) | (0.170) | (0.204) | (0.204) | (0.0432) | (0.0434) | (0.426) | (0.421) | (0.459) | (0.456) | (0.110) | (0.110) | |

| Eco-friendly strategy | 0.0802 | 0.0807 | 0.0608 | 0.0628 | 0.00484 | 0.00479 | 0.183 ** | 0.197 *** | 0.216 *** | 0.228 *** | 0.0400 ** | 0.0382 ** |

| (0.0495) | (0.0494) | (0.0578) | (0.0577) | (0.0120) | (0.0120) | (0.0737) | (0.0731) | (0.0785) | (0.0782) | (0.0181) | (0.0182) | |

| Excess growth | 0.0472 * | 0.0263 | 0.0648 ** | 0.0328 | 0.00233 | 0.00267 | −0.00194 | −0.0505 | 0.0131 | −0.0303 | 0.000409 | 0.00569 |

| (0.0243) | (0.0285) | (0.0284) | (0.0338) | (0.00550) | (0.00637) | (0.0305) | (0.0378) | (0.0327) | (0.0408) | (0.00723) | (0.00865) | |

| Eco-friendly strategy × Excess growth | 0.0450 | 0.0650 * | −0.000844 | 0.0920 ** | 0.0826 * | −0.0125 | ||||||

| (0.0324) | (0.0379) | (0.00794) | (0.0432) | (0.0468) | (0.0113) | |||||||

| Constant | −0.951 | −1.003 | 0.0210 | −0.0548 | −0.996 *** | −0.996 *** | −1.766 | −2.061 | −0.789 | −1.052 | −0.970 *** | −0.973 *** |

| (1.053) | (1.052) | (1.265) | (1.262) | (0.0192) | (0.0193) | (1.379) | (1.370) | (1.492) | (1.489) | (0.0282) | (0.0283) | |

| Observations | 394 | 394 | 403 | 403 | 459 | 459 | 240 | 240 | 243 | 243 | 280 | 280 |

| R-squared | 0.264 | 0.269 | 0.176 | 0.183 | 0.859 | 0.859 | 0.251 | 0.274 | 0.200 | 0.217 | 0.843 | 0.844 |

| Number of id | 88 | 88 | 88 | 88 | 94 | 94 | 87 | 87 | 87 | 87 | 94 | 94 |

| Id FE | YES | YES | YES | YES | YES | YES | YES | YES | YES | YES | YES | YES |

| Year FE | YES | YES | YES | YES | YES | YES | YES | YES | YES | YES | YES | YES |

| VARIABLES | ROA | ROE | Tobin’s Q | |||

|---|---|---|---|---|---|---|

| First Stage | Second Stage | First Stage | Second Stage | First Stage | Second Stage | |

| Excess growth | 0.00235 | 0.109 *** | 0.00235 | 0.100 *** | 0.00235 | 0.00964 ** |

| (0.0192) | (0.0227) | (0.0192) | (0.0242) | (0.0192) | (0.00420) | |

| Eco-friendly strategy × Excess growth | 0.0249 | 0.00965 | 0.0249 | 0.0323 | 0.0249 | −0.00322 |

| (0.0239) | (0.0267) | (0.0239) | (0.0282) | (0.0239) | (0.00529) | |

| Market share | −0.137 | 0.668 *** | −0.137 | 0.708 *** | −0.137 | 0.0525 |

| (0.156) | (0.196) | (0.156) | (0.205) | (0.156) | (0.0336) | |

| R&D investment | 0.00590 | −27.55 *** | 0.00590 | −27.54 *** | 0.00590 | 0.0752 *** |

| (0.104) | (3.680) | (0.104) | (3.945) | (0.104) | (0.0223) | |

| Cash flow | 0.0937 ** | 0.0340 | 0.0937 ** | 0.0201 | 0.0937 ** | 0.00993 |

| (0.0447) | (0.0540) | (0.0447) | (0.0573) | (0.0447) | (0.0107) | |

| Debt ratio | −0.0164 | −0.499 *** | −0.0164 | −0.188 ** | −0.0164 | 0.670 *** |

| (0.0523) | (0.0695) | (0.0523) | (0.0730) | (0.0523) | (0.0113) | |

| Firm size | 0.0992 | −0.167 | 0.0992 | −0.469 ** | 0.0992 | 0.0125 |

| (0.159) | (0.227) | (0.159) | (0.232) | (0.159) | (0.0349) | |

| Firm age | −0.0449 | −0.0724 | −0.0449 | −0.0941 | −0.0449 | −0.00131 |

| (0.0910) | (0.117) | (0.0910) | (0.125) | (0.0910) | (0.0242) | |

| Lagged eco-friendly strategy | 0.143 *** | 0.143 *** | 0.143 *** | |||

| (0.0342) | (0.0342) | (0.0342) | ||||

| Eco-friendly strategy expectation | 0.537 ** | 0.674 ** | 0.00739 | |||

| (0.260) | (0.277) | (0.0521) | ||||

| Constant | 0.0343 ** | 0.282 | 0.0343 ** | 1.086 *** | 0.0343 ** | −0.868 *** |

| (0.0142) | (0.174) | (0.0142) | (0.187) | (0.0142) | (0.00674) | |

| Observations | 1029 | 909 | 1029 | 921 | 1029 | 1025 |

| R-squared | 0.030 | 0.233 | 0.030 | 0.192 | 0.030 | 0.819 |

| Number of id | 210 | 202 | 210 | 202 | 210 | 210 |

| Id FE | YES | YES | YES | YES | YES | YES |

| Year FE | YES | YES | YES | YES | YES | YES |

| Durbin (score) chi2(1) | 0.543 | 0.771 | 0.020 | |||

| p-value | 0.461 | 0.380 | 0.889 | |||

| Wu–Hausman F | 0.537 | 0.762 | 0.019 | |||

| p-value | 0.464 | 0.383 | 0.889 | |||

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2022 by the author. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Cho, Y. ESG and Firm Performance: Focusing on the Environmental Strategy. Sustainability 2022, 14, 7857. https://doi.org/10.3390/su14137857

Cho Y. ESG and Firm Performance: Focusing on the Environmental Strategy. Sustainability. 2022; 14(13):7857. https://doi.org/10.3390/su14137857

Chicago/Turabian StyleCho, Yoonkyo. 2022. "ESG and Firm Performance: Focusing on the Environmental Strategy" Sustainability 14, no. 13: 7857. https://doi.org/10.3390/su14137857

APA StyleCho, Y. (2022). ESG and Firm Performance: Focusing on the Environmental Strategy. Sustainability, 14(13), 7857. https://doi.org/10.3390/su14137857