Clarifying the Concept of Corporate Sustainability and Providing Convergence for Its Definition

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Abstract

:1. Introduction

- Broadens the analysis to the meanings of corporate sustainability alongside their definitions,

- Performs an ontological analysis through a historical excursion into the evolution of corporate sustainability and its associated concepts, and

- Performs a necessary condition analysis to identify the constitutive components of the concept of corporate sustainability.

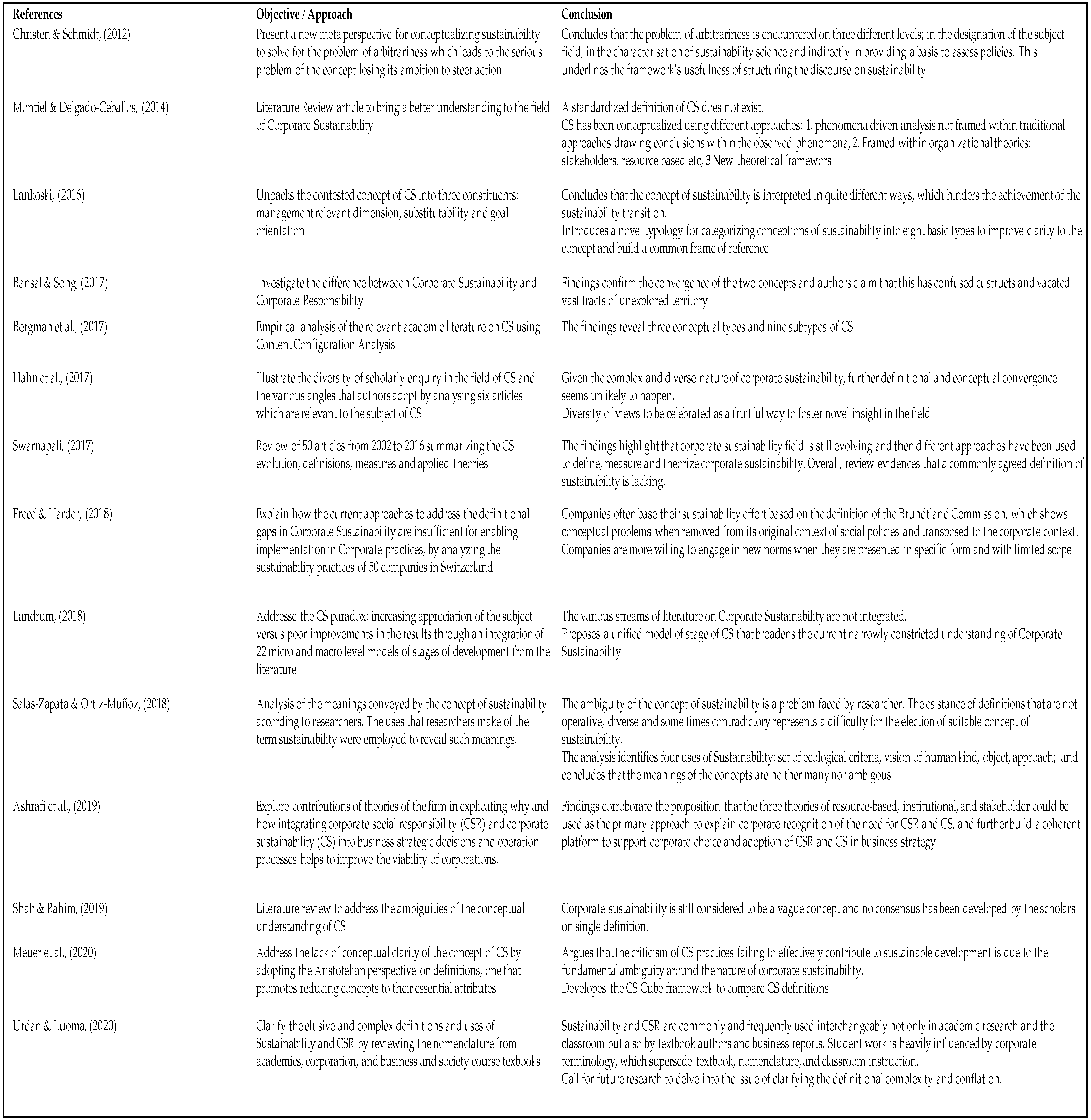

2. Literature Review

2.1. Ontological Analysis of Corporate Sustainability

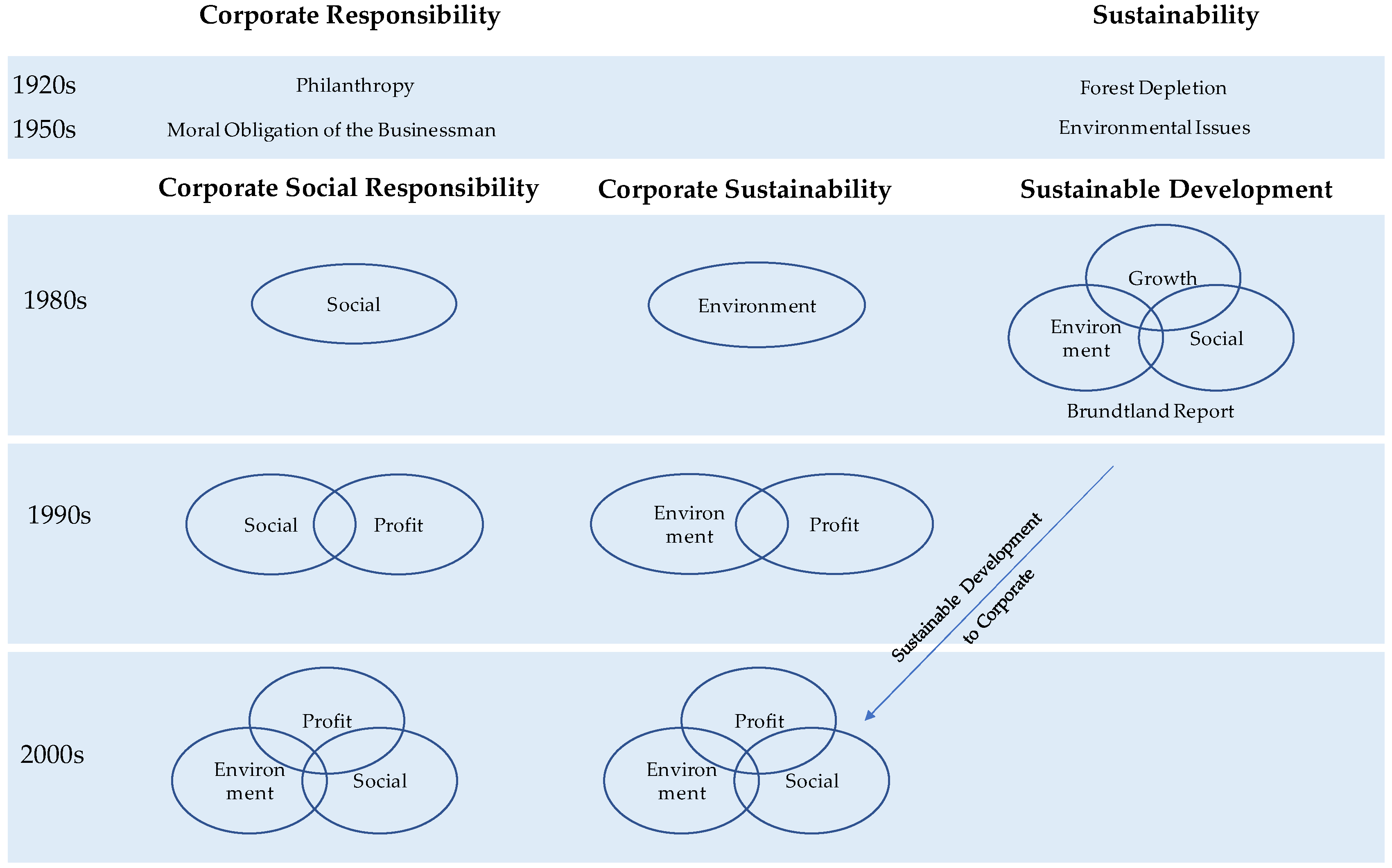

2.1.1. Sustainability, Sustainable Development and Corporate Sustainability

- Broadness: they have a large scope with multiple, overlapping and sometimes conflicting definitions;

- Normative Attractiveness: they have an overwhelmingly positive connotation—it is hard to be against them;

- Implication of Consensus: they deny or downplay the existence of conflicting interests; and

- Global Marketability: they are known and used by practitioners and academics [44].

2.1.2. Corporate Social Responsibility

2.1.3. Identified Themes around the Evolution of the Concept Corporate Sustainability

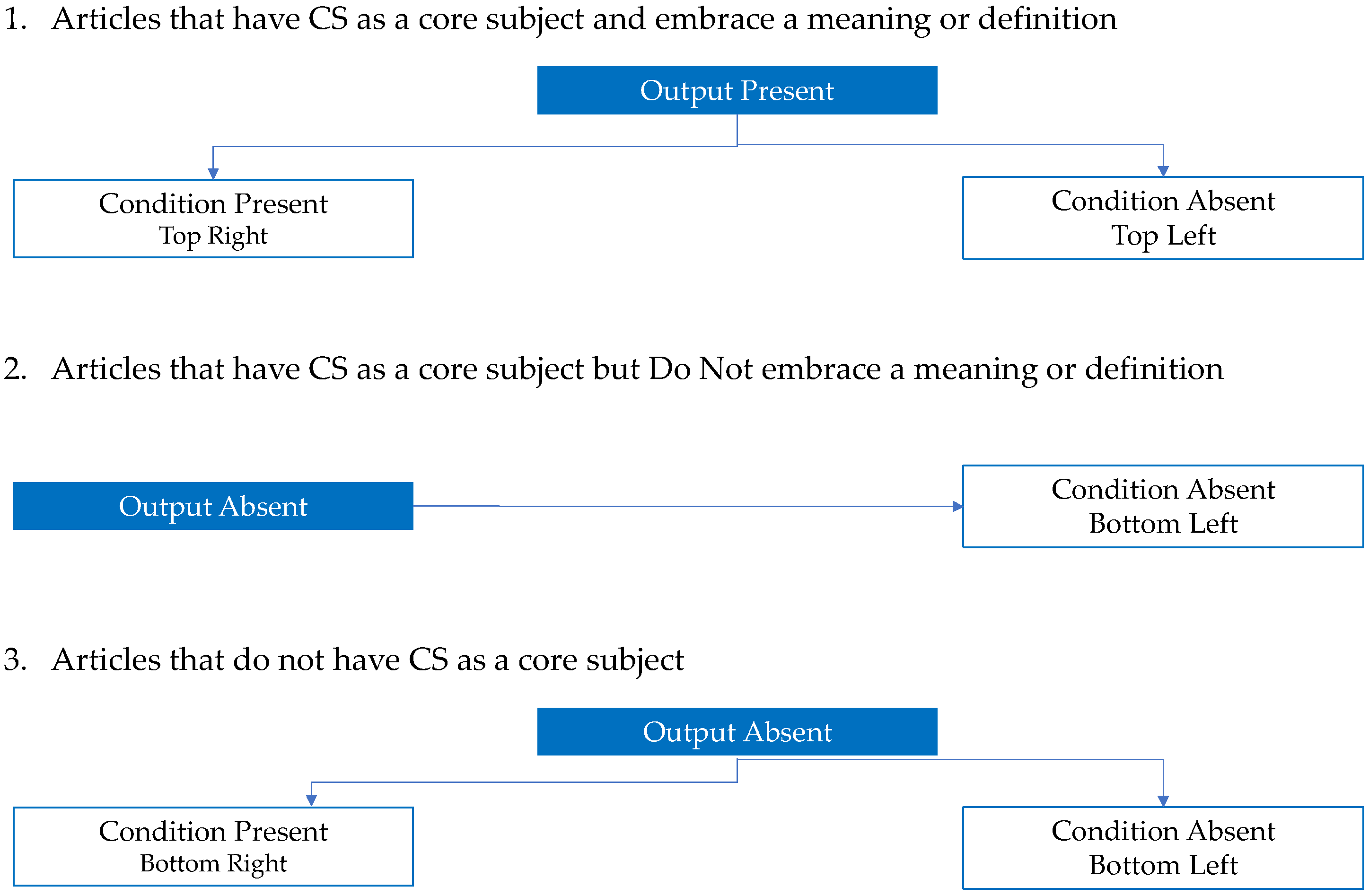

3. Methodology

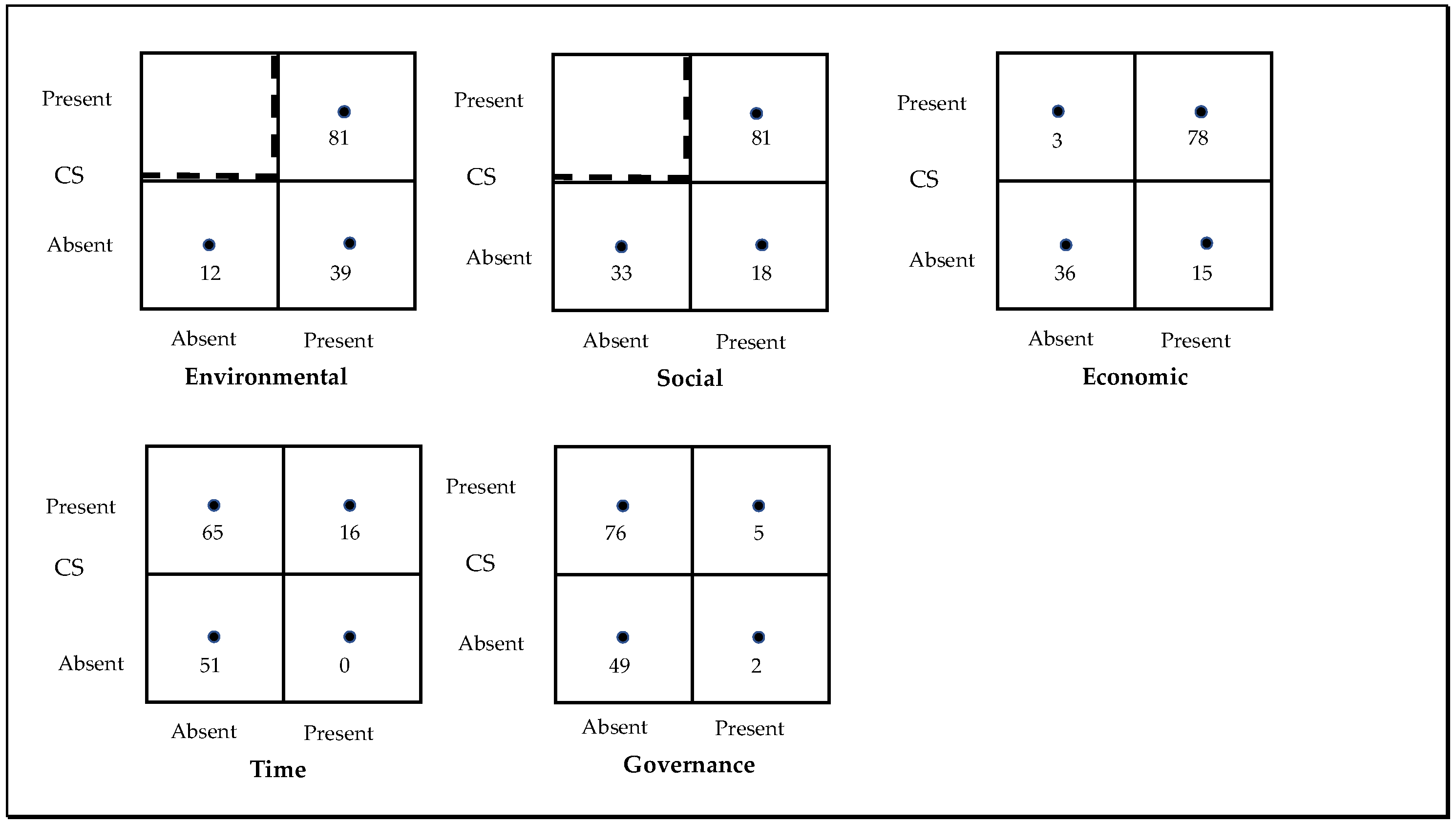

4. Results & Discussion

What Is Corporate Sustainability?

5. Conclusions

Supplementary Materials

Author Contributions

Funding

Informed Consent Statement

Data Availability Statement

Conflicts of Interest

References

- Montiel, I.; Delgado-Ceballos, J. Defining and Measuring Corporate Sustainability: Are We There Yet? Organ. Environ. 2014, 27, 113–139. [Google Scholar] [CrossRef]

- Meuer, J.; Koelbel, J.; Hoffmann, V.H. On the Nature of Corporate Sustainability. Organ. Environ. 2020, 33, 319–341. [Google Scholar] [CrossRef]

- Sanchez-Planelles, J.; Segarra-Oña, M.; Peiro-Signes, A. Building a Theoretical Framework for Corporate Sustainability. Sustainability 2020, 13, 273. [Google Scholar] [CrossRef]

- Amini, M.; Bienstock, C.C. Corporate Sustainability: An Integrative Definition and Framework to Evaluate Corporate Practice and Guide Academic Research. J. Clean. Prod. 2014, 76, 12–19. [Google Scholar] [CrossRef]

- Goertz, G. Social Science Concepts and Measurement. Available online: https://press.princeton.edu/books/hardcover/9780691205465/social-science-concepts-and-measurement (accessed on 16 May 2022).

- Mill, J.S. A System of Logic: Ratiocinative and Inductive; Originally Published in 1843; University Press of the Pacific: Honolulu, HI, USA, 2002; p. 622. [Google Scholar]

- Cohen, M.; Nagel, E. An Introduction to Logic and Scientific Method. Nature 1935, 135, 51. [Google Scholar] [CrossRef]

- Salas-Zapata, W.A.; Ortiz-Muñoz, S.M. Analysis of Meanings of the Concept of Sustainability. Sustain. Dev. 2019, 27, 153–161. [Google Scholar] [CrossRef] [Green Version]

- Jan Dul—Necessary Condition Analysis—Erasmus Research Institute of Management—ERIM. Available online: https://www.erim.eur.nl/necessary-condition-analysis/personal-pages/jan-dul/ (accessed on 16 May 2022).

- Editorial, G.; Hahn, T.; Figge, F.; Alberto Aragón-Correa, J.; Sharma, S. Advancing Research on Corporate Sustainability: Off to Pastures New or Back to the Roots? Bus. Soc. 2017, 56, 155–185. [Google Scholar] [CrossRef]

- Bergman, M.M.; Bergman, Z.; Berger, L. An Empirical Exploration, Typology, and Definition of Corporate Sustainability. Sustainability 2017, 9, 753. [Google Scholar] [CrossRef] [Green Version]

- Frecè, J.T.; Harder, D.L. Organisations beyond Brundtland: A Definition of Corporate Sustainability Based on Corporate Values. J. Sustain. Dev. 2018, 11, 184. [Google Scholar] [CrossRef] [Green Version]

- Urdan, M.S.; Luoma, P. Designing Effective Sustainability Assignments: How and Why Definitions of Sustainability Impact Assignments and Learning Outcomes. J. Manag. Educ. 2020, 44, 794–821. [Google Scholar] [CrossRef]

- Tøllefsen, T. Sustainability as a “Magic Concept”. Available online: https://web.p.ebscohost.com/abstract?direct=true&profile=ehost&scope=site&authtype=crawler&jrnl=11308354&AN=150379838&h=7IRq6kCmpF%2fv8SOKgj5At%2f6SR1mu%2be4UPCLL6jTUoCsMZoj%2fBOfM3EerTJWIBIYjLhZsdKVAPYIez49hV5xj5A%3d%3d&crl=c&resultNs=AdminWebAuth&resultLocal=ErrCrlNotAuth&crlhashurl=login.aspx%3fdirect%3dtrue%26profile%3dehost%26scope%3dsite%26authtype%3dcrawler%26jrnl%3d11308354%26AN%3d150379838 (accessed on 16 May 2022).

- Kantabutra, S.; Ketprapakorn, N. Toward a Theory of Corporate Sustainability: A Theoretical Integration and Exploration. J. Clean. Prod. 2020, 270, 122292. [Google Scholar] [CrossRef]

- Swarnapali, R. Corporate Sustainability: A Literature Review. 2017. Available online: https://www.researchgate.net/publication/317428267_Corporate_sustainability_A_Literature_review (accessed on 16 May 2022).

- Pdxscholar, P.; Marshall, S.; Brown, D.; Marshall, R.; Brown, D. The Strategy of Sustainability: A Systems Perspective on Environmental Initiatives. Calif. Manag. Rev. 2003, 46, 101–126. [Google Scholar]

- Banerjee, S.B. Who Sustains Whose Development? Sustainable Development and the Reinvention of Nature. Organ. Stud. 2003, 24, 143–180. [Google Scholar] [CrossRef]

- Costa, A.J.; Curi, D.; Bandeira, A.M.; Ferreira, A.; Tomé, B.; Joaquim, C.; Santos, C.; Góis, C.; Meira, D.; Azevedo, G.; et al. Literature Review and Theoretical Framework of the Evolution and Interconnectedness of Corporate Sustainability Constructs. Sustainability 2022, 14, 4413. [Google Scholar] [CrossRef]

- Christen, M.; Schmidt, S. A Formal Framework for Conceptions of Sustainability—A Theoretical Contribution to the Discourse in Sustainable Development. Sustain. Dev. 2012, 20, 400–410. [Google Scholar] [CrossRef]

- Landrum, N.E. Stages of Corporate Sustainability: Integrating the Strong Sustainability Worldview. Organ. Environ. 2018, 31, 287–313. [Google Scholar] [CrossRef]

- Bolis, I.; Morioka, S.N.; Sznelwar, L.I. When Sustainable Development Risks Losing Its Meaning. Delimiting the Concept with a Comprehensive Literature Review and a Conceptual Model. J. Clean. Prod. 2014, 83, 7–20. [Google Scholar] [CrossRef]

- Lankoski, L. Alternative Conceptions of Sustainability in a Business Context. J. Clean. Prod. 2016, 139, 847–857. [Google Scholar] [CrossRef]

- Bowen, H. Social Responsibilities of the Businessman, 1st ed.; Harper: New York, NY, USA, 1953. [Google Scholar]

- Smith, P.A.C.; Sharicz, C. The Shift Needed for Sustainability. Learn. Organ. 2011, 18, 73–86. [Google Scholar] [CrossRef]

- Nikolaou, I.E.; Tsalis, T.A.; Evangelinos, K.I. A Framework To Measure Corporate Sustainability Performance A Strong Sustainability-Based View of Firm. Sustain. Prod. Consum. 2019, 18, 1–18. [Google Scholar] [CrossRef]

- Ahi, P.; Searcy, C.; Jaber, M.Y. A Quantitative Approach for Assessing Sustainability Performance of Corporations. Ecol. Econ. 2018, 152, 336–346. [Google Scholar] [CrossRef]

- Jerónimo Silvestre, W.; Antunes, P.; Leal Filho, W. The Corporate Sustainability Typology: Analysing Sustainability Drivers and Fostering Sustainability at Enterprises. Technol. Econ. Dev. Econ. 2018, 24, 513–533. [Google Scholar] [CrossRef] [Green Version]

- Sheehy, B.; Farneti, F. Corporate Social Responsibility, Sustainability, Sustainable Development and Corporate Sustainability: What Is the Difference, and Does It Matter? Sustainability 2021, 13, 5965. [Google Scholar] [CrossRef]

- Bansal, P.; Song, H.C. Similar But Not the Same: Differentiating Corporate Sustainability from Corporate Responsibility. Acad. Manag. Ann. 2016, 11, 105–149. [Google Scholar] [CrossRef]

- Ashrafi, M.; Magnan, G.M.; Adams, M.; Walker, T.R. Understanding the Conceptual Evolutionary Path and Theoretical Underpinnings of Corporate Social Responsibility and Corporate Sustainability. Sustainability 2020, 12, 760. [Google Scholar] [CrossRef] [Green Version]

- Schrippe, P.; Ribeiro, J.L.D. Preponderant Criteria for the Definition of Corporate Sustainability Based on Brazilian Sustainable Companies. J. Clean. Prod. 2019, 209, 10–19. [Google Scholar] [CrossRef]

- Lozano, R. Addressing Stakeholders and Better Contributing to Sustainability through Game Theory. Available online: https://www.academia.edu/1514216/Addressing_Stakeholders_and_Better_Contributing_to_Sustainability_through_Game_Theory (accessed on 16 May 2022).

- Farley, H.M.; Smith, Z.A. Sustainability: If It’s Everything, Is It Nothing? 2nd ed.; Series: Critical Issues in Global Politics; Abingdon; Oxon: New York, NY, USA, 2020; ISBN 9781351124928. [Google Scholar]

- Grober, U. Sustainability: A Cultural History; UIT Cambridge Ltd.: Chicago, IL, USA, 2012; ISBN 9780857840462. [Google Scholar]

- Robinson, J. Squaring the Circle? Some Thoughts on the Idea of Sustainable Development. Ecol. Econ. 2004, 48, 369–384. [Google Scholar] [CrossRef]

- Lozano, R. Proposing a Definition and a Framework of Organisational Sustainability: A Review of Efforts and a Survey of Approaches to Change. Sustainability 2018, 10, 1157. [Google Scholar] [CrossRef] [Green Version]

- Johnson, E.W.; Greenberg, P. The US Environmental Movement of the 1960s and 1970s: Building Frameworks of Sustainability. In Routledge Handbook of the History of Sustainability; Routledge: Abingdon, UK, 2017; pp. 137–150. [Google Scholar] [CrossRef]

- Meadows, D.H.; Meadows, D.L.; Randers, J.; Behrens, W.; Club of Rome; Potomac Associates. The Limits to Growth: A Report for the Club of Rome’s Project on the Predicament of Mankind; Potomac Associates: Washington, DC, USA, 1974; ISBN 0876639015. [Google Scholar]

- Kidd, C.V. The Evolution of Sustainability. J. Agric. Environ. Ethics 1992, 5, 1–26. [Google Scholar] [CrossRef]

- Andrushkiv, B.; Melnyk, L.; Palianytsia, V.; Sorokivska, O.; Sherstiuk, R. Prospects for Implementation of Corporate Environmental Responsibility Concept: The Eu Experience for Ukraine. Indep. J. Manag. Prod. 2020, 11, 600. [Google Scholar] [CrossRef]

- Carson, R. Silent Spring; Smithsonian Institution: Washington, DC, USA, 1962. [Google Scholar]

- Johnston, P.; Everard, M.; Santillo, D.; Robèrt, K.H. Reclaiming the Definition of Sustainability (7 Pp). Environ. Sci. Pollut. Res. Int. 2007, 14, 60–66. [Google Scholar] [CrossRef]

- Pollitt, C.; Hupe, P. Talking About Government. Publ. Cover. Public Manag. Rev. 2011, 13, 641–658. [Google Scholar] [CrossRef]

- Rist, G.D. As a buzzword. In Deconstructing Development Discourse Buzzwords and Fuzzwords, 21st ed.; Cornwall, A., Eade, D., Eds.; Oxfam GB: Oxford, UK, 2010. [Google Scholar]

- Daly, H.E. Steady-State Economics versus Growthmania: A Critique of the Orthodox Conceptions of Growth, Wants, Scarcity, and Efficiency. Available online: https://www.jstor.org/stable/4603736 (accessed on 16 May 2022).

- Mebratu, D. Sustainability and Sustainable Development: Historical and Conceptual Review. Environ. Impact Assess. Rev. 1998, 18, 493–520. [Google Scholar] [CrossRef]

- Redclift, M. Sustainable Development (1987-2005): An Oxymoron Comes of Age. Sustain. Dev. 2005, 13, 212–227. [Google Scholar] [CrossRef] [Green Version]

- Sarkar, S.; Searcy, C. Zeitgeist or Chameleon? A Quantitative Analysis of CSR Definitions. J. Clean. Prod. 2016, 135, 1423–1435. [Google Scholar] [CrossRef]

- Roblek, V.; Bach, M.P.; Meško, M.; Kresal, F. Corporate Social Responsibility and Challenges for Corporate Sustainability in First Part of the 21st Century. Cambio. Riv. Sulle Trasformazioni Soc. 2020, 10, 31–46. [Google Scholar] [CrossRef]

- Dyllick, T.; Muff, K. Clarifying the Meaning of Sustainable Business: Introducing a Typology From Business-as-Usual to True Business Sustainability. Organ. Environ. 2016, 29, 156–174. [Google Scholar] [CrossRef] [Green Version]

- Steurer, R.; Langer, M.E.; Konrad, A.; Martinuzzi, A. Corporations, Stakeholders and Sustainable Development I: A Theoretical Exploration of Business–Society Relations. J. Bus. Ethics 2005, 61, 263–281. [Google Scholar] [CrossRef]

- Dyllick, T.; Hockerts, K. Beyond the Business Case for Corporate Sustainability. Bus. Strategy Environ. 2002, 11, 130–141. [Google Scholar] [CrossRef]

- Frederick, W.C. Corporation, Be Good!: The Story of Corporate Social Responsibility; Dog Ear Publishing: Indianapolis, IN, USA, 2006; ISBN 1598581031. [Google Scholar]

- Berle, A.A. Corporate Powers as Powers in Trust. Harv. Law Rev. 1931, 44, 1049. [Google Scholar] [CrossRef] [Green Version]

- Dodd, E.M. For Whom Are Corporate Managers Trustees? Harv. Law Rev. 1932, 45, 1145. [Google Scholar] [CrossRef]

- Carroll, A.B.; Shabana, K.M. The Business Case for Corporate Social Responsibility: A Review of Concepts, Research and Practice. Int. J. Manag. Rev. 2010, 12, 85–105. [Google Scholar] [CrossRef]

- Carroll, A.B. Corporate Social Responsibility: Evolution of a Definitional Construct. Bus. Soc. 1999, 38, 268–295. [Google Scholar] [CrossRef]

- Freeman, R.E. Strategic Management: A Stakeholder Approach; Pitman: Boston, MA, USA, 1984. [Google Scholar]

- Griffin, J.J.; Mahon, J.F. The Corporate Social Performance and Corporate Financial Performance Debate: Twenty-Five Years of Incomparable Research. Bus. Soc. 1997, 36, 5–31. [Google Scholar] [CrossRef]

- Waddock, S.A.; Graves, S.B. The Corporate Social Performance-Financial Performance Link. Strateg. Manag. J. 1997, 18, 303–319. [Google Scholar] [CrossRef]

- Margolis, J.D.; Walsh, J.R.; Adler, P.; Aldrich, H.; Andreasen, A.; Austin, J.; Behling, C.; Cohen, M.; Dolan, B.; Gentile, M.; et al. Misery Loves Companies: Rethinking Social Initiatives by Business. Adm. Sci. Q. 2003, 48, 268–305. [Google Scholar] [CrossRef] [Green Version]

- Orlitzky, M.; Schmidt, F.L.; Rynes, S.L. Corporate Social and Financial Performance: A Meta-Analysis. Organ. Stud. 2003, 24, 403–411. [Google Scholar] [CrossRef]

- Baumol, W.J. Enlightened Self-Interest and Corporate Philanthropy. In A New Rationale for Corporate Social Policy; Committee for Economic Development: New York, NY, USA, 1970; pp. 3–19. [Google Scholar]

- Wood, D.J. Corporate Social Performance Revisited. Acad. Manag. Rev. 1991, 16, 691. [Google Scholar] [CrossRef]

- European Commission. Corporate Social Responsibility Main Issues; Oce for Ocial Publications of the European Communities: Brussels, Belgium, 2002; Available online: https://www.europarl.europa.eu/meetdocs/committees/deve/20020122/com(2001)366_en.pdf (accessed on 16 May 2022).

- van Marrewijk, M.; Werre, M. Multiple Levels of Corporate Sustainability. J. Bus. Ethics 2003, 44, 107–119. [Google Scholar] [CrossRef]

- van Marrewijk, M. Concepts and Definitions of CSR and Corporate Sustainability: Between Agency and Communion. J. Bus. Ethics 2003, 44, 95–105. [Google Scholar] [CrossRef]

- Jennings, P.D.; Zandbergen, P.A. Ecologically Sustainable Organizations: An Institutional Approach. Acad. Manag. Rev. 1995, 20, 1015–1052. [Google Scholar] [CrossRef]

- O’Riordan, T. The Challenge for Environmentalism. In New Models in Geography, 1st ed.; Peet, R., Thrift, N., Eds.; Unwin Hyman: London, UK, 1989. [Google Scholar]

- Pearce, D.; Turner, R.K.; Riordan, T.O.; Atkinson, G. Blueprint 3: Measuring Sustainable Development; Earthscan: London, UK, 1993; ISBN 9781853831836. [Google Scholar]

- Roome, N.J. Looking Back, Thinking Forward: Distinguishing between Weak and Strong Sustainability. Oxf. Handb. Bus. Nat. Environ. 2012, 620–629. [Google Scholar]

- Ott, K.; Muraca, B.; Baatz, C. Strong Sustainability as a Frame for Sustainability Communication. In Sustainability Communication; Springer: Dordrecht, The Netherlands, 2011; pp. 13–25. [Google Scholar] [CrossRef]

- Hediger, W. Reconciling “Weak” and “Strong” Sustainability. Int. J. Soc. Econ. 1999, 26, 1120–1144. [Google Scholar] [CrossRef]

- Gladwin, T.N.; Kennelly, J.J.; Krause, T.-S. Shifting Paradigms for Sustainable Development: Implications for Management Theory and Research. Acad. Manag. Rev. 1995, 20, 874. [Google Scholar] [CrossRef]

- Hawken, P. The Ecology of Commerce: A Declaration of Sustainability; Harper Business: New York City, NY, USA, 1993; Volume 11, ISBN 0887306551. [Google Scholar]

- Shrivastava, P. Environmental Technologies and Competitive Advantage. Strateg. Manag. J. 1995, 16, 183–200. [Google Scholar] [CrossRef]

- Schoenmaker, D.; Schramade, W. Principles of Sustainable Finance. Available online: https://global.oup.com/academic/product/principles-of-sustainable-finance-9780198869818?lang=en&cc=nl (accessed on 16 May 2022).

- Suddaby, R. Editor’s Comments: Construct Clarity in Theories of Management and Organization. Acad. Manag. Rev. 2010, 35, 346–357. [Google Scholar]

- Dobson, A. Environment Sustainabilities: An Analysis and a Typology. Environ. Politics 1996, 5, 401–428. [Google Scholar] [CrossRef]

- Chalmers, A.F.; Alan, F. What Is This Thing Called Science? Hackett Publishing: Cambridge, MA, USA, 1999; ISBN 9780335201099. [Google Scholar]

- Hjørland, B. Concept Theory. J. Am. Soc. Inf. Sci. Technol. 2009, 60, 1519–1536. [Google Scholar] [CrossRef]

- Sterman, J.; Amengual, M.; Gibbons, R.; Gulati, R.; Henderson, R.; Jay, J.; Keith, D.; King, A.; Lyneis, J.; Repenning, N.; et al. Stumbling towards Sustainability. Lead. Sustain. Chang. 2015, 50–80. Available online: https://www.hbs.edu/faculty/Shared%20Documents/conferences/2013-change-and-sustainability/Sterman.pdf (accessed on 12 February 2022).

- Dahlsrud, A. How Corporate Social Responsibility Is Defined: An Analysis of 37 Definitions. Corp. Soc. Responsib. Environ. Manag. 2008, 15, 1–13. [Google Scholar] [CrossRef]

- Kleine, A.; von Hauff, M. Sustainability-Driven Implementation of Corporate Social Responsibility: Application of the Integrative Sustainability Triangle. J. Bus. Ethics 2009, 85, 517–533. [Google Scholar] [CrossRef]

- Cheng, B.; Ioannou, I.; Serafeim, G. Corporate Social Responsibility and Access to Finance. Strat. Manag. J. 2014, 35, 1–23. [Google Scholar] [CrossRef]

- Delmas, M.A.; Toffel, M.W. Organizational Responses to Environmental Demands: Opening the Black Box. Strateg. Manag. J. 2008, 29, 1027–1055. [Google Scholar] [CrossRef]

- Herva, M.; Franco, A.; Carrasco, E.F.; Roca, E. Review of Corporate Environmental Indicators. J. Clean. Prod. 2011, 19, 1687–1699. [Google Scholar] [CrossRef] [Green Version]

- Ehrenfeld, J.; Hoffman, A.J. Flourishing: A Frank Conversation about Sustainability; Stanford University Press: Redwood City, CA, USA, 2013; ISBN 9780804784146. [Google Scholar]

- Boiral, O.; Gendron, Y. Sustainable Development and Certification Practices: Lessons Learned and Prospects. Bus. Strategy Environ. 2011, 20, 331–347. [Google Scholar] [CrossRef]

- Figge, F.; Hahn, T. Sustainable Value Added—Measuring Corporate Contributions to Sustainability beyond Eco-Efficiency. Ecol. Econ. 2004, 48, 173–187. [Google Scholar] [CrossRef]

- Ayres, R.U.; van den Bergh, J.C.J.M.; Gowdy, J.M. Strong versus Weak Sustainability: Economics, Natural Sciences, and Consilience. Environ. Ethics 2001, 23, 155–168. [Google Scholar] [CrossRef]

- Beckmann, M.; Hielscher, S.; Pies, I. Commitment Strategies for Sustainability: How Business Firms Can Transform Trade-Offs Into Win-Win Outcomes. Bus. Strategy Environ. 2014, 23, 18–37. [Google Scholar] [CrossRef]

- Bansal, P.; DesJardine, M. Business Sustainability: It Is about Time. Strateg. Organ. 2014, 12, 70–78. [Google Scholar] [CrossRef]

- Kim, E.H.; Lyon, T.P. Greenwash vs. Brownwash: Exaggeration and Undue Modesty in Corporate Sustainability Disclosure. Organ. Sci. 2015, 26, 705–723. [Google Scholar] [CrossRef] [Green Version]

- Griffiths, A.; Petrick, J.A. Corporate Architectures for Sustainability. Int. J. Oper. Prod. Manag. 2001, 21, 1573–1585. [Google Scholar] [CrossRef]

- Funk, K. Sustainability and Performance. MIT Sloan Manag. Rev. 2003, 44, 65–70. [Google Scholar]

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2022 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Pazienza, M.; de Jong, M.; Schoenmaker, D. Clarifying the Concept of Corporate Sustainability and Providing Convergence for Its Definition. Sustainability 2022, 14, 7838. https://doi.org/10.3390/su14137838

Pazienza M, de Jong M, Schoenmaker D. Clarifying the Concept of Corporate Sustainability and Providing Convergence for Its Definition. Sustainability. 2022; 14(13):7838. https://doi.org/10.3390/su14137838

Chicago/Turabian StylePazienza, Mariapia, Martin de Jong, and Dirk Schoenmaker. 2022. "Clarifying the Concept of Corporate Sustainability and Providing Convergence for Its Definition" Sustainability 14, no. 13: 7838. https://doi.org/10.3390/su14137838

APA StylePazienza, M., de Jong, M., & Schoenmaker, D. (2022). Clarifying the Concept of Corporate Sustainability and Providing Convergence for Its Definition. Sustainability, 14(13), 7838. https://doi.org/10.3390/su14137838