1. Introduction

The concept of infrastructure-led (regional) development was first proposed in 2007, but, in fact, transport infrastructure has been a central topic in the study of national/regional development among economists and geographers for a long time, which includes an extensive part of transport infrastructure-led development research [

1]. Encouraged by rapid economic development, which coincided with the historical period of infrastructure construction in Western Europe, Japan, and the United States, research on transport infrastructure-led development path/model has continued to accumulate, especially in the context of the well-recognized experience of the “China miracle” [

2,

3,

4]. Theories and assumptions have proliferated regarding accessibility and mobility, trade facilitation, agglomeration and specialization effects, spillover effects, technological innovation, risk assessment, financing patterns, and policy-making, etc. [

5,

6,

7,

8,

9]. Among these, economic return and the effect of transport infrastructure on development have drawn scholars’ attention.

Moreover, there are few signs of abating of the booming range of development programs and initiatives relying heavily on transport infrastructure, influenced by the belief in the infrastructure-led development path/model—in both the Global North and Global South, nationally or across borders—to promote development and foster convergence. Some illustrative examples include the Program for Infrastructure Development in Africa, the Lamu Port-South Sudan-Ethiopia Transport Corridor, the Abidjan-Lagos Transport Corridor Project, the New International Land-Sea Trade Corridor between Chongqing and Singapore, and China’s Belt and Road Initiative (BRI). International organizations are also enthusiastic about such a development model. For example, in 2018, the Asian Infrastructure Investment Bank (AIIB) released a transport sector strategy focusing on sustainable transport projects, and priority was given to trunk linkages and cross-border connectivity projects that will promote transport integration and the upgrading of existing transport infrastructure [

10]. The Connecting Europe Facility, a funding instrument established by the European Union with a total budget of EUR 24.05 billion for transport in 2014—2020, also focuses on cross-border projects to strengthen connections on the European continent and other projects aimed at removing bottlenecks, such as upgrading the railways and modernizing the port infrastructure, and puts more emphasis on the sustainable development of transport [

11].

Recently, however, some practices have encountered difficulty in achieving sustainable development in many countries, especially in developing countries and emerging economies, which are “trapped” by large scale development of transport infrastructures. Although there has been a variety of perspectives and knowledge to understand transport infrastructure-led development, they fail to explain the failure, and further studies are needed. Thus, there is a call for rethinking the transport infrastructure-led development model, in particular its conditions of sustainability.

The complexity of transport infrastructure has been increasing as more and more practical projects involve larger spatial ranges (across national borders) [

12]. Moreover, transport infrastructures are semi-public goods, which is significantly different from pure public goods. In many areas of infrastructures and in many countries, there is a tradition of “user pays”, which creates various ways of private participation in infrastructure development based largely on the market mechanism but with government subsidies, e.g., the popular public–private-partnership (PPP) model [

13]. This indicates that the financing sources and structures of infrastructure development are becoming more and more diversified. These practices and transitions open up an interesting area of geographic study. From the standpoint of economic geographers, the sustainability of transport infrastructure is a precondition for subsequent development, and it requires sophisticated interactive processes between financing patterns and development benefits to be achieved. The well-documented economic and broader impacts of transport infrastructure on development can be recognized only through an integrated approach that seeks to consciously manage the process, in which not only the development benefits but also the constraints of financing patterns are emphasized.

Therefore, this paper attempts to reveal the precondition for the transport infrastructure-led development model by focusing on the sustainability of transport infrastructure itself, i.e., to understand what kind of development benefits can be achieved under different degrees of financing constraints. The structure of the paper is as follows.

Section 2 presents a brief review of the existing literature on transport infrastructure-led development with a particular emphasis on the preconditions, then puts forward our theoretical framework.

Section 3 introduces the specific characteristics of diversified financing structures. To improve our understanding of the constraints of financing patterns, the trade-offs involved in both cash-back by user payments and long-term development of transport infrastructure are interpreted in

Section 4. Further discussion is provided at the end.

2. Literature Review and Theoretical Framework

Current studies are mainly focused on the benefits produced by transport infrastructure for development, that is, the mechanism of transport infrastructure-led development model, including immediate socioeconomic effects, economic growth, and long-term spillover effects. The immediate socioeconomic effects originate from the essential feature of transport infrastructure as a production sector in a particular form [

14]. Apart from its own production benefits, transport infrastructure facilitates the development of upstream production sectors and those sectors that take the former as intermediate products due to its extremely close relationship with various social and economic sectors [

15]. In addition, transport infrastructure produces socioeconomic benefits by creating jobs, reducing poverty, and improving socioeconomic conditions [

16].

In fact, transport infrastructures are semi-public goods, with “externality” playing an integral role in creating indirect long-term impacts on economic development, which is referred to as wider economic benefits or impacts [

17,

18]. There are two main aspects of the theoretical and empirical findings in this regard. One is the identification of multiple mechanisms with economic and geographic theories to link transport infrastructure and economic growth. For instance, transport infrastructure creates indirect positive externalities and smooths the business cycle by reducing production and transport costs and increasing the productivity of input factors [

19,

20]. Meanwhile, it is widely and typically acknowledged that transport infrastructure fundamentally improves accessibility, which causes a series of economic impacts [

21,

22,

23]. Specifically, it provides the necessary conditions for the agglomeration and diffusion of a spatial economy (transport-induced agglomeration effects) and makes agglomerations or large spatial clusters possible; hence, a variety of agglomeration economies and endogenous growth effects follow, thereby augmenting the economic effects of transport infrastructure [

14,

24,

25].

The other aspect has to do with the long-term spillover effects, which refer to economic, technical, knowledge growth, and other effects within and across regions as the impacts of transport infrastructure increase [

7,

26]. It is well documented that transport infrastructure can facilitate local and foreign investments and materialize in new capital formation, thus spurring economic activities through its impact on the private sector and can significantly raise land prices in and around the hinterland, which is difficult to quantify but profound [

25].

The benefits mentioned above mainly reflect improvement after transport infrastructure is implemented. Notice that cash-back by user payments is another representation of benefits, as it is both a manifestation of satisfied demand, considering that a shortage of transport infrastructure would limit economic development, and an improvement of long-term development potential [

14]. However, failures occur where transport infrastructure does not achieve expectations, even though there may be some benefits. With regard to this concern, some authors argue that transport infrastructure can generate sufficient returns to repay the associated debt, interest, and fees with the rise of neoliberalism [

27,

28]. If projects do not yield sufficient “flow” of income, not only does the follow-up construction, updating, and upgrading suffer from a dilemma but also the confidence and trust among investors may collapse [

29], such that a more detrimental boomerang effect may occur: the accumulation of non-performing loans increases the national debt risk [

30].

Moreover, the complexity of transport infrastructure has varied and has evolved immensely with respect to ownership, financing, regulation, and use rights as its spatial range has widened and the participants have become more diversified [

12,

18,

31]. Studies have noted that sustainability is fundamental to settle failed practices, or in other words, transport infrastructure should aim for self-sustained growth to contribute to the attainment of transport infrastructure-led development. In fact, complicated financing is significantly involved in sustainability as well, while generally, research on transport infrastructure-led development only considers benefits. Therefore, we argue that the sustainability of transport infrastructure requires that development benefits respond to the different constraints of financing patterns, or in other words, a trade-off is needed by which transport infrastructure as semi-public goods both generates cash-back by user payments and achieves long-term development to adapt to the financing constraints.

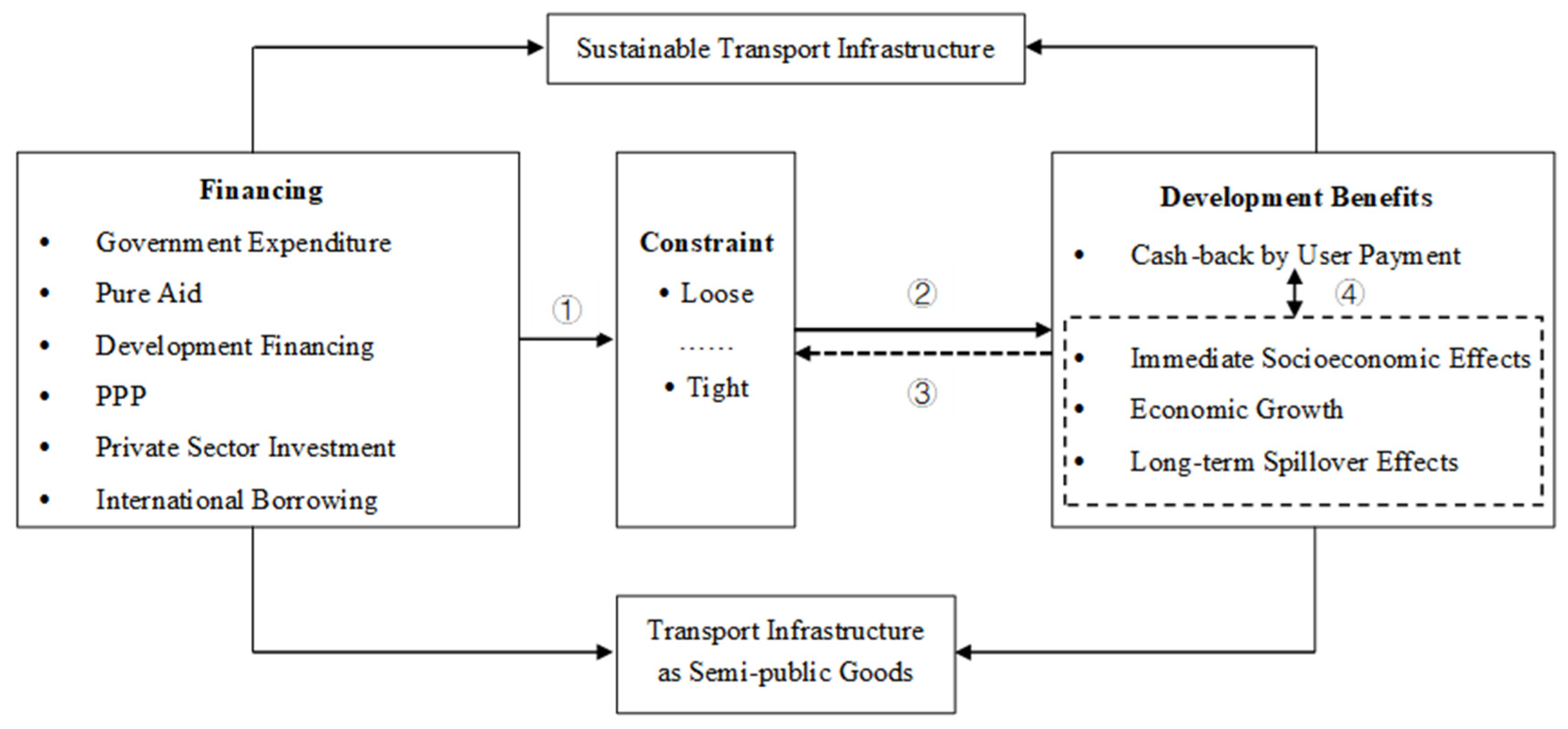

The above discussion is summarized and illustrated in

Figure 1. We contest that financing structure and the delivery of development benefits are two major factors in realizing sustainable transport infrastructure given transport infrastructures are semi-public goods. On the one hand, financing varies from a single tool such as government expenditure to combined patterns involving pure aid, development financing, PPP, private sector investment, and international borrowing as building infrastructures, as semi-public goods offer opportunities for the private sector and third parties. Correspondingly, different participants concentrate on different development benefits, including socioeconomic growth and long-term spillover effects as well as cash-back. One the other hand, it has been widely discussed that in order to realize sustainable development of transport infrastructure, appropriate financing and development benefits are required. Here, we highlight the trade-off between cash-back in the short term and other socioeconomic effects in the relatively longer term and argue that the trade-off has a lot to do with to the constraints from financing patterns. Thus, our purpose is to clarify how the constraint ranges from loose to tight, how development benefits are traded off, and how the impacts and responses are delivered.

3. Financing Pattern: Sources and Characteristics

Considering transport infrastructures as semi-public goods, their financing can come from both the public and private sources, and different financing patterns have different meanings [

32]. Public sources mainly consist of central and local government expenditure and bilateral and multilateral development finance institutions (DFIs), while private sources consist of corporate financing and project financing, with the PPP mode as an example (PPP is not emphasized as a financing method, although it can assume the financing function in many cases, and is discussed as a component of financing patterns in this paper). Notwithstanding the Basel III Accord, adopted after the global financial crisis in 2008, imposing more stringent requirements on the banking system and restrictions on the provision of project financing, bank loans are still the main source of funds for infrastructure. In developing countries, some projects are inclined to seek international borrowing as a result of the difficulty in borrowing from domestic banks and the lack of a bond market and institutional investors interested in transport infrastructure. To specify the intricate financing patterns in practice, the different sources and their characteristics are described here.

Government expenditure has traditionally been the main funding source for transport infrastructure [

33]. From the Second World War to the early 1980s, transport infrastructure planning and investment were primarily undertaken by governments, which also assumed the risks [

34]. Although high public debt and budget deficits as well as government expenditure may not continue in many countries, these governments keep supporting transport infrastructure with national infrastructure funds or bonds with long maturity in local currency, which encounters lower foreign currency risks and minimizes maturity mismatches [

33].

Under conditions of fiscal constraint and indebtedness, DFIs such as national policy banks, multilateral development banks, and bilateral agencies support the needs of transport infrastructure investment and fill the financing gaps by mobilizing long-term funds through capital markets, explicit guarantees, and special co-financing arrangements involving the World Bank, Asian Development Bank (ADB), AIIB, Agence Francaise de Développment (AFD), Kreditanstalt für Wiederaufbau (KfW), Japan Bank for International Cooperation, and Japan International Cooperation Agency. As most development financing in the form of loans reflects the expected economic returns on investments, concerns arise about the sustainability of transport infrastructure.

In the late 1990s, the World Bank advocated the application of commercial operation principles against the background of state-led infrastructure investment and construction [

35]. Meanwhile, the unrest of the stock market has promoted the global infrastructure investment market, and the use of the private sector has gradually become prevalent, directly or indirectly (e.g., purchasing bonds) [

36,

37,

38]. Globally, private sector investment accounts for 61% of the total investment in transport infrastructure in high-income countries and 44% in low-to-middle-income countries [

39]. Private capital remarkably flows into transport infrastructure as PPP increases significantly.

PPP projects can be conducted through various modalities, given that they lie between traditional public sector-led investment and the complete privatization of infrastructure. According to the World Bank’s most recent report, transport infrastructure projects comprise the largest recipient of PPP project investment (at USD 14.4 billion across 40 projects), accounting for 40% of global PPI investments in the first half of 2021 [

40]. Fundamentally, PPP, as a kind of project financing, takes future income and project assets as the source of funds to repay a loan, which indicates a preference for satisfactory performance of projects. While PPPs are diversified among transport infrastructure projects, they have advantages in common, including reasonable risk allocation in early stages of the project, reducing financing difficulty as the government also shares some risk, compensating private capital to some extent, and reducing the financial burden [

41]. It is undeniable that many developing countries encounter challenges in engaging with the private sector when applying PPP mode, such as laws prohibiting foreign involvement in or private operation of government-owned assets, as well as misaligned incentives and risks among public, private, and other entities [

39].

The financing of specific transport infrastructure is actually a combination of the above methods because of the enormous fund demand, which brings about various constraints under different financing patterns and characteristics. Particularly in developing countries, international borrowing has become indispensable in the era of overseas investment and probably imposes tighter constraints [

42].

The financing patterns in practical projects can be explained as follows. In

Table 1, we provide financing information of four typical transport infrastructure projects to illustrate how financing constraints range from tight to loose. They are Mombasa–Nairobi Standard-Gauge Railway (MNSGR), Pakistan National Motorway M-4, Jakarta–Bandung High-Speed Railway (JBHSR), and China–Laos Railway (CLR). In the MNSGR project, 90% of the total investment came from borrowing from the Export–Import Bank of China with a mixture of concessional loans and commercial loans, while the remaining 10% was funded by the Kenyan government expenditure [

43]. The two sides have reached a consensus that the debt could be repaid by export concessions and self-operated loans, which gives slight elasticity to the relatively tight constraint. As for the M-4 project, the financing involved AIIB (36.6%), ADB (36.6%), the Department for International Development of China (12.5%), and the Pakistani government (14.3%) in the form of sovereign loans and appropriations [

41]. A large proportion of borrowing from international institutions imposes a high financing constraint on the Pakistani government.

JBHSR is carried out by PT Kereta Cepat Indonesia China (KCIC) (KCIC is composed of five Chinese and four Indonesian companies. The Chinese Enterprise Consortium, led by China State Railway Group Co., Ltd., comprises CRIC, China Railway Group Limited, SINOHYDRO Corporation Limited, CRRC Corpo-ration Limited, and China Railway Signal and Communication Co., Ltd. The Indonesian Enterprise Consortium is led by PT. Wijaya Karya (Persero) Tbk and also comprises PT. Kereta Api Indonesia, PT. Jasa Marga (Persero) Tbk, and PT. Perkebunan Nusantara VIII), a joint venture consortium by Chinese and Indonesian enterprises in the build–operate–transfer (BOT) mode, which has a long practical history in infrastructure construction such as expressways, power plants, ports, and wharfs. In the BOT mode, the responsibility for guaranteeing investment and financing for construction and operation has been conveyed from the Indonesian government to KCIC, which was granted a 50-year franchised operation. The financing was mainly realized through loans from the China Development Bank without the Indonesian government budget. KCIC undertook the remaining 25% of the investment, of which the Chinese and Indonesian consortia account for 40 and 60%, respectively [

44].

In fact, the PPP mode, with its unique advantages, has gradually become the preferred choice for the investment and financing of large-scale transport infrastructure projects. Similar to BOT, PPP is also provided by franchises from the government, but it makes up for BOT’s shortcomings of a long return period and political risk from changing policies [

41]. Specifically, a concession contract would be signed by the government department and the special purpose company (SPC) (SPC is generally a limited company composed of the bid-winning construction company and a service operation company or a third party investing in the project); the government also participates and undertakes risks, though it is the SPC that is responsible for financing, construction, and operation. The income from the project would be used to repay the loan, the bond, and other financing instruments and their interest. Taking the CLR as an example, the SPC (China–Laos Railway Co., Ltd., is 30% owned by the Laos State Railway Co., Ltd., on behalf of the Laotian government, while the remaining 70% is owned by Boten-Vientiane Railway Co., Ltd., (40%), Yukun Investment Co., Ltd., (20%), and the Peo-ple’s Government of Yunnan Province (10%)) as debtor transacted loans from the Export–Import Bank of China (60%), while the capital base accounts for the other 40%, of which 30% was provided by the Laotian government in the form of budget and sovereign loans from the Export–Import Bank of China. The former loan was assigned with a 25-year repayment period and a 5-year grace period, while the latter loan was assigned with a 20-year repayment period and a 5-year grace period [

44].

With the BOT and PPP modes in use, related enterprises and governments share both benefits and risks, which means that an accordant focus on the expected economic returns on investments encourages them to coordinate the development benefits via policy and other implementation to bring higher elasticity to financing constraints and thus facilitate the sustainability of transport infrastructure.

4. Dynamics of Financing Pattern Constraints and Development Benefit Responses

A trade-off in development benefits in relation to financing constraints is essential for the sustainability of transport infrastructure and achieving transport infrastructure-led development. Beyond proposing, it is necessary to provide a specific demonstration of the dynamics of responses to constraints. As indicated in the previous section, the financing pattern is characterized by involving diverse sources with a generally accepted recovery period related to the goal preference for further pursuit of corresponding development benefits. Thus, the issue arises that various conditions of the financing pattern impose constraints of different degrees on the benefit expectations, while the benefits attained evolve and the impacts of constraints fluctuate such that the trade-off can be approached by implementing development in response to the constraints and/or reconciling the constraints into appropriate forms.

Government expenditure, development financing, and pure aid are the predominant categories of financing, which obviously favor obtaining long-term benefits. Traditionally, government expenditure has been emphasized when promoting national safety and network coverage and building new capacity to meet the ever-rising demand for development by providing and maintaining public works such as transport infrastructure, which has occurred since Keynesianism [

18]. Evidently, long-term preference is implied in the prosperous anticipation of national development. Development financing embodies the will of the government with national credit, as it is conventionally owned and empowered to operate by the government and is mainly used for development. Pure aid indicates economic and political diplomacy, generally focusing on long-term prospects. Consequently, these types of financing have fewer constraints and offer the possibility to focus on a broader set of benefits associated with transport infrastructure, although they are difficult to quantify, thus making economic and social accumulation more feasible throughout their long duration. However, there are disadvantages of the financial gap for the illustrative example of China before the reform and opening up, when government expenditure contributed the most to transport infrastructure. Hence, attention should also be drawn to the fact that a trade-off is needed between cash-back and long-term development under a relatively loose constraint to overcome the potential lackluster economic performance.

Comparatively, with private sector investments, cash-back by user payments is preferred. Inherently, the pursuit of capital wielded by discerning private sector entities is a relatively definite and stable return, and transport infrastructure is increasingly seen as an asset that provides income-oriented investment returns [

45]. In terms of international borrowing, it is because the availability of funds in the immediate term is sufficient to meet the demand for fixed repayment terms and to avoid adverse outcomes (e.g., repayment of debt is repeatedly postponed so that all of the cost falls on future generations, which implies unsustainability) that international borrowing is attracted by the financial performance of reliable return on investment. When capital from the private sector and international borrowing prevail in the financing pattern, the cash-back feature should remain persuasive for a sufficiently long period so that the investment will be considered fairly remunerated.

Between the former two categories of financing is PPP, with a hybrid nature as a growing strategic approach for sustainable financing, which apparently integrates wide-ranging sources according to the characteristics of specific transport infrastructure. Correspondingly, if cash-back by user payments is persuasive, the initial impact exerted by the constraints is gradually alleviated and the priority of long-term benefits makes itself clear, considering the continuous dominant role of government as an integral actor in transport infrastructure [

45,

46]. As a matter of fact, PPP is complicated in practical cases because of both the diverse incorporated participants and the various domestic and foreign funds, especially when overseas projects are involved.

Two cases are presented here for a brief explanation: the well-acknowledged development of China in terms of transport infrastructure, and the Addis Ababa–Djibouti railway re-development through trade-off after debt default. In China, the degree of constraints has increased since the reform and opening up due to the fact that available financing for transport infrastructure was diversified beyond government expenditure, such as developing financing from the World Bank, private sector, international borrowing, etc. The Chinese government has taken measures to increase cash-back as a stable source of funding through market-oriented reform by raising the standard of road use charges, levying vehicle purchase surcharges, and implementing road construction with loans and repayment with fees (“

dai kuan xiu lu, shou fei huan dai”). Another part of the measures addresses the “rail + property” mode by which the government compensates the construction expenditure of the project through the land value increment brought by the rail. In the case of financing the Addis Ababa–Djibouti railway, international borrowing from the Export–Import Bank of China has a 70% share of the funds in the Ethiopia section and 85% in the Djibouti section. Given that previous debt default has happened, the development mode of “railway + industrial park” has been carried out to deliver the spillover effect via scale economy owing to the complementarity between transport infrastructure and industrial parks [

47]. Both of these cases demonstrate trade-off and prove the significance in which the climbing of cash-back and the efforts on the spillover effect stimulate development and help to moderate the constraints.

The aforementioned cases indicate that trade-off shapes a delicate balance to alleviate the impact of the constraints and to bring about sustainable development by conducting development implementations and/or reconciling constraints to an appropriate degree. In conclusion, it is significant to have trade-off but complicated to integrate cash-back and benefits in the long term because constraints of the appropriate degree from the expected financing pattern might not be easily available, and measures for securing the benefit of responding to constraints would also face obstacles considering the practical status of transport infrastructure projects. If government expenditure and/or development financing dominate, there remains a relative higher possibility of long-term development benefits. On the contrary, if the private sector and/or international borrowing account for a greater share, development benefits would be expected to be attained in the immediate term under tight constraints. However, neither one of these, the other side of cash-back or long-term benefit, should be overlooked. As far as PPP is concerned, the relationship between the public and private sectors involves complicated coordination involving the former two processes. Hence, it is essential to adopt instruments to attain a trade-off once those elements are considered together.

5. Conclusions and Discussion

While many existing studies have argued for the transport infrastructure-led development model from a long-term perspective and some development practices have provided evidence for such a model, many transport infrastructure projects failed to sustain and deliver greater development benefits due to the constrains put by financing patterns or poor financial performance. As such, controversies and concerns have been raised about the recovery of enormous capital in these financing projects, especially regarding increased foreign funds and subsequent debt risk. Obviously, there are binary and isolated perspectives regarding the model, i.e., one focusing on long-term benefits and the other on cash-back in the short term. To narrow the gap, one must figure out how to ensure cash-back in the short term from the perspective of attaining long-term development benefits and how to make the transport infrastructure project evolve into real economic development. By introducing the analytical framework on sustainable transport infrastructure with attention on the constraints of financing patterns, this paper has tried to combine the binary perspectives on the transport infrastructure-led development model.

In doing so, we offer a more generalized perspective on the transport infrastructure-led development model: We suggest that a trade-off between short- and long-term benefits is significant; that is, transport infrastructure-led development can be achieved only if the financial sustainability of transport infrastructure projects is ensured by balancing the cash-back and long-term benefits and by manipulating tight and loose constraints from different financing patterns. As we repeatedly emphasized, the expected recovery period of financing is related to the preference for expected development benefits, while the coordination of benefits also demands sophisticated consideration of the financing pattern.

In current practices, large amounts of funds in the form of various types of loans (e.g., preferential loans and commercial loans) have poured from creditors of other sovereign governments and important multilateral financial institutions into transport infrastructure investment and construction, in which governments and/or the private sector have probably played a role as debtors [

48]. Considering the demand for fulfilment, domestic loans can achieve responses through various financial instruments (e.g., monetization of government debt combined with fiscal policy and monetary policy) to alleviate the impact of constraints while the means to repay foreign loans are limited [

49]. It can be recognized that financing from foreign capital tends to impose a tight constraint compared with the loose constraint on transport infrastructure by domestic capital investment. With regard to the loose constraint, its elasticity is also limited despite domestic efforts to adapt, given that possible financial collapses could occur if it is exceeded. As for the tight constraint, failure might lead not only to direct losses of debt default and credit crisis but also to the domino effect, endangering many fields.

Moreover, it is fundamental to understand the trade-off for sustainable transport infrastructure, considering that complexity evolves in the responses of trade-off benefits to financing constraints and in the decision-making process, impacted by the context when integrating different financing. The responses, together with the development outcomes (positive or negative), actually form an intricately dynamic process regarding the uncertainty in approaching development benefits, which is analyzed as static in this paper but needs to be explained further. Moreover, the decision-making process of the financing pattern is also complicated, entangled with related policies, which impacts the feasibility of trade-offs. To sum up, there is a prospective domain in transport infrastructure-led development awaiting research to understand the sustainability of transport infrastructure, especially trade-offs under constraints, and to guide practice.

{kind=link}