A Systematic Literature Review on Sustainability in Family Firms

Abstract

1. Introduction

2. Sustainability

3. Family Firms

3.1. Family Firms and Sustainability

3.2. Socio Emotional Wealth (SEW) Theory

3.3. Corporate Social Responsibility

3.4. Stakeholder Theory

3.5. Resource-Based View (RBV)

3.6. Stewardship Theory

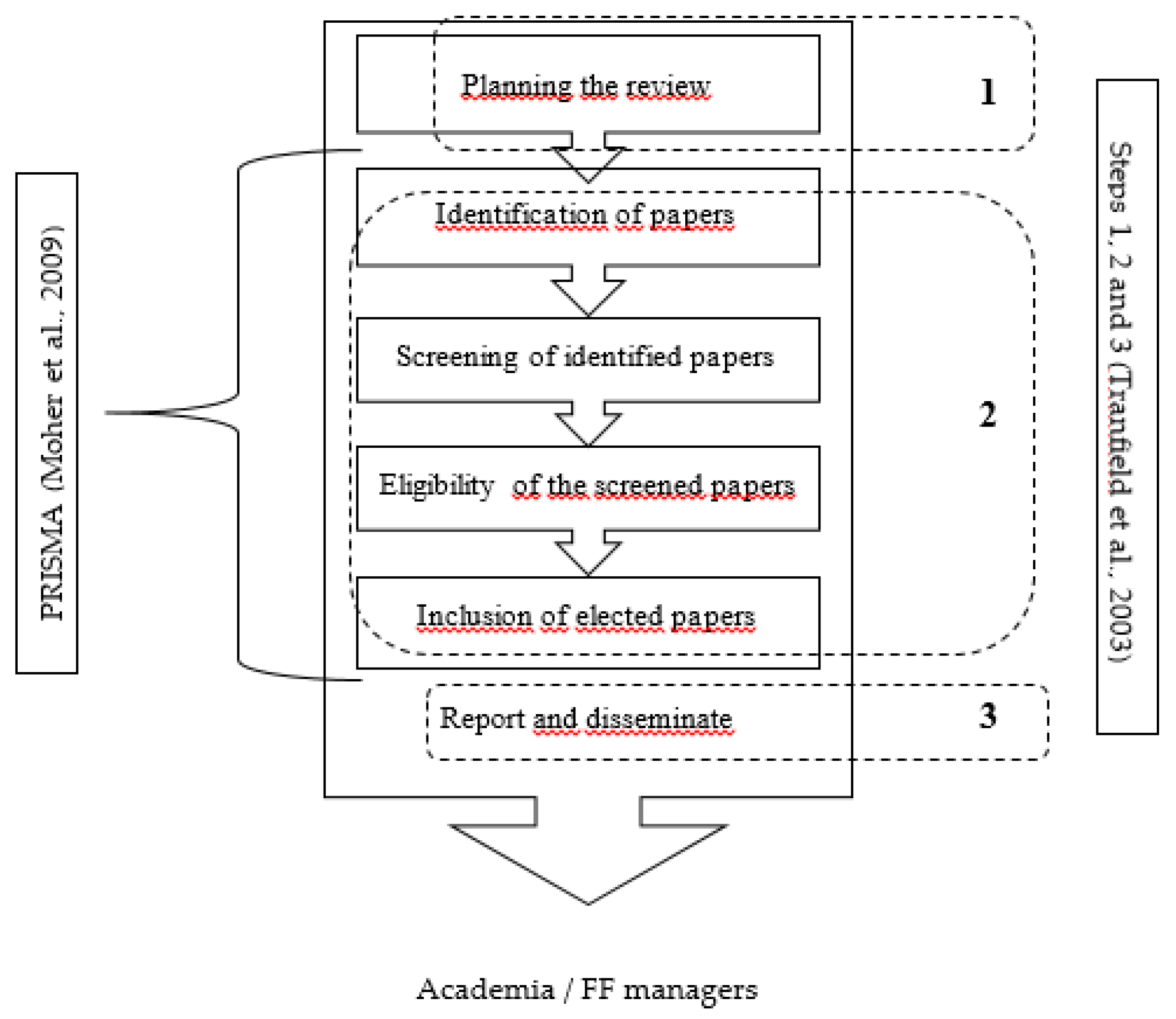

4. Methods

Data Collection

5. Analysis and Results

6. Discussion

- FFs share more CSR reports than NFFs [7].

- The effect of CSR is greater among FFs than among NFFs [49].

- The more the family manager is committed to the FF, the more easily the objectives of the firm are met vis-à-vis a balance between internal (employees) and external (customers and community) stakeholders’ interests [52].

- FFs that have a family CEO tend to choose an internal CEO as their successor [53].

- FFs that have a relevant level of external (to the family) shareholders tend to choose an external CEO [53].

- The adequate succession of the CEO is essential for the sustainability of FFs [53].

- Family ties are essential in passing on knowledge to maintain the relationships with stakeholders, while the utilitarian power of the family weakens the relationship the FF has with unfamiliar stakeholders [52].

- The market pressures FFs to promote sustainable development. As a result, FFs face crises by innovating and adapting through sustainability and survival strategies [56].

- If the family control over the FF is too strong, it does not promote CSR practices [51].

- CSR practices vary depending on the FF’s industry [58].

7. Conclusions

Limitations and Future Research

- Problems in the sample—being too small, addressing only a singular cultural context or a single country, and simply addressing SMEs and focusing on a single industry. Studies should expand the sample sizes across several regional settings, industries, and FF sizes;

- Issues related to data—incomplete or lower-quality secondary data sources and having a single correspondent per FF. Future work should involve more complete databases and high quality data that could require strong and reliable partnerships with industrial associations, governmental entities, and policymakers. Enlarging the number of participants per FF would generate richer databases and the possibility of developing studies using employer–employees or supervisor–subordinate matched samples;

- Quality of findings—most of the results cannot be generalized due to methodological limitations and less accurate answers and testimonies from the studies’ participants due to the sensitive topic. Upcoming research should guarantee the methodological approach and quality of data to ensure the generalized power of results, and thus directly contribute to further theoretical developments on sustainability in the context of FFs.

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Acknowledgments

Conflicts of Interest

Appendix A

{kind=link}

| Paper ID | Papers–References | Citations |

|---|---|---|

| PP3 | Altindag, E.; Tanriverdi, H.; Cakmak, C. The Relationship of Organizational Culture and Wage Policies in Turkish Family Firms. Bus. Manag. Dynamics 2016, 5, 1–16. | 8 |

| PP7 | Ardito, L.; Messeni Petruzzelli, A.; Pascucci, F.; Peruffo, E. Inter-Firm R&D Collaborations and Green Innovation Value: The Role of Family Firms’ Involvement and the Moderating Effects of Proximity Dimensions. Bus. Strat. Environ. 2019, 28, 185–197, doi:10.1002/bse.2248. | 44 |

| PP6 | Arena, C.; Michelon, G. A Matter of Control or Identity? Family Firms’ Environmental Reporting Decisions along the Corporate Life Cycle. Bus. Strat. Environ. 2018, 27, 1596–1608, doi:10.1002/bse.2225. | 6 |

| PP57 | Broccardo, L.; Zicari, A. Sustainability as a Driver for Value Creation: A Business Model Analysis of Small and Medium Entreprises in the Italian Wine Sector. J. Cleaner Prod. 2020, 259, 120852, doi:10.1016/j.jclepro.2020.120852. | 0 |

| PP8 | Campopiano, G.; De Massis, A. Corporate Social Responsibility Reporting: A Content Analysis in Family and Non-Family Firms. J. Bus. Ethics 2015, 129, 511–534, doi:10.1007/s10551-014-2174-z. | 260 |

| PP49 | Chou, S.Y.; Chang, T.; Han, B. A Buddhist Application of Corporate Social Responsibility: Qualitative Evidence from a Case Study of a Small Thai Family Business. Small Enter. Res. 2016, 23, 116–134, doi:10.1080/13215906.2016.1221359. | 7 |

| PP60 | Cunha, C.; Kastenholz, E.; Carneiro, M.J. Entrepreneurs in Rural Tourism: Do Lifestyle Motivations Contribute to Management Practices That Enhance Sustainable Entrepreneurial Ecosystems? J. Hospit. Tourism Manag. 2020, 44, 215–226, doi:10.1016/j.jhtm.2020.06.007. | 7 |

| PP11 | Dayan, M.; Ng, P.Y.; Ndubisi, N.O. Mindfulness, Socioemotional Wealth, and Environmental Strategy of Family Businesses. Bus. Strat. Environ. 2019, 28, 466–481, doi:10.1002/bse.2222. | 14 |

| PP10 | de la Cruz Déniz-Déniz, M.; Cabrera-Suárez, M.K.; Martín-Santana, J.D. Family Firms and the Interests of Non-Family Stakeholders: The Influence of Family Managers’ Affective Commitment and Family Salience in Terms of Power. Bus. Ethics A Eur. Rev. 2018, 27, 15–28, doi:10.1111/beer.12155. | 12 |

| PP1 | de la Cruz Déniz-Déniz, M.; Cabrera-Suárez, M.K.; Martín-Santana, J.D. Orientation Toward Key Non-Family Stakeholders and Economic Performance in Family Firms: The Role of Family Identification with the Firm. J. Bus. Ethics 2020, 163, 329–345, doi:10.1007/s10551-018-4038-4. | 5 |

| PP4 | Dieleman, M.; Koning, J. Articulating Values Through Identity Work: Advancing Family Business Ethics Research. J. Bus. Ethics 2020, 163, 675–687, doi:10.1007/s10551-019-04380-9. | 4 |

| PP45 | Duarte Alonso, A.; Kok, S.; O’Shea, M. Family Businesses and Adaptation: A Dynamic Capabilities Approach. J. Fam. Econ. Issues 2018, 39, 683–698, doi:10.1007/s10834-018-9586-3. | 13 |

| PP17 | Engeset, A.B. “For Better or for Worse”—The Role of Family Ownership in the Resilience of Rural Hospitality Firms. Scand. J. Hospit. Tour. 2020, 20, 68–84, doi:10.1080/15022250.2020.1717600. | 3 |

| PP43 | Konopaski, M.; Jack, S.; Hamilton, E. How Family Business Members Learn About Continuity. AMLE 2015, 14, 347–364, doi:10.5465/amle.2014.0244. | 58 |

| PP88 | Lewis, K.V.; Cassells, S.; Roxas, H. SMEs and the Potential for A Collaborative Path to Environmental Responsibility: SMEs & Collaborative Paths to Environmental Responsibility. Bus. Strat. Environ. 2015, 24, 750–764, doi:10.1002/bse.1843. | 74 |

| PP73 | Loh, L.; Thomas, T.; Wang, Y. Sustainability Reporting and Firm Value: Evidence from Singapore-Listed Companies. Sustainability 2017, 9, 2112, doi:10.3390/su9112112. | 74 |

| PP12 | López-Pérez, M.; Melero-Polo, I.; Vázquez-Carrasco, R.; Cambra-Fierro, J. Sustainability and Business Outcomes in the Context of SMEs: Comparing Family Firms vs. Non-Family Firms. Sustainability 2018, 10, 4080, doi:10.3390/su10114080. | 1 |

| PP37 | Luan, C.-J.; Chen, Y.-Y.; Huang, H.-Y.; Wang, K.-S. CEO Succession Decision in Family Businesses—A Corporate Governance Perspective. Asia Pac. Manag. Rev. 2018, 23, 130–136, doi:10.1016/j.apmrv.2017.03.003. | 33 |

| PP24 | McGrath, H.; O’Toole, T. Extending the Concept of Familiness to Relational Capability: A Belgian Micro-Brewery Study. Internat. Small Bus. J. 2018, 36, 194–219, doi:10.1177/0266242617730885. | 11 |

| PP14 | Molly, V.; Uhlaner, L.M.; De Massis, A.; Laveren, E. Family-Centered Goals, Family Board Representation, and Debt Financing. Small Bus. Econ. 2019, 53, 269–286, doi:10.1007/s11187-018-0058-9. | 27 |

| PP36 | Oro, I.; Lavarda, C. Interaction Between Strategy and Organizational Performance: The Influence of Family Management. BBR 2017, 14, 493–509, doi:10.15728/bbr.2017.14.5.3. | 7 |

| PP70 | Oudah, M.; Jabeen, F.; Dixon, C. Determinants Linked to Family Business Sustainability in the UAE: An AHP Approach. Sustainability 2018, 10, 246, doi:10.3390/su10010246. | 39 |

| PP12 | Pérez-Pérez, M.; López-Férnandez, M.C.; Obeso, M. Knowledge, Renewal and Flexibility: Exploratory Research in Family Firms. Adm. Sci. 2019, 9, 87, doi:10.3390/admsci9040087. | 3 |

| PP22 | Peters, M.; Kallmuenzer, A. Entrepreneurial Orientation in Family Firms: The Case of the Hospitality Industry. Curr. Issues Tour. 2018, 21, 21–40, doi:10.1080/13683500.2015.1053849. | 73 |

| PP15 | Pieper, T.M.; Williams, R.I.; Manley, S.C.; Matthews, L.M. What Time May Tell: An Exploratory Study of the Relationship Between Religiosity, Temporal Orientation, and Goals in Family Business. J. Bus. Ethics 2020, 163, 759–773, doi:10.1007/s10551-019-04386-3. | 7 |

| PP20 | Rodríguez-Aceves, L.; Baños-Monroy, V.; Ramírez-Solís, E. Environmental Dynamism as a Moderator of Familiness and Performance in Mexican SMEs. Latin Amer. Bus. Rev. 2018, 19, 219–243, doi:10.1080/10978526.2018.1534546. | 2 |

| PP19 | Schellong, M.; Kraiczy, N.D.; Malär, L.; Hack, A. Family Firm Brands, Perceptions of Doing Good, and Consumer Happiness. Entrep. Theory Pract. 2019, 43, 921–946, doi:10.1177/1042258717754202. | 17 |

| PP31 | Xue, K.; Yu, M.; Xu, S. Corporate Social Responsibility and Chinese Family-Owned Small- and Medium-Sized Enterprises. Soc. Behav. Pers. 2019, 47, 1–14, doi:10.2224/sbp.7597. | 2 |

References

- El Ghoul, S.; Guedhami, O.; Wang, H.; Kwok, C.C.Y. Family Control and Corporate Social Responsibility. J. Bank. Financ. 2016, 73, 131–146. [Google Scholar] [CrossRef]

- Broccardo, L.; Truant, E.; Zicari, A. Internal Corporate Sustainability Drivers: What Evidence from Family Firms? A Literature Review and Research Agenda. Corp. Soc. Responsib. Environ. Manag. 2019, 26, 1–18. [Google Scholar] [CrossRef]

- Adomako, S.; Amankwah-Amoah, J.; Danso, A.; Konadu, R.; Owusu-Agyei, S. Environmental Sustainability Orientation and Performance of Family and Nonfamily Firms. Bus. Strat. Environ. 2019, 28, 1250–1259. [Google Scholar] [CrossRef]

- Dayan, M.; Ng, P.Y.; Ndubisi, N.O. Mindfulness, Socioemotional Wealth, and Environmental Strategy of Family Businesses. Bus. Strat. Environ. 2019, 28, 466–481. [Google Scholar] [CrossRef]

- Marques, P.; Presas, P.; Simon, A. The Heterogeneity of Family Firms in CSR Engagement: The Role of Values. Fam. Bus. Rev. 2014, 27, 206–227. [Google Scholar] [CrossRef]

- López-Pérez, M.; Melero-Polo, I.; Vázquez-Carrasco, R.; Cambra-Fierro, J. Sustainability and Business Outcomes in the Context of SMEs: Comparing Family Firms vs. Non-Family Firms. Sustainability 2018, 10, 4080. [Google Scholar] [CrossRef]

- Campopiano, G.; De Massis, A. Corporate Social Responsibility Reporting: A Content Analysis in Family and Non-Family Firms. J. Bus. Ethics 2015, 129, 511–534. [Google Scholar] [CrossRef]

- Seidel, S.; Recker, J.; Pimmer, C.; vom Brocke, J. Enablers and Barriers to the Organizational Adoption of Sustainable Business Practices. In Proceedings of the 16th Americas conference on information systems: Sustainable IT collaboration around the globe, Lima, Peru, 12–15 August 2010; Association for Information Systems: Atlanta, GA, USA, 2010; pp. 1–10. [Google Scholar]

- McKenzie, S. Social Sustainability: Towards Some Definitions; Hawke Research Institute Working Paper: Adelaide, Australia, 2004; p. 27. [Google Scholar]

- Graute, U. Local Authorities Acting Globally for Sustainable Development. Reg. Stud. 2016, 50, 1931–1942. [Google Scholar] [CrossRef]

- THE 17 GOALS|Sustainable Development. Available online: https://sdgs.un.org/goals (accessed on 11 November 2020).

- Caputo, F.; Veltri, S.; Venturelli, A. Sustainability Strategy and Management Control Systems in Family Firms. Evidence from a Case Study. Sustainability 2017, 9, 977. [Google Scholar] [CrossRef]

- Shields, J.; Welsh, D.; Shelleman, J. Sustainability Reporting and Its Implications for Family Firms. J. Small Bus. Strategy 2018, 28, 66–71. [Google Scholar]

- Bina, O. The Green Economy and Sustainable Development: An Uneasy Balance? Environ. Plann. C Gov. Policy 2013, 31, 1023–1047. [Google Scholar] [CrossRef]

- Morrow, K. Rio+20, the Green Economy and Re-Orienting Sustainable Development. Environ. Law Rev. 2012, 14, 279–297. [Google Scholar]

- Loiseau, E.; Saikku, L.; Antikainen, R.; Droste, N.; Hansjürgens, B.; Pitkänen, K.; Leskinen, P.; Kuikman, P.; Thomsen, M. Green Economy and Related Concepts: An Overview. J. Clean. Prod. 2016, 139, 361–371. [Google Scholar] [CrossRef]

- Moore, S.B.; Manring, S.L. Strategy Development in Small and Medium Sized Enterprises for Sustainability and Increased Value Creation. J. Clean. Prod. 2009, 17, 276–282. [Google Scholar] [CrossRef]

- Darcy, C.; Hill, J.; McCabe, T.; McGovern, P. A Consideration of Organisational Sustainability in the SME Context: A Resource-Based View and Composite Model. Eur. J. Train. Dev. 2014, 38, 398–414. [Google Scholar] [CrossRef]

- Elkington, J. The Triple Bottom Line. Environ. Manag. Read. Cases 1997, 2, 49–62. [Google Scholar]

- Kuhlman, T.; Farrington, J. What Is Sustainability? Sustainability 2010, 2, 3436–3448. [Google Scholar] [CrossRef]

- Raj, D.; Ma, Y.J.; Gam, H.J.; Banning, J. Implementation of Lean Production and Environmental Sustainability in the Indian Apparel Manufacturing Industry: A Way to Reach the Triple Bottom Line. Int. J. Fash. Des. Technol. Educ. 2017, 10, 254–264. [Google Scholar] [CrossRef]

- Shields, J.; Shelleman, J. Integrating Sustainability into SME Strategy. J. Small Bus. Strategy 2015, 25, 59–78. [Google Scholar]

- Laguir, I.; Elbaz, J. Family Firms and Corporate Social Responsibility (CSR): Preliminary Evidence from The French Stock Market. JABR 2014, 30, 971–988. [Google Scholar] [CrossRef][Green Version]

- Baggia, A.; Leskvar, R.; Delibasic, B.; Petrovic, N. Opportunities of Sustainable Business Practices in SME’s. In Proceedings of the 32nd International Conference on Organizational Science Development, Portoroz, Slovenia, 20–22 March 2013. [Google Scholar]

- Caldera, H.; Desha, C.; Dawes, L. Evaluating the Relationship between Lean Thinking and Environmental Performance in Small to Medium Scale Enterprises. In European Roundtable for Sustainable Consumption and Production, 2017-10-01–2017-10-05. Available online: https://eprints.qut.edu.au/113171/ (accessed on 29 March 2021).

- European Community SME Definition. Available online: https://ec.europa.eu/growth/smes/sme-definition_en (accessed on 14 November 2020).

- European Family Businesses—About EFB. Available online: http://www.europeanfamilybusinesses.eu/about-us (accessed on 14 November 2020).

- Harms, H. Review of Family Business Definitions: Cluster Approach and Implications of Heterogeneous Application for Family Business Research. IJFS 2014, 2, 280–314. [Google Scholar] [CrossRef]

- Astrachan, J.H.; Klein, S.B.; Smyrnios, K.X. The F-PEC Scale of Family Influence: A Proposal for Solving the Family Business Definition Problem. Fam. Bus. Rev. 2002, 15, 45–58. [Google Scholar] [CrossRef]

- European Commission. Final Report of the Expert Group—Overview of Family-Business; Relevant Issues: Research, Networks, Policy Measures and Existing Studies; European Commission: Brussels, Belgium, 2009. [Google Scholar]

- Molina, M.; Rutterford, J. Towards a Theory of The Family Firm: Approach to an Operational Definition and a Framework for Family Businesses Research. In Global Financial & Business Networks & Information Management Systems; European Academic Publishers: Madrid, Spain, 2010. [Google Scholar]

- Doluca, H.; Wagner, M.; Block, J. Sustainability and Environmental Behaviour in Family Firms: A Longitudinal Analysis of Environment-Related Activities, Innovation and Performance. Bus. Strat. Environ. 2018, 27, 152–172. [Google Scholar] [CrossRef]

- Breton-Miller, I.L.; Miller, D. Family Firms and Practices of Sustainability: A Contingency View. J. Fam. Bus. Strategy 2016, 7, 26–33. [Google Scholar] [CrossRef]

- Crotto, F.; Theodoulidis, B.; Diaz, D.; Rancati, E. Exploring Corporate Social Responsibility and Financial Performance through Stakeholder Theory in the Tourism Industries. Tour. Manag. 2017, 62, 173–188. [Google Scholar]

- Hiebl, M.R.W. Peculiarities of Financial Management In Family Firms. IBER 2012, 11, 315. [Google Scholar] [CrossRef]

- Chrisman, J.; Fang, H.; Memili, E.; Welsh, D. Family Firms’ Professionalization: Institutional Theory and Resource-Based View Perspectives. Small Bus. Inst. J. 2012, 8, 12–34. [Google Scholar]

- Barney, J.B. Is the Resource-Based “View” a Useful Perspective for Strategic Management Research? Yes. Acad. Manag. Rev. 2001, 26, 41–56. [Google Scholar] [CrossRef]

- Curado, C. Organizational Learning and Organizational Design. Learn. Organ. 2006, 13, 25–48. [Google Scholar] [CrossRef]

- Kraus, S.; Harms, R.; Fink, M. Family Firm Research: Sketching a Research Field. IJEIM 2011, 13, 32–47. [Google Scholar] [CrossRef]

- Dao, V.; Langella, I.; Carbo, J. From Green to Sustainability: Information Technology and an Integrated Sustainability Framework. J. Strateg. Inf. Syst. 2011, 20, 63–79. [Google Scholar] [CrossRef]

- Pearson, A.W.; Marler, L.E. A Leadership Perspective of Reciprocal Stewardship in Family Firms. Entrep. Theory Pract. 2010, 34, 1117–1124. [Google Scholar] [CrossRef]

- Snyder, H. Literature Review as a Research Methodology: An Overview and Guidelines. J. Bus. Res. 2019, 104, 333–339. [Google Scholar] [CrossRef]

- Tranfield, D.; Denyer, D.; Smart, P. Towards a Methodology for Developing Evidence-Informed Management Knowledge by Means of Systematic Review. Br. J. Manag. 2003, 14, 207–222. [Google Scholar] [CrossRef]

- Moher, D.; Liberati, A.; Tetzlaff, J.; Altman, D.G.; For the PRISMA Group. Preferred Reporting Items for Systematic Reviews and Meta-Analyses: The PRISMA Statement. BMJ 2009, 339, b2535. [Google Scholar] [CrossRef]

- Curado, C.; Oliveira, M.; Macada, A. Mapping Knowledge Management Authoring Patterns and Practices. Afr. J. Bus. Manag. 2011, 5, 9137–9153. [Google Scholar]

- Pérez, P.F.; Raposo, N.P. Bonsais in a Wild Forest? A Historical Interpretation of the Longevity of Large Spanish Family Firms. RHE/JILAEH 2007, 25, 459–497. [Google Scholar] [CrossRef]

- Chou, S.Y.; Chang, T.; Han, B. A Buddhist Application of Corporate Social Responsibility: Qualitative Evidence from a Case Study of a Small Thai Family Business. Small Enter. Res. 2016, 23, 116–134. [Google Scholar] [CrossRef]

- Pieper, T.M.; Williams, R.I.; Manley, S.C.; Matthews, L.M. What Time May Tell: An Exploratory Study of the Relationship Between Religiosity, Temporal Orientation, and Goals in Family Business. J. Bus. Ethics 2020, 163, 759–773. [Google Scholar] [CrossRef]

- Loh, L.; Thomas, T.; Wang, Y. Sustainability Reporting and Firm Value: Evidence from Singapore-Listed Companies. Sustainability 2017, 9, 2112. [Google Scholar] [CrossRef]

- Ardito, L.; Messeni Petruzzelli, A.; Pascucci, F.; Peruffo, E. Inter-Firm R&D Collaborations and Green Innovation Value: The Role of Family Firms’ Involvement and the Moderating Effects of Proximity Dimensions. Bus. Strat. Environ. 2019, 28, 185–197. [Google Scholar] [CrossRef]

- Arena, C.; Michelon, G. A Matter of Control or Identity? Family Firms’ Environmental Reporting Decisions along the Corporate Life Cycle. Bus. Strat. Environ. 2018, 27, 1596–1608. [Google Scholar] [CrossRef]

- Déniz-Déniz, M.d.l.C.; Cabrera-Suárez, M.K.; Martín-Santana, J.D. Family Firms and the Interests of Non-Family Stakeholders: The Influence of Family Managers’ Affective Commitment and Family Salience in Terms of Power. Bus. Ethics A Eur. Rev. 2018, 27, 15–28. [Google Scholar] [CrossRef]

- Luan, C.-J.; Chen, Y.-Y.; Huang, H.-Y.; Wang, K.-S. CEO Succession Decision in Family Businesses—A Corporate Governance Perspective. Asia Pac. Manag. Rev. 2018, 23, 130–136. [Google Scholar] [CrossRef]

- Duarte Alonso, A.; Kok, S.; O’Shea, M. Family Businesses and Adaptation: A Dynamic Capabilities Approach. J. Fam. Econ. Issues 2018, 39, 683–698. [Google Scholar] [CrossRef] [PubMed]

- Pérez-Pérez, M.; López-Férnandez, M.C.; Obeso, M. Knowledge, Renewal and Flexibility: Exploratory Research in Family Firms. Adm. Sci. 2019, 9, 87. [Google Scholar] [CrossRef]

- Engeset, A.B. “For Better or for Worse”—The Role of Family Ownership in the Resilience of Rural Hospitality Firms. Scand. J. Hosp. Tour. 2020, 20, 68–84. [Google Scholar] [CrossRef]

- Dieleman, M.; Koning, J. Articulating Values Through Identity Work: Advancing Family Business Ethics Research. J. Bus. Ethics 2020, 163, 675–687. [Google Scholar] [CrossRef]

- Xue, K.; Yu, M.; Xu, S. Corporate Social Responsibility and Chinese Family-Owned Small- and Medium-Sized Enterprises. Soc. Behav. Pers. 2019, 47, 1–14. [Google Scholar] [CrossRef]

- Cohen, B.; Smith, B.; Mitchell, R. Toward a Sustainable Conceptualization of Dependent Variables in Entrepreneurship Research. Bus. Strategy Environ. 2008, 17, 107–119. [Google Scholar] [CrossRef]

- Glavas, A.; Mish, J. Resources and Capabilities of Triple Bottom Line Firms: Going over Old or Breaking New Ground? J. Bus. Ethics 2015, 127, 623–642. [Google Scholar] [CrossRef]

- Dangelico, R.M. Green Product Innovation: Where We Are and Where We Are Going: Green Product Innovation. Bus. Strat. Environ. 2016, 25, 560–576. [Google Scholar] [CrossRef]

- Alves, M.W.F.M.; Mariano, E.B. Climate Justice and Human Development: A Systematic Literature Review. J. Clean. Prod. 2018, 202, 360–375. [Google Scholar] [CrossRef]

| Criteria and Results | Outcomes |

|---|---|

| Platform: | B-On |

| Keywords: | “family firms” + “sustainability” + “empirical study” |

| Filters: | Search the full text: Apply to equivalent subjects; Available in the library collection Analyzed by peers |

| Publication dates: | 1 January 2015–31 December 2020 |

| Sources: | Academic Journals |

| Order: | Relevancy |

| Topics: | “Sustainability” “Family-owned Business Enterprises” |

| Results: | 95 papers |

| Theories Used in the Studies | Papers (%) |

|---|---|

| Socio Emotional Wealth Theory | 10 (35.7) |

| None | 9 (32.1) |

| Corporate Social Responsibility | 8 (28.6) |

| Stakeholders Theory | 6 (21.4) |

| Resource-Based View | 4 (14.3) |

| Stewardship Theory | 4 (14.3) |

| Agency Theory | 3 (10.7) |

| Expectations Theory | 2 (7.1) |

| Legitimacy Theory | 2 (7.1) |

| Triple Bottom Lune | 2 (7.1) |

| Contingency Theory | 1 (3.6) |

| Social Identity Theory | 1 (3.6) |

| Expectancy Theory | 1 (3.6) |

| Mindfulness Theory | 1 (3.6) |

| Signal Theory | 1 (3.6) |

| Methods & Data Collection Tools | Papers (%) |

|---|---|

| Qualitative | 16 (57.1) |

| Quantitative | 11 (39.3) |

| Qualitative and Quantitative | 1 (3.6) |

| Survey | 6 (21.4) |

| Documental analysis | 5 (17.9) |

| Interviews | 4 (14.3) |

| Documental analysis & Survey | 4 (14.3) |

| Documental analysis & Interviews | 2 (7.1) |

| Interviews & Survey | 2 (7.1) |

| Documental analysis, Interviews & Observation | 2 (7.1) |

| Documental analysis & Observation | 1 (3.6) |

| Interviews & Observation | 1 (3.6) |

| Documental analysis, Interviews & Survey | 1 (3.6) |

| Paper ID (From Appendix A) | Environmental Issues | Social Issues | Economic Issues |

|---|---|---|---|

| PP1 | ✕ | ✕ | |

| PP3 | ✕ | ||

| PP4 | ✕ | ✕ | |

| PP6 | ✕ | ✕ | ✕ |

| PP7 | ✕ | ✕ | ✕ |

| PP8 | ✕ | ✕ | |

| PP10 | ✕ | ||

| PP11 | ✕ | ✕ | ✕ |

| PP12 | ✕ | ||

| PP14 | ✕ | ||

| PP15 | ✕ | ||

| PP17 | ✕ | ||

| PP19 | ✕ | ✕ | ✕ |

| PP20 | ✕ | ||

| PP22 | ✕ | ✕ | |

| PP24 | ✕ | ||

| PP31 | ✕ | ✕ | |

| PP36 | ✕ | ||

| PP37 | ✕ | ||

| PP43 | ✕ | ||

| PP45 | ✕ | ||

| PP49 | ✕ | ✕ | |

| PP57 | ✕ | ||

| PP60 | ✕ | ✕ | |

| PP68 | ✕ | ✕ | ✕ |

| PP70 | ✕ | ||

| PP73 | ✕ | ✕ | ✕ |

| PP88 | ✕ |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2021 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Curado, C.; Mota, A. A Systematic Literature Review on Sustainability in Family Firms. Sustainability 2021, 13, 3824. https://doi.org/10.3390/su13073824

Curado C, Mota A. A Systematic Literature Review on Sustainability in Family Firms. Sustainability. 2021; 13(7):3824. https://doi.org/10.3390/su13073824

Chicago/Turabian StyleCurado, Carla, and António Mota. 2021. "A Systematic Literature Review on Sustainability in Family Firms" Sustainability 13, no. 7: 3824. https://doi.org/10.3390/su13073824

APA StyleCurado, C., & Mota, A. (2021). A Systematic Literature Review on Sustainability in Family Firms. Sustainability, 13(7), 3824. https://doi.org/10.3390/su13073824