The Impact of Fintech on Economic Growth: Evidence from China

Abstract

:1. Introduction

2. Literature Review and Hypothesis Development

2.1. Literature Review

2.2. Hypothesis Development

3. Data and Methodology

3.1. Data

3.2. Methodology

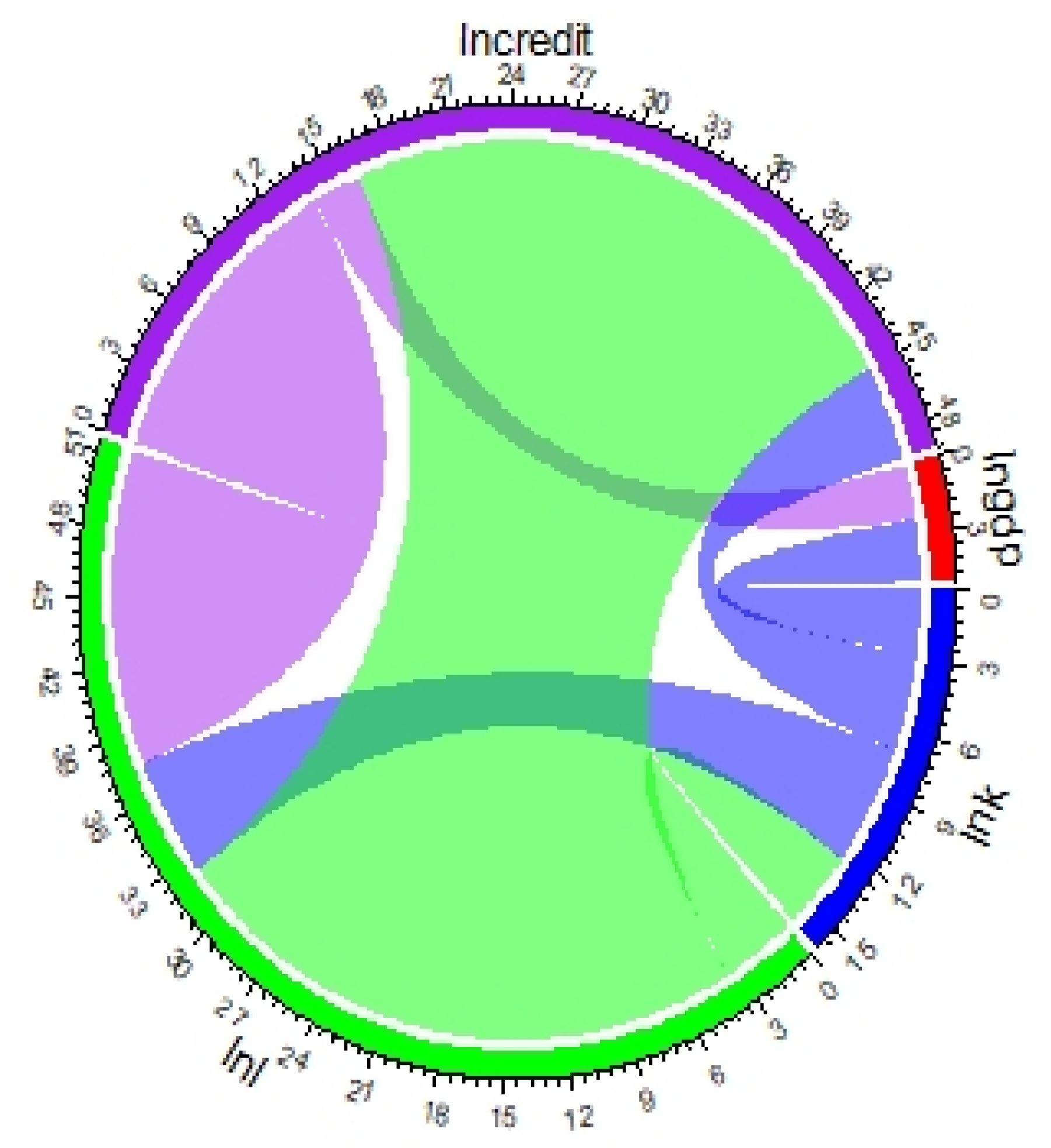

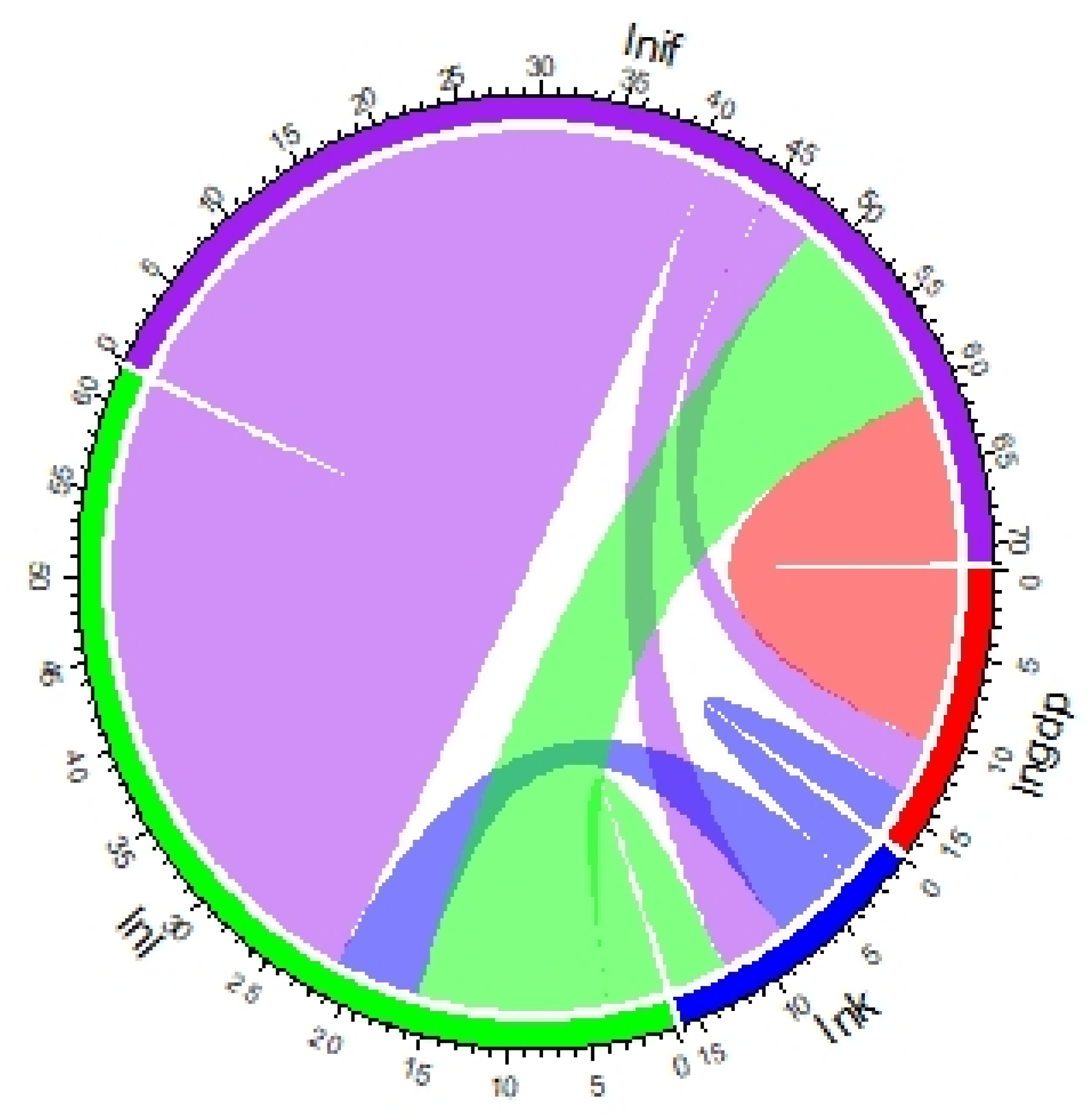

3.3. Causality Model

4. Results and Discussion

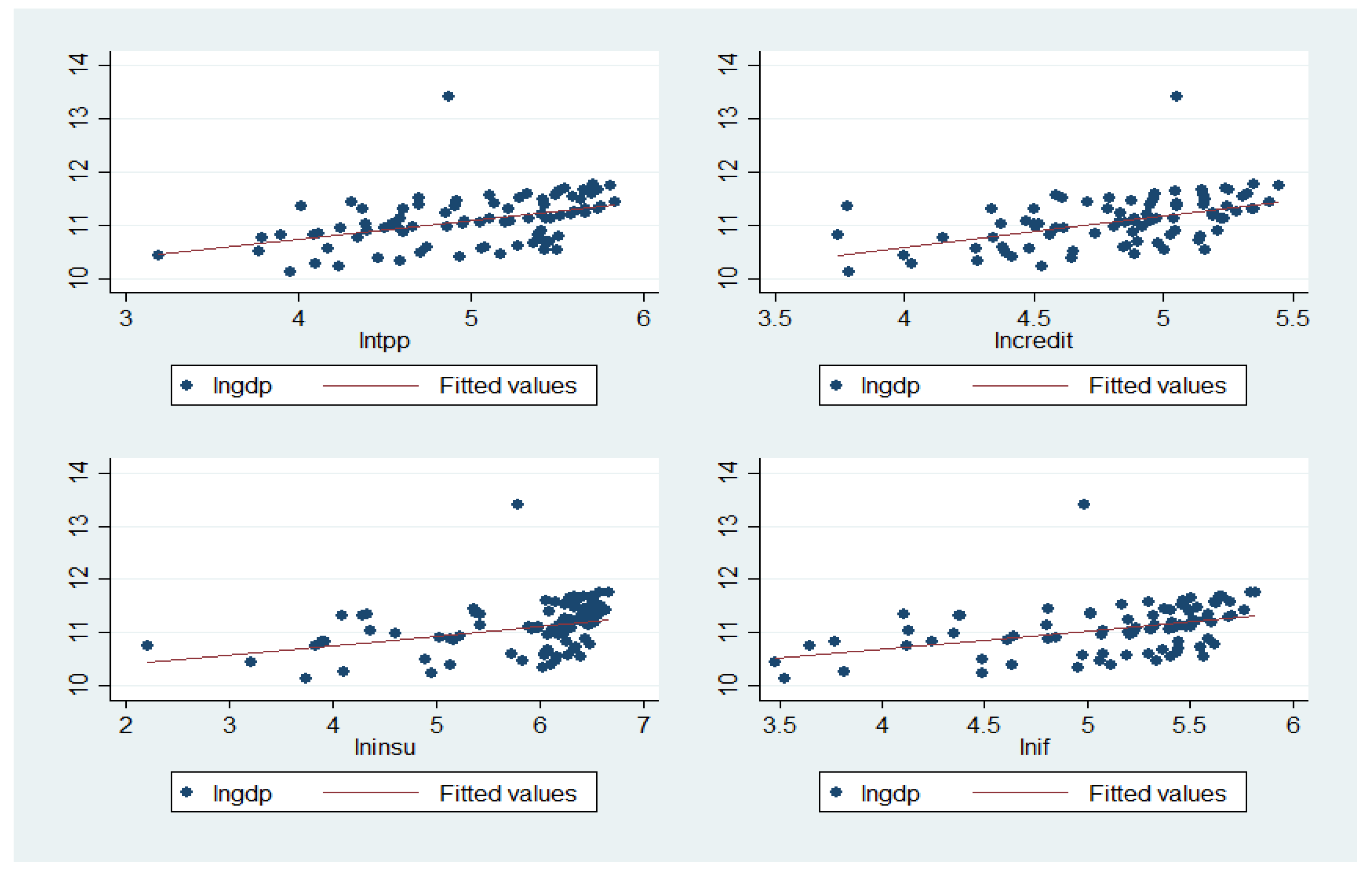

4.1. Full Sample Results

4.2. Regional Analysis

4.3. Causality Analysis

4.4. Further Analysis

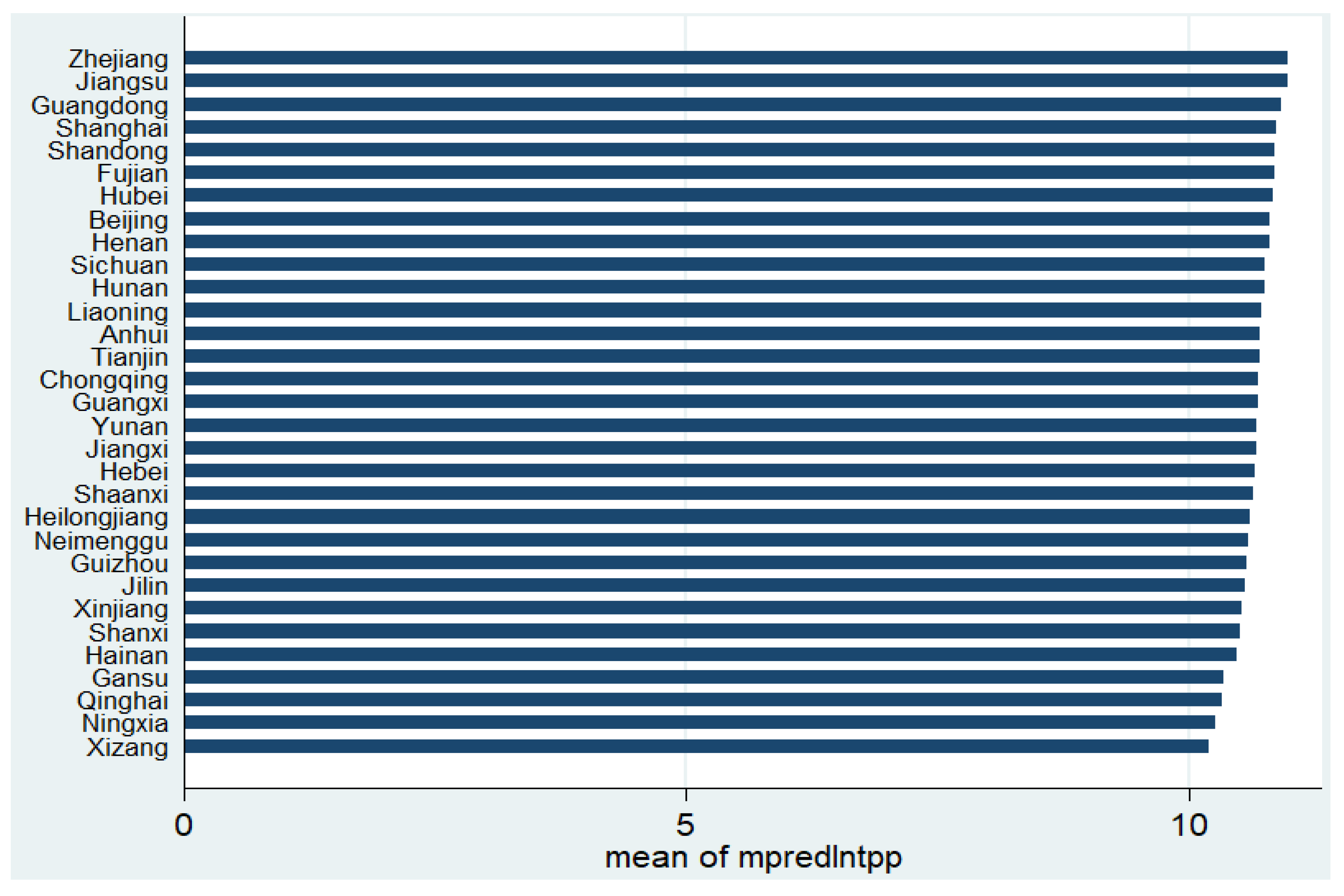

4.5. Province-Specific Analysis

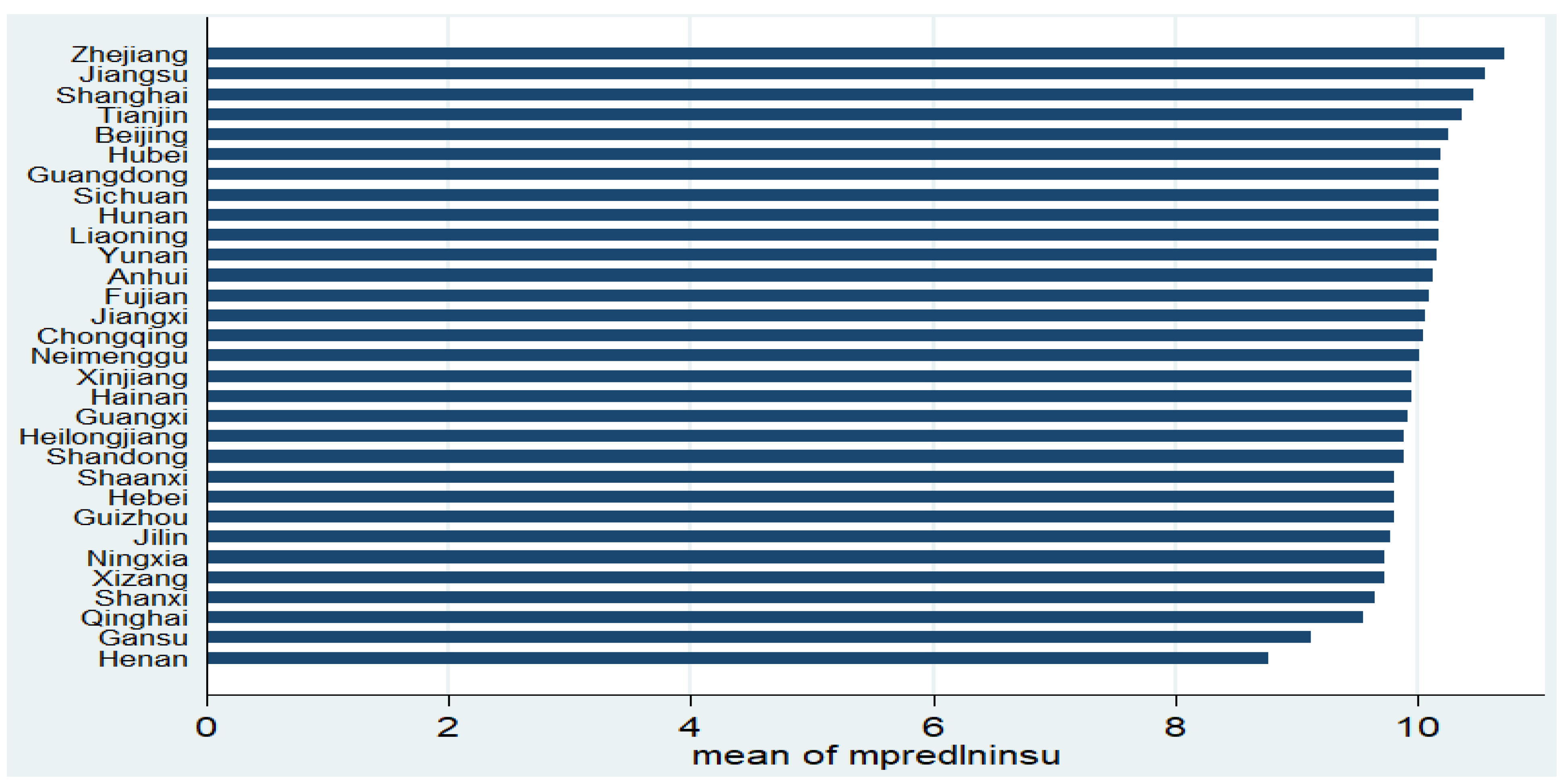

4.5.1. Province-Specific Effect of Third-Party Payment on Economic Growth

4.5.2. Province-Specific Effect of Credit on Economic Growth

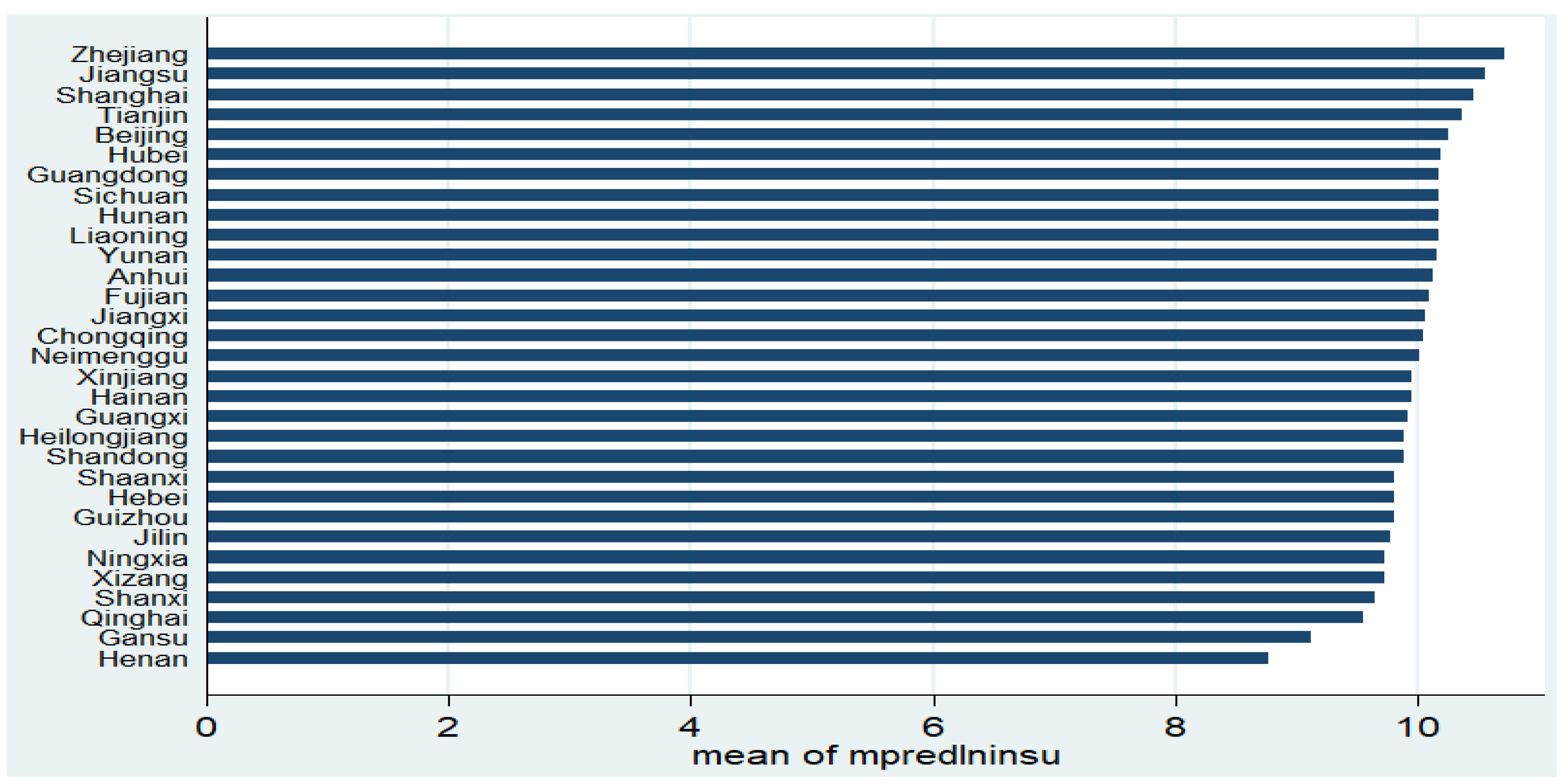

4.5.3. Province-Specific Effect of Insurance on Economic Growth

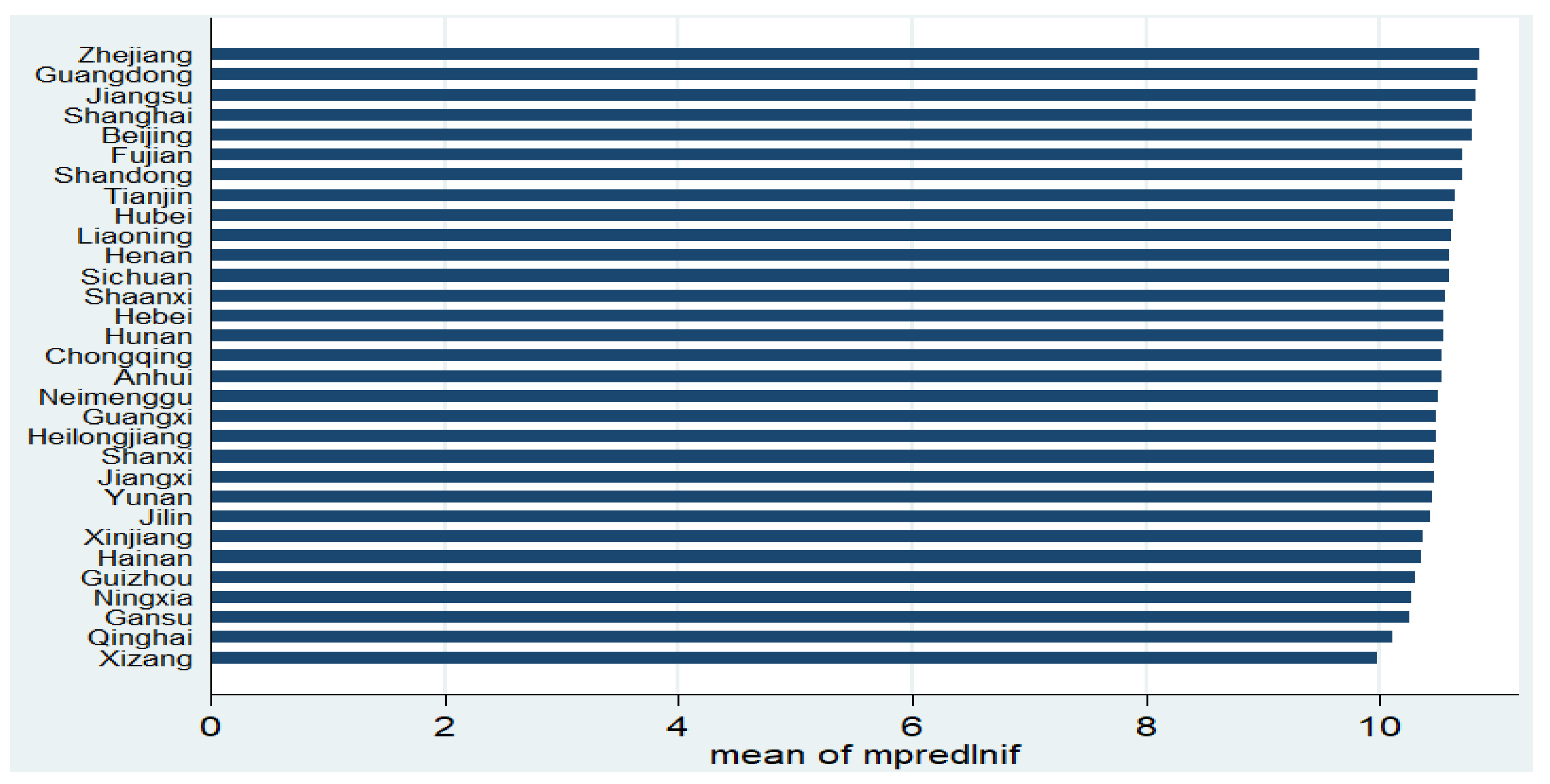

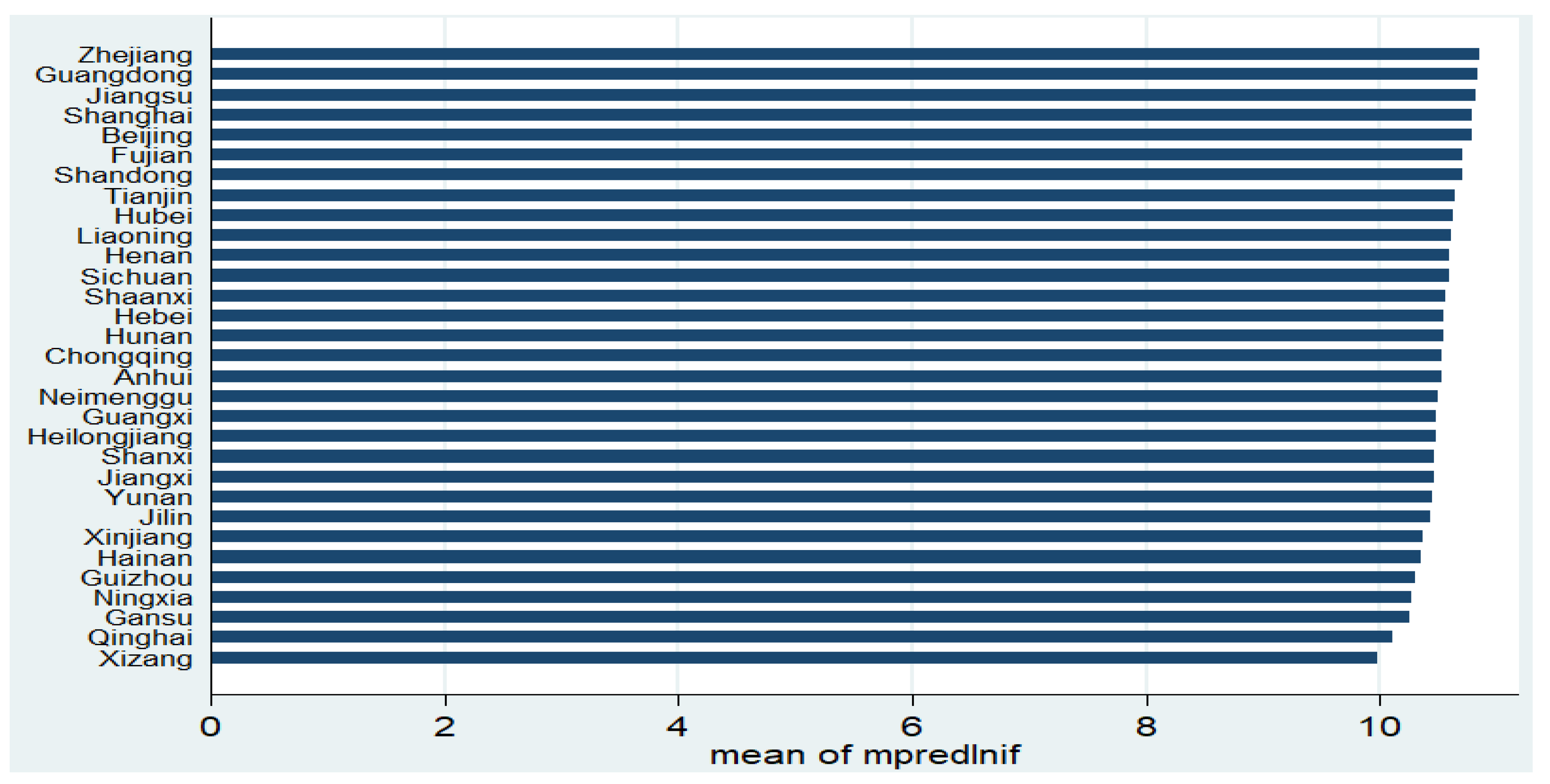

4.5.4. Province-Specific Effect of Fintech on Economic Growth

5. Conclusions and Policy Recommendations

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Conflicts of Interest

References

- Shim, Y.; Shin, D.-H. Analyzing China’s Fintech Industry from the Perspective of Actor—Network Theory. Telecomm. Policy 2016, 40, 168–181. [Google Scholar] [CrossRef]

- Xu, J. China’s Internet Finance: A Critical Review. China World Econ. 2017, 25, 78–92. [Google Scholar] [CrossRef]

- Appiah-Otoo, I.; Song, N. The impact of fintech on poverty reduction: Evidence from China. Sustainability 2021, 13, 5225. [Google Scholar] [CrossRef]

- Chen, T.; Chang, R. Using machine learning to evaluate the influence of FinTech patents: The case of Taiwan’ s financial industry. J. Comput. Appl. Math. 2021, 390, 113215. [Google Scholar] [CrossRef]

- Abbasi, K.; Alam, A.; Anna, M.; Luu, T.; Huynh, D. FinTech, SME efficiency and national culture: Evidence from OECD countries. Technol. Forecast. Soc. Change 2021, 163, 120454. [Google Scholar] [CrossRef]

- Guo, Y.; Zhou, W.; Luo, C.; Liu, C.; Xiong, H. Instance-based credit risk assessment for investment decisions in P2P lending. Eur. J. Oper. Res. 2016, 249, 417–426. [Google Scholar] [CrossRef]

- Odinet, C.K.; College, O. Consumer BitCredit and Fintech Lending. Ala. Law Rev. 2018, 69, 781–858. [Google Scholar]

- Abbasi, K.; Alam, A.; Noor, A.B.; Imtiaz, A.B.; Shahzad, N. P2P lending fintech’s and SME’s access to finance. Econ. Lett. 2021, 204, 109890. [Google Scholar] [CrossRef]

- Wei, S. Internet lending in China: Status quo, potential risks and regulatory options. Comput. Law Secur. Rev. Int. J. Technol. Law Pract. 2015, 31, 793–809. [Google Scholar] [CrossRef]

- Ding, C.; Kavuri, A.S.; Milne, A. Lessons from the rise and fall of Chinese peer-to-peer lending. J. Bank. Regul. 2021, 22, 133–143. [Google Scholar] [CrossRef]

- Zhongkai, T.; Hassan, A.F.S. Internet Finance and Its Potential Risks: The Case of China. Int. J. Account. Financ. Bus. 2019, 4, 45–51. [Google Scholar]

- Chen, R.; Yu, J.; Jin, C.; Bao, W. Internet finance investor sentiment and return comovement. Pacific Basin Financ. J. 2019, 56, 151–161. [Google Scholar] [CrossRef]

- Appiah-Otoo, I.; Song, N. The impact of ICT on economic growth-Comparing rich and poor countries. Telecomm. Policy 2021, 45, 102082. [Google Scholar] [CrossRef]

- Anyanwu, J.C. Factors Affecting Economic Growth in Africa: Are There any Lessons from China? Afr. Dev. Rev. 2014, 26, 468–493. [Google Scholar] [CrossRef]

- Asongu, S.A.; Odhiambo, N.M. Foreign direct investment, information technology and economic growth dynamics in Sub-Saharan Africa. Telecomm. Policy 2020, 44, 101838. [Google Scholar] [CrossRef]

- Maruta, A.A.; Banerjee, R.; Cavoli, T. Foreign aid, institutional quality and economic growth: Evidence from the developing world. Econ. Model. 2019, 89, 444–463. [Google Scholar] [CrossRef]

- Dai, X.; Sun, Z. Does firm innovation improve aggregate industry productivity? Evidence from Chinese manufacturing firms. Struct. Chang. Econ. Dyn. 2021, 56, 1–9. [Google Scholar] [CrossRef]

- Acheampong, A.O.; Adams, S.; Boateng, E. Do globalization and renewable energy contribute to carbon emissions mitigation in Sub-Saharan Africa? Sci. Total Environ. 2019, 677, 436–446. [Google Scholar] [CrossRef]

- Appiah-Otoo, I.; Song, N.; Acheampong, A.O.; Yao, X. Crowdfunding and renewable energy development: What does the data say? Int. J. Energy Res. 2022, 46, 1837–1852. [Google Scholar] [CrossRef]

- Hou, X.; Gao, Z.; Wang, Q. Internet finance development and banking market discipline: Evidence from China. J. Financ. Stab. 2016, 22, 88–100. [Google Scholar] [CrossRef]

- Guo, P.; Shen, Y. The impact of Internet finance on commercial banks’ risk taking: Evidence from China. China Financ. Econ. Rev. 2016, 4, 16. [Google Scholar] [CrossRef] [Green Version]

- Dong, J.; Yin, L.; Liu, X.; Hu, M.; Li, X. Impact of internet finance on the performance of commercial banks in China. Int. Rev. Financ. Anal. 2020, 72, 101579. [Google Scholar] [CrossRef]

- Meifang, Y.; He, D.; Xianrong, Z.; Xiaobo, X. Impact of payment technology innovations on the traditional financial industry: A focus on China. Technol. Forecast. Soc. Change 2018, 135, 199–207. [Google Scholar] [CrossRef]

- Zhang, X.; Zhang, J.; Wan, G.; Luo, Z. Fintech, Growth, and Inequality: Evidence from China’s Household Survey Data. Singap. Econ. Rev. 2020, 65, 75–93. [Google Scholar] [CrossRef]

- Wang, X.; He, G. Digital financial inclusion and farmers’ vulnerability to poverty: Evidence from rural China. Sustainability 2020, 12, 1668. [Google Scholar] [CrossRef] [Green Version]

- Zhang, X.; Tan, Y.; Hu, Z.; Wang, C.; Wan, G. The Trickle-down Effect of Fintech Development: From the Perspective of Urbanization. China World Econ. 2020, 28, 23–40. [Google Scholar] [CrossRef]

- Li, J.; Wu, Y.; Xiao, J.J. The impact of digital finance on household consumption: Evidence from China. Econ. Model. 2019, 86, 317–326. [Google Scholar] [CrossRef] [Green Version]

- Liu, T.; Pan, B.; Yin, Z. Pandemic, Mobile Payment, and Household Consumption: Micro-Evidence from China. Emerg. Mark. Financ. Trade 2020, 56, 2378–2389. [Google Scholar] [CrossRef]

- Yin, Z.; Gong, X.; Guo, P.; Wu, T. What Drives Entrepreneurship in Digital Economy? Evidence from China. Econ. Model. 2019, 82, 66–73. [Google Scholar] [CrossRef]

- Munyegera, G.K.; Matsumoto, T. Mobile Money, Remittances, and Household Welfare: Panel Evidence from Rural Uganda. World Dev. 2016, 79, 127–137. [Google Scholar] [CrossRef]

- Li, Y.; Jin, X.; Tian, W. Econometric analysis of disequilibrium relations between internet finance and real economy in China. Int. J. Comput. Intell. Syst. 2019, 12, 1454–1464. [Google Scholar] [CrossRef] [Green Version]

- Deng, X.; Huang, Z.; Cheng, X. FinTech and sustainable development: Evidence from China based on P2P data. Sustainability 2019, 11, 6434. [Google Scholar] [CrossRef] [Green Version]

- Ding, R.; Shi, F.; Hao, S. Digital Inclusive Finance, Environmental Regulation, and Regional Economic Growth: An Empirical Study Based on Spatial Spillover Effect and Panel Threshold Effect. Sustainability 2022, 14, 4340. [Google Scholar] [CrossRef]

- Liu, Y.; Luan, L.; Wu, W.; Zhang, Z.; Hsu, Y. Can digital financial inclusion promote China’s economic growth? Int. Rev. Financ. Anal. 2021, 78, 101889. [Google Scholar] [CrossRef]

- Ahmad, M.; Majeed, A.; Khan, M.A.; Sohaib, M.; Shehzad, K. Digital financial inclusion and economic growth: Provincial data analysis of China. China Econ. J. 2021, 14, 291–310. [Google Scholar] [CrossRef]

- Ye, B.; Yuan, J.; Guan, Y. Internet Finance, Financing of Small and Micro Enterprises and the Macroeconomy. Emerg. Mark. Financ. Trade 2022, 1–16. [Google Scholar] [CrossRef]

- Ang, J.B. A survey of recent developments in the literature of finance and growth. J. Econ. Surv. 2008, 22, 536–576. [Google Scholar] [CrossRef]

- Appiah-Otoo, I.; Song, N. Finance-growth nexus: New insight from Ghana. Int. J. Financ. Econ. 2020. [Google Scholar] [CrossRef]

- Sun, Y.; Liu, C. Research of Internet Finance Support for ‘Mass Entrepreneurship and Innovation’. Acad. Res. Int. 2016, 7, 168–174. [Google Scholar]

- Honglei, G. Internet Finance Innovation and Entrepreneurship Based on Classification Algorithm; Springer: Berlin/Heidelberg, Germany, 2021. [Google Scholar] [CrossRef]

- Shao, Z.; Zhang, L.; Li, X.; Guo, Y. Antecedents of trust and continuance intention in mobile payment platforms: The moderating effect of gender. Electron. Commer. Res. Appl. 2019, 33, 100823. [Google Scholar] [CrossRef]

- Fernandes, A.M.; Mattoo, A.; Nguyen, H.; Schiffbauer, M. The internet and Chinese exports in the pre-ali baba era. J. Dev. Econ. 2019, 138, 57–76. [Google Scholar] [CrossRef] [Green Version]

- Fu, J.; Liu, Y.; Chen, R.; Yu, X.; Tang, W. Trade openness, internet finance development and banking sector development in China. Econ. Model. 2020, 91, 670–678. [Google Scholar] [CrossRef]

- Wu, T.-P.; Wu, H.-C.; Liu, S.-B.; Hsueh, H.-P.; Wang, C.-M. Causality between peer-to-peer lending and bank lending in China: Evidence from a panel data approach. Singap. Econ. Rev. 2020, 65, 1537–1557. [Google Scholar] [CrossRef]

- Zhong, W.; Jiang, T. Can internet finance alleviate the exclusiveness of traditional finance? Evidence from Chinese P2P lending markets. Financ. Res. Lett. 2020, 40, 101731. [Google Scholar] [CrossRef]

- Peia, O.; Roszbach, K. Finance and growth: Time series evidence on causality. J. Financ. Stab. 2015, 19, 105–118. [Google Scholar] [CrossRef]

- Hook, S.; Singh, N. Does too much finance harm economic growth? J. Bank. Financ. 2014, 41, 36–44. [Google Scholar] [CrossRef] [Green Version]

- Feng, G.; Jingyi, W.; Zhiyun, C.; Yongguo, L.; Fang, W.; Aiyong, W. The Peking University Digital Financial Inclusion Index of China (2011–2018); Institute of Digital Finance at the Peking University: Beijing, China, 2019; pp. 1–72. [Google Scholar]

- Adeleye, N.; Eboagu, C. Evaluation of ICT development and economic growth in Africa. Netnomics Econ. Res. Electron. Netw. 2019, 20, 31–53. [Google Scholar] [CrossRef]

- Ordanini, A.; Miceli, L.; Pizzetti, M.; Parasuraman, A. Crowd-funding: Transforming customers into investors through innovative service platforms. J. Serv. Manag. 2011, 22, 443–470. [Google Scholar] [CrossRef]

- Laidroo, L.; Koroleva, E.; Kliber, A.; Rupeika-apoga, R. Business models of FinTechs—Difference in similarity? Electron. Commer. Res. Appl. 2021, 46, 101034. [Google Scholar] [CrossRef]

- Levin, A.; Lin, C.F.; Chu, C.S.J. Unit root tests in panel data: Asymptotic and finite-sample properties. J. Econom. 2002, 108, 1–24. [Google Scholar] [CrossRef]

- Solow, R.M. A contribution to the theory of economic growth. Q. J. Econ. 1956, 70, 65–94. [Google Scholar] [CrossRef]

- Peprah, J.A.; Ofori, I.K.; Asomani, A.N. Financial development, remittances and economic growth: A threshold analysis. Cogent. Econ. Financ. 2019, 7, 1625107. [Google Scholar] [CrossRef]

- Baum, C.F.; Schaffer, M.E.; Stillman, S. Instrumental variables and GMM: Estimation and testing. Stata J. 2003, 3, 1–31. [Google Scholar] [CrossRef] [Green Version]

- Dumitrescu, E.I.; Hurlin, C. Testing for Granger non-causality in heterogeneous panels. Econ. Model. 2012, 29, 1450–1460. [Google Scholar] [CrossRef] [Green Version]

- Sepehrdoust, H.; Ghorbanseresht, M. Impact of information and communication technology and financial development on economic growth of OPEC developing economies. Kasetsart J. Soc. Sci. 2019, 40, 546–551. [Google Scholar] [CrossRef]

- Haftu, G.G. Information communications technology and economic growth in Sub-Saharan Africa: A panel data approach. Telecomm. Policy 2019, 43, 88–99. [Google Scholar] [CrossRef]

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Variables | Code | Definition | Unit of Measurement |

|---|---|---|---|

| Economic growth | gdp | GDP per capita | Yuan |

| Fintech | if | Third-party payment, crowdfunding, P2P lending, insurance, blockchain, robotic investment advice, cryptocurrencies, and wealth management | Index |

| Third-party payment | tpp | Third-party payment denotes payment services offered on an unbiased payment platform other than banks that are connected to the bank payment and settlement systems of e-commerce firms and commercial banks [23] | Index |

| Credit | credit | In this study, credit is defined as crowdfunding. Crowdfunding is “a collective effort by consumers who network and pool their money together, usually via the Internet, to invest in and support efforts initiated by other people or organizations” [50] | Index |

| Internet insurance | insu | Internet insurance is the marriage of insurance services (brokerage and underwriting) and technology, and it is often termed as InsurTech [51] | Index |

| Labor force | l | Total employment | Yuan |

| Gross fixed capital formation | k | Investment | Yuan |

| Variables | Obs. | Mean | SD | Min | Max | LLC (0) | LLC (1) |

|---|---|---|---|---|---|---|---|

| lngdp | 217 | 10.740 | 0.463 | 9.706 | 13.405 | −9.585 *** | −11.700 *** |

| lnk | 217 | 9.126 | 0.797 | 6.305 | 10.556 | −7.449 *** | −7.849 *** |

| lnl | 217 | 6.008 | 0.897 | 3.149 | 7.587 | −12.261 *** | −70.036 *** |

| lntpp | 215 | 4.805 | 0.689 | 2.381 | 5.840 | −8.884 *** | −369.629 *** |

| lncredit | 217 | 4.547 | 0.662 | 0.148 | 5.446 | −29.353 *** | −28.144 *** |

| lninsu | 217 | 5.664 | 1.032 | −1.386 | 6.666 | −27.175 *** | −11.194 *** |

| lnif | 217 | 4.973 | 0.678 | 2.786 | 5.819 | −67.984 *** | −16.924 *** |

| Variables | Model 1 | Model 2 | Model 3 | Model 4 | Model 5 | Model 6 | Model 7 | Model 8 | Model 9 | Model 10 | Model 11 | Model 12 |

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| OLS | RE | IV-GMM | ||||||||||

| lnk | 0.120 | 0.116 | 0.153 | 0.084 | 0.253 ** | 0.300 ** | 0.381 *** | 0.177 | 0.123 | 0.079 | 0.256 ** | 0.102 |

| (0.110) | (0.109) | (0.109) | (0.109) | (0.110) | (0.123) | (0.092) | (0.143) | (0.124) | (0.122) | (0.113) | (0.115) | |

| lnl | 0.055 | 0.016 | 0.068 | 0.094 | 0.028 | 0.044 | −0.054 | 0.041 | 0.042 | −0.009 | −0.092 | 0.043 |

| (0.098) | (0.094) | (0.100) | (0.098) | (0.112) | (0.126) | (0.111) | (0.139) | (0.101) | (0.098) | (0.095) | (0.093) | |

| lntpp | 0.245 *** | 0.136 *** | 0.392 *** | |||||||||

| (0.037) | (0.020) | (0.074) | ||||||||||

| lncredit | 0.270 *** | 0.131 *** | 0.495 *** | |||||||||

| (0.066) | (0.043) | (0.091) | ||||||||||

| lninsu | 0.130 *** | 0.066 *** | 1.593 *** | |||||||||

| (0.022) | (0.011) | (0.351) | ||||||||||

| lnif | 0.260 *** | 0.165 *** | 0.792 *** | |||||||||

| (0.038) | (0.026) | (0.121) | ||||||||||

| Constant | 8.140 *** | 8.358 *** | 8.199 *** | 8.114 *** | 7.618 *** | 7.146 *** | 7.211 *** | 8.063 *** | 7.402 *** | 7.786 *** | −0.850 | 5.390 *** |

| (0.411) | (0.414) | (0.404) | (0.387) | (0.508) | (0.484) | (0.390) | (0.492) | (0.547) | (0.542) | (2.118) | (0.613) | |

| R2 | 0.290 | 0.294 | 0.266 | 0.313 | 0.303 | 0.294 | 0.251 | 0.399 | ||||

| R2_w | 0.417 | 0.414 | 0.411 | 0.432 | ||||||||

| R2_o | 0.255 | 0.244 | 0.234 | 0.297 | ||||||||

| R2_b | 0.220 | 0.216 | 0.196 | 0.265 | ||||||||

| Rho | 0.778 | 0.807 | 0.780 | 0.480 | ||||||||

| RMSE | 0.391 | 0.391 | 0.399 | 0.386 | 0.175 | 0.175 | 0.177 | 0.205 | 0.334 | 0.337 | 0.347 | 0.311 |

| F | 43.986 | 33.284 | 50.927 | 54.836 | 32.125 | 21.915 | 27.344 | 43.887 | ||||

| J | 0.024 | 0.016 | 3.375 | 25.005 | ||||||||

| JP | 0.876 | 0.900 | 0.066 | 0.000 | ||||||||

| VIF | 4.49 | 4.88 | 4.78 | 4.92 |

| Variables | Model 1 | Model 2 | Model 3 | Model 4 | Model 5 | Model 6 | Model 7 | Model 8 | Model 9 | Model 10 | Model 11 | Model 12 |

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Eastern Region | Central Region | Western Region | ||||||||||

| lnk | −0.215 | −0.151 | 0.079 | −0.254 * | 0.627 *** | 0.636 *** | 0.688 *** | 0.615 *** | 0.386 *** | 0.330 *** | 0.332 ** | 0.351 *** |

| (0.152) | (0.158) | (0.178) | (0.140) | (0.048) | (0.050) | (0.061) | (0.047) | (0.100) | (0.106) | (0.142) | (0.107) | |

| lnl | 0.337 ** | 0.196 | 0.088 | 0.381 *** | −0.725 *** | −0.726 *** | −0.761 *** | −0.707 *** | −0.275 *** | −0.263 *** | −0.238 ** | −0.257 *** |

| (0.158) | (0.166) | (0.174) | (0.147) | (0.042) | (0.047) | (0.058) | (0.042) | (0.070) | (0.072) | (0.100) | (0.076) | |

| lntpp | 0.492 *** | 0.123 *** | 0.116 | |||||||||

| (0.104) | (0.031) | (0.078) | ||||||||||

| lncredit | 0.843 *** | 0.134 *** | 0.173 ** | |||||||||

| (0.167) | (0.040) | (0.069) | ||||||||||

| lninsu | 1.592 *** | 0.477 * | 0.738 | |||||||||

| (0.502) | (0.248) | (0.537) | ||||||||||

| lnif | 0.941 *** | 0.188 *** | 0.309 ** | |||||||||

| (0.178) | (0.061) | (0.140) | ||||||||||

| Constant | 8.384 *** | 7.109 *** | −0.211 | 5.958 *** | 8.665 *** | 8.585 *** | 6.017 *** | 8.298 *** | 8.085 *** | 8.312 *** | 4.414 | 7.244 *** |

| (0.717) | (0.926) | (3.487) | (1.071) | (0.317) | (0.337) | (1.650) | (0.373) | (0.524) | (0.439) | (2.788) | (0.614) | |

| R2 | 0.362 | 0.321 | 0.270 | 0.426 | 0.824 | 0.812 | 0.760 | 0.831 | 0.304 | 0.342 | 0.314 | 0.388 |

| RMSE | 0.311 | 0.321 | 0.333 | 0.295 | 0.092 | 0.096 | 0.108 | 0.091 | 0.205 | 0.200 | 0.204 | 0.192 |

| F | 11.488 | 13.486 | 6.751 | 16.855 | 99.807 | 75.986 | 55.069 | 94.256 | 9.038 | 11.389 | 8.589 | 10.747 |

| J | 1.238 | 0.024 | 6.496 | 11.614 | 1.541 | 0.012 | 3.461 | 3.866 | 0.465 | 0.016 | 0.006 | 1.352 |

| JP | 0.266 | 0.877 | 0.011 | 0.001 | 0.214 | 0.914 | 0.063 | 0.049 | 0.495 | 0.899 | 0.939 | 0.245 |

| Variables | Model 1 | Model 2 | Model 3 | Model 4 | Model 5 | Model 6 | Model 7 | Model 8 | Model 9 | Model 10 | Model 11 | Model 12 |

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| OLS | RE | IV-GMM | ||||||||||

| lnk | 0.029 | 0.020 | 0.027 | 0.014 | 0.040 * | 0.040 * | 0.053 *** | 0.026 | 0.031 | 0.017 | 0.050 * | 0.021 |

| (0.022) | (0.024) | (0.024) | (0.023) | (0.022) | (0.024) | (0.019) | (0.021) | (0.026) | (0.027) | (0.027) | (0.027) | |

| lnl | −0.377 *** | −0.384 *** | −0.373 *** | −0.369 *** | −0.312 *** | −0.297 *** | −0.332 *** | −0.330 *** | −0.372 *** | −0.381 *** | −0.399 *** | −0.372 *** |

| (0.020) | (0.020) | (0.021) | (0.020) | (0.046) | (0.048) | (0.049) | (0.045) | (0.022) | (0.021) | (0.023) | (0.021) | |

| lntpp | 0.051 *** | 0.023 *** | 0.081 *** | |||||||||

| (0.011) | (0.004) | (0.019) | ||||||||||

| lncredit | 0.055 *** | 0.023 *** | 0.086 *** | |||||||||

| (0.016) | (0.007) | (0.026) | ||||||||||

| lninsu | 0.027 *** | 0.014 *** | 0.324 *** | |||||||||

| (0.007) | (0.003) | (0.102) | ||||||||||

| lnif | 0.052 *** | 0.028 *** | 0.137 *** | |||||||||

| (0.012) | (0.004) | (0.037) | ||||||||||

| Constant | 3.584 *** | 3.714 *** | 3.679 *** | 3.665 *** | 3.237 *** | 3.149 *** | 3.265 *** | 3.440 *** | 3.378 *** | 3.574 *** | 1.788 *** | 3.160 *** |

| (0.144) | (0.147) | (0.145) | (0.152) | (0.260) | (0.312) | (0.317) | (0.291) | (0.177) | (0.191) | (0.659) | (0.245) | |

| R2 | 0.897 | 0.900 | 0.898 | 0.901 | 0.909 | 0.910 | 0.909 | 0.915 | ||||

| R2_w | 0.294 | 0.320 | 0.288 | 0.295 | ||||||||

| R2_o | 0.895 | 0.898 | 0.896 | 0.900 | ||||||||

| R2_b | 0.906 | 0.905 | 0.903 | 0.906 | ||||||||

| Rho | 0.925 | 0.932 | 0.931 | 0.903 | ||||||||

| RMSE | 0.103 | 0.106 | 0.107 | 0.105 | 0.029 | 0.030 | 0.030 | 0.030 | 0.094 | 0.098 | 0.099 | 0.096 |

| F | 247.071 | 268.224 | 256.077 | 280.100 | 192.891 | 225.434 | 230.168 | 229.000 | ||||

| J | 1.766 | 0.013 | 0.050 | 7.066 | ||||||||

| JP | 0.184 | 0.908 | 0.824 | 0.008 | ||||||||

| VIF | 4.49 | 4.88 | 4.78 | 4.92 |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2022 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Song, N.; Appiah-Otoo, I. The Impact of Fintech on Economic Growth: Evidence from China. Sustainability 2022, 14, 6211. https://doi.org/10.3390/su14106211

Song N, Appiah-Otoo I. The Impact of Fintech on Economic Growth: Evidence from China. Sustainability. 2022; 14(10):6211. https://doi.org/10.3390/su14106211

Chicago/Turabian StyleSong, Na, and Isaac Appiah-Otoo. 2022. "The Impact of Fintech on Economic Growth: Evidence from China" Sustainability 14, no. 10: 6211. https://doi.org/10.3390/su14106211

APA StyleSong, N., & Appiah-Otoo, I. (2022). The Impact of Fintech on Economic Growth: Evidence from China. Sustainability, 14(10), 6211. https://doi.org/10.3390/su14106211