Toward a Chatbot for Financial Sustainability

Abstract

1. Introduction

2. Background

2.1. Financial Chatbot Service

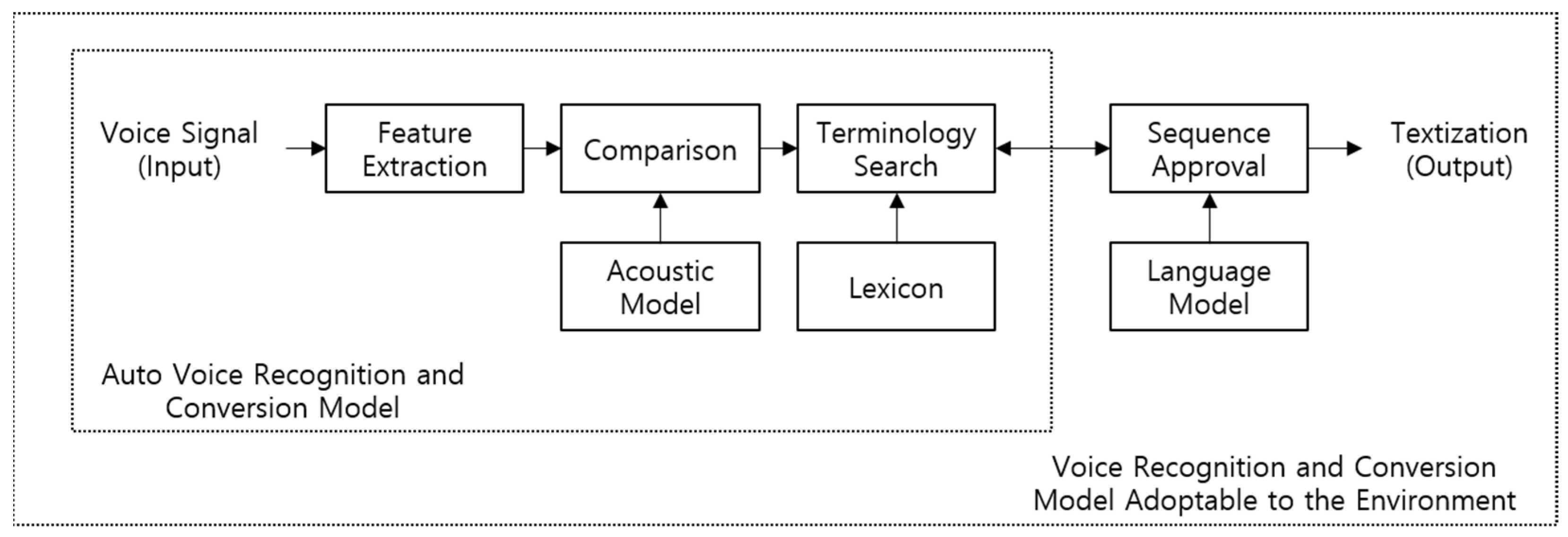

2.2. Telemarketing and Technical Elements of Alternative Systems

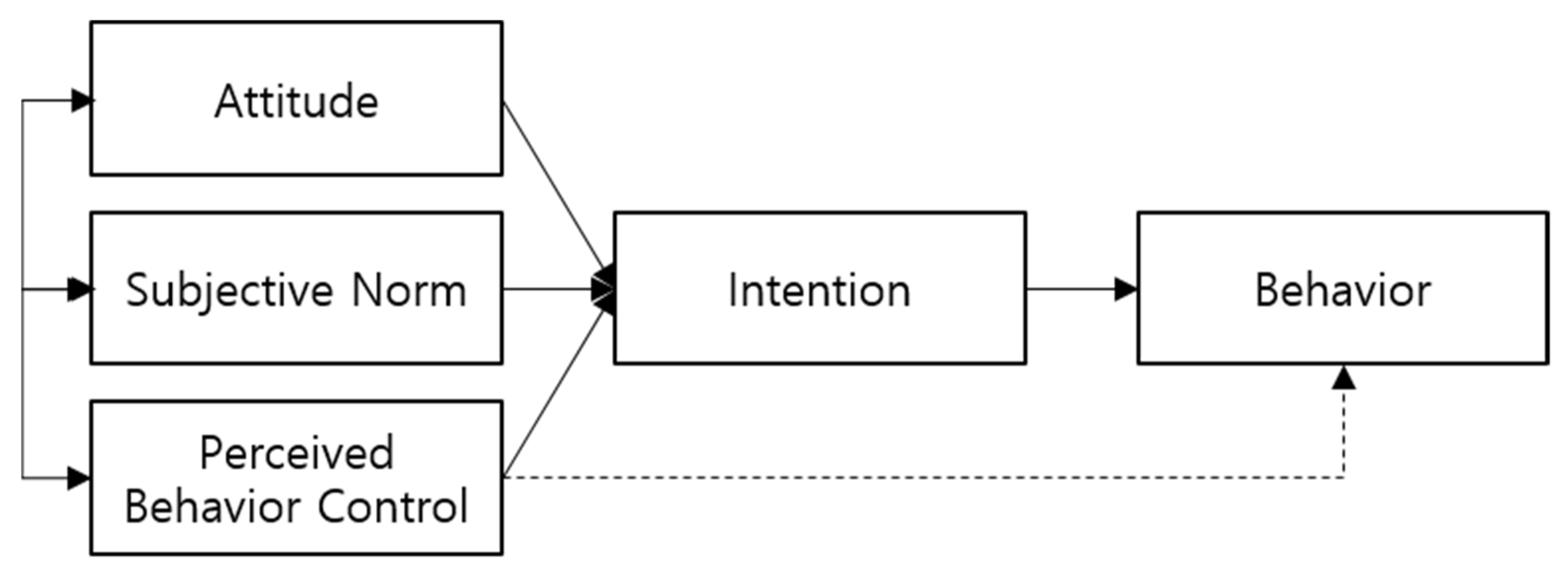

2.3. Intention to Accept New Technology and Its Spread

2.4. Profitability Indicators

3. Methods

3.1. Samples and Data Collection

3.2. Operational Definition and Preprocessing

3.3. Descriptive Analysis

3.4. Hypotheses

4. Results

4.1. Statistical Hypothesis Testing

4.2. Cube Model Interpretation

5. Conclusions

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Conflicts of Interest

References

- Brundage, M.; Avin, S.; Wang, J.; Belfield, H.; Krueger, G.; Hadfield, G.; Khlaaf, H.; Yang, J.; Toner, H.; Fong, R. Toward trustworthy AI development: Mechanisms for supporting verifiable claims. arXiv 2020, arXiv:2004.07213. [Google Scholar]

- Zoonky, L. Ask about the Future. JoongAng Ilbo, 25 January 2021. Available online: https://news.joins.com/article/23977466 (accessed on 25 January 2020).

- Burström, T.; Parida, V.; Lahti, T.; Wincent, J. AI-enabled business-model innovation and transformation in industrial ecosystems: A framework, model and outline for further research. J. Bus. Res. 2021, 127, 85. [Google Scholar] [CrossRef]

- Bender, E.M.; Friedman, B. Data statements for natural language processing: Toward mitigating system bias and enabling better science. Trans. Assoc. Comput. Linguist. 2018, 6, 587. [Google Scholar] [CrossRef]

- Ha, J.-W.; Nam, K.; Kang, J.G.; Lee, S.-W.; Yang, S.; Jung, H.; Kim, E.; Kim, H.; Kim, S.; Kim, H.A. ClovaCall: Korean goal-oriented dialog speech corpus for automatic speech recognition of contact centers. arXiv, 2020; arXiv:2004.09367. [Google Scholar]

- Okuda, T.; Shoda, S. AI-based chatbot service for financial industry. Fujitsu Sci. Tech. J. 2018, 54, 4. [Google Scholar]

- Lin, T.C. Artificial Intelligence, Finance, and the Law. Fordham L. Rev. 2019, 88, 531. [Google Scholar]

- Fadziso, T. Ethical Issues on Utilization of AI, Robotics and Automation Technologies. Asian J. Humanit. Art Lit. 2020, 7, 79. [Google Scholar]

- Malali, A.B.; Gopalakrishnan, S. Application of Artificial Intelligence and Its Powered Technologies in the Indian Banking and Financial Industry: An Overview. IOSR J. Humanit. Soc. Sci. 2020, 25, 55. [Google Scholar]

- Przegalinska, A.; Ciechanowski, L.; Stroz, A.; Gloor, P.; Mazurek, G. In bot we trust: A new methodology of chatbot performance measures. Bus. Horiz. 2019, 62, 785–797. [Google Scholar] [CrossRef]

- Serban, I.V.; Sankar, C.; Germain, M.; Zhang, S.; Lin, Z.; Subramanian, S.; Kim, T.; Pieper, M.; Chandar, S.; Ke, N.R. A deep reinforcement learning chatbot. arXiv, 2017; arXiv:1709.02349. [Google Scholar]

- Yu, S.; Chen, Y.; Zaidi, H. A Financial Service Chatbot based on Deep Bidirectional Transformers. arXiv 2020, arXiv:2003.04987. [Google Scholar]

- Moysan, Y.; Zeitoun, J. Chatbots as a lever to redefine customer experience in banking. J. Digit. Bank. 2019, 3, 242. [Google Scholar]

- Sharma, S.; Sharma, N.; Vyas, R. Artificial Intelligence: Legal Aspects, Risks: Are We Ready for Such Intelligent Autonomous Machines? Neoteric Multidiscip. Res. J. NR Res. Publ. 2018, 1, 1–12. [Google Scholar]

- Kim, J.W.; Jo, H.I.; Lee, B.G. The Study on the Factors Influencing on the Behavioral Intention of Chatbot Service for the Financial Sector: Focusing on the UTAUT Model. J. Digit. Contents Soc. 2019, 20, 41. [Google Scholar] [CrossRef]

- Tammewar, A.; Pamecha, M.; Jain, C.; Nagvenkar, A.; Modi, K. Production ready chatbots: Generate if not retrieve. arXiv, 2017; arXiv:1711.09684. [Google Scholar]

- Karri, S.P.R.; Kumar, B.S. Deep learning techniques for implementation of chatbots. In Proceedings of the International Conference on Computer Communication and Informatics (ICCCI), Da Nang, Vietnam, 30 November–3 December 2020; IEEE: Piscataway, NJ, USA, 2020; pp. 1–5. [Google Scholar]

- Wu, W.; Yan, R. Deep chit-chat: Deep learning for chatbots. In Proceedings of the 42nd International ACM SIGIR Conference on Research and Development in Information Retrieval, Paris, France, 21–25 July 2019; pp. 1413–1414. [Google Scholar]

- Karna, M.; Juliet, D.S.; Joy, R.C. Deep learning based Text Emotion Recognition for Chatbot applications. In Proceedings of the 4th International Conference on Trends in Electronics and Informatics (ICOEI)(48184), Tamilnadu, India, 16–18 April 2020; IEEE: Piscataway, NJ, USA, 2020; pp. 988–993. [Google Scholar]

- Ukpabi, D.C.; Aslam, B.; Karjaluoto, H. Chatbot adoption in tourism services: A conceptual exploration. In Robots, Artificial Intelligence, and Service Automation in Travel, Tourism and Hospitality; Emerald Publishing Limited: Bingley, UK, 2019. [Google Scholar]

- Handoyo, E.; Arfan, M.; Soetrisno, Y.A.A.; Somantri, M.; Sofwan, A.; Sinuraya, E.W. Ticketing chatbot service using serverless NLP technology. In Proceedings of the 5th International Conference on Information Technology, Computer, and Electrical Engineering (ICITACEE), Jakarta, Indonesia, 27–28 September 2018; IEEE: Piscataway, NJ, USA, 2018; pp. 325–330. [Google Scholar]

- Ciechanowski, L.; Przegalinska, A.; Magnuski, M.; Gloor, P. In the shades of the uncanny valley: An experimental study of human–chatbot interaction. Future Gener. Comput. Syst. 2019, 92, 539–548. [Google Scholar] [CrossRef]

- Jain, M.; Kumar, P.; Kota, R.; Patel, S.N. Evaluating and informing the design of chatbots. In Proceedings of the Designing Interactive Systems Conference, Hong Kong, China, 9–13 June 2018; pp. 895–906. [Google Scholar]

- Nguyen, T. Potential Effects of Chatbot Technology on Customer Support: A Case Study. Master’s Thesis, Aalto University, Espoo, Finland, 2019. [Google Scholar]

- Dewnarain, S.; Ramkissoon, H.; Mavondo, F. Social customer relationship management: An integrated conceptual framework. J. Hosp. Mark. Manag. 2019, 28, 172–188. [Google Scholar] [CrossRef]

- Zerbino, P.; Aloini, D.; Dulmin, R.; Mininno, V. Big Data-enabled customer relationship management: A holistic approach. Inf. Process. Manag. 2018, 54, 818–846. [Google Scholar] [CrossRef]

- Chi, N.W.; Wang, I.A. The relationship between newcomers’ emotional labor and service performance: The moderating roles of service training and mentoring functions. Int. J. Hum. Resour. Manag. 2018, 29, 2729–2757. [Google Scholar] [CrossRef]

- Grandey, A.A.; Melloy, R.C. The state of the heart: Emotional labor as emotion regulation reviewed and revised. J. Occup. Health Psychol. 2017, 22, 407. [Google Scholar] [CrossRef] [PubMed]

- Cho, Y.J.; Song, H.J. Determinants of turnover intention of social workers: Effects of emotional labor and organizational trust. Public Pers. Manag. 2017, 46, 41–65. [Google Scholar] [CrossRef]

- Adam, M.; Wessel, M.; Benlian, A. AI-based chatbots in customer service and their effects on user compliance. Electron. Mark. 2020, 1–19. [Google Scholar] [CrossRef]

- Zhang, Y.; Zhang, M.; Luo, N.; Wang, Y.; Niu, T. Understanding the formation mechanism of high-quality knowledge in social question and answer communities: A knowledge co-creation perspective. Int. J. Inf. Manag. 2019, 48, 72–84. [Google Scholar] [CrossRef]

- Garcia, N.; Otani, M.; Chu, C.; Nakashima, Y. KnowIT VQA: Answering knowledge-based questions about videos. In Proceedings of the AAAI Conference on Artificial Intelligence, New York, NY, USA, 7–12 February 2020; Volume 34, pp. 10826–10834. [Google Scholar]

- Mohemad, R.; Noor, N.M.M.; Ali, N.H.; Li, E.Y. Ontology-Based Question Answering System in Restricted Domain. J. Telecommun. Electron. Comput. Eng. 2017, 9, 29–33. [Google Scholar]

- Kumar, V.; Rajan, B.; Venkatesan, R.; Lecinski, J. Understanding the role of artificial intelligence in personalized engagement marketing. Calif. Manag. Rev. 2019, 61, 135–155. [Google Scholar] [CrossRef]

- Singh, N. Automatic speaker recognition: Current approaches and progress in last six decades. Glob. J. Enterp. Inf. Syst. 2017, 9, 45–52. [Google Scholar] [CrossRef] [PubMed]

- Wang, H. Two-step Judgment Algorithm for Robust Voice Activity Detection Based on Deep Neural Networks. In Proceedings of the International Computers, Signals and Systems Conference (ICOMSSC), Dalian, China, 28–30 September 2018; IEEE: Piscataway, NJ, USA, 2018; pp. 84–86. [Google Scholar]

- Perez, C. Structural change and assimilation of new technologies in the economic and social systems. Futures 1983, 15, 357–375. [Google Scholar] [CrossRef]

- Pavlou, P.A. Consumer acceptance of electronic commerce: Integrating trust and risk with the technology acceptance model. Int. J. Electron. Commer. 2003, 7, 101–134. [Google Scholar]

- Lee, Y.; Kozar, K.A.; Larsen, K.R. The technology acceptance model: Past, present, and future. Commun. Assoc. Inf. Syst. 2003, 12, 50. [Google Scholar] [CrossRef]

- Chuttur, M.Y. Overview of the technology acceptance model: Origins, developments and future directions. Work. Pap. Inf. Syst. 2009, 9, 9–37. [Google Scholar]

- Dearing, J.W. Applying diffusion of innovation theory to intervention development. Res. Soc. Work. Pract. 2009, 19, 503–518. [Google Scholar] [CrossRef] [PubMed]

- Min, S.; So, K.K.F.; Jeong, M. Consumer adoption of the Uber mobile application: Insights from diffusion of innovation theory and technology acceptance model. J. Travel Tour. Mark. 2019, 36, 770–783. [Google Scholar] [CrossRef]

- Ajzen, I. The theory of planned behavior: Frequently asked questions. Hum. Behav. Emerg. Technol. 2020, 2, 314–324. [Google Scholar] [CrossRef]

- Im, I.; Hong, S.; Kang, M.S. An international comparison of technology adoption: Testing the UTAUT model. Inf. Manag. 2011, 48, 1–8. [Google Scholar] [CrossRef]

- Williams, M.D.; Rana, N.P.; Dwivedi, Y.K. The unified theory of acceptance and use of technology (UTAUT): A literature review. J. Enterp. Inf. Manag. 2015, 28, 443–488. [Google Scholar] [CrossRef]

- Steg, L.; Bolderdijk, J.W.; Keizer, K.; Perlaviciute, G. An integrated framework for encouraging pro-environmental behavior: The role of values, situational factors and goals. J. Environ. Psychol. 2014, 38, 104–115. [Google Scholar] [CrossRef]

- Burja, C. Factors Influencing the Companies’ Profitability. Ann. Univ. Apulensis Ser. Oeconomica 2011, 2, 1–3. [Google Scholar] [CrossRef]

- Sufian, F. Profitability of the Korean banking sector: Panel evidence on bank-specific and macroeconomic determinants. J. Econ. Manag. 2011, 7, 43–72. [Google Scholar]

- Kumar, V.; Thrikawala, S.; Acharya, S. Financial inclusion and bank profitability: Evidence from a developed market. Global Financ. J. 2021, 100609. [Google Scholar] [CrossRef]

- Kim, M.K.; Eom, J.G. A Study on Determinants of Banks` Profitability: Focusing on the Comparison between before and after Global Financial Crisis. Int. J. Contents. 2018, 18, 196–209. [Google Scholar]

- Hoang, V.H.; Hoang, N.T.; Yarram, S.R. Efficiency and shareholder value in Australian banking. Econ. Rec. 2020, 96, 40–64. [Google Scholar] [CrossRef]

- Ali, M.; Puah, C.H. The internal determinants of bank profitability and stability. Manag. Res. Rev. 2019, 42, 49–67. [Google Scholar] [CrossRef]

- Xu, M.T.; Hu, K.; Das, M.U.S. Bank Profitability and Financial Stability; International Monetary Fund: Washington, DC, USA, 2019. [Google Scholar]

- Demirgüç-Kunt, A.; Levine, R. (Eds.) Financial Structure and Economic Growth: A Cross-Country Comparison of Banks, Markets, and Development; MIT Press: Cambridge, MA, USA, 2004. [Google Scholar]

- Ehigiamusoe, K.U.; Guptan, V.; Lean, H.H. Impact of financial structure on environmental quality: Evidence from panel and disaggregated data. Energy Sources Part B Econ. Plan. Policy 2019, 14, 359–383. [Google Scholar] [CrossRef]

- Um, T.; Kim, T.; Chung, N. How does an Intelligence Chatbot Affect Customers Compared with Self-Service Technology for Sustainable Services? Sustainability 2020, 12, 5119. [Google Scholar] [CrossRef]

- Erkut, B. From digital government to digital governance: Are we there yet? Sustainability 2020, 12, 860. [Google Scholar] [CrossRef]

- Toader, D.C.; Boca, G.; Toader, R.; Măcelaru, M.; Toader, C.; Ighian, D.; Rădulescu, A.T. The effect of social presence and chatbot errors on trust. Sustainability 2020, 12, 256. [Google Scholar] [CrossRef]

{kind=link}

{kind=link}

| Type | Financial Institution | Chatbot Name | Service Platform | Starting from |

|---|---|---|---|---|

| Banking Corps. | Shinhan | Aurora | Shinhan Sol | 2018. 02 |

| Kookmin | Smartly (TalkTalk) | Liiv TalkTalk | 2017. 07 | |

| NH | Consultation Talk | NH banking | 2018. 11 | |

| Hana | HAI | Hana Members | 2017. 09 | |

| Woori | Wibee-bot | WibeeTalk | 2018. 09 | |

| Credit Card Company | Shinhan | FANi | Shinhan Paypal | 2017. 06 |

| Samsung | Sam | Chatbot Sam | 2019. 03 | |

| Hyundai | Henry & Fiona | Buddy | 2017. 08 | |

| Lotte | LOCA | The Loca Lab | 2018. 04 | |

| Others (Securities, Insurance, and Third Bank Sector) | Daishin (Sec.) | Benjamin | Kakao Talk | 2017. 09 |

| Samsung (Ins.) | Tabot | TABOT | 2017. 06 | |

| Welcome (3rd S.) | Welcomebot | Kakao Talk | 2017. 09 | |

| OK (3rd S.) | Oktok | Kakao Talk | 2017. 08 | |

| JT (3rd S.) | JT Mobile Chatbot | Kakao Talk | 2018. 05 |

| Process | Design Element | Interface Example |

|---|---|---|

| Access Screen | Functional Design | Chatbot location |

| Value Design | Chatbot icon and name by function | |

| Start Screen | Visual Design | Background color and overall layout |

| Functional Design | Help on key features | |

| Answer Screen | Functional Design | Speech bubble space utilization and option selection function |

| Value Design | Character and profile image | |

| Information Screen | Visual Design | Graphic information |

| Division | Component | |

|---|---|---|

| Interactive interface | Speech recognition, multimodal, context recognition | |

| Semantic reasoning | Intelligence level | Assistant chatbot, intelligent assistant, cognitive assistant |

| Conversation process | Goal-oriented conversation processing, question and answer skills | |

| Knowledge | Semantic Web, ontology-based technical data | |

| Other services | Modeling, big data analysis, web service | |

| Financial Goods | Customer Service | Chatbot | Total | % |

|---|---|---|---|---|

| Fund subscription | 28,435 | 2531 | 30,996 | 8.8 |

| Housing-subscription savings | 49,937 | 4365 | 54,302 | 15.4 |

| Loan interest payment | 54,833 | 6350 | 61,183 | 17.4 |

| Utility bill | 187,233 | 18,843 | 206,076 | 58.5 |

| Total | 320,438 | 32,089 | 352,527 | 100.0 |

| Variable | Preprocessing | Remarks |

|---|---|---|

| Customer Number | Assign a unique number after masking | Excluding the first 2 digits |

| Age | Age of subscribers | |

| Age Group * | Age category of subscribers | 0 = under and equal 45, 1 = over 45 |

| Purchase Date * | Date of first contact | |

| Approval Date | Subscription savings, loan payment, and utility bills are processed in real time (same with Purchase Date) | Fund needs to adjust date according to conditions |

| Amount1 | Subscription amount of Funds | |

| Amount2 | Amount of housing-subscription savings | |

| Amount3 | Amount of loan interest payment | |

| Amount4 | Amount of utility bills payment | Includes national tax, local tax, and other utility expenses |

| Purchase Channel | - Customer service: employee #- Chatbot: HQ unique code (CB0-#) | |

| Channel Classification * | Customer service and chatbot channel classification | 0 = customer service, 1 = chatbot |

| Net profit1 * | Revenue from Funds—Expenses | -Exp1: Counselor salary -Exp2: Chatbot cost (develop and maintenance)/average IT infra depreciation period (daily-base) |

| Net profit2 * | Revenue from housing-subscription savings—Expenses | |

| Net profit3 * | Revenue from loan interest—Expenses | |

| Net profit4 * | Revenue from utility bills—Expenses |

| Channel | Goods | Age Groups | Total (%) | ||||

|---|---|---|---|---|---|---|---|

| Junior (%) | Senior (%) | ||||||

| Customer Service | Fund | 15,665 | (46.9) | 17,770 | (53.1) | 33,435 | (10.5) |

| H.S.S. | 23,469 | (42.7) | 31,468 | (57.3) | 54,937 | (17.3) | |

| L.I. | 22,845 | (44.1) | 28,988 | (55.9) | 51,833 | (16.3) | |

| Bills | 81,729 | (46.1) | 95,504 | (53.9) | 177,233 | (55.8) | |

| Total | 143,708 | (45.3) | 173,730 | (54.7) | 317,438 | ||

| Chatbot | Fund | 2,023 | (79.9) | 508 | (20.1) | 2,531 | (7.4) |

| H.S.S. | 2,798 | (64.1) | 1,567 | (35.9) | 4,365 | (12.8) | |

| L.I. | 3,787 | (59.6) | 2,563 | (40.4) | 6,350 | (18.6) | |

| Bills | 13,105 | (62.7) | 7,738 | (37.1) | 20,843 | (61.1) | |

| Total | 21,713 | (63.7) | 12,376 | (36.3) | 34,089 | ||

| Total | Fund | 17,688 | (49.2) | 18,278 | (50.8) | 35,966 | (10.2) |

| H.S.S. | 26,267 | (44.3) | 33,035 | (55.7) | 59,302 | (16.9) | |

| L.I. | 26,632 | (45.8) | 31,551 | (54.2) | 58,183 | (16.6) | |

| Bills | 94,834 | (47.9) | 103,242 | (52.1) | 198,076 | (56.3) | |

| Total | 165,421 | (47.1) | 186,106 | (52.9) | 351,527 | ||

| Combination | Channel | Col. Ratio | Row Ratio | |||

|---|---|---|---|---|---|---|

| Customer Service | Chatbot | Total | ||||

| Junior | New Products Sales | 39,134 | 4821 | 43,955 | 8.1 | 26.6 |

| Provision of Existing Services | 104,574 | 16,892 | 121,466 | 6.2 | 73.4 | |

| Total | 143,708 | 21,713 | 165,421 | 6.6 | ||

| Senior | New Products Sales | 49,238 | 2075 | 51,313 | 23.7 | 27.6 |

| Provision of Existing Services | 124,492 | 10,301 | 134,793 | 12.1 | 72.4 | |

| Total | 173,730 | 12,376 | 186,106 | 14.0 | ||

| Total | 317,438 | 34,089 | 351,527 | 9.3 | ||

| DF | SS | MS | F-Value | p-Value | |

|---|---|---|---|---|---|

| Model | 2 | 145.3548 | 72.6774 | 18.8893 | <0.0001 |

| Error | 357,435 | 1,375,248.4582 | 3.8475 | ||

| Total | 357,437 | 1,375,393.8130 | |||

| Parameter | DF | Estimate | S.E. | T for H0 | p-value |

| Intercept | 1 | −1.4275 | 0.05251 | −2.719 | 0.0014 |

| T | 1 | 0.0215 | 0.1457 | 0.148 | <0.0001 |

| NT | 1 | 0.0378 | 0.2437 | 0.155 | <0.0001 |

| DF | SS | MS | F-Value | p-Value | |

|---|---|---|---|---|---|

| Model | 2 | 645.3548 | 322.6774 | 70.1013 | <0.0001 |

| Error | 357,435 | 1,645,278.4582 | 4.6030 | ||

| Total | 357,437 | 1,645,923.8130 | |||

| Parameter | DF | Estimate | S.E. | T for H0 | p-value |

| Intercept | 1 | 3.4572 | 0.4251 | 8.133 | 0.073 |

| T | 1 | 0.0035 | 0.0024 | 1.458 | <0.0001 |

| NT | 1 | 0.0081 | 0.0075 | 1.080 | <0.0001 |

| Variance | DF | t-Value | p-Value | |

|---|---|---|---|---|

| Pooled | Equal | 43,953 | 1.4352 | 0.312 |

| Satterthwaite | Unequal | 43,864.245 | 1.4345 | 0.416 |

| Equality of Variance | Num DF | Den DF | F-value | p-value |

| Folded F | 39,134 | 4821 | 8.12 | 0.357 |

| Variance | DF | t-Value | p-Value | |

|---|---|---|---|---|

| Pooled | Equal | 121,464 | 18.2142 | 0.012 |

| Satterthwaite | Unequal | 121,435.328 | 14.2146 | 0.011 |

| Equality of Variance | Num DF | Den DF | F-value | p-value |

| Folded F | 104,574 | 16,892 | 6.19 | 0.452 |

| Variance | DF | t-Value | p-Value | |

|---|---|---|---|---|

| Pooled | Equal | 51,311 | 21.0113 | <0.0001 |

| Satterthwaite | Unequal | 51,304.525 | 34.1223 | <0.0001 |

| Equality of Variance | Num DF | Den DF | F-value | p-value |

| Folded F | 49,238 | 2075 | 23.73 | <0.0001 |

| Variance | DF | t-Value | p-Value | |

|---|---|---|---|---|

| Pooled | Equal | 134,791 | −13.1452 | 0.026 |

| Satterthwaite | Unequal | 134,731.583 | −12.1025 | 0.025 |

| Equality of Variance | Num DF | Den DF | F-value | p-value |

| Folded F | 124,492 | 10,301 | 12.09 | <0.034 |

| New Products (Y1) | X1–Y1 (H3a) Not significant | X2–Y1 (H3c) Positive in net profit from Customer Service |

| Existing Service (Y2) | X1–Y2 (H3b) Negative in net profit from Chatbot | X2–Y2 (H3d) Negative in net profit from Customer Service |

| Junior Group (X1) | Senior Group (X2) |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2021 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

Hwang, S.; Kim, J. Toward a Chatbot for Financial Sustainability. Sustainability 2021, 13, 3173. https://doi.org/10.3390/su13063173

Hwang S, Kim J. Toward a Chatbot for Financial Sustainability. Sustainability. 2021; 13(6):3173. https://doi.org/10.3390/su13063173

Chicago/Turabian StyleHwang, Sewoong, and Jonghyuk Kim. 2021. "Toward a Chatbot for Financial Sustainability" Sustainability 13, no. 6: 3173. https://doi.org/10.3390/su13063173

APA StyleHwang, S., & Kim, J. (2021). Toward a Chatbot for Financial Sustainability. Sustainability, 13(6), 3173. https://doi.org/10.3390/su13063173